Sample Category Title

Global Data Flows In The Headlines On Tuesday

The economic calendar ramps up once again on Tuesday, with headline reports from both sides of the Atlantic Ocean. The facts and figures released over the coming hours could have a direct impact on key currency pairs, including the EUR/USD, GBP/USD and USD/JPY.

The European session kicks off with headline German GDP data. Europe's largest economy is forecast to grow 0.4% in January-March down from 0.6% the previous quarter. This likely translates into a year-over-year growth rate of 1.7%.

France is scheduled to release multiple data sets at 06:45 GMT, including the monthly consumer price index and Q1 nonfarm payrolls. Consumer inflation is projected to rise 0.1% month-on-month. Meanwhile, first-quarter nonfarm payrolls are projected to rise 0.4%.

In the UK, the Office for National Statistics will release the latest employment figures for April. Britain's claimant count change is expected to rise by 7,500, signaling higher unemployment. However, the jobless rate is forecast to hold steady at 4.2% in the three months through March. Average hourly earnings including bonuses likely rose 2.6% annually in the first quarter.

ZEW will produce its monthly indicator of German investor sentiment at 09:00 GMT. At the same time, the European Commission's statistical agency will report on first quarter GDP for the 19-member currency zone. The Eurozone economy likely rose 0.4% in the January-March period.

Shifting gears to North America, the US Department of Commerce will report on retail sales at 12:30 GMT. Receipts at retail stores, long viewed as an important proxy for consumer spending, are forecast to rise 0.3% for April.

Meanwhile, the Federal Reserve Bank of New York will produce the Empire State manufacturing survey at 12:30 GMT. The headline indicator is forecast to show slight weakness during May.

In terms of monetary policy, Federal Open Market Committee (FOMC) members Robert Kaplan and John Williams are scheduled to deliver speeches.

EUR/USD

Europe's common currency was upended on Monday, as prices failed to break above the 1.2000 US barrier. At the time of writing, EUR/USD was trading around 1.1940, where it continues to face resistance at the psychological level.

GBP/USD

Cable prices also broke down on Tuesday as the US dollar strengthened against a basket of world currencies. The GBP/USD exchange rate fell from a high near 1.3605 all the way back down to 1.3565. The pair faces immediate resistance at 1.3600, followed by the 1.3715 area.

USD/JPY

The greenback rebounded against the yen at the start of the week as the DXY dollar index rose to fresh yearly highs. USD/JPY is now trading around 109.72, where it is coming up against firm resistance near 109.80 and 110.00. On the opposite side of the ledger, immediate support is located near the session low of 109.40.

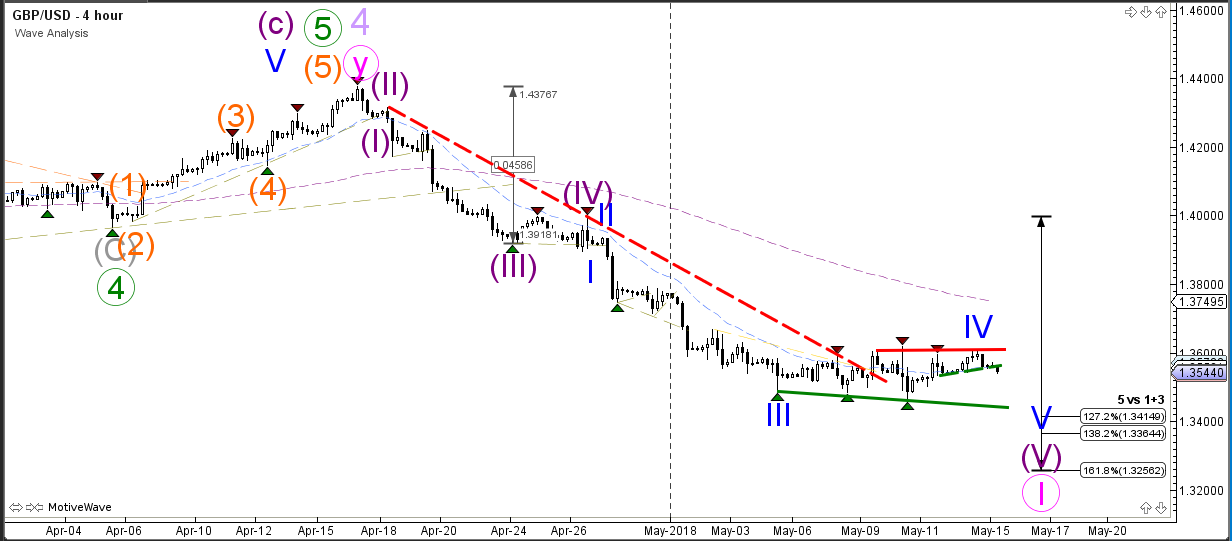

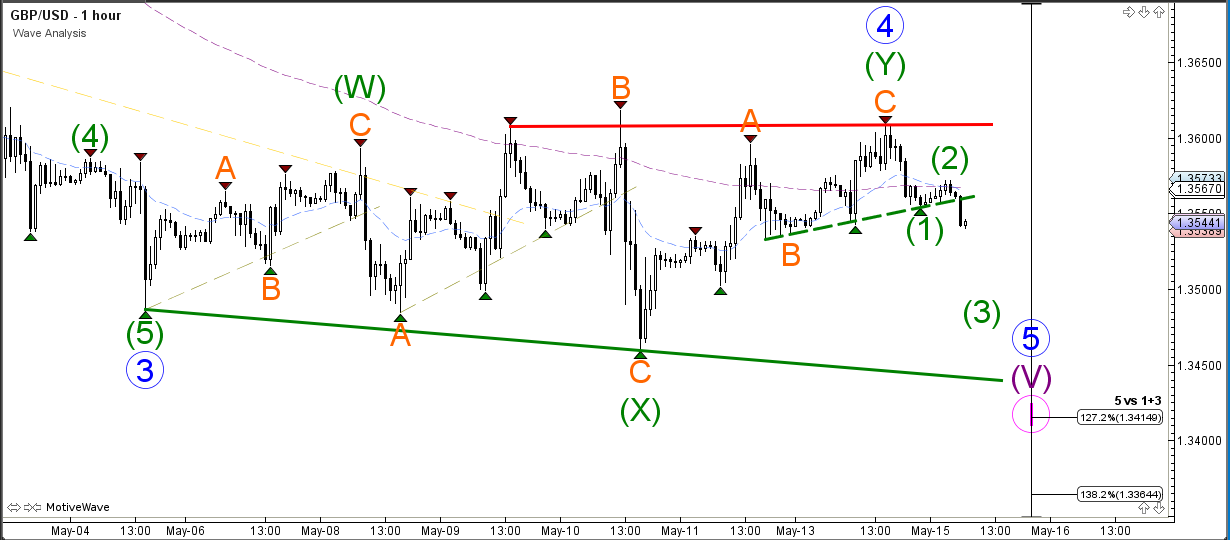

GBP/USD Reverses At 1.36 Resistance And Shows Bearish Breakout

The GBP/USD seems to have completed a sideways consolidation zone which is most likely a wave 4 (blue) pattern. Price is now trying to break below the support trend line (dotted green) which could indicate the end of wave 4 and the start of a bearish wave 5 (blue). The targets are at the Fibonacci levels of wave 5 (blue). Price could be reversing if price manages to break above the resistance trend line (red) at 1.36 – 1.3650.

The GBP/USD could have completed the wave 4 (green) as price stayed below the 50% Fibonacci retracement level. Price could now be building a bearish breakout which could be a wave 1 or 3 (green) within the larger wave 5 (blue).

EUR/USD Bearish Reversal At 1.20 Fibonacci Resistance Levels

The EUR/USD respected and reversed at Fibonacci resistance levels of wave 4 (green). The uptrend channel ran out of steam and is now building a bearish turn. Price is now testing the support trend line (green) of the uptrend channel and a bearish breakout could indicate a continuation of the 5th wave (blue). The main target is probably 1.1750 whereas a break above the 50% Fib at 1.2118 makes the current wave 4 less likely.

The EUR/USD seems to have completed a rising wedge chart pattern and larger WXY (orange) correction.Price is now trying to build a bearish breakout which could be a wave 5 (orange) of wave 1 (green). In that case, there could be a bullish retracement in wave 2 before a bearish continuation within wave 5 (orange) takes place

USD/JPY Bounces In Uptrend Channel And Tests 110 Resistance

The USD/JPY bounced at the key support trend line (blue) of the bullish channel and price is now retesting the resistance trend line (red) from the previous top. A bullish breakout could indicate the continuation of the bullish channel towards 111.50 which is where the 50% Fib is located.

The USD/JPY broke above the resistance trend line (dotted red) for a bullish breakout. Price will now test the previous top which is a new bounce or break spot. Sideways price action could indicate a continuation chart pattern.

NAFTA talks unlikely to have breakthrough before My 17

Canadian Prime Minister Justin Trudeau discussed with Trump on phone yesterday on brining NFATA renegotiation to a "prompt conclusion". But US Commerce Secretary Wilbur Ross side that none of the "big hot topics" were resolved as the May 17 deadline looms. He added hose are "very complex issues", and are still "a work in progress".

It's reported that, according to sources", there is no plan for Mexican Economy Minister Ildefonso Guajardo or Canadian Foreign Minister Chrystia Freeland, and U.S. Trade Representative Robert Lighthizer to meet this week. It's unlikely for any breakthrough in the negotiation.

Currently, Canada and Mexico have their US steel tariffs exemption extended to June 1. Ross said, "depending on where we are on NAFTA on June 1, the president will decide whether or not to extend their situation." And "it's unforecastable at the moment."

Currencies: Will US Retail Sales Be Strong Enough To Revive USD Rebound?

Rates: US 10-yr yield returns north of 3%

Core bonds lost ground yesterday with German Bunds underperforming. Inflation expectations rise further. The US 10-yr yield trades back above 3%. Attracted by key resistance at 3.07%, we think the sell-off could continue against the back of strong expected US eco data and probably relatively hawkish Fed comments.

Currencies: Will US retail sales be strong enough to revive USD rebound?

EUR/USD rebounded close to 1.20 yesterday, but the test was rejected. The focus turns to the US April retail sales today. After last week's ‘soft' US CPI, a good report is probably needed to keep the USD rally alive. For now, geopolitical tensions apparently are supporting the dollar more than the euro. Sterling traders will keep a close eye at the UK wage growth data.

The Sunrise Headlines

- US stock markets opened strong, but trimmed gains as US rates and the dollar were upwardly oriented during US dealings. Asian bourses face some selling pressure this morning with India outperforming.

- The US and China are “still very far apart” on disputes over trade, technology, and market access, the US ambassador to China said, managing expectations ahead of a visit to Washington by a senior Chinese envoy. (FT)

- China reported weaker-than-expected investment (7% Y/Y) and retail sales (9.4% Y/Y) in April and a drop in home sales, clouding its economic outlook. Industrial production (7% Y/Y) was this morning's bright spot. (Reuters)

- The IMF has sounded a fresh warning about Ireland's surging property market, saying residential prices appear “modestly overvalued” by some measures. They also called for “close attention” to the upswing in Irish commercial property. (FT)

- Turkish President Erdogan said he intends to tighten his grip on the economy and take more responsibility for monetary policy if he wins an election next month. EUR/TRY set a new all-time high above 5.20. (BB)

- The EU warned Britain time was running out to seal a Brexit deal this autumn and ensure London does not crash out of the bloc next March, adding to pressure on PM May. (Reuters)

- Today's eco calendar contains US retail sales, Empire manufacturing, the UK labour market report, German ZEW-survey, 2nd reading of Q1 EMU GDP and several Fed speakers.ay's eco calendar contains US retail sales, Empire manufacturing, the UK labour market report, German ZEW-survey, 2nd reading of Q1 EMU GDP and several Fed speakers.

Currencies: Will US Retail Sales Be Strong Enough To Revive USD Rebound?

Will US retail sales revive USD rebound?

The USD decline since last week's US CPI initially continued yesterday. The trade-weighted dollar drifted south. Some euro strength was also in play. ECB‘s Villeroy indicated that APP will probably halt this year and it won't take ‘years' for the ECB to raise rates after APP. LT interest rate differentials narrowed in favour of the euro. EUR/USD came close to the 1.20 area, but the rally ran into resistance and gains couldn't be sustained. The pair even closed the day with a small loss at 1.1926. At the same time USD/JPY remained well bid (close at 109.66). So, in the end, the dollar showed quite resilient despite some intraday gyrations.

Asian equities mostly trade with modest losses overnight. The oil price continues to push higher with Brent above $78/barrel. The US 10-y yield regained the 3.0% barrier. Geopolitical tensions in the Middle East and higher US yields for now tilt the balance again in favour of the dollar. USD/JPY is nearing the 110 mark. EUR/USD also trades with a slightly negative bias (1.1920 area).

Today, the EMU and German Q1 GDP and German ZEW sentiment will be published. Yesterday's price action shows that the euro is not immune for EMU news. However, the focus for FX trading will probably turn to the US retail sales. Last week's ‘soft' US CPI suggests that negative news might make the market more cautious on the scenario of four Fed rate hikes this year. So, the USD probably at least needs an in-line outcome to resume its recent rebound. At the same time, the USD shows good resilience given the rise in the oil price. We also have the impression that the USD profits more from (geopolitical) uncertainty than the euro. Yesterday, we indicated that we didn't see a trigger for a big USD decline yet. We hold on to that view even as multiple conflicting factors are in play. Yesterday's rejected test of EUR/USD 1.20 and the solid rise in USD/JPY might give USD bulls some comfort. The 1.1823 correction low is the first reference in EUR/USD ahead of 1.1718.

UK labour data will be released today and the government will again meet on Brexit. UK job growth is expected solid and earnings (ex-bonus) are expected to rise to 2.9% Y/Y. Meeting the consensus could lift the probability of an August rate hike again. After last week's BoE decision, the EUR/GBP rebound halted near 0.8850. Some modest sterling gains are possible in case of a decent labour report. However, we don't expect a sustained GBP rally yet.

EUR/USD rebound blocked near 1.20. Focus turns to US retail sales

U.K. Jobs Under The Radar, Turkish Lira Falls To New Low

Stocks in Asia were uninspired by the slight gains onWall Street during Monday trading. Although the easing of U.S.-China trade tensions was supposed to be positive forrisk assets, the rise in global yields is making stocks less attractive. Comments from the Bank of France Governor, François Villeroy de Galhau, that the European Central Bank will not delay exiting quantitative easing pushed yields on European bonds higher, promoting profit taking. Meanwhile, U.S. 10-year treasury yields are back above 3%, suggesting that investors will require more risk premium for holding equities. Unless growth offsets the rise in risk premium, equities will likely face some challenging times ahead. European stocks are set to open lower and U.S. futures are also indicating a lower open.

Brent above $78

Brent continued its upward momentum on Monday, reaching a new three-and-a-half year high of $78.53. Conflict escalation in the Middle East following the U.S. ‘s withdrawal from the Iranian nuclear deal and the inauguration of the U.S. embassy in Jerusalem, added further geopolitical risk premium to the already elevated prices.

Higher oil prices, which were recently a positive indicator ofrisk, will start having an adverse effect on global equities. If energy prices sustain theirupward trajectory, it will be just a short matter of time before we start seeing the shockwaves reaching Wall Street. The energy sector weighs only 5.90% in the S&P 500, but the effect of company costs and consumer disposable income will largely outweigh the benefits for this relatively small sector, compared to the overall economy.

Pound traders await jobs report

The pound has lost more than 800 pips from April highs, after a series of weak economic releases led the Bank of England to stand pat on rates. A slight improvement in data will likely be enough to bring the bulls back, so will the U.K. jobs report boost confidence?

Economists expect unemployment to hold steady at 4.2%, but it’s the average earnings that will drive the direction of the pound. After U.K. inflation fell to 2.5% in March from 2.7%, an upside surprise in wages will refuel expectations of a BOE rate hike leading to a recovery in GBPUSD.

Turkish Lira hit new record low

Turkish President Recep Tayyip Erdogan’s intention to exert more influence on monetary policy if he wins the general election next month wasn’t received well by traders. The Turkish Lira fell to a new record low of 4.39 after his comment. On Wednesday, the Turkish president called a meeting to discuss the exchange rate. Market participants thought that this meeting would lead to a hike in interest rates;however, this now seems off the cards, so expect further losses in the coming weeks.

UK Jobs Report Due From The UK Today

At 08:30 GMT, UK Average Earnings excluding Bonus (3Mo/Yr) (Mar) is expected to come in at 2.9% from 2.8% previously. Claimant Count Change (Apr) is expected at 7.5K from a previous reading of 11.6K. ILO Unemployment Rate (3M) (Apr) is expected to be unchanged at 4.2%. Average Earnings including Bonus (3Mo/Yr) (Mar) is expected to be 2.6% from 2.8% previously. Claimant Count Rate (Mar) was 2.4% previously. Wage growth had been expected to continue to tick up last month, having stabilised at 2.5% and risen to 2.8% in the previous months, however, it missed the 3.0% consensus. The unemployment rate is at multi-decade lows, which should normally lead to higher wage growth, as competition to attract workers takes hold. The BOE will study wage data to see any indication of a pick-up and decide whether they need to maintain their hawkish tone. GBP crosses could be influenced by this data release.

At 09:00 GMT, German ZEW Survey – Current Situation (May) is expected at 86.2 against a prior 87.9. ZEW Survey – Economic Sentiment (May) is expected to be unchanged at -8.2. These data points are expected to soften, as the strengthening in the Euro affects business. The deteriorating trade environment is also a headwind for business outlook. Last month was the first negative forecast in sentiment since Brexit. EUR crosses may be affected by this data.

At 09:00 GMT, Eurozone Gross Domestic Product s.a. (QoQ) (Q1) is expected to come in unchanged at 0.4%. Gross Domestic Product s.a. (YoY) (Q1) is also expected to be unchanged at 2.5%. Industrial Production w.d.a. (YoY) (Mar) will be released with a consensus of 3.7% from a prior of 2.9%. Industrial Production s.a. (MoM) (Mar) is expected at 0.7% from -0.8% previously. The monthly figure had dipped to -1.0% but rebounded last month, with a much stronger rebound expected today. The EUR may be moved by this data.

At 10:30 GMT, The Central Bank of Russia will release its Interest Rate Decision. The rate was held at 7.25% previously. RUB pairs may see volatility increase around this event.

At 12:30 GMT, US Retail Sales (MoM) (Apr) will be released with an expected 0.3% from 0.6% previously. Retail Sales ex Autos (MoM) (Apr) is expected at 0.5% from 0.2% prior. Retail Sales Control Group (Apr) is expected to be unchanged at 0.4%. It is expected that sales will slip after last month’s beat, despite an expected stronger performance from Autos. USD crosses could see increased volatility around this data release.

At 17:00 GMT, FOMC Member Williams is expected to speak at the Economic Club of Minnesota May Luncheon, in Minneapolis. Audience questions are expected. USD crosses may be affected by any comments made.

Chinese Retail Sales Data Registers Lowest Reading In Over A Decade

China was one of the top stories overnight, as Moody’s released their analysis on the China/US trade war. They believe that China is unable to meet the US request to reduce its trade surplus “by $200B by 2020 without causing significant disruptions to its economy”. They also believe that this measure would be incompatible with the Chinese government’s policy objectives. Chinese Retail sales were released earlier at 9.4%, missing the expected 10.0% and the previous 10.1% reading. This is the lowest reading for this data in over a decade. Industrial Production came in at 7.0%, beating expectations of 6.3%, and the previous 6.0% reading. USDCNY is up overnight from 6.3385 to 6.3486.

German Gross Domestic Product (QoQ) (Q1) was 0.3% against an expected 0.4%, from 0.6% prior. Gross Domestic Product (YoY) (Q1) was 1.6% against an expected 1.8%, from 2.3% prior. Gross Domestic Product w.d.a. (YoY) (Q1) was released with a reading of 2.3%, against a consensus number of 2.4% and a prior of 2.9%. This data shows a continued decline in German GDP numbers.

The RBA released its Meeting Minutes earlier this morning, with the board agreeing there was not a case for a near-term move in policy. They also agreed that, given the current circumstances, the next rate move would likely be up rather than down. Unemployment and inflation are likely to show only a gradual improvement. AUDUSD started to rally from a low of 0.75216 in the lead-up to the release, then peaked at 0.75372 after the event. It has since fallen to a fresh low of 0.75069.

EURUSD is down -0.05% overnight, trading around 1.19211.

USDJPY is up 0.19% in early session trading at around 109.864.

GBPUSD is down -0.04% this morning, trading around 1.35497.

Gold is down -0.11% in early morning trading at around $1,311.89.

WTI is down -0.36% this morning, trading around $70.99.

BoJ Kuroda: “Absolutely no plan” to raise yield target

BoJ Governor Kuroda told the parliament today that there is "absolutely no plan" to raise the yield target under the Yield Curve Control for now, as inflation is still distant from 2%. He also explained that removing the time frame to meet the 2% inflation target is not necessarily related to the side effect of monetary policy on bank profits.

Regarding YCC, Kuroda said bond purchases are more sustainable under the framework, as the central bank has more flexibility. And, it's be able to maintain long term year near 0% with smooth operations in JGB purchases.