Sample Category Title

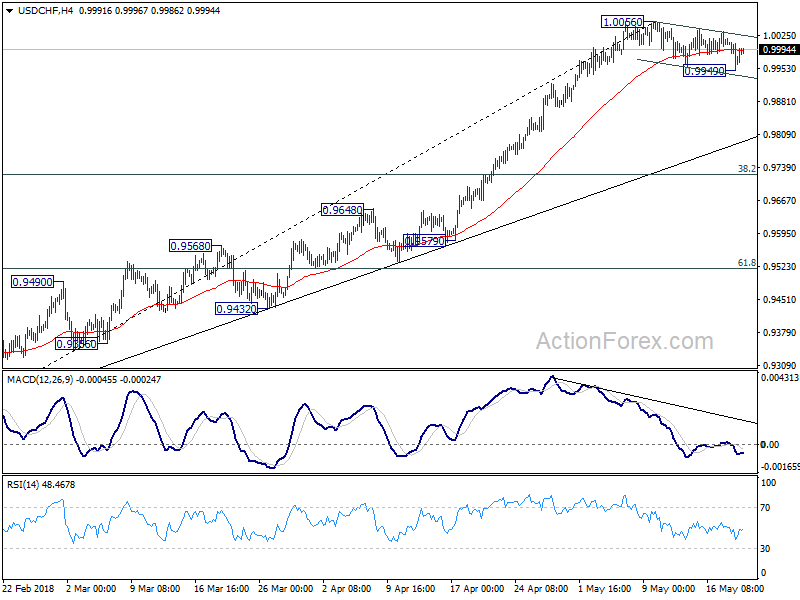

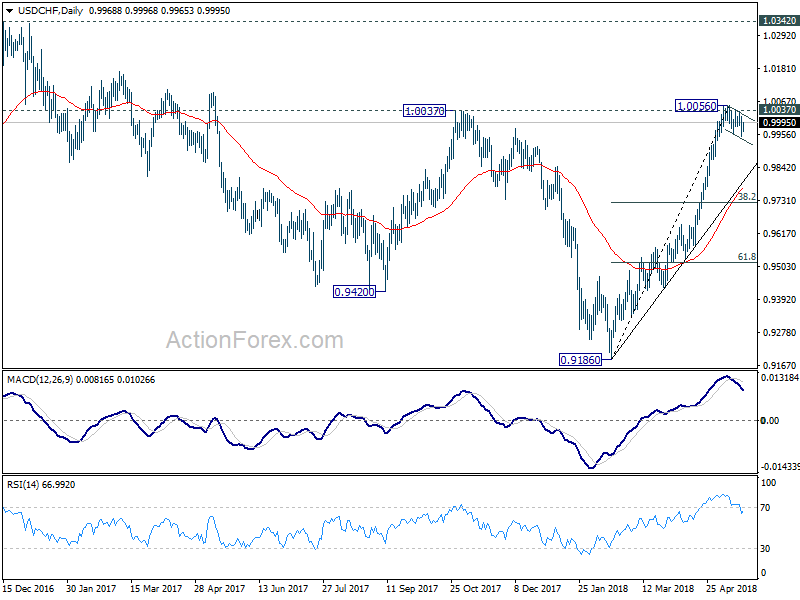

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9943; (P) 0.9983; (R1) 1.0015; More...

Intraday bias in USD/CHF is turned neutral again with today's recovery. Overall, price actions from 1.0056 are seen as a corrective pattern. Deeper pull back cannot be ruled out. But we'd expect strong support from trend line (now at 0.9799) to contain downside to bring rebound. On the upside, firm break of 1.0056 will confirm rise resumption for 1.0342 key resistance.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

Yen Lower as Receding Trade War Fears Lifts Risk Appetite, Dollar Extending Rally

Yen suffers broad based selling in today as lifted by return of risk appetite. Asian equities trade generally higher on receding fear of US-China trade war. The joint statement released on Saturday is seen as a "vow" to avoid trade war. It's affirmed by comments from US Treasury Secretary Steven Mnuchin that it's "on hold". Nikkei close up 0.31% at 23002.37. HK HSI is up 1% at the time of writing. In the currency markets, Australian, Canadian and US Dollar are the strongest one so far. New Zealand Dollar follows as Yen as the second weakest after poor retail sales data.

Technically, GBP/USD's downside breakout catches most attention as the fall from 1.4376 finally resumes. USD/JPY and EUR/USD are extending recent dollar bullish move. A question in mind is whether USD/CHF's consolidation from 1.0056 has completed. Also, AUD/USD and USD/CAD are kept in range so far and need more stimulus for a breakout.

US-China joint statement vowing not to launch a trade war

US and China issued a joint statement on Saturday to conclude the trade talks with Chinese Vice Premier Liu He on May 17 and 18. There was no mentioning of any number, but the statement said there were "consensus on taking effective measures to substantially reduce" US trade deficit in goods with China. And, China agreed to "significantly increase purchase" of US goods and services.

Additionally, there would be "meaningful increases" in US agriculture and energy exports to China, "expanding trade" in manufactured goods and services, encouraging "two-way investment" with "fair, level playing field for competition". China also pledged to work on laws and regulations on intellectually property protections.

The Chinese State-owned Xinhua news agency described the statement as "vowing not to launch a trade war against each other". Full statement could be found here.

Mnuchin: Trade war with China on hold

Commenting on the US-China joint statement on trade, Treasury Secretary Steven Mnuchin said "we are putting the trade war on hold." And he added, "we have agreed to put the tariffs on hold while we try to execute the framework", referring to the agreement.

Trump's top economic adviser Larry Kudlow said they made "a lot of progress", even surpassed their own expectation after the Beijing meeting. But it's not at the stage of taking the threat of tariffs on USD 150B of products yet. And, it's "too soon to lock that (USD 200B reduction in trade deficit) in" yet. Though he emphasized that "the direction here is the key".

Kudlow also added that Commerce Secretary Wilbur Ross will go to China and "looking into a number of areas where we're going to have greatly significant increases," including energy, liquefied natural gas, agriculture and manufacturing".

NAB pushed forecast of first RBA hike away to May 2019

The National Australia Bank finally gave up on their forecast of an RBA rate hike within 2018. Their expectation on the next move is now pushed from November to May 2019. The change put them back in line with market pricing, as well as with other major bank forecasters.

RBA chief economist Alan Oster noted that the " change reflects the fact there is no sign yet of stronger wages growth and unemployment has been stuck around 5.5% for the best part of a year." Also, he added that once the tightening cycle starts "further rate increases will be very gradual". And after the first move in May 2019, the next move will be "not until November 2019".

Oster also noted that the economy is still expected to strengthen and lead to falling unemployment. And that should "eventually translate into stronger wages growth and give the RBA confidence that inflation will track back to its 2.5% target". However, there is "considerable uncertainty around the timing at which wages growth will strengthen".

New Zealand retail sales grew 0.1% qoq in Q1, big disappointment

New Zealand retail sales was a big disappointment to the markets. Ex-inflation retail sales volume grew merely 0.1% qoq in Q1, much lower than expectation of 1.0% qoq. That's also a sharp slowdown from Q4's 1.4% qoq. Besides, it's the weakest quarter since 2015.

Stats NZ noted in the release that "retail spending in the first three months of the year was relatively flat despite rising job numbers, high migration, and record international tourism."

"Of the 15 retail industries, seven had higher sales volumes in the March 2018 quarter, and eight experienced lower sales volumes."

Looking ahead, big week for Euro and Sterling

The calendar is rather empty today with Swiss, France, Germany and Canada on bank holiday. The upcoming events in the week, though, will be crucial to Euro and Sterling. The question in ECB policy makers mind is whether Q1's slowdown was temporary, or is it something deeper. The PMIs and German Ifo data will provide more insight. In added, ECB monetary policy meeting accounts will shed some lights on how worried ECB officials were.

For GBP, the main question is whether BoE is ready to raise interest rate in August, November, or no at all? The BoE announcement earlier this month was not dovish at all. Governor Mark Carney viewed Q1 slowdown as temporary. And he expected upward revision from the dismal 0.1% qoq growth. We'll have that revision, if any, on Friday. In addition, there will be inflation report hearing on Tuesday, CPI on Wednesday, and retail sales on Thursday too. We believe that by the end of this week, we'll see if there is any chance of August hike.

From US, there will be FOMC minutes and durable goods orders. But we're not expecting anything special from there.

Here are some highlights for the week ahead:

- Tuesday: UK inflation report hearings, public sector net borrowing; Canada wholesale sales

- Wednesday: Japan PMI manufacturing, all industry index; Eurozone PMIs; UK CPI , PPI; US PMI, new home sales, FOMC minutes

- Thursday: New Zealand trade balance; Germany Gfk consumer sentiment, GDP final; UK retail sales; ECB meeting accounts; US jobless claims, house price index, existing home sales

- Friday: Japan Tokyo CPI; German Ifo; UK GDP revision, index of services; US durable goods orders

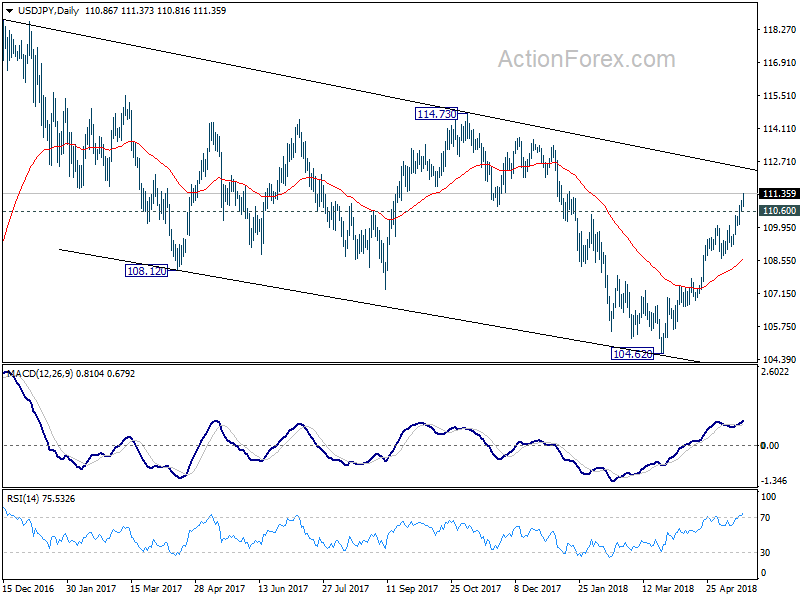

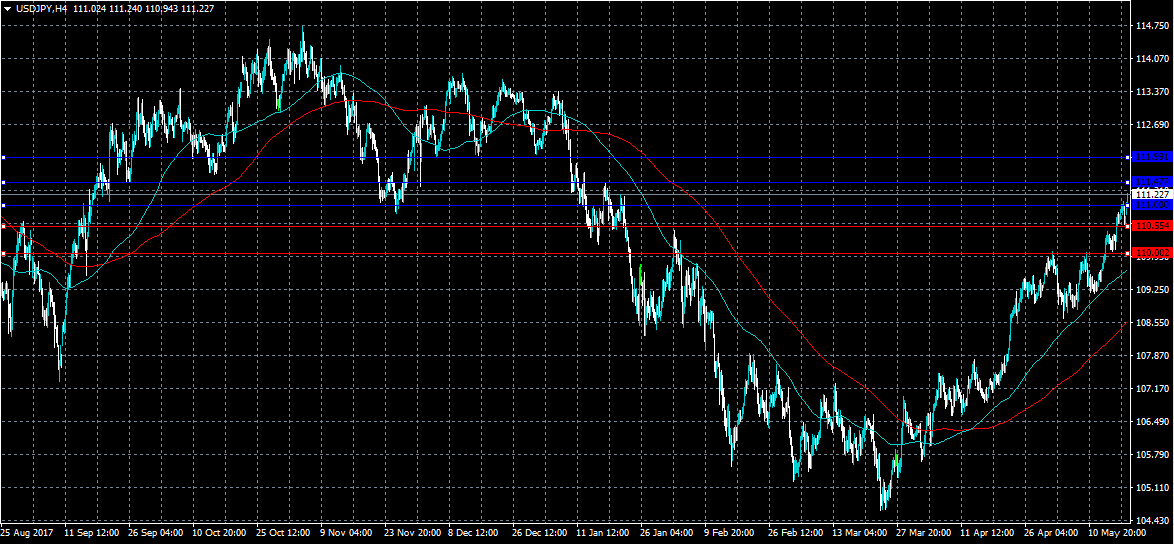

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.55; (P) 110.82; (R1) 111.02; More...

USD/JPY's rally resumed after very brief consolidation and reaches as high as 111.37 so far. Intraday bias is back on the upside for trend line resistance at 112.33. Firm break there will target 114.73 resistance next. On the downside, below 110.60 minor support will turn bias neutral again and bring consolidations. But strong support should be seen from 109.14/110.02 support zone to bring rally resumption.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 55 day EMA (now at 108.65) holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Ex Inflation Q/Q Q1 | 0.10% | 1.00% | 1.70% | 1.40% |

| 23:01 | GBP | Rightmove House Prices M/M May | 0.80% | 0.40% | ||

| 23:50 | JPY | Trade Balance (JPY) Apr | 0.55T | 0.11T | 0.12T | 0.17T |

| 8:00 | EUR | ECB Financial Stability Review | ||||

| 12:30 | USD | Chicago Fed Nat Activity Index Apr | 0.1 |

Italy Policy Turmoil Not Yet Resolved although More Hurdles Cleared for New Government

Italy’s two populist parties – the anti-establishment Five Star Movement and the far-right League- have agreed on a prime minister candidate, clearing another hurdle to forming a new coalition government. Over the weekend, members of both parties approved the joint economic policy, finalized last Friday, which showed softer stance towards the EU. Yet, it was replaced by a more aggressive fiscal expansion program. The final hurdle would approval by Italian President Sergio Mattarella today (May 21)

The latest version of the economy policy excludes the request for a 250B euro debt relief from the ECB while a mechanism under which countries could leave the EU is not proposed. Yet, it indicates that ECB’s purchase of government under the QE program should not count towards the debt-to-GDP ratio. Meanwhile, it calls for a reevaluation of the EU budget and a review of “European economic governance”, which the parties criticizes as based more on the “predominance of the market” than on economic and social needs. The focus of the plan was on fiscal stimulus. According to former fiscal commissioner and IMF alumnus Cottarelli, the measures might result in a deficit slippage of 108-125B euro (6-7% GDP), in addition to the current 30B euro (1.7% GDP).

| Fiscally expansionary measures | Billion Euro | Fiscally contractionary measures | Billion Euro |

| Income tax cuts | 50 | Reduction of MPs | 0.1 |

| Sterilisation of planned VAT hikes | 12.5 | Cut in high pensions | 0.1 |

| Reduction in oil taxation | 6 | Politicians’ lifelong pensions | 0.1 |

| ‘Universal income’ | 17 | Cut in foreign aid | 0.2 |

| Job centres | 2 | ||

| Early retirements | 5 | ||

| Pension reform | 8.1 | ||

| Policies for families | Up to 17 | ||

| Investments | 6 | ||

| Penitentiary police hires | 0.2 | ||

| Police hires | 0.2 | ||

| Civil indemnities | 1.8 | ||

| Total | 108.7-125.7 | 0.5 |

Source: CPI Observatory

The policy plan, if approved by Italian President Sergio Mattarella, would set the basis for governing for the five-year legislative term. However, Italy’s politics is notorious for the short lifespan of a government. Recalling the election back in March, Five Star Movement emerged as the biggest party securing 265 out of 630 seats in the parliament. Together with the League won 125 seats, the two populist parties have only managed to get a thin majority. Worse still, the relations between the League and its former ally Forza Italia, led by Silvio Berlusconi, have soured recently. It was reported that the strong commitment to combat corruption included in the joint economic policy has displeased Berlusconi. What is foreseeable is that political uncertainty in Italy is far from settling down, as the new government is likely to face strong opposition from both the center-left Democratic Party as well as the center right.

Euro and Yield Spread

The impact of Italian political turmoil on the financial markets has been mainly reflected in the euro and widening in bond yields. The single currency reversed the short-lived recovery against the greenback after the media leaked the draft proposal, which included request of the debt relief mentioned above and other harsh reforms of the EU, of the populist duo last week. EURCHF has also commenced another leg of downtrend with safe haven demand of Swiss franc lifted amidst uncertainty. The tone of anti-EU has been watered down in the final proposal. We also do not expect the new government would pursue a strategy to leave the Eurozone. However, the government, as well as the general public would remain Euro-skeptical so as to get an upper hand on future negotiations. Such sentiment, together with soft economic data in the Eurozone in general, would be negative for the euro in the medium to long term.

Meanwhile, Italian bond yield spreads have widened rapidly of late. 10-year yield spread between Italian and German bonds have spiked to over 160 bps as of May 18, from 129 bps on May 15. The jump has triggered caution of the ECB with Vice President Vitor Constancio indicating last Thursday that the members are monitoring the developing, as “it’s a change from what has been happening recently”. While some have raised concerns about re-emergence of a debt crisis, we believe the case remains remote as Italy’s economy remains in the recovery path. The gradual pick up of economic growth, as well as ECB’s ongoing purchases, should lend confidence to the bond market. A recession is probably a sign of rising risk of a debt crisis.

https://s3-eu-west-1.amazonaws.com/associazionerousseau/documenti/contratto_governo.pdf

http://osservatoriocpi.unicatt.it/cpi-tavola_contrattodigoverno.pdf

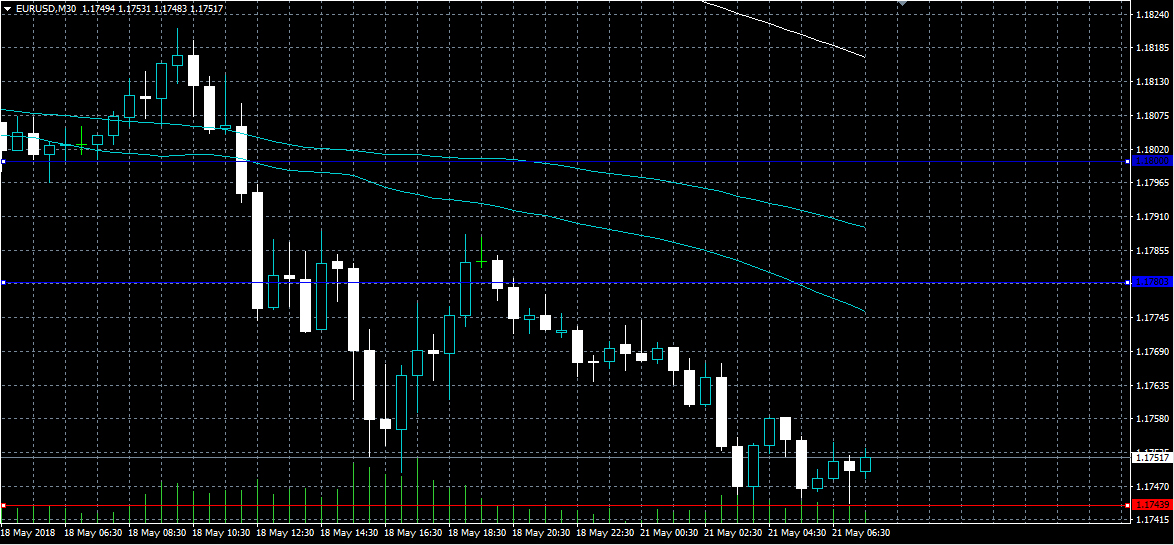

EURUSD Further Bearish Below 1.1750 Level

The euro currency remains under heavy selling pressure against the US dollar after falling to a fresh monthly-low in early Monday trading, hitting 1.1743. The EURUSD pair currently trades around the 1.1750 level, with downside pressures building as traders continue to buy the higher-yielding US dollar. Italian political and economic uncertainty and continued strength in the greenback remain the key drivers of the EURUSD.

The EURUSD should experience further selling below the 1.1750 level, key support is found at the 1.1711 and 1.1650 levels.

If the EURUSD pair holds above the 1.1750 level, buyers may test back towards the 1.1780 and 1.1800 resistance level.

USDJPY Intraday Bullish Above 111.00 Level

The US dollar continues to move higher against the Japanese yen currency, with price moving to a new monthly trading high this morning, hitting 111.23. The USDJPY pair currently trades around the 111.20 level, and remains strongly bullish on an intraday basis while trading above the key 111.00 level. Traders look towards the next move in the US dollar index, and scheduled speeches from FOMC members Bostic, Harker and Kashkari.

The USDJPY pair is intraday bullish while trading above the 111.00 level, resistance is currently found at the 111.47 and 111.99 levels.

If the USDJPY pair moves below the 111.00 level, sellers may test towards the 110.55 and 110.00 support level.

FOMC Speakers Headline Slow Monday Session

Holidays in Europe and Canada make for a relatively quiet trading session on Monday. Traders who are active will be keeping tabs on a series of Federal Reserve speeches scheduled in the North American session.

The European Union will release its Financial Stability Review at 08:00 GMT. The biannual publication provides an overview of the region's financial health, highlighting risks and vulnerabilities facing the Eurozone's banking sector.

Shifting gears to North America, the Federal Reserve Bank of Chicago will release the National Activity Index at 12:30 GMT. The monthly report is designed to gauge overall economic activity in the world's largest economy. The April reading is forecast to come in at 0.14, up slightly from the previous month's 0.10.

Three members of the Federal Open Market Committee (FOMC) are scheduled to deliver speeches during the North American session, beginning with Raphael Bostic at 16:15 GMT. Patrick Harker will deliver remarks at 18:05 GMT followed by Neel Kashkari at 21:30 GMT.

Fed policymakers voted against raising interest rates at their most recent meeting earlier this month. However, officials are widely expected to hike interest rates by a quarter point at their upcoming policy meeting in June. A sizable minority of traders believes the Fed will hike interest rates three more times this year to combat inflation. Most forecasts suggest two more upward adjustments are coming in 2018.

Despite a slow start to the week, the economic calendar features a deluge of market-moving events beginning on Wednesday. Eurozone PMI, British inflation and US durable goods orders are just some of the biggest market-moving events scheduled. The minutes of the May 1-2 FOMC meeting are also due to be released on Wednesday.

EUR/USD

Europe's common currency is coming off another disappointing week, as prices resumed their general downtrend. EUR/USD bottomed at 1.1761 on Friday as the US dollar continued to strengthen against a basket of world peers. The pair fell again at the start of Asian trading on Monday. Immediate support is located at 1.1740. On the flipside, resistance is likely found at 1.1800.

GBP/USD

Cable continued to drift lower last week, as a stronger US dollar provided strong headwinds. GBP/USD traded around 1.3480 in Asia, having declined 0.3% from the previous close. Immediate support levels include 1.3450 and 1.3410. On the opposite side of the spectrum, resistance levels are likely found at 1.3490 and 1.3520.

USD/JPY

The USD/JPY is coming off a strong week of gains, as prices briefly surpassed 111.00 for the first time since mid-January. The pair is likely to enjoy support at the beginning in the interim after China and the United States agreed not to engage in a trade war. USD/JPY traded around 110.82 in Asia on Monday.

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.55; (P) 110.82; (R1) 111.02; More...

USD/JPY's rally resumed after very brief consolidation and reaches as high as 111.37 so far. Intraday bias is back on the upside for trend line resistance at 112.33. Firm break there will target 114.73 resistance next. On the downside, below 110.60 minor support will turn bias neutral again and bring consolidations. But strong support should be seen from 109.14/110.02 support zone to bring rally resumption.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 55 day EMA (now at 108.65) holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above.

The Fed And ECB Minutes As Well As PMI Figures Will Be In Focus

Market movers today

We have a quiet start to the week with no global market movers released. Markets will continue to focus on the political developments in Italy , where the new prime minister candidate might be named as early as today (see our take Italian Election monitor - Stand-off between EU and new Italian government looming ).

Later this week, the Fed and ECB minutes as well as PMI figures will be in focus.

Selected market news

Italy's two populist parties have reached a deal on a prime minister. Today, the anti-immigration League and the Five Star Movement could recommend a cabinet to Italy's President Sergio Mattarella. We expect further EUR weakening in the near term, but stronger in the medium term.

The US administration has decided not to impose tariffs on China's products, putting the trade war on hold for now. In last Saturday s joint statement, China proposed to 1significantly increase purchases of US goods and services.

USD/JPY, AUD and CAD gained on the Sydney open from Friday s New York close on the news. US equity futures opened up.

Euro-Zone’s Trade Surplus Widened Above Expectations In March

For the 24 hours to 23:00 GMT, the EUR declined 0.24% against the USD and closed at 1.1768 on Friday, dragged by prolonged political uncertainty in Italy.

In economic news, the Euro-zone's seasonally adjusted trade surplus widened more-than-expected to €21.2 billion in March, after recording a revised surplus of €20.9 billion in the previous month, while markets were expecting the region's trade surplus to widen to €21.0 billion. Meanwhile, the region's seasonally adjusted current account surplus narrowed to €32.0 billion in March, compared to a revised surplus of €36.8 billion in the prior month.

Separately, in Germany, the producer price index (PPI) index climbed 2.0% on an annual basis in April, higher than market expectations for a gain of 1.8%. In the prior month, the PPI had advanced 1.9%.

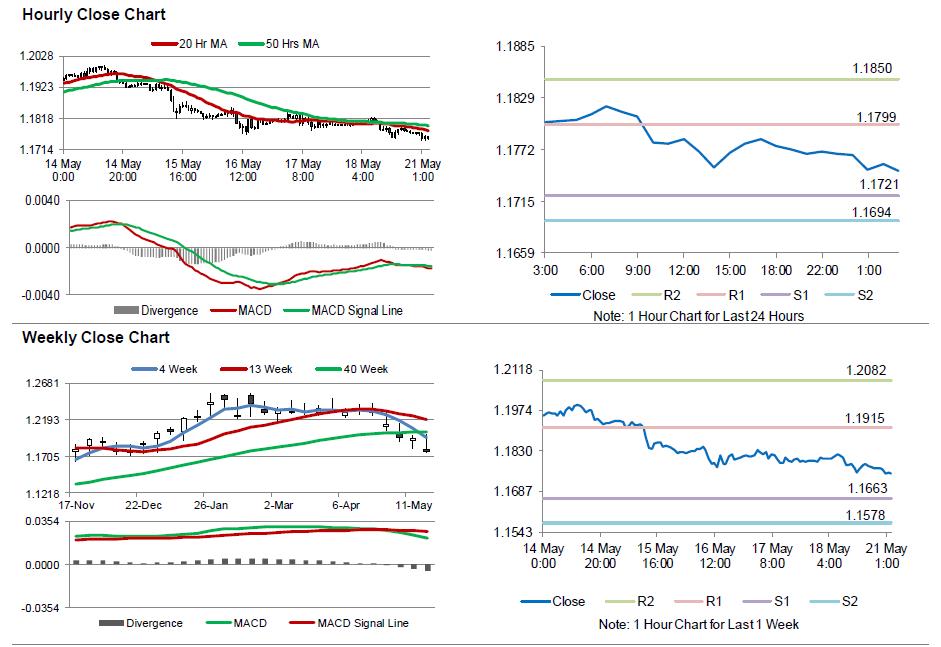

In the Asian session, at GMT0300, the pair is trading at 1.1749, with the EUR trading 0.16% lower against the USD from Friday's close.

The pair is expected to find support at 1.1721, and a fall through could take it to the next support level of 1.1694. The pair is expected to find its first resistance at 1.1799, and a rise through could take it to the next resistance level of 1.1850.

Amid a lack of macroeconomic releases in the Euro-bloc today, investors would focus on the US Chicago Fed national activity index for April, slated to release later in the day.

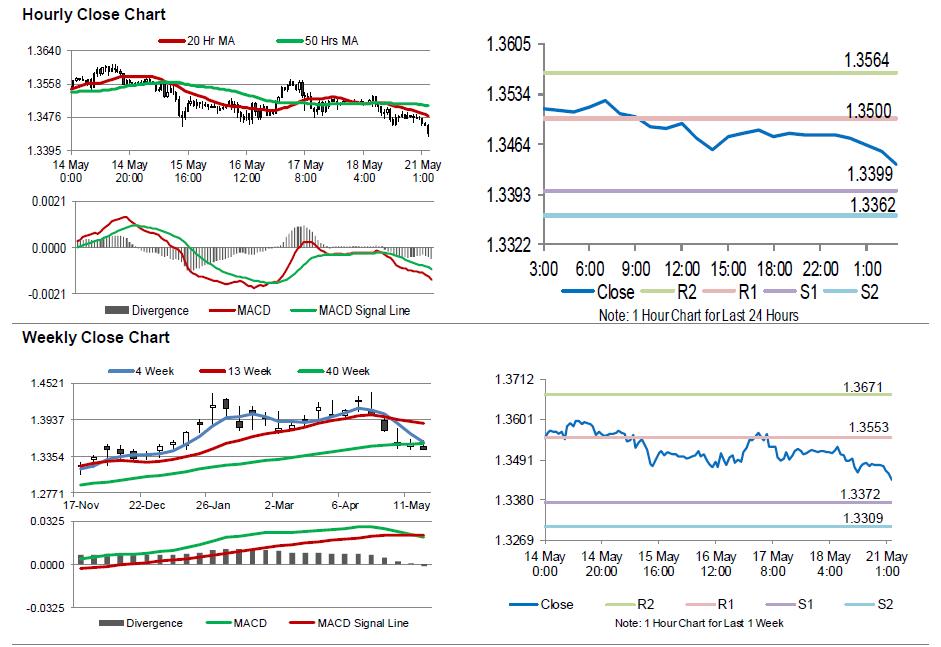

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Pound Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the GBP declined 0.27% against the USD and closed at 1.3478 on Friday.

In the Asian session, at GMT0300, the pair is trading at 1.3435, with the GBP trading 0.32% lower against the USD from Friday’s close.

Overnight data revealed that Britain’s Rightmove house price index rose 0.8% on a monthly basis in May, compared to a gain of 0.4% in the previous month.

The pair is expected to find support at 1.3399, and a fall through could take it to the next support level of 1.3362. The pair is expected to find its first resistance at 1.3500, and a rise through could take it to the next resistance level of 1.3564.

With no further macroeconomic releases in the UK today, investor sentiment would be determined by global macroeconomic events.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.