Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.15; (P) 109.35; (R1) 109.56; More...

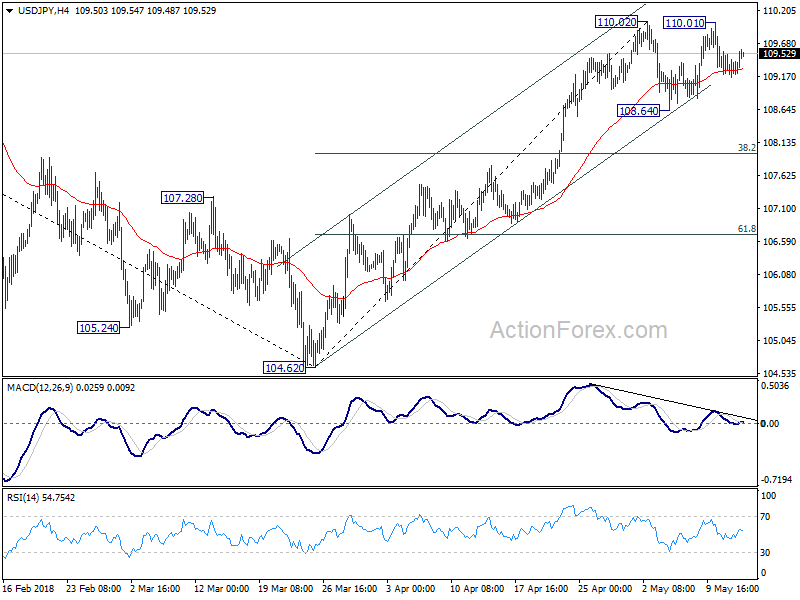

Intraday bias in USD/JPY remains neutral as consolidation from 110.02 short term top continues. Below 1108.64 will bring deeper pull back. But downside should be contained by 38.2% retracement of 104.62 to 110.02 at 107.95 to bring rally resumption. On the upside, break of 110.02 will resume the rise from 104.62 to 61.8% retracement of 114.73 to 104.62 at 110.86 next.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 38.2s% retracement of 104.62 to 110.02 at 107.95 holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above.

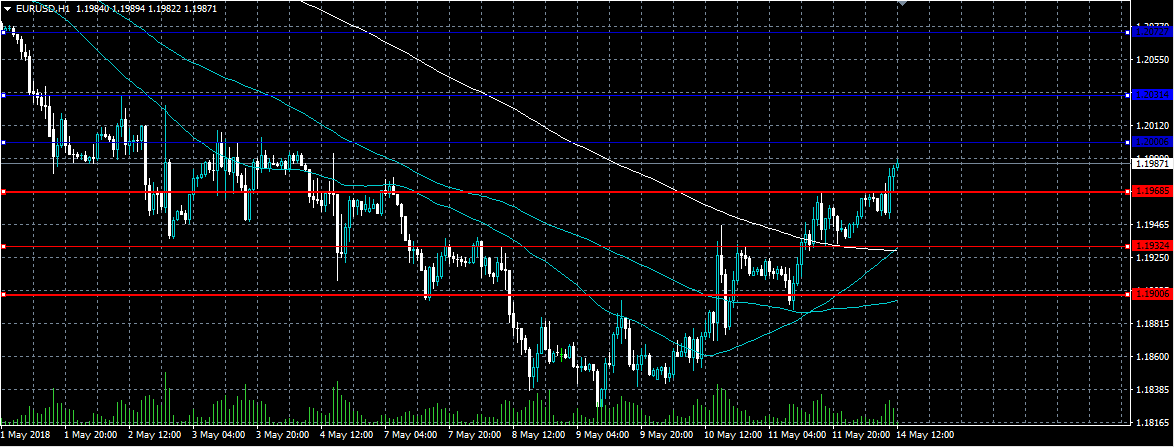

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1897; (P) 1.1932 (R1) 1.1974; More....

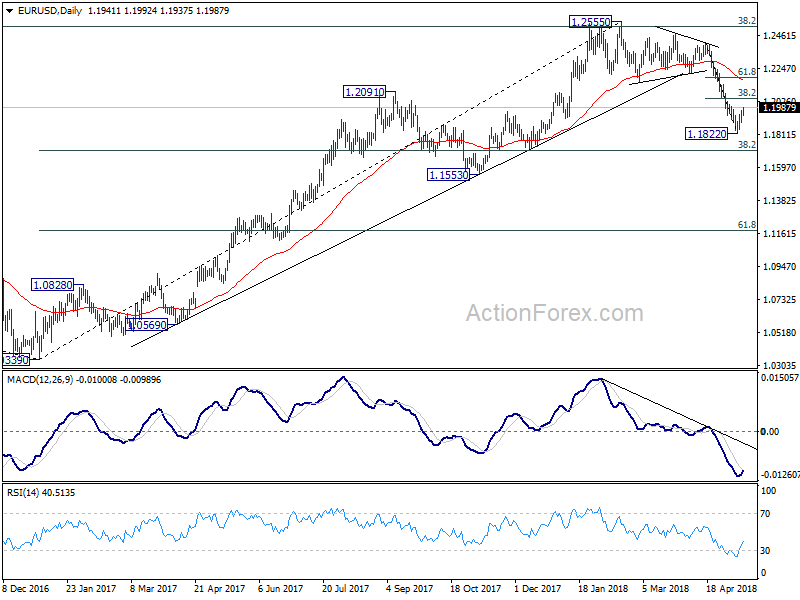

EUR/USD's rebound from 1.1822 short term is still in progress and reaches as high as 1.1992 so far. Intraday bias remains on the upside for 38.2% retracement of 1.2413 to 1.1822 at 1.2048. We'd expect strong resistance from there to limit upside to bring fall resumption. On the downside, below 1.1932 minor support will turn bias to the downside for 1.1822 first. Break will resume the whole decline from 1.2555 and target 1.1708 medium term fibonacci level next.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will target 61.8% retracement at 1.1186. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2179) holds.

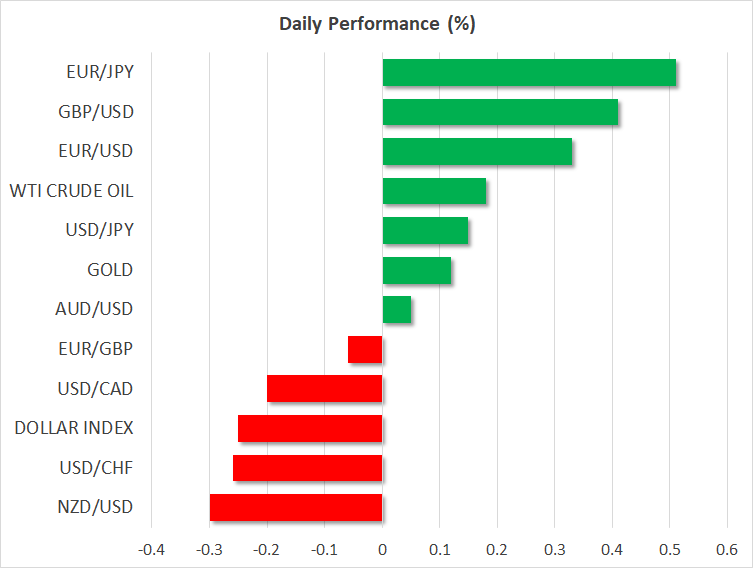

Euro Jumps as ECB Villeroy Indicates Rate Hikes Just Some Quarters Away from End of QE

Euro rises broadly today as lifted by hawkish comments from an ECB official. Sterling closely follow as the second strongest one. On the other hand, New Zealand dollar continues to suffer broad based selling pressure today, in particular against Australian Dollar. Yen follows as the second weakest on optimism of easing trade tension between US and China. Dollar is trading as the third weakest as correction extends. The US economic calendar is empty today. And without any fresh inspirations, activity could drop a bit until tomorrow's RBA minutes.

Technically, Dollar is staying in corrective mode against other major currencies. In particular, GBP/USD's recovery has been very weak so far, limited below 1.3617 minor resistance, comparing to last week's low at 1.3459. A key event that could trigger a range break out is tomorrow's job and wage data. But some traders could jump the gun ahead of it. So 1.3459 and 1.3617 are two key levels to watch ahead. 86.05 in CAD/JPY is another level to watch today. CAD/JPY lags behind other yen crosses and is help in range of 85.37/86.05 today. But it's near term bullish outlook is indeed more solid as the rise from March low of 80.52 has just resumed late last week. Break of 86.05 will extend this medium term rally.

ECB Villeroy de Galhau: Rate hike some "quarters" not "years" after ending QE

ECB Governing Council member, Bank of France Governor Francois Villeroy de Galhau said today that "the time when our net asset purchases will end is approaching". Currently, ECB's EUR 30B per month asset purchase program is set to end after September. Villeroy de Galhau said whether it will end in September, or December is not "a deep existential question". Regarding interest rates, he added that "we could give additional guidance on its timing–well past meaning at least some quarters but not years–and its contingency on the inflation outlook."

Trump offered concession ahead of US-China trade talks

China's Vice Premier Liu He, President Xi Jinping's top economic adviser is traveling to Washington to start the second round of trade talks tomorrow, with US Treasury Secretary Steven Mnuchin. Liu and his team will stay from May 15 to 19 according to a Foreign Ministry spokesperson.

Ahead of the meeting, Trump tweeted "President Xi of China, and I, are working together to give massive Chinese phone company, ZTE, a way to get back into business, fast. Too many jobs in China lost. Commerce Department has been instructed to get it done!" This is seen a concession by Trump ahead of the trade talks, which offers some hope of a positive outcome.

White House spokeswoman Lindsay Walters confirmed that US officials were in contact with Beijing about ZTE. And, Commerce Secretary Wilbur Ross is expected to "exercise his independent judgment, consistent with applicable laws and regulations, to resolve the regulatory action involving ZTE based on its facts."

Cleveland Fed Mester: Fed fund rates could overshoot long run level

In a speech titled "Issues for U.S. Monetary Policy", Cleveland Fed President Loretta Mester expressed her support for further rate hike. She noted that "the medium-run outlook supports the continued gradual removal of policy accommodation; it seems the best strategy for balancing the risks to both of our policy goals and avoiding a build-up of financial stability risks.

Regarding inflation, she noted that it will take a year or two to stabilize around the 2% target. And, she added that "we want to give inflation time to move back to goal … this argues against a steep path" on tightening. But, "as the expansion continues, it could be that in order to maintain our policy goals, we may need to move the fed funds rate, for a time, a bit above the level of the funds rate that is expected to prevail over the longer run".

She also pointed to Fed's March economic projections that fed funds rates could move a bit above the longer-run level at 3% by 2020. She noted that "2020 is a long time away and the policy path actually followed will be responsive to changes in the outlook.

OPEC raised both supply and demand forecasts, concerned with US trade relations

In May's Monthly Oil Market Report, OPEC rated both 2018 oil supply and demand forecasts. For 2018, oil demand growth is forecast to increase by around 1.65mb/d to average 98.85 mb/d. Growth was revised higher from prior month by 25tb/d. China is anticipated to lead oil demand growth in 2018, followed by Other Asia and OECD Americas. Non-OPEC supply growth was revised up by 0.01mbs in 2018 to 1.75mb/d, averaging 59.62mb/d in total. Meanwhile, OPEC production rose 12tb/d to average 31.93mb/d in April.

In the section regarding world economy, OPEC warned of the risk of development in trade relations. In particular, it "the latest rounds of US sanctions on Russia, tariffs on Chinese products in combination with considerable requests by the US in trade negotiations with China, US tariffs on steel and aluminium, prolonged North American Free Trade Agreement (NAFTA) negotiations, as well as the US withdrawal from the Joint Comprehensive Plan of Action (JCPOA) with IR Iran all point to rising uncertainty.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1897; (P) 1.1932 (R1) 1.1974; More....

EUR/USD's rebound from 1.1822 short term is still in progress and reaches as high as 1.1992 so far. Intraday bias remains on the upside for 38.2% retracement of 1.2413 to 1.1822 at 1.2048. We'd expect strong resistance from there to limit upside to bring fall resumption. On the downside, below 1.1932 minor support will turn bias to the downside for 1.1822 first. Break will resume the whole decline from 1.2555 and target 1.1708 medium term fibonacci level next.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will target 61.8% retracement at 1.1186. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2179) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Apr | 2.00% | 2.00% | 2.10% | |

| 6:00 | JPY | Machine Tool Orders Y/Y Apr P | 22.00% | 28.10% |

Canadian Dollar Gains Ground, US Retail Sales Ahead

The Canadian dollar has started the week with gains. Currently, USD/CAD is trading at 1.2756, down 0.34% on the day. On the economic front, Canada releases key jobs data. The economy is expected to add 17.8 thousand jobs, compared to 32.3 thousand a month earlier. The unemployment rate is expected to remain steady at 5.8 percent. In the US, the markets are expecting UoM Consumer Sentiment to improve to 98.4 points.

Canadian employment numbers were mixed on Friday. The economy shed 1100 jobs in April, surprising analysts that had predicted a strong gain of 17.8 thousand. This marked the first decline since January. There was better news from wage growth, which jumped 3.3% in April on an annualized basis. The Canadian currency has received a boost from strong oil prices, which are at the highest level in 3-1/2 years. President Trump’s bombshell announcement that the US would withdraw from the Iran nuclear deal, as well as tensions in the Middle East have raised fears of supply disruptions and have significantly pushed up the price of crude.

With the U.S economy firing on all cylinders, the U.S consumer is feeling very optimistic. On Friday, the UoM Consumer Sentiment improved to 98.8 in April, beating the estimate of 98.4 points. The U.S labor market is at near or full employment, which has resulted in a slowdown in job growth due to a shortage of skilled workers. This was underscored last week, as JOLTS Job Openings climbed to a record 6.6 million. At the same time, inflation levels remain low, as the Federal Reserve target of 2 percent remains elusive. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. Inflation levels will be an important factor for the Fed in its monetary policy projection, which remains at two more hikes in 2018. The odds of a rate hike at the June hike stands close to 100%.

DAX Dips, All Eyes on German GDP

After an uneventful week, the DAX has posted slight losses in the Monday session. Currently, the DAX is at 12,958 points, down 0.33% on the day. There are no German or eurozone releases in the Monday session. On Tuesday, here are two key events out of Germany – Preliminary GDP and ZEW Economic Sentiment.

Investors will be keeping a close eye on German data on Tuesday, with the release of Preliminary GDP and ZEW Economic Sentiment. The eurozone will also publish these indicators. Growth in the eurozone slowed in the first quarter, and GDP in both Germany and the eurozone is expected to fall from 0.6% in the fourth quarter to 0.4% in the first quarter of 2018. The markets are also bracing for weak numbers from the monthly ZEW surveys, which examines confidence levels among institutional investors and analysts. The German release was very soft in April, dropping -8.2 points. Another poor reading is expected in May, with an estimate of -8.0 points. The ZEW eurozone indicator also dropped sharply in April to 1.9, and little change is forecast in the May release.

In the U.S, April inflation levels remain low, as the Federal Reserve target of 2 percent remains elusive. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. Inflation levels will be an important factor for the Fed in its monetary policy projection, which remains at two more hikes in 2018. The odds of a rate hike at the June hike stands close to 100%.

OPEC raised both supply and demand forecasts, concerned with US trade relations

In May's Monthly Oil Market Report, OPEC rated both 2018 oil supply and demand forecasts.

For 2018, oil demand growth is forecast to increase by around 1.65mb/d to average 98.85 mb/d. Growth was revised higher from prior month by 25tb/d. China is anticipated to lead oil demand growth in 2018, followed by Other Asia and OECD Americas. Non-OPEC supply growth was revised up by 0.01mbs in 2018 to 1.75mb/d, averaging 59.62mb/d in total. Meanwhile, OPEC production rose 12tb/d to average 31.93mb/d in April.

In the section regarding world economy, OPEC warned of the risk of development in trade relations. In particular, it "the latest rounds of US sanctions on Russia, tariffs on Chinese products in combination with considerable requests by the US in trade negotiations with China, US tariffs on steel and aluminium, prolonged North American Free Trade Agreement (NAFTA) negotiations, as well as the US withdrawal from the Joint Comprehensive Plan of Action (JCPOA) with IR Iran all point to rising uncertainty.

Full report can be found here.

Euro Heads Higher As Political Noise Eases

Here are the latest developments in global markets:

FOREX: The euro headed for a third consecutive day of gains on Monday although the dollar posted some gains as well against the yen, with investors keeping a close eye on political developments in Italy, where a coalition government may be formed earlier than expected. Euro/dollar rose to to 1.1982 (+0.33%), while dollar/yen touched 109.57 (+0.16%). The US dollar index fell to 92.29 (-0.26%), set to complete a third red day in a row. Pound/dollar rose by 0.34% ahead of Tuesday’s employment figures out of the UK. This comes after the BoE held rates steady and cut its growth projections last week. In the antipodean sphere, aussie/dollar reached a two-week high of 0.7548 (+0.05%), while kiwi/dollar ticked down to 0.6952 (-0.29%). Dollar/loonie fell to 1.2765 (-0.20%), while the Turkish lira moved lower versus the greenback on Monday (-0.15%), as investors continued to worry about the central bank’s ability to rein in double-digit inflation. Data out of the country showing a wider-than-expected current account deficit in March added further pressure to the currency.

STOCKS: European equities eased today with bonds as political strains from Italy to the UK outweighed optimism over waning global trade tensions. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.20% and 0.01% respectively at 1100 GMT. In Germany, the DAX retreated by 0.32 %, while the French CAC 40 fell by 0.21%. In Italy, the FTSE MIB 100 was down by 0.61%, while the British FTSE 100 was weaker by 0.20%. The Spanish IBEX 35 traded lower by 0.14%. Turning to the US, futures tracking the Dow Jones, S&P 500, and Nasdaq 100 were all in positive territory, pointing to a higher open today, continuing the upward movement from last week.

COMMODITIES: Oil prices jumped after OPEC raised world oil demand forecasts for 2018, saying that geopolitical risks might weigh on oil supply in the coming months. West Texas Intermediate (WTI) crude oil and Brent climbed t0 $70.81 (+0.14%) and $77.37 (+0.32%) per barrel in the wake of the news. In precious metals, gold was up by 0.13%, trading close to $1,320 per ounce level.

Day ahead: OPEC delivers monthly oil report; Aussie eyes RBA meeting minutes & Chinese industrial production

The economic calendar will be lacking major releases later today, while geopolitical and trade developments are expected to remain in the spotlight following Trump’s decision last week to pull out of the 2015 Iranian nuclear deal. Moreover, an inconclusive meeting between the US and the Chinese trade negotiating teams in early May signaled that a trade agreement regarding the US import tariffs might come later rather than sooner, but Trump’s order on Sunday to assist a Chinese telecom company eased those worries ahead of the next round of trade talks in Washington this week.

NAFTA negotiations will be gathering interest as well after the US, Canada, and Mexico failed for once again to reach a trade agreement on Friday. The pressure to reach a deal, though, has increased after the US House of Representatives speaker Paul Ryan said he needed details on the new NAFTA by May 17.

In the Eurozone, eyes will remain on Italy in the absence of key data releases out of the bloc as the populist parties, the anti-establishment Five Star Movement and the far-right League party, are said to be nearing to lock a coalition deal. Today, the leaders of the two parties are scheduled to meet the Italian President to inform him of their plans. Note that the aforementioned Eurosceptic parties gained significant support against the traditional centrist parties during the latest Italian general elections, shedding a dark light on the country’s relationship with the EU.

As for today’s, public appearances, speeches by ECB Chief Economist Peter Praet and St. Louis Fed President James Bullard (a non-voting FOMC member in 2018) will be in focus.

Early on Tuesday, the RBA will publish minutes from its latest policy meeting at 0130 GMT, providing details on its decision to leave interest rates unchanged for the 19th consecutive month. A half an hour later readings on Chinese industrial production and retail sales will follow, adding further volatility to the aussie. According to analysts, industrial production in China is anticipated to grow faster in yearly terms in April, while annual retail sales are said to inch down in the same month.

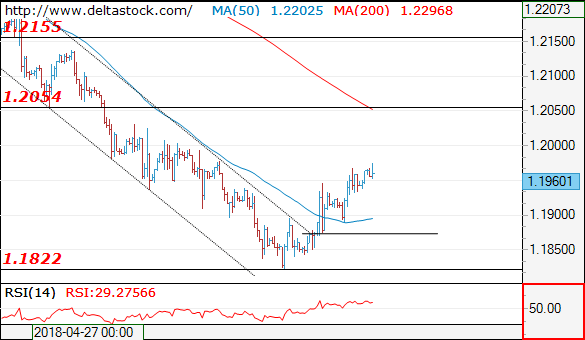

EURUSD Turning Bullish Above 1.2000

The euro currency continues to drift higher against the greenback, as the recent weakness in the US dollar index has largely continued throughout today’s European trading session. The EURUSD pair is currently trading around the 1.1985 level, with buyers now looking for a potential break of the key 1.2000 technical level. Moving into the US trading session traders are watching the 92.00 level on the US dollar index, and the key 1.2000 level on the EURUSD.

The EURUSD pair will turn further bullish above the key 1.2000 level, with upside resistance then found at the 1.2031 and 1.2072 level.

If the EURUSD pair fails to move above the 1.2000 level, we may see a move lower back towards the 1.1968 and 1.1932 support levels.

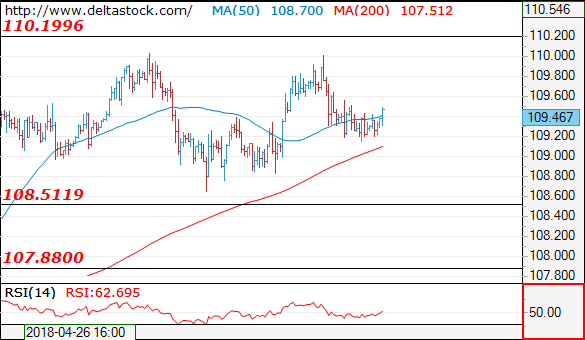

USDJPY Now Turning Bullish Above 109.39 Level

The US dollar has started to move higher against the Japanese yen currency in early week trading, as rising global stock prices boost risk-on trading sentiment. The USDJPY pair is currently trading around the 109.50 level, with the risk-sensitive pair starting to diverge away from the recent theme of broad-based US dollar weakness. Moving into the US trading session, USDJPY traders will be watching the key 110.00 resistance level and US stock market movements.

The USDJPY pair is intraday bullish while trading above the key 109.39 level, key technical resistance is now located at the 109.72 and 110.00 levels.

If the USDJPY pair starts to trade below the 109.39 level, traders may test towards the 109.20 and 109.00 support levels.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1960

The bias remains positive above 1.1927, for a rise towards 1.2000, en route to 1.2060 major hurdle.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1900 | 1.2060 | 1.1840 | 1.1840 |

| 1.2060 | 1.2160 | 1.1720 | 1.1720 |

USD/JPY

USD/JPY

Current level - 109.46

My outlook is still bearish below 109.60, for a slide towards 108.50 zone.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 109.60 | 110.20 | 108.50 | 107.90 |

| 110.20 | 111.90 | 108.50 | 104.60 |

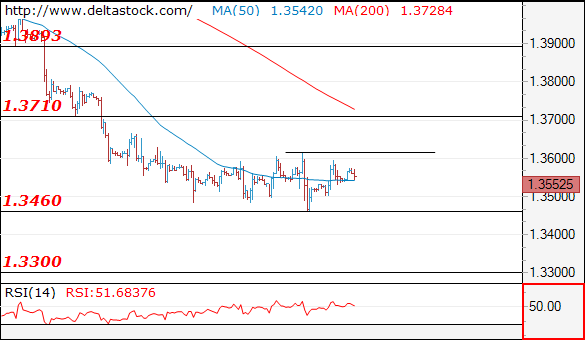

GBP/USD

Current level - 1.3552

The rebound after 1.3460 signals a possible reversal of the whole slide since 1.4380 and the intraday bias is positive, for a break through 1.3610 area, towards 1.3710.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3615 | 1.3990 | 1.3460 | 1.3460 |

| 1.3710 | 1.4100 | 1.3310 | 1.3310 |