Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3523; (P) 1.3566; (R1) 1.3598; More...

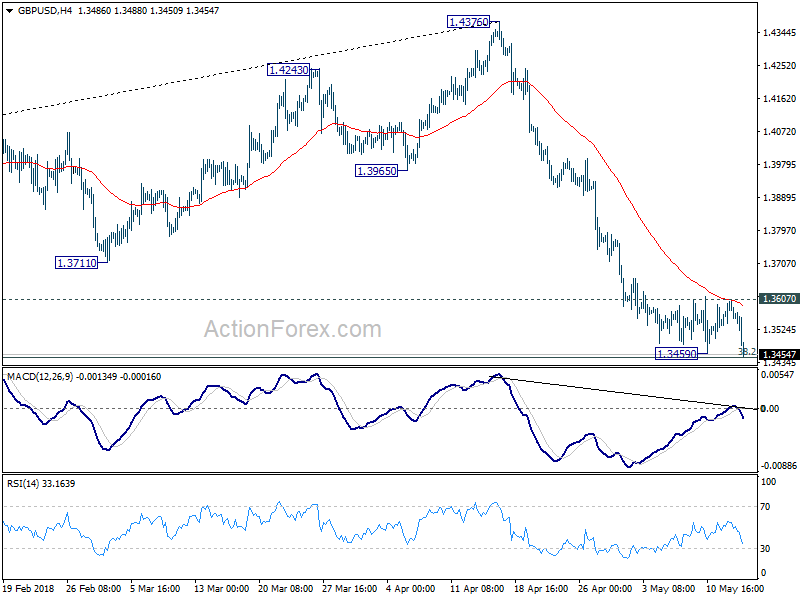

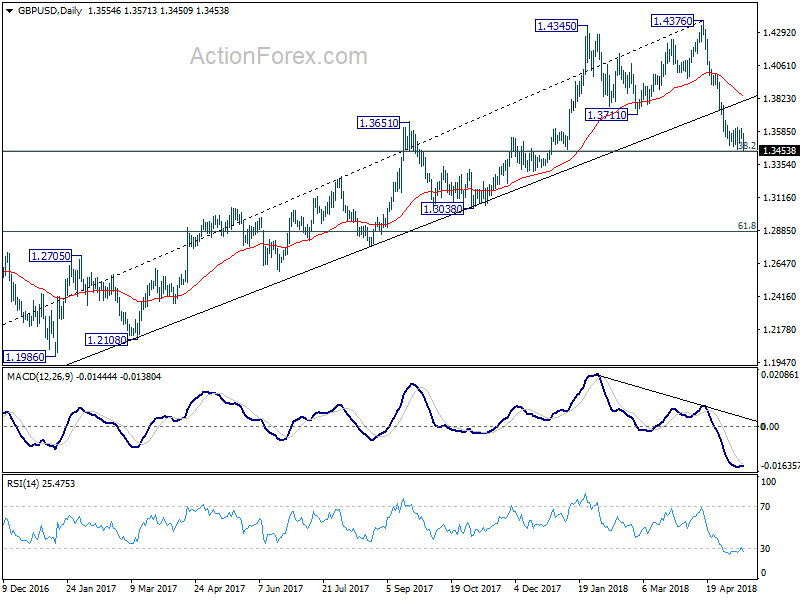

GBP/USD's steep decline and breach of 1.3459 support indicate that consolidation has completed at 1.3607, after rejection by 4 hour 55 EMA. Intraday bias is back on the downside to extend the decline from 1.4376. Sustained trading below 1.3448 fibonacci level will pave the way to next one at 1.2874. On the upside, break of 1.3607 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 was almost met. Break there will target 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3861) holds, even in case of strong rebound.

US: Healthy April Retail Sales Set-up Q2 Rebound in Consumer Spending

Retail sales increased 0.3% in April according to the advance Census Bureau report – on par with expectations. Better yet, the healthy gain came atop of a blowout upward revision to the March tally, which was now reported as a 0.8% gain – previously 0.6%.

Sales at motor vehicle & parts dealers (+0.1%) did little for the headline, unlike gasoline station sales, which rose by a robust 0.8%. Taken together, the two largely matched the gains elsewhere, with the measure that excludes autos and gas also up 0.3% – just shy of the 0.4% expected.

Building materials (0.4%) had a fairly decent month, but spending at eating and drinking place sales (-0.3%) pulled back for the first time in seven months. Excluding gas, autos, building materials, and food services, the so-called 'control group' used in calculating GDP was up 0.4% on the month – also matching the consensus call. Apart for the decline in health store spending (-0.4%) and a touch lower spending at electronics and sporting goods stores (-0.1%), the remaining categories saw gains, with clothing (+1.4%) and miscellaneous stores (+0.9%) leading the pack.

Key Implications

This was a really solid spending report, with little in the way of 'skeletons' to be found in the details. The report indicated that consumers have definitely shed the winter blues and were out in full force in April – following up on the surge in activity already seen in March.

While the pullback in spending on discretionary categories, such as sporting goods and restaurants, was not necessarily welcome, the declines were quite negligible and come after months of good gains. As such, we don't believe this to be signaling a lack of comfort of spending on 'wants' instead of just 'needs'. With everyone who wants a job effectively having it – as the jobless rate fell below 4% in April – and wage gains becoming more pronounced – average hourly earnings rose by an annualized 3.0% in Q1 for instance – there is every reason to expect consumer spending to continue to grow at a healthy pace.

All in all, this report re-affirms our expectations for a bounce-back in consumer spending in Q2 after a weak showing in the first quarter of the year. Spending looks on track to advance by close to 3%, helping along the economy to advance by a similar magnitude. This will be a positive signal for the FOMC, with many members of the committee expecting that the Q1 weakness was transitory. As such, the report further solidifies the expectations for a June rate hike, with at least one other hike (and perhaps two) likely in the second half of the year.

Canadian Dollar Slips, US Retail Sales Misses Mark

The Canadian dollar has posted considerable slight losses in the Tuesday session. Currently, USD/CAD is trading at 1.2897, up 0.66% on the day. On the economic front, there are no Canadian events on the schedule. In the US, the focus is on consumer spending reports. Retail Sales dipped to 0.3%, shy of the estimate of 0.4%. Core Retail Sales edged up to 0.3%, but missed the forecast of 0.5%. On Wednesday, Canada releases Manufacturing Production and the US will release construction reports.

Canadian employment numbers were mixed on Friday. The economy shed 1100 jobs in April, surprising analysts that had predicted a strong gain of 17.8 thousand. This marked the first decline since January. There was better news from wage growth, which jumped 3.3% in April on an annualized basis. The Canadian currency has received some help from strong oil prices, which are at the highest level in 3-1/2 years. President Trump’s bombshell announcement that the US would withdraw from the Iran nuclear deal, as well as tensions in the Middle East have raised fears of supply disruptions and have significantly pushed up the price of crude.

With the U.S economy performing well in 2018, the U.S consumer is feeling very optimistic. On Friday, the UoM Consumer Sentiment improved to 98.8 in April, beating the estimate of 98.4 points. The U.S labor market is at near or full employment, which has resulted in a slowdown in job growth due to a shortage of skilled workers. This was underscored last week, as JOLTS Job Openings climbed to a record 6.6 million. At the same time, inflation levels remain low, as the Federal Reserve target of 2 percent remains elusive. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. Inflation levels will be an important factor for the Fed in its monetary policy projection, which remains at two more hikes in 2018. The odds of a rate hike at the June hike stands close to 100%.

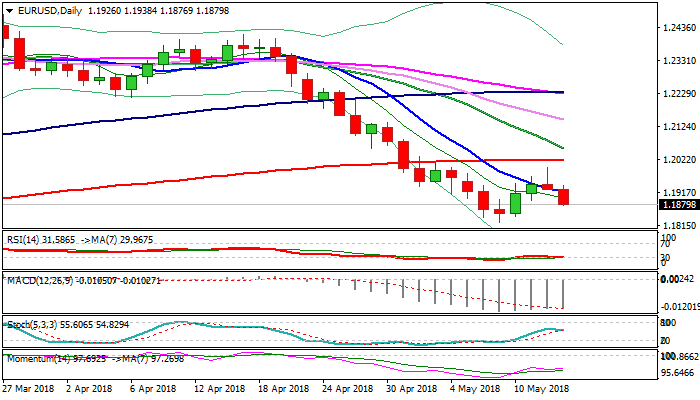

EURUSD – Bearish Bias Strengthens on Acceleration Below Thick 4-hr Cloud

Strong acceleration lower in the mid-European session confirms Euro’s bearish stance, as dollar rallies on higher US yields.

Fresh weakness broke below 4-hr cloud base 1.1906 and cracked next pivot at 1.1888 (Fibo 61.8% of 1.1822/1.1996 upleg) in extension.

Falling thick 4-hr cloud weighs heavily as the pair extends weakness towards 1.1863/49 ( Fibo 76.4% / rising weekly 55SMA), with key support at 1.1822 (09 May low) coming in focus.

Growing bearish sentiment needs confirmation on firm break below weekly 55SMA and 1.1822 low to signal extension of pullback from 1.2555 (2018 high) towards next key support at 1.1709 (Fibo 38.2% of 1.0340/1.2555, Dec 2016/Feb 2018 rally).

Falling 10SMA (currently at 1.1920) capped today’s action and maintains bearish pressure

US Apr retail sales are in focus as key event of the American session.

Res: 1.1945; 1.1963; 1.1980; 1.1996

Sup: 1.1910; 1.1889; 1.1875; 1.1863

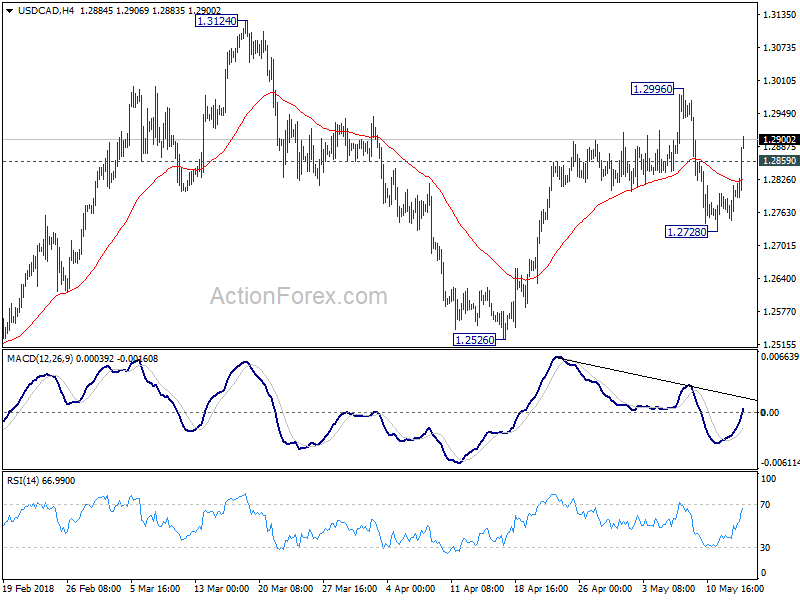

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2762; (P) 1.2793; (R1) 1.2843; More....

USD/CAD's strong rebound and break of 1.2859 minor resistance argues that pull back from 1.2996 has completed at 1.2728 already. Intraday bias is back on the upside for 1.2996 first. Break will affirm our bullish view that rebound from 1.2061 hasn't completed. Retest of 1.3124 key resistance should be seen next. This bullish case will remain in favor as long as 1.2728 support holds.

In the bigger picture, current development suggests that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048

EURAUD Holds in Narrow Range in Bear Term; Touches and Rebounds on Ascending Trend Line in Long Term

EURAUD remains under pressure as it continues to trade within a trading range in the short-term over the last two months with upper boundary the 1.6140 resistance level and lower boundary the 1.5775 support level. The price hit the long-term ascending trend line and rebounded creating two consecutive bullish days. The near-term technical indicators suggest a bullish movement.

Looking at the daily timeframe, the RSI indicator is holding below the 50 level but is sloping upwards, while the stochastic oscillator is moving higher, following the bullish crossover within the %K line and %D line.

Upsides moves are likely to find resistance at 1.6140. Moving above this region would help the pair to endorse the bullish structure and touch the 1.6190 strong barrier, taken from the high on March 28. Further gains would drive EURAUD towards the 1.6580 key level, identified by the August 2015 high.

Should the price reverse lower and decline below the uptrend line, immediate support should come at the 1.5600 handle, which stands near the 23.6% Fibonacci retracement level of the upleg from 1.3620 to 1.6190. Below that, the 38.2% Fibonacci is another major support around the 1.5210 level.

Overall, EURAUD has been developing within an ascending movement since February 2017 and touched the diagonal line several times in the past.

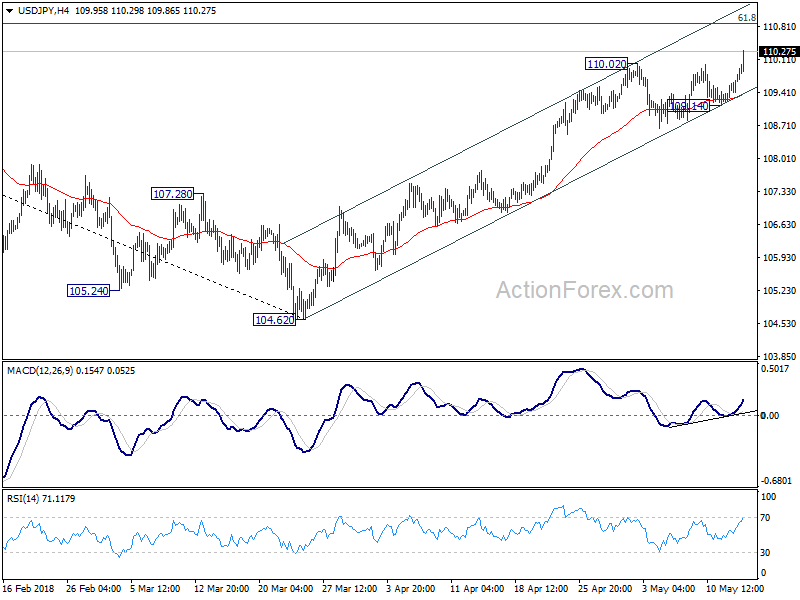

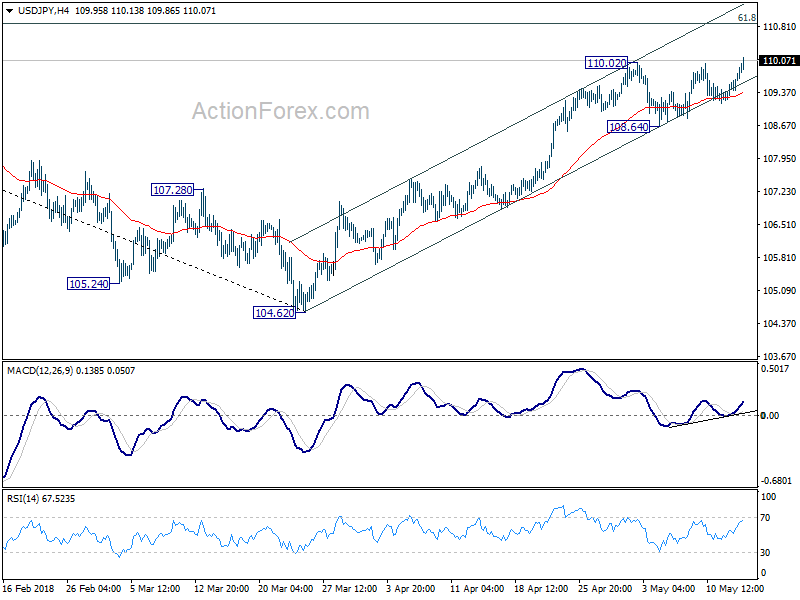

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.33; (P) 109.50; (R1) 109.82; More...

USD/JPY rises to as high as 110.29 so far and the strong break of 110.02 resistance confirms rally resumption. Intraday bias is back on the upside as rise from 104.62 should now target 61.8% retracement of 114.73 to 104.62 at 110.86 next. Firm break there will target medium term trend line resistance at 112.43. On the downside, below 109.14 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 55 day EMA (now at 108.30) holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above.

Dollar Shines as 10 Year Yield Hits Highest Since 2011

Dollar surges broadly today as boosted by strong rally in treasury yield. 10 year yield reaches as high as 3.049 so far today and breaks key resistance level of 3.036 (2013 high). TNX reaches the highest level since 2011. Released from US, retail sales rose 0.3% mom in April, in line with expectation. Ex-auto sales rose 0.3% mom, below expectation of 0.5% mom. Empire state manufacturing index rose to 20.1, up from 15.8 and beat expectation of 15.0. But these data are shrugged off by traders.

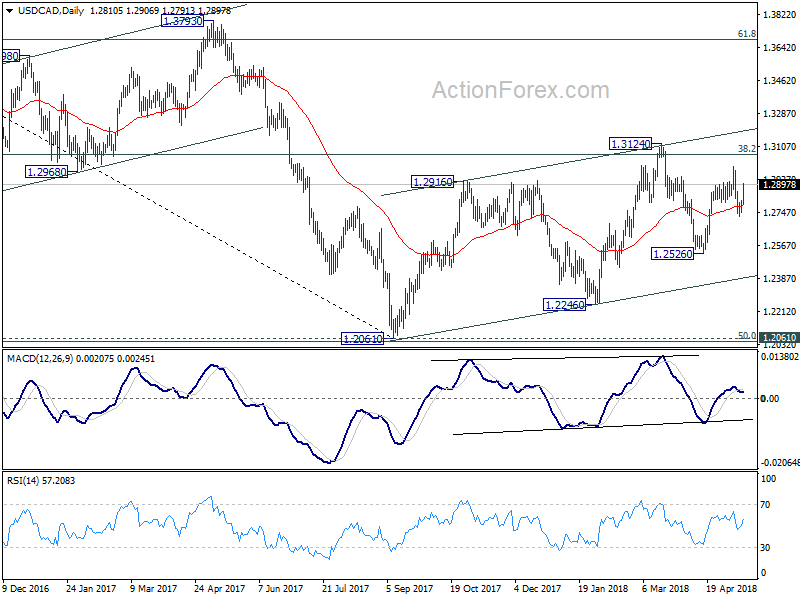

Technically, USD/JPY leads the way with 110.02 short term top broken. Such development is consistent with yield driven Dollar rally. Rise from March low at 104.62 has resumed for 61.8% retracement of 114.73 to 104.62 at 110.86 next. USD/CAD's breach of 1.2859 minor resistance suggests that pull back from 1.2996 has completed and further rise should be seen to retest this level.

For now, EUR/USD is holding above 1.1822 short term bottom. GBP/USD above 1.3459 short term bottom as the data release from European session provided little inspiration. These two levels will be watched closely today. Also, 1.0036 in USD/CHF will also be eyed.

German ZEW economic expectations deteriorated, UK wage growth met expectation

German ZEW Economic Sentiment was unchanged at -8.2 in May, in line with expectation. German Assessment of Current Situation dropped -0.5 to 87.4, above expectation of 85.2. Eurozone ZEW Economic Sentiment rose 0.5 to 2.4, above expectation of 2.0. Assessment of Current Situation dropped -1.6 to 56.1.

ZEW President Achim Wambach noted in the release that "the US decision to back out of the nuclear treaty with Iran and fears of a further escalation of the international trade conflict with the US, as well as a further rise of crude oil prices, have had an overall negative impact on economic expectations in Germany."

Also released from during European session, Eurozone GDP grew 0.4% qoq in Q1, unrevised from first estimate. Industrial production rose 0.5% mom in March. German GDP rose 0.3% qoq in Q1, below expectation of 0.4% qoq. Swiss PPI accelerated to 2.7% yoy in April, but miss expectation of 3.0% yoy.

UK unemployment stayed unchanged at 4.2% in March, at the lowest level since 1975. Average weekly earnings rose 2.6% 3moy including bonus, met expectations. Claimant count rose 31.2k in April versus expectation of 13.3k. Sterling's reaction to the data was muted.

IMF forecasts slower Eurozone growth in 2018, 2019. Urges fiscal reforms

IMF forecasts Eurozone growth to slow to 2.3% this year, from 2017's 2.4%, and drop further to 2.0% in 2019. IMF noted that "with economic prospects continuing to improve in the short term but medium-term prospects less bright, policymakers should seize the moment to rebuild room for fiscal manoeuvre and push forward with reforms to boost growth potential"

And it pointed out that "policymakers should strive to bring fiscal deficits within range of balance over the next few years.:" With that " automatic stabilizers and fiscal stimulus can be deployed again, should downside risks materialize."

BoJ Kuroda: "Absolutely no plan" to raise yield target

BoJ Governor Kuroda told the parliament today that there is "absolutely no plan" to raise the yield target under the Yield Curve Control for now, as inflation is still distant from 2%. He also explained that removing the time frame to meet the 2% inflation target is not necessarily related to the side effect of monetary policy on bank profits.

Regarding YCC, Kuroda said bond purchases are more sustainable under the framework, as the central bank has more flexibility. And, it's be able to maintain long term year near 0% with smooth operations in JGB purchases.

RBA minutes reiterated no strong case for near term hike

RBA May meeting minutes reiterated that central bank's stance that it's not in rush to lift interest rates. The minuted noted that "stronger growth was expected over the following couple of years, which could reduce spare capacity in the economy and lead to a further gradual decline in the unemployment rate." But, "the increase in wages growth and inflation was expected to be gradual however because spare capacity in the economy was expected to be reduced only slowly." And, "as progress in lowering unemployment and having inflation return to the midpoint of the target range was expected to be gradual, members also agreed that there was not a strong case for a near-term adjustment in monetary policy."

RBA Debelle: 2% is the focal point for wage outcomes now

RBA Deputy Governor Guy Debelle delivered a speech titled "The Outlook for the Australian Economy" at the CFO Forum in Sydney today, where he talked about wages. He noted that "the experience of other countries with labour markets closer to full capacity than Australia's is that wages growth may remain lower than historical experience would suggest."

Currently in Australia "2% seems to have become the focal point for wage outcomes, compared with 3–4% in the past." Even so, ""there is a risk that it may take a lower unemployment rate than we currently expect to generate a sustained move higher than the 2% focal point evident in many wage outcomes today".

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.33; (P) 109.50; (R1) 109.82; More...

USD/JPY rises to as high as 110.29 so far and the strong break of 110.02 resistance confirms rally resumption. Intraday bias is back on the upside as rise from 104.62 should now target 61.8% retracement of 114.73 to 104.62 at 110.86 next. Firm break there will target medium term trend line resistance at 112.43. On the downside, below 109.14 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 55 day EMA (now at 108.30) holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA May Meeting Minutes | ||||

| 02:00 | CNY | Retail Sales Y/Y Apr | 9.40% | 10.00% | 10.10% | |

| 02:00 | CNY | Industrial Production Y/Y Apr | 7.00% | 6.40% | 6.00% | |

| 04:30 | JPY | Tertiary Industry Index M/M Mar | -0.30% | -0.20% | 0.00% | 0.10% |

| 06:00 | EUR | German GDP Q/Q Q1 P | 0.30% | 0.40% | 0.60% | |

| 07:15 | CHF | Producer & Import Prices M/M Apr | 0.40% | 0.30% | -0.20% | |

| 07:15 | CHF | Producer & Import Prices Y/Y Apr | 2.70% | 3.00% | 2.00% | |

| 08:30 | GBP | Jobless Claims Change Apr | 31.2K | 13.3K | 11.6K | 15.7K |

| 08:30 | GBP | Claimant Count Rate Apr | 2.50% | 2.40% | ||

| 08:30 | GBP | Average Weekly Earnings 3M/Y Mar | 2.60% | 2.60% | 2.80% | |

| 08:30 | GBP | ILO Unemployment Rate 3Mths Mar | 4.20% | 4.20% | 4.20% | |

| 09:00 | EUR | Eurozone Industrial Production M/M Mar | 0.50% | 0.70% | -0.80% | -0.90% |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.40% | 0.40% | 0.40% | |

| 09:00 | EUR | German ZEW Economic Sentiment May | -8.2 | -8.2 | -8.2 | |

| 09:00 | EUR | German ZEW Current Situation May | 87.4 | 85.2 | 87.9 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment May | 2.4 | 2 | 1.9 | |

| 12:30 | USD | Empire State Manufacturing May | 20.1 | 15 | 15.8 | |

| 12:30 | USD | Retail Sales Advance M/M Apr | 0.30% | 0.30% | 0.60% | |

| 12:30 | USD | Retail Sales Ex Auto M/M Apr | 0.30% | 0.50% | 0.20% | |

| 14:00 | USD | Business Inventories Mar | 0.10% | 0.60% | ||

| 14:00 | USD | NAHB Housing Market Index May | 70 | 69 | ||

| 20:00 | USD | Net Long-term TIC Flows Mar | 49.0B |

USD ignores retail sales, surges as 10 year yield hit highest since 2011

US retail sales rose 0.3% mom in April, in line with expectation. Ex-auto sales rose 0.3% mom, below expectation of 0.5% mom.

Empire state manufacturing index rose to 20.1, up from 15.8 and beat expectation of 15.0.

Dollar pays little attention to the data release. Instead, it's following treasury yields higher. 10 year yield reaches as high as 3.045 so far. It has now breached key resistance of 2013 high at 3.036, hitting highest since 2011.

Into US session: Dollar back in form, yields watched

Dollar surges broadly as markets are entering into US session. AUD is trading as the weakest. US treasury yield will be a focus today, on whether 10 year yield could stay above 3% level and challenge 3.035 high.

In particular, USD/JPY breaks through 110.02 resistance to resume recent rally from March low at 104.62. More importantly, it's holding well within near term rising channel. Next target is 61.8% retracement of 114.73 to 104.62 at 110.86.

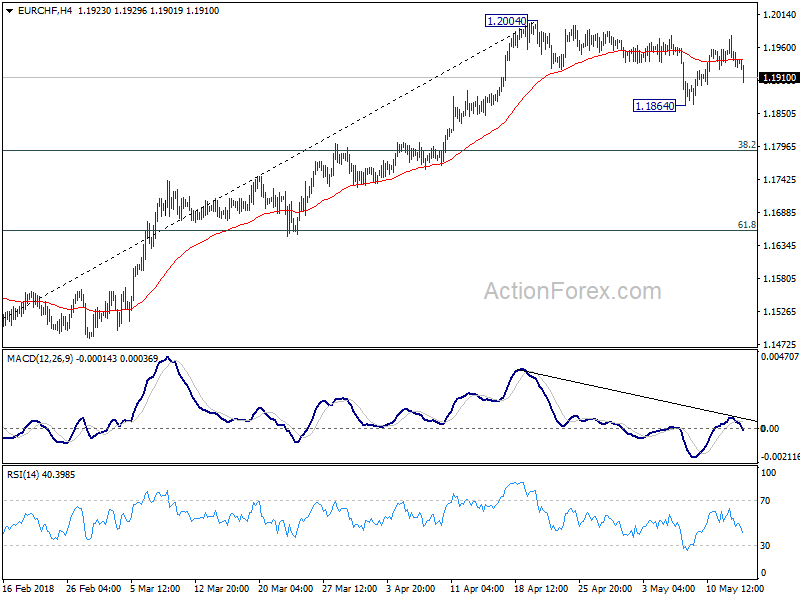

On development to watch is the sharp fall in EUR/CHF. The consolidation pattern from 1.2004 is set to extend with another falling leg, likely through 1.1864. That could give EUR extra pressure against USD, JPY and GBP.