Sample Category Title

China Industrial Production Beats Expectations

General Trend:

- Asian indices trade generally lower: Hang Seng on track for first decline in 7 days

- MSCI announces China A-share index changes ahead of June 1st additions to the EM index

- Tencent is expected to report quarterly earnings on Wednesday, May 16th

- Australia’s Bluescope Steel raises H2 outlook on strength in US operations

- Japanese megabank SMFG rises over 2%, announced FY outlook and buyback

- China April industrial production growth accelerates, beat ests

- China April YTD fixed asset investment below ests: Gov’t notes moves to clean up certain infrastructure projects

- US Ambassador to China says both countries are still very far apart on trade

- Moody’s suggests China could disrupt its economy if it meets US trade surplus reduction demand of $200B

- PBoC injects cash in open market operation (OMO), as no reverse repos matured

- Few surprises seen in RBA minutes, reiterates rate comments; Assistant Gov Debelle notes recent decline in money market rates

- Australian interest rates track Monday’s increase in US Treasury yields

- Malaysian assets trade calmly on session vs. recent election related volatility

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.1%; closed -0.2%

- Topix Real Estate index -2.3%, Securities -0.6%; Iron & Steel +0.4%

- Megabanks trade broadly higher with earnings in focus

- (JP) Japan is considering tax reductions on home and vehicle purchases to ease the sting of a consumption tax hike planned for next year - Nikkei

- Nissan Motors, [+0.7%], 7201.JP Reports FY17/18 Net ¥747B v ¥727Be; Op ¥574.8B v ¥566.4Be; Rev ¥12.0T v ¥12.0Te (after the close yesterday)

- Toshiba, [+1.2%], 6502.JP Reports FY17/18 Net ¥804B v ¥ y/y; Op ¥64.1B v ¥ y/y; Rev ¥3.95T v ¥4.87T y/y, to conduct 10 to 1 reverse stock split

- (JP) Japan MoF sells ¥699B v ¥700B indicated in 0.8% (0.8% prior) 30-yr bonds; Avg yield: 0.746% v 0.714% prior; Bid to cover: 4.41x v 4.34x prior

Korea

- Kospi opened 0.0%

- (KR) South Korea Apr Export Price Index M/M: 0.0% v -0.9% prior; Y/Y: -2.0% v -0.9% prior; Import Price Index M/M: 1.2% v 0.5% prior; Y/Y: 4.0% v 3.1% prior

- (KR) Satellite imagery shows North Korea has begun dismantling the Punggye-ri Nuclear test site - 38North

- (KR) South Korea Unification Ministry confirms high level talks with North Korea on May 16th

China/Hong Kong

- Hang Seng opened +0.1%, Shanghai Composite +0.2%

- Hang Seng Info Tech index -2%, Industrial Goods -1%, Financials -0.9%; Telecom +0.2%

- (CN) MSCI: 234 large cap mainland China companies to be added to EM and China indexes; The 234 A-shares will have a combined market cap of ~$22.0B

- (CN) US Ambassador to China Branstad: China and US still very far apart on trade; President Trump wants 'dramatic' increase in farm exports to China

- (CN) US Pres Trump tweets: "ZTE, the large Chinese phone company, buys a big percentage of individual parts from U.S. companies. This is also reflective of the larger trade deal we are negotiating with China and my personal relationship with President Xi."

- (CN) CHINA APR INDUSTRIAL PRODUCTION Y/Y: 7.0% V 6.4%E

- (CN) CHINA APR RETAIL SALES Y/Y: 9.4% V 10.0%E

- (CN) China PBoC Open Market Operation (OMO): Injects CNY180B in 7-day and 14-day reverse repos v skips prior; Net injects CNY180B

- (CN) China PBoC sets yuan reference rate 6.3486 v 6.3345 prior

- (CN) China State Council senior adviser Xia Bin: China’s financial risk greater than official numbers suggest - SCMP

- (CN) Moody's: China unlikely to meet US demands on bilateral trade

- (CN) China Apr Surveyed Jobless Rate: 4.9% v 5.1% prior

- (CN) China Apr Fixed Assets Urban YTD y/y: 7.0% v 7.4%e

- (CN) China NBS Comments on April data: Economy steadied with improvement in April; US/China trade frictions have yet to show impact on domestic economy

- (CN) MSCI: 234 large cap mainland China companies to be added to emerging markets (EM) and China indexes on June 1st

- (HK) Hong Kong Monetary Authority (HKMA) Chief Chain reiterates has confidence to maintain stable HKD peg; HK$ falls to lower end of trading band

- (HK) Two China bitcoin mining equipment makers planning to IPO in Hong Kong this year - press

Australia/New Zealand

- ASX 200 opened +0.1%, closed -0.5%

- ASX 200 Telecom index -4.6% (Telstra -5.6%), Utilities -1.5% Energy -0.9%, Resources -0.8%, Financials -0.3%

- (AU) RBA Deputy Gov Debelle: Sees no pressure to raise rates; economy is on a slowly improving trajectory, but that doesn't make a case for raising interest rates in the near term - The Outlook for the Australian Economy – at the CFO Forum

- (AU) Reserve Bank of Australia (RBA) April Meeting Minutes: members agreed that it was more likely that the next move in the cash rate would be up, rather than down

- (AU) Australia AOFM prices A$1.7B in June 2019 bonds through syndication; yield to maturity 3.205%

Other Asia

- Taiwan's Hon Hai declines over 1% after Q1 profits missed ests

- (VN) Fitch raises Vietnam sovereign rating to BB from BB-; Outlook Stable

North America

- (CA) Canada PM Trudeau's office: Pres Trump and PM Trudeau discussed in call the possibility of reaching a prompt conclusion of NAFTA deal - press

- TSLA, Engineers said to have has concerns about autopilot before first fatal crash; had wanted to add sensors to keep drivers attentive, but CEO Musk and other executives said no, citing costs - financial press

Europe

- (UK) UK Labour Leader Corbyn said to rule out ‘Norway-style’ Brexit option – UK Press

- (EU) European Commission is considering invoking a 19th century law to prohibit European companies from submitting to US sanctions, in the event they are imposed as a result of its withdrawal from the Iranian nuclear pact

German press

- (EU) ECB's Coeure: divergence between our key policy rates and market rates could become more important in the future once policy rates begin to normalize

- First Group [FGP.UK]: The co. is being urged to consider a full sale, along with other options - UK Press

- Carrefour Brazil reported Q4 (BRL) Net 596M v 494Me; Rev 13.7B v 13.8Be

Levels as of 02:00ET

- Hang Seng -1.2%; Shanghai Composite -0.2%; Kospi -0.8%

- Equity Futures: S&P500 -0.2%; Nasdaq100 -0.2%, Dax -0.2%; FTSE100 -0.2%

- EUR 1.1938-1.1912; JPY 109.92-109.66; AUD 0.7537-0.7508;NZD 0.6928-0.6892

- Jun Gold -0.5% at $1,311/oz; Jun Crude Oil +0.0% at $70.95/brl; Jul Copper -0.3% at $3.08/lb

German GDP growth slowed to 0.3% qoq in Q1, Swiss PPI rose to 2.7% yoy in March

First batch of data in European session saw German GDP rose 0.3% qoq, 2.3% yoy in Q1, below expectation of 0.4% qoq, 2.4% yoy. That's also notably slower than Q4's 0.6% qoq, 2.9% yoy. But nonetheless, the figures are decent.

Swiss PPI rose 0.4% mom, 2.7% yoy, in April, up from March's -0.2% mom, 2.0% yoy.

UK employment data are upcoming. In particular, unemployment rate is expected to be unchanged at 4.2% in March. Average weekly earnings are expected to grow 2.6% 3m/y.

Eurozone will also release industrial production, GDP. More focus will be on German ZEW economic sentiment.

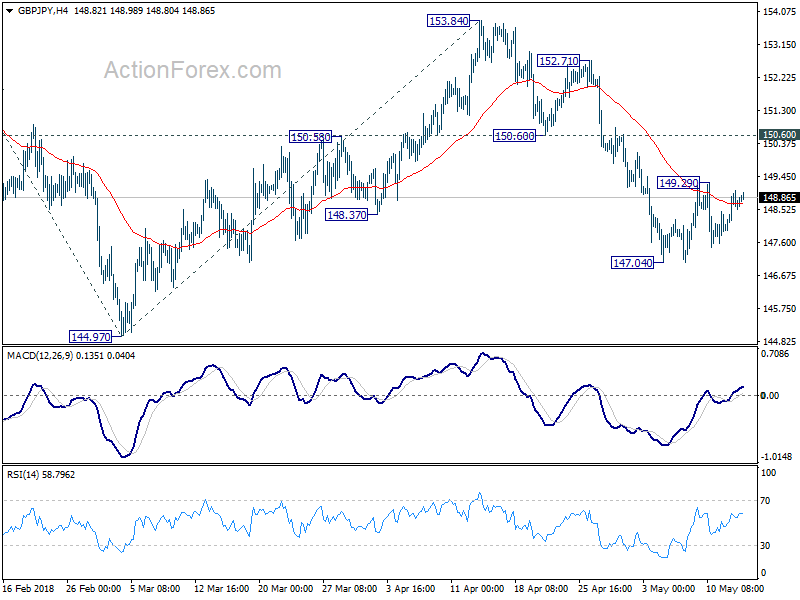

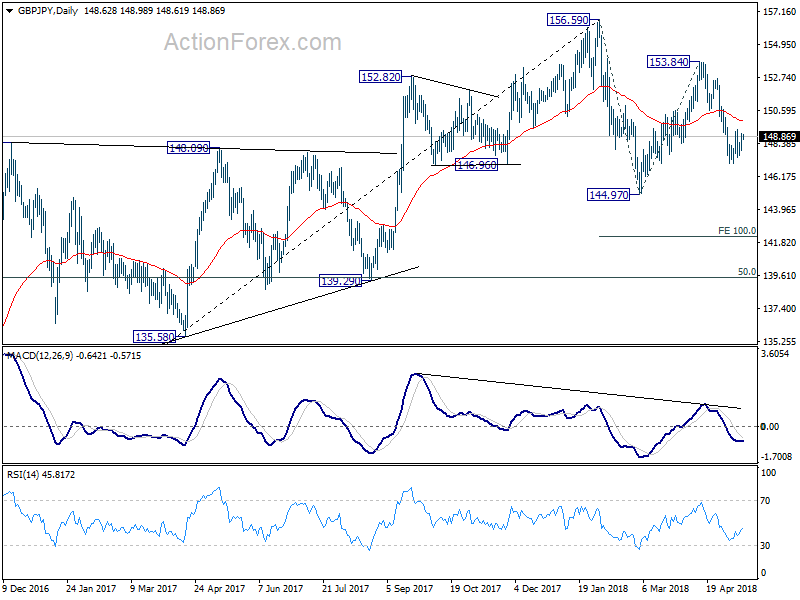

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.03; (P) 148.55; (R1) 149.15; More...

Intraday bias in GBP/JPY remains neutral for the moment. Consolidation from 147.04 temporary low could extend. But upside should be limited below 150.60 support turned resistance to bring fall resumption. Below 147.04 will target 144.97 first. Break there will resume the fall from 156.59 and target 100% projection of 156.59 to 144.97 from 153.84 at 142.22 next.

In the bigger picture, for now, we're treating price actions from 156.59 as a corrective move. Therefore, while deeper fall is expected, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. There is still prospect of extending the rise from 122.36. However, considering that GBP/JPY failed to sustain above 55 month EMA (now at 153.94), firm break of 139.29 will confirm trend reversal and turn outlook bearish.

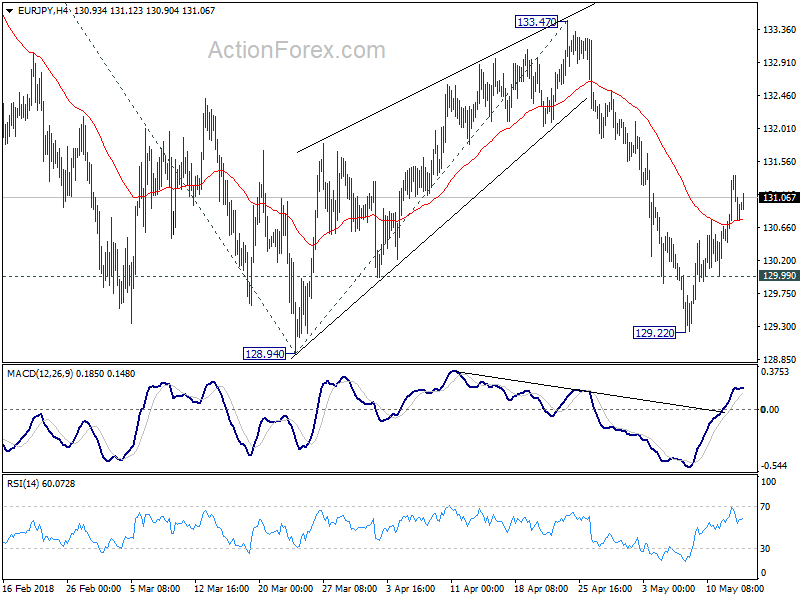

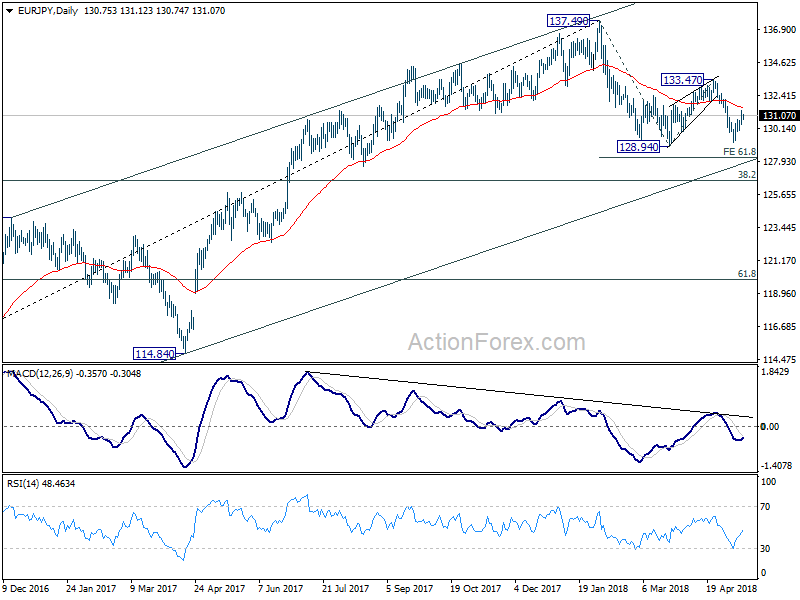

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.39; (P) 130.88; (R1) 131.27; More....

With 129.99 minor support intact, EUR/JPY's rebound from 129.22 could extend higher, possibly to 55 day EMA (now at 131.59). But we'd expect strong resistance below 133.47 resistance to bring fall resumption. Below 129.99 minor support will turn bias back to the downside for 128.94. Break will resume the corrective fall from 137.49 and target 61.8% projection of 137.49 to 128.94 from 133.47 at 128.18 next.

In the bigger picture, for now, price actions from 137.49 are viewed as a corrective pattern only. Hence, while, deeper decline would be seen, strong support is expected at 38.2% retracement of 109.03 to 137.49 at 126.61 to contain downside and bring rebound. Up trend from 109.03 (2016 low) is expected to resume afterwards. Though, sustained break of 126.61 will be an important sign of trend reversal and will turn focus to 124.08 resistance turned support.

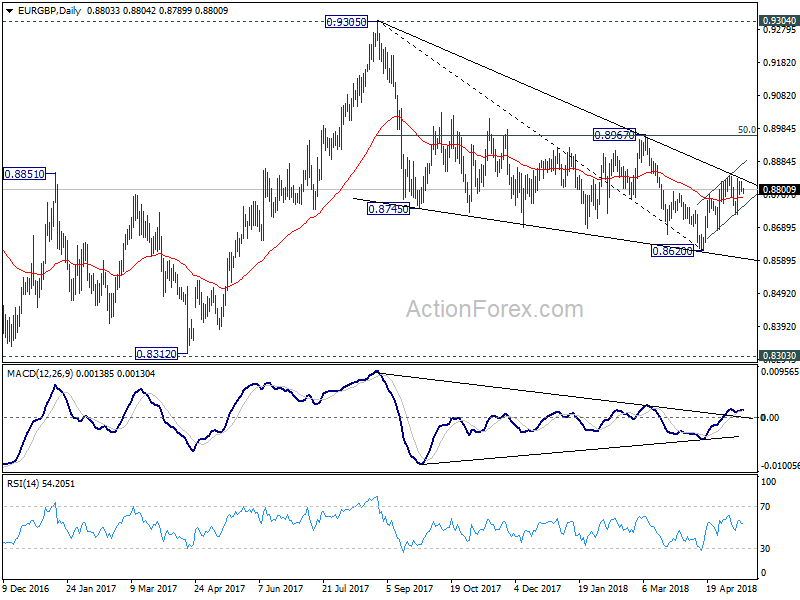

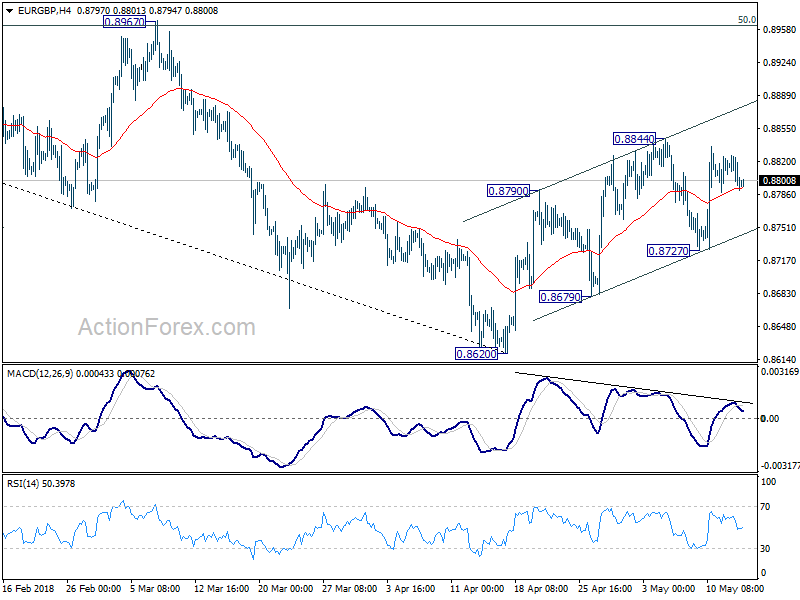

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8786; (P) 0.8808; (R1) 0.8820; More...

Intraday bias in EUR/GBP stays neutral for the moment and near term outlook is a bit mixed. On the upside, break of 0.8844 will revive the case of bullish trend reversal. Intraday bias will be turned back to the upside for 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963) to confirm. On the downside, however, below 0.8727 will target a test on 0.8620 low instead.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

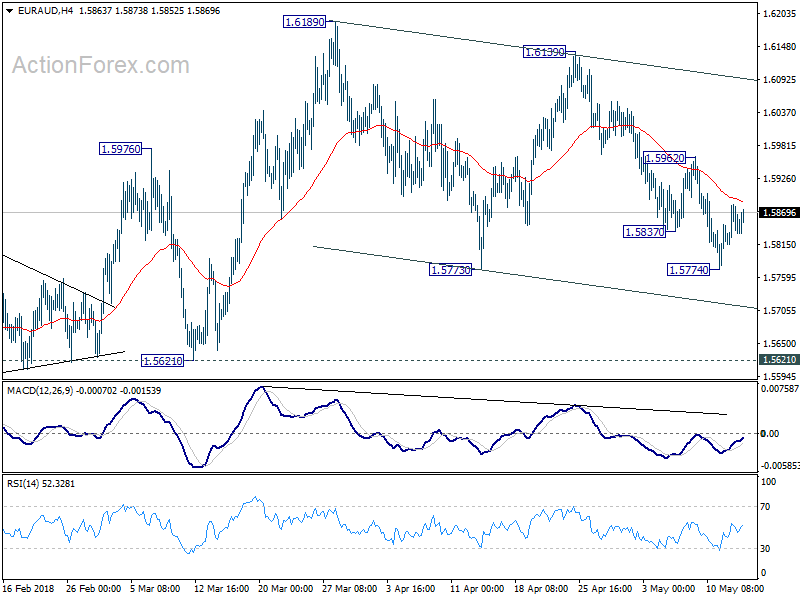

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5815; (P) 1.5850; (R1) 1.5886; More....

Intraday bias in EUR/AUD remains neutral at this point. Consolidation pattern from 1.6189 is till unfolding. Deeper decline could be seen through 1.5773 support. But we'd expect downside to be contained above 1.5621 support to bring rebound. On the upside, above 1.5962 will turn bias to the upside for 1.6139 resistance and above.

In the bigger picture, while there is bearish divergence condition in daily MACD, there is no clear sign of reversal yet. Current rally from 1.3624 could extend to 1.6587 key resistance (2015 high). Nonetheless, we'd expect further loss of upside momentum, and strong resistance from 1.6587 to limit upside and bring reversal. On the downside, sustained break of 1.5621 support should confirm reversal and turn outlook bearish for 1.5153 support and below.

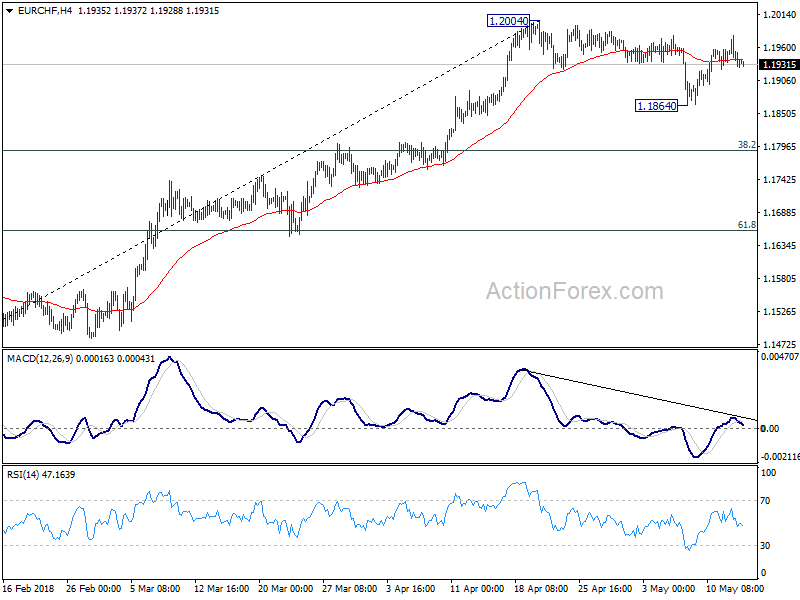

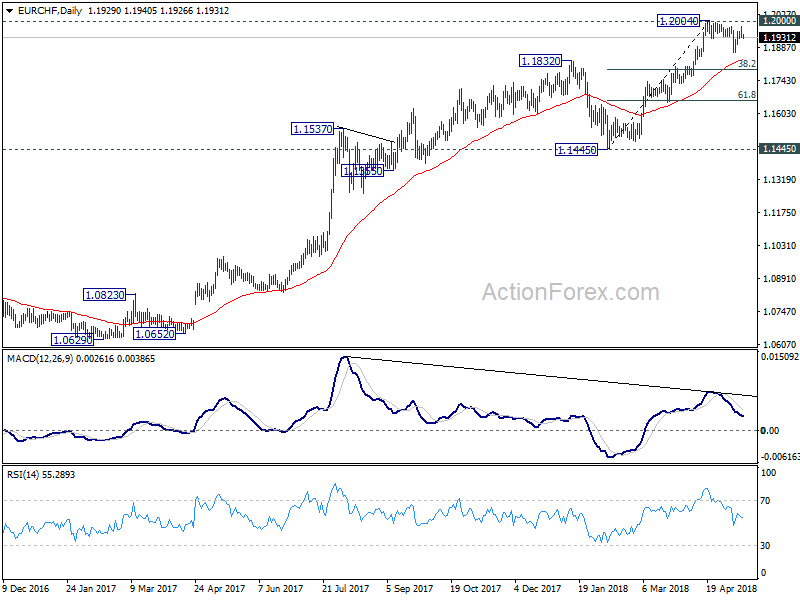

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1913; (P) 1.1949; (R1) 1.1968; More...

EUR/CHF is still struggling in range below 1.2004 and intraday bias remains neutral. Consolidation could extend with risk of deeper pull back. But in that case, we'd expect strong support from 38.2% retracement of 1.1445 to 1.2004 at 1.1790 to contain downside and bring rebound. On the upside, decisive break of 1.2004 will confirm up trend resumption.

In the bigger picture, long term up trend in EUR/CHF is still in progress. Prior SNB imposed floor at 1.2000 was already met but there is no sign of reversal yet. As long as 1.1445 support holds, we'd expect the up trend to extend to 2013 high at 1.2649 next. However, considering bearish divergence condition in daily MACD. Break of 1.1445 will be an indication of medium term reversal and will turn outlook bearish.

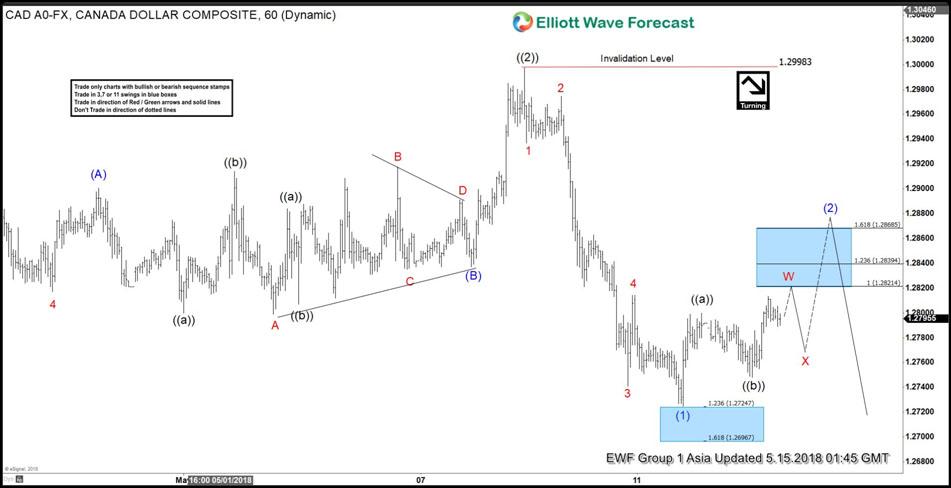

Elliott Wave View: USDCAD Correction May Fail For Extension Lower

USDCAD Short Term Elliott Wave view suggests that the rally to 1.2998 on May 08,2018 high ended Primary wave ((2)). The internals of Primary wave ((2)) unfolded as a Zigzag Elliott Wave structure where Intermediate wave (A) ended at 1.29. Afterwards, the sideways consolidation to 1.2837 low ended Intermediate wave (B) as a triangle Elliott Wave structure and rally to 1.2998 high ended Intermediate wave (C) of ((2)).

Down from there, Primary wave ((3)) remains in progress as an Impulse Elliott Wave structure. Internals of Wave (1) of ((3)) subdivided as an impulse structure of a lesser degree. Minor wave 1 ended at 1.2937, Minor wave 2 ended at 1.2975, Minor wave 3 ended at 1.2741 low. Minor wave 4 ended at 1.2814 and Minor wave 5 of (1) ended at 1.2725 low. Above from there, Intermediate wave (2) of ((3)) remains in progress to correct cycle from 5.8.2018 high and expected to do a double correction in 7 swing structure.

Near-term focus remain towards 1.2821 – 1.2839, which is 100% – 123.6% Fibonacci extension area of ((w))-((x)), to end Minor wave W. Pair should then do a 3 wave pullback in Minor wave X before another leg higher in Minor wave Y of (2) takes place. As far as a pivot at 5.8 high (1.2998) remains intact, pair should eventually resume lower. We don’t like buying the pair into the proposed rally.

USDCAD Elliott Wave 1 Hour Chart

Bond Markets Fell, As Bund Yields Rose 5bps

Market movers today

Most of this week's key data is being released today. US retail sales for April are expected to show a decent rise of 0.4% m/m for the core measure (control group). US private consumption was soft at the beginning of the year but is expected to recover in Q2. However, the recent rise in oil prices could postpone a rebound in private consumption. The US is also due to release the Empire index; the first regional survey for April.

German ZEW expectations survey was very weak in April, which may be partly related to the uncertainty over a potential US-China trade war. Consensus looks for a stabilisation in the index in May at -8.2.

In the UK. It is time for the labour market report for March. Month-on-month wage growth has been remarkably stable in recent months and we estimate another increase of 0.2% m/m, taking the annual growth in average hourly earnings ex bonuses (3M average) to 2.9% y/y from 2.8%. The unemployment rate (3M average) is expected to remain at 4.2% but risk is skewed towards a fall to 4.1%.

Norway is due to release Q1 GDP data, see page 2.

Selected market news

ECB Governing Council member Francois Villeroy de Galhau commented that the first rate hike would come some quarters and not years after the end of QE. He also quipped that the exact timing of the end of QE was ‘not a deep existential question'. Bond markets fell, as Bund yields rose 5bps. We are surprised by the market reaction, as Villeroy's commentary is in line with previous ECB commentary (see more on page 2).

Italy is close to forming a coalition government between the Five Star Movement and League parties. However, last minute hiccups have emerged such as choosing a prime minister. Some very radical populist ideas are being floated such as flat income tax at 15% (League) and guaranteed income for the poor (Five Star). These ideas will not sit well in Brussels or the bond market.

In terms of market reaction, after years of fear over a populist government in Italy, the bond market reaction has the distinct air of nonchalance. Italian bond yields have risen only moderately over other periphery or core debt. Or as Villeroy de Galhau might say, the bond market does not view the composition of Italian government as a deep existential question.

Euro Trading A Tad Higher, Ahead Of Key Economic Releases Across The Euro-Zone

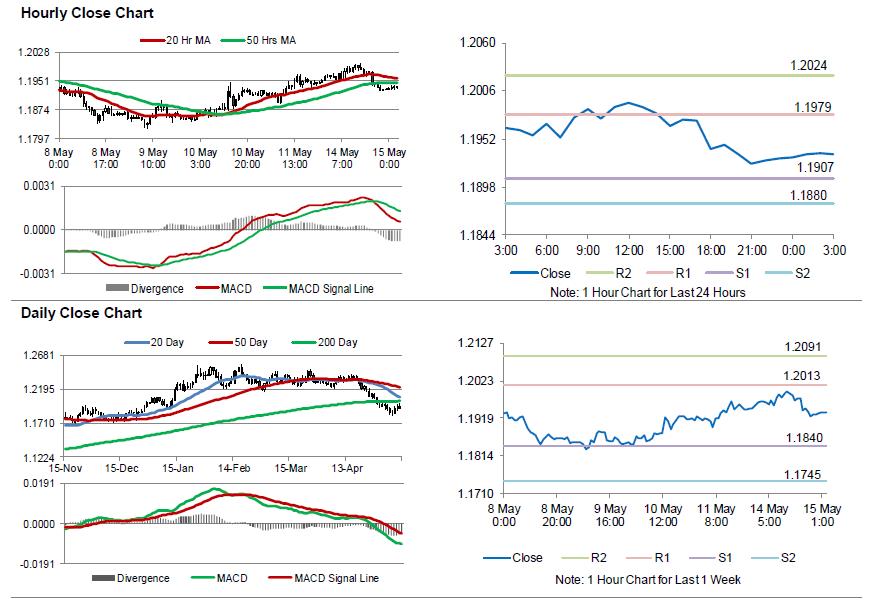

For the 24 hours to 23:00 GMT, the EUR declined 0.30% against the USD and closed at 1.1930.

In the Asian session, at GMT0300, the pair is trading at 1.1935, with the EUR trading slightly higher against the USD from yesterday’s close.

The pair is expected to find support at 1.1907, and a fall through could take it to the next support level of 1.1880. The pair is expected to find its first resistance at 1.1979, and a rise through could take it to the next resistance level of 1.2024.

Trading trend in the Euro today is expected to be determined by flash 1Q GDP data, scheduled to release across the Euro-zone in a few hours. Moreover, the release of ZEW economic sentiment index for May, will be eyed by market participants. Later in the day, the US advance retail sales for April, the NAHB housing market index for May and business inventories for March, will keep investors on their toes.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.