Sample Category Title

Gold surges and regain 1300 as Kim-Trump meeting is called off

Gold jumps sharply and is back above 1300 handle on news that Trump cancels his summit with North Korean Leader Kim Jong Un.

1282.27 is now seen as a short term bottom. More importantly, the the long term trend line, established since De 2016 at 1122.81, was defended.

Focus will now be back on 55 day EMA (now at 1316.59) and 1325.91 resistance zone. As long as these zone holds, further fall is still mildly in favor. And sustained break of the trend line support will be a strong indication of bearish reversal.

Nonetheless, firm break of 1325.91 will set the stage for a test on 1366.05. And, probably the real key resistance at 1380.56.

USDJPY heading lower after Trump cancels summit with North Korean Kim

Stocks tumble sharply, while treasury yields dive as Trump announced to cancel the meeting with North Korean Leader Kim Jong Un in Singapore on June 12. At the time of writing, DOW is down -0.5%, at around 24770. Deeper fall could be seen but the key is whether near term support at around 24600 would hold. There is some distance to this level yet.

But 10 year yield is looking much worse. TNX opened the day at 3% and hit as long as 2.963 so far. There is some clear downside acceleration after Trump's announcement through the White House. And the sharp fall in TNX drags USD/JPY to 109.10so far.

Below is the tweet from the White House regarding the cancellation.

https://twitter.com/WhiteHouse/status/999647796218269697

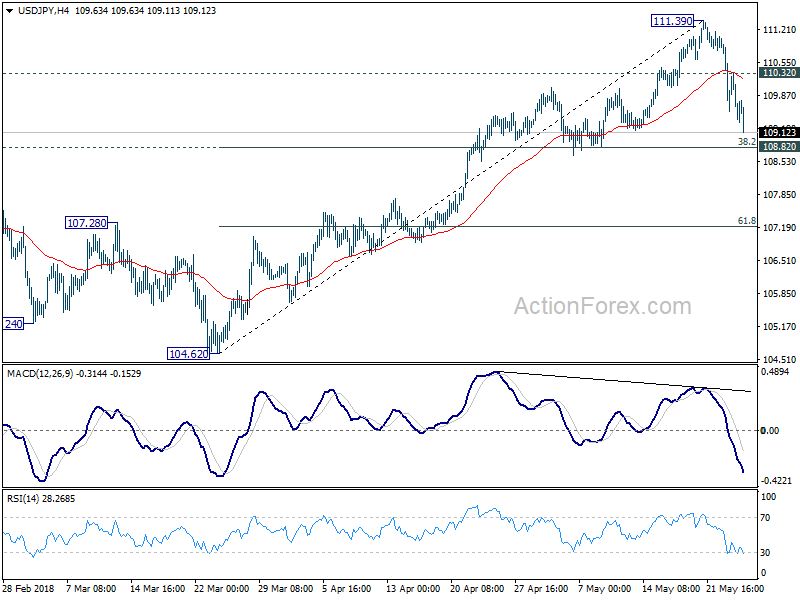

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.44; (P) 110.19; (R1) 110.83; More...

USD/JPY's fall extends to as low as 109.12 in early US session. Intraday bias remains on the downside for 108.82 cluster support (38.2% retracement of 104.62 to 111.39 at 108.80). For now, we'd still expect strong support from there to contain downside and bring rebound. On the upside, above 110.32 minor resistance will argue that the pull back is completed. And, in that case, retest of 111.39 high should be seen. But, decisive break there is now needed to confirm rally resumption. Otherwise, more corrective trading would be seen in near term.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as108.82 support holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above. However, decisive break of 108.82 will dampen the bullish outlook and revive the case of a break of 104.62 low before bottoming.

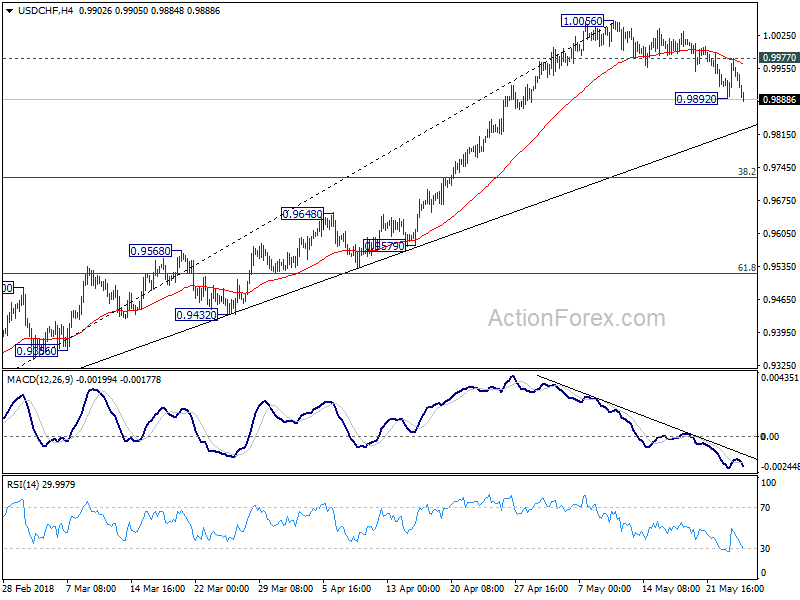

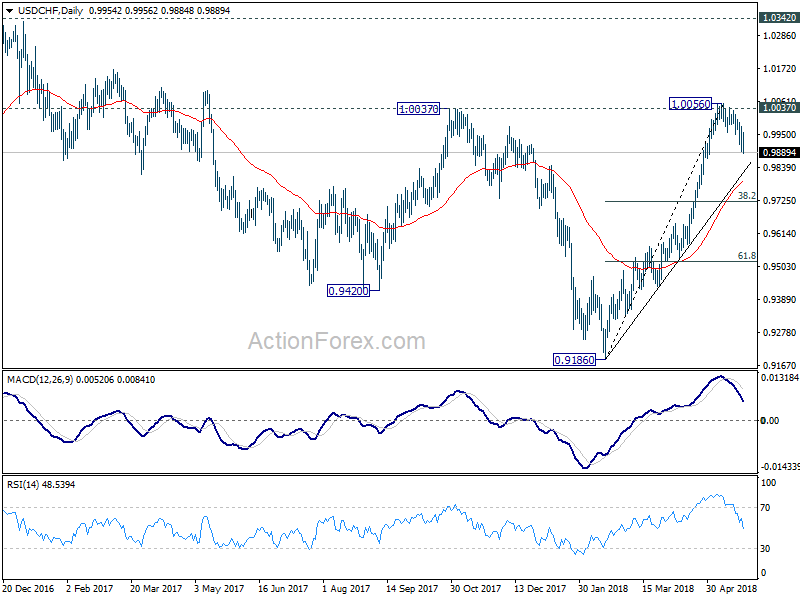

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9908; (P) 0.9944; (R1) 0.9993; More...

USD/CHF's corrective fall from 1.0056 resumed today by breaking 0.9892. Intraday bias is back on the downside. For now, we'd still expect strong support from trend line (now at 0.9825) to contain downside and bring rebound. On the upside, above 0.9977 will suggest that the pull back is finished and bring retest of 1.0056 high.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

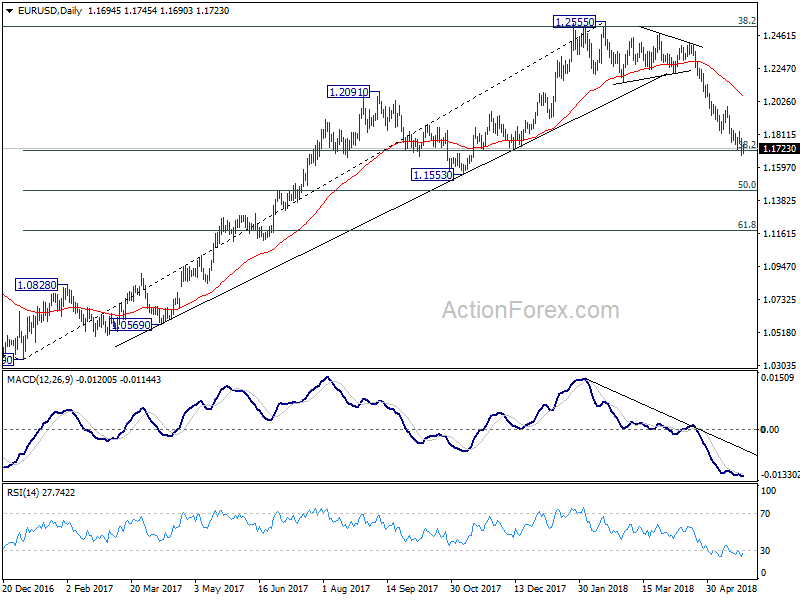

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1652; (P) 1.1721 (R1) 1.1766; More....

No change in EUR/USD's outlook. Intraday bias remains on the downside at this point. Current decline from 1.2555 would target 50% retracement of 1.0339 to 1.2555 at 1.1447 next. Though, considering bullish convergence condition in 4 hour MACD, break of 1.1829 minor resistance will suggest short term bottoming. And, lengthier consolidation would be seen in this case, before staging another fall.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will pave the way to 61.8% retracement at 1.1186. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2076) holds.

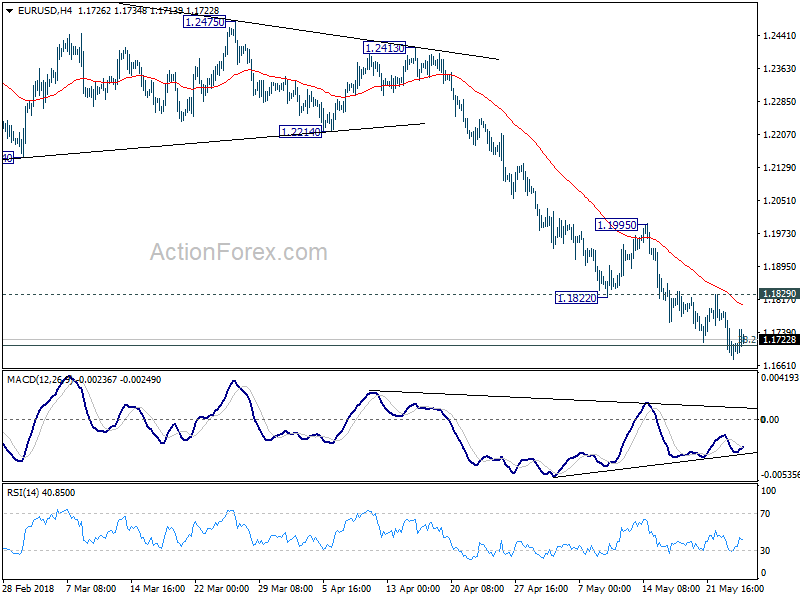

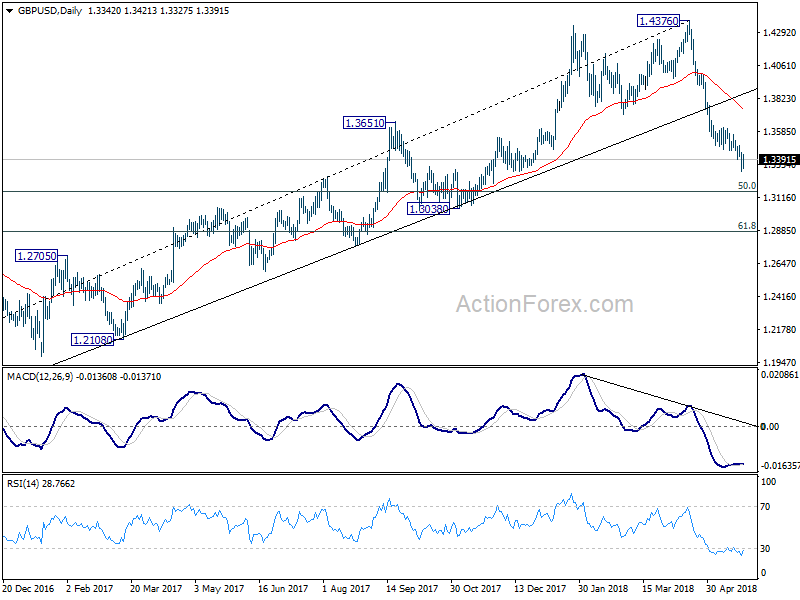

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3289; (P) 1.3366; (R1) 1.3427; More...

A temporary low is in place at 1.3303 in GBP/USD with today's recovery. Intraday bias is turned neutral for consolidations first. Upside should be limited by 1.3617 resistance to bring fall resumption. On the downside, below 1.3303 will extend the decline fro 1.4376 to 50% retracement of 1.1946 to 1.4376 at 1.3161. Break will target 61.8% retracement at 1.2874. Nonetheless, firm break of 1.3617 will confirm short term bottoming and bring stronger rebound.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4249). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 should now be firmly taken out. Next target will be 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3761) holds, even in case of strong rebound.

Trade Wars and Auto Tariffs Dominate the Markets, 10 Year Yield Losing 3% Handle

Sterling recovers mildly today as there was finally a piece of better than expected key data from the UK. Nonetheless, Swiss Franc outshines Sterling as the strongest one for today. And the Pound is still the weakest one for the week, followed by Euro. Canadian Dollar, on the other hand, is the weakest one for today, followed by Dollar and other commodity currencies. WTI crude oil dips back below 71 handle is a factor dragging the Loonie down. US's intention to impose auto tariffs also create additional uncertainty for NAFTA negotiations.

Trade war and protectionism back as the main theme in the markets today. US President Donald Trump has ordered Commerce Secretary Wilbur Ross to start a Section 232 national security investigation on auto imports. And he's considering to impose as much as 25% tariffs on import cars. Mexico, Canada, Japan, South Korea and Germany are major car importers to the US. Mexico and Canada combined export 4.2m cars to US in 2017. Hence, some saw the tariff as a move to force concessions in NAFTA talks.

It could also be a target to Germany which exported 0.5m cars to the US last year and is persistently having a trade surplus with US. South Korea will likely be alright as it was the first one to get permanent exemption from the steel tariffs, demonstrating it's strategic relationship with the US. Japan, however, could be a casualty again. It's the only close ally and top steel importer to the US who's not even given a temporary exemption on steel tariffs. And Japan, who sold 1.7m cars to the US in 2017, rely on vehicle exports for growth.

On the fundamental front, trade tensions, North Korea, Italy government will also remain on radar. But technical developments in bonds could drive some volatility in the markets again today. It now looks like US 10 year yield is kissing 3% handle goodbye. German 10 year bund yield also cannot get hold of 0.5%. Deeper fall in yield would drag down Yen pairs again.

Released from US, initial jobless claims rose 11k to 234k in the week ended May 19, above expectation of 220k. Four-week moving average of initial claims rose 6.25k to 219.75k. Continuing claims rose 29k to 1.741m in the week ended May 12. Four-week moving average of continuing claims dropped 23.25k to 1.752m, hitting the lowest since 1973. House price index rose 0.1% mom in March, below expectation of 0.5% mom.

UK retail sales bear market expectations, rose 1.6% mom in April

UK headline retail sales jumped 1.6% mom in April, much higher than expectation of 0.7%. Excluding auto and fuel, retail sales also jumped solidly by 1.3% mom, versus expectation of 0.4% mom.

The ONS noted that "the effects of the adverse weather on sales introduces further volatility to the monthly growth rate in April 2018." And, "combining March and April to compare the two months with the same two months a year earlier provides a more stable picture of the year-on-year growth".

Combining both March and April, sales grew 1.3% in 2018, much lower than 2.9% back in 2017.

ECB: Risks from protectionism had become more prominent

In the April meeting accounts, ECB offered not nothing new to the markets, but just a little more cautiousness. Despite recent moderation in activity, data remained consistent with "solid and broad-based expansion". And underlying economic strength added to the Governing Council's "confidence" that inflation will "gradually" move back to 2% target over medium term. But since underlying inflation remain subdued, without signs of sustained upward trend, "patience, persistence and prudence with regard to monetary policy remained warranted."

Risks to outlook remain "broadly balanced". But ECB pointed to "risks related to global factors, including the threat of increased protectionism". ECB noted that those risks "had become more prominent and warranted monitoring with regard to their implications for the medium-term outlook for growth and prices.

ECB Praet: There are some clouds despite good economic conditions

ECB Chief Economist Peter Praet said in in an event in Brussels today that economic conditions in Eurozone remain good. Recent data softness was partly due to temporary factors and "supply constraints" only. But he noted "there are some clouds and we should be watchful because that can go into confidence in a more fundamental way." Those clouds include the loose fiscal policy of Italy's new eurosceptic government, as well as international trade tensions.

ECB Governing Council member Vitas Vasiliauskas also noted that geopolitical factors would be analyzed before the central bank make a decision on its asset purchase program. In particular, Vasiliauskas noted the markets have already reacted to the Italian government change. And he said ECB has to take that into account.

EU Katainen: US auto tariffs probe very difficult to understand

European Commission Vice President Jyrki Katainen respond to the Trump's intention to impose new tariffs on automobile imports. Katainen criticized that would be "against the WTO" and "it's very difficult to imagine it to create any sort of threat to national security. He reiterated that "it's very difficult to understand".

But he also noted that "we have now just heard what has been said and there is a long journey to the practice ... We don't expect this to further complicate the issue. We just have to find a solution that is fair."

German Merkel welcomed in her visit to China

German Chancellor Angela Merkel is having a fruitful visit to China. Chinese Premier Li Keqiang said, in joint appearance with Merkel, that "China's door is open" and welcome German vehicle makes to invest there. Li also pledged that "if they come across any problems during their investment, especially when it comes to legal protections, I can clearly tell you that China is striding forward to being a country with rule of law."Li also said China has always supported a unified and prosperous Europe and that China and Germany uphold free trade.

Besides, Li also noted "the euro is an important choice in our foreign currency reserves, and so we are continuing to buy European debt." And, "even when certain European countries had sovereign debt crises, China kept the broader picture in mind."

In addition, Merkel also secured the support from China on the current Iran nuclear deal, despite US withdrawal.

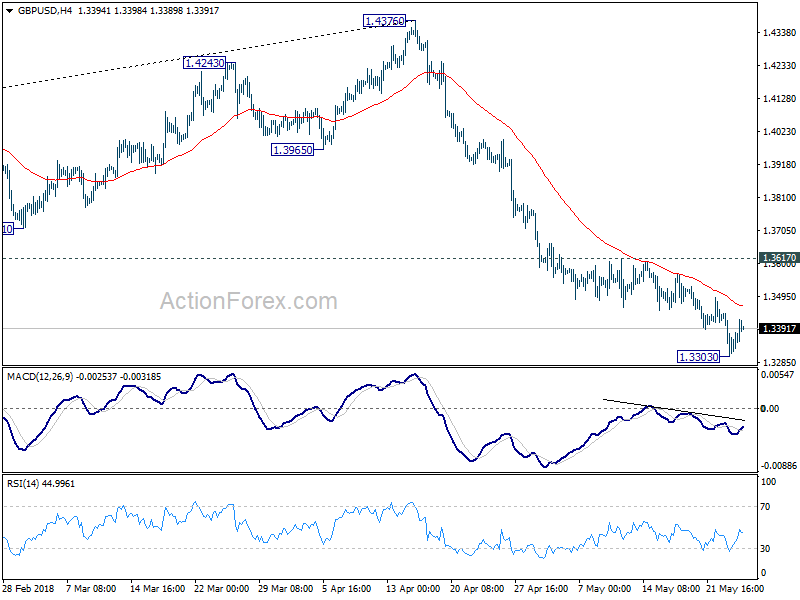

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3289; (P) 1.3366; (R1) 1.3427; More...

A temporary low is in place at 1.3303 in GBP/USD with today's recovery. Intraday bias is turned neutral for consolidations first. Upside should be limited by 1.3617 resistance to bring fall resumption. On the downside, below 1.3303 will extend the decline fro 1.4376 to 50% retracement of 1.1946 to 1.4376 at 1.3161. Break will target 61.8% retracement at 1.2874. Nonetheless, firm break of 1.3617 will confirm short term bottoming and bring stronger rebound.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4249). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 should now be firmly taken out. Next target will be 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3761) holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance Apr | 253M | 198M | -86M | -156M |

| 06:00 | EUR | German GDP Q/Q Q1 F | 0.30% | 0.30% | 0.30% | |

| 06:00 | EUR | German GfK Consumer Confidence Jun | 10.7 | 10.8 | 10.8 | |

| 08:30 | GBP | Retail Sales M/M Apr | 1.60% | 0.80% | -1.20% | -1.10% |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | USD | Initial Jobless Claims (MAY 19) | 234K | 220K | 222K | 223 |

| 13:00 | USD | House Price Index M/M Mar | 0.10% | 0.50% | 0.60% | |

| 14:00 | USD | Existing Home Sales Apr | 5.55M | 5.60M | ||

| 14:30 | USD | Natural Gas Storage | 92B | 106B |

US initial claims rose 11k to 234k in the week ended May 19

US initial jobless claims rose 11k to 234k in the week ended May 19, above expectation of 220k.

Four-week moving average of initial claims rose 6.25k to 219.75k.

Continuing claims rose 29k to 1.741m in the week ended May 12.

Four-week moving average of continuing claims dropped 23.25k to 1.752m, hitting the lowest since 1973.

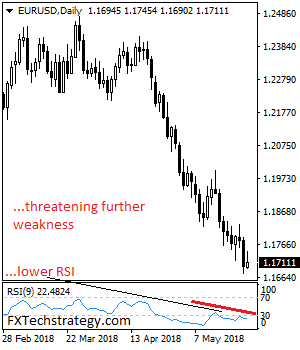

EURUSD – Declines, Looks To Weaken Further

EURUSD - The pair remains weak and vulnerable to the downside as it looks for trend continuation. On the upside, resistance comes in at 1.1750 level with a cut through here opening the door for more upside towards the 1.1800 level. Further up, resistance lies at the 1.1850 level where a break will expose the 1.1900 level. Conversely, support lies at the 1.1650 level where a violation will aim at the 1.1600 level. A break of here will aim at the 1.1550 level. Below here will open the door for more weakness towards the 1.1500. All in all, EURUSD faces further downside pressure.

DAX Steadies After Sharp

The DAX index is steady in the Thursday session, after sharp losses on Wednesday. Currently, the DAX is at 12,951, down 0.21% on the day. On the release front, Germany Final GDP dropped to 0.3%, matching the estimate. GfK Consumer Climate ticked lower to 10.7, just shy of the forecast of 10.8 points. Next up, the ECB will publish the minutes of its April policy meeting. On Friday, Germany releases Ifo Business Climate.

PMI reports disappointed on Wednesday and German stock markets responded with sharp losses. The DAX declined by 1.3 percent. Investors are particularly concerned that both German and eurozone manufacturing PMIs dropped for a fifth straight month. German Manufacturing PMI posted its weakest gain in 16 months, while the eurozone indicator posted its worst reading in 18 months. These numbers, while certainly disappointing, should not cause any alarm, as the PMIs continue to indicate expansion in the services and manufacturing sectors. Still, the fact that growth was softer than expected could give ECB policymakers reason to re-evaluate the planned wind-up of its stimulus program in September.

Earlier this week, US President Trump sounded skeptical over progress in trade talks between the US and China. On Tuesday, Trump said that he was ‘not really’ satisfied with the negotiations. Trump’s comments have confused the markets, as Treasury Secretary Steven Mnuchin declared on the weekend that the trade spat was ‘on hold’. Investor risk appetite has also waned as there is uncertainty whether North Korean leader Kim Jong-un will meet with President Trump next month. On Tuesday, Trump acknowledged that there was a ‘substantial’ chance that the summit planned with Kim in Singapore on June 12 would not take place.