Sample Category Title

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

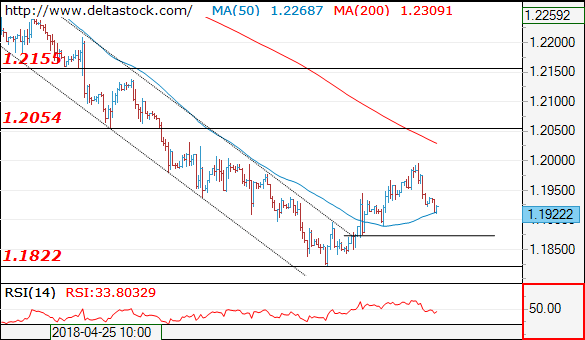

EUR/USD

Current level - 1.1922

The reversal below 1.2000 marks the finale of the first leg after 1.1820 and I expect 1.1870 to limit the downside, for another upswing, towards 1.2060 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2000 | 1.2060 | 1.1870 | 1.1840 |

| 1.2060 | 1.2160 | 1.1840 | 1.1720 |

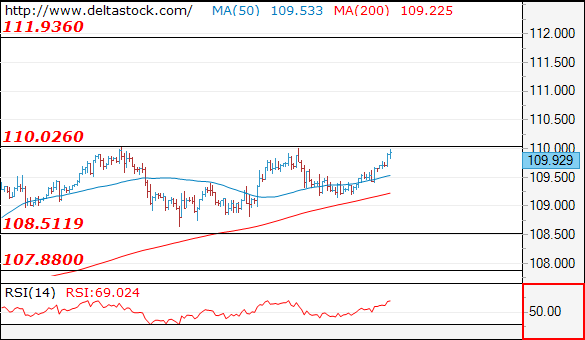

USD/JPY

USD/JPY

Current level - 109.92

The violation of 109.60 led to a new test of 110.00 area and an eventual break here will unleash a move towards 111.90. While 110.00 hurdle is intact, the outlook will be bearish, for a continuation of the consolidation pattern towards 108.50.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 110.00 | 110.20 | 108.50 | 107.90 |

| 110.20 | 111.90 | 108.50 | 104.60 |

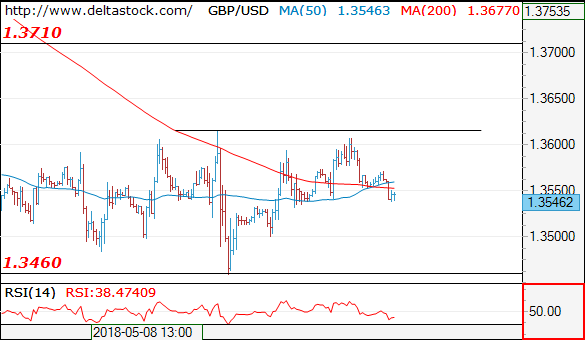

GBP/USD

Current level - 1.3546

The upmove since 1.3460 low is already over with yesterday's peak at 1.3607, so intraday allow a dip to 1.3500 area, before another leg upwards, to 1.3710. Minor intraday resistance lies at 1.3575.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3575 | 1.3990 | 1.3460 | 1.3460 |

| 1.3710 | 1.4100 | 1.3310 | 1.3310 |

History Repeats Itself – Argentina Seeks IMF Bailout

Failure to rescue currency slump despite aggressive rate hike has led Argentina to seek IMF bailout. Last week, it was reported by the government has asked for a flexible credit line worth $30B from the world lender. According to President Mauricio Macri, “this is going to allow us to strengthen our growth and development program” and “allow us to face the new global scenario and avoid a crisis like the ones we have faced before in our history”. In its statement released on May 14, the IMF noted that an informal meeting is scheduled on May 18 with Argentina regarding the access of the funding program.

Causes of Peso’s Weakness

The country’s central bank lifted the policy rate to 30%, from 27%, on April 27, followed by two more hikes on May 3 and May 4, sending the rate to 40% at present. Despite the aggressive moves, the recovery on peso (ARS) was muted. Closing at a record low of 24.9 per USD, ARS has dived -18% so far this month and down over -30% from December last year. The recent weakness in peso has been driven by a confluence of the following factors. Monetary policy divergence between the US and other economies has re-emerged as the theme since 2Q17. Solid US economic indicators have raised speculations the Fed might raise interest rates for four times this year. This comes in contrast with a less hawkish/ more dovish stance of other central banks (e.g. BOE, BOC, ECB). The divergence has led to capital flow to the US from other countries, resulting in renewed strength in US dollar. the divergence was exacerbated by the mistaken monetary policy decisions made by the Argentinean central bank which cut the policy rate twice in January.

On the economic front, Argentina has been suffering from high Inflation which has stayed at elevated level of 25%, despite a significant decline from 40% in 2016. Record high current account deficit has reached nearly 5% of GDP and about 39% of the country’s total exports. The country has been financing much of its fiscal deficit (3.9% of GDP in 2017) with FX-denominated public debt, which has taken up around 65% of the total. While the government has pledged to trim the fiscal deficit to 2.7% of GDP this year, via a series of reforms including reduction in spending and tariff. The path could be challenging. Indeed, political pressure to change the utilities tariffs scheme earlier this month has already sent the government’s popularity to a record low since President Macri took office.

IMF Bailout: A 2001 Deja Vu

The current problem is reminiscent of Argentinean crisis in 2001/02 (peso was pegged to US back then), when depressing economic and financial conditions had led the Latin American country to seek funding from the IMF. The stringent austerity measures associated with the program have been criticized as a major cause of the downward spiral of Argentina’s depression. Eventually, Argentina the then-new President Rodriguez Saá announced the default on US$ 93B of the sovereign debt in December 2001. As much as four different presidents had tried to rule Argentina in that single month. Yet, none of them managed to remain in office. The economy contracted by -28% from 1998 to 2002.

The relation between the IMF and Argentina has been contentious since then. The crisis has revealed the fragility of the IMF’s economic solution. This is notoriously known as the Washington Consensus which prescribes the "standard" reform package to virtually all countries with economic and financial problems. The IMF, as well as the World Bank, usually fails to customize solutions specific to the country in question. We expect Argentina would secure bailout from the IMF, again with conditionality. We believe the government would have to implement more stringent fiscal consolidation than it has announced previously. While the pro-IMF camp suggests that an IMF program could help ensure discipline on fiscal consolidation, the market would remain cautious and volatility on emerging market currencies is expected.

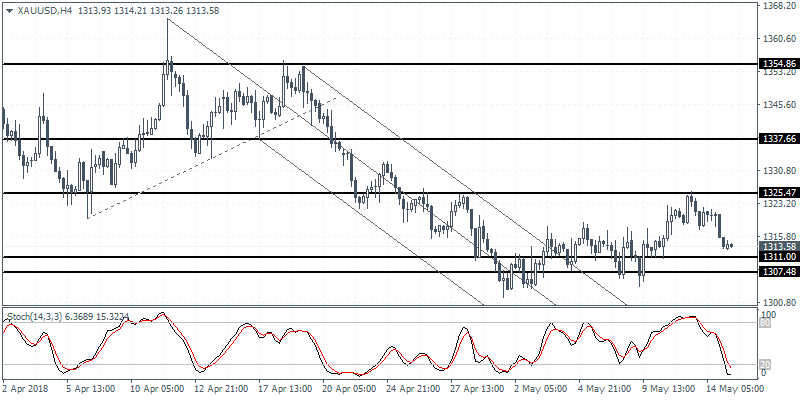

XAUUSD Intraday Analysis

XAUUSD (1313.58): Gold prices continued to drift lower after testing the upper resistance level of 1325 previously. We expect the sideways range to be maintained within 1325 resistance and 1311 level of support in the near term. The 4-hour Stochastics oscillator currently points to a hidden bullish divergence. This could mean that price action will likely test the lower support of 1311 ahead of another rebound in prices. Unless gold prices break out from the range, we expect this flat trading to continue.

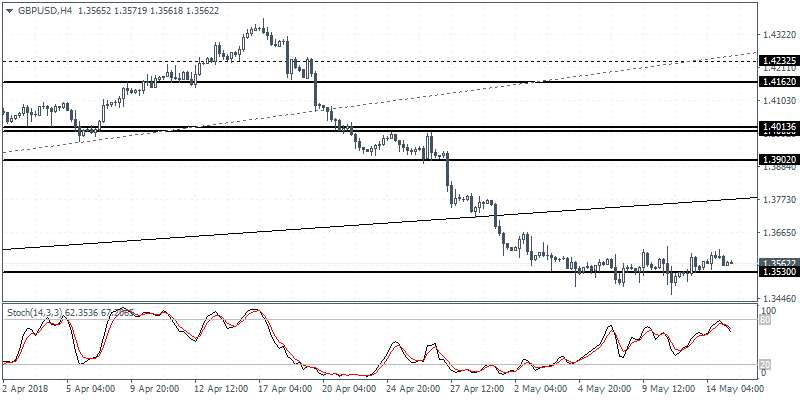

GBPUSD Intraday Analysis

GBPUSD (1.3562): GBPUSD continues to trade flat with price action consolidating near 1.3530 level. The rather prolonged sideways movement is likely to trigger a volatile breakout in the near term. The support level at 1.3530 could hold the declines in the near term, with the downside breakout pushing prices closer to the 1.3500 level of support. To the upside, there is a strong possibility of a correction in prices with the intial target coming in around 1.3737 followed by the horizontal resistance level of 1.3902.

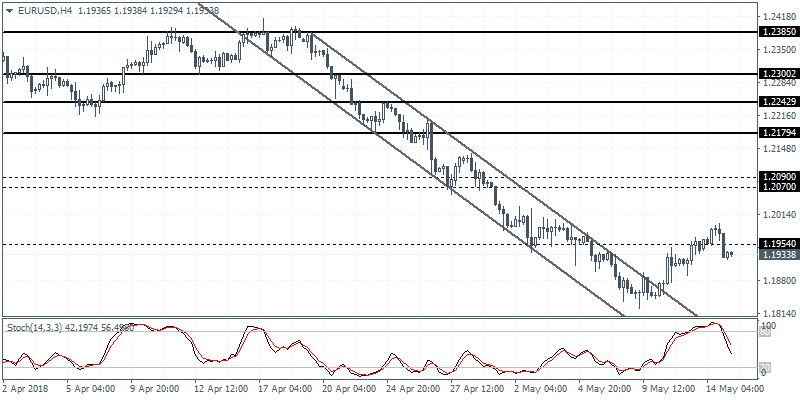

EURUSD Intraday Analysis

EURUSD (1.1933): The EURUSD rallied to a seven day high on Monday with price reaching intraday highs of 1.1963 before easing back on the day. The declines came off the highs as it coincided with the recently breached support level that has now turned into resistance. A bearish close below 1.1920 could potentially signal a near term decline in price. On the 4-hour chart, we see a hidden bearish divergence which is likely to signal the downside in price. A higher low being formed off this reversal could mean that prices are likely to rebound in the near term, provided the resistance level of 1.1920 - 1.1960.

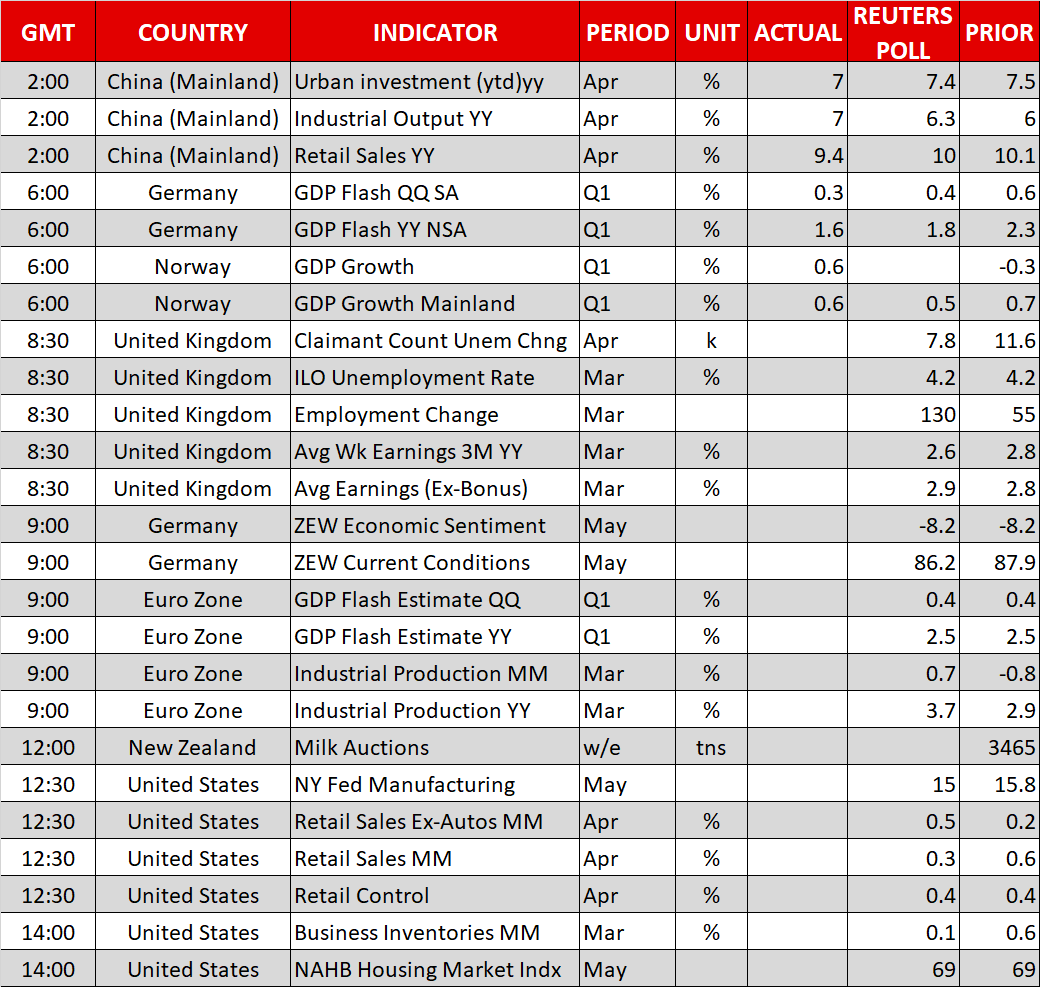

Investors Eye Eurozone GDP, UK Jobs Report

The markets were seen trading mixed with the U.S. dollar showing signs of easing back on Monday. Economic data was sparse with only the speech by Cleveland Fed President Loretta Mester.

Speaking at a conference in Paris, Mester said that the Federal Reserve will most likely maintain its rate hike guidance for the year while at the same time tolerate an overshoot of inflation target. The comments however failed to push the U.S. dollar higher on the day.

Looking ahead, the economic data for the day will be dominated by the preliminary GDP release from Germany and the French final inflation rate. Later in the day, the UK's labor market data will be released. Expectations show that the UK's unemployment rate held steady at 4.2% in the three months ending April. Wage growth is expected to rise at a modestly slower pace of 2.7% compared to the 2.8% increase seen previously.

The Eurozone second revised GDP estimates will also be coming out today. The median expectations point to 0.4% increase, unchanged from the preliminary increase.

Economic data from the United States will see the release of the retail sales report followed by the Empire State Manufacturing Index.

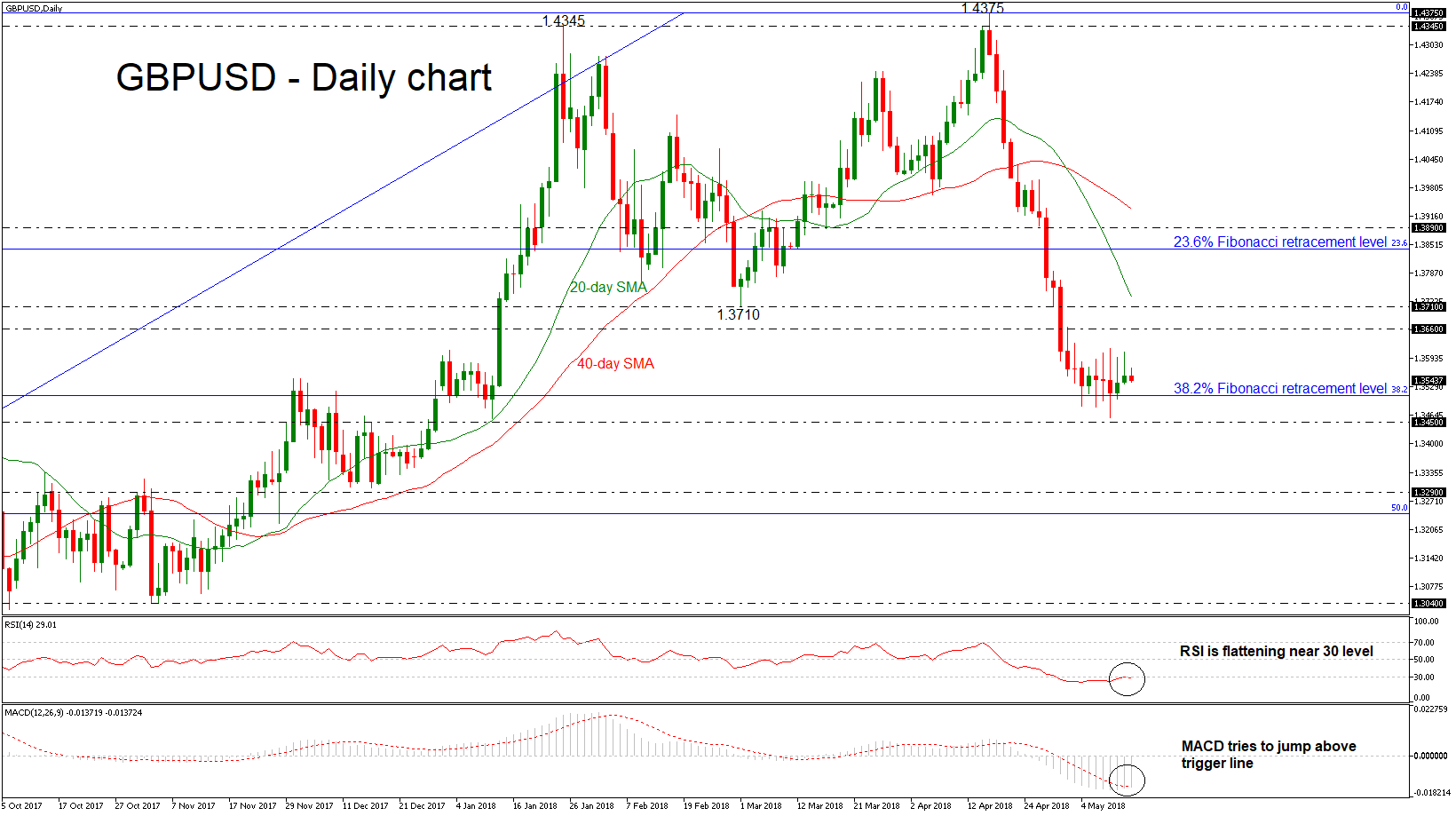

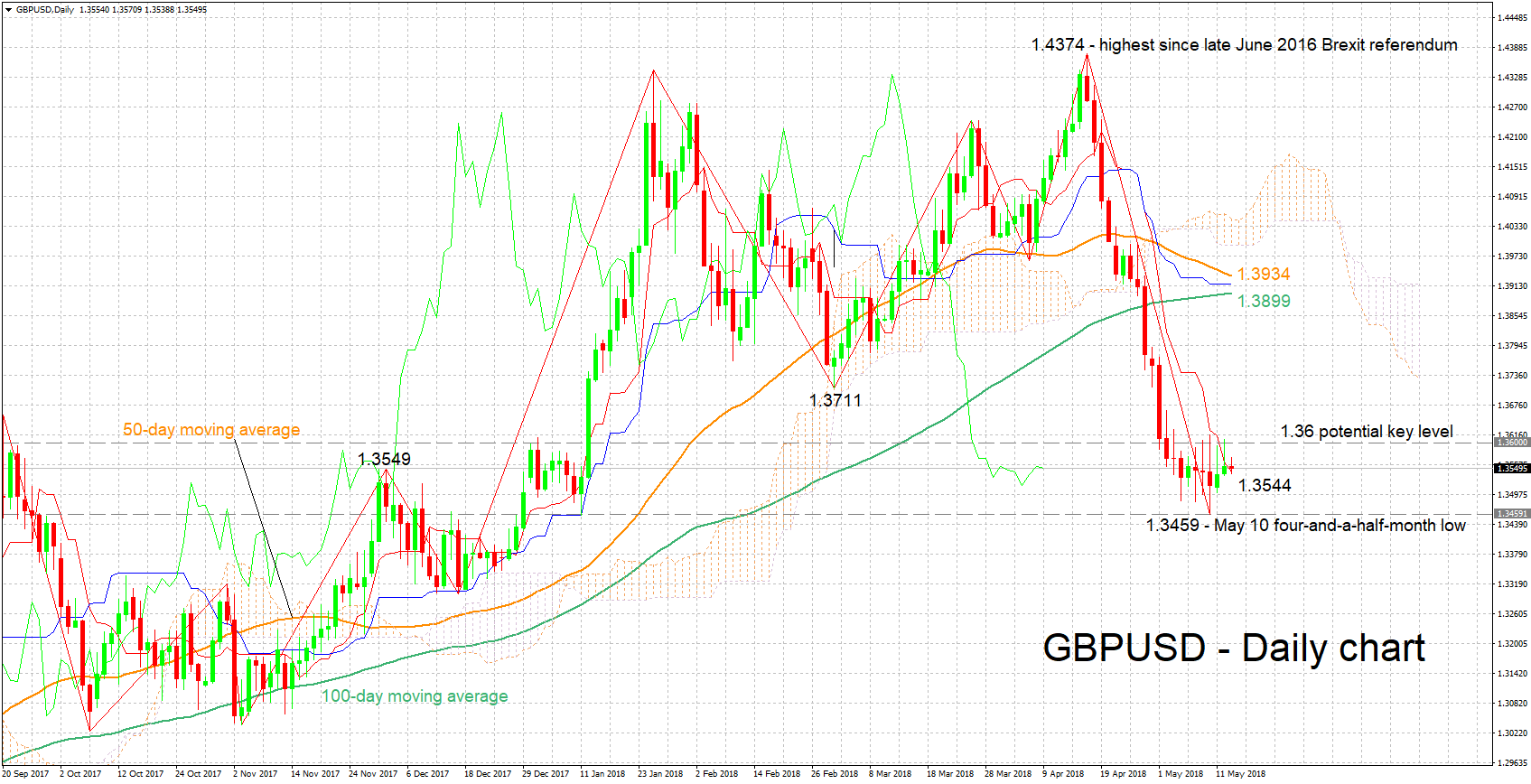

GBPUSD Maintains Weak In Near Term, Broader Trend Is Bearish

GBPUSD has been underperforming in the past eight days as it has failed to post a significant day of gains or losses. The pair is consolidating slightly above the 38.2% Fibonacci retracement level of 1.3510 of the upleg from March 12 to May 15. Last Thursday, the cable recorded a fresh four-month low of 1.3459, while at the short-term picture the pair lacks a clear trend.

In the daily timeframe, prices are moving sideways and based on technical indicators, momentum is too weak to provide a sustained move higher. The RSI indicator is flattening in the oversold level near the 30 barrier, while the MACD oscillator is trying to jump above its trigger line to create a bullish cross.

If price action remains above the 38.2% Fibonacci mark (immediate support), there is scope to test the 1.3660 resistance level. Clearing this key level would see additional gains towards the next resistance of 1.3710. Rising above it and surpassing the 20-day simple moving average (SMA) near 1.3730 would see prices re-test the 23.6% Fibonacci of 1.3840.

However, if the 1.3510 support fails, then the focus would shift to the downside again towards the 1.3450 support, taken from the low on January 11. If this level is breached, it would increase downside pressure and challenge the 1.3290 hurdle.

To sum up, GBPUSD has been neutral since peaking at 1.3615 and finding support at 1.3450. Near-term weakness is expected to remain as long as price action is taking place near the 38.2% Fibonacci.

Dollar Rebounds Ahead Of Key Events, UK Employment Data Eyed

Here are the latest developments in global markets:

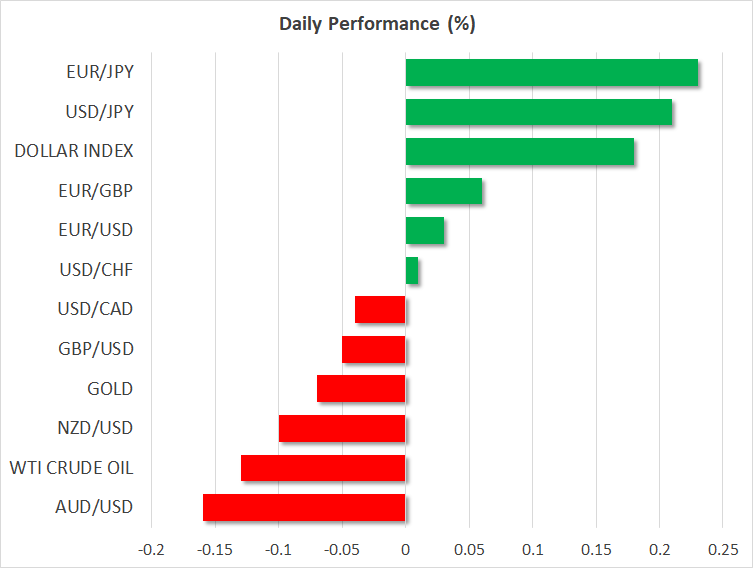

FOREX: The US dollar index is nearly 0.2% higher on Tuesday, building on the gains it recorded yesterday on the back of a surge in longer-term US bond yields. The Japanese yen, which is seen as a safe haven asset, is on the back foot as trade risks have moved out of the spotlight and focus has turned to potential solutions through negotiations.

STOCKS: Wall Street closed higher on Monday, though the gains were only modest. The Dow Jones led the way, rising by 0.27%, while the Nasdaq Composite and the S&P 500 climbed 0.11% and 0.09% respectively. Futures tracking the Dow, S&P, and Nasdaq 100 are all currently flashing red, pointing to a lower open. In terms of events today, traders will look to the release of US retail sales, as well as testimonies by two Fed nominees. In Asia, market sentiment soured after some relatively soft data out of China. In Japan, the Nikkei 225 and the Topix declined by 0.21% and 0.04% correspondingly, while in Hong Kong, the Hang Seng fell 1.04%. Europe was a similar story, with futures following the major benchmarks being a sea of red, suggesting these indices may open lower.

COMMODITIES: Oil prices are marginally lower today, with both WTI and Brent declining roughly 0.1%, giving back some of the gains they posted yesterday after OPEC raised its 2018 forecast for global crude demand. Prices remain elevated near the three-and-a-half year highs reached last week, as markets are still scrambling to determine how much impact the US sanctions on Iran will have on global supply, and whether other major players will “fill the gap” by raising their own production. In precious metals, gold is 0.07% lower today, extending losses from yesterday. It is trading just above the $1,311/ounce zone and looks to be headed for a test of its 200-day moving average at $1,307, which has halted several declines this month.

Major movers: Dollar gains ground ahead of key events; ECB’s Villeroy briefly boosts euro

The US dollar index was on the back foot during yesterday’s European session but managed to pare all its losses and finish the day higher overall, buoyed by a surge in longer-term US bond yields. The yield on 10-year Treasuries jumped back above the psychological 3.0% handle, and currently rests at 3.02%, hovering just below the four-year high reached in early April.

Today, the dollar will probably get its cue from US retail sales data. Of equal importance may be some remarks before the US Senate from Richard Clarida and Michelle Bowman, who have been nominated to become Fed Vice Chair and Board Governor respectively. Markets will attempt to gauge where they lean on the hawk-dove spectrum, and what their appointments might mean for upcoming Fed decisions, since both positions hold permanent voting rights in the FOMC.

Euro/dollar started to move higher after some hawkish-perceived comments from ECB Governing Council member Francois Villeroy de Galhau, but met resistance just below the round figure of 1.2000, and turned back down as the dollar started to recover. Villeroy said the first ECB rate hike may come some quarters and not years after the Bank ends its QE program. While his comments were more or less in line with previous ECB guidance and current market pricing, investors still reacted by pushing the euro higher. That said, the common currency erased all its gains to finish the day lower versus the dollar and sterling, but not the yen, which has been on the back foot lately as trade risks appear to be fading.

In the antipodean sphere, aussie/dollar is 0.15% lower today, following the release of the minutes from the latest RBA policy gathering and a speech by RBA Deputy Governor Guy Debelle. The minutes revealed nothing new, reaffirming the Bank will remain patient as it waits for wages to pickup. Meanwhile, Debelle erred on the side of caution, saying he does not see a “strong case” for a near-term rate increase. Elsewhere, kiwi/dollar was down by 0.1%, trading not far above a five-month low of 0.6890.

Day ahead: UK wage growth and US retail sales in focus; German ZEW survey, eurozone GDP & industrial production also on the horizon

Tuesday’s calendar is a rather packed one, with UK employment data and US retail sales being among the releases expected to attract most attention.

At 0830 GMT, UK employment data for March, as well as the unemployment benefits claimant count for April will be made public. The unemployment rate is anticipated to remain at the multi-decade low of 4.2% in March. Wage growth figures will be closely watched, as maybe they have the greatest capacity to stoke expectations for a rate hike by the Bank of England sooner rather than later. In this respect, the three-month average of average weekly earnings is projected to grow by 2.6% y/y, easing from February’s 2.8%. Still, if expectations materialize, this would mark the second straight month of positive real wage growth. Excluding bonuses, average earnings are expected to edge higher, expanding by 2.9% y/y, versus February’s 2.8%. The BoE next meets in late June, with markets currently assigning a less than 15% chance for an increase in rates, according to UK overnight index swaps.

Updated Q1 GDP figures out of the eurozone at 0900 GMT are forecast to confirm growth at 0.4% on a quarterly basis and 2.5% on an annualized basis. There are fears of easing economic activity in the euro area and in this respect the ZEW surveys gauging business morale in Germany, the eurozone’s largest economy, will be of interest. Further weakness in the surveys will add to worries, whereas strong numbers might start changing the narrative, pointing to a transitory slowdown. The institute’s economic sentiment index is expected to remain in negative territory in May – it turned negative for the first time since July 2016 in April – while the current conditions index is anticipated to decline for the fourth straight month.

Eurozone industrial production figures for March will also be released at 0900 GMT; an acceleration in activity is expected.

Kiwi traders will be paying attention to the bi-weekly milk auction due later in the day – it carries a tentative release time of 1200 GMT; New Zealand is a major diary exporter.

Out of the US, the main data point of the day are retail sales for the month of April (1230 GMT), which are expected to moderate on a monthly basis, expanding by 0.3%, half the pace recorded in March. Core retail sales that exclude automobiles will also be monitored. A disappointment in the data could further put off the table a fourth rate hike in total during 2018 by the Federal Reserve – following last week’s weaker CPI numbers – leading to a weakening US currency. The New York Fed manufacturing survey for May as well as data on April’s retail control are scheduled for release at the same time.

Also out of the US, are business inventories data for March, as well as the National Association of Home Builders housing market index. Both are due at 1400 GMT.

In relation to bilateral trade talks between the US and China, Liu He, the latter’s Vice Premier who also serves as President Xi’s top economic adviser, will be in Washington today.

As the markets attempt to gauge the situation following the Trump administration’s decision to walk away from the Iran nuclear deal, a meeting between EU foreign policy chief Federica Mogherini and the foreign ministers of Britain, France and Germany might be of interest.

API data on crude oil stocks are due at 2030 GMT.

Policymakers sharing remarks include Riksbank First Deputy Governor Kerstin af Jochnick (0725 GMT) who will be talking on the Swedish central bank’s monetary policy, Dallas Fed President Robert Kaplan (non-voting FOMC member in 2018 – 1200 GMT) who will be talking on “Energy, Trade, and Economic Growth”, and San Francisco Fed President John Williams who will be speaking at 1710 GMT – Williams will take over the role of New York Fed chief in June (the New York Fed President holds permanent voting rights within the FOMC). Moreover, the Senate Banking Committee will be holding a hearing on the nominations of Richard Clarida as member and vice chairman of the Federal Reserve Board of Governors, and Michelle Bowman as member of the Federal Reserve Board of Governors at 1400 GMT.

Lastly, regional tensions after the Trump administration’s decision to move the US embassy to Jerusalem are not to be ignored. Protests took place following the move yesterday, with Israeli forces killing dozens of Palestinians.

Technical Analysis: GBPUSD short-term bearish; possibly oversold

GBPUSD has recorded considerable losses since around mid-April and after rising to its highest since June 2016’s Brexit referendum (1.4374). On Thursday, it touched a four-and-a-half-month low of 1.3459. The negatively aligned Tenkan- and Kijun-sen lines are attesting to the negative bias. However, the Kijun-sen has halted its decline and the Chikou Span may be pointing to an oversold market; a reversal in the near-term should not be ruled out.

Stronger-than-expected UK data later in the day are likely to boost the pair, with resistance potentially coming around the 1.36 round figure and further above from the region around 1.3710 (this being a previous bottom, with the area around it encapsulating the 1.37 handle).

On the downside, and in case of weaker-than-anticipated figures, support could come around last week’s low of 1.3459, given that the range around the Tenkan-sen at 1.3544 which seems to be providing immediate support, is conclusively violated first.

US releases also have the capacity to move the pair.

EURUSD Bearish Below 1.1900 Level

The euro currency has fallen sharply lower against the US dollar, after buyers failed to move the pair above the key 1.2000 level on Monday. The EURUSD pair is currently trading around the 1.1915 level, and is under heavy selling pressure as the US dollar index starts to find buying interest again. Traders will now look for a break of the key 1.1900 support level, which would likely increase technical selling in the EURUSD pair.

The EURUSD pair is strongly bearish while trading above the 1.1900 level, further downside towards 1.1852 and 1.1822 seems possible.

If the EURUSD pair moves above the 1.1938 level, we may see a correction back towards the 1.1968 and 1.1995 resistance levels.

USDJPY Bullish Above 110.03 Level

The US dollar has continued to advance higher against the Japanese yen currency, with buyers pushing price within close distance of the key 110.00 technical level. The USDJPY pair currently trades around the 109.85 level, with bullish upside momentum growing across both MACD and Stochastic indicators. Trader are watching for a bullish move above the monthly-high, at 110.03, and the bullish inverted head and shoulders pattern across the lower-time frame charts.

The USDJPY pair is strongly bullish while trading above the 110.03 level, key resistance is then located at the 110.40 and 111.00 levels.

If the USDJPY pair starts to fail around the 110.00 level, sellers may move the pair back towards the 109.65 and 109.39 support levels.