Sample Category Title

Is There an End in Sight to the Turkish Lira’s Freefall?

The Turkish lira has continued to plummet so far in 2018, sinking to fresh all-time lows as a worrisome cocktail of economic developments diminished demand for Turkish assets. While a potential rate hike by the central bank may help to ease the selling pressure or even trigger a short-term rebound – for the lira’s decade-long downtrend to truly reverse, it may require much more comprehensive reforms outside the scope of monetary policy.

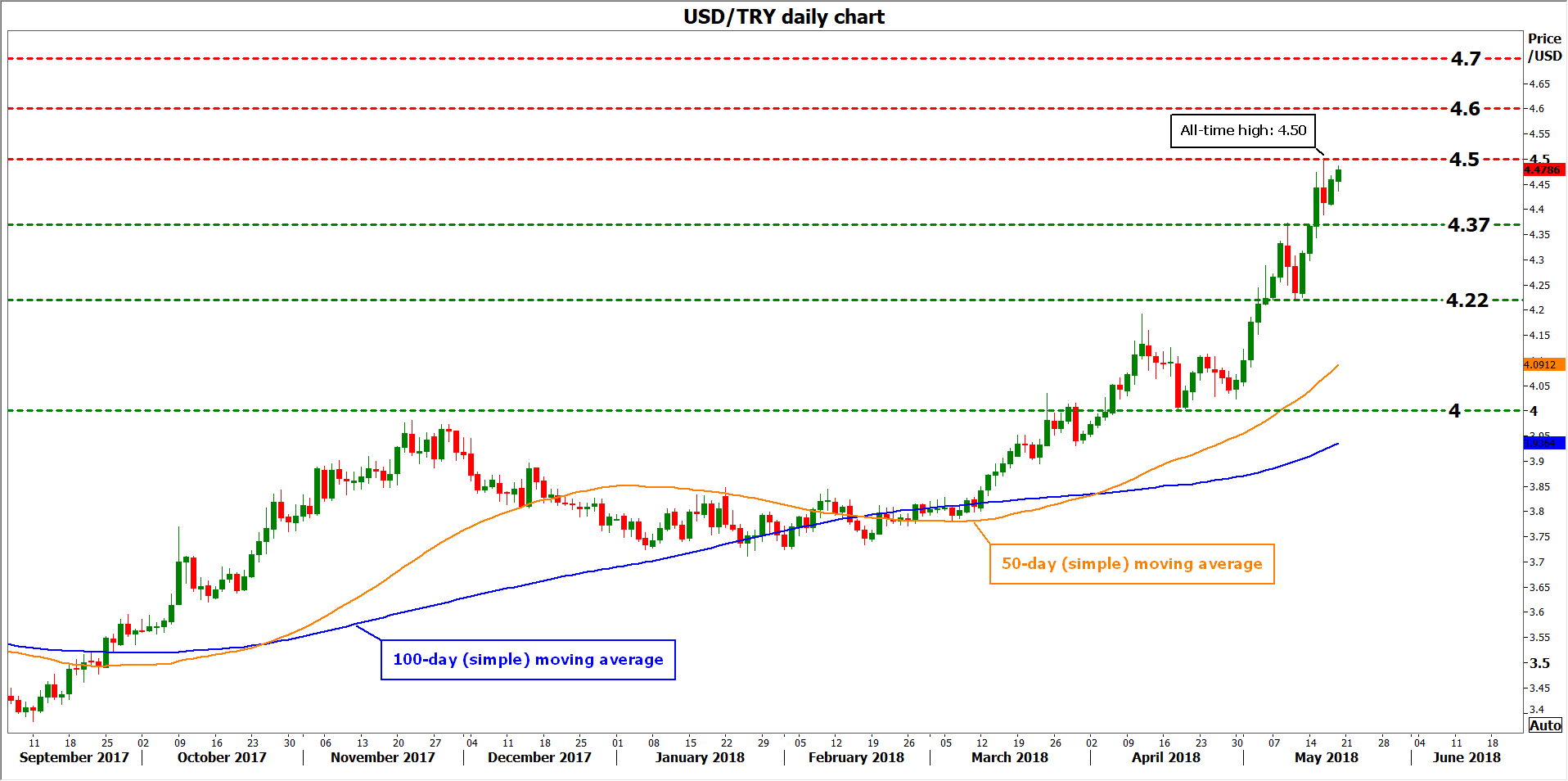

To say that the Turkish lira is in dire straits would be an understatement. The currency is down by 18.5% against the dollar so far this year and 16.2% lower versus the euro, frequently recording fresh all-time lows against both. This is not a new phenomenon, in fact the lira fell 7.4% versus the dollar and 22.3% against the euro last year, while it has been in a broader downtrend for a decade. Lately though, the currency’s plunge seems to have accelerated, something owed to a multitude of troubling economic developments that are causing capital to flee the country.

A worrisome economic cocktail

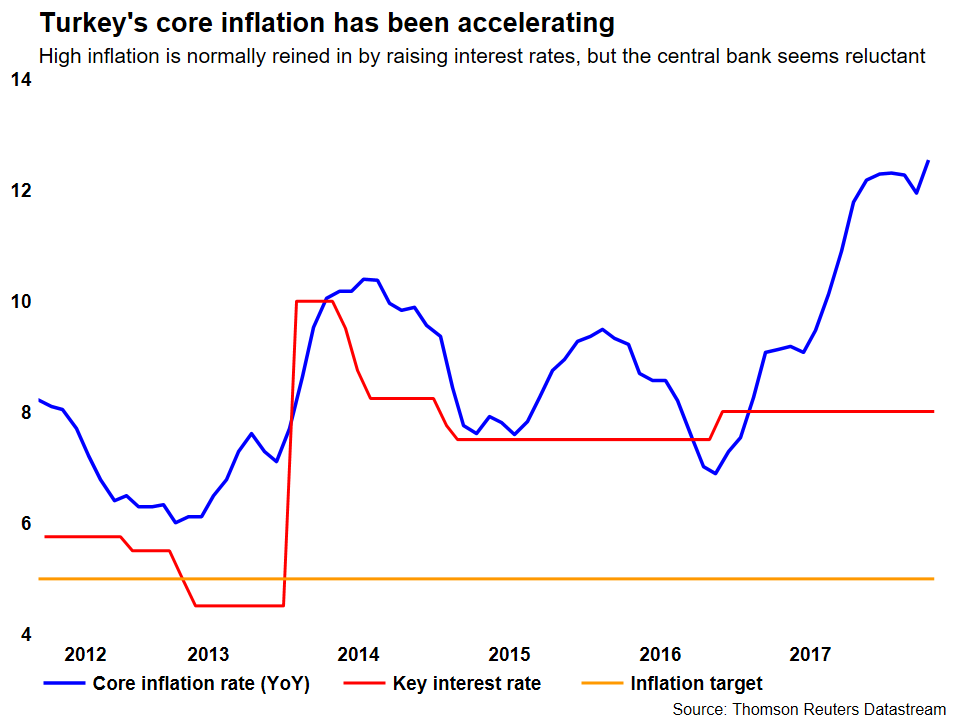

While Turkey boasted an impressive growth rate of 7.4% last year, other macroeconomic indicators have been less than inspiring, increasingly pointing to an overheating economy. Core inflation currently stands well-into the double digits, at 12.4%, more than double the 5% targeted by the nation’s central bank. Meanwhile, the current account (CA) deficit has widened significantly in recent years, rendering Turkey increasingly exposed to shifts in global market sentiment.

When a country runs a large CA deficit, it essentially means it’s a net borrower, importing more than it exports and relying on capital inflows from abroad to finance the difference. If foreign investors for any reason decide to withdraw their investments, that would probably require the country to run surpluses to repay what it borrowed previously, resulting in a sharp drop in consumption, investment, and government expenditure. In BoE Governor Mark Carney’s words, running large CA deficits is like “relying on the kindness of strangers”. To make matters worse, both the government and the private sector have high levels of debt in foreign currencies, which become much harder to pay back with a depreciating lira.

In such an environment, central bank policymakers should be raising interest rates in order to rein in high inflation and prevent the economy from overheating. Rate increases would also make it more attractive for foreign money to stay in Turkey, thereby keeping the current account stable and reducing the selling pressure on the Turkish lira. Alas, the monetary authority appears reluctant to take the necessary steps, which many pundits have attributed to political pressure, raising questions about the Bank’s independence.

President Erdogan has long been a critic of high interest rates, even describing them as “the mother of all evil”. Bearing in mind his economic views, it was no surprise to see the lira slide again this week after he insinuated that he will take greater control of Turkey’s monetary policy after next month’s election. For investors, the message was that rates could remain unchanged, instead of being raised to combat economic imbalances.

So higher rates would solve Turkey’s issues?

Not everything, but they would certainly help with the current situation. Notably higher interest rates would exert downward pressure on inflation, stabilize or even narrow the CA deficit, and provide a helping hand to the battered lira. There are costs of course – economic growth would slow, consumers would be faced with higher borrowing costs, and Turkish banks may see increased numbers of nonperforming loans. All of these, however, are likely smaller than the costs associated with keeping rates low. Runaway inflation, a ballooning current account deficit, and a plunging lira amid a mass “exodus” of foreign money could quickly set the stage for a much greater crisis.

Will the central bank raise rates?

Markets certainly seem to think so. In fact, expectations around this appear to have halted the lira’s slide lately. The currency stabilized earlier this week, once the central bank announced that it is monitoring “unhealthy” moves in the FX market and will take necessary actions. The next policy meeting is scheduled for June 7, though the Bank could call an emergency meeting before then.

In the event it does raise rates, the magnitude and scope of any hike will be crucial for the market reaction. Will policymakers hike rates substantially to fight inflation and defend the currency, or will they deliver a smaller and mostly symbolic increase to keep the government happy as well? Market chatter seems to suggest that anything less than a 100bps hike would be viewed as a disappointment, as it may generate speculation the Bank will only take “half measures”.

Assuming the Bank hikes rates in a material manner soon, then the Turkish lira could rebound. Looking at dollar/lira, immediate support to declines may come at 4.370, the high of May 9. Further down, the May 10 low of 4.220 could come into view, and lower still, the 4.000 psychological level could halt declines.

On the other hand, if the Bank delivers something less than what markets anticipate – or worse still doesn’t hike rates at all – then the currency could resume its freefall. A clear break above the all-time high of 4.500 would bring the pair into uncharted territory, with resistance to advances potentially coming around the round figures of 4.600, 4.700, and 4.800.

But monetary policy is only a short-term fix

While a sizeable increase in rates could stem the lira’s plunge in the short run, monetary policy can’t solve everything – interest rate changes can only do so much. Without deeper structural reforms that improve the prospects of the Turkish economy, the lira’s multi-year downfall may resume before long. The IMF has recently pointed to severance pay, backwards looking wage indexation, pensions, and improving quality of education, as the main areas in need of reform that would help support sustainable growth in the economy. Until Turkey begins taking steps in that direction, one feels hesitant to call for an end to the lira’s broader slide.

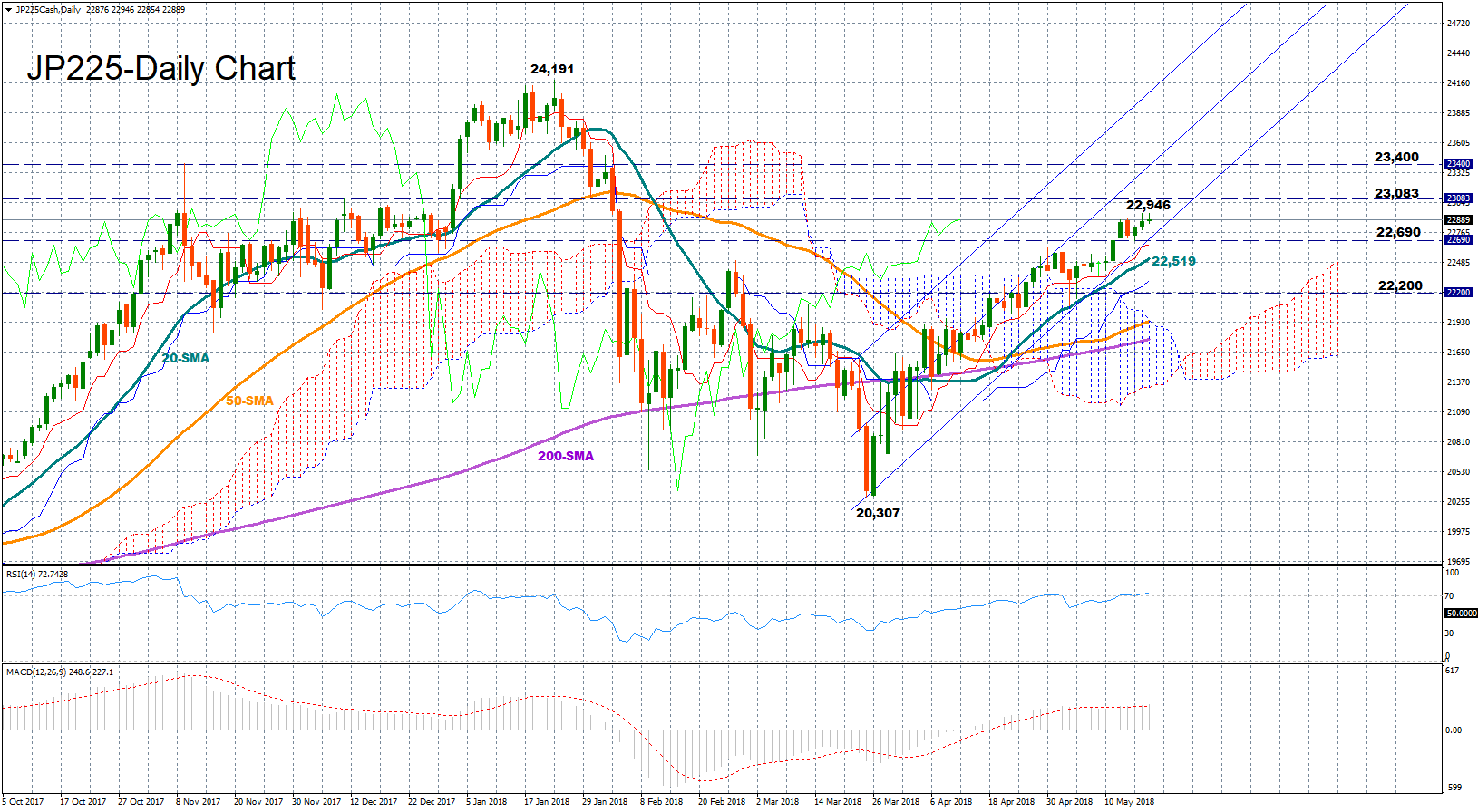

Japan 225 Index Runs Bullish and Overbought at 3 ½-Month Highs

Japan 225 stock index has been fairly bullish over the past two months, printing higher highs and higher lows during the period to peak at levels last seen in early February. The bullish trend is expected to stretch into the short-term as long as the price manages to stay above the Ichimoku cloud and its moving averages which are all positively sloped. Momentum, however, could weaken according to the RSI which is currently flirting with overbought levels. Yet, the MACD supports that there is still some room for improvement as the index continues to strengthen slowly above zero and its red signal line.

Should the market gain further, nearby resistance could be found at the 3 ½-month high of 22,946 reached on Thursday before the focus shifts to December’s high of 23,083. Above from here, the next target could be met around the middle of the ascending channel, near 23,400.

Alternatively, dips in the price could face a barrier at this week’s support level of 22,690, where the lower bound of the channel happens to be. If the market fails to hold inside the channel, then negative pressures could strengthen towards the 20-day simple moving average currently standing at 22,519. Steeper decreases below that level could also test the area around 22,200, found at the 50% Fibonacci of the downleg from 24,191 to 20,307.

Turning to the medium-term picture, the outlook is expected to remain positive as far as the market continues to trade above 22,500.

Sunset Market Commentary

Markets:

Global core bonds traded with a marginal upward bias today after a hectic week. The eco/event calendar was uneventful. The most important news came from the Italian political scene, where 5SM and Lega presented their government programme. They didn’t mention the anti E(M)U measures which circulated in media earlier this week, but fully draw the fiscal stimulus card. Italian BTP’s underperformed on peripheral bond markets. The Italian 10-yr yield spread added 11 bps with again spill-over effect to other peripheral bonds markets (Greece: +10 bps, Portugal +7 bps, Spain +6 bps). German yield drop by 1.6 bps (30-yr) to 2.8 bps (5-yr) at the time of writing. US yields shift 1.2 bps to 2.5 bps lower. In both cases, the belly of the curve outperforms the wings. The US 10-yr and 30-yr yields remain above key resistance levels for now, respectively at 3.07% and 3.22%.

Global markets reacted rather calm to the agreement of the 5SM and the Lega to form a new anti-establishment government in Italy. Italian assets (bonds and equities) underperformed. EUR/USD declined back below the 1.18 level after the announcement. Investors probably turned a bit more cautious on the euro as it is unclear what the exact consequences will be of the policy of the new Italian government. At the same time, underlying USD strength was also still at work. There were no important data in the US. However, sentiment turned slightly more risk off this afternoon. In the current environment, this supports the dollar more than the euro. EUR/USD is setting new 2018 lows. The pair currently trades just north of 1.1750. Interest rate differentials between the euro and the dollar narrowed marginally today, but this didn’t affect the USD positive momentum. USD/JPY remains also well bid even as risk sentiment is turning less buoyant. The pair trades currently just below the 111 handle. So, USD strength remains the name of the game. Uncertainty on Italy was a slight additional negative for the euro.

There was very little to tell on sterling trading today. EUR/GBP held a tight range close to, but mostly slightly below 0.8750. There were no UK eco data and we didn’t see any high profile ‘new’ news on Brexit (customs union debate). The intraday price action tentatively followed the intraday price pattern of EUR/USD. Cable dropped back below 1.35 on USD strength. The 1.3451 correction low is coming close.

News Headlines:

Italy’s anti-establishment Five Star Movement and the far-right League struck a deal to bring a populist government on a platform of fiscal expansion, an aggressive crackdown on immigration and a shift towards Russia in foreign policy (FT).

China denied that it had offered a package to slash the US trade deficit by up to $200 bn, hours after it dropped an anti-dumping probe into US sorghum imports in a conciliatory gesture as top negotiators meet in Washington. (Reuters).

Cleveland Fed Mester said that “monetary policy should be on the table” to defend financial stability if macroprudential tools fail to contain stability risks. (BB)

Belgium’s consumer confidence index declined for a 2nd consecutive month in May, dropping to 11-month low of zero from 2 in April, as the outlook for the labor market and the economy deteriorates further, according to emailed statement from National Bank of Belgium.

Canadian Inflation Treaded Water in April

Highlights:

- All items inflation edged back down to 2.2% year-over-year in April after having increased to 2.3% in March. Market expectations, and our own, were for headline inflation to hold steady at 2.3%.

- CPI ex food and energy also dipped slightly to 1.8% from 1.9%.

- The Bank of Canada’s core measures, however, generally increased in April. The trim and median measures both rose to 2.1%. Including CPI-common, the average of the three was 2.0% after rounding for a third consecutive month.

- After accelerating over the last two months, energy inflation slowed on a year-over-year basis as a sharp increase in gasoline prices in April 2017 was not matched this year. We should see the opposite in May, with pump prices having increased recently compared with a decline a year ago.

- Lower prices for recreational goods and services, and particularly travel services, weighed on inflation in April.

Our Take:

One of the first things Governor Poloz said in his April press conference was that, “inflation is on target and the economy is operating close to potential”. Today’s inflation and retail sales data, the last major releases before the BoC’s May 30 meeting, reinforce that view. The bank’s core inflation measures averaged 2.0% for a third consecutive month. We saw some evidence of underlying inflation accelerating earlier this year—seasonally adjusted prices excluding food and energy were up an annualized 2.7% in Q1—but that wasn’t the case in April with core prices coming in flat month-over-month. Rising gasoline prices should push headline inflation higher in the near term, but the BoC anticipated that (their Q2 forecast is 2.5%) and has indicated some tolerance for above-target inflation given downside misses in recent years. As for the economy operating close to potential, this morning’s increase in retail sales provides further evidence that January’s soft GDP was transitory. We continue to expect GDP growth in Q1 as a whole was right on the BoC’s 1.8% estimate of the economy’s potential. The upshot is the bank has little reason to deviate from their narrative that less stimulus will be required over time. But with reasons to remain cautious, we continue to think the next hike will be in July rather than May.

Canadian Retail Sales up 0.6% in March

Highlights:

- Retail sales rose 0.6% in nominal terms in January — marking a third straight monthly gain.

- Volume sales rose 0.8% to mark a second consecutive monthly increase. The measure was still down 4.0% at an annualized rate in Q1 but a return to positive growth in the last two months increases the odds that an upward trend resumes in Q2.

- E-commerce sales, which represents 2.6% of overall retail sales, were up 11.1% from a year ago.

Our Take:

The nominal sales increase was a touch stronger than expected and sale volumes increased a larger 0.8% in March. Even with that gain, earlier weakness left volume sales down 4.0% at an annualized rate in the first quarter. Some ’payback’ was probably due, though, after sale volumes posted their strongest rise since 2004 last year as a whole. Stronger increases over the last two months bode well for a return to positive growth in the second quarter. To be sure, the latest increase in March was heavily concentrated in motor vehicle and parts sales but sales of clothing, furniture and general merchandise sales also increased solidly . The volume of gasoline station sales and food store sales both fell sharply for a third straight month.

The retail sales data follows already reported increases in manufacturing activity and exports. Labour markets have also continued to improve. We continue to expect GDP increased about 0.2% in March. That would leave growth in Q1 at a still-respectable 1.8% — right in line with the Bank of Canada’s estimate of ‘potential’ growth despite transitory disruptions that weighed on overall economic output in January.

Stand-off Between EU and New Italian Government Looming

This week, Italian election headlines have been dominating financial markets, as there seems to have been a breakthrough in the formation of a new government. Benchmark yield spreads vis-à-vis Germany are now at higher levels than prior to the election. In the context of the famous spaghetti western movie, 'The good, the bad, the ugly', we may be moving towards an ugly scenario for both Italy and Europe (which we laid out in our Election Monitor - The good, the bad and the ugly scenarios for Italy, 25 February). The coalition's draft proposal is in clear breach of EU rules, in our view; hence, we expect a sharp reaction from Brussels. Consequently, heightened uncertainty should be expected in the near future, until a more fiscally modest policy programme is presented from the Italian side.

The draft agreement

A draft agreement leaked on Sunday entailed some very unrealistic initiatives, such as debt forgiveness by the ECB of EUR250bn, the ECB's PSPP holdings not counting in the Maastricht debt-to-GDP ratio as well as a euro opt-out mechanism spooked fears in markets. In addition, a flat tax (entailing a sizeable income tax cut) and rollback of pension reforms was received with the same scepticism by markets.

While the M5S/League coalition pushed back, pointing to this leaked agreement being an old version, the initiatives still took their toll on markets and indicated the kind of government proposals that may come. Early in the week, the prime positive note from the headlines was that the coalition indicated that it would only propose a budget that would be realistic for Brussels to accept.

Nevertheless, the most recent draft from Thursday, still including fiscal easing measures, indicated an order of expansion of around EUR109-126bn, according to Italian Observatoria CPI (see table to the right). The most expensive measure is the introduction of a flat tax estimated at EUR50bn, followed by citizenship income. What is striking with this proposal is that financing only accounts for EUR0.5bn. All in all, this proposal would equate to an expansion of fiscal expenditures by 6-7% of GDP, which on 'back of the envelope' calculations could increase Italian fiscal deficit to 5-6% of GDP (adjusting for fiscal multiplier), and would clearly breach the EU's excessive deficit procedure rules.

Furthermore, the idea of excluding the ECB-held part of Italian sovereign debt from the Maastricht Treaty debt definition would not fly with the Eurostat and EU commission either. More concerning is that some of the proposed initiatives (such as citizenship income) even reinforce the structural problems that the economy is facing.

Looking ahead, as long as the president views a potential government formation with proposals that are not seen as unconstitutional, the negotiations could drag on. Nevertheless, Monday next week is claimed by the coalition to be the focal date when a prime minister candidate will be announced. Regarding the unconstitutional proposals, the current very unbalanced (expenditure financing) proposal could be seen as unconstitutional. In addition, the coalition's intentions to establish a government body that operated to settle disputes within the coalition could also be viewed as unconstitutional.

Only in the case of the president not seeing progress can he either propose a technocratled government or call for new elections.

View from Brussels: the ancient Roman debt tragedy unfolding

While the proposals and the government formation are in clear breach of the excessive deficit procedure rules and therefore not welcomed by Brussels, the market pressure observed over the past few days will probably suit Brussels well, hoping that the market will make the new government think twice. For now, until a concrete official government programme is available, however, we expect Brussels to stay silent.

Furthermore, even in a marked sell-off, we would have to observe dramatically higher rates in order for the ECB to step in at this stage. In return for any support from the ECB's side, there would have to be a more credible policy programme in place, possibly agreed between Italy and the ESM. The last time the ECB was seriously concerned about market pressure was in 2012, when Mario Draghi uttered the famous three words 'whatever it takes'. At that stage, 10Y BTP yields were touching 6.5%. However, the Monti government was also undertaking fiscal austerity and structural reforms in striking contrast with the new Italian government's policy intentions.

That said, since December 2017, the ECB has voiced concerns about government debt levels and made reference to this subject in its introductory statement in March 2018. The subject is now firmly back in the introductory statement after being absent for almost three years as references to 'governing debt' were very frequent in 2014 (the ECB took note of positive developments in 2015). Prior to the Italian elections, we outlined the debt dynamics in different coalition agreements. In the piece, which is the 'ugly' scenario, we took into account the proposals at that time and that debt/GDP levels could rise to 156% in 2028.

On a final note, we emphasise that there is no longer a euro exit plan in the draft proposal, which would be viewed positively by Brussels. However, according to EU, it should never have been discussed. However, the coalition still wants to renegotiate the treaties, something which is being met with scepticism by the EU.

FX: the safe haven flows

The events over the past week have triggered some reaction in FX markets. Notably, we have seen EUR/CHF fall on the news flow outlined above, while EUR/DKK has been untouched by the development. Going forward, we expect FX markets to be in wait-andsee mode. FX markets should remain calm as a euro exit does not form part of the coalition talks. Furthermore, as we noted above, the situation does not warrant a response from the ECB either at this stage, which could be another factor to trigger a response in the FX markets. Hence, for now, the political development will not lead us to change our FX views, but it does bear watching due to the high uncertainty surrounding the result.

FI: BTP market under pressure

The recent political development has taken its toll on the Italian bond market and the 10Y spread to Germany is now more or less back to the level at the beginning of 2018. Earlier this week, we saw an almost 2011 déjà vu as the curve started to flatten intra-day as the market began to price in a real risk of a debt write down. In a write-down scenario, shorterdated bonds would tend to suffer more as an investor would prefer to lose a part of the cash flow (principal) as late as possible. However, in general, the market reaction has been a steepening of the curve as the market has priced in a higher risk premium.

There are few 'high-yielding' alternatives to BTPs for investors in European government bonds. In that respect, investors might return to the BTP market as soon as we see some stabilisation. However, given the fiscal outlook for Italy, the risk of further pressure on the market is evident.

We might also start to see reactions from the rating agencies. The next regular rating update is from Fitch due on 31 August, but look out for comments from the rating agencies when we have a full official government programme.

Canada: Inflation Slows to 2.2% in April, But Higher Oil Prices Will Push it Higher in the Months Ahead

Consumer prices were up 2.2% year-on-year in Canada in April, down from 2.3% in March and below the consensus call for 2.3%. Adjusted for seasonal patterns, prices rose 0.1% month-on-month.

By category, the biggest (seasonally adjusted) month-on-month gainers were clothing & shoes (+1.2%), alcohol and tobacco (+1.0%), and household operations (+0.7%). On the other side of the ledger, recreation and education prices fell 1.5%, health and personal care prices were down 0.5%, and transportation prices edged lower by 0.2%.

Still, most categories were up on a year-on-year basis, led by energy (+6.3%). Only recreation and education prices are lower than year ago levels (down 0.2%)

Two of three of the Bank of Canada's core price measures edged higher in the month, with CPI-Trim and CPI-Median rising to 2.1% (from 2.0%). CPI-common remained unchanged at 1.9%.

Key Implications

Inflation in Canada continues to run close to the Bank of Canada's 2% target, but shows little signs of breaking much higher.

Higher energy prices will pull up the headline measure over the next several months, but core inflation should remain relatively well contained. The Canadian economy is operating close to its potential, but unlike last year, is running right around its trend rate rather than well above it.

With a relatively benign inflation outlook, the Bank of Canada will remain focused on the risks to the Canadian economy, namely headwinds to growth from a slowing housing market and uncertainty around NAFTA, which, as of today, looks to remain a thorn in the side of policy makers for some time to come.

Canada: Autos Drive Retail Sales Higher in April

Retail sales advanced a 0.6% (m/m) in April, a touch higher than March's slightly upwardly revised 0.5% gain. The increase was entirely due to volumes, which rose 0.8% during the month.

Sales at motor vehicle and parts dealers revved higher by 3.0% during the month, making the largest contribution to the overall gain. Excluding this category, the picture was softer, as sales dipped 0.2%. In terms of other categories, notable gains were recorded in clothing and accessories (+2.5%), general merchandise stores (+1.0%) and furniture and home furnishing stores (+3.9%). On the other hand, a large drop was recorded at electronics and appliances stores (-2.4%) while lower volumes led to dropping sales at gasoline stations (-1.9%).

Sales were higher in seven of ten provinces, with gains concentrated in Quebec (1.3%) and Ontario (0.6%). There were also relatively large increases in New Brunswick (+2.5%), Manitoba (+3.2%) and B.C. (+0.6%) . Conversely, sales dropped in Nova Scotia (-2.6%), Saskatchewan (-1.8%) and PEI (-0.5%).

Key Implications

With a healthy gain in volumes, today's report painted a relatively upbeat picture of retail activity in March. For the first quarter overall, volumes were down 1.0%, pointing to slower consumer spending. However, momentum improved as the quarter progressed which is a positive signal for near-term activity and supports our view that growth improved to an above-trend pace in the second quarter.

Healthy labour markets and solid income gains should keep consumers spending at a decent clip this year, despite the negative impacts of weaker housing market activity, rising interest rates and higher gasoline prices.

The increase in volumes in March leaves GDP growth tracking a 1.8% (annualized) first quarter increase, higher than the Bank of Canada's first quarter estimate of 1.3%. While the tone of data has improved in recent months, we continue to expect the Bank of Canada to maintain a gradual approach to rate normalization in the face of continued domestic and external risks to the outlook, with the next hike anticipated in July.

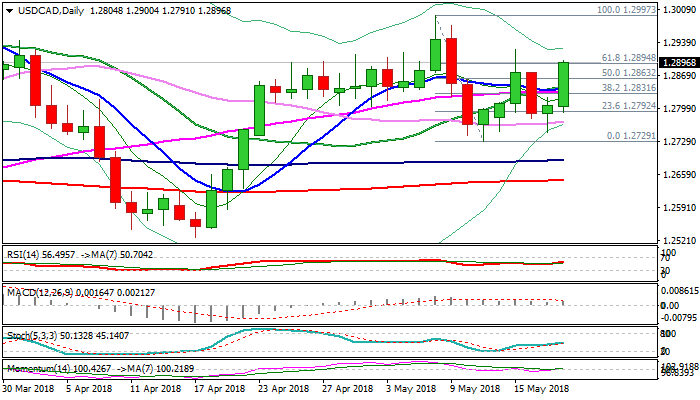

USDCAD Surged on Weak Canada’s Inflation; Bullish Greenback Eyes 1.30 Barrier

The USDCAD surged in early US trading after data showed Canada’s inflation rate dipped in April.

Annualized figure dipped to 2.2% in April, missing forecast for 2.3% which was also last month’s result.

On the other side, Canada’s retail sales climbed in March, as 0.6% rise overshot expectations for 0.3% increase while previous month’s figure was revised upward to 0.5% from 0.4%.

However, better than expected retail sales were not able to improve negative impact from weak inflation numbers, as the greenback remains well supported and accelerated across the board at the beginning of the US session.

Fresh strength surged through thick 4-hr cloud and probes through double-Fibonacci barrier at 1.2896 (Fibo 61.8% of 1.3124/1.2527 fall and Fibo 61.8% of 1.2997/1.2729 bear-leg), close above which would generate bullish signal for renewed attack at psychological 1.30 barrier after initial attempt stalled just ticks ahead on 08 May.

Today’s rally broke above converged 10/20/55SMA’s, bringing daily MA’s into full bullish configuration.

Strengthening 14-d momentum broke into positive territory and adds to bullish outlook.

Cluster of MA’s at 1.2846/33 zone marks solid support which is expected to protect the downside.

Res: 1.2927; 1.2974; 1.3000; 1.3076

Sup: 1.2863; 1.2846; 1.2833; 1.2791

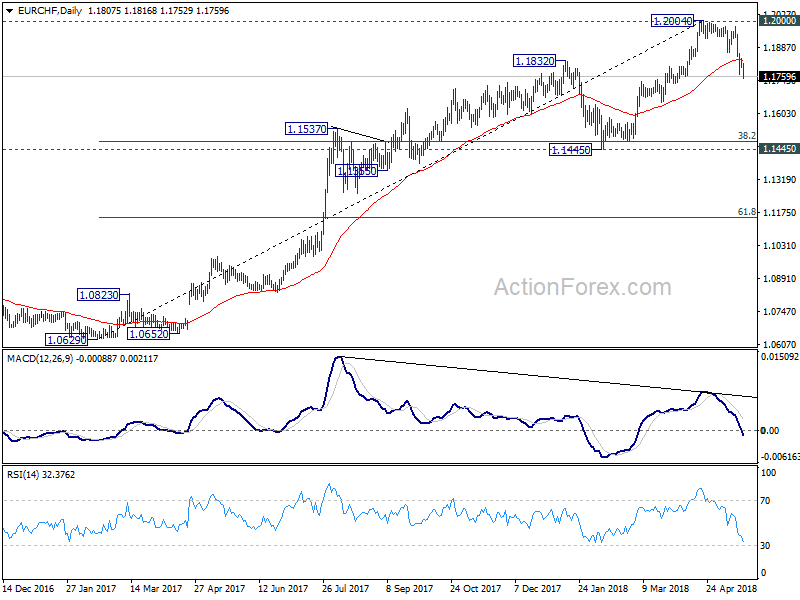

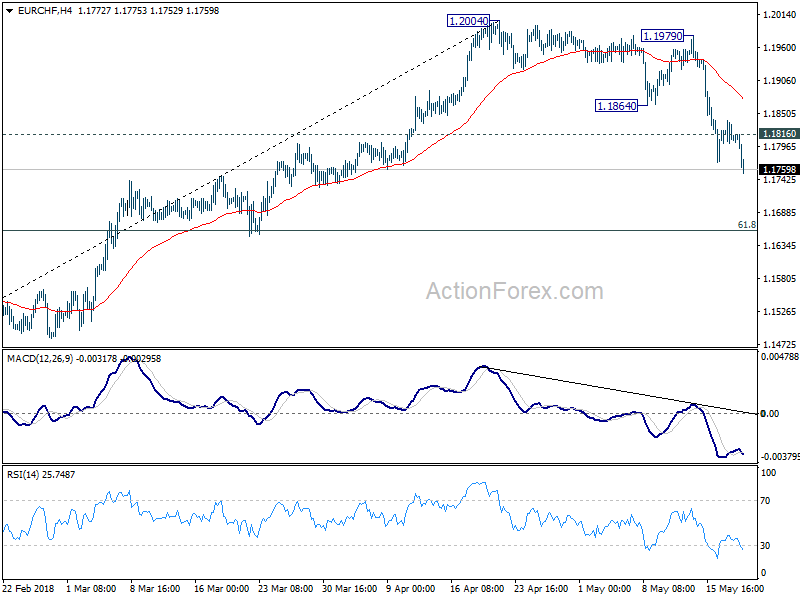

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.1775; (P) 1.1818; (R1) 1.1866; More...

EUR/CHF's decline resumed after brief consolidation. It breaks 1.1770 temporary low and reaches as low as 1.1752 so far. Intraday bias is back on the downside for 61.8% retracement of 1.1445 to 1.2004 at 1.1659 and below. On the upside, above 1.1816 minor resistance will turn intraday bias neutral again. But outlook will stay bearish as long as 1.1864 support turned resistance holds.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily MACD, 1.2004 could be a medium term top. And price action from 1.2004 is corrective the up trend from 1.0629. Hence, for now, deeper fall could be seen back to 1.1445, which is close to 38.2% retracement of 1.0629 to 1.2004 at 1.1479. We'd expect strong support from there to bring rebound to extend the medium term corrective pattern.