Sample Category Title

NAB pushed forecast of first RBA hike away to May 2019

The National Australia Bank finally gave up on their forecast of an RBA rate hike within 2018. Their expectation on the next move is now pushed from November to May 2019. The change put them back in line with market pricing, as well as with other major bank forecasters.

RBA chief economist Alan Oster noted that the "change reflects the fact there is no sign yet of stronger wages growth and unemployment has been stuck around 5.5% for the best part of a year." Also, he added that once the tightening cycle starts "further rate increases will be very gradual". And after the first move in May 2019, the next move will be "not until November 2019".

Oster also noted that the economy is still expected to strengthen and lead to falling unemployment. And that should "eventually translate into stronger wages growth and give the RBA confidence that inflation will track back to its 2.5% target". However, there is "considerable uncertainty around the timing at which wages growth will strengthen".

Mnuchin: Trade war with China on hold

Commenting on the US-China joint statement on trade, Treasury Secretary Steven Mnuchin said "we are putting the trade war on hold." And he added, "we have agreed to put the tariffs on hold while we try to execute the framework", referring to the agreement.

Trump's top economic adviser Larry Kudlow said they made "a lot of progress", even surpassed their own expectation after the Beijing meeting. But it's not at the stage of taking the threat of tariffs on USD 150B of products yet. And, it's "too soon to lock that (USD 200B reduction in trade deficit) in" yet. Though he emphasized that "the direction here is the key".

Kudlow also added that Commerce Secretary Wilbur Ross will go to China and "looking into a number of areas where we're going to have greatly significant increases," including energy, liquefied natural gas, agriculture and manufacturing".

Market Morning Briefing: Dollar Yen Has Seen A High Near 111.07

STOCKS

Dow (24715.09, +0.0045%) is stuck near 24700 for the last few sessions. Resistance on the daily candle chart near 25200 is holding well for now. There could be some scope of testing lower levels of 24400 or even lower in the medium to long term while 25200 holds.

Dax (13077.72, -0.28%) continues to remain within the near term uptrend. 13000 is the immediate support which could push the index to higher levels of 13200-13400 in the coming sessions.

Nikkei (23037.90, +0.47%) is also trading along the channel support on the daily candles. An eventual rise towards 23400 or higher looks possible in the medium term.

Shanghai (3214.04, +0.65%) after coming off from resistance near 3200 once again rose up sharply today and is trading above the 3200 levels. If the index manages to sustain the current rise, we may negate a fall towards 3100 or lower in the coming sessions and instead see the index targeting an upside of 3250.

Political tensions over the Karnataka elections are moving the Indian equities just now. With news of Yedurappa resigning on Saturday and the BJP skipping the floor test, the impact on the Nifty could be negative. Nifty (10596.40, -0.81%) did come down slightly on Friday and could continue to move down today also. Immediate downside target is 10500-10000 levels.

COMMODITIES

Brent (79.05) and Nymex WTI (71.89) could see some near term short dip towards 77 and 70.50 respectively before attempting another rise. Some stability could be expected just now near current levels.

Gold (1288.70) is almost stable near current levels. A fall below 1275 is not expected just now and instead the price could rise towards 1300 again in the near term.

Copper (3.0845) has support near 3.05 and while that holds, there could be chances of a bounce towards 3.15 in the medium term. Overall immediate view is bullish.

FOREX

Dollar index (93.79) saw a high near 93.8 on Friday and is continuing to trade near those levels. A dip, if it happens, might be restricted till 93.4-93.5 (support on daily candles). There are good chances of the Dollar Index testing its upside target near 95 in this week or max by next week. We have been saying that the upside is likely to be capped till 95. The 89 weeks MA near 95.65 is a possible extension level which should produce a dip, if tested.

Euro (1.1753) could test 1.155 as the Dollar Index tests levels near 95. The 89 weeks MA for the Euro which could produce a bounce is near 1.145. Any upward correction during the week might be restricted till 1.18 (downward channel on daily candles).

Dollar Yen (111.03) has seen a high near 111.07 and is trading near those levels currently. As mentioned on Friday, the revised upside target would be levels near 112, which corresponds with crucial long term resistance on weekly candles. In this week, it could first rise a little more towards 111.50, then see correction towards 111.00-110.75 and then rise back again towards 112 by next week possibly.

Euro Yen (130.49): After having bounced from support on 3 day candles near 129.5 last week, it looks like it could test resistance on daily candles near 131.5 in this week. However, individual forecasts on Euro and Yen present a slightly different possibility – with Euro headed downward towards 1.155 and Dollar Yen's upside capped till 112, Euro Yen might dip towards support near 129 again very soon.A dip towards 129 is hence preferred in this week.

Pound (1.3453): As mentioned on Friday, Pound could possibly see a phase of ranging between the levels 1.345 and 1.36 (possibly extending upto 1.37). It has been trading near 1.345 in the last couple of sessions (seen as support on daily and 3 day candles). If it breaks this support, our forecast of ranging movement would be proven incorrect and it would turn bearish again.

Dollar Rupee (68.0050): While some steady movement within the 67.50-68.30 region is possible in this week, there is also a possibility of a sharp rise towards 69, sooner than the markets are expecting. It needs to be seen if the Karnataka outcome on Saturday leads to any volatility today.

INTEREST RATES

US yields saw an important rally last week in which the 10 Year yield finally rose past the 3% level decisively. We now expect this rally to possibly continue in the near term towards the following upside targets:

3.2%-3.3% (10 Year), 3.4%-3.5% (30 Year), 3.15% (5 Year) and 2.56% (2 Year)

US 10 Yr Yield (3.06%), 30 Yr (3.20%), 5 Yr (2.90%), 2 Yr (2.57%):

The 10 year yield looks like it could dip slightly more towards 3.04%-3.05% to test support on short term charts and then rise again.

The 5 Year yield is near support and could rise towards 2.94%2.95% again in the next couple of sessions.

The 30 year yield could also see its downside restricted till 3.20%.

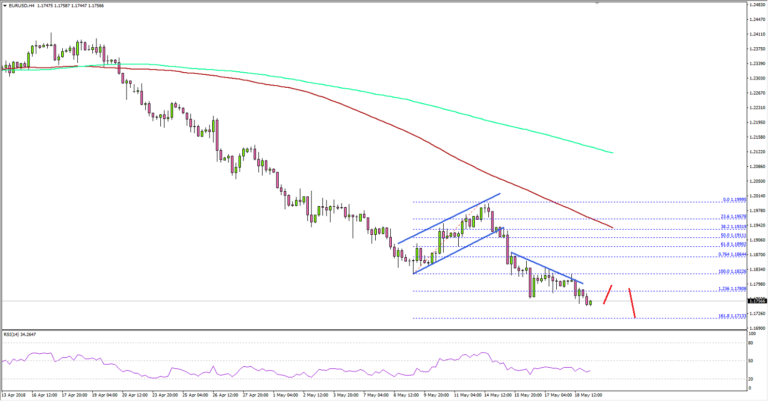

EUR/USD Could Accelerate Declines Below 1.1800

Key Highlights

- The Euro faced an increased selling pressure recently and declined below 1.1800 against the US Dollar.

- There is a short-term connecting bearish trend line forming with resistance at 1.1800 on the 4-hours chart of EUR/USD.

- Euro Area’s Trade Balance in March 2018 posted a trade surplus of €21.2B, more than the forecast of €20.7B.

- Canada’s CPI in April 2018 increased 0.3% (MoM), less than the forecast of 0.4%.

EURUSD Technical Analysis

The Euro came under a lot of bearish pressure this past week and declined below 1.1880 support against the US Dollar. The EUR/USD pair accelerated declines and even closed the week below 1.1800.

Looking at the 4-hours chart, the pair is clearly in a downtrend from the 1.1999 swing high. During the downside, the pair broke an ascending channel with support at 1.1930. It opened the doors for more losses and the pair tumbled below the last swing low of 1.1822.

The pair even broke the 1.236 Fib extension of the last wave from the 1.1822 low to 1.1999 high. It seems like the pair may continue to move down and it could even break the 1.1720 support.

The next stop for sellers could be the 1.618 Fib extension of the last wave from the 1.1822 low to 1.1999 high. On the upside, there is a short-term connecting bearish trend line forming with resistance at 1.1800 on the 4-hours chart of EUR/USD.

As long as the pair is below 1.1800 and 1.1820, it remains at a risk of more losses in the near term.

Other major pairs such as GBP/USD also remained in a bearish zone this past week below 1.3550. On the other hand, USD/JPY jumped higher and traded above the 110.50 level.

The overall bias is positive for the US Dollar, suggesting more declines or limited upsides in the Euro, British Pound and the Japanese Yen.

USDCHF – Remains Vulnerable On Corrective Pullback

USDCHF - The pair looks to weaken further on corrective pullback. On the downside, support lies at the 0.9950 level. A turn below here will open the door for more weakness towards the 0.9900 level and then the 0.9850 level. On the upside, resistance resides at the 1.0050 level where a break will clear the way for more strength to occur towards the 1.0100 level. Further out, resistance comes in at the 1.0150 level. Above here if seen will turn attention to 1.0200. All in all, USDCHF faces further corrective downside pressure.

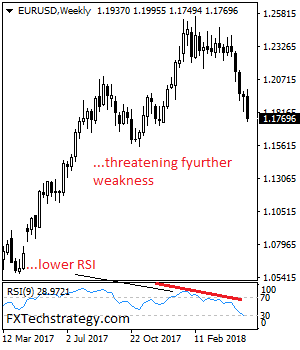

EURUSD – Weakens Further, Eyes The 1.1700 Zone

EURUSD - The pair faces further bear pressure as it continues to hold on to its bear pressure after closing lower on Friday. On the upside, resistance comes in at 1.1800 level with a cut through here opening the door for more upside towards the 1.1850 level. Further up, resistance lies at the 1.1900 level where a break will expose the 1.1950 level. Conversely, support lies at the 1.1700 level where a violation will aim at the 1.1650 level. A break of here will aim at the 1.1600 level. Below here will open the door for more weakness towards the 1.1550. All in all, EURUSD faces further downside pressure.

A Test Of The Breakouts

A test of the breakouts

This week should be all about contesting and consolidating last week’s significant breakouts in 10 year UST, EURUSD, USDJPY and Oil Prices. And despite weekend inspired short-covering in US fixed income, we’ve seen a weekly close in US 10y above 3.05 %. And with the Baker Hughes rig count holding steady, the tumultuous trifecta of USYields, US Dollar and OIl prices, should get set to resume their upward trajectory.

While significant economic data fixtures will be far and few this week, markets will be inundated with central bank speakers, including four central bank governors (Fed Chair Powell, RBA Governor Lowe, Riksbank Governor Ingves, and BoE Governor Carney). Also, traders will navigate the May FOMC minutes, April ECB minutes and Riksbank Financial Stability Report.

The May FOMC minutes will be of particular interest after the markets shaded the May 2 FOMC meeting dovish. But with the market now slightly leaning to the four rate hike camp this year, any hawkish glean would raise that conviction and should propel the dollar to new yearly highs.

The latest statement on the China-US trade suggests both parties are happy to avoid the dreaded tit for tat escalation while working towards a more market-friendly bilateral trade agreement. But the intentional vagueness delivered by both parties statements suggests a great divide, but there’s a hint of a consensus, none the less, to bridge that gap. So given the possible worst-case scenario was avoided the market should view the latest trade discussions as a favourable and equity market should be in that happy place, at least for today

Oil prices

The US and China agreeing to no trade war will be positive for Oil prices given that the possibility of a full-out trade war would have dealt a significant blow to global growth.

The well documented dual supply disruptions from Iran and Venezuela continue to drive current sentiment. But with the pipeline constraints in the Permian Basin in focus and continuing to factor, the supply side dynamics suggest prices will remain firm through 2018. And throw in a positive demand fillip from a de-escalation of trade wars and prices could run higher for longer.

No change in US oil rig counts this week holding steady at 844 and about half of the heyday numbers of the Oct 2014 high, when oil was at $80. Suggesting no Monday morning downside test is in the offing

Gold Prices

Gold prices rebounded off weakly lows as the US dollar eased on the back of profit-taking ahead of the weekend. With geopolitical premiums getting exhausted, gold bulls are in search of the next significant catalyst. But, gold remains under pressure from the US dollar and utterly vulnerable to higher US bond yields which are showing signs of a strong topside breakout after the 10-year Treasury note yield breached 3.1 % last week. The inflationary overtones from oil prices coupled with a strong US retail sales print have increased Fed rate hike expectations. This week FOMC minutes could be a key driver for near-term USD sentiment so we should expect Gold and the USD to remain relatively rangy head of the release

Currencies

The depth of USD appreciation in recent weeks has exceeded virtually everyone expectations. What started as a purge of long EURUSD positioning has manifest into a full USD bull. I think G-10 dealer will go AUD and JPY route to express stronger US dollar bias from a catch-up perspective. EURO could start to take cues from the USDJPY which could assert itself as the dominant driver near-term

JPY: With equities stabilised and 10y yields in the US breaking out of 3.05, USDJPY has arguably underperformed so we could see USDJPY lead the USD bulls to charge over the near term. Correlation with fixed income remains robust and UsdJpy touching 111.00 as US 10 year yields reached 3.125

MYR: Oil prices remain high but so too does political risk, particularly the discussion around GST and SST and how the Credit agencies will view the drop in budget finances

Also, the USD continues to firm against all Asian currencies, and this may be caused by US and China trade negations that will carry on tomorrow.

Outside of oil positivity, the negatives are building as the USD could continue to grind higher near-term

Eco Data 5/21/18

[php_everywhere instance="1"]

USD Index Futures Recorded Net Length, First Time since March

As we expected, USD Index futures turned to NET LENGTH of 18 contracts in the week ended May 15. This was driven by increasing pessimism over other major currencies. According to CFTC's Commitments of Traders report, reduction in speculative long positions greatly surpassed that of short for EUR futures, resulting in a decline of -5 391 contracts in NET LENGTH to 115 114 for the week. NET LENGTH for GBP futures fell -3 367 contracts to 5 621.

It's a tale of currencies in terms of safe haven assets. JPY futures drifted to NET LENGTH of 3 680 contracts last week, thanks to a significant increase in speculative long positions (up +13 114 contracts). On the other hand, CHF futures deepened into NET SHORT of 36 393 contracts, increasing +3 791 from the prior week.

Concerning the commodity currencies, NET SHORT for AUD futures increased +6 340 futures to 23 106 while that for CAD futures dropped -205 contracts to 23 656. While staying in NET LENGTH, that for NZD futures tumbled -10 593 contracts to 1 953 for the week.

Traders Trimmed Long Position on Crude Oil as Price Approaches Peak in Near Term

Speculators generally stayed bullish over the energy complex in the week ended May 15. Although Net LENGTH for crude oil futures slumped -35 484 contracts from a week ago to 644 444, that for heating oil rose +9 610 contracts to 42 070. Also, net LENGTH for gasoline added +11 166 contracts to 95 919. Net SHORT for natural gas decreased -30 595 contracts to 93 428 for the week.

Speculators were also mixed over the precious metal complex last week. Net LENGTH for gold slumped -14 997 contracts to 92 443. Silver drifted to net LENGTH of 658 contracts for the week. For PGMs, net LENGTH for platinum dropped -2 192 contracts to 8 196 while that for palladium added +388 contracts to 10 684.