Sample Category Title

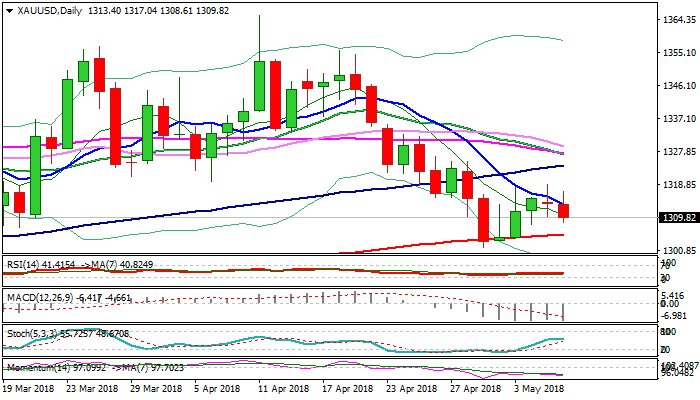

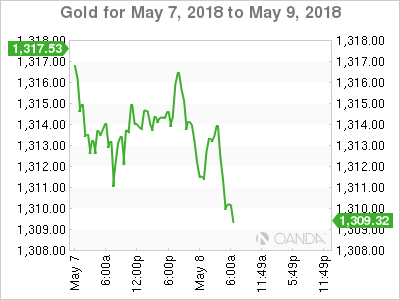

Spot Gold Eases After Recovery Stall, Risks Retest Of 200SMA

Gold holds in red on Tuesday as dollar strengthened and eases back to $1308, retracing Fibo 61.8% of $1301/$1918 recovery leg. Negative near-term bias is establishing after Monday's long-legged Doji signaled strong indecision and recovery stall, which received confirmation on today's fresh easing. Falling 10SMA continues to limit upside attempts despite repeated spikes above and maintaining bearish pressure along with weakening momentum. Fresh bears off $1318 need close below $1308 to confirm reversal and open way for retest of key support provided by 200SMA ($1305) and renewed probe through psychological $1300 support. Conversely, eventual close above 10SMA ($1313) would ease downside pressure and signal fresh recovery attempts which need close above $1322 (Fibo 38.2% of $1355/$1301 fall) to spark stronger correction of $1355/$1301 fall.

Res: 1313, 1318, 1322, 1325

Sup: 1308, 1305, 1301, 1295

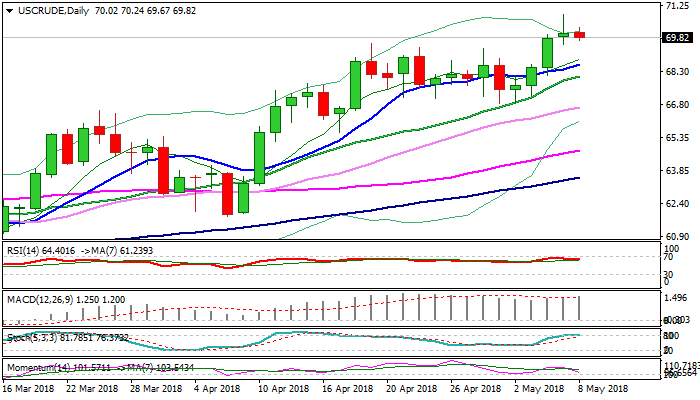

WTI Oil Eases From New Highs Awaiting US President Trump’s Decision On Iran

WTI oil stands at the back foot and returns below $70 handle in early trading on Tuesday, following quick pullback from Monday's new 3 1/2 year high at $70.81. Traders are cautious ahead of announcement of US President Trump whether the US will pull out of nuclear deal with Iran, made in 2015. The agreement provided lifting of sanctions on Iran's oil export in return to stopping its nuclear program. US decision to withdraw from the deal would hit Iran's oil exports and tighten oil market, as Iran is the major oil producer in the Middle East, as well as member of OPEC and new sanctions on exports of Iranian oil would signal shortage in the market and lift oil price. Based on expectations of US withdrawal, current easing could be seen as positioning for fresh rally. Break and close above $70 mark would be bullish signal for extension towards projections at $72.04 and $73.32 and would expose barriers at $74.94 (04 Oct 2011 low) and $76.35 (Fibo 61.8% of $107.45/$26.04 fall). If the US stays in the deal, oil price could ease further, as weakening momentum studies maintain near-term pressure, with deeper pullback and stronger close in red today to complete reversal pattern and signal deeper pullback. President Trump's announcement would likely overshadow release of API crude stocks data, due later today, which are expected to show the situation with crude inventories which unexpectedly rose strongly last week. Rising thick hourly cloud (spanned between $69.79 and $68.94) marks strong support and guards pivotal support provided by rising 10SMA ($68.59) loss of which would generate stronger bearish signal.

Res: 70.24, 70.81, 71.21, 71.60

Sup: 69.79, 69.50, 68.94, 68.59

In to US session: A look at AUDUSD and EURCHF

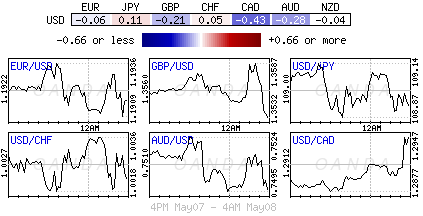

Heading into US session, CHF and JPY are notably higher against others. Commodity currencies are the weakest, together with EUR.

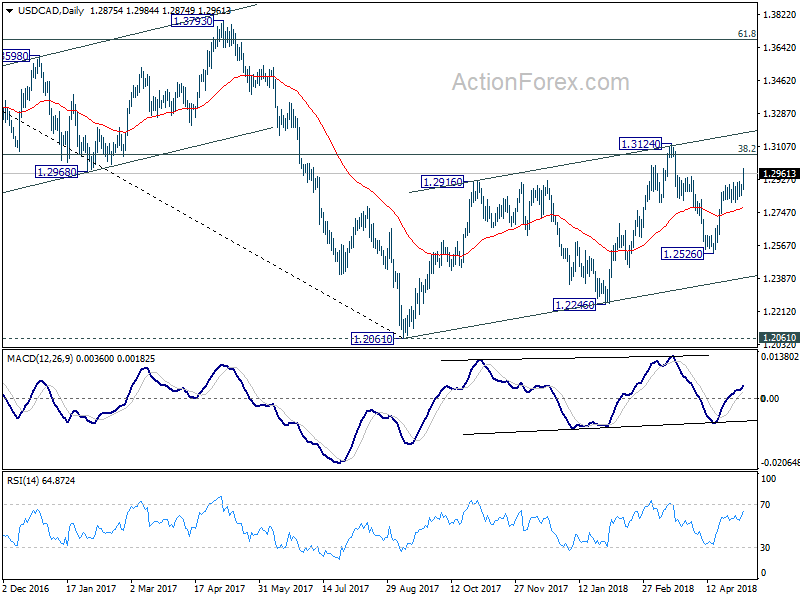

The surge in USD/CAD earlier in European session first caught out attention. As mentioned earlier, it's on course for 1.3124 resistance.

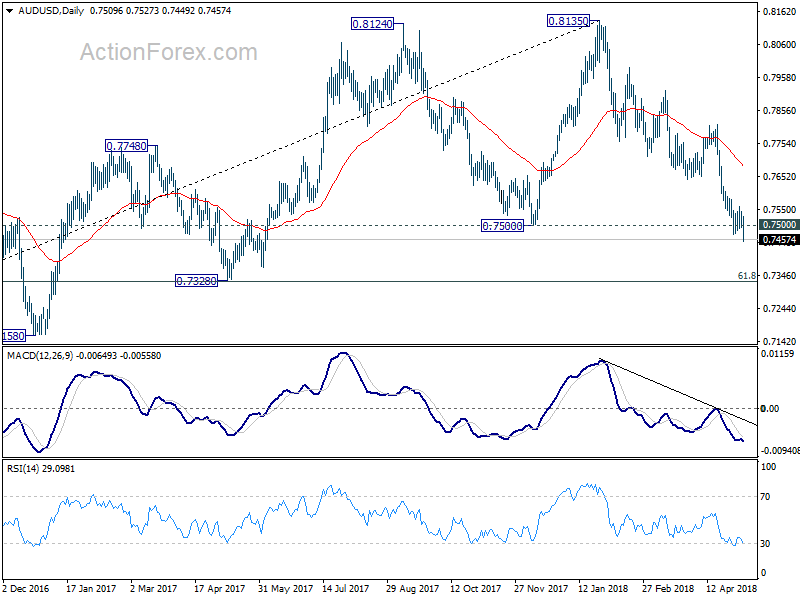

Selling of AUD and EUR came in later. AUD/USD traders should have finally made up them mind to push the pair through 0.7500 key support level. Such development should confirm medium term reversal in the pair and should pave the way to 0.7328 support next.

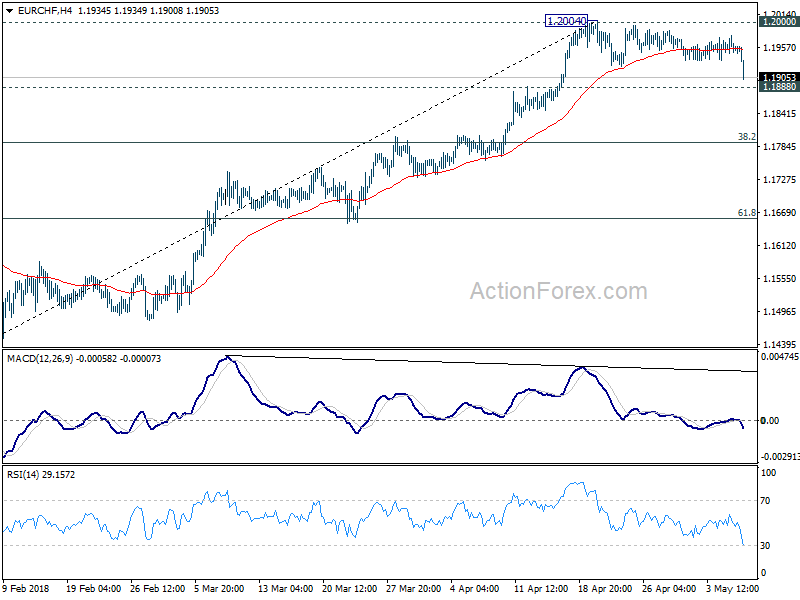

Also, the steep fall in EUR/CHF suggests that it's finally being rejected by 1.2 key handle. Break of 1.1888 support will confirm near term reversal. And deeper pull back should be seen to 38.2% retracement of 1.1445 to 1.2004 at 1.1790 next.

Decision Day: Trump, Oil And Iran

The most important event of the week is today

The oil price has closed above the $70 mark

Oil prices have seen one particular trend during the last few weeks and this trend has one particular direction- skewed to the upside. The US could change its position on Iranian nuclear deal which president Donald Trump has drummed many times as the worst deal in the history. If the US changes its stance on the Iranian nuclear deal, it would have an adverse impact on Iran's ability to raise foreign investments. A failure of foreign investment would curb the country's oil output which may remain flat or lower through 2025.

Back in January, President Trump agreed with the current deal however his frustration since then has only grown.

The most important event of the week is today. Investors would be watching the Donald Trump's decision on Iran very closely. The spillover effects of this aren't only going to be limited to Iran only, but also it will impact the US relations with allies. So, let's call it a decision day. The US must make a right decision and Trump should not take any hasty choice which would undo all the hard work done not only by the previous administration but also other nation's labour.

U.K, France and Germany, all have made it clear for the US that opting out of the Iranian nuclear deal will not be short of a disaster. Speculators have already placed their bets on the unpredictable nature of Donald Trump. The oil price has closed above the $70 mark yesterday because the odds are that he would do what he does the best; jeopardising the deal and surprise the world.

Having said this, he could still surprise world's leader by agreeing to the deal. Under such circumstances, I would expect retracement in the oil price and the WTI price could move back towards $65-68 range.

Iran, on the other hand, has also been unpredictable in its statements; the recent statement is the friendliest one where the President of the country, Hassan Rounani, confirmed that Iran may still stay in the agreement provided that the country's demands are met.

DAX Slips On Concerns Over Possible ECB Stimulus Extension

The DAX index has recorded considerable losses in the Tuesday session, after posting gains for two straight sessions. Currently, the DAX is at 12,875 points, down 0.56% on the day. On the release front, Germany indicators were solid, as Industrial Production and Trade Balance both beat their estimates. Later in the day, US President Trump will announce whether he will pull the US out of the Iran nuclear agreement.

Germany has posted some soft numbers recently, which could have major ramifications for ECB fiscal policy. The ECB cut its stimulus package at the start of the year from EUR 60 billion to 30 billion, while at the same time it extended the program to September. However, soft eurozone numbers, especially in Germany, have raised concerns that the bank may decide to again extend stimulus into 2019. German Factory Orders posted a second decline in the past three months, and the most recent PMIs in the services and manufacturing sectors also headed lower. On Tuesday, German indicators bounced back after a weak start to the week. Industrial Production climbed 1.0%, beating the estimate of 0.8% and ending a nasty streak of three straight declines. As well, Germany posted a trade surplus of EUR 22.0 billion, easily beating the estimate of EUR 19.9 billion. This marked a 4-month high.

The Federal Reserve’s newest regional Fed president, Thomas Barkin, delivered a major speech on Monday, and his tone was decidedly upbeat. Barkin said that the economy is “remarkably strong: above-trend growth, low unemployment, inflation at target”. Barkin added that although the labor market is strong, it is not causing pressure on wages, but low unemployment should lead to an increase in inflationary pressures. As for upcoming rate increases, Barkin was careful to remain mum on how many rate hikes he expects this year. The Fed raised rates in March by a quarter-point and continues to forecast two additional increases this year. However, some policymakers are calling for three more hikes, given the strong health of the US economy.

Euro Dips Under 1.19 Despite Solid German Numbers

EUR/USD has posted losses in the Tuesday session. Currently, the pair is trading at 1.1884, down 0.33% on the day. On the release front, Germany posted strong numbers, as Industrial Production and Trade Balance both beat their estimates. The US will release JOLTS Jobs Openings and Federal Reserve Chair Jerome Powell will speak at an event in Zurich. Later in the day, US President Trump will announce whether the US will leave the nuclear agreement with Iran. On Wednesday, the US releases PPI reports.

The ECB cut its stimulus package at the start of the year from EUR 60 billion to 30 billion, while at the same time it extended the program to September. However, soft eurozone numbers, especially in Germany, have raised concerns that the bank may decide to again extend stimulus into 2019. German Factory Orders posted a second decline in the past three months, and the most recent PMIs in the services and manufacturing sectors also headed lower. On Tuesday, German numbers were solid, but this didn’t prevent the euro from dropping lower. Industrial Production climbed 1.0%, beating the estimate of 0.8% and ending a nasty streak of three straight declines. As well, Germany posted a trade surplus of EUR 22.0 billion, easily beating the estimate of EUR 19.9 billion. This marked a 4-month high.

The Federal Reserve’s newest regional Fed president, Thomas Barkin, delivered a major speech on Monday, and his tone was decidedly upbeat. Barkin said that the economy is “remarkably strong: above trend growth, low unemployment, inflation at target”. Barkin added that although the labor market is strong, it is not causing pressure on wages, but low unemployment should lead to an increase in inflationary pressures. As for upcoming rate increases, Barkin was careful to remain mum on how many rate hikes he expects this year. The Fed raised rates in March by a quarter-point and continues to forecast two additional increases this year. However, some policymakers are calling for three more hikes, given the strong health of the US economy.

Italian Politics Weighs On The Euro

Capital markets are back to full capacity after yesterday’s May Day celebrations in parts of Europe.

Euro stocks are drifting lower despite the broad advances in Asia overnight, while crude prices come under some pressure ahead of President Trump’s decision on the Iran nuclear deal at 02:00 pm EDT.

The ‘mighty’ dollar again has found some traction as Treasury prices steadied despite the amount of U.S debt supply hitting capital markets this week (approx. +$73B, 3-, 10- and 30- year bonds).

Expect oil trading to dominate proceedings today amid speculation the U.S. may pull out of a nuclear accord with Iran, escalating tensions in the Middle East and potentially disrupting supplies from OPEC’s third-largest producer.

On Tap this week: Nafta talks resumed yesterday – it remains a critical period for the tri-nations, and its no surprise that the U.S is still pushing a hardline. On Thursday, the BoE takes center stage with its rate announcement, while U.S inflation data for April is due the same day.

1. Stocks mixed results

In Japan, the Nikkei share average rallied on Tuesday as banking stocks found support while Takeda Pharmaceutical climbed ahead of news the drug maker had agreed to buy London-listed Shire. The Nikkei ended +0.2%higher, while the broader Topix gained +0.4%.

Down-under, Aussie shares ended mostly flat overnight, coming off a three-month high as investors attempted to reduce their exposure before today’s federal budget. The S&P/ASX 200 index rose +0.12%. In S. Korea, tech shares also lifted the Kospi index, which rose +0.4%.

In Hong Kong, stocks end higher as Sino-U.S trade war fears ease. The Hang Seng index ended +1.4% higher, while the China Enterprises Index closed up +1.5%.

In China, stocks posted robust gains overnight, amid hopes that resumption of Sino-U.S talks next week in Washington could help avert a trade war. The blue-chip CSI300 index rose +1.2%, while the Shanghai Composite Index gained +0.8%.

In Europe, the Stoxx Europe 600 Index declined after two days of gains, dragged lower by oil and gas companies and miners. In Italy, stocks have been the worst performers in the region as the country-looks set for new elections, while in the U.K; the FTSE 100 index has found some support as it reopened following a long weekend.

Indices: Stoxx600 -0.4% at 388.5, FTSE +0.1% at 7577, DAX -0.7% at 12864, CAC-40 -0.5% at 5506, IBEX-35 -0.2% at 10124, FTSE MIB -2.1% at 24027, SMI -0.4% at 8944, S&P 500 Futures -0.3%

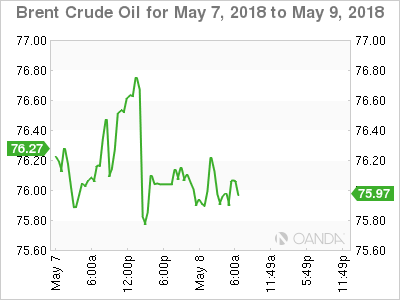

2. Oil prices fall as market awaits Trump decision on Iran, gold lower

Oil prices have retreated from their four-year highs overnight as the market waits on an announcement by President Trump on whether the U.S will reimpose sanctions on Iran.

If Trump pulls the U.S out of the multi-nation agreement, Iranian crude exports will be hit, adding to tightness in the oil market.

Brent crude futures are down -67c, or -0.9%, at +$75.50, having jumped +1.7% to settle at +$76.17 in yesterday’s session. U.S West Texas Intermediate (WTI) crude futures have dropped -78c, or -1.1%, to +$69.95 a barrel. They settled above +$70 for the first time since November 2014 on Monday.

Investors will take their cues from today’s announcement at 02:00 pm EDT – dealers believe that if President Trump goes back to the 2012 sanctions, the estimated loss of -0.4m barrels a day of Iranian supply based would be ‘bullish’ for the commodity market.

Ahead of the U.S open, gold prices remain subdued as the ‘big’ dollar hovers around its four-month peak. Spot gold is down about -0.1% at +$1,313.20 per ounce, after closing marginally lower in the previous session. U.S gold futures for June delivery are unchanged at +$1,314.10 per ounce.

3. Chances of BoE rate hike this week fade sharply

A lack of a Bank of England (BoE) interest-rate rise on Thursday – previously widely expected – the resumption of Brexit negotiations, and a slowing U.K economy is expected again to put the pound (£1.3510) under renewed pressure. Many do not foresee a rate rise this year, while the last phase of Brexit negotiations are likely to raise new concerns.

Even PM Theresa May’s government has been able to cast some doubt over the timing, as too have U.K rate ‘hawks,’ who suggest that the recent set of soft U.K data also appears to speak against a rate raise anytime soon.

The yield on U.S 10-year Treasuries has decreased less than -1 bps to +2.95%. In Germany, the 10-year Bund yield advanced less than +1 bps +0.53%, while in the U.K, the 10-year Gilt yield has dipped -1 bps to +1.391%.

Also of note, it’s a busy week with U.S supply. There is a combined +$73B of 3-, 10-, and 30-year securities to be taken down by Friday.

4. Dollar trades atop of its four-year highs

The DXY dollar index is expected to trade between 92 and 93 for the time being, while USD/JPY (¥108.94) is expected to come under some renewed pressure ahead of today’s Iranian nuclear deal announcement. If President Trump does happen to pull the U.S out of the pact or say he wants a renegotiation, there will be a flight to quality by some investors.

The pound (£1.3510) is under renewed pressure ahead of the U.S open after U.K Secretary of State for Foreign Affairs Boris Johnson criticized a proposal for a post-Brexit customs arrangement, favoured by PM Theresa May. GBP/USD is last down -0.4% at £1.3502, partly also due to broad-based dollar strength.

Note: Techies believe that a drop below £1.3487 would mark its lowest since Jan.

EUR/USD (€1.1889) has not been able to sustain initial gains above the psychological €1.19 handle despite Germany having presented some decent economic data. Italian political concerns seemed to be weighing on market sentiment. President Mattarella has called for a neutral government to be in place until the year-end to put together a 2019 budget plan before any new election.

The loonie (C$1.2975) is under pressure outright, as investors remain unsure that higher oil prices will lead to additional investment in infrastructure in energy production. Higher crude oil prices have yet to convince investors that demand for crude will persist at levels that will make additional spending on more production economically sensible.

In emerging markets (EM), the Turkish lira ($4.2939) has slumped to a fresh record low outright. Yesterday’s tweak of the reserve option mechanism (ROM) by the central bank (CBRT), lowering the upper limit for the forex maintenance facility to +45% from +55%, in a bid to tighten lira liquidity, has done little to help the currency.

5. Australian retail sales stall in March

Data overnight from Australia showed that the retail sales report for March came in below expectations.

According to the Australian Bureau of Statistics (ABS), sales were flat in seasonally adjusted terms, coming in below the +0.2% gain forecasted by the street. February’s increase was left unchanged at +0.6%.

Despite the soft March report, annual growth in sales actually accelerated, lifting to +3.2% from +3% m/m, the fastest increase since July last year.

Digging deeper, cafes, restaurants and takeaways, at +0.8%, led the falls, but other retailing (+0.6%), household goods retailing (+0.3%), department stores (+0.5%) and clothing, footwear and personal accessory retailing (+0.2%) also fell.

Note: The result was almost the opposite to that seen one month earlier, hinting that record Chinese tourist arrivals in February may have helped to temporarily boost spending levels during that period.

Awaiting Trump’s Decision On Iran Nuclear Accord

Notes/Observations

- All eyes will be on the announcement from US President Trump on the Iran nuclear deal at 14:00 ET (18:00 GMT)

- Germany Mar Industrial production come in above expectations

- Italian Center-right parties reject President Mattarella’s call for a neutral govt to be in place until year-end to put together a 2019 budget plan before any new election

Asia:

- Australia Mar Retail Sales M/M: 0.0% v 0.2%e; Q1 Retail Sales Ex Inflation Q/Q: 0.2% v 0.6%e

- New Zealand Q2 2-year Inflation Expectation Survey: 2.01% v 2.11% prior

- China Apr Trade Balance (USD): $28.8B v +$27.8Be; Exports Y/Y: +12.9% v +8.0%e; Imports Y/Y: 21.5% v 16.0%e . (Note: Trade surplus with US +$22.2B v $15.4B m/m)

Europe:

- ECB's Praet (Belgium, chief economist): euro area data pointed to some moderation but remained consistent with a broad-based and solid expansion. Reiterated view that an ample degree of monetary stimulus remained key to meeting the ECB’s inflation goal of 2%. Measures of underlying inflation had yet to show a convincing sign of sustained upward trend

- ECB's Smets (Belgium): recent economic data was consistent with continued robust expansion; ECB might have better understanding of data at June or July meetings. ECB could announce phaseout of QE over the summer

- Italy President Mattarella confirmed there was no possibility of forming a political govt; urged parties to support a "neutral" non-partisan govt. Was against having an early election in the summer because of need for 2019 budget

- Italy 5-Star Party leader Di Maio stated that he would not support a neutral govt; new elections should be held in July

- Italy’s Northern League: Italy must have a center-right govt or else immediate elections; ruled out Presidents suggestion of neutral government

- PM May has delayed discussion of a customs partnership with the EU until next Wednesday, May 16th

- ESM chief Regling reiterated that Euro Zone Finance Ministers could then consider prolonging loan repayment periods to provide Greece with further debt relief

Americas:

- US President Trump expected to make decision on Iran deal later on Tuesday

- Reports circulated that US and European diplomats were near a deal on Iran seeking to persuade PresidentTrump to stay in Iran nuclear deal

- Fed's Barkin (FOMC voter): Fed policy was still fairly accommodative (Doesn't comment on how many rate hikes he sees in 2018)

Economic Data:

- (NL) Netherlands Apr CPI M/M: 0.4% v 0.4%e; Y/Y: 0.9% v 0.9%e

- (NL) Netherlands Apr CPI EU Harmonized M/M: 0.6% v 0.6%e; Y/Y: 0.7% v 0.7%e

- (CH) Swiss Apr Unemployment Rate: 2.7% v 2.9%e; Unemployment Rate (seasonally adj)2.7% v 2.9%e

- (DE) Germany Mar Current Account Balance: €29.1B v €27.0Be; Trade Balance: €25.2B v €22.5B); Exports M/M: +1.7% v +1.8%e; Imports M/M: -0.9% v +1.0%e

- (DE) Germany Mar Industrial Production M/M: 1.0% v 0.8%e; Y/Y: 3.2% v 3.0%e

- (FI) Finland Mar Preliminary Trade Balance: -€0.2B v -€0.3B prior - (CH) Swiss Q1 UBS Real Estate Bubble Index: 1.10 v 1.21 prior

- (NO) Norway Mar Industrial Production M/M: -0.7% v -0.5% prior; Y/Y: 0.2% v 1.8% prior

- (NO) Norway Mar Manufacturing Production M/M: -0.1% v +0.2% prior; Y/Y: 0.9% v 0.2% prior

- (ZA) South Africa Apr Gross Reserves: $49.5B v $49.5Be; Net Reserves: $43.1B v $43.4Be

- (HU) Hungary Mar Industrial Production M/M: -0.7% v 0.0%e; Y/Y: 1.9% v 3.0%e

- (UK) Halifax House Prices M/M: -3.1% v -0.2%e; 3M/Y: 2.2% v 3.2%e

- (SE) Sweden Apr Budget Balance (SEK): B v 6.4B prior

- (TW) Taiwan Apr CPI Y/Y: 2.0% v 1.8%e; CPI Core Y/Y: 1.3% v 1.5%e; WPI Y/Y: 2.5% v 1.2%e

Fixed Income Issuance:

- (ID) Indonesia sold IDR0T (nil) in 3-month, 9-month Bills, 5-year, 10-year and 20-year Bonds (rejects all bids)

- (NL) Netherlands Debt Agency (DSTA) sold €1.79B vs. €1.5-2.5B indicated range in 0.75% July 2028 DSL bonds; Avg Yield: 0.676% vs. 0.791% prior

- (ES) Spain Debt Agency (Tesoro) sold total €4.505B vs. €4.0-5.0B indicated range in 6-month and 12-month bills (Apr 3rd )

- Sweden sold SEK5.0B vs. SEK5.0B indicated in 3-month Bills; Avg Yield: -0.8349% v -0.8596% prior; bid-to-cover: x v 3.46x prior

- (CH) Switzerland sold CHF513.7M in 3-month Bills; Yield: -0.858% v -0.849% prior

- (AT) Austria Debt Agency (AFFA) sold €1.15B vs. €1.15B indicated in 2028 and 2047 RAGB bonds

- Sold €650M in 0.75% 2028 RAGB bond; Avg Yield: 0.707% v 0.666% prior; Bid-to-cover: 2.21x v 2.45x prior

- Sold €350M in 1.5% Feb 2047 RAGB; Avg Yield: 1.459% v 1.477% prior; Bid-to-cover: 2.28x v 2.08x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.4% at 388.5, FTSE +0.1% at 7577, DAX -0.7% at 12864, CAC-40 -0.5% at 5506, IBEX-35 -0.2% at 10124, FTSE MIB -2.1% at 24027, SMI -0.4% at 8944, S&P 500 Futures -0.3%]

- Market Focal Points/Key Themes: European Indices trade mostly lower with the exception of the FTSE 100 which trades slightly higher after being closed for UK Bank Holiday yesterday. The Dax leads the decliners after outperformance yesterday, with shares of Deutsche Post a notable decliner after a miss on the top and bottom line. LafargeHolcim another decliner after a fall in EBITDA, with EOAN, Uniper, Munich Re, PNL, DSM and Axel Springer other decliners after earnings. To the upside Zalando trades higher after a Revenue beat. In the M&A space Virgin Money trades higher after confirming bid interest from CYBG, First Group trades lower after Apollo dropped their pursuit for the company. Shire trades higher after the board recommends the takeover offer from Takeda. Looking ahead notable earners include JD.com, Veritiv, Aramark and Crocs.

Movers

- Consumer Discretionary [ FirstGroup [FGP.UK] -6.4% (Apollo drops takeover attempt), Sky [SKY.UK] -1.5% (Comcast has filed formal notice to EC of intention to acquire Sky), Zalando [ZAL.DE] +3.5% (Earnings)]

- Industrials [ Deutsche Post [DPW.DE] -6.2% (Earnings), LafargeHolcim [LHN.CH] -3.1% (Earnings), Virgin Money [VM.UK] +8.3% (Confirm approach by CYBG), PNL [PNL.NL] -3.1% (Earnings)]

- Financials [Munich Re [MUV2.DE] -0.9% (Earnings)]

- Healthcare [Shire [SHP.UK] +4% (Confirms take over £49.0/shr by Takeda),

- Energy [Uniper [UN01.DE] -1.0% (Earnings)]

Speakers

- Sweden Central Bank (Riksbank) Apr Minutes: Members did discuss development of the exchange rate. Forecast for the repo rate had been revised down since the monetary policy meeting in February and indicated that slow increases in the repo rate would not be initiated until towards the end of the year.

- Riksbank Gov Ingves: Rate of inflation had developed well in line with target but was still not moving lastingly around the target. No completely on firm footing regarding inflation. Rapid SEK currency (Krona) appreciation could impede inflation

- Riksbank Dep Gov Ohlsson (dissenter): Inflation around 2% was decisive argument for rate hike

- Riksbank Member Skingsley: Significant part of recent SEK currency (Krona) weakness was seen as temporary; likely to support a rate hike in Oct or Dec

- Riksbank Member Floden: Supported the Repo rate path outlook but preferred smaller revision of forecasts. Hardly appropriate to support a rate hike in July and wanted to see clearer signs of underlying inflation not taken a weaker course

- Sweden Central Bank (Riksbank) Dep Gov Jansson (speech) stated that inflation needed continued support by monetary policy. Domestic economy was strong with inflation close to the 2% target

- Turkey President Erdogan reiterated view that weakness in TRY currency (Lira) had no fundamental or technical basis

- Fed Chair Powell (in Geneva) stated that Fed policy normalization was manageable for emerging markets. Risk sentiment would bear close watching as normalization proceeded. Many emerging markets had adopted more flexible exchange rates, and reduced their vulnerabilities. Some investors and institutions might not be well positioned

Currencies

- USD continued its firm tone and was at fresh 2018 highs against numerous pairs

- EUR/USD could not sustain initial gains above the 1.19 as Germany finally had some decent economic data. Italian political concerns seemed to weigh on sentiment. Italy 5-year Credit Default Swap at approx 91bps and at 2-week highs as the Center-right rejected President Mattarella’s call for a neutral govt to be in place until year-end to put together a 2019 budget plan before any new election.

- GBP/USD probed below the 1.35 level despite some analysts concerns that there were some hawkish risks at Thursday's BoE meeting (market currently not pricing anything at this time). Dealers noting that current UK economic conditions were at five year lows and un-phased by any potential for a hawkish surprise

Fixed Income

- Bund Futures trade 8 ticks lower at 159.18 as Italian/German 10-year gap hits the widest in 3-weeks at 127bps. Upside targets 159.75, while a return lower targets the 157.25 level.

- Gilt futures trade at 122.54 lower by 2 ticks, approaching the highs made in March. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Tuesday’s liquidity report showed Monday's excess liquidity fell to €1.892T from €1.898T prior. Use of the marginal lending facility decreased from €14M to €12M.

Looking Ahead

- (PT) Bank of Portugal Reports Apr ECB financing to Portuguese Banks: €B v €22.0B prior

- (RU) Russia Apr Light Vehicle Car Sales Y/Y: 15%e v 14% prior

- (AR) Argentina Central Bank (BCRA) Interest Rate Decision: Expected to leave 7-Day Repo Reference Rate unchanged at 40.00%

- (UK) Commons reconvenes after May recess

- 05:30 (AU) Australia Govt announces 2018/19 budget

- 05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

- 05:30 (EU) ECB allotment in 7-day Main Financing Tender ( - 05:30 (DE) Germany to sell €750M in 2030 and 2046 Inflation-linked bonds (Bundei)

- 05:30 (BE) Belgium Debt Agency (BDA) to sell €2.4-2.8B 6-month and 12-month Bills

- 05:30 (ZA) South Africa to sell combined ZAR2.4B in 2031, 2040 and 2044 bonds

- 06:00 (US) Apr NFIB Small Business Optimism: 104.7e v 104.7 prior

- 06:30 (EU) ESM to sell €2.0B in 3-month bills - 06:45 (US) Daily Libor Fixing

- 07:00 (RU) Russia announces upcoming OFZ bond auction (held on Wed)

- 07:00 (CL) Chile Apr CPI M/M: 0.1%e v 0.2% prior; Y/Y: 1.7%e v 1.8% prior, CPI Ex Food and Energy M/M: 0.2%e v 0.3% prior; Y/Y: No est v 1.6% prior

- 07:00 (BR) Brazil Apr FGV Inflation IGP-DI M/M: 0.6%e v 0.6% prior; Y/Y: 2.7%e v 0.8% prior

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:00 (HU) Hungary Central Bank (MNB) Apr Minutes

- 08:05 (UK) Baltic Dry Bulk Index

- 08:15 (CA) Canada Apr Annualized Housing Starts: 220.0Ke v 225.2K prior

- 08:55 (US) Weekly Redbook Sales

- 09:00 (EU) Weekly ECB Forex Reserves

- 10:00 (US) Mar JOLTS Job Openings: 6.10Me v 6.052M prior

- 10:00 (FI) ECB’s Liikanen (Finland)

- 10:30 (TR) Turkey Apr Cash Budget Balance (TRY): No est v -6.7B prior

- 11:30 (US) Treasury to sell 4-Week Bills

- 12:00 (US) DOE Short-Term Crude Outlook

- 13:00 (US) Treasury to sell 3-Year Notes

- (AR) Argentina Central Bank (BCRA) Expected to leave 7-Day Repo Reference Rate unchanged at 40.00%

- 16:30 (US) Weekly API Oil Inventories

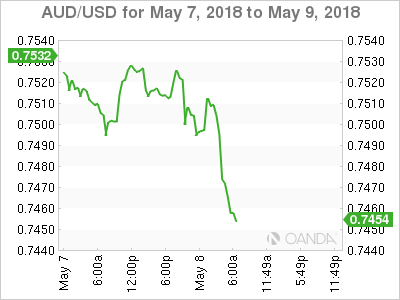

AUD/USD Bearish Consolidation

AUD/USD bearish pattern from 0.7813 (19/04/2018) pauses, currently trading at 0.7515 and approaching the 0.7495 range. Hourly resistance remains at 0.7879 (28/02/2018 high). The technical structure suggests short-term sideways trading moves.

In the long-term, the upward trend slows down after failing to reach key resistance at 0.8164 (14/05/2015 low). Key support stands at 0.6009 (31/10/2008 low). A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Edging Higher

USD/CAD bullish trend is contained, trading sideways since end-April. The pair is expected to head along the 1.2915. Hourly support and resistance are given at 1.2621 (23/02/2018 low) and 1.2949 (22/03/2018 high). The technical structure suggests short-term upward moves.

In the longer term, the pair is trading between resistance point at 1.3805 (05/05/2017 high) and support at 1.2128 (18/06/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head lower. The pair is trading above its 200 DMA