Sample Category Title

IMF forecasts slower Eurozone growth in 2018, 2019. Urges fiscal reforms

IMF forecasts Eurozone growth to slow to 2.3% this year, from 2017's 2.4%, and drop further to 2.0% in 2019. IMF noted that "with economic prospects continuing to improve in the short term but medium-term prospects less bright, policymakers should seize the moment to rebuild room for fiscal manoeuvre and push forward with reforms to boost growth potential"

And it pointed out that "policymakers should strive to bring fiscal deficits within range of balance over the next few years.:" With that " automatic stabilizers and fiscal stimulus can be deployed again, should downside risks materialize."

EU Katainen to US: No concession to get permanent exemption from steel tariffs

European Commission Vice-President Jyrki Katainen said they're "open for improving our trade relations" with the US. But he warned that "it's not a concession in order to get a permanent exemption from higher steel and aluminium tariffs."

Katainen emphasized that "there's no reason for those tariffs... It wouldn't be logical to give up under pressure that is unjustified. We don't negotiate under any kind of threat."

Euro, Pound Turn Lower As Dollar Enjoys Gains, Eyes On US Retail Sales

Here are the latest developments in global markets:

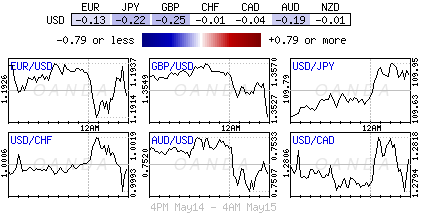

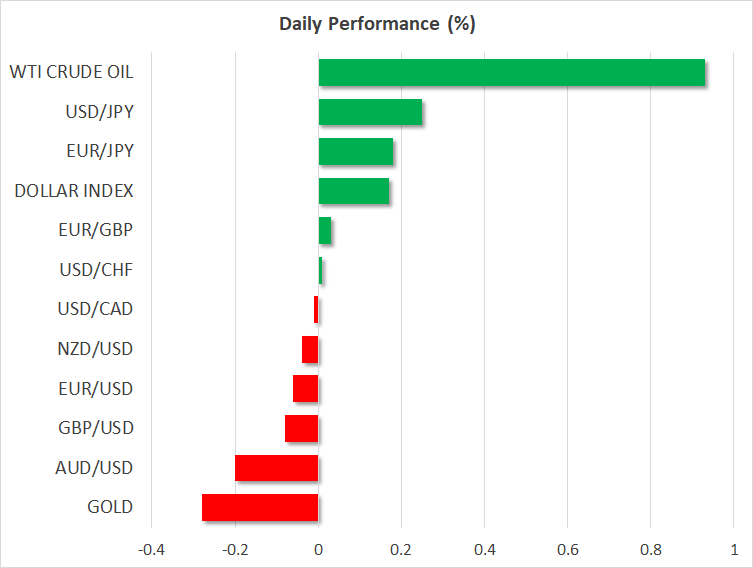

FOREX: Stronger US long-term Treasury yields continued to underpin the dollar during the early European afternoon, sending dollar/yen slightly above the 110 key-level before a slip to 109.90 (+0.23%). The US dollar index pulled back from an almost two-week peak of 92.80 touched on Monday but was set to complete a second green day in a row, last trading at 92.75 (+0.18%). The greenback will be looking for direction from US retail sales later in the session. Pound/dollar fell initially to 1.3522 in the wake of a mixed employment report but managed to pare some of its losses afterwards inching up to 1.3540 (-0.08%). The data showed a larger-than-expected employment increase in March but wage growth moderated from the previous month. The unemployment rate remained unchanged at 4.2%. Following disappointing German ZEW economic sentiment and Eurozone industrial production readings, euro/dollar dropped to an intra-day low of 1.1910 and remained around that level thereafter. In antipodean currencies, aussie/dollar extended losses towards 0.7514 (-0.13%) after touching a two-week high of 0.7537 earlier in the session, while kiwi/dollar managed to recover earlier loses, climbing to 0.6919 (+0.01%). Dollar/loonie slipped marginally to 1.2810 (-0.01%). Meanwhile, dollar/lira recorded a fresh high of 4.3969 (+0.43%) after Turkish President Recep Tayyip Erdogan said he intends to take greater control and take more responsibility for monetary policy if he wins the country’s elections next month.

STOCKS: European stocks were moving mixed at 1000 GMT. The pan-European STOXX 600 was up by 0.05%, while the blue-chip Euro STOXX 50 was down by 0.08%. In Germany, the DAX eased by 0.14%, while the French CAC 40 rose by 0.07%. In Italy, the FTSE MIB 100 was up by 0.10%, while the British FTSE 100 traded higher by 0.21%. The Spanish IBEX 35 traded lower by 0.32%. Turning to the US, futures tracking the Dow Jones, S&P 500, and Nasdaq 100 were all in negative territory, pointing to a lower open today after facing a sharp buying interest in the previous days.

COMMODITIES: West Texas Intermediate (WTI) crude oil and Brent climbed to $71.13 (+0.24%) and $78.69 (+0.56%) per barrel respectively as persisting geopolitical tensions between Iran and the US continued to support oil prices. In precious metals, gold dropped to $1,309.38 (-0.23%) per ounce on the back of the rising dollar despite escalating tensions in Gaza.

Day ahead: US retail sales in focus; oil eyes API weekly crude oil report

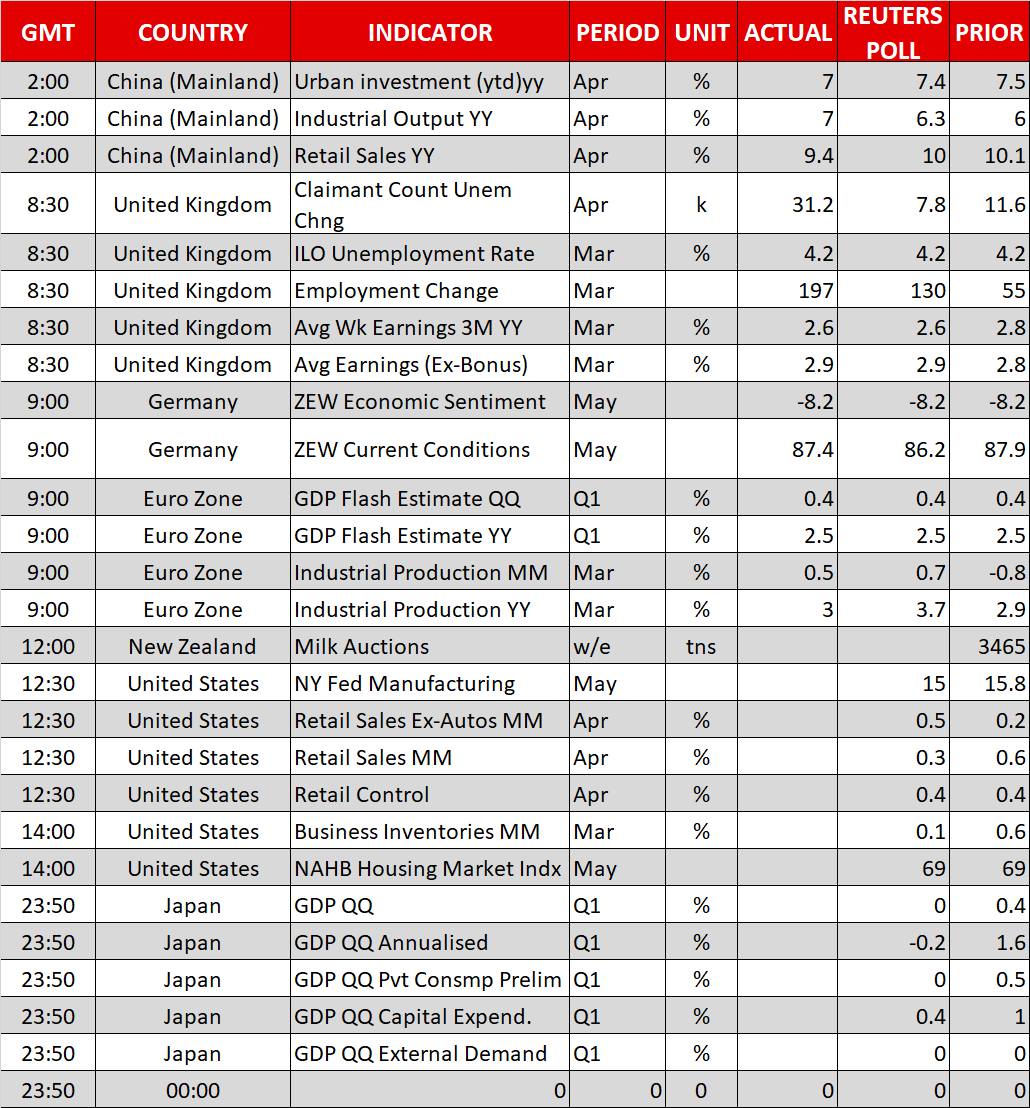

Tuesday’s economic calendar will be a little bit busy for the remainder of the day, with US data dominating the session.

At 1230 GMT, the US Census Bureau is scheduled to release retail sales figures, bringing fresh volatility to the strengthening dollar which faced significant buying pressure today on the back of rising US long-term Treasury yields as well as easing trade tensions. Particularly analysts expect retail sales to slow down for the third consecutive month in April, increasing by 0.3% m/m after rising by 0.6% in the prior month. Higher oil prices and an unusually cold weather could have curbed consumption during the month. In case of a negative surprise in the data, optimism for a fourth-rate hike by the Fed this year could fade, driving the dollar subsequently lower. On the other hand, better-than-expected numbers could provide further gains to the greenback.

At the same time, the New York Fed will be publishing its Empire State Manufacturing survey for the month of May, while a few hours later at 1400 GMT readings on business inventories and NAHB housing prices are expected to attract attention as well.

Elsewhere, global dairy prices delivered at a tentative time out of New Zealand are expected to challenge the kiwi, whereas, in oil markets, investors will be waiting for the American Petroleum Institute to report on US crude oil stocks for the week ending May 11.

Trade headlines will remain in focus as China’s top economic aid to President Xi Jinping will be holding talks with the US Treasury Secretary Steven Mnuchin this week. This comes a day after Trump ordered his officials to assist the Chinese Telecom company ZTE to “get back into business”. Note that American companies were banned from selling their products to the company for the past seven years.

Developments around the 2015 Iranian nuclear deal would also attract interest, with EU foreign policy chief Federica Mogherini and the foreign ministers of Britain, France, and Germany gathering today to discuss the topic.

As of today’s, public appearances, a number of Fed policymakers are set to make comments. At 1200 GMT, Dallas Fed President Robert Kaplan (non-voting FOMC member in 2018) will be talking on “Energy, Trade, and Economic Growth”. Later at 1710 GMT San Francisco Fed President John Williams will be speaking at 1710 GMT. Moreover, the Senate Banking Committee will be holding a hearing on the nominations of Richard Clarida as member and vice chairman of the Federal Reserve Board of Governors, and Michelle Bowman as a member of the Federal Reserve Board of Governors at 1400 GMT.

At 1150 GMT, preliminary figures on GDP growth as well as data on GDP consumption and capital expenditure components out of Japan are expected to move the yen, while the aussie is also anticipated to face some volatility after the release of the Australian Westpac consumer sentiment and wage growth index at 0030 GMT and 0130 GMT respectively.

Iran FM Zarif had “very good and constructive” meeting with EU Mogherini

Iranian Foreign Minister Mohammad Javad Zarif said the meeting with European Union's foreign policy chief, Federica Mogherini in Brussels was "very good and constructive". Zarif also said that both sides were on the "right track" to ensure that the interests of the JCPOA's "remaining participants, particularly Iran, will be preserved and guaranteed." Zarif's comments came before meeting with foreign ministers of Germany, France and the UK, on continuing the JCPOA nuclear agreement after US withdrawal.

Separately, IRNA news agency quoted Iranian President Hassan Rouhani asking EU to stand against the US' "illegal and illogical" actions of pulling out from JCPOA.

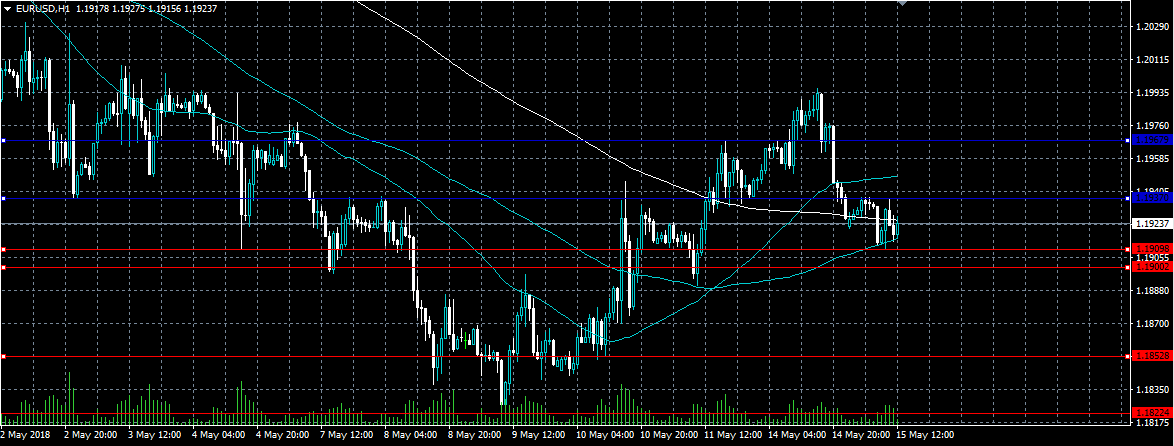

EURUSD Still Holding Above 1.1900

The euro has remained weak against the US dollar during the European trading session, with sellers moving the pair to a new weekly trading-low, at 1.1909. Dip-buying in the EURUSD pair has so far remained quite muted, with price only managing a shallow bounce towards the 1.1937 level before sellers moved in again. Traders now look for further losses below the 1.1900 level, and the release of key monthly Retail Sales numbers from the US economy.

The EURUSD pair is intraday bearish while trading below the 1.1938 level, further downside towards 1.1900 and 1.1852 remains likely.

If the EURUSD pair moves above the 1.1938 resistance level, buyers may be encouraged to test towards the 1.1967 and 1.1996 levels.

GBPUSD Lowe After Technical Failure

The British pound has started to drift lower against the US dollar, after buyers failed to hold price above the key 1.3600 level on Monday. The GBPUSD pair was sold aggressively from the 1.3606 level during yesterday’s US session, and has so far found daily technical support from the 1.3523 level. During the European session, the pair failed to react to important UK economic data, and traders now look towards key Retail Sales figures from the US economy.

The GBPUSD pair remains bearish while trading below the 1.3600 level. Key support remains at the 1.3523 and 1.3501 levels.

If the GBPUSD pair starts to trade above the 1.3600 level, buyers may be encouraged to test towards the 1.3650 and 1.3700 levels.

DAX Trading Sideways After Eurozone, Germany GDP

The DAX continues to trade quietly this week. Currently, the DAX is at 12,991 points, up 0.10% on the day. On the release front, German Preliminary GDP came in at 0.3%, close to the forecast of 0.4%. Eurozone GDP came in at 0.4%, matching the forecast. German ZEW Economic Sentiment came in at -8.2, weaker than the estimate of -8.0 points. Eurozone ZEW Economic Sentiment was stronger, improving to 2.4 points. This beat the estimate of 2.0 points. On Wednesday, Germany and the eurozone release CPI reports and ECB Governor Mario Draghi will speak at an ECB event in Frankfurt.

There were no surprises from German and Eurozone GDP data for the first quarter, as both indicators were within expectations. The data has raised concerns, however, as the Q1 numbers are pointing to a slowdown – in Q4 of 2018, both Germany and the eurozone posted gains of 0.6%. Will economic conditions improve in Q2? Institutional analysts don’t seem optimistic, according to the well-respected ZEW Economic Sentiment surveys. The German indicator posted a sharp drop of -8.2 for a second straight month – the first declines since July 2016. The eurozone release improved to 2.4, but low reading certainly doesn’t show much optimism. The markets are bracing for more soft numbers on Wednesday, as Germany and eurozone release CPI reports. If these indicators miss their estimates, the euro could lose ground.

Bank of France Governor Francois Villeroy de Galhau raised some eyebrows on Monday after making hawkish comments about ECB interest rates hikes. Villeroy said that the ECB could soon provide additional guidance on the timing of a rate hike. In its last rate statement, the ECB said that any rate hikes would occur ‘well past’ the wrap-up of the stimulus program, which is slated to end in September. Villeroy stated that ‘well past’ could be a matter of quarters, rather than years. Investors snapped up euros on Monday after Villeroy’s comment, but the euro failed to hold onto these gains and ended the Monday session with small losses.

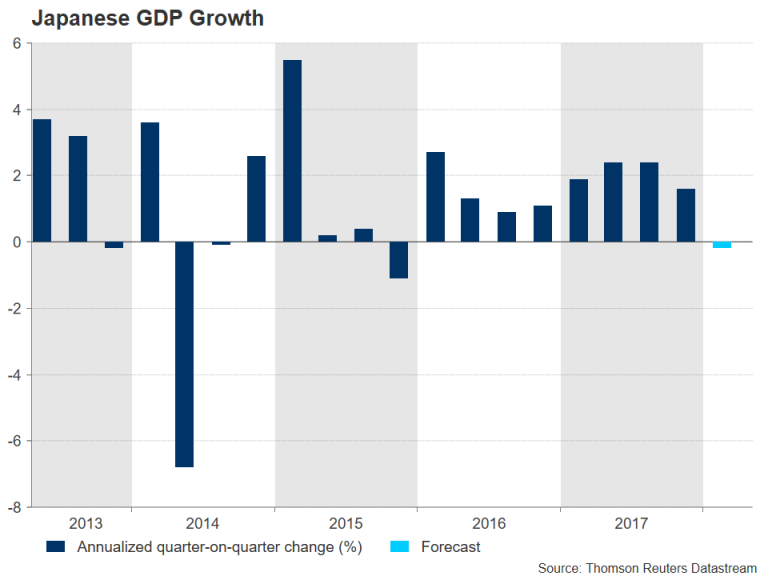

Japan’s Impressive Run Of GDP Growth Likely Ended In Q1

GDP data out of Japan will come into focus on Wednesday (Tuesday, 23:50 GMT) as investors watch how resilient the Japanese economy was to the soft patch in global growth during the first three months of 2018. After achieving eight straight quarters of growth at the end of 2017 – the longest streak of expansion since the 1980s – the big question is whether any contraction at the start of 2018 will be a blip or a major bump in the road for policymakers.

Japan's economy is forecast to have shrunk by 0.2% on an annualized basis in the first three months of the year. On a quarter-on-quarter basis, this translates to a mere 0.05% contraction, or 0% when rounded. Sluggish household consumption and weaker demand for exports are likely to have proved a drag on economic growth in the January-March period.

However, capital expenditure is expected to have held up reasonably well, suggesting businesses remain optimistic about the future. Core machinery orders – a key gauge for future business spending – rose robustly in both January and February, though they are forecast to drop by 3% month-on-month in March in data due on Thursday. If global demand picks up in the coming months and consumer spending also recovers, GDP growth should rebound in the current quarter.

Other economies have also suffered a slowdown in the first quarter, mainly the Eurozone and the United Kingdom. But assuming there are no unexpected headwinds such as higher US trade barriers, an oil price shock from an escalation of tensions over Iran, or a fresh political crisis in Europe, the outlook for global growth for the rest of 2018 remains upbeat and this should be positive for Japanese exporters.

A bigger concern though for the Bank of Japan, as well as the Abe government, is persistent weakness in real incomes and consequently, consumer spending. Japanese households have been struggling to raise their expenditure following the sales tax increase of 2014 as wage growth has been stagnant. This has weighed on growth and has added to the Bank of Japan's challenges in meeting its 2% inflation target.

However, there are some signs that wage pressures are finally starting to build up. Data out last week showed wages in Japan rose by an annual rate of 2.1% in March – the fastest pace since June 2003, while real wages turned positive for the first time in four months. If the wage picture continues to improve, higher consumer spending should follow suit and growth should bounce back in the coming quarters.

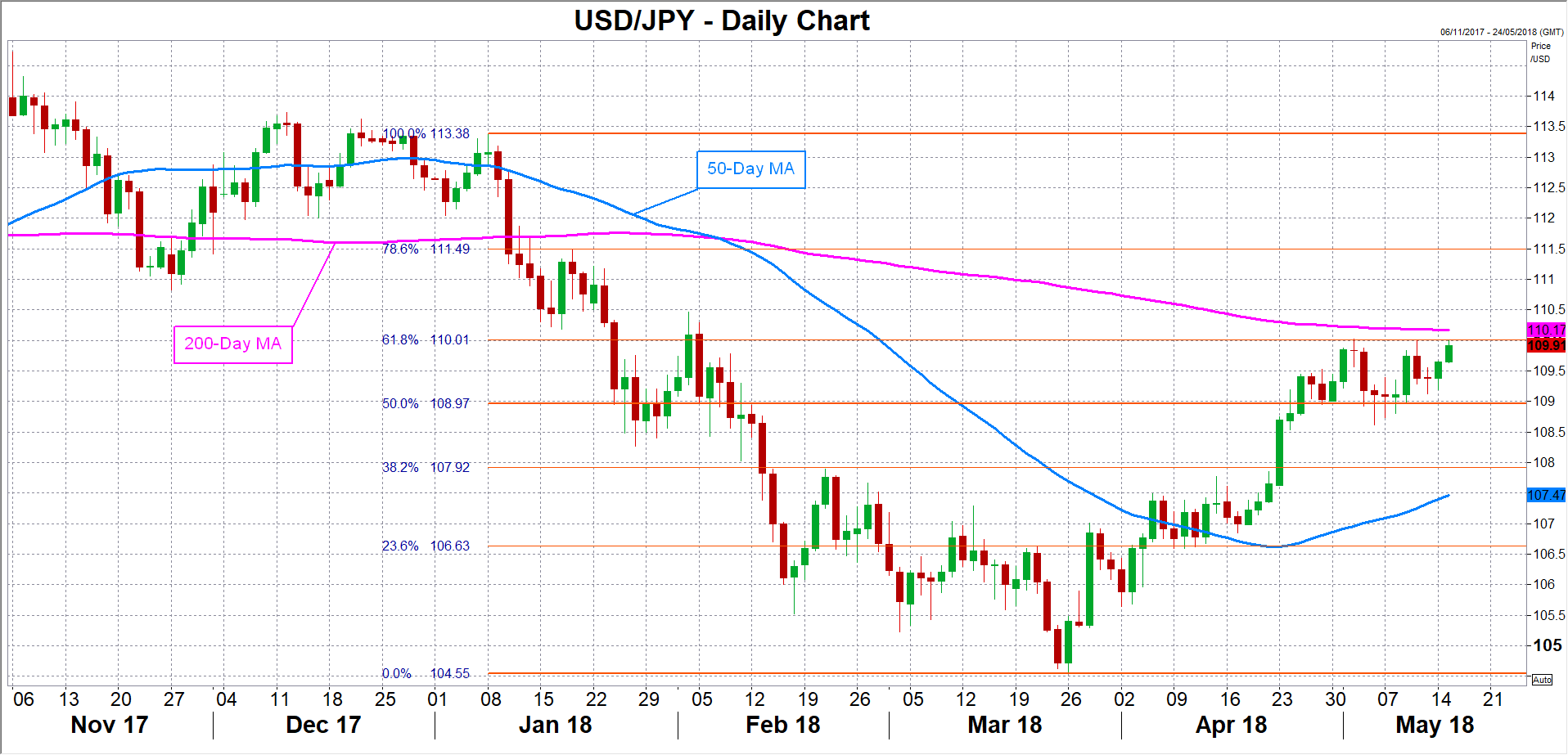

A modest drop in quarterly GDP growth on Wednesday would support this view and could help the yen strengthen in forex markets. Dollar/yen could slip to around the 109 level (the 50% Fibonacci retracement of the downleg from 113.38 to 104.55) if the data comes in largely in line with estimates. A better-than-expected GDP figure could exert a bigger downwards pressure on the pair, pulling it towards the 108 level (38.2% Fibonacci). However, should the data miss expectations and the economy shrinks more than anticipated, dollar/yen could find fresh upside momentum to make a convincing break above key resistance at the 110 level (61.8% Fibonacci).

Selling Pressure In Emerging Market Currencies Accelerates Following Latest Lira Decline

Emerging market currencies across the globe are coming under renewed selling pressure during trading this week.

The exact catalyst behind why the emerging market currencies continue to be plagued by selling momentum is a difficult one to determine, although the latest indications suggest that the motivator could now be beyondcentral bank expectations for higher US interest rates. It is being suggested that the persistent Turkish Lira weakness could be weighing down on the general emerging market sentiment.

Although investors were previously treating developments around currencies like the Turkish Lira and the Argentine Peso as idiosyncratic matters, we are now noticing similarities between the selloff in Turkey and Argentina leading to declines in emerging markets elsewhere. The latest indication of this was on Tuesday morning when comments from Turkish President Erdogan on domestic central bank policy appear to have encouraged weakness in emerging market currencies outside of Turkey.

The early morning comments from Erdogan were clearly not what investors wanted to hear. Erdogan made it clear that he intends to have more influence on monetary policy and economic matters if he wins the election next month, which is seen at the very least as a severe threat to central bank independence. This has resulted in the Turkish Lira hitting yet another historic low against the US Dollar with the latest milestone level being marginally close to 4.40 against the Dollar.

Investor confidence in Turkey is already at severely low levels. If Erdogan is able to insert more influence around central bank policy and economic matters we can’t rule out the possibility that the Lira will weaken all the way to 5 against the Dollar by the end of the summer. This would represent another dramatic turn towards the worst, when you consider that the market finally appeared ready to consider purchasing the Lira on reports last week that Erdogan would call a summit to discuss improving the fortunes of the Lira. Following the latest comments from Erdogan we can consider this optimism to be over.

Erdogan is a clear advocate for lower interest rates in Turkey. If he is able to influence central bank policy by cutting interest rates there would be a risk of removing one of the only options out there to combat dangerously high inflation and encourage inflows into Turkey. It would also risk weighing further on the political risk factor that deters investors away from the Lira and despite the currency probably standing as the most undervalued around the globe, it would be difficult to see a road for recovery.

The indications that the always developing Turkey story is weighing on investor sentiment elsewhere represents a fresh worry for the emerging markets.

There is a massive election in Turkey next month and the latest comments from Erdogan this morning are going to risk the Lira nosediving even further against the US Dollar, if he does win the election. This ultimately means that we can’t rule out the risk that other emerging market currencies will selloff if the fears around the Turkish Lira intensify further as a result of reduced investor appetite towards taking on risk.

Rate Differentials And Trade Fears Handcuff Capital Markets

Tuesday May 15: Five things the markets are talking about

Risk-off trading action and higher sovereign yields dominated capital markets overnight session.

Euro stocks continue to struggle for traction following Australasia mixed equity session as investors grappled with worries around global trade, growth and geopolitics.

This week's U.S Treasury bond sell-off continues to deepen and is allowing the dollar to find support against G10 currency pairs on rate differentials. Crude oil prices are on the precipice of exploding higher.

In the U.K, data this morning showed that employment jumped, but strong wage growth remains elusive. While in Germany their economy cools a tad.

On tap: China's Vice Premier, Liu He, is expected in Washington for more trade talks today. U.S retails sales are due at 08:30 am EDT.

1. Equities see ‘red'

In Japan, stocks pulled back from atop of their four-year highs overnight, hit by profit taking, although financials staged a rally on hopes of strong earnings for the sector. The Nikkei share average ended -0.2% lower, while the broader Topix was unchanged.

Down-under, Aussie stocks slide deeper into the close and ended more than a week of broad gains. The S&P/ASX 200 fell -0.6% to register only its fifth decline in 22-sessions. The index was driven down mostly by the resource sector. In S. Korea, more selling in Samsung helped the Kospi fall -0.7% – the electronics giant dropped -1.4% to a one-month closing low.

In Hong Kong, stocks snapped a six-day winning streak to end lower overnight, amid renewed fears of a Sino-U.S trade war and worries about China's economy. The Hang Seng index ended -1.2% down, while the China Enterprises Index closed -0.8% lower.

In China, stocks ended higher on Tuesday, supported by optimism towards MSCI inclusion of 234 Chinese large caps – this has helped some investors to overcome worries about China's economy and Sino-U.S trade war. The blue-chip CSI300 index ended +0.4% higher, while the Shanghai Composite Index closed up +0.6%.

In Europe, regional bourses trade little changed, following a plethora of earnings this morning and weaker U.S futures.

U.S stocks are set to open in the ‘red' (-0.3%).

Indices: Stoxx600 flat at 392.3, FTSE +0.2% at 7725.4, DAX -0.2% at 12955, CAC-40 +0.1% at 5545, IBEX-35 -0.3% at 10229, FTSE MIB +0.3% at 24305, SMI flat at 8999, S&P 500 Futures -0.3%

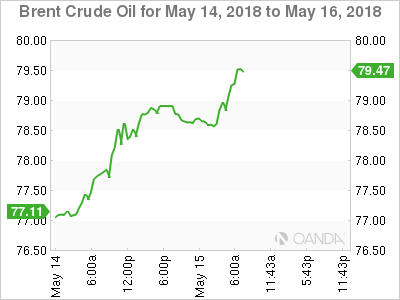

2. Iran sanctions, tight supply send oil to new multi-year high, gold unchanged

Oil prices trade atop of their four year high this morning, supported by tight supply and planned U.S sanctions against Iran that are likely to restrict crude oil exports from one of the biggest producers in the Middle East.

Benchmark Brent crude oil reached +$78.60 a barrel, up +37c and its highest since November 2014. U.S light crude (WTI) is +5c higher at +$71.01 a barrel.

U.S crude continues to trade at a hefty “discount” to Brent due to the sharp rises in domestic production to +10.7m bpd, which has left the U.S market well supplied.

Note: World oil prices have surged by +70% over the last year as demand has risen sharply and OPEC has restricted production.

Data yesterday from OPEC showed that oil inventories in OECD industrialized nations in March fell to +9m barrels above the five-year average, down from +340m barrels above the average in January 2017.

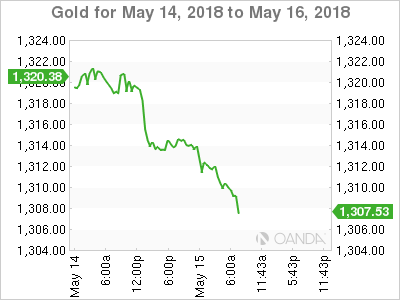

Ahead of the U.S open, gold has been trading little changed overnight, buoyed by Middle East safe-haven demand with the upside potential restricted by a stronger U.S dollar and outlook for higher interest rates stateside. Spot gold is unchanged at +$1,311.51 per ounce. U.S gold futures for June delivery are down -0.5% at +$1,311.30 per ounce.

3. Sovereign yields back up

Behind the divergence of E.U/U.S interest rates has been the divergence of inflation. Last year, U.S inflation was +30 bps on top of the E.U in April, and 12-months on, the spread has widened even further to +120 bps.

Hawkish comments yesterday from some FOMC members have again helped to back up U.S 10-year yields above their psychological +3% handle.

Note: Fed fund odds indicate that U.S policy makers will raise rates three more times this year – they have rallied to +50%, up from +39% a month ago.

Other G7 sovereign yields have also being getting a helping hand from the Banque De France (BoF), whose governor, François Villeroy de Galhau, hinted that the ECB might raise rates next year.

Overnight down-under, the Reserve Bank of Australia (RBA) released their monetary minutes. Members agreed that it was more likely that the next move in the cash rate would be up, rather than down. However, RBA Deputy Governor Debelle sees “no pressure to raise rates” as the Aussie economy is on a slowly improving trajectory, but that doesn't make a case for raising interest rates in the near term.

The yield on U.S 10's has gained +1 bps to +3.02%, the highest in almost three-weeks. In Germany, the 10-year Bund yield climbed +1 bps to +0.62%, also the highest in almost three-weeks. In the U.K, the 10-year Gilt yield increased +1 bps to +1.482%.

4. Sterling pares losses despite wage growth miss

The ‘mighty' USD is steady as market participants continue to focus on yields. The U.S 10-year yield has moved back above the +3% territory, again steepening the U.S curve, which is giving the greenback some support.

The EUR/USD (€1.1929) hovers near its four-month low as various European Q1 GDP data (see below) confirmed the anticipated deceleration in growth.

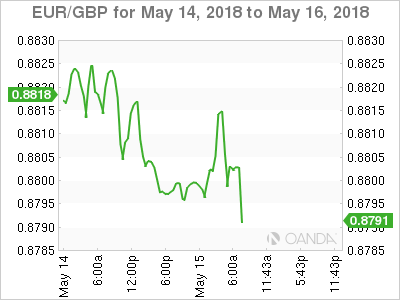

The pound (£1.3557) has pared most of its losses ahead of the U.S open after data this morning showed that U.K wage growth picked up further in March, though the currency's gains are limited as the figures were in line with expectations (see below). EUR/GBP is at €0.8796, down from €0.8813 beforehand.

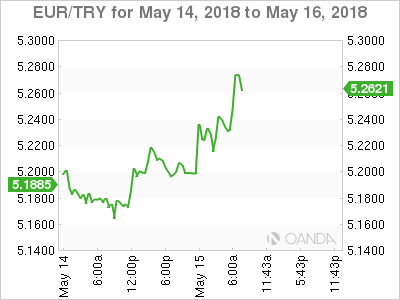

EUR/TRY (€5.2420) hit a new high after Turkish President Erdogan said he intends to tighten his grip on the economy and take more responsibility for monetary policy if he wins an election next month.

5. U.K wage growth disappoints, while German economy cools

Data this morning showed that U.K employers hired many more workers than expected at the start of 2018, but wage growth has yet to accelerate sharply – today's releases will probably do little to alter the outlook for Bank of England (BoE) interest rates.

Employment in Britain rose by +197k during Q1. It's the biggest jump in three years and far exceeding the +130k consensus. U.K average earnings growth ex-bonuses in Q1 was +2.9%, comfortably above the inflation rate of +2.5%. Unemployment also remained low at +4.2%.

Elsewhere, Europe's largest economy cooled sharply in Q1 due to high levels of illness and labor disputes. Germany's annualized growth rate slowed to +1.2% from +2.5% in Q4, 2017.

Note: Market expectations were looking for E.U Q1 GDP growth to decelerate, but, is the effect temporary?

Digging deeper, the “Beats” – Norway, Hungary and Poland and the “Misses” – Germany, Netherlands, Portugal Romania, Czech Republic and “in-line” was the Euro Zone.