Sample Category Title

Euro Unchanged As German, Eurozone GDP Meet Expectations

EUR/USD is almost unchanged in the Tuesday session. Currently, the pair is trading at 1.1927, unchanged on the day. On the release front, German Preliminary GDP came in at 0.3%, close to the forecast of 0.4%. Eurozone GDP came in at 0.4%, matching the forecast. German ZEW Economic Sentiment came in at -8.2, weaker than the estimate of -8.0 points. Eurozone ZEW Economic Sentiment was stronger, improving to 2.4 points. This beat the estimate of 2.0 points. In the US, the focus will be on consumer spending indicators. Retail Sales is expected to dip to 0.4%, while Core Retail Sales is expected to post a gain of 0.5%.

First-quarter eurozone and German GDP data were within expectations, but investors should not become too sanguine, as the numbers pointed to a slowdown in the eurozone economy. Both Germany and the eurozone posted gains of 0.6% in the fourth quarter of 2017. Will economic conditions improve in Q2? Institutional analysts don’t seem optimistic, according to the well-respected ZEW Economic Sentiment surveys. The German indicator posted a sharp drop of -8.2 for a second straight month – the first declines since July 2016. The eurozone release improved to 2.4, but low reading certainly doesn’t show much optimism. The markets are bracing for more soft numbers on Wednesday, as Germany and eurozone release CPI reports. If these indicators miss their estimates, the euro could lose ground.

With the U.S economy performing well in 2018, the U.S consumer is feeling very optimistic. On Friday, the UoM Consumer Sentiment improved to 98.8 in April, beating the estimate of 98.4 points. The U.S labor market is at near or full employment, which has resulted in a slowdown in job growth due to a shortage of skilled workers. This was underscored last week, as JOLTS Job Openings climbed to a record 6.6 million. At the same time, inflation levels remain low, as the Federal Reserve target of 2 percent remains elusive. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. Inflation levels will be an important factor for the Fed in its monetary policy projection, which remains at two more hikes in 2018. The odds of a rate hike at the June hike stands close to 100%.

WTI OIL – Bullish Tone Is Boosted By Geopolitical Tensions And Reduced Production

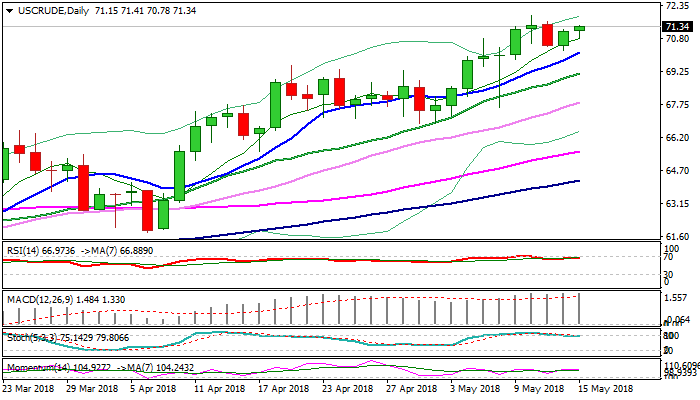

WTI oil price returned above $71 on Tuesday and probes above Monday’s high at $71.23, posted after strong rally from two-day correction low at $70.25.

Fresh bullish sentiment on escalation of tensions in the Middle East and stronger than required production cut from OPEC, keeps oil prices supported as recovery retraced over 61.8% of $71.86/$70.25 pullback.

Scope exists for retest of recent 3 ½ year high at $71.86, break of which would expose $73.21 (14 Nov 2014 low) and $76.35 (Fibo 61.8% of $107.45/$26.04 fall).

Rising 10SMA continues to track the advance and offer solid support at $70.15.

Res: 71.61, 71.86, 72.00, 72.48

Sup: 70.78, 70.15, 70.00, 69.54

Q1 Euro Area Growth Decelerates As Projected

Notes/Observations

Asia:

- EU Q1 GDP growth decelerated (as expected), the key questions remains was the effect temporary??? (Beats: Norway, Hungary; Poland Misses: Germany, Netherlands, Portugal Romania, Czech Republic; in-line: Euro Zone)

- UK employment picture improved but dealers noted that strong wage growth remained elusive. Earnings (ex-bonus) at its fastest pace since Aug 2015

- Germany May ZEW Current Situation beat expectations (87.4 v 85.5e)

Asia:

- RBA May Minutes: members agreed that it was more likely that the next move in the cash rate would be up, rather than down

- China Apr Industrial Production Y/Y: 7.0% v 6.4%e

- China Apr Retail Sales Y/Y: 9.7% v 9.9%e

- China Stats Bureau: US/China trade frictions yet to have an impact on China economy; economy maintaining steady and improving trend in April; steady economic growth sets a good foundation for achieving FY growth target;

Europe:

- ECB's Coeure (France): divergence between our key policy rates and market rates could become more important in the future once policy rates begin to normalize

- Italy President Mattarella said gave more time to 5-Star, League to reach a deal with no deadline given. No intention of hampering the formation of a Govt that can last a full term of office

- Northern League plans to hold informal referendum on May 19-20 for members to vote on eventual govt deal with Five Star Party

- EU Barnier: cannot underestimate the importance of June Leader summit as the key date. Reiterated that could be no transition without a Brexit deal

- EU Commission is considering invoking a 19th century law to prohibit European companies from submitting to US sanctions, in the event they are imposed as a result of its withdrawal from the Iranian nuclear pact - German press

Americas:

- US Ambassador to China Branstad: China and US still very far apart on trade; President Trump wants 'dramatic' increase in farm exports to China. US wanted to see timetable and have things happen sooner or later. China agreed to do a lot of opening up when they joined the WTO, but a lot of promises were not fulfilled.

- Fed Vice Chair nominee Richard Clarida releases testimony ahead of May 15 Senate hearing. Seek to preserve financial resilience, will take balanced approach to monetary policy and fully supported the Fed's dual mandate

Economic Data:

- (DE) Germany Q1 Preliminary GDP Q/Q: 0.3% v 0.4%e; Y/Y: 2.3% v 2.4%e, GDP NSA Y/Y: 1.6% v 1.7%e v 2.3% prior

- (FI) Finland Mar GDP Indicator WDA Y/Y: 3.1% v 2.4% prior

- (FI) Finland Mar Current Account: -€0.1B v +€0.3B prior

- (DK) Denmark Q1 GDP Indicator Q/Q: 0.3% v 0.9% prior

- (DK) Denmark Apr PPI M/M: +1.5% v -0.4% prior; Y/Y: 2.8% v 1.7% prior

- (RO) Romania Q1 Advance GDP Q/Q: 0.0% v 0.8%e; Y/Y: 4.0% v 5.5%e

- (NO) Norway Q1 GDP Q/Q: +0.6 v -0.3% prior; GDP Mainland Q/Q: 0.6% v 0.5%e

- (NO) Norway Apr Trade Balance (NOK): 19.4B v 13.8B prior

- (FR) France Apr Final CPI M/M: 0.2% v 0.1%e; Y/Y: 1.6% v 1.6%e; CPI (ex-tobacco): 102.59 v 102.56e

- (FR) France Apr Final CPI EU Harmonized M/M: 0.2% v 0.1%e; Y/Y: 1.8% v 1.8%e

- (FR) France Q1 Preliminary Private Sector Payrolls Q/Q: 0.3% v 0.4%e; Wages Q/Q: 0.7% v 0.2% prior

- (CZ) Czech Q1 Advance GDP Q/Q: 0.5% v 0.7%e; Y/Y: 4.5% v 4.8%e

- (HU) Hungary Q1 Preliminary GDP Q/Q: 1.2% v 1.0%e; Y/Y: 4.4% v 4.2%e

- (TR) Turkey Feb Unemployment Rate: 10.6% v 10.8%e

- (CH) Swiss Apr Producer & Import Prices M/M: +0.4% v -0.2% prior; Y/Y: 2.7% v 2.0% prior

- (NL) Netherlands Q1 Preliminary GDP Q/Q: 0.5% v 0.6%e; Y/Y: 2.8% v 3.4%e

- (NL) Netherlands Mar Trade Balance: €5.3B v €4.4B prior

- (TR) Turkey Apr Central Gov't Budget Balance (TRY): -2.8B v -20.2B prior

- (PL) Poland Apr Final CPI M/M: 0.5% v 0.5% prelim; Y/Y: 1.6% v 1.6% prelim

- (PL) Poland Q1 Preliminary GDP Q/Q: 1.6% v 1.3%e; Y/Y: 5.1% v 4.8%e

- (UK) Apr Jobless Claims Change: +31.2K v 15.7K prior; Claimant Count Rate: 2.5% v 2.4% prior

- (UK) Mar Average Weekly Earnings 3M/Y: 2.6% v 2.6%e; Weekly Earnings (ex-bonus) 3M/Y: 2.9% v 2.9%e

- (UK) Mar ILO Unemployment Rate: 4.2% v 4.2%e (matched the lowest rate since 1975); Employment Change: +197K v +129Ke

- (PT) Portugal Q1 Preliminary GDP Q/Q: 0.4% v 0.6%e; Y/Y: 2.1% v 2.4% prior

- (IT) Italy Mar General Government Debt: €2.302T v €2.286T prior

- (EU) Euro Zone Q1 Preliminary GDP (2nd reading) Q/Q: 0.4% v 0.4%e; Y/Y: 2.5% v 2.5%e

- (EU) Euro Zone Mar Industrial Production M/M: 0.5% v 0.7%e; Y/Y: 3.0% v 3.7%e

- (DE) Germany May ZEW Current Situation Survey: 87.4 v 85.2e; Expectations Survey: -8.2 v -8.2e

- (EU) Euro Zone May ZEW Expectations Survey: 2.4 v 1.9 prior

- (CY) Cyprus Q1 Preliminary GDP Q/Q: 0.8% v 1.1% prior; Y/Y: 3.8% v 3.9% prior

Fixed Income Issuance:

- (EU) ESM opened its book to sell 15-year bonds; guidance seen -15bps to mid-swaps

- (UK) DMO opened its book to sell Oct 2071 Gilt; guidance seen -0.5 bps to 3.5% 2068 gilts. Order book over £33B

- (ZA) South Africa to sell USD-denominated 2030 and 2048 bonds

- (ID) Indonesia sold total IDR4.06T vs. IDR4.0T indicated in 6-month Islamic Bills, 2-year, 4-year, 7-year and 15-year Project-based Sukuk (PBS)

- (CH) Switzerland sold CHF378.7M in 6-month Bills; Yield: -0.821% v -0.880% prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 flat at 392.3, FTSE +0.2% at 7725.4, DAX -0.2% at 12955, CAC-40 +0.1% at 5545, IBEX-35 -0.3% at 10229, FTSE MIB +0.3% at 24305, SMI flat at 8999, S&P 500 Futures -0.3%]

- Market Focal Points/Key Themes: European Indices trade little changed, following a swath of earnings this morning and weaker US futures. In the UK shares of Easyjet trades higher after losses narrowed, with Telecom giant Vodafone trading lower after results and the naming of a new CEO. In Germany Merck, ThyssenKrupp , Metro, Carl Zeiss all trade lower following earnings, with Commerzbank trading higher. Iliad falls the most in almost 12 years on weaker Fixed line business, and Sales which missed consensus, with Credit Agricole trading higher despite a miss in earnings. Pandora falls sharply after a miss on the top and bottom line. Looking ahead notable earners include Home Depot, AZZ and Virtusa.

Movers

- Consumer Discretionary [ Easyjet [EZJ.UK] +2.8% (Earnings), Pandora [PNDORA.DK] -8.5% (Earnings), Metro Ag [B4B.DE] -3.2% (Earnings), Premier Foods [PFD.UK] +2.0% (Earnings)]

- Consumer Staples [ Carl Zeiss [AFX.DE] -2.4% (Earnings)

- Industrials [Bauer [B5A+2.6% (Earnings)]

- Materials [ThyssenKrupp [TKA.DE] -5.0% (Earnings)

- Healthcare [Merck [MRK.DE] -5.2% (Earnings)]

- Financials [ Credit Agricole [ACA.FR] +1.6% (Earnings), Commerzbank [CBK.DE] +3.2% (Earnings)]

- Telecoms [Vodafone [VOD.UK] -3.9% (Earnings), Iliad [ILD.FR] -17% (Earnings)]

- Energy [ RWE [RWE.DE] -1.3% (Earnings) ]

Speakers

- Sweden Central Bank (Riksbank) af Jochnick: Important that inflation expectations stabilized around 2% to begin raising rates. Too early to begin raising interest rates at this time. Underlying inflation was somewhat weak and reiterated that had no target for SEK currency (Krone)

- German Fin Min Scholz: Budget was the basis for future growth. Saw investment increasing year after year

- Upcoming EU Leader Summit said to discuss options available to shield its economic interest in Iran in the aftermath of the US withdrawal from the Iranian nuclear accord

- German ZEW Economists noted that US withdrawal from Iran nuclear agreement, concerns over trade, rising oil prices all hwere aving negative impact on expectations

- Norway Fin Min Jensen: Q1 GDP data supported its 2018 forecasts

- Norway Govt revised budget projections which maintained growth outlook for both 2018 and 2019. Maintained 2018 non-oil GDP growth at 2.5% and 2019 non-oil GDP growth at 2.6%

- Turkey President Erdogan: Would take more responsibility for monetary policy if he won in the upcoming June elections. To tighten grip on economy and rate policy

- German Economic Ministry reiterated view that the domestic economic upturn remained intact

- BOJ Gov Kuroda testified in parliament and reiterated view that there were many uncertainties on inflation, CPI remained distant from target. Not considering the removal of the 10-year yield control target at this time; but won't stick with it at all costs

Currencies

- USD was steady as market participants focused on yields. The US 10-year yield moved back above the 3% level with the curve steepening thus giving the greenback some support.

- The EUR/USD hovered near 4-month lows as various European Q1 GDP data confirmed the anticipated deceleration in growth.

- GBP/USD was basically steady in the wake of mixed economic data. The main focus was on wage data with ex-bonus earnings in-line at 2.9% for its fastest pace since Aug 2015 and registering a small improvement from month ago levels. The GBP currency did manage to trims losses in the aftermath of the data release. Overall the employment picture improved but dealers noted that strong wage growth remained elusive

- USD/JPY against briefly tested the 110 level for the 2nd time in a week and again failed to muster enough momentum for any sustained break above the key psychological level.

- The TRY currency (Lira) slumped another 0.4% to record low levels after President Erdogan stated he would take more responsibility for monetary policy if he won the elections next month

Fixed Income

- Bund Futures trade 20 ticks lower at 158.07 following the move lower with Treasuries. Upside targets 159.75, while a return lower targets the 157.25 level.

- Gilt futures trade at 121.75 lower by 9 ticks after UK weekly earnings comes in line with expectation. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Tuesday’s liquidity report showed Monday's excess liquidity stayed steady at €1.908T. Use of the marginal lending facility decreased from €59M to €44M.

- Corporate issuance saw 10 issuers raise $17.4B in the primary market

Looking Ahead

- (RU) Russia PM Medvedev to present new Cabinet

- (CN) China's Vice Premier (and top economic adviser to President Xi) Liu in Washington DC

- (SE) Sweden Central Bank (Riksbank) Dep Gov Skingsley speaks in Malmo

- (UR) Ukraine Q1 Preliminary GDP Q/Q: No est v 0.5% prior; Y/Y: 2.5%e v 2.2% prior

- 05:30 (ZA) South South Q1 Unemployment Rate: 27.4%e v 26.7% prior

- 05.30 (UK) Weekly John Lewis LFL sales data

- 05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

- 05:30 (EU) ECB allotment in 7-day Main Financing Tender

- 06:00 (TR) Turkey to sell 2019 and 2023 bonds

- 06:45 (US) Daily Libor Fixing

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:00 (BR) Brazil Mar IBGE Services Sector Volume Y/Y: No est v -2.2% prior

- 08:00 (IS) Iceland Apr Unemployment Rate: No est v 2.4% prior

- 08:00 (US) Fed’s Kaplan (dove, non-voter) on outlook

- 08:00 (RU) Russia announces weekly OFZ bond auction (held on Wed)

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) May Empire Manufacturing: 15.0e v 15.8 prior

- 08:30 (US) Apr Advance Retail Sales M/M: 0.4%e v 0.6% prior; Retail Sales Ex Auto M/M: 0.5%e v 0.2% prior, Retail Sales Ex Auto/Gas: 0.4%e v 0.3% prior; Retail Sales Control Group (used for GDP calc): 0.4%e v 0.4% prior

- 08:55 (US) Weekly Redbook Sales

- 09:00 (EU) Weekly ECB Forex Reserves:

- 09:00 (CA) Canada Apr Existing Home Sales M/M: No est v 1.3% prior

- 09:30 (NZ) Fonterra Global Dairy Trade Auction: Dairy Trade price index

- 10:00 (US) Mar Business Inventories: 0.2%e v 0.6% prior

- 10:00 (US) May NAHB Housing Market Index: 70e v 69 prior

- 10:00 (US) Fed nominees Clarida and Bowman testify before Senate

- 10:30 (CA) Canada to sell 3-month, 6-month and 12-month bills

- 11:30 (IL) Israel Apr CPI M/M: 0.4%e v 0.3% prior; Y/Y: 0.4%e v 0.2% prior

- 11:30 (US) Treasury to sell 4-Week Bills

- 12:00 (CO) Colombia Q1 GDP Q/Q: No est v 0.3% prior; Y/Y: 2.2%e v 1.6% prior

- 13:00 (US) Fed's Williams (moderate, voter)

- 15:00 (CO) Colombia Mar Economic Activity Index (Monthly GDP) Y/Y: No est v 2.4% prior

- 15:00 (AR) Argentina Apr National CPI M/M: No est v 2.3% prior; Y/Y: No est v 25.4% prior

- 16:00 (US) Mar Total Net TIC Flows: No est v $44.7B prior; Net Long-term TIC Flows: No est v $49.0B prior

- 16:30 (US) Weekly API Oil Inventories

USD Struggles To Extent Rally

USD dead cat bounce

The US dollar reversed losses yesterday amid heightening geopolitical tensions in the Middle East. Indeed, after the Syrian situation and the Iran nuclear deal, now we got the Gaza killings following the official opening of the US embassy in Jerusalem. After falling as low as 92.24 Monday afternoon, the dollar index surged 0.60% to 92.80. The rise of the index was mostly driven by the debasement of the Japanese yen (-0.50%), the Canadian dollar (-0.20%) and the euro (-0.18%).

However, it seems the rally is overstretched as buyers are shying away. April’s retail sales are due for release today with the headline gauge expected to ease to 0.3%m/m from 0.6% in March. However, when excluding auto sales, the measure should have accelerate with median forecast of 0.5%m/m compared to 0.2% in the previous month. We think that the risk is mostly on the downside for the greenback today as a disappointing read could re-fuel worries about the US growth outlook.

Overall, we maintain our bearish view on the buck as we estimate that the recent dollar appreciation is widely overdone.

GBP overly bearish

Sterling has been dragged down by the changing BoE rhetoric and repricing of the timing tightening cycle. Since February weak economic data ended the all-but-sure May rate hike. Yet, expectations of monetary policy strategy has become worryingly short sighted, data dependent in our view. Today mixed labor market data, growth rising 2.9% weekly earning x-bonus yet softer 2.6% average weekly earnings will spark debate. Data indicate only now responding to soft patch. Give the sharp decline in sterling we suspect that positive news will have a larger effect on pricing then negative reads. In addition, evidence of inflation will more likely trigger expectations of higher interest rates then sluggish growth. A widely expected at recent policy meeting, the MPC left the Bank Rate unchanged at 0.5% with Committee voting 7-2.

The BoE has acknowledged the recent weakness (which is consistent with broader global slowdown) in growth and inflation data (waning FX impact) but the door remains open for August hike. We understand the MPC comment is that express concern over the strength of the economy and see the bar for future rate hikes as high. However, dovishness is overpriced. As marginal recovery, bounce takes place markets will quickly reload on GBP long (German ZEW current situation rose to 87.4). In the longer term, much depends on Brexit and direction of free trade negotiations. Our based scenario is for EU-UK friendly outcome. We are positioned for a positive swing in oversold GBP on either good news on Brexit or pickup in domestic data.

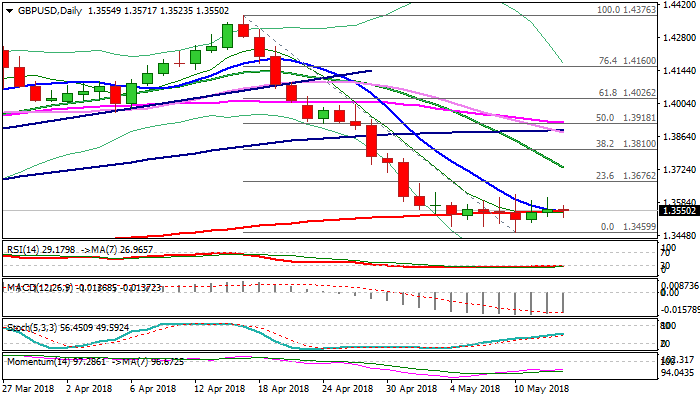

GBPUSD Slightly Higher After Mixed UK Data But Remains Within Larger Range

Cable bounced some 30-pips from session low at 1.3523 after UK data and looks to catch fresh bid.

UK average earnings missed forecast (2.6% in Mar vs 2.7% f/c and 2.8% previous) and jobless claims unexpectedly jumped to 31.2K in Apr vs 13.3K f/c and downward revised Mar figure at 15.7, but negative impact was partially offset by better than expected employment data which jumped to 197K in Q1, beating forecast at 129.

Sentiment for BoE rate hike in August remains at 50/50 as today’s releases provided little help to improve the outlook.

Pound remains bid after releases, but key barriers at 1.3608/17 are still far.

Near-term action is also weighed by thick falling 4-hr cloud and formation of 10/200SMA bear-cross, which could keep the downside at risk.

Stronger direction signal could be expected on break of either boundary of near-term range.

Res: 1.3571, 1.3617, 1.3676, 1.3733

Sup: 1.3523, 1.3500, 1.3484, 1.3460

US Futures Pare Gains Ahead Of Retail Sales Data

- US Equities Looking Less Vulnerable After Recent Breakouts;

- Retail Sales Expected to Rebound After Tough Winter;

- UK Jobs Data in Line as Wages Rise Most Since 2015.

US equity markets have been on a good run of late but are poised to open slightly lower on Tuesday, paring the steady gains achieved over the last couple of weeks.

This comes after the Dow and S&P 500 both surpassed the previous peak which came almost a month earlier in what could be a symbolic indication that the worst of this particular correction is now behind us. From a technical standpoint, the failure to make a new low a couple of weeks ago before now making a new high is encouraging as a signals the end of a downtrend.

There's a number of data releases that will grab traders' attention today and could determine whether we see an early rebound in stock markets. The most notable of these is the retail sales data for April, which is expected to be relatively good for a second consecutive months following a few poor numbers that were a little worrying. Core retail sales are also expected to be good, rising by 0.5% compared to March.

The UK labour market figures offered little support to the struggling pound this morning, which continued to hover around four month lows against the dollar and look vulnerable to further declines. While unemployment remains at the lowest since 1975 and employment at the highest since records began, the numbers were all pretty much in line with expectations and was therefore priced in.

The potential for upside would have likely come from the earnings data but even this was in line, although excluding bonuses, they did rise to 2.9% which is the highest since August 2015. Still, with inflation still high, real wages were unchanged once bonuses were taken into consideration which is likely to continue to weigh on the economy and confuse matters for the Bank of England, which is being heavily criticised after not raising rates last week.

Clearly traders don't view the increase in wages as increasing the chances of a rate hike from current expectations. It could well be that traders view the recent wage data as being a temporary response to last year's increase in the cost of living due to higher inflation as opposed to something more sustainable or that the recent improvement is being flattered by the year on year comparison after a dip 12 months ago.

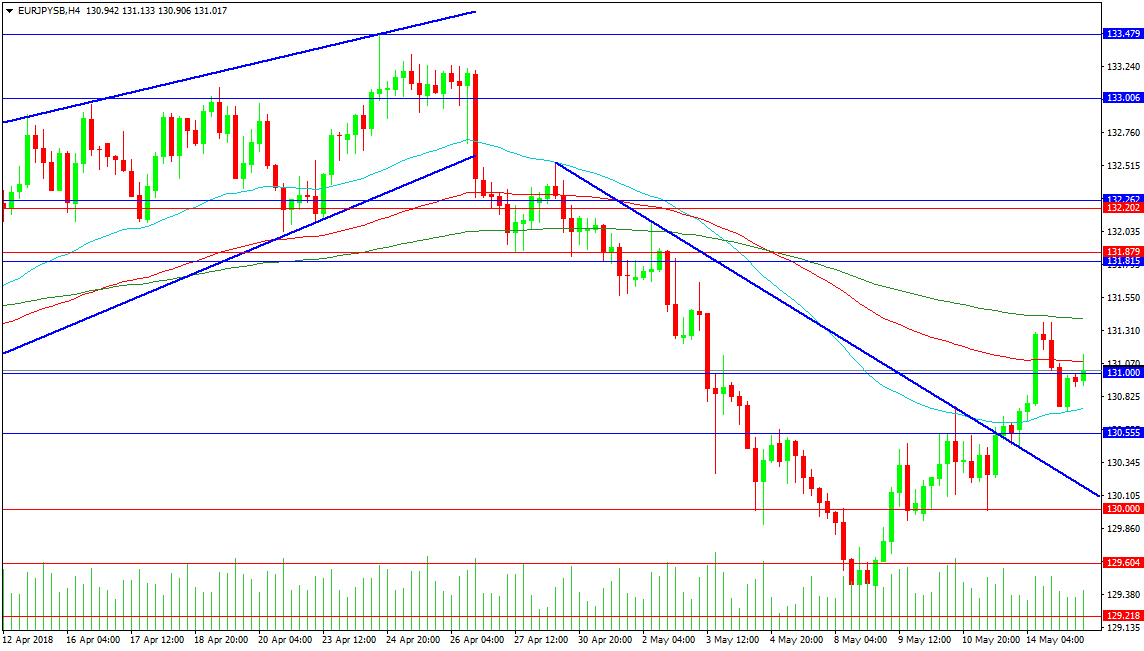

Forex Analysis: EURJPY And GER 30

The EURJPY pair is retracing higher following its rejection of the 133.479 level in late April and its sell-off to 129.218. The breakout higher came on the 11th of May, with the move above the blue trend line, but traders who bought the retest of 130.000 that morning have also done very well. The price is now consolidating between its moving averages on the 4-hour time frame, with the 50-period acting as support at 130.737 and the 130.555 as added support below. The trend line is located at 130.105 today, just above the 130.000 level. A loss of this area could suggest a resumption of the move lower to target 1.29604 and 1.29218, with 1.29000 in extension.

Resistance comes at the 200-period MA at 131.400, followed by a strongly resistive area between 131.815 and 132.262. This area was where price consolidated recently and a break higher could see a rapid move to 133.000 and the 1.33479 level above.

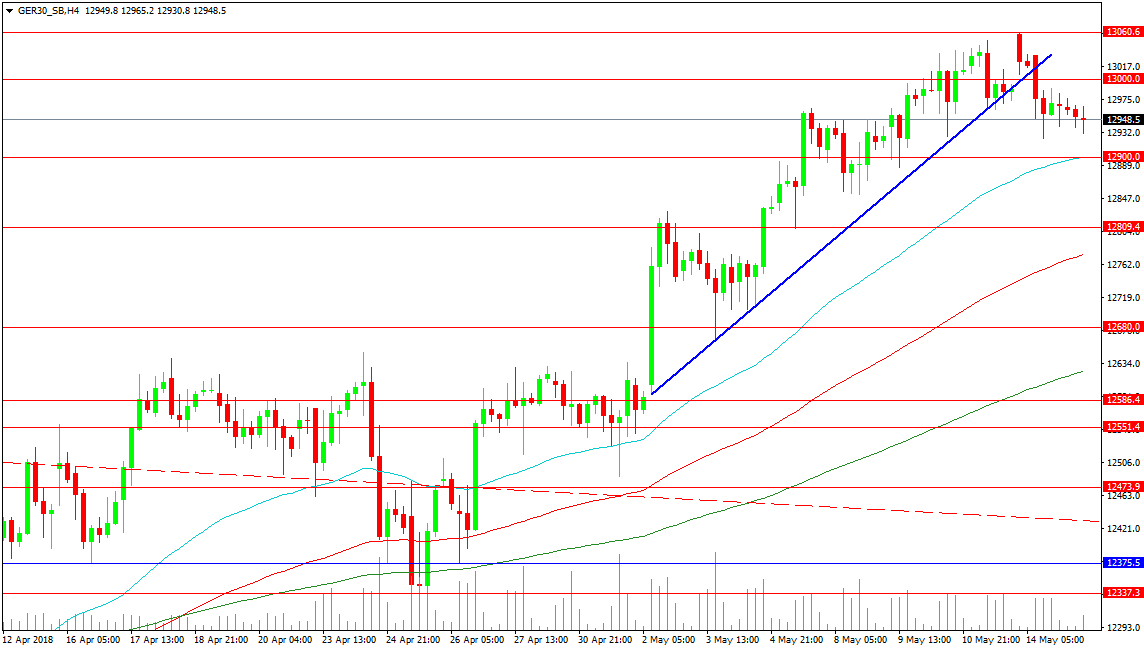

GER 30 Index

The German index has put together a rally despite plenty of headwinds to reach for the 13000.00 area during the month of May. The breakout from the red trend line was very slow and used much of the energy needed for the drive higher afterwards. The rally from the resistance level of 12650.00 managed to add approximately 400 pips. The current retracement can be seen as small, but it is too early to predict what the outcome will be. A push higher looks to build on the uptrend and targets 13200.00, 13350.00 and 136000.00 in extension.

Support may need to be tested in order to lay stronger foundations for the move higher. The 12900.00 level is playing host to the 50-period MA today, with the 12800.00 level used as support recently. The 100-period MA at 12775.00 could find buyers but the zone from 12680.00 to the 200-period MA at 12624.20 may generate more interest.

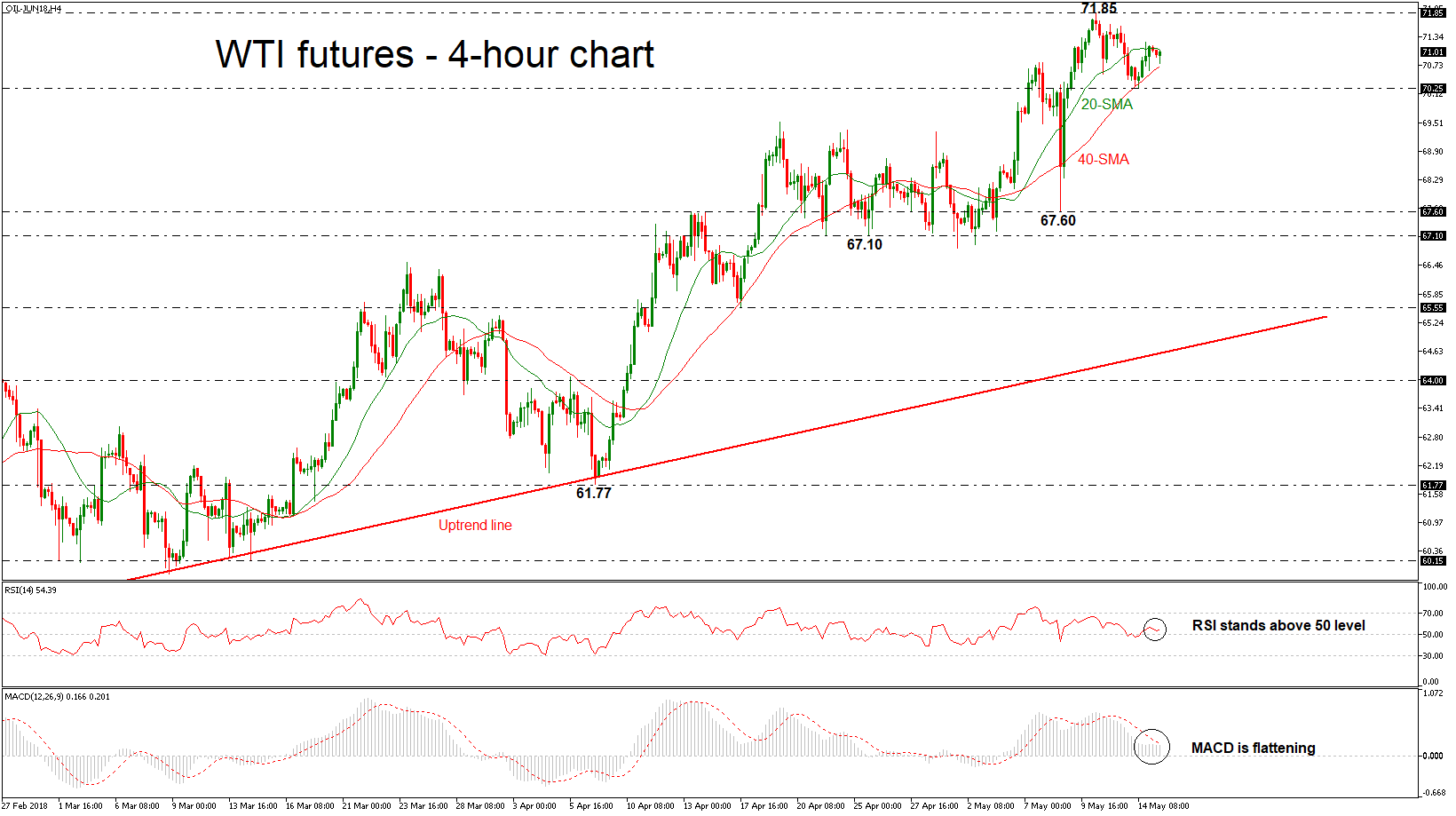

WTI Futures Ease Below 3½-Year High, Capped By 20-SMA

West Texas Intermediate (WTI) crude oil futures have eased after the pullback on the fresh three-and-a-half-year high of 71.85 reached last Thursday. The price is being capped by the 20-simple moving average (SMA) but remains above the 40-SMA in the 4-hour chart. Short-term technical indicators are endorsing the scenario for a potential bearish retracement.

Looking at momentum indicators, the RSI stands slightly above the 50 level with weak momentum, while the MACD oscillator is flattening in the positive territory below its trigger line, suggesting that a negative movement is near.

In the event of a slip below the 40-SMA, this would open the door for the immediate support level of 70.25. A successful close below this level could see a re-test of the previous lows of 67.60, while in case of steeper declines the oil could breach this trough, diving to the 67.10 region.

On the flip side, a move to the upside again could touch the aforementioned three-and-a-half-year high but should the market increase positive momentum above this area, the 73.30 could be the next major focus, taken from the low on November 2014. A strong barrier, though, could be found at the 75.00 handle, identified from the September 2011 low. As a side note, the psychological levels of 71.00, 72.00, 73.00, 74.00 could act as significant obstacles for the bulls as well.

Overall, the crude oil started a bearish correction confirmed by the technical indicators in the near-term, however, the main trend is still bullish in the medium term.

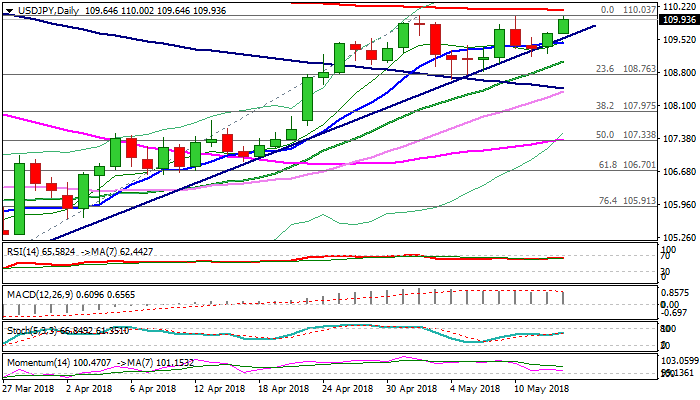

USDJPY Attacks 110 Barrier For The Third Time

The pair attacked 110 barrier again on Tuesday, but so far unable to break higher. Bullish bias remains in play as bull-trendline off 104.63 low continues to track advance and contained corrective dips, with daily MA’s in bullish configuration.

The notion is partially offset by weakening momentum studies, which make more difficulties for bulls to eventually break through key barriers at 110.00/15 (psychological resistance / 200SMA).

Clear break here is needed to generate strong signal for bullish continuation and expose barriers at 110.48 (02 Feb high) and 110.87 (Fibo 61.8% of 114.73/104.63 fall).

Repeated failure at 110 barrier would signal extended consolidation while the price holds above pivotal supports t 109.58 (trendline) and 109.43 (10SMA).

Break here would weaken near-term structure and risk further easing towards 109.05 (rising 20SMA) and key support at 108.64 (04 May trough).

Res: 110.00, 110.15, 110.48, 110.87

Sup: 109.58, 109.43, 109.05, 108.82

Bitcoin Continued Weakness

Bitcoin rise started in mid-April pauses, the pair is decreasing, trading below 9000 and heading along 8610. Bitcoin bearish pattern started in March 2018 strengthens. The pair is contained between hourly support and resistance given at 6306 (13/11/2017 low) and 10232 (01/02/2018 high). The technical structure suggests further short-term decrease.

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 7'000 - 12'000 in 2018. Bitcoin is trading slightly above its 200 DMA (8500 range).