Sample Category Title

U.S Dollars Plight Shaped By Trade Talks And Geopolitics

Monday May 14: Five things the markets are talking about

Last week was a light week on the economic data front as the market focused again on the continued outpouring of earnings reports and geopolitical news from Asia and the Middle East.

This week there are no central bank meeting scheduled, however, there are a number of moving parts that are expected to keep capital markets on their toes.

U.S and Chinese officials will meet in Washington for a second round of trade talks mid-week, after apparently making little progress in discussions in Beijing earlier this month. Also stateside, both Canada and Mexico are 'not' doing a convincing job in trying to downplay the urgency to reach a Nafta deal/outline this week.

Elsewhere, flash Q1 GDP data will be released for the Eurozone, Germany and Japan (May 15). In the U.K, it releases its April labour market report (May 15), while down-under we get Aussie employment data (May 16).

Stateside, U.S retail sales (May 15) and industrial production are due while we close out the week with Canadian CPI and core-retail sales (May 18).

In the Middle East, investors can expect this powder keg to remain a key focus with displays of aggression between Israel and Iran on the rise.

1. Stocks in the 'black'

Global equities head higher on hopes of thawing trade tensions.

In Japan, the Nikkei share average rose to a four-month high overnight following sharp gains in cosmetics after better-than-expected earnings offset weak tech shares. The Nikkei ended +0.5% while the broader Topix rallied +0.6%.

Down-under, Aussie shares rose on Monday, carried higher by BHP hitting its highest in four-years. The S&P/ASX 200 index rose +0.3%. In S. Korea, the Kospi ended the session flat.

In Hong Kong, stocks rose for a six consecutive session and hit a more than seven-week high overnight, as Sino-U.S trade tensions eased. The Hang Seng index rose +1.4%, while the China Enterprises Index gained +1.6%.

In China, it was a similar story, easing trade tensions between Beijing and Washington gave investors the green light. The blue-chip CSI300 index rose +0.9%, while the Shanghai Composite Index rose +0.3%.

In Europe, regional indices trade mostly lower in a subdued session, however, there is one exception, the Swiss SMI trades slightly higher.

U.S stocks are expected to open a tad higher (+0.2%).

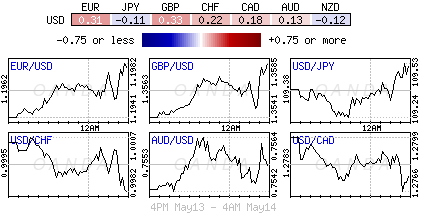

Indices: Stoxx600 -0.2 at 391.8, FTSE -0.1% at 7717.4, DAX -0.2% at 12972, CAC-40 -0.2% at 5532.3, IBEX-35 -0.2% at 10254, FTSE MIB -0.1% at 24127, SMI +0.2% at 9010, S&P 500 Futures +0.2%

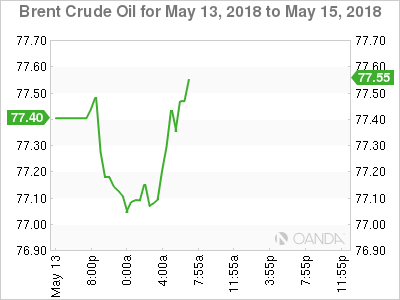

2. Oil slips from multi-year highs as U.S rig count rises, gold higher

Oil prices eased from just shy of their four-year highs overnight as resistance emerged in Europe and Asia to U.S sanctions against major crude exporter Iran, while rising U.S drilling pointed to higher N. American production.

Benchmark Brent is down -40c at $76.72 a barrel, while U.S light crude oil is down -35c at +$70.35.

Note: Both oil futures contracts hit their highest levels in nearly four-years last week at +$78 and +$71.89 a barrel respectively, as markets anticipated a sharp fall in Iranian crude supply once U.S sanctions bite later this year.

U.S Iran sanctions is supporting China's newly established crude oil futures, and may spur efforts to start trading oil in yuan rather than dollars. Since launching in March, Shanghai crude oil futures have seen a steady pick-up in daily trading, with daily volumes hitting a record +250k lots last week.

Note: According to Baker Hughes data on Friday, capping crude prices is U.S drillers adding 10 oil rigs in the week to May 11, bringing the total to 844, the highest level since March 2015.

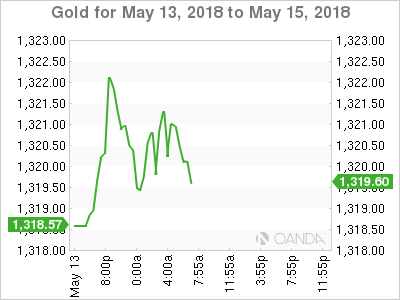

Ahead of the U.S open, gold prices are a tad better bid on the back of a subdued dollar as the market considers the prospects of fewer interest rate hikes in the U.S this year. Spot gold is up +0.2% at +$1,320.80 per ounce, while U.S gold futures for June delivery is little changed at +$1,320.80 per ounce.

3. German Bund yields rally to a two-week high

The benchmark German 10-year bund yield has pushed back to a two-week high ahead of the U.S open and is set for the biggest daily rise in three-weeks, after the ECB's Francois Villeroy de Galhau said the central bank could give fresh guidance on the timing of its first rate hike as the end of its bond stimulus approaches.

His comments have certainly caught the fixed income market flat footed in a relatively thin market and in a week where European corporate bond supply is expected to dominate sentiment.

The German 10-year bund yield has backed up to +0.60%, its highest level since April and up +4 bps on the day.

Elsewhere, the yield on two-year Treasuries has dipped less than -1 bps to +2.53%, the first retreat in more than a week, while the yield on 10-year Treasuries climbed less than +1 bps to +2.97%. In the U.K, the 10-year Gilt yield has advanced +2 bps to +1.467%.

4. Dollar under pressure

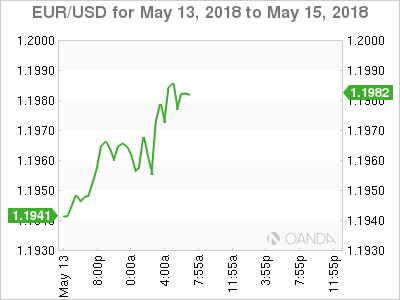

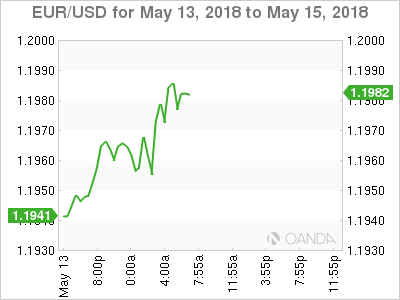

The EUR (€1.1978) is better bid heading into the U.S session, mainly due to dollar weakness, but also because Italy's 5-Star Movement and far-right League have agreed to form a government.

Although there may be concerns about a government made up of anti-establishment parties, but should reduce for the time being any enduring risks of another Italian election and ongoing political impasse. However, follow-through price support for the single unit is expected to be somewhat minimal as the market awaits details on policy proposals and the name of Italy's next Prime Minister.

GBP/USD (£1.3580) is edging aging towards the pivotal £1.3600 resistance. The market is looking to Tuesday's U.K jobs data for guidance. A sustainable move above the psychological £1.3630 area could flush out weak shorts in the short-term.

Note: U.K average earnings for Q1 are expected to have risen +2.9% compared with a +2.8% rise in Q4, 2017.

Elsewhere, Bitcoin (BTC) continues to fall, down -4% to $8,357 in the euro session. Last week it lost -13% mainly due to criticizing comments from Warren Buffet and Bill Gates, and the fact that S. Korean's biggest cryptocurrency exchange was raided by the regulators.

5. Banque De France – French growth to slow

Banque De France (BoF) expects the French economy to continue growing in Q2, albeit at the slower pace it set at the start of the year.

Q2 GDP will rise +0.3% on quarter, according to the central bank's monthly survey of business activity that was conducted in April. At +0.3%, growth marks a slowdown from 2017 when the French economy accelerated sharply. In Q4 2017, GDP expanded at +0.6% on quarter.

Digging deeper, sentiment indicators for April inched down in manufacturing and services, with both falling to 102 from 103. In construction, the sentiment indicator declined slightly to 104 from 105. The long-term average for the sentiment indicators is 100.

Euro Gains Ground, Markets Look Ahead To Eurozone, Germany GDP

EUR/USD is unchanged in the Monday session. Currently, the pair is trading at 1.1981, up 0.33% on the day. It’s a very quiet start to the day, with no eurozone or U.S indicators on the schedule. The sole U.S event is a speech from FOMC member Loretta Mester. On Tuesday, there are two key events out of Germany – Preliminary GDP and ZEW Economic Sentiment. The US will release Retail Sales and Core Retail Sales.

With the U.S economy firing on all cylinders, the U.S consumer is feeling very optimistic. On Friday, the UoM Consumer Sentiment improved to 98.8 in April, beating the estimate of 98.4 points. The U.S labor market is at near or full employment, which has resulted in a slowdown in job growth due to a shortage of skilled workers. This was underscored last week, as JOLTS Job Openings climbed to a record 6.6 million. At the same time, inflation levels remain low, as the Federal Reserve target of 2 percent remains elusive. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. Inflation levels will be an important factor for the Fed in its monetary policy projection, which remains at two more hikes in 2018. The odds of a rate hike at the June hike stands close to 100%.

Investors will be keeping a close eye on German data on Tuesday, with the release of Preliminary GDP and ZEW Economic Sentiment. The eurozone will also publish these indicators. Growth in the eurozone slowed in the first quarter, and GDP in both Germany and the eurozone is expected to fall from 0.6% in the fourth quarter to 0.4% in the first quarter of 2018. The markets are also bracing for weak numbers from the monthly ZEW surveys, which examines confidence levels among institutional investors and analysts. The German release was very soft in April, dropping -8.2 points. Another poor reading is expected in May, with an estimate of -8.0 points. the ZEW eurozone indicator also dropped sharply in April to 1.9, and little change is forecast in the May release.

EU Should Use Iranian Situation To Emboss Euro As A Bench Mark Currency

The birth of the Euro was based on the idea that it would become an alternative reserve currency

Iran seesawed about accepting Bitcoin and had a soft to hard stance toward Bitcoin.

It is not every day that you get an opportunity of a lifetime but when you have it, one should not miss that. The European Union clearly has this at their doorstep and they should thank the President of the United States, Donald Trump, for deciding to pull out of the Iranian nuclear deal.

Really? Of course, every situation has two angles. It all depends where you focus more.

I think the current situation could make the EU position a lot stonger and it is an opportunity for France and Germany to play a global role and emboss Euro as an alternative benchmark currency like the US dollar.

This is not a new idea at all. After all the birth of the Euro was based on the idea that it would become an alternative reserve currency, a benchmark which countries could use to trade.

Thanks to the evolution of the cryptocurrency King, Bitcoin, which has stretched this idea to its bone, countries are open to trade the most important commodity - oil - by using Bitcoin. Russia, a long-time rival for the US, has bounced this idea and a few others have nodded to this. Trump has just put fuel to the fire by pulling out of the nuclear deal and imposing sanctions on Iran.

Iran seesawed about accepting Bitcoin and had a soft to hard stance toward Bitcoin. But mostly there was no clear idea about the cryptocurrency. However, after Venezuela showed the world that the cryptocurrency could be the route to block sanctions, I think Iran would be very serious in looking at the options of how to explore further avenues which would not hurt its economy. The country is in a much stronger position and it is well prepared as compared to the previous occasions. There are more options on their doorsteps now and this would limit the damage to the economy.

The EU: France, Germany and the UK are not pleased with the US situation especially, France particularly. The President of the country, Emmanuel Macron, has played a distinct role to keep the US in the deal. The country has large exposure in Iran and the EU needs to protect the mini-boom in trade. The number stands at €20bn for last year and this number has tripled from the pre-deal low of €6.2bn back in 2013.

EU, France, Germany and the UK would meet Iran on May 15 and the discussion would involve one key area; Iran needs assurance that the nuclear deal will not be sabotaged. The EU would be interested in defending the interest of the European companies and they would have to find a solution or way around the US sanctions.

Of course, if Bitcoin had progressed further with the regulators, the cryptocurrency would have been as one of the options but for now, it would not be the option. But, it is my opinion that the EU would speed up the process of legitimising Bitcoin by the regulators so that they have an alternative to the dollar. If Donald Trump pushes the SEC to void that somehow, that would be a different argument, especially considering how far he could go with that.

A shining option on the table would be loans denominated in Euro. The EU should show the US that they are fully capable of salvaging the deal forward forged under the Obama administration. The EU must take this opportunity to show the strength of the European Bank and its currency.

Italy already issued euro-based sovereign credit line worth of €5bn so bilateral deals could easily be done with the help of the European central bank. Most importantly, Banque Delubac & Cie, a family-owned bank in Paris, has deep roots in Iran and under the French treasury suggestion it is active in building commercial ties.

EU would have to convince the companies such as Total, Airbus, Sanofi, Renault, Peugeot (just a few names which come to mind) which need assurance from both sides: Iran and the EU to continue their involvement.

As long as they are complying with the EU regulations and the loans are Euro denominated with no exposure to the dollar, the common currency and the EU could create an example like no other.

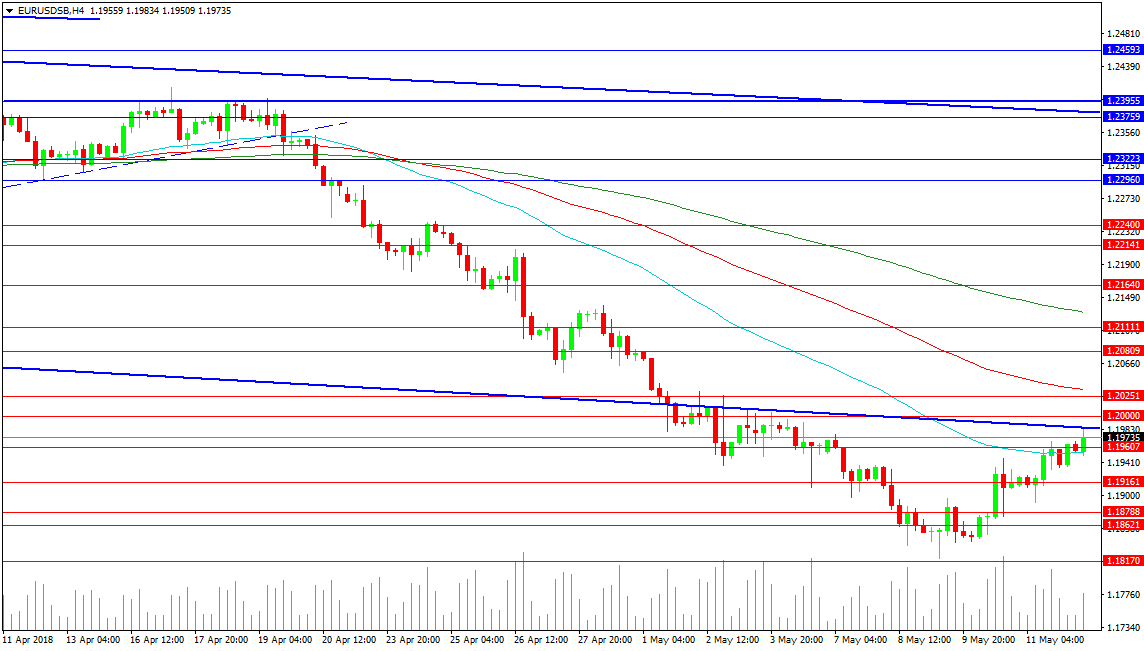

Forex Analysis: EURUSD And AUDUSD

The EURUSD pair found its short-term bottom at 1.18170 last week and has this morning rallied into previous trend line support at 1.19835. The price has used the 50-period MA to prop up today’s advance and this is now the first point of support at 1.19544. There is also support to be found at 1.19161, 1.19000 and 1.18788. A loss of 1.18621 could result in a retest of the low of last week, giving a chance for a double bottom or leading to a further collapse into the 1.17000 area.

Resistance can be seen at the 1.20000 level and a break targets the 1.20250 level, with the 100-period MA at 1.20335. Further upward progress would target the zone around 1.21000 and the 200-period MA at 1.21308. The 1.21640 area offers minor resistance, with the 1.22000 zone giving a chance at a run higher to the 1.24000 level. At this point, resistance should become much firmer.

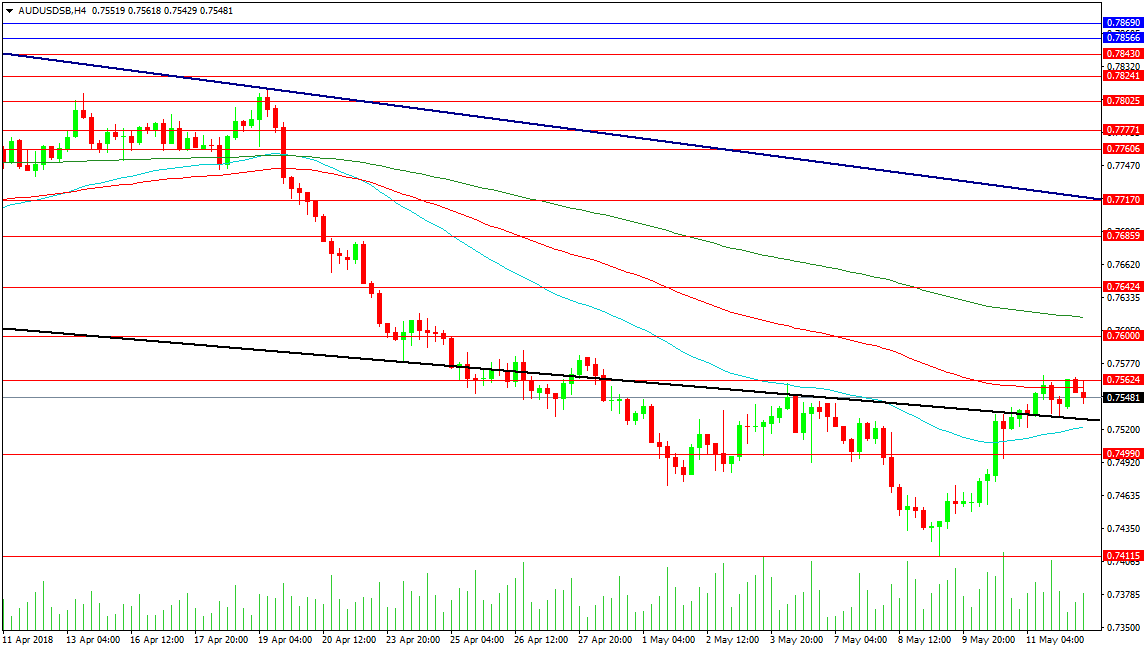

AUDUSD

This pair is also feeling the effects of moves in the USD. The pair found support at 0.74115 and rallied back above the support area at 0.74990, before testing the 50 MA and the lightly held falling black trend line. Price on the chart is consolidating at the 100-period MA at 0.75560. The 50-period MA is currently at 0.75200 and supportive, with a loss of this area suggesting a revisit to the lows of last week. The 0.74000 area could provide support below.

The resistance on the chart comes from the 0.76000 level, which was the point at which the drop from the 0.78000 area started to weaken. Price consolidated around this level on the move down and may wish to repeat that pattern on any move higher. The 200-period MA is located at 0.76168 and is softly reinforcing the ceiling of the 0.76000 area. A break higher through this zone targets the 0.77000 area and the falling resistance trend line at 0.77170. The 0.77600 level marks a strong level within another previous zone of consolidation.

Italy Getting Closer To Putting Together A Populist Govt

Notes/Observations

- Italy populist duo said to be near completion of a coalition govt

Asia:

- North Korea said to be planning to dismantle nuclear test site in a ceremony scheduled between May 23-25th. Journalists from South Korea, China, Russia, the United States and Britain will be invited to cover the dismantling ceremony on-site

- China PBOC Quarterly Report: Will properly implement the prudent and neutral monetary policy to create a moderate financial environment for supply-side structural reform and high-quality development

Europe:

- Italy 5-Star Movement and League Party reached consensus around measures that include a universal basic income, a flat tax and roll back of pension reforms from 2011

- EU said to push for an optional six-month extension to the Brexit transition period to be built in to the UK’s withdrawal agreement to protect its own interests maximize the chance of it being accepted

- Recent press reports noted that May Cabinet said to be divided into two rival groups to fight out how Britain should manage its EU customs arrangements after Brexit. Over the weekend reports suggested that at least a dozen of the 28 ministers in PM May’s cabinet were planning to block her proposal on “customs partnership”

- SNB Vice President Zurbruegg: the CHF currency (Swiss Franc) could quickly strengthen; there's no need to give up negative interest rates

- UK Apr Visa Consumer Spending registered its largest fall since July 2017 (3M/3M: -1.6% v -1.3% prior)

Americas:

- US Sec of State Pompeo: denuclearization of North Korea will require robust verification process. If North Korea agrees to dismantle nuclear program then it would lead to sanctions relief and American private investment

Energy:

- Russia's Novak to remain energy minister in new govt

- Russia Energy Min Noval: Too early to say if Russia will change position on OPEC+ agreement. Oil price under influence of geopolitics but market is seeking balance

- UAE Oil Min Mazrouei: Not targeting a certain oil price worried about level of oil investments in 2019/20

Economic Data:

- (RO) Romania Apr CPI M/M: 0.5% v 0.6%e; Y/Y: 5.2% v 5.2%e

- (FI) Finland Apr CPI M/M: 0.2% v 0.2% prior; Y/Y: 0.8% v 0.8% prior

- (FI) Finland Mar Final Retail Sales Volume Y/Y: 2.7% v 3.8% prelim

- (SE) Sweden Apr PES Unemployment Rate: 3.6% v 3.8% prior

- (FR) Bank of France Business (Industrial) Sentiment: 102 v 103e

- (IN) India Apr Wholesale Prices (WPI) Y/Y: 3.2% v 2.9%e

- (TR) Turkey Mar Current Account Balance: -$4.8B v -$4.2Be

- (SE) Sweden Apr Average House Prices (SEK): 3.067M v 3.069M prior

- (CH) SNB Total Sight Deposits for Week Ended May 11th (CHF): 576.2B v 575.9B prior

- (CZ) Czech Mar Current Account Balance (CZK): -5.6B v +30.0Be

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.2 at 391.8, FTSE -0.1% at 7717.4, DAX -0.2% at 12972, CAC-40 -0.2% at 5532.3, IBEX-35 -0.2% at 10254, FTSE MIB -0.1% at 24127, SMI +0.2% at 9010, S&P 500 Futures +0.2%]

- Market Focal Points/Key Themes: European Indices trade mostly lower in a subdued session so far in Europe with slight declines across the major Indices with the exception of the Swiss SMI which trades slightly higher. US Index futures point to a higher open following a mixed session on Friday. On the earnings front, Lonmin trades higher after its production results, and planned job cuts, with Bauer, Centrica, Dignity and HelloFresh among other risers following results. ABN Amro trades over 4% lower as CET1 ratio came in below expectations. Other fallers include Victrex and Mothercare. In the M&A space IWG trades over 20% higher after confirming its received a takeover approach.

Movers

- Consumer Discretionary [ IWG [IWG.UK] +21% (Confirms takeover approach), Dignity [DTY.UK] +3.1% (Earnings), Hellofresh [HFG.UK] +9.2% (Earnings)]

- Industrials [Bauer [B5A]+3.6% (Earnings)

- Materials [Lonmin [LMI.UK] +6.5% (production update), Victrex [VCT.UK] -4.8% (Earnings)

- Financials [ ABN Amro [ABN.UK] -4.3% (Earnings)]

- Energy [Centrica [CNA.UK] +0.5% (Earnings)]

Speakers

- ECB’s Villeroy (France): Getting closer to ending the QE bond buying program. Ending the program in Sept of Dec was not an existential question. ECB aimed to be predictable but will not pre-commit. Inflation to resume progress in coming months. ECB rate path to be contingent on inflation outlook

- ECB's Greece mission chief Drudi: a credit line would benefit Greece

- Italy President Mattarella to meet 5-Star and League leaders later today. To meet 5-Star leader Di Maio at 10:30 ET (14:30 GMT) and meet League leader Salvini at 12:00 ET (16:00 GMT)

- Reports circulated that Italy’s League sought Sapelli as PM while 5-Star wanted Conte (Note: Sapelli is an economist and former Eni Board member; Cont is law professor)

- South Africa ruling ANC party: No talks on holding an early election (Insight: South Africa next scheduled elections are planned in 2019)

- Fed's Mester (FOMC voter, hawk): Improved economic outlook supported more rate hikes; gradual rate hikes to keep economy from overheating. Now was the time for Fed to assess whether it needed to make changes to its monetary policy framework. Too soon to say the central bank has meet its inflation target on a sustained basis. Inflation would reach Fed's symmetric goal of 2% on sustainable basis over next one to two years

Currencies

- USD retracement from recent cycle highs continued during the session. The session saw European bond yields move higher while the US lagged.

- EUR/USD was trying to edge back to the 1.20 area as the Italian political situation appeared to ward off another election. ECB speak also helping the Euro as they reiterate confidence in achieving the 2% inflation target. Yields were higher across the board in Europe. Some dealers noted that the 1.20 area provided some decent resistance and attractive selling levels

- GBP/USD edged higher to approach the pivotal 1.36 resistance area. A sustain move above 1.3630 area could flush out weak shorts in the pair.

Fixed Income

- Bund Futures trade 28 ticks lower at 158.64 with the focus on Wednesday’s 10-year bund auction. Upside targets 159.75, while a return lower targets the 157.25 level.

- Gilt futures trade at 121.84 lower by 21 ticks, as treasuries remain in demand. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Monday’s liquidity report showed Friday's excess liquidity rose to €1.908T from €1.901T. Use of the marginal lending facility decreased from €227M to €59M.

- Corporate issuance saw high grade issuers raise $43B raised last week

Looking Ahead

- 05:30 (DE) Germany to sell €2.0B in 6-Month BuBills; Avg Yield: % v -0.6637% prior; Bid-to-cover: x v 1.7x prior

- 06:00 (PT) Portugal Q1 Labour Costs Y/Y: No est v 4.7% prior

- 6:00 (IL) Israel to sell Bonds

- 06:00 (RO) Romania to sell Bonds

- 06:15 (DE) ECB’s Lautenschlager (Germany)

- 06:45 (US) Daily Libor Fixing

- 07:25 (BR) Brazil Central Bank Weekly Economists Survey

- 07:40 OPEC Monthly Report

- 07:45 (BE) ECB’s Praet (Belgium, chief economist) in London

- 08:00 (IN) India Apr CPI Y/Y: 4.4%e v 4.3% prior

- 08:00 (PL) Poland Mar Current Account: -€1.1B v -€1.0B prior; Trade Balance: Trade Balance: -€0.5Be v -€0.6B prior; Exports: €18.1Be v €16.3B prior; Imports: €18.5B v €16.5B prior

- 08:00 (RO) Romania Central Bank (NBR) May Minutes

- 08:00 (ES) Spain Debt Agency (Tesoro) announces of upcoming issuance

- 08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (CA) Canada Apr Teranet/National Bank HPI M/M: No est v 0.0% prior; Y/Y: No est v 6.6% prior; HPI Index: No est v 218.96 prior

- 08:55 (FR) France Debt Agency(AFT) to sell combined €4.4-5.6B in 3-month, 6-month and 12-month bills

- 09:30 (EU) ECB announces Covered-Bond Purchases

- 09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

- 09:40 (Fed’s Bullard(dove, non-voter) in NY

- 11:30 (US) Treasury to sell 3-Month and 6-Month Bills

- 13:45 (FR) ECB’s Coeure (France) in Geneva

- 16:00 (US) Weekly Crop Progress Report

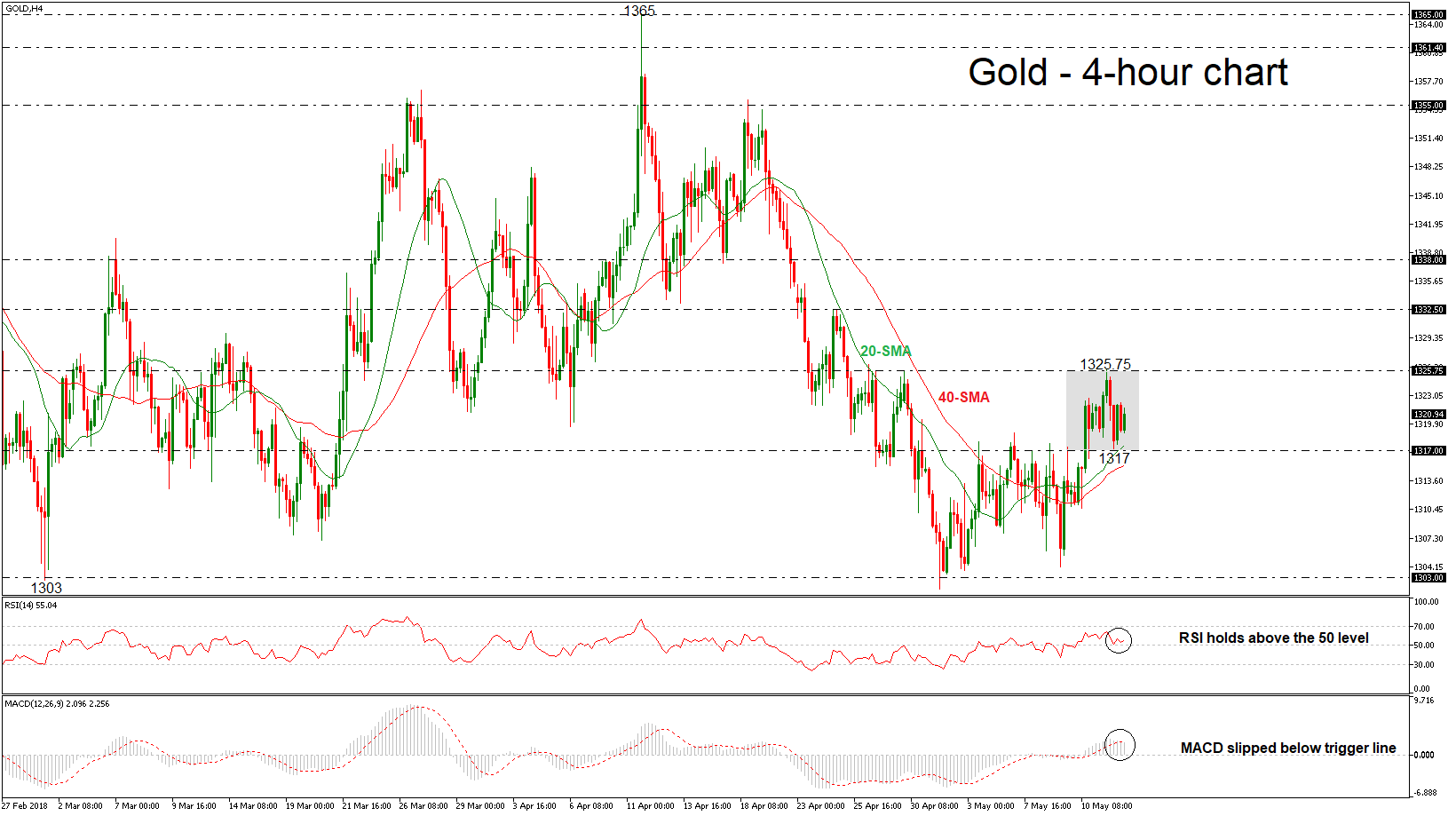

Gold Still Consolidating, Unable To Post Significant Gains

Gold has been consolidating in a narrow range over the last couple of trading days with upper boundary the 1325.75 resistance level and lower boundary the 1317 support barrier. The price is moving above the 20- and 40-simple moving averages (SMAs) in the 4-hour chart with weak momentum.

In the short-term, prices rebounded on the 20-SMA, but based on technical indicators, momentum is too weak to provide a sustained move higher. The RSI is holding slightly above the 50 level and the MACD created a bearish cross with its trigger line in the positive area.

In the wake of positive pressures, the market could meet resistance at the 1325.75 level, confirming the trading range, while if there is a jump above this area, prices could manage to touch the 1332.50 barrier. A stronger hurdle though could be found at the 1338 resistance, identified by the low on April 17.

Conversely, if prices are able to break the 1317 support level and also slip below the moving averages, this could open the door for the 1303 significant key level, where the price touched it several times in the past.

Turning to the medium-term picture, the market seems to be in neutral mode given that the precious metal has been trading within the 1303 – 1365 zone since January 25 .

Trump Extends ‘Olive Branch’ To China, Italian Politics Monitored

Here are the latest developments in global markets:

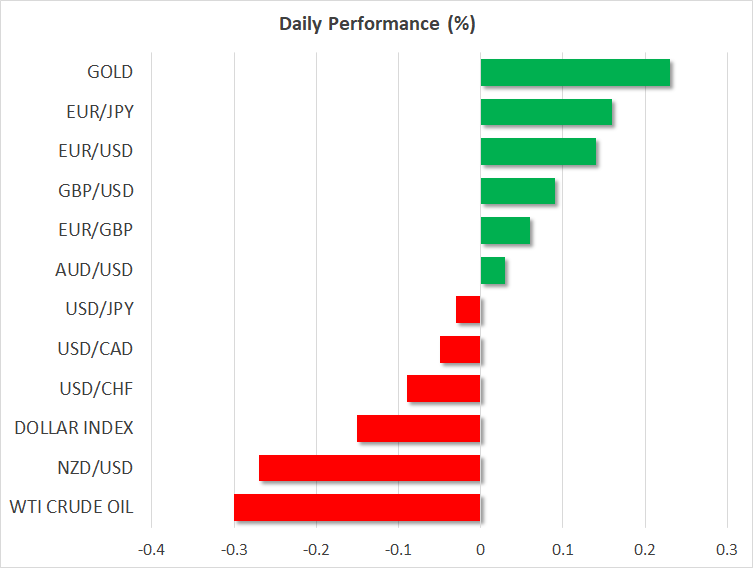

FOREX: The US dollar index is lower by 0.15% on Monday, extending the losses it posted on Friday. The disappointment in the US core CPI last week appears to have taken the wind out of the greenback's sails, with yields on 10-year US Treasuries unable to sustain a foothold above the widely-touted 3.0% level.

STOCKS: US markets closed mostly higher on Friday. The Dow Jones and the S&P 500 rose by 0.37% and 0.17% respectively but the tech-heavy Nasdaq Composite closed marginally lower (-0.03%), dragged down mainly by cybersecurity software maker Symantec (-33.1%). The company announced an internal investigation will delay its annual report and may lead to a restatement of its earnings. As for today, futures tracking the Dow, S&P, and Nasdaq 100 are all pointing to a higher open, probably due to encouraging news over the weekend regarding the US-China trade talks (see below). The positive sentiment was evident in Asia today, with Japan's Nikkei 225 and Topix climbing by 0.47% and 0.61% correspondingly. In Hong Kong, the Hang Seng advanced 1.12%. In Europe, futures following the major indices were mixed, though all were close to neutral territory.

COMMODITIES: Oil prices are lower on Monday, after having retreated on Friday as well. WTI and Brent are down by 0.3% and 0.4% respectively. The retreat may be partly owed to comments from the UAE oil minister, who said OPEC has enough spare capacity to offset any crude lost due to sanctions on Iran. Another marked increase in the Baker Hughes rig count on Friday may have played a role too. In precious metals, gold is 0.2% higher today, remaining close to the $1,320/ounce mark. The yellow metal has been unable to assume a clear direction lately, trading between its 100-day and 200-day moving averages. A potential break of either of these technical barriers may determine the next directional wave in the metal.

Major movers: Dollar corrects lower; risk sentiment buoyed by Trump's 'olive branch'

The US currency was on the back foot on Monday, extending the losses it posted on Friday. The optimistic sentiment surrounding the dollar looks to have cooled for now, as the disappointing US inflation data last week probably scaled back some bets for aggressive rate hikes by the Fed this year.

Euro/dollar (+0.15%) crossed back above 1.1950, with the common currency remaining largely unfazed by political developments in Italy, where the next government looks increasingly more likely to be formed by anti-establishment parties.

Sterling/dollar was up by nearly 0.1%, having recovered nearly all of its BoE-induced losses from last week. That said, the recovery appears to be owed more to dollar weakness than sterling strength, considering that euro/sterling has remained elevated following the BoE meeting, with the pound unable to gain ground versus the euro.

Dollar/loonie rebounded on Friday, after it touched a three-week low of 1.2730, following the release of soft employment data out of Canada. While the unemployment rate held steady as expected, the net change in employment turned negative, and the labor force participation rate ticked down. Despite the miss, markets did not materially pare back expectations for near-term BoC rate increases. Investors currently assign a 40% probability for a rate hike at the May meeting, and a 74% chance for that to occur in July.

On the trade front, President Trump extended an 'olive branch' to China by ordering the US Commerce Department to help Chinese telecommunications giant ZTE to 'get back into business, fast'. The firm had suspended its operations last month after the Commerce Department banned US companies from selling it components. Also, China's Vice Premier and top economic adviser Liu He will visit the US for further negotiations. It thus appears that both sides are committed to finding solutions through talks, which diminishes the likelihood of the situation escalating any further, in the near-term at least. Any signs that tensions are subsiding may support risk appetite in the coming days, potentially helping stocks advance and weighing on safe-haven assets like the yen.

Day ahead: Italian politics eyed; geopolitics and trade remain a consideration

The calendar is practically empty of major releases out of the world's largest economies for the rest of the day. In the absence of economic data, attention is likely to be diverted elsewhere, such as on the potential outcome in negotiations to form a government between Italy's major anti-establishment parties.

Any updates on the political situation in Italy will be closely watched as they definitely have the capacity to act as euro drivers. In this respect, anti-establishment parties 5-Star Movement and far-right League spent the weekend attempting to find common ground to govern the country. The two parties said they made progress towards that goal.

Other topics that might gain attention in an empty calendar are geopolitical developments in the aftermath of the Trump administration's decision to leave the Iran nuclear deal, as well as any updates on global trade. Relating to the latter, China is planning to send Vice Premier Liu He to Washington for more talks.

In equities, the final leg of the earnings season is taking place. One of the notable names releasing results this week is retail giant Walmart (Thursday).

Today's calendar features numerous policymakers making appearances, including BoE Governor Mark Carney, ECB Chief Economist Peter Praet, and St. Louis Fed President James Bullard (a non-voting FOMC member in 2018). However, the topics of discussion are such that are unlikely to lead to market-sensitive comments.

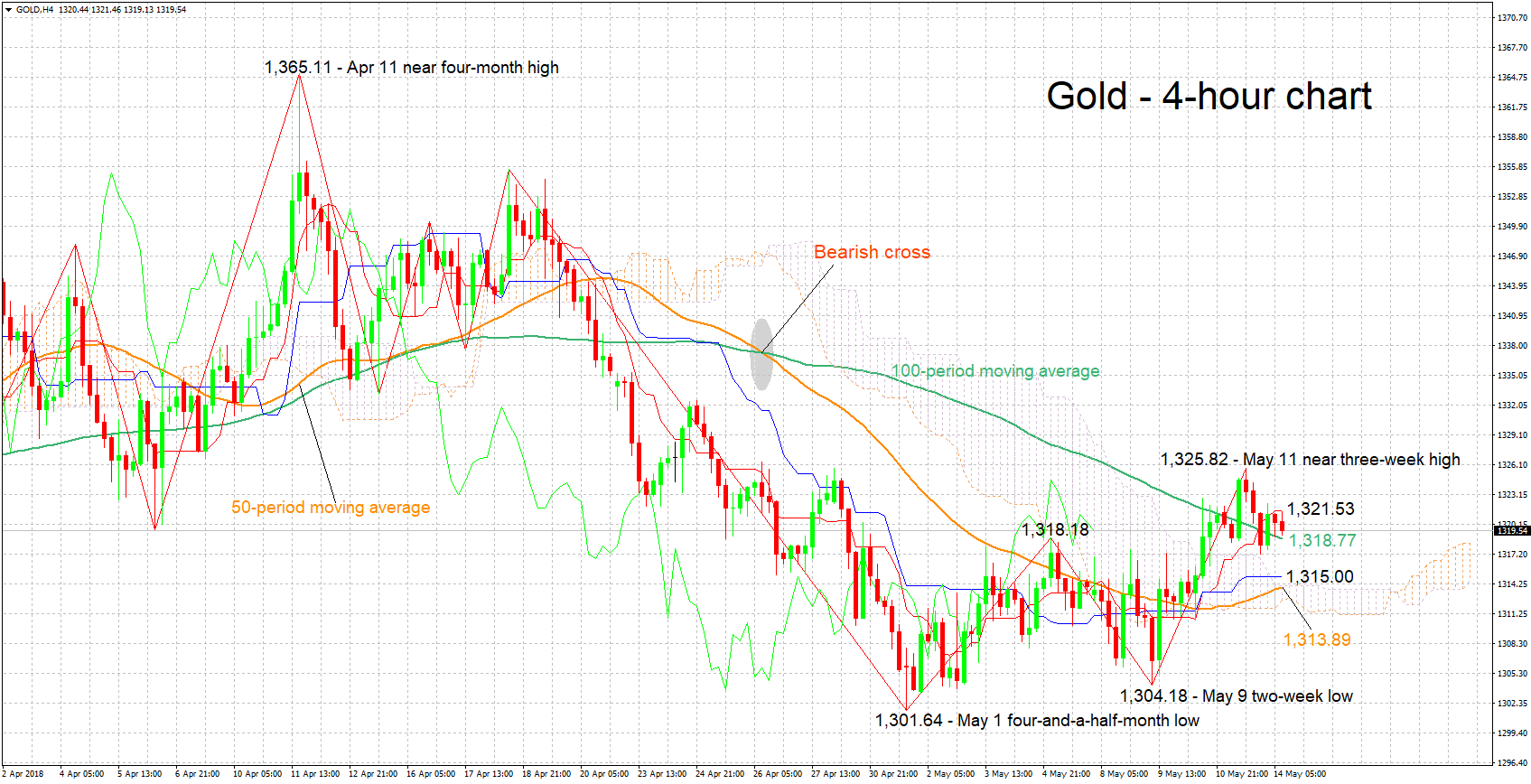

Technical Analysis: Gold short-term bullish, though positive momentum seems to be easing

Gold is trading not far below a near three-week high of 1,325.82 hit on Friday. The Tenkan- and Kijun-sen lines are positively aligned, pointing to a bullish short-term picture. Notice though that the latter has flatlined, with the implication being that positive momentum is easing.

Increasing political, geopolitical or trade uncertainty can boost the safe-haven perceived asset. Immediate resistance could be taking place around the current level of the Tenkan-sen at 1,321.53, with last week's high of 1,325.82 being eyed next in the event of stronger bullish movement.

On the downside and in case of receding uncertainty that diverts funds out of the yellow metal and into riskier instruments, support could come around the current level of the 100-period moving average at 1,318.77, and further below from the region around the Kijun-sen at 1,315.00.

The greenback's direction can also affect the precious metal; a stronger US currency weighs on the dollar-denominated commodity and vice versa.

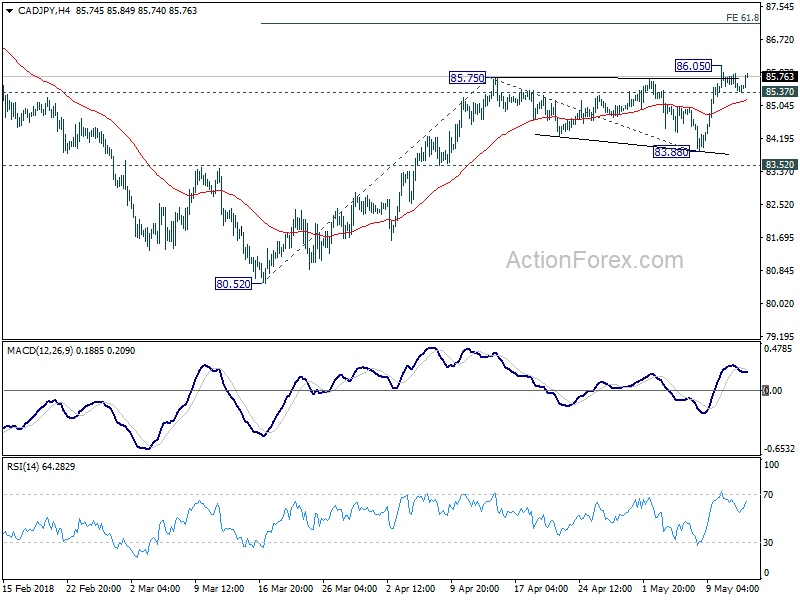

A look at EURJPY and CADJPY as JPY in selloff mode

We'd soon enter into US session. JPY continues to trade with one of the weakest, along with NZD.

A quick glance at JPY Action Bias table, we can that EURJPY and GBPJPY are the stronger ones intraday. But both D Action Bias are neutral. CADJPY may lack momentum in H Action Bias, but 6H and D Action Bias argue it's in a trend. That prompts us to have a deeper look.

EURJPY D action bias chart clearly shows that it's rebounding after a prior decline halts ahead of near term support around 129 level. Current rebound, while strong, is not in clearly a trend yet. It could be part of a range consolidation pattern.

On the other hand, CADJPY D action bias chart showed it's in a solid up move from around 80 level. The moved turned into consolidation after failing 86. The rally could indeed be resuming with last week's breakout. So, while EURJPY is stronger today, CADJPY is a better candidate for trend trading.

Back at the regular bar chart, for now, intraday bias in CADJPY stays neutral. But break of 86.05 will confirm rise resumption. CADJPY should target 61.8% projection of 80.52 to 85.75 from 83.88 at 87.11. Though, break of 85.13 will delay the bullish case and bring more consolidation first.

Italian Ignorance, Crude Knowledge

Market ignoring risks

Interestingly markets seem to be ignoring the political risk building in Italy. Peripheral European yield spreads failed to react to Northern League and 5-Star have reached a tentative coalition agreement. Despite the dramatic cost this coalition might have on Italy government spending Euro continues to firms against the USD. Industrial metals such as copper and iron ore are threating to break higher conveying a renewed risk appetite.

President Trump's decision to withdraw from the JCPOA should be considered a major geopolitical shift. The unexpected announcement has pushed oil prices above $77 / bbl for the first time since 2014. Tighter supplies are forcing analysts to raise price forecasts for 2018. Rising prices, in addition to cost cuts is allowing oil companies once again turn a profit. Valuations have lagged oil price due to skepticism over diminishing supply glut but the removal of Iranian oil will likely have investors allowing for higher forward outlook. On the FX front we anticipate commodity currencies CAD, NOK and AUD to improve.

NZD keeps falling despite broad USD pullback

The New Zealand dollar was one of the few G10 currencies to lose ground against the greenback as speculators scaled down bullish bets. Indeed, according to data released by the CFTC last Friday, speculators trimmed long Kiwi positions significantly last week with net long positions falling to 12,546 contracts from 16,573 a week earlier - this correspond to a decrease from 44% of total open interest to around 25%.

The last four weeks were rough for the New Zealand dollar has it gave up more 6.5% against the buck to reach a multi-month low at $0.6903 on May 10th amid widening interest differential and a cautious RBNZ. . However, the debasement has stopped for now with NZD/USD climbing back to $0.6950. On the downside, the currency pair is approaching a key technical support area at between $0.6869 (50% Fibonacci on March 2009- September 2011 rally) and $0.6781 (low from November 2017). Despite the solid debasement of the last few weeks, we think that sellers are not exhausted yet as speculators are still net long Kiwie and may continue to unwind long positions.

Turkey current account deficit deepens

After announcing its withdrawal from Iran deal last Tuesday, United States decision caused further uncertainty in the Middle East region. The diplomatic confrontation between Israel and Iran keeps on tightening following Israel's Prime Minister Benjamin Netanjahu declaration with regard to Iran's engagement towards its nuclear program freeze. The Iran deal is in danger though European effort to maintain it could worsen its relationship with the US, who temporarily put aside trade tariffs against the Old Continent.

Recent Turkey current account balance deficit of USD -4.81 billion (prior: -4.52 billion) continues to expand, strongly impeded by a continued decline in goods trade (USD -4.6 billion) and employee compensation (USD -1.31 billion, at 3-years low). On the other side, positive numbers in services (USD +1.12 billion), though estimated below its 5-year average at USD 1.85 billion continue to support the current account balance.

Accordingly, the downtrend with regard to EM currencies continues, strongly impacted by continued risk-off effect. We expect the USD/TRY to maintain its strength, as long as no intermediation with regard to Iran deal are found, adding up with Central Bank of Turkey relative inaction with regard to its required monetary policy tightening.

Currently trading at 4.32, USD/TRY regains strength following recent decline at 4.22 (10/05/2018 low), heading along the 4.35 range in the short-term.

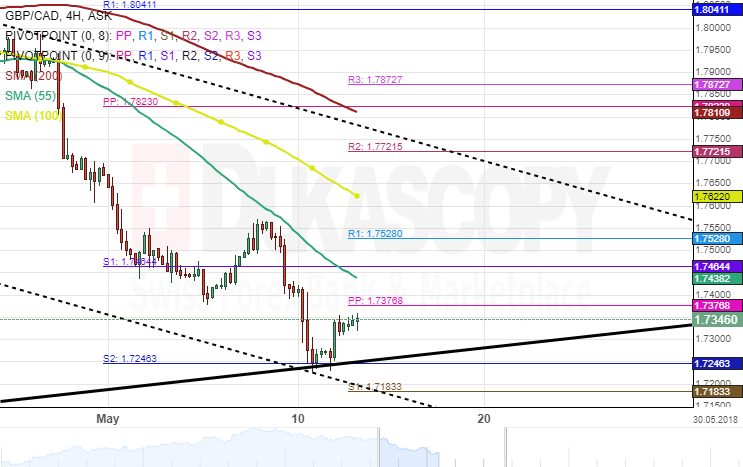

GBP/CAD 4H Chart: Finds Support

The GBP/CAD currency pair has been moving in a descending channel since mid-March. The exchange rate reversed from the upper boundary of a dominant ascending channel on March 20 and followed by a strong period of decline.

The Pound Sterling has reached the lower boundary of both the dominant and the junior patterns and could be prepared for a new wave to the upside during the following trading sessions. Nevertheless, the price movement needs to surpass the weekly pivot point and the 55– hour simple moving average near the 1.7376 regions.

Everything being equal, a breakout from the aforementioned PP could be expected within this session. However, technical indicators suggest that bears are likely to grow stronger in the nearest future