Sample Category Title

UK GDP And US Durable Goods Due With Geopolitics Back In The Spotlight

Here are the latest developments in global markets:

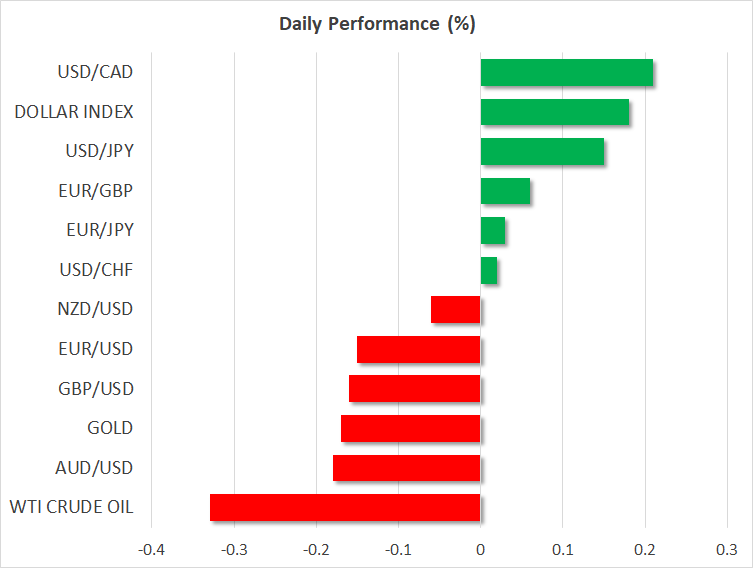

FOREX: The US dollar index – which tracks the greenback’s performance against a basket of six major currencies – is nearly 0.2% higher on Friday, ahead of a speech by Fed Chairman Jerome Powell. The index pulled back a little yesterday, mirroring a similar dip in longer-term US Treasury yields.

STOCKS: US markets closed lower on Thursday, as news that President Trump had cancelled his summit with North Korea weighed on risk sentiment. The Dow Jones fell by 0.30%, while the Nasdaq Composite and S&P 500 declined by 0.02% and 0.20% respectively. That said, sentiment seems to have reversed following a plea from North Korea overnight for a meeting “at any time”, with futures tracking the Dow, S&P, and Nasdaq 100 all pointing to a higher open today. In Asia, Japan’s Nikkei 225 ticked up by 0.06%, but the Topix edged down 0.22%. In Hong Kong, the Hang Seng fell 0.47%. Meanwhile in Europe, futures tracking the major indices were a sea of green, pointing to a notably higher open for all benchmarks today.

COMMODITIES: Oil prices tumbled yesterday and are lower today as well, amid hints from major producers that they may “open the taps” soon and increase production. WTI is down by nearly 0.35% on Friday and Brent by 0.45%, after Russian Energy Minister Alexander Novak hinted on Thursday that the OPEC & non-OPEC supply cuts may be slowly phased out after next month’s OPEC meeting. In precious metals, gold is down by almost 0.2% today, giving back some of the gains it posted yesterday following the cancellation of the US-North Korea summit. Prices surged to break back above the psychological $1300 mark but remain stuck below the crucial 200-day moving average, which keeps the technical picture cautiously negative for now.

Major movers: Risk aversion lingers as geopolitics come back under the spotlight

Another round of risk aversion hit the markets on Thursday, this time following news on the geopolitical front that US President Trump had canceled his planned summit with North Korea’s leader. The news ignited renewed demand for safe-haven currencies such as the Japanese yen and Swiss franc, while gold prices jumped as well. Yields on 10-year US Treasuries declined, signaling that investors turned back to bonds amid a flight to safety, while US equity markets closed lower.

Friday seems to be a different story though, with most of the aforementioned moves starting to reverse during the Asian trading session. Safe havens are lower, US equity futures are pointing to a higher open and US Treasury yields are up, all of which suggest that the pessimistic sentiment is easing. The reversal is likely owed to headlines overnight signaling North Korea is softening its stance even further, after the nation released a statement suggesting it is “open to resolving problems” with the US “at any time in any way”.

This was quite a sudden change of heart from North Korea, considering that just a couple of days ago it hinted at a “nuclear-to-nuclear showdown” with the US, which was also the reason cited by Trump for calling off the summit. While the motivation behind this turnaround is far from clear, in the market’s eyes it appears North Korea’s plea for a new meeting was a positive development that reduces the risk of further escalation.

Elsewhere, the minutes from the latest ECB meeting did not reveal anything new. If anything, the account was slightly on the dovish side, as it indicated that policymakers thought a more pronounced weakening of demand cannot be ruled out and that the uncertainty surrounding the outlook had increased. The euro reacted little to the release and finished the day lower against the yen and the pound, but higher versus the dollar.

The political situation in Italy, which has not been cleared up yet, and the continued signs of a loss of momentum in Eurozone’s economy are still posing headwinds for the common currency. That said, the recent dip in US Treasury yields appears to have taken some steam out of the dollar, which has probably been a factor keeping euro/dollar from touching fresh lows.

Day ahead: UK GDP, US durable goods and University of Michigan survey on the agenda; geopolitics also monitored

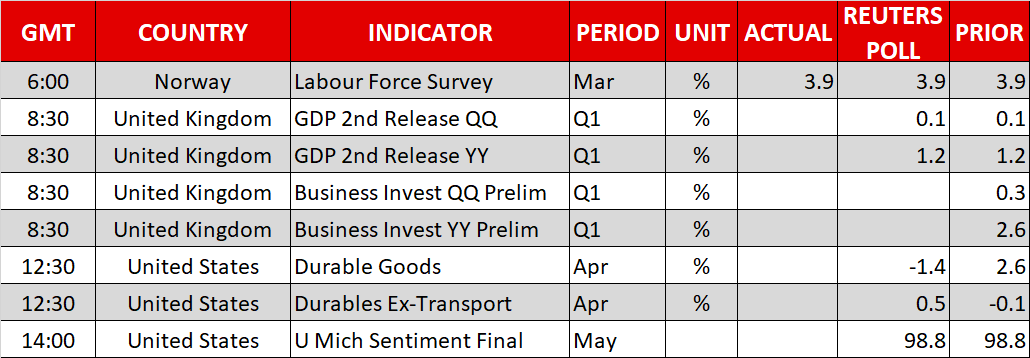

Friday’s economic calendar is rather light, featuring the second release of Q1 GDP growth out of the UK, durable goods orders out of the US and the University of Michigan’s survey on consumer sentiment.

At 0830 GMT, updated estimates on Q1 GDP growth will be made public out of the UK. The pace of growth is expected to be confirmed at 0.1% q/q and 1.2% y/y, reflecting a slowdown relative to Q4’s respective figures of 0.4% q/q and 1.4% y/y. First-quarter preliminary data on Q1 UK business investments are scheduled for release at the same time.

US durable goods orders for April are due at 1230 GMT. Orders are anticipated to decline for the second straight month, and specifically to contract by 1.4% m/m after rising by 2.6% in March. The previous month’s figures also reflected the largest fall in demand for machinery in almost two years. Core durable goods, that exclude transport, will also be watched by market participants.

Also out of the US is the University of Michigan final survey gauging consumer morale in May. The relevant index is expected to be confirmed at 98.8, the same as in April. Other information, such as the sub-index on inflation expectations, will also be of interest.

Of importance to currency markets, but also equity, commodity and fixed income ones, are geopolitical developments as well. After yesterday’s US-North Korea summit fallout, North Korea expressed willingness to get into talks, easing some concerns. Any updates on the story will be closely watched as they can affect flows in and out of safe-haven assets, such as gold. Another story that will be monitored pertains to the Italian political situation and on the individuals the two anti-establishment parties – 5-Star Movement and League – will choose to serve on key government positions.

The US Baker Hughes oil rig count is due at 1700 GMT.

Fed chief Jerome Powell together with numerous regional Fed presidents, Bank of England Governor Mark Carney, ECB executive board member Benoit Coeure and Bundesbank President Jens Weidmann – considered by some as Mario Draghi’s likely successor to head the ECB – will be among those attending the Riksbank’s 350th conference. Specifically, Powell will be participating in a discussion on “Financial Stability and Central Bank Transparency” at 1320 GMT.

Also on the agenda is the St. Petersburg Forum. Russian President Vladimir Putin, French President Emmanuel Macron, Japanese Prime Minister Shinzo Abe and IMF Managing Director Christine Lagarde will be among those participating in panel discussions. Meanwhile, European Union finance ministers will be discussing the latest developments on Brexit deliberations in Brussels.

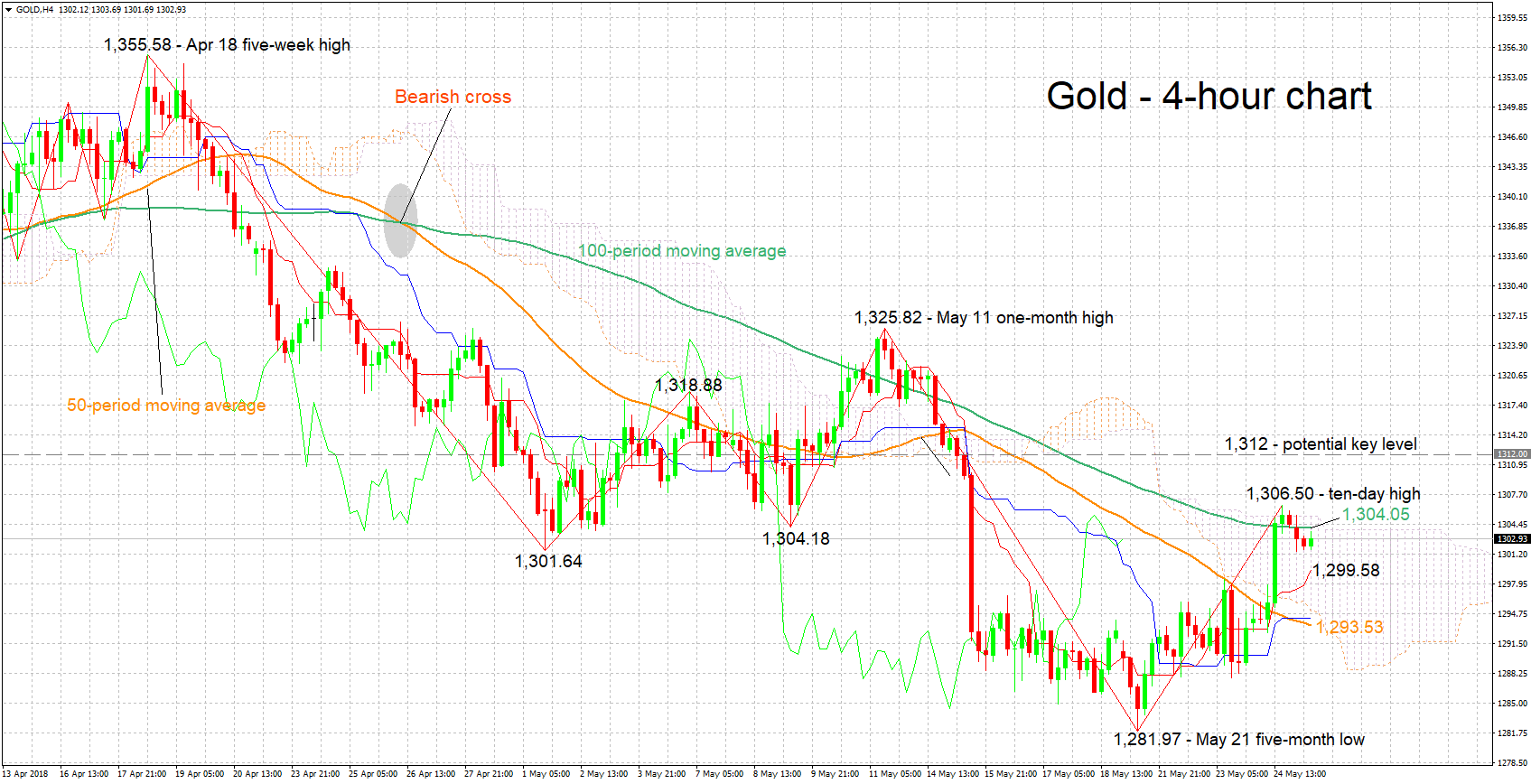

Technical Analysis: Gold close to 10-day high; bullish momentum seems to ease

Gold touched a 10-day high of 1,306.50 on Thursday, while it is currently trading in proximity to this peak. The Tenkan-sen is above the Kijun-sen line, this being a positive short-term signal, though notice that the Kijun-sen has flatlined. The latter is an indication that bullish momentum is easing.

Rising geopolitical uncertainty is likely to boost the safe-haven perceived asset. Immediate resistance seems to be taking place around the current level of the 100-period moving average line at 1,304.05. The area around this level includes a bottom from the recent past (1,304.18), yesterday’s 10-day high (1,306.50), and the Ichimoku cloud top (1,305.36). Further above, the region around 1,312 was congested in previous weeks and may be of significance.

Conversely, easing uncertainty could divert funds out of gold and into riskier assets. Support to declines might come around the current level of the Tenkan-sen at 1,299.58; the region around this encapsulates the 1,300 round figure and a trough from early May at 1,301.64. Sharper losses would turn the attention to the area around the 50-period MA at 1,293.53.

Gold is denominated in dollars and the direction of the greenback can also affect the precious metal; a weaker US currency is projected to support the yellow metal and vice versa.

Yesterday, Core Bonds Continued Trading With A Positive Bias

Markets

Yesterday, core bonds continued trading with a positive bias. Several (geo)political issues were pending. European bond investors still pondered the potential impact of mediocre eco data for ECB policy going forward. The safe haven bid for bonds intensified as US president Trump cancelled the meeting with North Korea's Kim Jung Un. However, the risk-off reaction was modest and petered out later in US dealings. US yields declined between 1.1bp (5y) and 2.7 bps (30-y). Bunds outperformed (yields declining between -1.6 bps (2-y) and -4.8 bps for 30-y). On the Intra-EMU markets, Italian spreads couldn't maintain an initial narrowing (10-y + 3bps). Most other peripheral markets succeeded a modest tightening (-2 bpsfor Spain and Portugal, -7 bps for Greece). Investors took a wait-and-see approach on Italy, awaiting the composition of the new government. This morning, Asian markets are reacting calmly to the cancelation of the US-North Korea meeting. Regional equities mostly shows modest losses. US equity futures are rebounding and US yields are rising slightly. Later today, IFO German business confidence will be published. In the US, the durable goods orders and the final U of Michigan consumer confidence will be published. The German IFO release takes centre stage. A stabilisation is expected (98.5 vs 98.7 for the expectations). Of late several EMU data pointed to a substantial cooling of the EMU growth momentum. Will the Ifo confirm this trend? After the decline in German/EMU yields, quite some bad news should already be discounted. Even so, the Bund contracts (160 area) and the German 10-y yield is closing in on key technical levels (0.47%/0.5%). We maintain the working assumption that these levels shouldn't be re-broken if the European economy remains on an acceptable growth path and if the prospect for ECB normalisation later this year and next year remains in place. However, given recent eco developments and given the uncertainty on Italy, we keep a close eye how the test evolves. Aside from the data, several ECB and Fed members will speak.

Yesterday, the dollar traded with a slightly negative bias. EUR/USD tried a rebound off the 1.17 area but the move had no strong legs. USD/JPY drifted back south to test the 109 area, but rebounded later in line with equities. A very poor German Ifo release would probably be a negative for the euro. However, as is the case for EMU/German yields, we have the impression that quite some euro negative news should already be discounted. That said, if sentiment on risk (US equities) holds up relatively well and the decline in US yields would halt, this is maybe still some room for further USD gains short-term, both against the euro and the yen.

Yesterday, UK April retail sales were stronger than expected. The provided a temporary support for sterling. However, day didn't change overall investor expectations on the path for future BoE rate hikes. EUR/GBP closed the session little changed in the 0.8760 area. Headlines from the EU-UK Brexit negotiations suggest that little progress has been made. Today, the details of the UK Q1 GDP will be published. The composition of GDP is interesting info on the status of the UK economy, but we don't expected it to have a meaningful impact on sterling trading. More consolidation of EUR/GBP in the 0.87 big figure might be on the cards.

News Headlines

Yesterday US President Donald Trump cancelled a summit with North Korea's Kim Jong Un. Trump said it would be 'inappropriate' after the 'tremendous anger' displayed by Pyongyang but held out the prospect of a new meeting. North Korea replied it is still willing to meet Trump and that it is open to 'resolving problems at any time in any way'.

BoE's Carney issued a warning on the dangers of a 'disruptive Brexit', saying they would be forced back into some of the same measures they pursued in the aftermath of the Brexit referendum if the 'transition isn't smooth'.

US Commerce Secretary Wilbur Ross will visit China early next month for another round of talks amid ongoing trade frictions between the world's two largest economies. (Reuters)

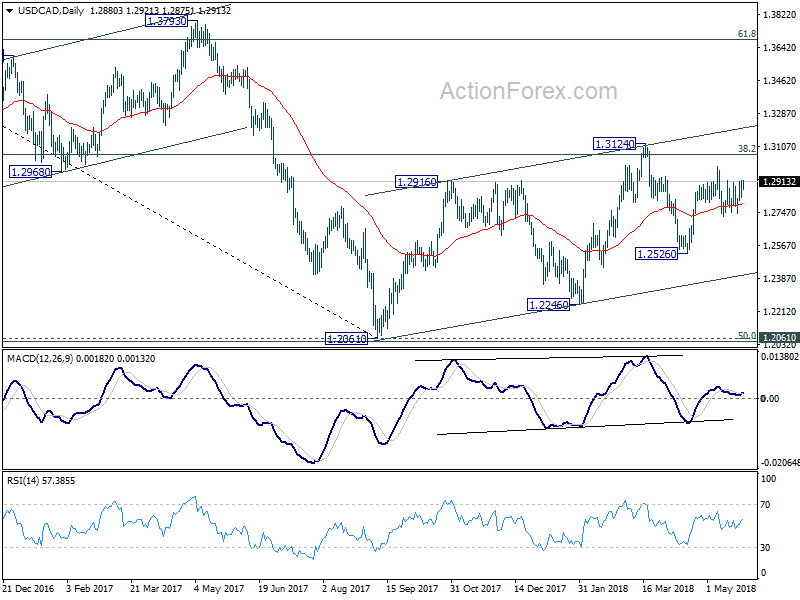

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2788; (P) 1.2856; (R1) 1.2905; More.....

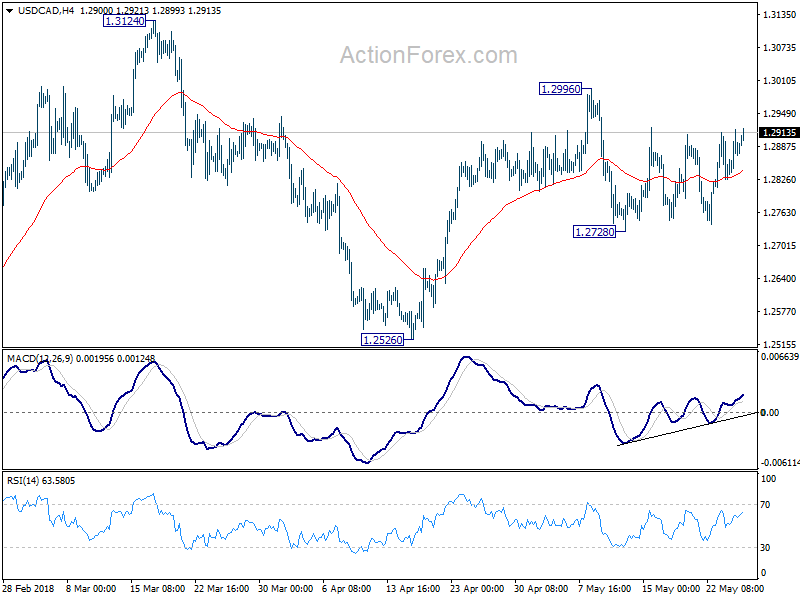

Intraday bias in USD/CAD remains neutral as it's bounded in range of 1.2728/2996. We'd maintain our view that price actions from 1.3124 as a corrective move that could be completed at 1.2526 already. Break of 1.2996 will turn bias to the upside and extend the rise from 1.2526 to 1.3124 key resistance next. However, break of 1.2728 will dampen this bullish view and bring deeper fall back to 1.2526 and possibly below.

In the bigger picture, we're favoring the case that that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

Equity Markets Trade Mixed After US Cancellation Of North Korea Summit

General Trend:

- Automakers in Asia remain weaker after recent US auto imports probe announcement

- Shares of Samsonite [1910.HK] remain under pressure following report by short-seller

- Yen (JPY) trades generally weaker, led by declines in JPY/KRW

- Corporate defaults remain a topic in the Chinese press

- Reserve Bank of Australia (RBA) faces temporary labor strike

- US Commerce Sec Ross to visit China from June 2-4th to discuss trade - Xinhua

Headlines/Economic Data

Australia/New Zealand

- ASX 200 opened -0.3%; closed flat

- ASX 200 Energy index -1.5%, Resources -1.4%, REIT -0.5%; Telecom +2.8%, Consumer Discretionary +1.5%, Financials flat

- (AU) Australia banknote printer workers said to plan to go on temporary strike, seeking pay increase of 4%; Note Printing Australia is owned by the Reserve Bank of Australia (RBA) – Australian Press

- (AU) Australia sells A$500M v A$500M indicated in Nov 2029 bonds, avg yield 2.8273% v 2.8181% prior, bid to cover 5.21x v 3.57x prior

- (AU) Australia to sell new May 21, 2030 bond during week of June 4th

China/Hong Kong

- Shanghai Composite opened -0.2%, Hang Seng -0.3%

- Hang Seng Energy index -3.4%, Telecom -0.7%, Info Tech -0.6%; Consumer Goods +0.8%, Materials +0.8%, Industrial Goods +0.5%, Financials flat

- Rusal [486.HK]: Says Oleg Deripaska resigns as non-executive board member; effective May 25 2018

- (CN) China NDRC said to plan to hold a meeting with miners and utilities later today related to coal prices - US financial press

- (CN) China regulator said to urge sellers of bonds to manage cash flows; Official rules out systemic risks related to bond defaults - Chinese Press

- (CN) China PBoC Open Market Operation (OMO): Skips OMO v CNY40B injected in 7 and 14-day reverse repos prior: Net: v CNY0B prior

- (CN) For the week, the PBOC drained a net of CNY30B through OMOs v CNY410B net injection w/w

Japan

- Nikkei 225 opened -0.3%; closed +0.1%

- TOPIX Marine Transportation index -1.7%, Iron & Steel -1.5%, Real Estate -1.5%, Information & Communications -0.7%, Securities -0.3%

- Automakers remain weaker

- Softbank and other telecoms decline: Japan government said to issue guidance to Softbank related to phone discounts (Japanese press)

- Fast Retailing +0.8% (declined over 1% on prior session)

- (JP) Japan May Tokyo CPI Y/Y: 0.4% v 0.5%e; Ex-Fresh Food (Core) Y/Y: 0.5% v 0.6%e

- (JP) Japan Fin Min Aso: Financial sanctions against North Korea may be prolonged after cancellation of US/North Korea summit

- (JP) Japan Chief Cabinet Sec Suga: Sees progress as more important than holding summit with North Korea

Korea

- Kospi opened -0.5%

- Samsung rises after Apple patent ruling; The ruling ordered Samsung to pay ~$533M in damages vs the $1B in damages that Apple had sought.

- (KR) North Korea Vice Foreign Min Kim Kye Gwan: Willing to talk with US at 'any time'; no change in will to do the best for peace - KCNA

- (KR) Pres Trump sends letter to North Korea's Kim: says inappropriate to have June 12 summit at this time; looks forward very much to meeting some day; The anger and open hostility in your most recent statement makes a meeting inappropriate at this time

- (US) Pres Trump: Possible existing summit could take place or it could take place at a later date

Other

- IMF Deputy Managing Dir Zhang: Short-term outlook for Asia and global economies is ‘strong’; Low inflation in Asia mainly due to temporary factors

- (ID) Indonesia Rupiah (IDR) on track to trade lower for the 6th straight week – US financial press

- (MY) Malaysia Finance Minister Lim Guan Eng said the government will honor all payments on debt raised by state investment fund 1MDB – financial press

- (SG) Singapore Apr Industrial Production M/M: 0.2% v 1.2%e; Y/Y: 9.1% v 8.0%e

- Nanya Technology [2408.TW]: Said to see sales growth on higher DRAM prices (Taiwanese Press)

North America

- US equity markets closed mixed: Dow -0.3%, S&P500 -0.2%, Nasdaq flat, Russell 2000 flat

- S&P500 Energy -1.7%, Financials -0.8%

- (US) NY Fed Survey of Primary Dealers: expect 3 more Fed rate hikes this year (responses submitted between 4/19-4/23)

- (US) According to Fed data, foreign holdings of US Treasuries declined for the 4th straight week – FT

- (BR) Brazil Gov't: Has reached 'deal' with certain truckers unions, under the agreement the nationwide strike will end for 15 days

Europe

- (UK) BOE Gov Carney: the gentle path for rate hikes expected by BOE is dependent on GDP growing faster than the 1.5% trend rate; Rates might rise quicker than the path described in May if investment recovers much more robustly; Brexit will be key factor in BOE rate policy; Uncertainty about consumer spending is elevated due to slower consumer lending and spending and the state of the housing market

- (ES) PSOE Leader Sanchez reportedly considering triggering no confidence vote against Spain PM Rajoy following corruption verdict this morning – press

- (SA) Saudi Oil Min Falih: Aims for balancing and not 'over correction' of oil market, Easing OPEC+ caps is on the table but no decision yet

- (RU) Russia Energy Min Novak: OPEC+ will in June for sure discuss easing caps

- (RU) Russia Energy Min Novak: the global oil glut is over

Levels as of 02:00ET

- Hang Seng -0.4%; Shanghai Composite -0.2%; Kospi -0.2%

- Equity Futures: S&P500 +0.3%; Nasdaq100 +0.4%, Dax +0.2%; FTSE100 +0.2%

- EUR 1.1705-1.1727 ; JPY 109.12-109.76 ; AUD 0.7561-0.7583 ;NZD 0.6923-0.6939

- Jun Gold -0.2% at $1,301/oz; Jun Crude Oil -0.1% at $70.66/brl; Jul Copper -0.2% at $3.094/lb

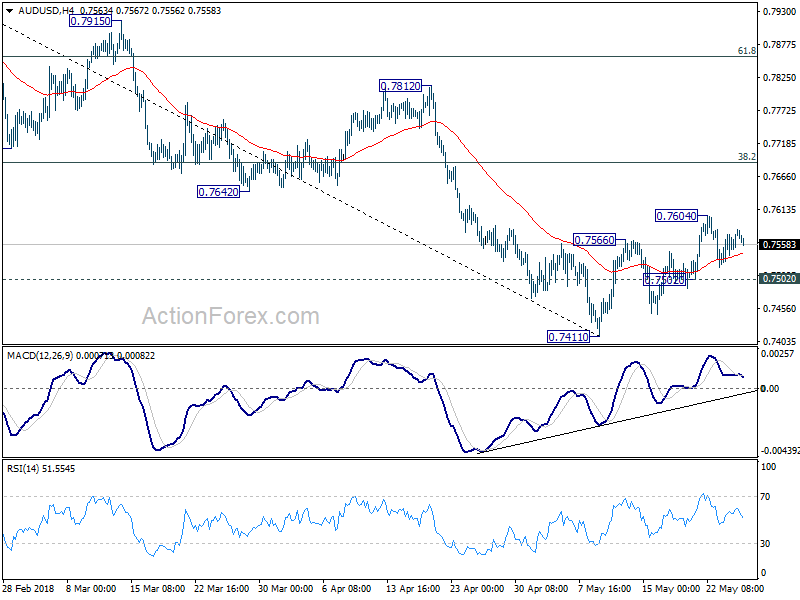

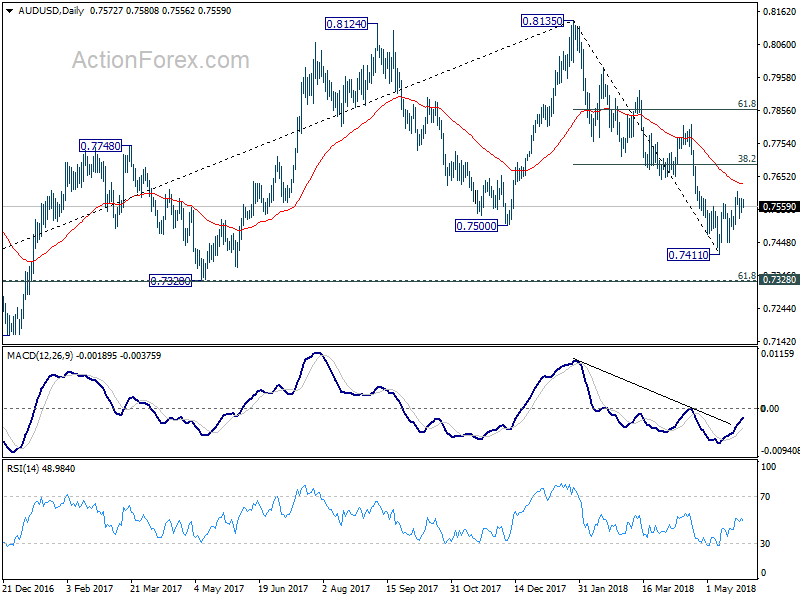

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7551; (P) 0.7568; (R1) 0.7593; More...

Intraday bias in AUD/USD stays neutral for the moment. While corrective rise from 0.7411 could extend, we'd expect strong resistance from 38.2% retracement of 0.8135 to 0.7144 at 0.7688 to limit upside and bring decline resumption eventually. On the downside, below 0.7502 minor support will argue that the corrective rise is completed and bring retest of 0.7411 low. Firm break there will resume the fall from 0.8135 and target cluster support at 0.7328 (61.8% retracement of 0.6826 to 0.8135 at 0.7326).

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Break of 0.7500 key support suggests that such correction is completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

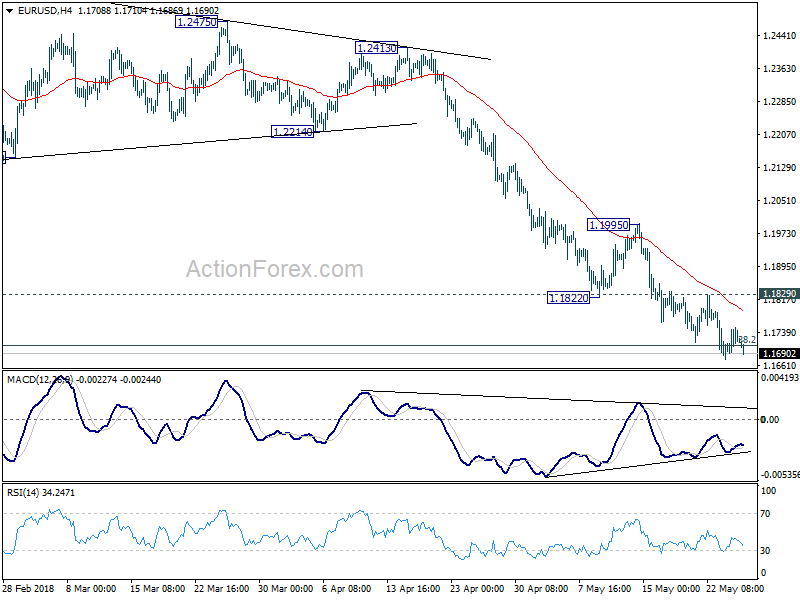

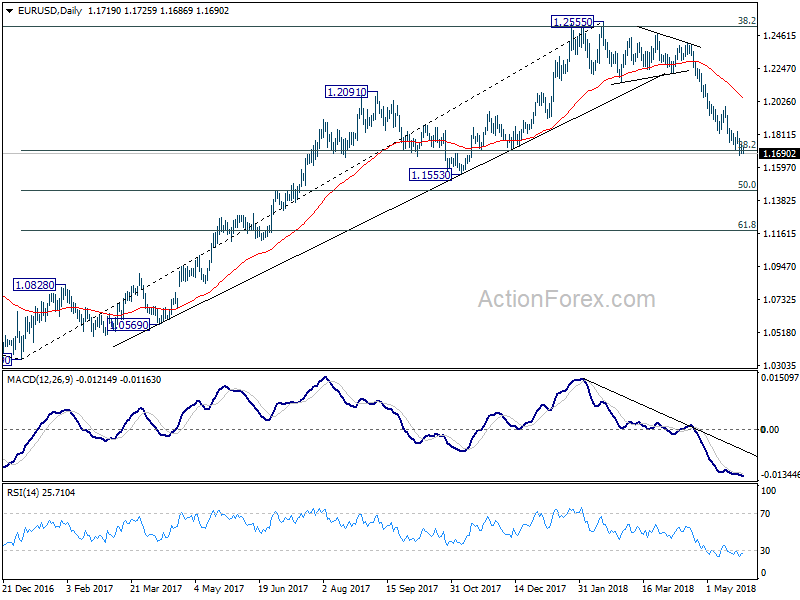

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1691; (P) 1.1720 (R1) 1.1750; More.....

Intraday bias in EUR/USD remains on the downside for the moment. The fall from 1.2555 is still in progress and should target 50% retracement of 1.0339 to 1.2555 at 1.1447 next. Though, considering bullish convergence condition in 4 hour MACD, break of 1.1829 minor resistance will suggest short term bottoming. And, lengthier consolidation would be seen in this case, before staging another fall.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will pave the way to 61.8% retracement at 1.1186. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2076) holds.

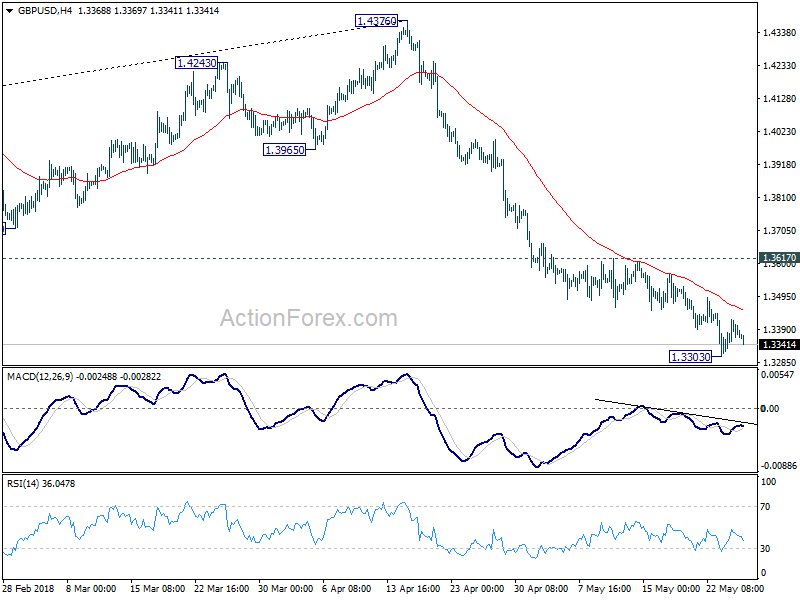

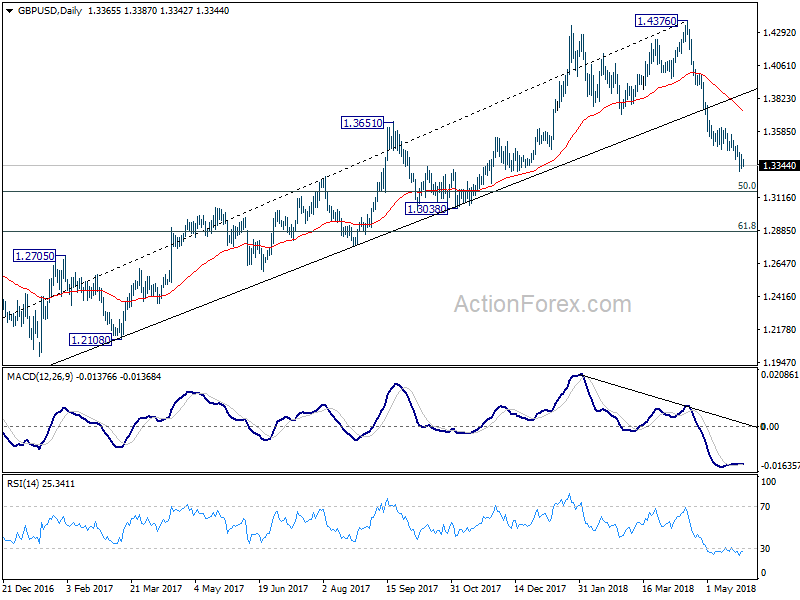

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3333; (P) 1.3377; (R1) 1.3426; More...

Intraday bias in GBP/USD remains neutral for consolidation above 1.3303. Another rise cannot be ruled out. But upside should be limited by 1.3617 resistance to bring fall resumption. On the downside, below 1.3303 will extend the decline fro 1.4376 to 50% retracement of 1.1946 to 1.4376 at 1.3161. Break will target 61.8% retracement at 1.2874. Nonetheless, firm break of 1.3617 will confirm short term bottoming and bring stronger rebound.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4249). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 should now be firmly taken out. Next target will be 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3761) holds, even in case of strong rebound.

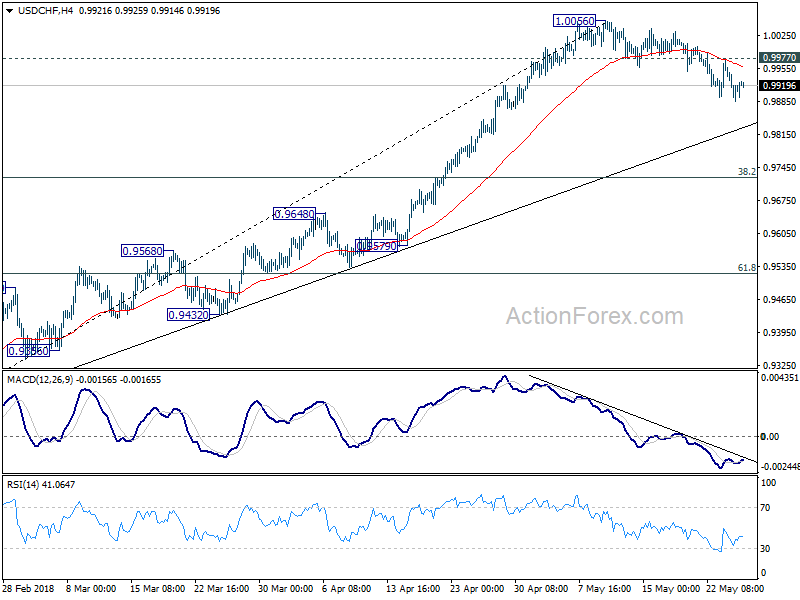

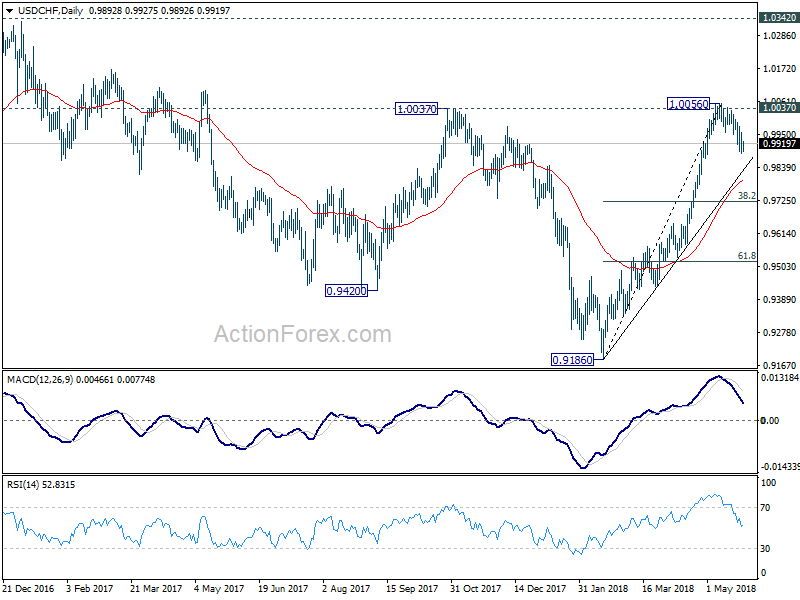

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9877; (P) 0.9921; (R1) 0.9956; More...

With 0.9977 minor resistance intact, correction from 1.0056 could extend lower. But we'd expect strong support from trend line (now at 0.9830) to contain downside and bring rebound. On the upside, above 0.9977 will suggest that the pull back is finished and bring retest of 1.0056 high.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

Italian Government Bond Yield Spreads Tightened Versus Germany

Market movers today

In the US, capital goods orders figures are due for release. Overall, business investments have been increasing since 2016 but over the past couple of months numbers have moved sideways – probably due to lower growth in the manufacturing sector. Figures for April will give us an impression of whether investments have stabilised temporarily or more persistently.

In the UK, the second estimate of GDP growth in Q2 will also attract attention for two reasons. The first is because the initial estimate of only 0.1% q/q was lower than expected by most economists. The second is because it is the first time we get the expenditure components so that we can see why growth was weak from a demand perspective.

In the euro area, German ifo expectations are released, where consensus is for another decline following the weak PMI numbers earlier this week.

In Scandinavia, today's key release will be Norwegian unemployment data for May (see next page).

Selected market news

Yesterday was another session with risk-off sentiment in global financial markets amid geopolitical tensions with the US-North Korean summit cancellation. In general, global equity markets where under pressure and 10-year US and German government bond yields edged lower.

Yesterday, Italian government bond yield spreads tightened versus Germany from the morning after President Sergio Mattarella approved Giuseppe Conte's nomination as premier Wednesday. During yesterday's session though, Italian government bond yield spreads re-widened versus Germany. We expect a slow convergence between Italian government bonds relative to the core EU in the coming months, but there are a number of risk factors ahead.

ECB minutes for the April meeting released yesterday revealed little news. On the back of the minutes German government bonds continued the rally, most likely in line with other ‘usual' risk-off dynamics, which sent the 10-year German government bond yield some basis points below the 0.5% level.

In the US, Fed Chairman Powell speaks today. The FOMC minutes released Wednesday showed that the Fed discussed the recent flattening of the US yield curve. Hence, amongst other things, it will be interesting to look for further Fed thoughts on the risk of a yield curve inversion and potential impact on Fed's monetary policy.

US President Trump Pulls Out Of Peace Summit With North Korea

The US President dominated headlines and moved the market again yesterday when he wrote a letter to the North Korean Leader announcing his decision to pull out of the upcoming summit. The market reacted violently with traders seeking safety and sending stocks lower and the USD falling with USDJPY falling from 109.750 to 108.950 but the move faded into the US close and in the Asian session overnight. EURUSD rallied to 1.17500 and GBPUSD rallied to 1.34140 but have moved lower since. Gold tested resistance at the 1305.50 area while Oil fell from $71.68 to $70.50 support. The beleaguered USDTRY fell to lows at 4.55693 yesterday as the CBRT emergency hiked lending rates by 300 bps to counter the currency moves but moved higher with the dollar to 4.80556. It is currently trading around 4.78444. The CBRT is due to meet again on the 7th of June.

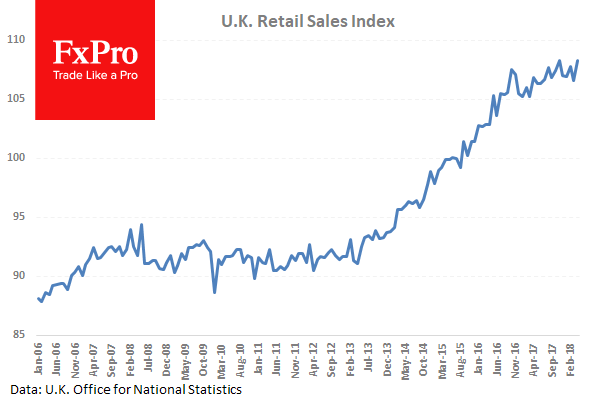

UK Retail Sales (YoY) (Apr) was 1.4% against an expected 0.1% from 1.1% previously which was revised up to 1.3%. Retail Sales (MoM) (Apr) was 1.6% against an expected 0.7% from a prior -1.2% which was revised up to -1.1%. Retail Sales ex-Fuel (YoY) (Apr) was 1.5% against an expected 0.1% from 1.1% previously which was revised up to 1.3%. Retail Sales ex-Fuel (MoM) (Apr) was 1.3% versus an expected 0.4% against a prior -0.5%. Yearly figures were expected to show a decrease but beat the consensus and exceeded last month’s readings. The monthly numbers exceeded expectations and show a jump in sales. This is a volatile data set but it does give a view on consumer spending. GBPUSD moved higher from 1.33838 to 1.34210 following this data release.

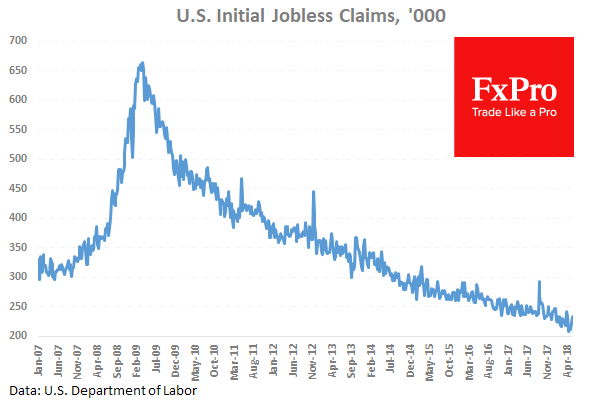

US Continuing Jobless Claims (May 11) were 1.741M versus an expected 1.754M against 1.707M previously which was revised up to 1.712M. Initial Jobless Claims (May 18) were 234K versus an expected 220K against 222K previously which was revised up to 223K. This data is showing an increase in the number of new claims.

US House Price Index (MoM) (Feb) was 0.1% against an expected 0.5% from 0.6% previously. This data slipped lower again after a strong improvement in the March reading.

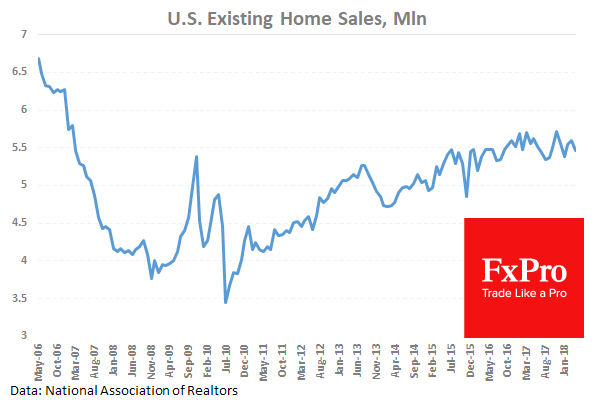

US Existing Home Sales (MoM) (Mar) were 5.46M versus an expected 5.57M against 5.60M previously. After reaching a seven year high in November at 5.81M, this data point had slipped lower over the following months signalling a little softness in the sector but recovered somewhat last month and in March. That recovery stalled with this reading. USDJPY initially moved higher from 109.558 to 109.723 as the jobs data hit but dropped to a low of 108.948 after housing data came in weaker coupled with the US/North Korea news.

EURUSD is down -0.11% overnight, trading around 1.17060.

USDJPY is up 0.30% in the early session, trading at around 109.567

GBPUSD is down -0.10% this morning trading around 1.33658.

USDCAD is up 0.22% overnight, trading around 1.29092

Gold is down 0.19% in early morning trading at around $1,302.03

WTI is down -0.30% this morning, trading around $70.47