Sample Category Title

France denied that Trump told Macron on Iran deal decision

Just earlier today, the New York times reported that Trump told French President Macron of the withdrawal of the Iran deal. And the report was "according to a person briefed on the conversation."

Then Reuters reported that Macron's office denied the New York Times story.

In the same report, Reuters said "one senior European official closely involved in Iran diplomacy told Reuters that U.S. officials had indicated late on Monday that Trump would withdraw from the agreement but it remained unclear on what terms and whether sanctions would be reimposed".

Again, unnamed source. Who to trust? When the President of the US can say something that overturn it completely the next day, you know what it's like in the post-truth world.

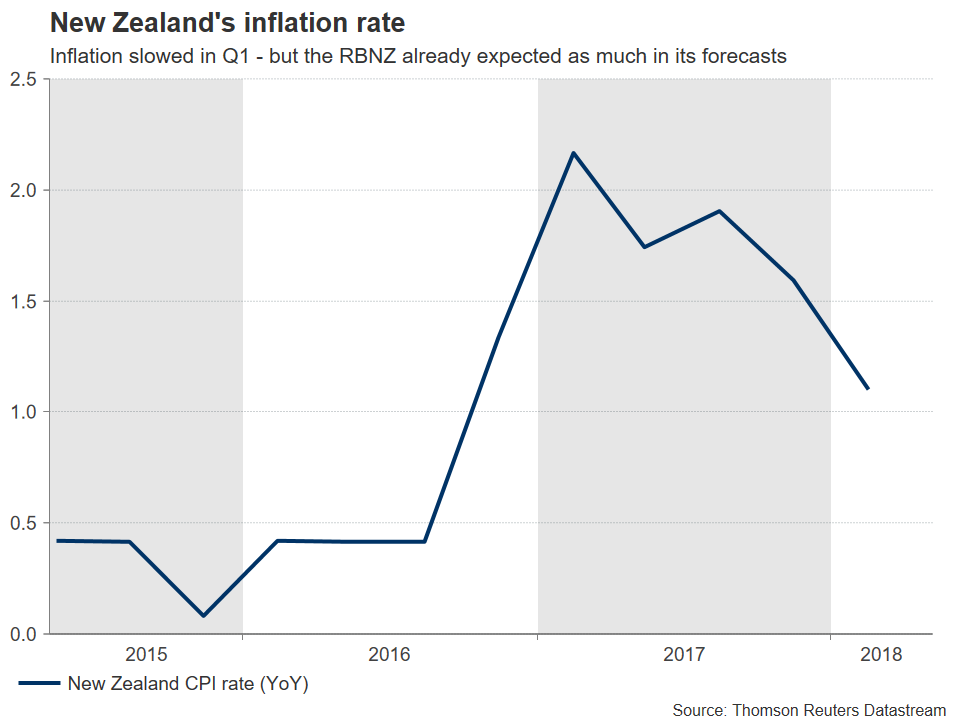

RBNZ Meeting: New Governor, Same Old Neutral Message?

The Reserve Bank of New Zealand (RBNZ) will announce its rate decision on Wednesday at 2100 GMT. Policymakers are widely expected to remain on hold, so price action will be driven by any changes in the accompanying statement, as well as the updated economic forecasts. While the broader policy message is likely to remain neutral, the Bank could revise slightly higher its inflation forecasts, which may help the battered kiwi get some reprieve.

The RBNZ’s upcoming meeting will be closely watched, as it will be the first one under both a new Governor and an expanded mandate, which now includes promoting full employment in addition to price stability. Even though the new RBNZ chief, Adrian Orr, is anticipated to maintain a “steady course” with regards to policy, the statement and subsequent press conference will still be scrutinized for any minor changes that might provide insight into Orr’s future decisions.

Since the Bank last met in March, developments have been mixed overall. On the inflation front, although the CPI rate dipped to 1.1% year-over-year in Q1, this is unlikely to have surprised RBNZ policymakers, who already expected inflation to tumble to 1.1% in their latest set of forecasts in February. What probably came as a surprise though, is the sharp decline in the kiwi’s exchange rate and the surge in commodity prices since the February forecasts, both of which argue for an upward revision in the new inflation forecasts.

As for the labor market, it posted another quarter of strong employment growth in Q1. However, wage growth remained stuck at 1.9% in yearly terms, likely disappointing those that expected a tight labor market to start producing higher wages, and consequently higher inflation down the road. Still, it’s not all bad news for the Bank, as the minimum wage was raised on April 1 and is anticipated to be raised many more times over the coming years.

As for the labor market, it posted another quarter of strong employment growth in Q1. However, wage growth remained stuck at 1.9% in yearly terms, likely disappointing those that expected a tight labor market to start producing higher wages, and consequently higher inflation down the road. Still, it’s not all bad news for the Bank, as the minimum wage was raised on April 1 and is anticipated to be raised many more times over the coming years.

What may be worrisome is the tightening in financial conditions that has occurred lately. Even though the RBNZ is maintaining its own rates unchanged, rising interest rates abroad are spilling over into slightly higher rates for New Zealand’s commercial banks. This was already flagged as a key risk by the Bank in February, as it may begin to manifest itself into higher mortgage rates for households, and thereby dampen consumption and economic growth.

Putting all the above together, policymakers are highly likely to maintain a broadly neutral tone, signaling that any rate increase is still far away. Price action in kiwi/dollar will probably depend on whether the Bank places more emphasis on the positive developments surrounding the inflation outlook, or the risk of rising mortgage rates. Although there is a lot of uncertainty involved, a reasonable scenario is one where the Bank raises its short-term inflation forecasts and signals that, it is monitoring mortgage rates closely and will act accordingly, but only if needed. To the extent that this amplifies speculation for slightly earlier rate hikes, kiwi/dollar could rebound, though any such reaction is unlikely to be massive.

Technically, advances in kiwi/dollar may encounter resistance near the 0.7052 level, which is the high of May 4. Further up, sell orders may be found initially at 0.7095, the top of April 27, and subsequently near 0.7150, the bottom of March 21.

On the downside, immediate support to declines may come around the 0.6950 handle, marked by the low of May 8. A downside break of that area could open the way for the 0.6915 barrier, which is the December 6 top, and afterwards for 0.6850, identified by the inside swing low on November 27.

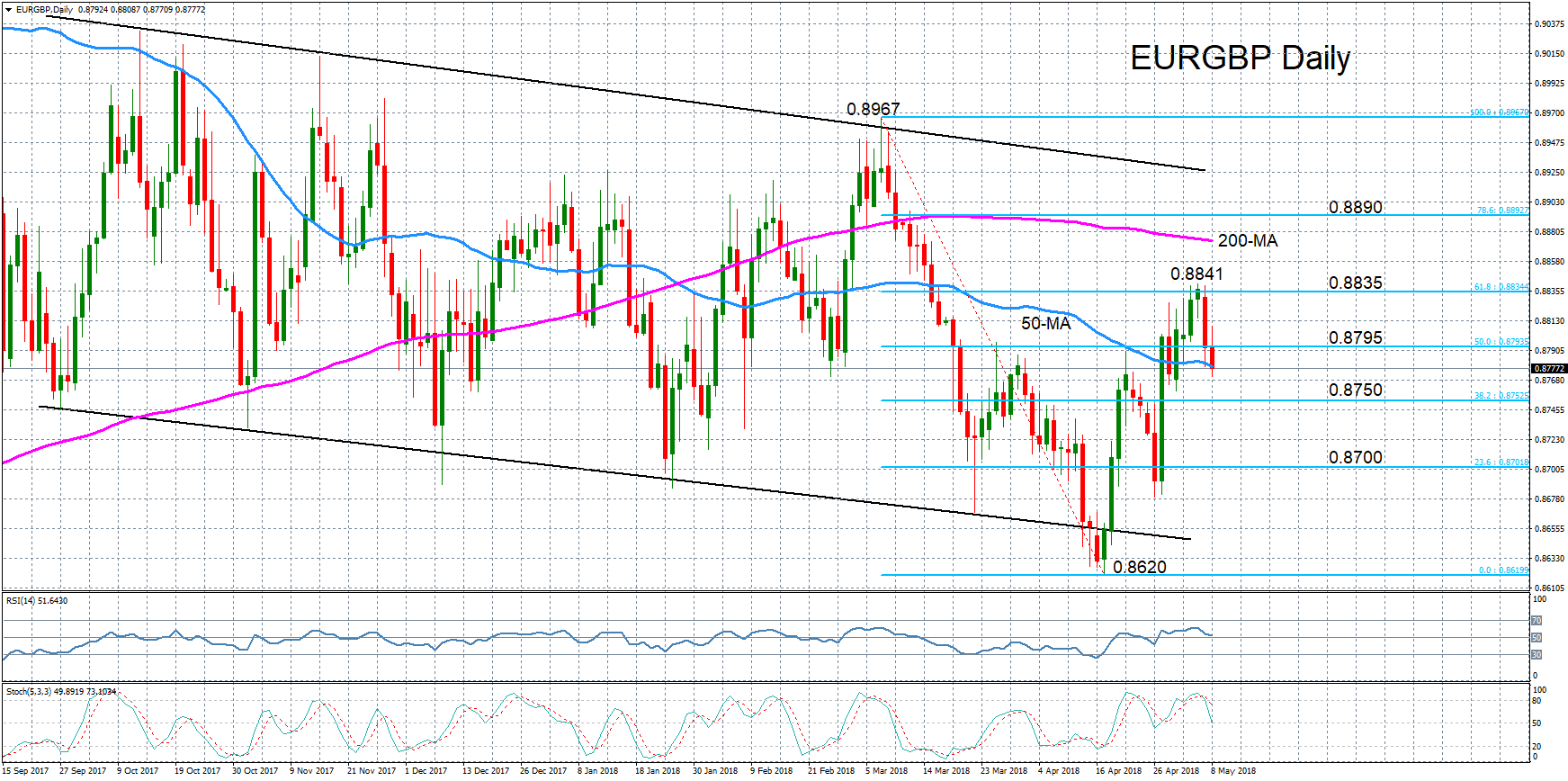

EURGBP Rebound Stalls at 61.8% Fibonacci; Bias Turns Neutral

EURGBP is looking more neutral in the short term after pulling back from multi-week highs reached on Friday. The rebound from 0.8620 (11-month low) to 0.8841 (7-week high) lost momentum after hitting resistance at the 61.8% Fibonacci retracement of the downleg from 0.8967 to 0.8620.

Momentum indicators point to further downside risks in the near term. The RSI has slid to just above the 50-neutral level, while the stochastics are pointing downwards and approaching negative territory.

Immediate support is being provided by the 50-day moving average (MA) around 0.8775. A daily close below the 50-day MA would shift the near-term bias to bearish and clear the way towards the 38.2% Fibonacci retracement at 0.8750. Further losses would bring prices within reach of the key psychological 0.87 level (the 23.6% Fibonacci).

However, if the pair manages to regain positive momentum, the 61.8% Fibonacci level around 0.8835 would once again come into focus. Prices would need to successfully challenge this barrier in order to turn attention back to the upside and resume the three-week old rally. Resistance above this mark would likely come from the 200-day moving average around 0.8875, followed by the 78.6% Fibonacci around 0.8890.

In the medium term, EURGBP remains within a slightly downward tilting channel that has been developing since late September 2017.

Gold Lower, Markets Eye Trump Announcement on Iran

Gold has posted considerable losses in the Tuesday session. In North American trade, the spot price for an ounce of gold is $1309.34, down 0.30% on the day. On the release front, JOLTS Jobs Openings jumped to 6.55 million, crushing the estimate of 6.02 million. Later in the day, US President Trump makes a major speech and will announce if he is pulling the United States out of the Iran nuclear agreement. On Wednesday, the US releases PPI reports.

As a safe-haven asset, gold tends to go up in value during times of crises. Traders will be keeping carefully monitoring President Trump’s televised speech later on Tuesday. Trump is widely expected to announce that the US will be pulling out of the 2015 Iran nuclear deal. This could lead to the entire agreement falling apart, without a ‘plan B’ in place to curtail the Iranian nuclear program. Aside from the nuclear deal, tensions between Iran and Israel have reached a fever pitch, as Iran has vowed to retaliate against Israel after a recent Israeli air strike in Syria resulted in Iranian casualties. Any military confrontation between the two foes would likely send gold prices higher.

The Federal Reserve’s newest regional Fed president, Thomas Barkin, delivered a major speech on Monday, and his tone was decidedly upbeat. Barkin said that the economy is “remarkably strong: above-trend growth, low unemployment, inflation at target”. Barkin added that although the labor market is strong, it is not causing pressure on wages, but low unemployment should lead to an increase in inflationary pressures. As for upcoming rate increases, Barkin was careful to remain mum on how many rate hikes he expects this year. The Fed raised rates in March by a quarter-point and continues to forecast two additional increases this year. However, some policymakers are calling for three more hikes, given the strong health of the US economy.

Pound Slips to 4-Month Low as Housing Inflation Sinks

The British pound has posted losses in the Tuesday session. In North American trade, GBP/USD is trading at 1.3592, down 0.47% on the day. There are no major events on the schedule. In the UK, Halifax HPI plunged 3.1%, its sharpest decline since 2010. Later in the day, the UK releases BRC Retail Sales Monitor, with the markets braced for a decline of 0.7%. Over in the US, JOLTS Jobs Openings jumped to 6.55 million, crushing the estimate of 6.02 million. All eyes are on US President Trump, who will announce if he is pulling the United States out of the Iran nuclear agreement. On Wednesday, the US releases PPI reports.

The pound continues to stumble. GBP/USD dropped to a low of 1.3484 earlier on Tuesday, its lowest level since late December. British GDP and other key indicators have pointed to weaker economic activity, and this may dissuade Bank of England policymakers from raising interest rates until the second half of 2018. Just a few weeks ago, analysts expected the bank to raise rates by a quarter-point, but the cautious BoE is now expected to delay a rate hike until August, at the earliest.

Prime Minister May hasn’t had an easy time with Brexit. May continues to face strong opposition to her Brexit strategy from the opposition and even within the government. To make matters even worse, the House of Lords has inflicted a number of political defeats on the government. On Tuesday, the House of Lords will vote on an amendment to the EU Withdrawal Bill which would instruct the government to enter negotiations over UK membership in the European Economic Area (EEA). This scheme would allow the UK full access to the European common market, but the UK would not be part of common agricultural policy. Proponents of the proposal say this would allow for a ‘soft’ Brexit, but opponents argue that Britain needs to make a clean break in order to gain full control over its economy

US-China Trade: Staying on the Negotiation Path

Good news on the trade front

China's top economic adviser and vice-premier Liu He is going to the US next week for further negotiations. This is a positive sign that the path of negotiation is still the preferred one after the US delegation was in Beijing last week. It is also positive that the US chief negotiator is Treasury Secretary Stephen Mnuchin as he is the more moderate voice in the US trade delegation, which also consists of the trade hawks Peter Navarro, Robert Lighthizer and Wilbur Ross.

Trump's spokeswoman Sarah Sanders said yesterday 'The president has a great relationship with President Xi and we are working on something we think will be great for everybody. China's top economic adviser, the vice premier, will be coming here next week to continue the discussions with the president's economic team. We will keep you posted as the discussions are ongoing.' See Bloomberg, Xi and Trump to Talk Trade, Korea as Chinese Aide Heads to U.S., 7 May 2018, and FT (paywall), China's vice-premier DC-bound for trade talks, 8 May 2018, for more on the story.

Our take: tough talks ahead

These are still going to be tough negotiations as there are key areas where US demands are unlikely to be met. Bloomberg presented a list of demands from each side here: Here's What the U.S., China Demanded of Each Other on Trade, 4 May 2018.

The 'Made-in-China 2025' strategy focusing on technology and innovation is non-negotiable for China as this is the core part of their development strategy. Technology is the big area of tension. The US has already tightened significantly on Chinese investments into the US and will probably create further restrictions in this area going forward (we still await a report on this in early June). The US may also put more restrictions on US exports of technology products to China, on top of putting tariffs on Chinese tech products – as already announced recently.

Reducing the US trade deficit by USD200bn as the US has demanded is also not realistic. China will also work to increase imports but cannot put a specific number on it. They also see the deficit partly as a reflection of very low savings in the US – which will probably decrease further with the rising budget deficit (lower public savings) in coming years. China also sees the trade deficit as over-estimated because China is often at the end of the global supply chain assembling parts imported from around the world. But the full value of the product is counted as Chinese exports.

However, in the area of protection of intellectual property rights China is likely to meet the US. China has already done a lot in the past years (see for example The Diplomat: How China is Emerging as a Leader in Global Innovation and IP Rights, 7 July 2017). It has been a central part of the policy to strengthen IPR protection as China's innovation agenda would get nowhere without this. Many Chinese companies have also complained about violations of property rights, with China now leading in the area of global patent applications, see IP Watchdog, 12 December 2017.

China will also open up more for inbound direct investments as demanded by the US. A series of initiatives have already been announced, opening up for example in the financial sector and in the manufacture of autos and aviation.

Finally, China has announced that tariffs will be cut for cars and some other consumer goods.

The question is, how many of the Chinese demands will be met? Many of these are within the area of access to technology investments and as noted above it seems very unlikely, the US is going to give anything here.

Next week, Republican Marco Rubio has announced he will introduce the Fair Trade With China Enforcement Act, which, as he writes in the Washington Post, Targeting China's tools of aggression, 2 May 2018, among other things will 'guard the American people against China's nefarious influence on national and economic security, directly targeting China's tools of economic aggression. The legislation will ban the sale of all sensitive technology or intellectual property to Chinese entities…'. A range of other protectionist measures are also mentioned, especially in the tech area.

Where to go? More protectionism but no trade war

The negotiations will likely take some time but the ultimate outcome will most likely be one of more US protectionism towards China, focusing on tech products, and other goods within the sectors mentioned in the 'Made in China 2025' strategy, with China increasingly looking towards other regions for tech supplies while intensifying the efforts to boost its own production of key tech components. The recent US ban on selling products to the Chinese telecom equipment maker ZTE sent a clear signal that the US cannot be counted on as a secure supplier of tech components (see SCMP, ZTE ban underlines the need for China to step up its own R&D, 20 April 2018, for more on this).

However, while we will probably end up with more US protectionism towards China, our baseline scenario is still that a tit-for-tat trade war with continued escalation will be avoided. The latest signs of negotiations underpin our expectations of this. US Trade Representative hinted in connection with the trip to Beijing last week that negotiations could take up to a year, so we should not expect a rapid resolve of the matter.

Sunset Market Commentary

Markets:

Global core bond trading remained lackluster today, with both the Bund and US Note future trading with a slight intraday downward bias. The move accelerates as US trading kicks in. Investors keep fate that US President Trump won’t blow up the Iranian nuclear accord (JCPOA) tonight. Heavy supply could be partially at play as well. Fed Chair Powell stressed the importance of flagging policy actions to markets, but made no suggestions of stepping up the tightening cycle. The German yield curve steepens at the time of writing with yield changes ranging between -0.4 bps (2-yr) and +2.7 bps (30-yr). US yields add 1.2 bps (30-yr) to 2.2 bps (5-yr) with the belly of the curve underperforming the wings. Italian assets underperformed as 5SM leader Di Maio and Lega Nord leader Salvini buried a last-ditch effort by Italian president Mattarella to form a government of national unity to solve the political deadlock. Both party leaders are in favour of July elections, boosted by favorable election polls. The prospect of a populist tandem 5SM-Lega Nord weighs on Italian bonds and stocks. The Italian 10-yr spread adds 7 bps, but there is no spill-over to other peripheral bonds markets. The Bund didn’t profit from safe haven flows.

Relative USD strength persisted. The US currency retained the benefit of the doubt as investors pondered the potential impact of president Trump’s decision on the Iranian nuclear deal. Technical considerations were also in play. EUR/USD dropped below the 1.1936 62 % retracement level, confirming the negative momentum in this cross rate. The euro faced additional selling during the day on headlines that Italy was heading for new Parliamentary elections. EUR/USD declined further below the 1.19 handle. A correction in the oil price also supported the dollar. EUR/USD trades currently in the 1.1850/55 area. As was the case over the previous days, USD/JPY underperformed the overall USD rally. The pair hovers in the low 109 area. EUR/JPY (currently around 129.50) is nearing the key 129 support area. A break of this level could trigger further stop-loss selling in other euro cross rates.

Sterling trading was driven by a sequence of conflicting factors today. In the end, the UK currency trades marginally stronger against a weak euro, but loses ground against the dollar. The UK currency profited temporary from the announcement of a big corporate take-over deal this morning. However, the positive impact on sterling was limited and short-lived. Much weaker than expected Halifax house Prices (-3.1% M/M vs only -0.2% expected) wrong-footed sterling longs. The report raised further doubts on the health of the UK economy. More negative headlines from the housing markets might be a reason for the BoE to keep a cautious approach. EUR/GBP jumped to the 0.8810 area. Later in the session, overall euro weakness also reversed this EUR/GBP up-tick. EUR/GBP trades currently again in the 0.8785 area. Cable dropped to the 1.35 area mirroring, both sterling softness and USD strength.

News Headlines:

US NFIB small business optimism improved slightly in April, from 104.7 to 104.8, beating 104.5 consensus. The indicator remains at historically high levels. Consumer spending, the new tax law and lower regulatory barriers are all supporting the surge in optimism across all small business industry sectors.

A stronger-than-expected rebound in German industrial output in March (1% M/M vs 0.8% M/M forecast), and a jump in exports in the same month (1.7% M/M), helped ease concerns that growth in Europe's biggest economy could have come to a standstill at the start of the year. Imports disappointed though, declining by 0.9% M/M. (Reuters)

Federal Reserve Chairman Powell said the central bank would communicate its interest-rate policy strategy “as clearly and transparently as possible” to avoid market turmoil that could ripple through foreign economies. (WSJ)

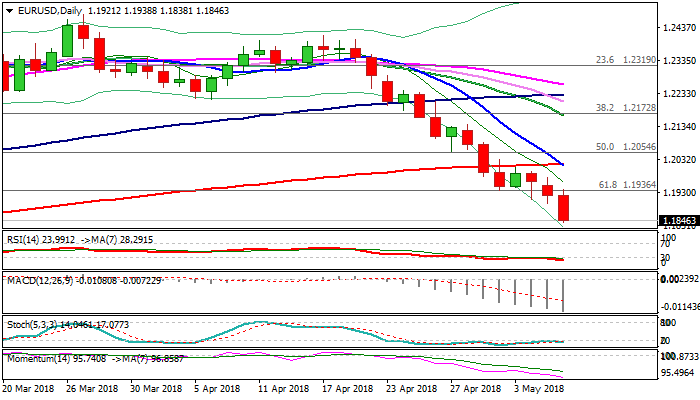

EURUSD – Bears Accelerate in the US Session, Eye Fibo Support at 1.1790

The Euro extends weakness in early US trading and hit session low at 1.1838 (the lowest since 22 Dec).

Strong bearish sentiment is reinforced by growing bearish momentum and formation of 10/200SMA death-cross.

Bears eye initial target at 1.1816 (22 Dec low) and more significant support at 1.1790 (Fibo 76.4% of 1.1553/1.2555).

Looking at larger picture, pullback from 2018 high at 1.2555 is correction of broader uptrend from 1.0340 (03 Jan 2017 low) to 1.2555 (16 Feb), which is expected to ideally reverse above 1.1709 (Fibo 38.2% of 1.0340/1.2555 rally) to keep larger bulls in play.

Res: 1.1873; 1.1897; 1.1936; 1.1978

Sup: 1.1838; 1.1816; 1.1790; 1.1737

Canada: Housing Starts Slow in April But Remain Healthy

Canadian housing starts dipped to 214k (annualized) units in April, down 4.9% from March's slightly upwardly revised pace of 225k. The pace disappointed expectations for a milder pullback, to 220k, but the rate of homebuilding in Canada remains strong. The underlying trend, defined as the six month moving average, edged slightly lower to 226k.

Single-detached starts decreased by 9.5% to 69k units, while multifamily starts dropped by 2.6% to 145k units during the month.

The bulk of April's decline was concentrated in B.C. (-8k to 41k), Newfoundland and Labrador (-5k to 1k) and Ontario (-5k to 70k). Starts were also lower in Manitoba and New Brunswick. On the flip side, relatively strong gains were observed in Quebec (+4k to 57k) and Alberta (+3k to 30k).

Starts fell for the second straight month in Toronto (-12k to 27k units), with declines in both the single-detached and multi-family sector. Starts also declined in Vancouver (-9k to 23k units). Conversely, starts were higher in Montreal (+13k to 33k units)

Key Implications

The pace of starts eased but remained solid in April, supported by continued population and income growth. Overall, we expect near-term starts to remain elevated – something telegraphed by permit issuance data.

Homebuilding is proceeding at firm pace across most of the country, and is particularly strong in B.C. and Quebec. The Prairie provinces remain as the key exception, with homebuilding under pressure from oversupplied markets in Alberta and Saskatchewan, with a decline anticipated in Manitoba after an outsized gain last year.

Looking ahead, we expect the pace of starts to pull-back closer to the 200k mark in the second-half of 2018, and dip below that level towards the fundamentally-supported pace next year as higher interest rates and regulatory changes weigh on demand.

Japanese Yen Edges Lower as Household Spending Declines

The Japanese yen continues to show little movement this week. In Tuesday’s North American session, USD/JPY is trading at 109.28, up 0.17% on the day. On the release front, Japanese Household Spending disappointed with a decline of 0.2%. This was well short of the forecast of a 1.2% gain. The US will release JOLTS Job Openings, which is expected to dip to 6.02 million. All eyes are on US President Trump, who will announce if he is pulling the United States out of the Iran nuclear agreement. On Wednesday, the US releases PPI reports and Japan publishes the current account surplus. As well, the Bank of Japan releases the summary of opinion from the April policy meeting.

Japanese consumer spending was dismal in March, according to a key indicator. Household Spending declined 0.2%, underscoring sluggish domestic demand and a pessimistic Japanese consumer. Although the employment market is very tight, consumers continue to hold tight to the purse strings, as companies have been reluctant to raise wages. However, Bank of Japan policymakers appear more confident in the Japanese economy, as the minutes from the March meeting were upbeat. The minutes said that the economy, as well as inflation, are likely to continue on an upward trend. The bank has long sought to reach an inflation target of around 2 percent, and if policymakers are correct and this goal is on its way to being achieved, the BoJ will be able to contemplate a reduction in its stimulus program, a move which could have a substantial impact on the yen. However, the cautious BoJ is likely to stick to current policy well into 2019, even if economic conditions improve and inflation moves closer to target.