Sample Category Title

Markets Cautious on US – China Trade Talks

Investors have entered today’s trading session adopting a cautious stance thanks to conflicting reports over the progress of high-level trade talks between the US and China.

Sentiment was initially boosted following reports of China proposing to purchase $200 billion worth of American goods in a bid to reduce its trade surplus with the United States. However, appetite for risk weakened on Friday after China’s Foreign Minister spokesman, Lu Kang, denied that such a proposal was made. With Donald Trump adding his touch of uncertainty by stating that China and other countries have become “very spoiled” when it comes to trade, markets may remain cautious over the current trade talks in Washington. Investors are likely to maintain a safe distance from riskier assets and flock to safety until more clarity is offered on the progress of the negotiations.

Dollar remains king

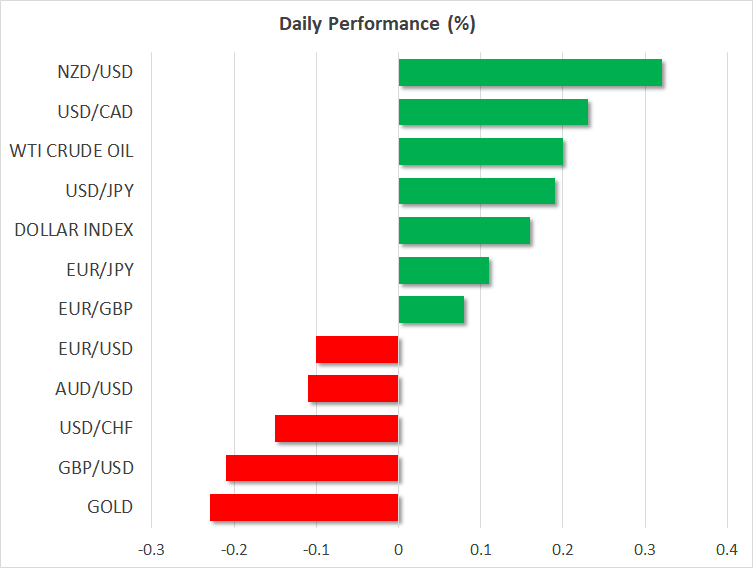

It has been an undeniably bullish trading week for the Dollar which has appreciated to its strongest levels in five months.

The story defining the Greenback’s incredible appreciation continues to revolve around rising US Treasury yields and positive domestic economic data. With bulls heavily supported by heightened expectations of higher US interest rates, the Dollar remains king. Taking a look at the technical picture, the Dollar Index remains heavily bullish on the daily charts. A decisive breakout above 93.50 could invite an incline towards 94.00 and 94.20, respectively.

Currency spotlight – GBPUSD

Sterling was mostly depressed this week following the disappointing UK jobs report, that clouded prospects of higher UK interest rates this year. An appreciating Dollar has compounded the Pound’s woes, with the GBPUSD trading marginally below 1.3500 as of writing. From a technical standpoint, the GBPUSD remains under pressure on the daily charts. A breakdown below 1.3470 could open a path towards 1.3360.

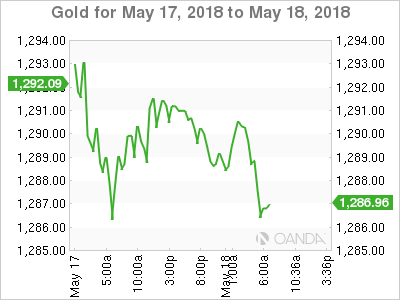

Commodity spotlight – Gold

The fact that Gold is poised to conclude the trading week below the $1300 psychological support level confirms that bears have officially won the four-and-a-half-month-long tug of war.

With the Dollar heavily supported by positive economic data and rate hike expectations, zero- yielding Gold is likely to remain vulnerable to heavy losses. While geopolitical tensions and uncertainty could offer some support, price action shows that bears remain firmly in control. Taking a look at the technical picture, previous support at $1300 could transform into a dynamic resistance that encourages a decline towards $1280.

Are WTI bulls back in town?

Crude oil prices were firmly bullish this week despite the Dollar’s aggressive appreciation.

While optimism over rising global demand may have supported oil, price action suggests that the rally remains driven by geopolitical risk factors. The looming Iran sanctions are likely to fuel speculation of tighter global supply, while heightened geopolitical tensions in the Middle East may spark fears of potential supply disruptions. Although oil could edge higher in the near term, robust US Shale production has the potential to create some headwinds for bulls down the road.

Taking a look at the technical picture, WTI Crude has scope to challenge $75 if bulls can secure a daily close above $72.

EU demonstrates commitment to Iran nuclear deal with measures on four fronts

European Commission formally announced the measures to protect interests of EU companies investing in Iran as part of the EU's continued commitment to the Joint Comprehensive Plan of Action (JCPoA), the Iran nuclear deal. The EU acted on four fronts. The proposals got unanimous backing of EU Heads of State of Government at the Sofia meeting.

Firstly, it launched the formal process to activiate the "Blocking Statute", by updating the list of US sanctions on Iran falling within its scope. It "forbids EU companies from complying with the extraterritorial effects of US sanctions, allows companies to recover damages arising from such sanctions from the person causing them, and nullifies the effect in the EU of any foreign court judgements based on them.". It's targeted to be in force before August 6, 2018.

Secondly, it launched the formal process to remove obstacles for the European Investment Bank (EIB) to decide under the EU budget guarantee to finance activities outside the European Union, in Iran.

Thirdly, as confidence building measures, the Commission will continue and strengthen the ongoing sectoral cooperation with, and assistance to, Iran.

Fourthly, EC is encouraging Member States to explore the possibility of one-off bank transfers to the Central Bank of Iran.

Full release here and details of the "Blocking Statute" here.

DAX Shrugs Off Weak German Inflation Numbers

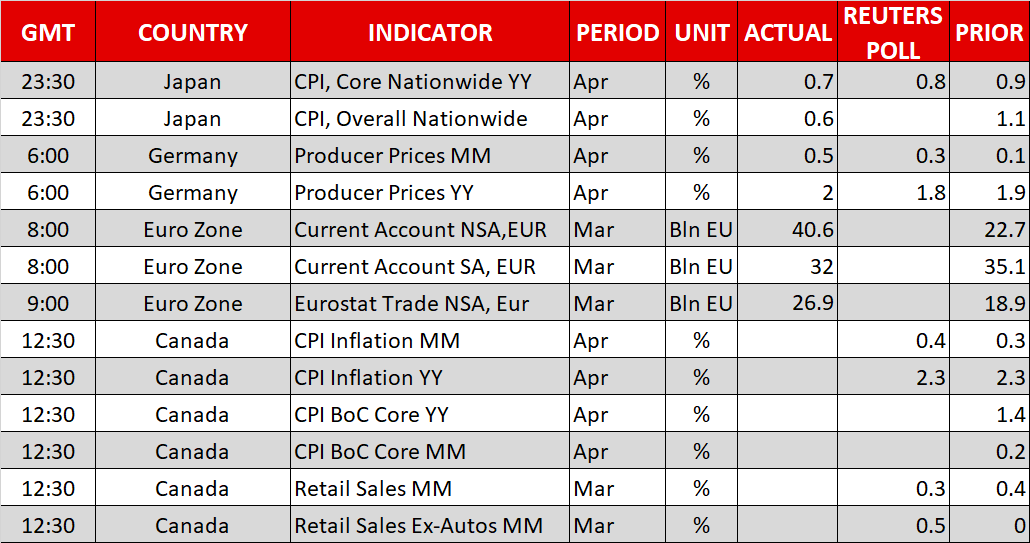

The DAX is showing little movement in the Friday session. Currently, the DAX is at 13,119, up 0.03% on the day. On the release front, German inflation indicators were unexpectedly stronger. PPI and WPI both improved to 0.5%, beating their estimates. In the eurozone, the numbers were mixed. The current account surplus narrowed to 32.0 billion, short of the estimate of EUR 35.1 billion. The trade balance surplus edged up to EUR 21.1 billion, above the forecast of EUR 20.7 billion.

German inflation indicators showed strong improvement in April. PPI improved from 0.1% in March to 0.5% in April, and WPI followed the same trend, climbing from 0.0% to 0.5%. These figures come on the heels of German CPI, which fell from 0.4% to 0.0%. The eurozone economy continues t0 perform well in 2018, but inflation has lagged behind and remains well below the ECB inflation target of around 2 percent. Weak inflation levels could have a significant impact on ECB fiscal policy, as policymakers may have to consider extending its stimulus scheme, which is scheduled to run until September. At the same time, higher oil prices could boost weak inflation levels. Brent crude hit $80 earlier this week, and the upward trend could continue as renewed U.S sanctions against Iran could hamper its oil exports.

The DAX hasn’t been making headlines, but the index continues to gain ground. The DAX is currently trading at its highest levels since the end of January. Investors continue to give a thumbs-up to the robust German economy, but there are some clouds on the horizon. A growing concern is the rising price of crude, which has crossed above the $80 level. Rising oil prices could trigger higher inflation and hamper economic growth, which could send the markets lower.

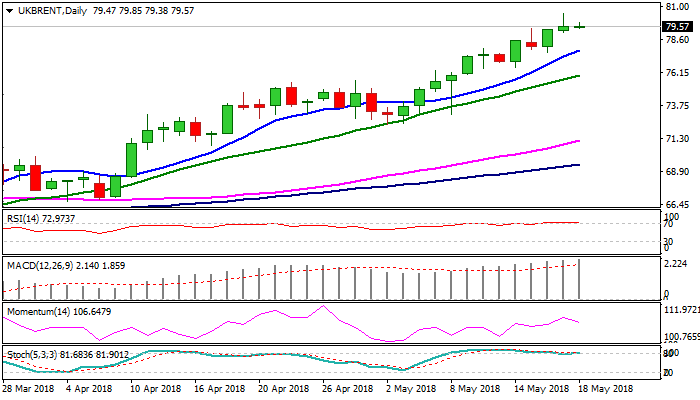

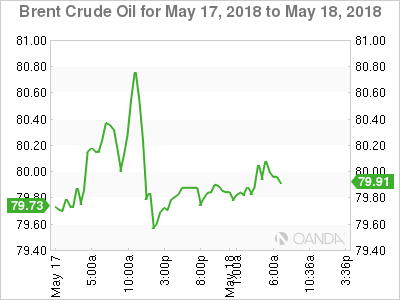

BRENT OIL Cracked Psychological $80 Barrier, Eyes Next Target At $81.84

Brent oil holds firm tone on Friday and trading just under psychological barrier at $80 which was cracked on Thursday’s spike to $80.48 (the highest since Nov 2014).

Oil prices remain supported by growing concerns about sanctions against Iran and heated geopolitical situation in the Middle East, as rising production of US oil had little impact on bulls.

Brent is on track for the third straight bullish weekly close, which adds to strong bullish outlook.

Weekly close above psychological $80 barrier would be strong bullish signal for extension towards next strong barrier at $81.84 (Fibo 61.8% of $115.68/$27.09, 2014/2016 fall).

Meanwhile, consolidative / corrective phase may precede fresh rally as daily studies are overbought slow stochastic bearish divergence warns.

Rising 10SMA ($77.82) is expected to hold and keep bulls intact.

Res: 79.85, 80.48, 81.00, 81.84

Sup: 79.10, 78.51, 77.82, 76.78

Canadian Inflation Awaited, Trade Talks Loom In Background

Here are the latest developments in global markets:

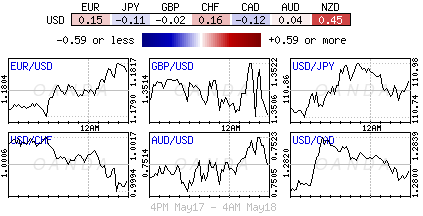

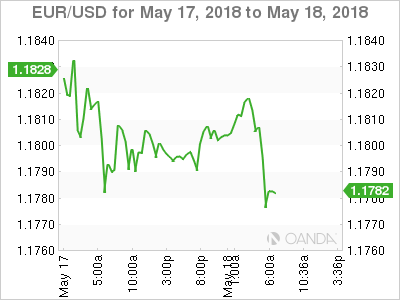

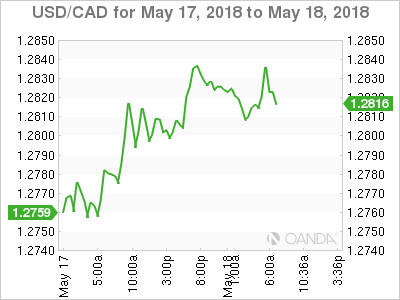

FOREX: The US dollar index edged higher on Friday (-0.05%), approaching once again the 5-month high of 93.63. The greenback remains one of the best-performing currencies this week, drawing support from the surge in 10-year US Treasury yields. Dollar/yen jumped to a new 4-month high near the 111.00 handle, adding 0.17% to its performance today. Euro/dollar inched down to 1.1777 (-0.11%) and approaches the 2018 low of 1.1762. The pair is set to post the fifth consecutive red week as political uncertainty in Italy kept investors cautious. Pound/dollar declined by 0.21% on Friday, after the government denied earlier reports on Thursday that it may consider staying in the customs union beyond 2021. In the antipodean sphere, aussie/dollar ticked lower by 0.08% to 0.7504, while kiwi/dollar advanced by 0.34% and hovered near the 0.6900 handle. Dollar/loonie was moving higher by 0.18% to 1.2826 ahead of Canadian inflation and retail sales data due for release later in the day.

STOCKS: European stocks were mixed on Friday at 1015 GMT. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.04% and 0.06% respectively. In Germany, the DAX rose by 0.03%, and it hit a fresh 15-month high of 13,133 earlier in the day. The French CAC 40 fell 0.26%, while in Italy, the FTSE MIB 100 was down by 0.15% as Italy's two anti-establishment parties have signed an accord to form a ruling coalition. The British FTSE 100 was down on the day (+0.02%) and the Spanish IBEX 35 fell by 0.07%. Turning to the US, futures tracking the Dow Jones, S&P 500, and Nasdaq 100 were all in positive territory, pointing to a higher open today.

COMMODITIES: Oil prices edged up during the European trading session Friday, trading a few cents below the multi-year highs reached on Thursday' session. WTI crude was up by 0.25% to $71.67 per barrel, while Brent advanced by 0.54% to $79.73 and is set to complete the sixth consecutive week of gains. In precious metals, gold prices edged lower by 0.24%, marking a fresh low for the year of $1,285.41.

Day ahead: Canadian inflation prints eyed; Potential trade comments also on the menu

On the data front, Canada's inflation and retail sales data will probably attract the most attention. Besides those, any developments in the ongoing US-China trade talks in Washington could also attract attention.

At 1230 GMT, Canada will see the release of its inflation data for April. The headline CPI rate is expected to have held steady at 2.3% in yearly terms, while no forecast is available for the core rate, which excludes the effects of volatile items such as food and energy. As for retail sales, expectations are mixed. On a monthly basis, the headline print is expected to have to have risen by 0.3% in March, down from 0.4% in February. Meanwhile, the core rate is anticipated to clock in at 0.5% month-on-month, after posting no growth previously.

Recall that at its latest policy meeting, the Bank of Canada (BoC) maintained a relatively cautious stance, dismissing the recent surge in inflation as reflecting mostly transitory factors that will fade over time. Hence, these data will likely be instrumental in shaping expectations regarding the timing of the Bank's next rate increase; markets currently see a 40% probability for a hike at the May 30 meeting. A strong set of prints that pushes that probability higher could work in favor of the loonie, and vice versa.

On the trade front, negotiations between US and China continue in Washington. Talks appeared to be gaining momentum after media reports suggested China had presented the US with proposals to reduce the trade deficit between the two by $200 billion. However, China's foreign ministry subsequently denied it made such an offer. Given this confusion, investors will likely look to comments from the officials themselves upon completion of the talks today, to gauge whether there has been progress. Any signs the talks are moving forward could support riskier assets, such as stocks. The opposite holds true as well.

In energy markets, attention will turn to the Baker Hughes oil rig count at 1700 GMT, for a fresh indication of whether US production continues to soar.

As for the speakers, Fed Board Governor Lael Brainard (permanent FOMC voter) will deliver remarks at 1315 GMT, while Dallas Fed President Robert Kaplan (non-voter for 2018) will also step up to the rostrum at the same time.

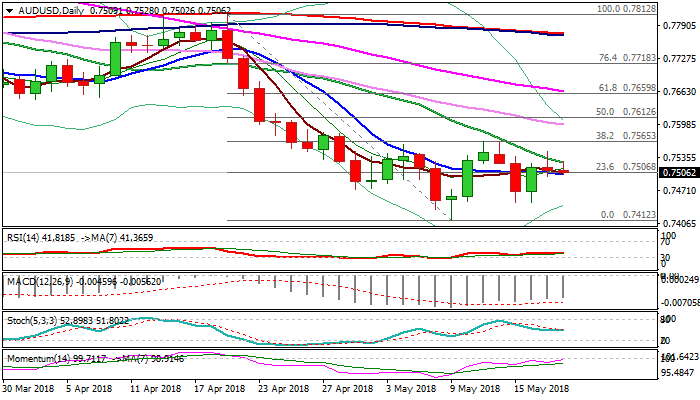

AUDUSD – Negative Outlook While Falling 20SMA Caps

The Aussie dollar stands at the back foot on Friday, with upside being repeatedly capped by falling 20SMA (0.7528) and fresh weakness probing through hourly cloud (0.7519/0.7497).

Initial bearish signal is generating on formation of 1/10SMA bear-cross as near-term recovery from 0.7447 higher base stalled at 0.7497 and closed below 20SMA.

Stronger dollar also keeps the pair under pressure, along with overall bearish daily techs, but the notion is partially offset by strengthening momentum.

Close below 10SMA (0.7500) is needed to maintain fresh pressure and open way for further easing.

Conversely, break and close above 20SMA would generate positive signal for retest of key barrier at 0.7565 (Fibo 38.2% of 0.7812/0.7412 / double upside rejection).

Res: 0.7528, 0.7547, 0.7565, 0.7598

Sup: 0.7497, 0.7472, 0.7447, 0.7433

Italian Populist Seal Agreement To Challenge The EU Establishment

Notes/Observations

- China Foreign Ministry plays down reports of a conciliatory tone on trade

- Italian Populist seal agreement to challenge the EU establishment

Asia:

- China trade delegation offers package to reduce US trade deficit by $200B annually. China said to offer increased imports of US products. The package had been speculated to include the removal of certain tariffs that China has already imposed on ~$4.0B worth of US farm products (including pork and sorghum)

- China Commerce Ministry (MOFCOM): to end dumping probe related to US Sorghum; cites 'public interest'. Investigation showed anti-dumping and anti-subsidy measures on US sorghum would affect the living costs of consumers, which was not in line with public interest.

- Japan Apr National CPI data below expectations with lowest core reading being the lowest since Sept 2017 (CPI YoY: 0.6% v 0.7%e; CPI Ex Fresh Food (Core) YoY: 0.7% v 0.8%e

- Noth Korea state media stated that the country would make more efforts to defuse military tensions

- North Korea leader Kim Jong Un said to have asked US Sec of State Pompeo to reduce strategic weapons or reduce the number of US troops in South Korea if peace continued

Europe:

- ECB's Nowotny (Austria): some governing council members (including himself) agree that ECB should not wait too long to normalize monetary policy

- EU Leaders reportedly brushed off PM May's idea for customs plan guarantees. EU believed that was too early to give any assurances due to the disorientating messages the EU was getting from London . PM May said to have used the EU Leader Summit to seek assurances that the bloc will accept UK proposals to prevent a hard Irish border

- Canadian rating agency DBRS: recent political developments in Italy have been disappointing. 5-star, League economic proposals unlikely to be self-financing and could threaten reduction in debt supporting current credit rating

Americas:

- US Trade Rep Lightizer: NAFTA countries are no where near close to a deal; will continue to engage in negotiations

- Mexico Central Bank (Banxico) left its Overnight Rate unchanged at 7.50% (as expected)

Energy:

- Saudi and UAE Oil Min joint statement saw ample supply of oil; had concerns about recent oil market volatility. Planned a meeting with Russia Energy Min Novak next week

Economic Data:

- (DE) Germany Apr PPI M/M: 0.5% v 0.3%e; Y/Y: 2.0% v 1.8%e

- (DE) Germany Apr Wholesale Price Index M/M: 0.5% v 0.0% prior; Y/Y: 1.4% v 1.2% prior

- (CZ) Czech Mar Export Price Index Y/Y: -4.3% v -4.7% prior; Import Price Index Y/Y: -5.9% v -6.5% prior

- (CZ) Czech Apr PPI Industrial M/M: 0.2% v 0.3%e; Y/Y: 0.0% v 0.0%e

- (CN) Weekly Shanghai copper inventories (SHFE): 268.5K v 279.5K tons prior

- (SE) Sweden Apr Budget Balance (SEK): 2.8B v 6.4B prior

- (EU) Euro Zone Mar Current Account (Seasonally Adj): €32.0B v €36.8B prior; Current Account NSA (unadj): €40.6B v €24.2B prior

- (PL) Poland Apr Employment M/M: 0.1% v 0.1%e; Y/Y: 3.7% v 3.7%e

- (PL) Poland Apr Average Gross Wages M/M: -0.9% v -1.6%e; Y/Y: 7.8% v 7.2%e

- (IT) Italy Mar Current Account: €3.4B v €0.9B prior

- (EU) Euro Zone Mar Trade Balance (Seasonally Adj): €21.2B v €21.0Be; Trade Balance NSA (unadj): €26.9B v €18.9B prior

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.3% at 394.5, FTSE -0.2% at 7770.4, DAX -0.1% at 13094, CAC-40 -0.3% at 5605, IBEX-35 -0.5% at 10163, FTSE MIB -1.1% at 23548, SMI -0.3% at 8960, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes:

- European Indices trade lower across the board following recent gains and slight weakness in US markets overnight.

- Richemont trades sharply lower following a miss in earnings, with Swatch also falling in sympathy. French name Vivendi trades lower after earnings and an update on universal music; Ubisoft trades higher after beating estimates, Vallourec and Natixis also in focus following results. In the healthcare space

- Astrazeneca trades over 2% lower after missing on the top and bottom line, but did affirm their outlook.

- In the M&A space Lloyds sold its Irish residential mortgage portfolio to Barclays for £4B.

- Looking ahead notable earners include Deere & Co and Campbell Soup.

Movers

- Consumer Discretionary Richemont [CFR.CH] -7% (Earnings), Swtach [UHR.CH] -1.7% (In sympathy with Richemont), Vivendi [VIV.FR] -0.9% (Earnings), Ubisoft [UBI.FR] +5.4% (Earnings)

- Industrials Vallourec [VK.FR] -3.5% (Earnings)

- Financials Natixis [KN.FR] +3.1% (Earnings)

- Healthcare Astrazeneca [AZN.UK] -2.7% (Earnings)

Speakers

- ECB's Lane (Ireland): Hard Brexit not very likely but still have to prepare for it

- Portugal Central Bank Gov Costa: Banks need to continue reducing non-performing loans (NPLs)

- Italy 5-Star Movement leader Di Maio confirmed agreement on govt contract with league

- The Italy govt Program contents said to include: review of EU fiscal and bail-in rules. Program said not to include the call for QE debt to be excluded from debt calculations but some investments must be excluded from deficit; dropped reference to Euro exit procedure. No mention of request for ECB to write off €250B in debt. The program sought limited deficit spending and a guaranteed minimum income for poorer Italians. Called for State shareholder to redefine Monte Dei Paschi Di Siena's mission and sought an end to sanctions on Russia

- Finland President Ninisto confirmed Olli Rehn as central bank gov (ECB representative)

- EU Commission said to have launched measures to protect EU companies in Iran **Reminder: On May 17th EU Leaders decided to preserve the Iran nuclear accord despite US withdrawal

- Turkey President Chief Adviser Ertem: Central bank has infinite instrumental independence and right to use all instruments at its disposal

- Fed's Mester (FOMC voter, hawk): Economy near Fed goals. Should not unwind post-crisis rules that helped to strengthen the banking sector until resiliency could be tested. Rate hikes a possible defense against financial stability risks

- China Foreign Ministry: Trade consultations were constructive, refuted reports that China offered to reduce its trade surplus with the US by $200B. Hoped to resolve trade concerns with the US

Currencies

- The USD was slightly softer in quiet European trading but still poised for its 5th week of gains

- EUR/USD holding above the 1.18 level but the Italian political uncertainty was providing additional impetus for a lower EUR. Italian Populist sealed its agreement to challenge the EU establishment.

Dealers noted that the recent widening in the BTP-bund spread had caught the ECB's attention and could pressure the ECB to keep providing accommodative policy support for now to support the weaker economies within the EMU. - The 10-year Italy/German Gov't bond spread was wider by over 5bps to approach 160bps (4-month high). The 10-year BTP yield higher by approx. 30bps during the week to its highest level since Oct abve 2.15% (worst week since Nov 2015)

- The GBP/USD was agai probing below the 1.35 level after reports circulated that EU Leaders brushed off PM May's idea for customs plan guarantees.

- The Steepening US yield curve continued to benefit the pair as it tested the 111 handle during Asia.

Fixed Income

- Bund Futures trade 10 ticks higher at 157.92 rebounding modestly from the mid-week lows. Upside targets 159.75, while a return lower targets the 157.25 level.

- Gilt futures trade at 121.14 higher by 14 ticks but still near the lows of the week. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Friday’s liquidity report showed Thursday's excess liquidity stayed fell from €1.909T to €1.891T. Use of the marginal lending facility decreased from €58M to €46M.

- Corporate issuance saw 3 issuers come to market for $5.2B

Looking Ahead

- 05:30 (IN)India to sell combined INR120B in 2020, 2026, 2031, 2033 and 2051 bonds

- 05:30 (ZA) South Africa to sell ZAR600M in I/L 2025, 2033 and 2046 bonds

- 06:00 (PT) Portugal Apr PPI M/M: No est v -0.8% prior; Y/Y: No est v +0.8% prior

- 06:00 (UK) DMO to sell combined £3.0B in 1-month, 6-month and 12-month Bills (£0.5B, £1.0B and £1.5B respectively)

- 06:30 (IS) Iceland switch auction

- 06:45 (US) Daily Libor Fixing

- 07:00 (BR) Brazil May IGP-M Inflation (2nd Preview): 1.1%e v 0.4% prior

- 07:30 (TR) Turkey May Central Bank TCMB Survey of Expectations

- 07:30 (IN) India Weekly Forex Reserves

- 08:00 (IN) India announces upcoming bill issuance (held on Wed)

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (CA) Canada Apr CPI M/M: 0.3%e v 0.3% prior; Y/Y: 2.3%e v 2.3% prior, CPI Core- Common Y/Y: 1.9%e v 1.9% prior, CPI Core- Median Y/Y: 2.1%e v 2.1% prior, CPI Core- Trim Y/Y: 2.1%e v 2.0% prior, Consumer Price Index: 133.3e v 132.9 prior

- 08:30 (CA) Canada Mar Retail Sales M/M: 0.3%e v 0.4 % prior; Retail Sales Ex Auto M/M: 0.5%e v 0.0% prior

- 08:30 (CL) Chile Central Bank Meeting Minutes

- 08:30 (CL) Chile Q1 GDP Q/Q: 1.0%e v 0.6% prior; Y/Y: 4.0%e v 3.3% prior

- 08:30 (CL) Chile Q1 Current Account: -$0.1Be v -$0.4B prior

- 09:00 (BE) Belgium May Consumer Confidence: No est v 2 prior

- 09:15 (US) Fed’s Kaplan (dove, non-voter) moderates Q&A

- 09:15 (US) Fed Brainard (voter, dove) on Community reinvestment act

- 11:00 (EU) Potential sovereign rating after the close ( Denmark Sovereign Debt to Be Rated by Moody's; Netherlands and Switzerland Sovereign Debt to be rated by S&P

- 13:00 (US) Weekly Baker Hughes Rig Count data

Italy’s “Contract for the Government of Change”

The populist parties of the League and the 5-Star Movement signed an accord to form a ruling coalition. The agreement is called "Contratto Per Il Governo Del Cambiamento" or "Contract for the Government of Change". Five Star leader Luigi Di Maio said on Facebook that "it has been 70 very intense days, so many things have happened, but in the end we managed to achieve what we announced in the campaign."

The 58-page document contains no mention of exit from the Eurozone. But it called for a review of EU governance and fiscal rules.

Regarding fiscal policies, it said "the government's actions will target a programme of public debt reduction not through revenue based on taxes and austerity, policies that have not achieved their goal, but rather through increased GDP by the revival of internal demand."

That indicates there could be less revenue and more debt for the governement in the near term. Italian 10 year yield jumps to high as 2.22 today, hitting the highest level since last July.

The joint program will be put to vote by 5-Star and League members. After approval, it will be presented to Italian President Sergio Mattarella.

Fundamentals: Gold And Oil

Asian oil demand is strong

Trump has indicated there may not be a favourable outcome

Oil prices are holding on to its gains as investors believe that the demand equation is sturdy and it would keep the price at its current levels. Asian oil demand is strong and as long as the demand is stronger than the supply, the basic law of economics would continue to support the price. Broadly speaking, the OPEC supply cut is the reason which reduced the supply glut. Having said this, we do believe the price has hit its ceiling for now, so expect consolidation or even a pull back to some extent is also on the table. The US shale producers remain the biggest threat to rattle the supply.

The precious metal has broken a key significant level of $1300, this effects the gold price. It has marked its lowest level for the year and the possibilities are we may stay below the $1300 for some time unless there is a major risk event. The strength of the dollar index and the subdued reaction to the geopolitical tensions by investors are the reasons behind the move. Failure of the US to reach any trade deal with China, as Trump has already indicated that there may not be a favourable outcome, could stimulate some demand for gold. Investors would seek safe haven due to a full blown trade war.

On the other hand, the Fed members are confident that the economy is fairly in a good shape and the US economy has reached the maximum threshold in terms of its full employment. This builds the strength for the Fed’s Hawkish stance towards their monetary policy.

Italian Politics To Decide Markets Fate

Friday May 18: Five things the market is talking about

In Europe, regional bourses are trading a tad lower as E.U stocks fail to follow their Asian counter parties higher on a potential breakthrough in trade negotiations between China and the U.S.

The yield on U.S 10-year notes (+3.105%) is steady after reaching their highest level in seven-years mid-week. The dollar remains little changed against G10 currency pairs, along with gold, amid reports that China offered to cut its annual trade surplus by -$200B, in part by increasing imports of U.S goods.

Brent crude continues to edge higher after topping +$80 a barrel yesterday amongst Middle East tensions and signs that global stockpiles continue to decrease. Even new uncertainty over peace on the Korean peninsula appears to have been brushed aside.

In Italy, the 5-Star movement leader Di Maio confirmed agreement on a government contract with the League party. The program is said not to include the call for QE debt to be excluded from debt calculations, and at the moment, have dropped reference to a Euro exit procedure with no mention of request for ECB to write off -€250B in debt.

On tap: Canadian retail sales and inflation numbers are due at 08:30 am EDT. Chinese Vice-Premier Liu is in Washington for more trade talks.

1. Stocks mixed results

Japan’s Nikkei share average rallied to a four-month high overnight and printed its eighth straight weekly gain after a weaker yen (¥111.00) lifted exporters. The Nikkei gained +0.4%, while the broader Topix rallied +0.5%.

Down-under, the Aussie stock benchmark struggled overnight, resulting in a third drop in four-days and put an end to the six-week winning streak. The S&P/ASX 200 eased -0.1%, putting the week’s decline at -0.5%. In S. Korea, stocks finished strongly. The Kospi rallied +0.5% to 2460.65, cutting the week’s drop to -0.7% in reversing last week’s gain.

China and Hong Kong stocks rose slightly overnight, as investors bet Beijing and Washington would reach a compromise in trade talks. The CSI300 index rose +0.1%, while the Shanghai Composite Index gained +0.3%. In Hong Kong, the Hang Seng index added +0.2%.

In Europe, indices trade lower across the board following recent gains and slight weakness in the U.S markets overnight.

U.S stocks are set to open in the ‘black’ (+0.1%).

Indices: Stoxx600 -0.3% at 394.5, FTSE -0.2% at 7770.4, DAX -0.1% at 13094, CAC-40 -0.3% at 5605, IBEX-35 -0.5% at 10163, FTSE MIB -1.1% at 23548, SMI -0.3% at 8960, S&P 500 Futures +0.1%

2. Oil prices firm on OPEC cuts and looming Iran sanctions, gold lower

Oil prices continue to hold firm on strong demand; ongoing supply cuts led by OPEC, and looming U.S. sanctions against major crude exporter Iran.

Nevertheless, surging U.S output is expected to offset at least some of the above shortfalls.

Brent crude futures are at +$79.55 per barrel, up +25c, or -0.3% from Thursday’s close. Brent broke through +$80 for the first time in seven years yesterday. U.S West Texas Intermediate (WTI) crude futures are at +$71.65 a barrel, up +16c, or +0.2%.

Crude prices have received broad support from voluntary supply cuts led by OPEC. However, U.S sanctions against Iran could remove more than +1m bpd from the market.

Note: Higher oil prices due to a tighter physical market and geopolitical tensions could weigh significantly on the macro outlook for EM.

Ahead of the U.S open, gold prices have eased, trading atop this year’s low, pressured by a firm U.S dollar amid surging U.S. Treasury yields. Spot gold is down about -0.1% at +$1,289.35 per ounce. The metal is heading for its biggest weekly decline since early December. U.S gold futures are -0.1% lower at +$1,288.60 per ounce.

3. Look to Italy for direction

The market continues to focus on Italy and their bond spreads. The 10-year Italy/German bond spread is wider by over +5 bps to approach +160 bps (a four-month high). The 10-year BTP yield has backed up +30 bps this week to its highest level since Oct above +2.15%.

Elsewhere, the yield on 10-year Treasuries fell -1 bps to +3.10%, the first retreat in more than a week. In Germany, the 10-year Bund yield decreased -1 bps to +0.63%, while in the U.K, the 10-year Gilt yield dipped -1 bps to +1.551%.

4. Dollar sees sideway trading

The USD is a tad softer in light trading and is still poised for its fifth consecutive week of gains.

EUR/USD (€1.1786) is trading atop of the psychological €1.1800 handle, however the Italian political uncertainty continues to provide additional impetus for a lower EUR.

Note: The recent widening in the BTP/Bund spread could pressure the ECB to keep providing accommodative policy support in the medium term.

The GBP/USD (£1.3485) is again probing below the £1.35 level after reports circulated that E.U Leaders brushed off PM May’s idea for customs plan guarantees.

USD/JPY (110.95) is little changed, however, the steepening U.S yield curve continues to benefit the pair as it tests the ¥111.

If Canadian April CPI and March retail sales show some growth this morning (08:30 am EDT), its expected to be “modestly” supportive of the loonie (C$1.2824) and should push USD/CAD below C$1.28 handle again.

5. Japan inflation disappoints

Overnight, Japanese inflation numbers disappointed as CPI fell -0.4% last month, putting the year-over-year figure back at +0.6%.

Consumer-price growth hit +1% in February, the first time it was that high in four-years and was considered a hopeful sign that the Bank of Japan (BoJ) years long effort to get inflation to +2% was again back on track.

But, it’s not to be and is reason enough why the BoJ recently scrapped its forecast on when Japanese policy makers thought +2% would be reached.

Note: The BoJ has pushed out the target date on a number of occasions in the past five-years. And if prices are barely rising, how long will the recent uptick in wages last?