Sample Category Title

Eco Data 5/15/18

[php_everywhere instance="1"]

British Pound Higher, Investors Eye U.K Employment Numbers

The British pound has started the week with gains. In the North American session, GBP/USD is trading at 1.3596, up 0.41% on the day. On the release front, there are no economic indicators in the U.K or the U.S. Tuesday will be busy, as the U.K. publishes unemployment claims and wage growth. Over in the U.S, the focus is on retail sales reports.

It was an uneventful week for the pound, and even a rate announcement from the Bank of England didn’t elicit much response from the currency. The markets were on the money with their estimates, correctly predicting that the bank would hold rates at 0.50% and that two of nine MPC members would vote for an immediate rate hike. In the BoE inflation report, policymakers noted concern over softness in consumer borrowing and the housing market. The markets were not surprised by the BoE decision, given the fact that first-quarter growth was just 0.1% and consumer spending and inflation levels weakened. On Friday, there was no relief from the NIESR GDP Estimate, which indicated a 0.1% expansion of the economy in April. Will economic growth rebound in the second quarter? Policymakers are adopting a wait-and-see attitude towards rate hikes, with any increase unlikely before August, which is when the next inflation report will be released.

With the U.S economy continuing to perform well in 2018, it comes as no surprise that the U.S consumer is feeling very optimistic. On Friday, the UoM Consumer Sentiment improved to 98.8 in April, beating the estimate of 98.4 points. The U.S labor market is at near or full employment, which has resulted in a slowdown in job growth due to a shortage of skilled workers. This was underscored last week, as JOLTS Job Openings climbed to a record 6.6 million. At the same time, inflation levels remain low, as the Federal Reserve target of 2 percent remains elusive. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. Inflation levels will be an important factor for the Fed in its monetary policy projection, which remains at two more hikes in 2018. The odds of a rate hike at the June hike stands close to 100%.

Japanese Yen Steady as Japanese Inflation Matches Estimate

The Japanese yen has started the week with small gains, after trading sideways on Friday. In the Monday session, USD/JPY is trading at 109.63, up 0.22% on the day. On the release front, Japanese PPI edged lower to 2.0%, matching the forecast. There are no US economic releases on the schedule. On Tuesday, the U.S releases retail sales and core retail sales.

Has the impressive streak come to an end? Japan has boasted eight consecutive quarters of economic growth, but the first quarter appears likely to buck the trend. The economy is expected to contract at an annualized rate of 0.2% in Q1, compared to strong growth of 1.6% in the fourth quarter. The sharp slowdown is being attributed to weak consumer spending and softer global demand for Japanese exports. Still, analysts are viewing the Q1 report card as a temporary blip, with second-quarter expected to rebound with annualized growth of 1.0%.

With the U.S economy firing on all cylinders, the U.S consumer is feeling very optimistic. On Friday, the UoM Consumer Sentiment improved to 98.8 in April, beating the estimate of 98.4 points. The U.S labor market is at near or full employment, which has resulted in a slowdown in job growth due to a shortage of skilled workers. This was underscored last week, as JOLTS Job Openings climbed to a record 6.6 million. At the same time, inflation levels remain low, as the Federal Reserve target of 2 percent remains elusive. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. Inflation levels will be an important factor for the Fed in its monetary policy projection, which remains at two more hikes in 2018. The odds of a rate hike at the June hike stands close to 100%.

Dow shrugs off yield rise, heading to 25000

DOW opens higher on some optimism over US-China trade talk. Rise in treasury yields is shrugged off by investors. 10 year yield is back above 2.99 and hit at high as 2.997 so far. But there is no impact on stocks so far.

For now 25000 is the next handle to overcome. But based on current momentum, the real hurdle is between 25800.35 resistance and 78.6% retracement of 26616.71 to 23360.29 at 25919.83. We'll keep monitoring the momentum to see if rise from 23531.31 is developing into an impulsive move to resume the larger up trend. For now, it's early to tell.

China on the Receiving End of Important Data; Global Trade and Aussie also in Focus

Chinese data on April’s fixed asset investment, industrial production and retail sales will be made public on Tuesday at 0200 GMT. Meanwhile, the aussie, which is widely viewed as a liquid proxy for China’s economy, will also be in focus as the numbers hit the markets. The currency is currently attempting a recovery versus the greenback after touching an 11-month low in the week that preceded.

Retail sales and fixed asset investment in urban areas are projected to have marginally eased in the year to April, growing by 10.0% and 7.4% respectively, versus March’s corresponding figures of 10.1% and 7.5%. Industrial production, on the other hand, is forecast to grow by 6.3% y/y, a faster pace compared to the previous month’s 6.0%.

The Chinese government has set a target for annual GDP growth to stand around 6.5% in 2018, the same as in 2017 when actual growth exceeded expectations to come in at 6.9%. One of the factors, though, contributing to a stronger expansion in the previous year was record-high bank lending. Policymakers, however, have vowed to clamp down on excessive lending, that has the capacity to fuel a credit bubble, in an effort to shift focus on the quality of growth rather than merely the quantity. In this respect, the above data might be negatively affected on the face of reduced loan availabilty. In the bigger picture though, such a deceleration is long-term positive so long as it minimizes the risks of a widespread credit crisis.

Turning to reaction in the FX markets, besides the yuan, the aussie will also be gathering attention as the abovementioned numbers go public. The Australian currency is seen by investors as a liquid proxy for China’s economy due to the close economic ties between China and Australia – the former is the latter’s largest export and import partner. Focusing on aussie/dollar, the pair came close to 0.74 last week, its lowest since June last year. It subsequently posted some gains and is currently trading roughly 150 pips above last week’s low. Strong readings out of China might allow the pair to extend its recovery.

A positive surprise in the figures could spur long aussie/dollar positions, with resistance to advances potentially coming around the 23.6% Fibonacci retracement level of the January 26 to May 9 downleg at 0.7581 – the region around this point also includes the 0.76 round figure. In case of a break to the upside, an additional barrier might be formed around the 38.2% Fibonacci mark at 0.7687. Notice that the area around this level also includes the current level of the 50-day moving average at 0.7676, as well as the 0.77 handle.

Conversely, a data miss might spur selling pressure in AUDUSD. Support to losses could initially come from the 0.75 round figure, with steeper losses starting to increasingly turn the attention to Wednesday’s 11-month low of 0.7410.

Lastly, trade developments cannot be taken out of the equation. Overall, China seems to be indeed rebalancing into an economy that increasingly relies on domestic demand, however economic activity remains largely driven by export growth. A threat to this are trade disputes between the US and China. On this front, it is encouraging that President Trump ordered the US Commerce Department to help Chinese telecommunications giant ZTE to get back into business. This comes a few weeks after the company was forced to suspend its operations as the Commerce Department banned US companies from selling it components on the back of “egregious” behavior. Moreover, Chinese Vice Premier Liu He is anticipated to be in Washington this week for more trade talks.

If discussions between the world’s two largest economies turn out to be fruitful, deviating from the narrative of protectionism, then risk assets are likely to attract funds. The aussie dollar is one of the currencies standing to gain due to Australia’s status as a major commodity exporter; barriers to trade can weigh on the currency and vice versa. Also of importance for aussie traders as the week unfolds, is the release of Australian data on employment on Thursday, while tomorrow the RBA will publish the minutes pertaining to its latest monetary policy meeting.

Sunset Market Commentary

Markets:

Global core bonds lost some ground today with German Bunds underperforming US Treasuries. Rising EMU inflation expectations and comments by ECB Villeroy were at play. The EMU 5y5y inflation forward trades at 1.72%, the highest level since February. German construction workers over the weekend reached agreement over a 6% pay hike and provide more anecdotic evidence that inflation pressures are building. IGM and the public sector already reached pay deals earlier this year. ECB Villeroy clarified the ECB’s current forward guidance on rates (rates will remain low well past the end of net asset purchases). “Well past” means that a first rate hike could come some quarters after ending net bond buying, but not years. Markets currently only discount a positive 3-month Euribor-rate by the end of 2019. Villeroy also suggested that APP will end in September or December. He blames the Q1 growth slowdown to temporary factors, but warned that growth rate can’t accelerate forever. ECB Lautenschlaeger and Mersch didn’t touch on monetary policy, while Praet repeated last week’s speech. ECB Coeuré speaks tonight. Cleveland Fed Mester, who votes on monetary policy this year, aligned with the ‘gradual’ dot plot. The US eco outlook is positive and inflation will remain at a sustained 2% over the next 1-2 years.

German yields add 1.7 bps (2-yr) to 4.3 bps (10-yr). Changes on the US yield curve range between + 1.3 bps (2-yr) and +2 bps (10-yr). The US 10-yr yield remains close to, but below the psychological 3% mark. The moves on rate markets gave the euro a slight edge over the dollar with EUR/USD up from 1.1950 overnight to the 1.1980 area currently. EUR/GBP on the other hand traded listless around the 0.8820 pivot ahead of tomorrow’s Brexit cabinet meeting to discuss plans for a post-withdrawal customs union. 10-yr yield spreads vs Germany narrowed up to 3 bps. Last week’s underperformance of BTP’s ended even if a populist Lega-5SM coalition is about the get the green light from President Mattarella. Greek bonds don’t react to rumours that the country’s debt agency plans to tap the market twice this year, including a first 10-yr issue for a decade.

News Headlines:

The Catalan parliament has voted committed separatist Joaquim Torra as the region’s new leader, ending a five-month political deadlock and setting the stage for fresh confrontations between Barcelona and Madrid. (FT)

A global oil glut has been virtually eliminated, according to OPEC figures, thanks in part to an OPEC-led supply cut deal in place since January 2017 and fast-rising global demand. Oil inventories in developed nations in March fell to 9 million barrels above the five-year average. That's down from 340 million barrels above the average in January 2017. (Reuters)

UK PM May will focus on negotiating a backstop plan to avoid a hard border between the UK and Ireland as the battle inside her Cabinet over a Brexit trade plan drags on. Discussions among senior ministers over how closely to mirror the EU’s tariff and customs rules after Brexit will probably last for at least another two weeks, according to an official. With that in mind, the summit of EU leaders at the end of June is likely to focus on finding an insurance plan that would avoid a hard border, if no other arrangements are in place, the official said.

Total EMU investment (both from the public and the private sector) was equivalent to 20.5% of GDP last year. That’s 2.7 percentage points below pre-crisis levels (23.2% in 2007).

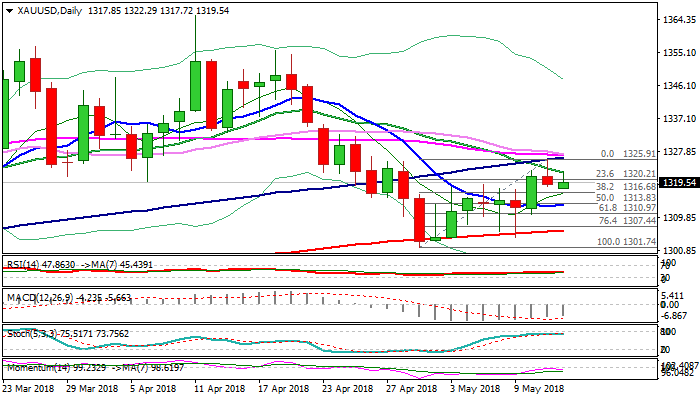

SPOT GOLD – Break Through $1316 or $1322 Pivots to Generate Clearer Direction Signal

Gold price dipped to $1317 low on Monday, remaining at the back foot following Friday’s strong upside rejection at $1325 and daily close in red.

Dip was so far contained by thick hourly cloud and found temporary footstep just ahead pivotal $1316 support (Fibo 38.2% of $1301/$1325 upleg).

Upside attempts today were capped by falling 20SMA ($1322) which also marks Fibo 38.2% of $1355/$1301 fall, barrier that was repeatedly cracked but bulls failed to close above and generate bullish signal.

mixed signals from daily studies show no clear near-term direction, as 10SMA/slow stochastic turn north, while momentum is losing traction, falling 20SMA caps for now, while converging 30/55/100SMA’s are on track to form multiple bull-cross.

Initial bullish signal could be expected on close above $1322, while confirmation of bullish continuation needs firm break above a cluster of MA’s at $1327 zone.

Conversely, close below $1316 Fibo support would weaken near-term structure and risk extension towards $1313/11 pivots (10SMA/Fibo 61.8% of $1301/$1325 upleg).

Res: 1322; 1325; 1327; 1335

Sup: 1316; 1313; 1311; 1307

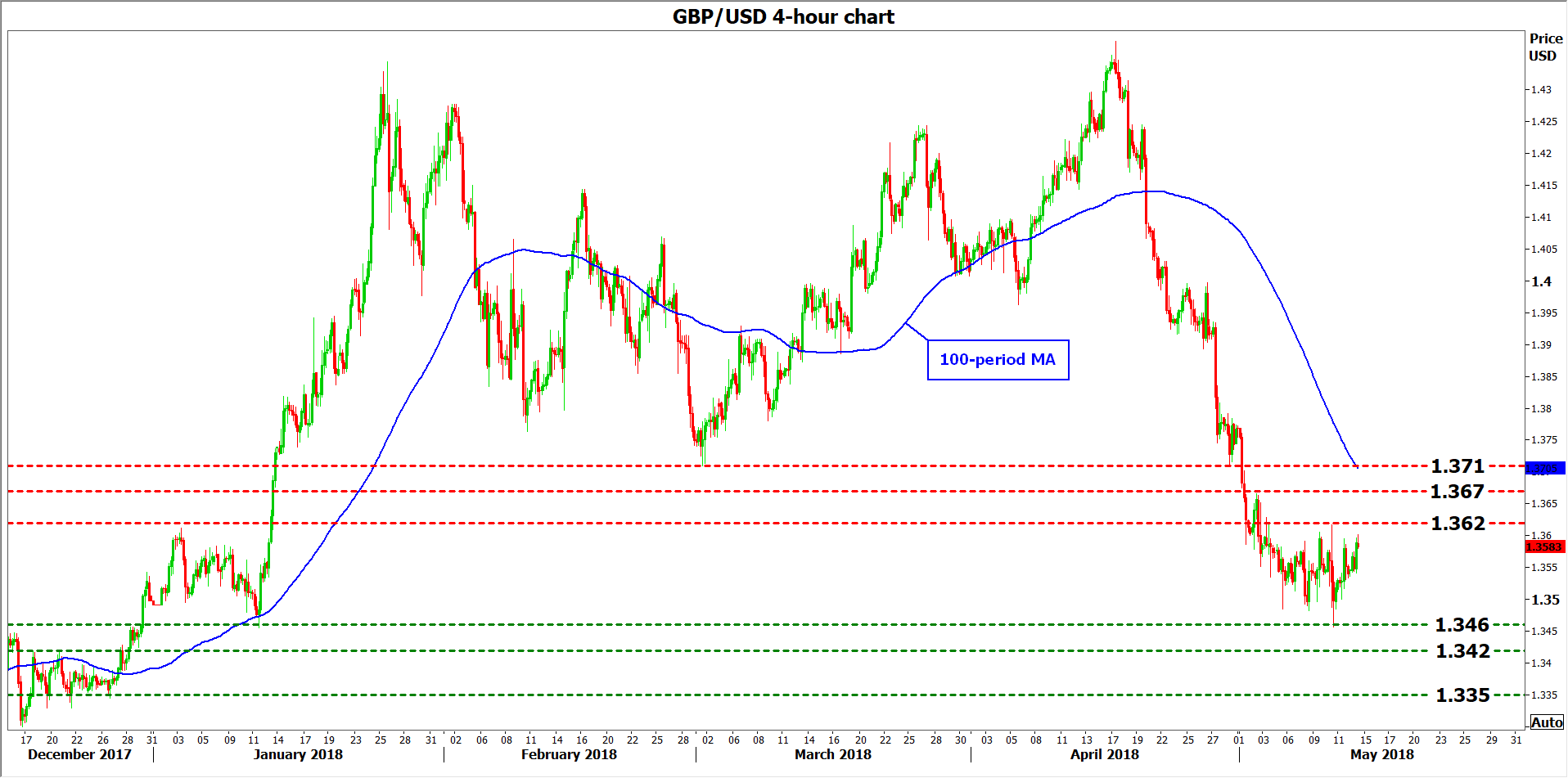

Sterling Looks to UK Jobs Data for Relief

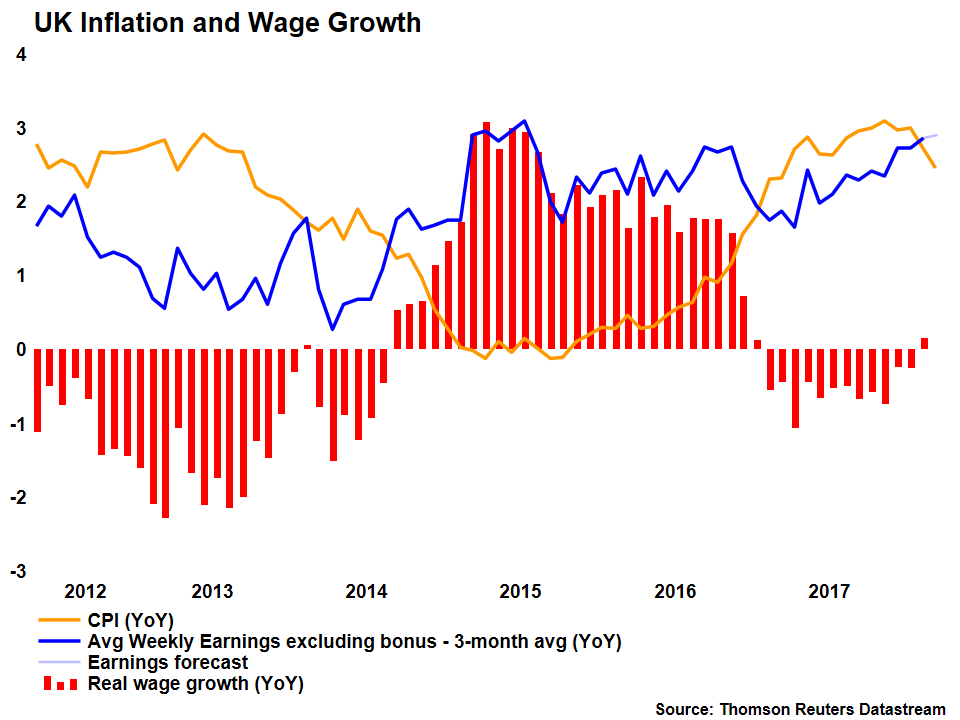

The UK will release its employment figures for March on Tuesday, at 0830 GMT. Forecasts point to further progress in the labor market, which would likely be encouraging news for Bank of England (BoE) policymakers, who appeared quite cautious recently. A strong set of data could revive speculation for a near-term rate increase by the Bank, and perhaps help sterling to recover some of its latest losses.

The British pound has taken a beating over the past month, after a streak of disappointing economic data for Q1 diminished expectations for a near-term rate increase by the BoE, and led the Bank to shift to a more cautious stance at its policy gathering last week. The BoE signaled it will take the sidelines for some time while it monitors incoming data and assesses whether the economy’s Q1 softness was temporary, or owed to more persistent factors. Against this backdrop, investors will look to the employment figures for March – and predominantly on wage growth – for fresh signals on how the Bank may act at its upcoming meetings.

In March, the UK unemployment rate is projected to have held steady, after ticking down to a multi-decade low of 4.2% in February. As for average weekly earnings, forecasts are mixed. The figure including bonuses is projected to have cooled to 2.6% year-on-year from 2.8% in February, but the rate excluding bonuses is expected to have risen to 2.9%, from 2.8% previously. Although both measures are important, the BoE tends to pay more attention to the print that strips out bonuses, as bonus pay tends to be volatile.

Gauges of the labor market were rather upbeat in March. The Markit UK Report on Jobs showed another sharp increase in permanent staff placements, supporting the forecast for an unchanged unemployment rate. On wages, the survey found that temporary staff pay rose at the quickest pace since last September, adding credence to expectations for an acceleration in wage growth.

At the time of writing, the implied probability for the BoE to raise rates at its August meeting rests at 42%. A positive surprise in these data – for instance a downtick in the unemployment rate or a greater-than-expected acceleration in earnings – could push that probability higher and thereby, help the pound recover some of its recent losses. Looking at sterling/dollar, advances in the pair may encounter immediate resistance near 1.3620, the high of May 10. Further up, sell orders may be found at 1.3670, the top from May 2, and subsequently at the April 30 low of 1.3710.

On the other hand, and in case of a disappointment in these figures, support to declines in Cable may be found initially at 1.3460, a hurdle that halted the May 10 decline. A downside break of that zone would open the way for 1.3420, defined by the peak of December 20. If the bears overcome that area too, the December 26 low of 1.3350 may come into play.

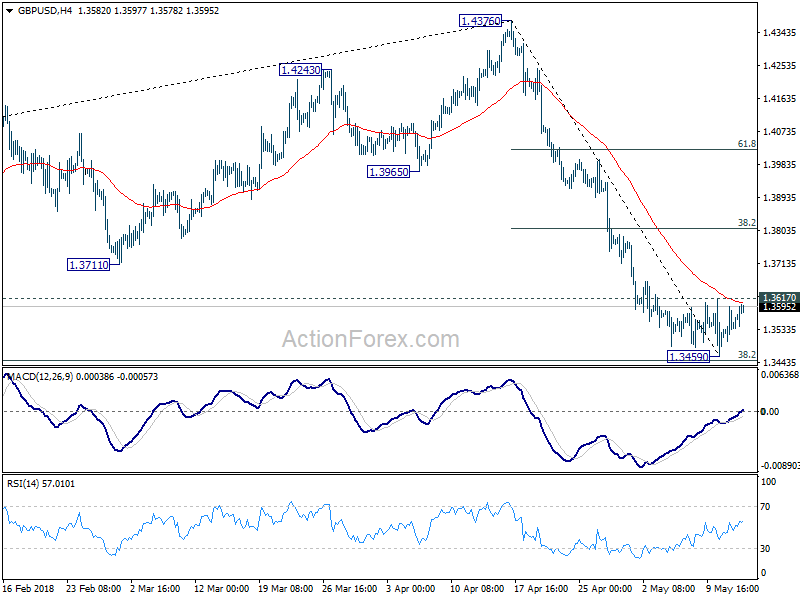

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3493; (P) 1.3545; (R1) 1.3588; More...

Intraday bias in GBP/USD remains neutral as consolidation from 1.3459 short term bottom continues. Break of 1.3617 will turn bias to the upside for stronger recovery. But upside should be limited by 38.2% retracement of 1.4376 to 1.3459 at 1.3809. On the downside, sustained break of 1.3448 fibonacci level will confirm resumption of whole fall from 1.4376 and target next fibonacci level at 1.2874.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 was almost met. Break there will target 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3861) holds, even in case of strong rebound.

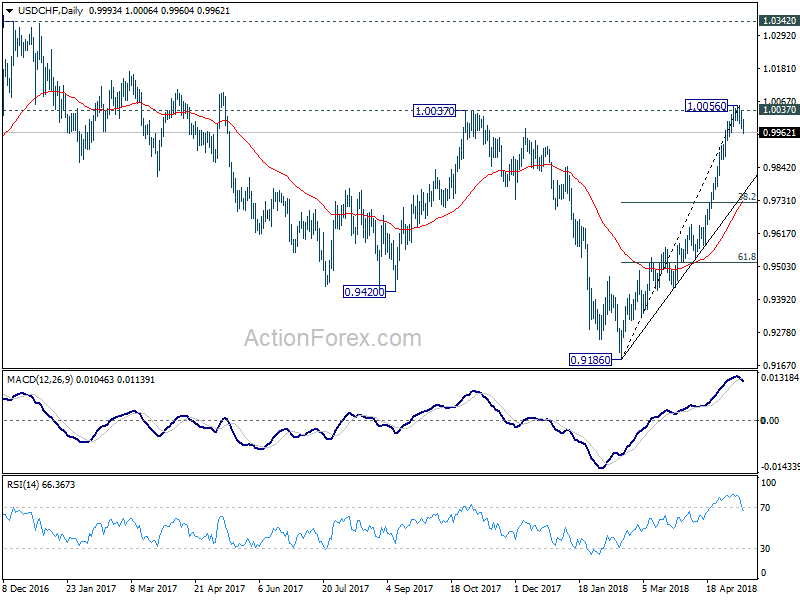

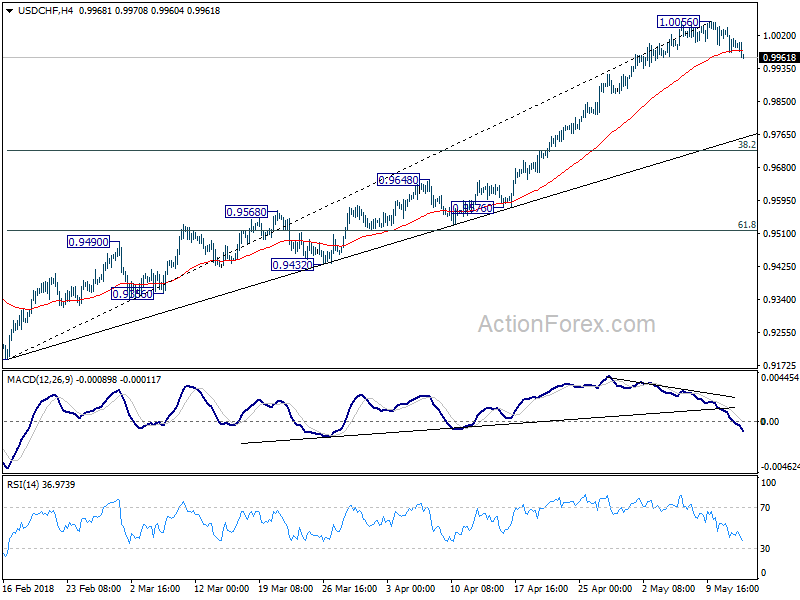

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9968; (P) 1.0004; (R1) 1.0032; More...

Intraday bias in USD/CHF remains on the downside as correction from 1.0056 is in progress. Deeper fall would be seen to trend line support (now at 0.9764). At this point, we'd expect strong support from there to bring rally resumption. On the upside, sustained break of 1.0037 will resume recent rise for 1.0342 key resistance next.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.