Sample Category Title

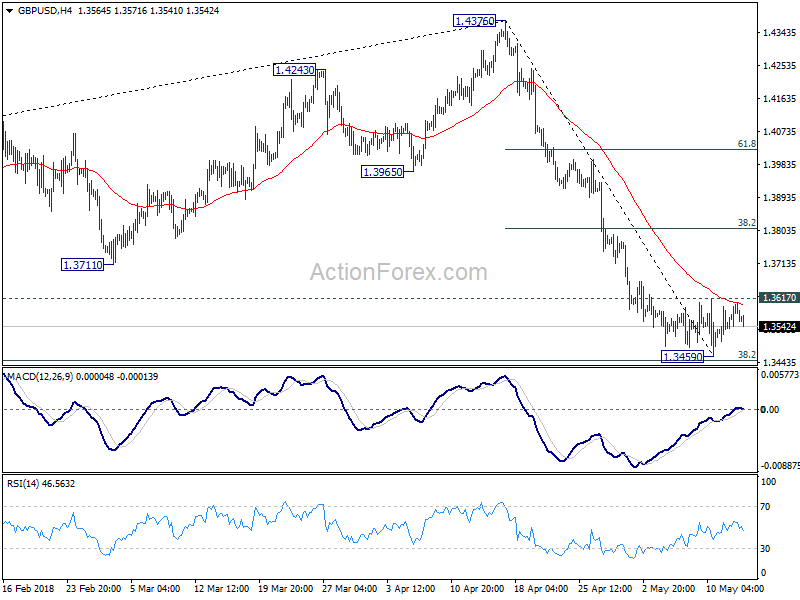

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3523; (P) 1.3566; (R1) 1.3598; More...

GBP/USD continues to be bounded in right range of 1.3459/3617 and intraday bias remains neutral. More consolidations could be seen. Break of 1.3617 will turn bias to the upside for stronger recovery. But upside should be limited by 38.2% retracement of 1.4376 to 1.3459 at 1.3809. On the downside, sustained break of 1.3448 fibonacci level will confirm resumption of whole fall from 1.4376 and target next fibonacci level at 1.2874.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 was almost met. Break there will target 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3861) holds, even in case of strong rebound.

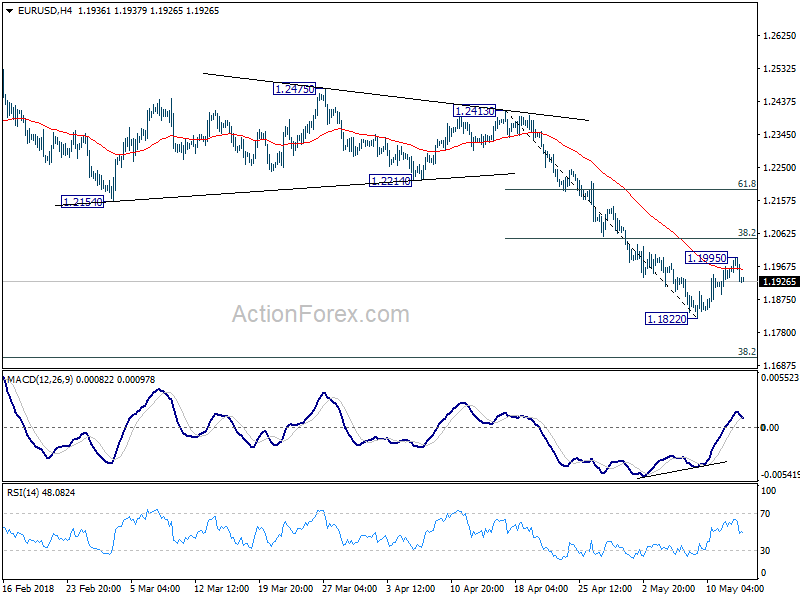

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1903; (P) 1.1950 (R1) 1.1975; More....

EUR/USD's recovery from 1.1822 short term bottom could have completed at 1.1995 already, ahead of 38.2% retracement of 1.2413 to 1.1822 at 1.2048. Intraday bias is turned back to the downside for retesting 1.1822 first. Break there will resume whole decline from 1.2555 and target 1.1708 medium term fibonacci level next. In case of another recovery as the correction extends, upside should be limited by 1.2048 to bring fall resumption eventually.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will target 61.8% retracement at 1.1186. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2179) holds.

Dollar Recovers as EURUSD Fails 1.2, UK Employment and German ZEW Watched

Dollar's corrective pull back yesterday was rather brief and shallow. EUR/USD reached 1.1995 but failed to break through 1.2 handle. It's now back at 1.1930. USD/CHF breached parity briefly to 0.9956 and is back above 1.0000 now. GBP.USD continued to stay in tight range above 1.3459 and failed even to take out 1.3617 minor resistance. The greenback is staying in corrective mode in general, awaiting some fresh stimulus.

There are a couple of market moving events today. UK employment data is a notable one in the European session. The timing of the next BoE rate hike, be it August or November or next year, is very much data dependent. Sterling has been so far resilient but it will be vulnerable should there be another downside surprise in wage growth released today.

Also featured in European session are Eurozone GDP and industrial production and Germany GDP. But ZEW economic sentiment could be the market moving one. ECB is unsure whether the slowdown in Q1 is due to temporary factors only. And policymakers will continue to look at incoming economic data to get a clearer picture. Whether ECB could stop the asset purchase program after September will depend on ECB's interpretation of the data.

Later in the day, US will release retail sales, business inventories, Empire state manufacturing index and NAHB housing index. We'd not expecting much inspirations from these data. While retail sales is always seen as an important one, the impact on Dollar is seldom long lasting. Instead, the focus will firstly be on US-China trade talks. And secondly, 10 year yield is back pressing 3% level yesterday, hitting as high as 2.997, closing at 2.995. We'll see if there is sustainable strength in yield that could give Dollar a lift.

RBA minutes reiterated no strong case for near term hike

RBA May meeting minutes reiterated that central bank's stance that it's not in rush to lift interest rates. The minuted noted that "stronger growth was expected over the following couple of years, which could reduce spare capacity in the economy and lead to a further gradual decline in the unemployment rate." But, "the increase in wages growth and inflation was expected to be gradual however because spare capacity in the economy was expected to be reduced only slowly." And, "as progress in lowering unemployment and having inflation return to the midpoint of the target range was expected to be gradual, members also agreed that there was not a strong case for a near-term adjustment in monetary policy."

RBA Debelle: 2% is the focal point for wage outcomes now

RBA Deputy Governor Guy Debelle delivered a speech titled "The Outlook for the Australian Economy" at the CFO Forum in Sydney today, where he talked about wages. He noted that "the experience of other countries with labour markets closer to full capacity than Australia's is that wages growth may remain lower than historical experience would suggest."

Currently in Australia "2% seems to have become the focal point for wage outcomes, compared with 3–4% in the past." Even so, ""there is a risk that it may take a lower unemployment rate than we currently expect to generate a sustained move higher than the 2% focal point evident in many wage outcomes today".

Trump's tweet on ZTE prompted bipartisan criticism

Trump's tweet regarding helping China telecoms company ZTE prompted bipartisan criticism and concerns on his softening stance. Republican Senator Marco Rubio said he hoped "this isn't the beginning of backing down to China." Democrat Senator Chuck Schumer said "this leads to the greatest worry, which is that the president will back off on what China fears most - a crackdown on intellectual property theft - in exchange for buying some goods in the short run."

On the other hand, Trump defended with another tweet saying that "ZTE, the large Chinese phone company, buys a big percentage of individual parts from U.S. companies. This is also reflective of the larger trade deal we are negotiating with China and my personal relationship with President Xi".

US Ambassador to China Branstad: Trump wants a "dramatic increase" in food exports to China

US Ambassador to China Terry Branstad said in Tokyo today that both countries are still "very far apart" on resolving trade frictions. Branstad, was present at the meeting between Treasury Secretary Steven Mnuchin and Chinese Vice Premier Liu He in Beijing earlier this month. He noted that "there are many areas where China has promised to do but haven't. We want to see a timetable. We want to see these things happen sooner or later." He added that Trump would like to see a "dramatic increase" in food exports to China" and "we'd like to see China being just as open as the United States."

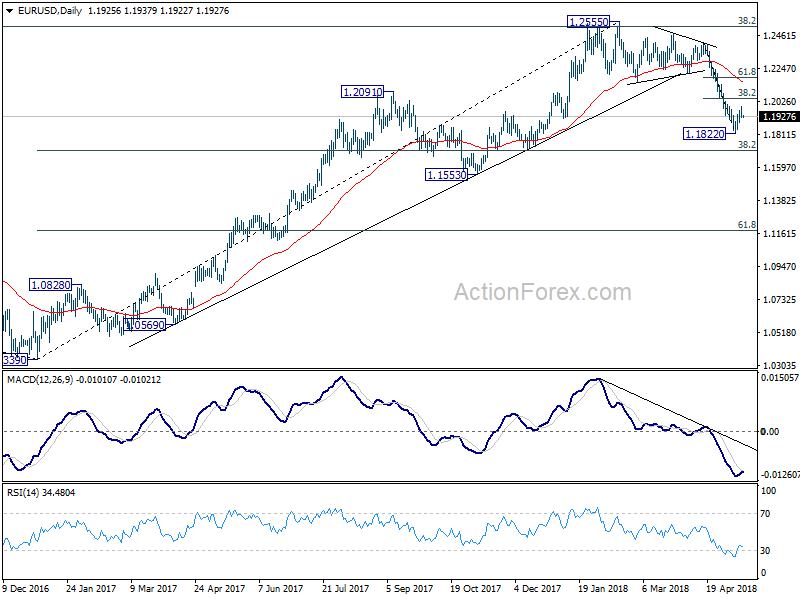

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1903; (P) 1.1950 (R1) 1.1975; More....

EUR/USD's recovery from 1.1822 short term bottom could have completed at 1.1995 already, ahead of 38.2% retracement of 1.2413 to 1.1822 at 1.2048. Intraday bias is turned back to the downside for retesting 1.1822 first. Break there will resume whole decline from 1.2555 and target 1.1708 medium term fibonacci level next. In case of another recovery as the correction extends, upside should be limited by 1.2048 to bring fall resumption eventually.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will target 61.8% retracement at 1.1186. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2179) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | RBA May Meeting Minutes | ||||

| 2:00 | CNY | Retail Sales Y/Y Apr | 9.40% | 10.00% | 10.10% | |

| 2:00 | CNY | Industrial Production Y/Y Apr | 7.00% | 6.40% | 6.00% | |

| 4:30 | JPY | Tertiary Industry Index M/M Mar | -0.20% | 0.00% | ||

| 6:00 | EUR | German GDP Q/Q Q1 P | 0.40% | 0.60% | ||

| 7:15 | CHF | Producer & Import Prices M/M Apr | 0.30% | -0.20% | ||

| 7:15 | CHF | Producer & Import Prices Y/Y Apr | 3.00% | 2.00% | ||

| 8:30 | GBP | Jobless Claims Change Apr | 13.3K | 11.6K | ||

| 8:30 | GBP | Claimant Count Rate Apr | 2.40% | |||

| 8:30 | GBP | Average Weekly Earnings 3M/Y Mar | 2.60% | 2.80% | ||

| 8:30 | GBP | ILO Unemployment Rate 3Mths Mar | 4.20% | 4.20% | ||

| 9:00 | EUR | Eurozone Industrial Production M/M Mar | 0.70% | -0.80% | ||

| 9:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.40% | 0.40% | ||

| 9:00 | EUR | German ZEW Economic Sentiment May | -8.2 | -8.2 | ||

| 9:00 | EUR | German ZEW Current Situation May | 85.2 | 87.9 | ||

| 9:00 | EUR | Eurozone ZEW Economic Sentiment May | 2 | 1.9 | ||

| 12:30 | USD | Empire State Manufacturing May | 15 | 15.8 | ||

| 12:30 | USD | Retail Sales Advance M/M Apr | 0.30% | 0.60% | ||

| 12:30 | USD | Retail Sales Ex Auto M/M Apr | 0.50% | 0.20% | ||

| 14:00 | USD | Business Inventories Mar | 0.10% | 0.60% | ||

| 14:00 | USD | NAHB Housing Market Index May | 70 | 69 | ||

| 20:00 | USD | Net Long-term TIC Flows Mar | 49.0B |

RBA Debelle: 2% is the focal point for wage outcomes now

RBA Deputy Governor Guy Debelle delivered a speech titled "The Outlook for the Australian Economy" at the CFO Forum in Sydney today, where he talked about wages.

He noted that "the experience of other countries with labour markets closer to full capacity than Australia's is that wages growth may remain lower than historical experience would suggest."

Currently in Australia "2% seems to have become the focal point for wage outcomes, compared with 3–4% in the past." Even so, ""there is a risk that it may take a lower unemployment rate than we currently expect to generate a sustained move higher than the 2% focal point evident in many wage outcomes today".

RBA minutes reiterated no strong case for near term hike

RBA May meeting minutes reiterated that central bank's stance that it's not in rush to lift interest rates.

The minuted noted that "stronger growth was expected over the following couple of years, which could reduce spare capacity in the economy and lead to a further gradual decline in the unemployment rate." But, "the increase in wages growth and inflation was expected to be gradual however because spare capacity in the economy was expected to be reduced only slowly."

And, "as progress in lowering unemployment and having inflation return to the midpoint of the target range was expected to be gradual, members also agreed that there was not a strong case for a near-term adjustment in monetary policy."

Trump’s tweet on ZTE prompted bipartisan criticism

Trump's tweet regarding helping China telecoms company ZTE prompted bipartisan criticism and concerns on his softening stance. Republican Senator Marco Rubio said he hoped "this isn't the beginning of backing down to China." Democrat Senator Chuck Schumer said "this leads to the greatest worry, which is that the president will back off on what China fears most - a crackdown on intellectual property theft - in exchange for buying some goods in the short run."

On the other hand, Trump defended with another tweet saying that "ZTE, the large Chinese phone company, buys a big percentage of individual parts from U.S. companies. This is also reflective of the larger trade deal we are negotiating with China and my personal relationship with President Xi".

GBP/USD Basing Above 1.3460 For Next Move

Key Highlights

- The British Pound declined this past week before finding buyers near 1.3460 against the US Dollar.

- There was a break above a crucial bearish trend line with resistance at 1.3520 on the 4-hour chart of GBP/USD.

- The pair may continue to consolidate above 1.3460 before the next move.

- Today, the UK Claimant Count Change for April 2018 will be released, which is forecasted to post 7.5K.

GBPUSD Technical Analysis

The British Pound declined heavily this past week and broke the 1.3800 and 1.3700 support levels against the US Dollar. The GBP/USD pair traded as low as 1.3461, and later started consolidating losses.

The pair is currently trading in a range and it recently tested the 23.6% Fib retracement level of the last decline from the 1.3998 high to 1.3461 low. During the recent upside, there was a break above a crucial bearish trend line with resistance at 1.3520 on the 4-hour chart of GBP/USD.

The pair is currently trading nicely above the 1.3460 pivot level with positive signs. On the upside, the pair faces a major hurdle near 1.3720 and the 50% Fib retracement level of the last decline from the 1.3998 high to 1.3461 low.

The 1.3700/20 area is close to the 100 simple moving average (red), which may act as a strong barrier for buyers should the pair continues to move higher.

A proper break and close above 1.3700/20 is needed for a bullish continuation. On the flip side, the 1.3460 support zone must hold to prevent further slides. Below 1.3460, the pair could test 1.3400 in the near term.

Economic Releases to Watch Today

- German Gross Domestic Product for Q1 2018 (YoY) (Preliminary) – Forecast 1.7%, versus 2.3% previous.

- German Gross Domestic Product for Q1 2018 (QoQ) (Preliminary) – Forecast 0.4%, versus 0.6% previous.

- German ZEW Business Economic Sentiment Index for March 2018 – Forecast -8.2, versus -8.2 previous.

- UK Claimant Count Change April 2018 – Forecast 7.5K, versus 11.6K previous.

- UK ILO Unemployment Rate March 2018 (3M) – Forecast 4.2%, versus 4.2% previous.

- UK Average Earnings Including Bonus March 2018 (3Mo/Year) – Forecast +2.6%, versus +2.8% previous.

- US Retail Sales April 2018 (MoM) – Forecast +0.3%, versus +0.6% previous.

US Ambassador to China Branstad: Trump wants a “dramatic increase” in food exports to China

US Ambassador to China Terry Branstad said in Tokyo today that both countries are still "very far apart" on resolving trade frictions. Branstad, was present at the meeting between Treasury Secretary Steven Mnuchin and Chinese Vice Premier Liu He in Beijing earlier this month. He noted that "there are many areas where China has promised to do but haven't. We want to see a timetable. We want to see these things happen sooner or later."

He added that Trump would like to see a "dramatic increase" in food exports to China and "we'd like to see China being just as open as the United States."

Trade talks will resume today with Liu arrived in Washington.

Yields In Focus , Again

Equity Markets

Equity markets clung on, at least for today, to the easing of trade tensions on the back of President Trumps ZTE reprieve from potentially crushing sanctions. But with US yields again moving higher and the key 10 Year UST nudging above 3 %, it indeed took the wind out of equity investor sails. None the less, the major US indices managed to eke out a positive close despite giving up earlier gains.

Look no further than then the far-reaching inflationary implication of higher oil prices underpinning US yields. Higher oil prices will continue to create the bumpy ride on equity markets, And while supportive of the enormous Oil conglomerate constituents, the cause and effect of higher US interest will most certainly weigh on valuations over a broader market.

While comments from US ambassador to China are on various newswires and he says, “ The United States and China are still “very far apart” on resolving trade frictions. He adds,”China agreed to do a lot of opening up when they joined the WTO, but a lot of the promises were not fulfilled. We want a timetable. We want to see these things happen sooner or later,” he said. Suggeting the divide remains wide

Currency Markets

US fixed income continues to trade offered. German Bunds had bettered those moves after the tepid CPI print which held the dollar bulls back from re-boarding the USD bandwagon. Last week’s weaker US inflation print caused investors to increase their curve flattening positions, where they favour longer-dated Treasuries over shorter-dated issues But with US 10y revisiting the 3 % level, the USD dollar is opening the Asia session with a bounce in its step. But, Traders are decidedly mixed in G-10 flipping positions on a dime as the market continues to trade hypersensitive to US yields. And of course, since no one seems to have a reasonable handle on the trajectory of US interest rates, therefore currency markets remain muddled.

Oil Markets

Oil markets turned bid again on geopolitics. Yemen’s backed Houthis launched missiles at a Saudi Aramco facility, but perhaps the most significant flashpoint is violence that broke out on the Gaza Strip in response to the US’s inauguration of its Jerusalem embassy.

Which has triggered much discussion about the WTI-Brent spread (CLCO1 Index), which has plumbed into deeper negative territory

The gain for U.S. benchmark oil prices wasn’t quite as impressive with traders wary of OPEC’s ability to offset crude supply declines and growing U.S. production. However, the wideners could be part and parcel with Oil traders going through the ritualistic Monday tendency of testing the markets downside resolve by overplaying the jump in Friday rig counts.

But adding the overall bullish narrative are signs that global oil market continues to tighten as the monthly OPEC report suggests a very balanced supply and demand dynamic with stockpiles running a small 9 million barrels above the five-year average.

But in general, the market is wholly focused on the hornet’s nest in the Middle that is an accident waiting to happen.

Gold Prices

Gold prices remain tethered to the hip of the USD which continues to be the most dominating factor driving sentiment. Also, investors are erring on the cautious side ahead of tomorrow Retail Sales, as history has a way of reminding us never to understatement the purchasing power of the US consumer. A better than expected print would give the Federal Reserve more cause to raise interest rates would naturally push the dollar higher. But with US yields testing the 3 % level in 10 Yeas UST, rates are also weighing on Gold sentiment, this despite slightly wobbly equity markets and the abundance of geopolitical headline risk.

Malaysia

The political risk premium has tentatively evaporated after the markets opened and traded reasonably well yesterday on affirmative council appointments made at the weekend, the central bank backstop after BNM reaffirmed it would continue to ensure clean conditions prevail in onshore financial markets, and of course the tight MYR-BCO (WTI) correlation.

But investors are indeed not crashing the gates to increase economic MYR risk; instead, it was the placid open which caused bearish MYR bets along with pre-election hedges to unwind. But the positive Ringgit sentiment came on the back of the local supply where Malaysian dealers were comfortable selling dollars using the BNM as a stop-loss order. Even more telling were the local Pension funds which were on the bid (bond and equity markets) all day providing strong support levels.

At 3.95 the market continues to bake in ~.05 political premium on the back of the GST uncertainty and how the debt agencies perceived scrapping the unpopular tax. But in addition to the to the political risk, ultimately what does matter is the future direction of both the USD and US bond yields. Given the anticipated bumpy ride over the next few weeks, for some, there was not enough of a fire sale to comfortably re-engage the Ringgit, and it remains highly unlikely investors will chase the MYR higher until the all the government’s cards are on the table. Expect some consolidation today.

Currencies Views

EUR: The long and short of it. Interest rate differential continues to drive the bus. While the lower EUR does suggest the ECB would be more willing to raise interest rates sooner than later, members are very guarded with their language not wanting to ignite an EUR rally and traders starts tripping over themselves to get EURUSD topside exposure on a definitive policy shift.

JPY: Providing JPY colour for the past few weeks has been a copy and paste, so why change today. “While US fixed income remains, the primary driver suggesting USDJPY moves to 110 but without a spark on the US inflation front Please make me a believer!!

Gold Trading Sideways, US Retail Sales Next

After a mostly quiet week, gold has continued the trend in the Monday session. In North American trade, the spot price for an ounce of gold is $1319.86, up 0.10% on the day. It’s a very quiet day on the fundamentals front, with no economic indicators on the schedule. On Tuesday, the focus will be on consumers spending, with the release of retail sales and core retail sales.

With the U.S economy continuing to perform well in 2018, it comes as no surprise that the U.S consumer is feeling very optimistic. On Friday, the UoM Consumer Sentiment improved to 98.8 in April, beating the estimate of 98.4 points. The U.S labor market is at near or full employment, which has resulted in a slowdown in job growth due to a shortage of skilled workers. This was underscored last week, as JOLTS Job Openings climbed to a record 6.6 million. At the same time, inflation levels remain low, as the Federal Reserve target of 2 percent remains elusive. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. Inflation levels will be an important factor for the Fed in its monetary policy projection, which remains at two more hikes in 2018. The odds of a rate hike at the June hike stands close to 100%.