Sample Category Title

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

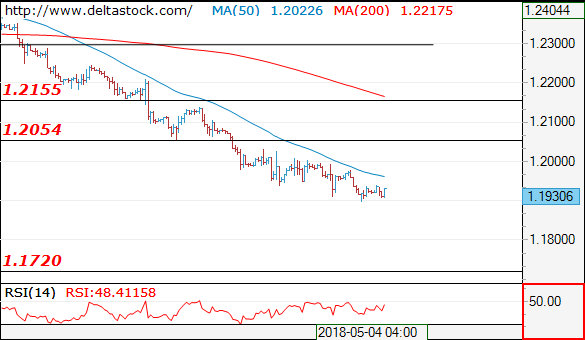

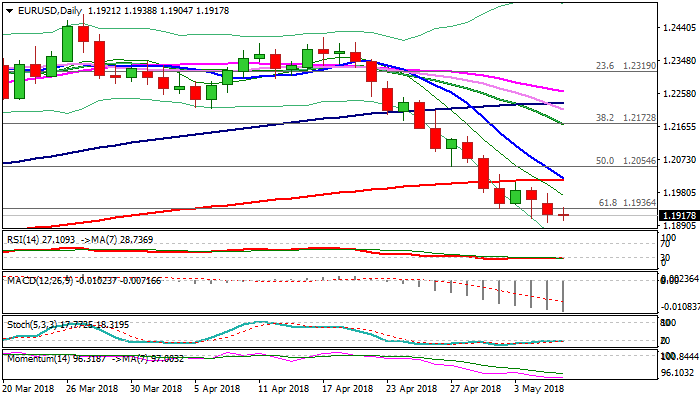

EUR/USD

Current level - 1.1930

The overall bias remains bearish, for a slide towards 1.1840, en route to 1.1720. Initial resistance lies at 1.2000 and crucial on the upside is 1.2060.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2060 | 1.2300 | 1.1900 | 1.1840 |

| 1.2160 | 1.2413 | 1.1840 | 1.1720 |

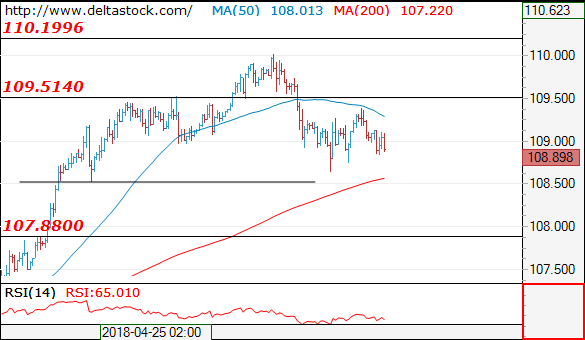

USD/JPY

USD/JPY

Current level - 108.89

My outlook is negative after the recent failure at 109.50, for a break through 108.50, towards 107.90.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 109.50 | 110.20 | 108.50 | 107.90 |

| 110.20 | 111.90 | 107.90 | 104.60 |

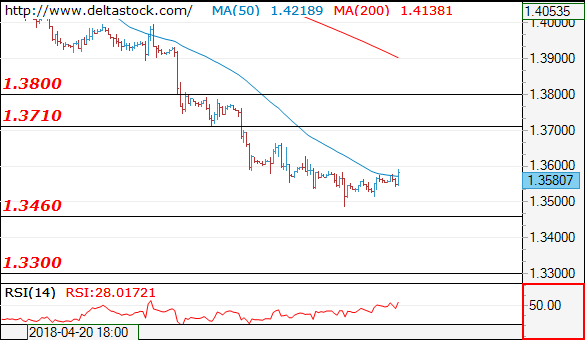

GBP/USD

Current level - 1.3580

Current rebound above 1.3480 is corrective, so a break through 1.3512 low will signal a renewal of the whole downtrend, towards 1.3460 and 1.3310.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3660 | 1.3990 | 1.3512 | 1.3460 |

| 1.3790 | 1.4100 | 1.3460 | 1.3310 |

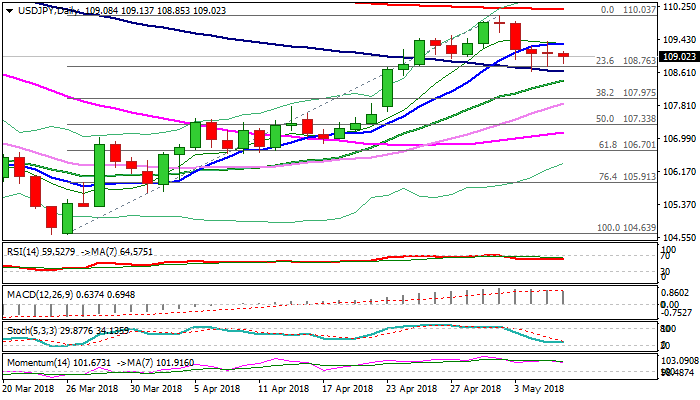

USDJPY Holds In Extended Directionless Mode Between 10 And 100SMA

The pair holds in choppy sideways mode for the third straight day, with the downside being contained by double Fibo supports at 108.83/76 (38.2% of 106.88/110.03 and 23.6% of 104.63/110.03 rally), reinforced by 100SMA, while 10SMA caps (currently at 109.31).

Monday's long-legged Doji confirmed indecision.

Daily techs are mixed and fresh direction signals could be expected on break of either side.

Loss of 108.83/64 pivots would expose rising 20SMA (108.42) and risk extension towards strong supports at 108 zone (double Fibo support / daily cloud top / rising 30SMA, which lay between 108.08 and 107.85.

Conversely, lift and close above 10SMA would signal formation of higher base and turn near-term focus towards cracked psychological 110 barrier and 200SMA (110.16).

Res: 109.13, 109.31, 109.88, 110.03

Sup: 108.76, 108.63, 108.42, 108.08

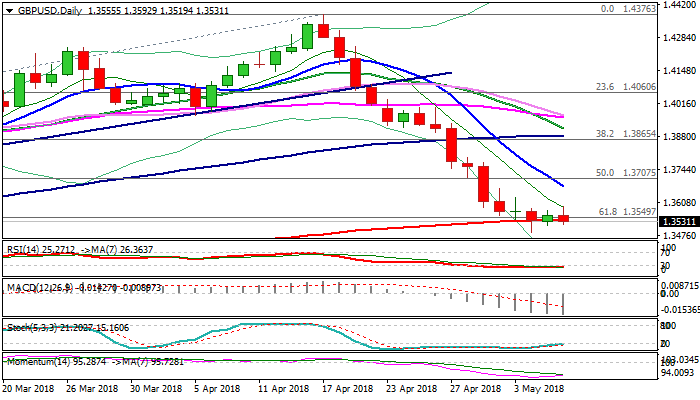

GBPUSD – Initial Signs Of Basing Near 200SMA Need Confirmation To Neutralize Persisting Downside Risk

Cable is holding around cracked 200SMA (1.3539) in early Tuesday’s trading, after steep fall from 1.4376 (17 Apr post-Brexit recovery peak) found footstep at this zone.

The pair generated initial positive signals on repeated close above 200SMA in past two days, which was underpinned by slow stochastic attempts to reverse from oversold territory and slowdown of strong bearish momentum.

Confirmation of basing requires stronger upside action and regain of falling 10SMA (currently at 1.3674) to sideline existing downside risk and signal correction.

Conversely, eventual close below 200SMA could be negative signal for extension of steep fall from 1.4376 and test of next strong support at 1.3442 (Fibo 38.2% of 1.1930/1.4376 recovery phase).

Res: 1.3575, 1.3593, 1.3629, 1.3674

Sup: 1.3515, 1.3486, 1.3442, 1.3400

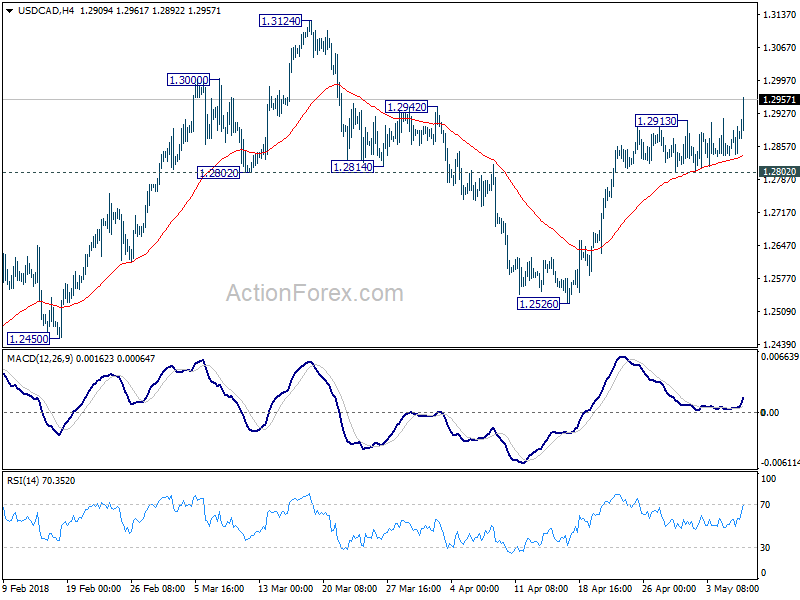

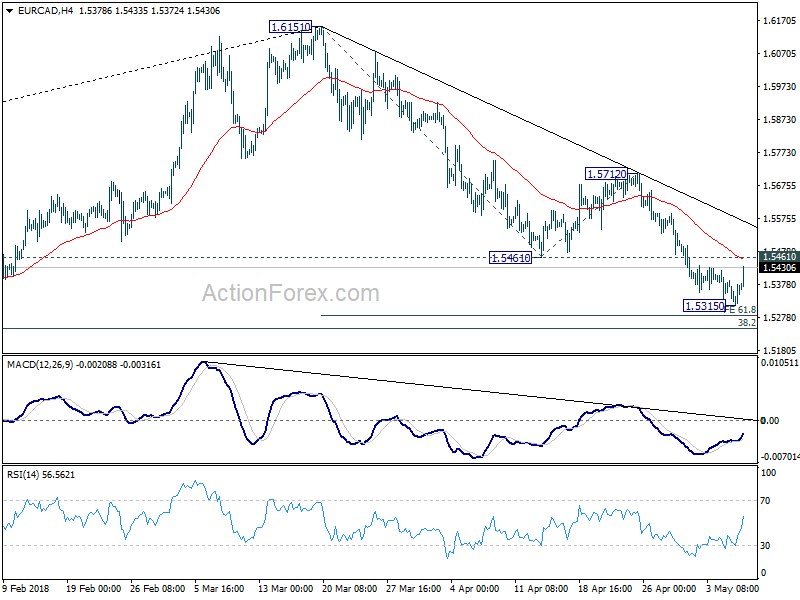

CAD tumbles broadly, EURCAD threatens bullish reversal

Canadian dollar tumbles broadly as the break of 1.2913 resistance in USD/CAD spills over to other pairs. There is no apparent trigger for the selloff but markets could be positioning ahead of Trump's announcement on Iran deal.

USD/CAD should now be heading to retest 1.3124 resistance next. And outlook will stay bullish as long as 1.2802 minor support holds.

Also, it looks like EUR/CAD's corrective fall from 1.6151 could be completed with three waves down to 1.5315, ahead of 61.8% projection of 1.6151 to 1.5461 from 1.5712 at 1.5286, the target we mentioned here. Immediate focus is now on 1.5461 support turned resistance. Break there will affirm this case of bullish reversal and target 1.5712 resistance next.

EURUSD – Close Below Key Fibo Support On Monday Reinforces Bearish Bias

The Euro holds in red in early European trading after brief recovery attempts were capped by broken Fibo support (61.8% of 1.1553/1.2555 ascend).

Monday's close below here was bearish signal, along with probes through round-figure 1.19 support, clear break of which would spark fresh acceleration lower and open targets at 1.1816 (22 Dec low) and 1.1790 (Fibo 76.4%).

Bearish techs support scenario as 14-d momentum continues to trend lower and converged 10/200SMA's are about to form death-cross which would generate fresh bearish signal and increase pressure.

Monday's high at 1.1978 marks initial resistance, guarding strong barriers at 1.20 zone (psychological resistance/200SMA) and only break here would neutralize immediate downside threats and signal stronger correction.

Mixed data from Germany (negative exports/imports, better than expected IP and widened trade surplus) made no significant impact on the euro. Focus turns towards release of EU economic forecasts and announcement of US decision about Iran's nuclear deal, due later today (18:00 GMT).

Res: 1.1938, 1.1978, 1.2016, 1.2052

Sup: 1.1897, 1.1846, 1.1816, 1.1790

Dollar Little Changed, Trump’s Iran Decision In The Spotlight

Here are the latest developments in global markets:

FOREX: The US dollar index, which gauges the greenback's strength against a basket of six major currencies, was practically flat on Tuesday ahead of a speech by Fed Chair Jerome Powell at 0715 GMT. It touched its highest level in five months yesterday, as the euro (which has by far the biggest weight in this basket) declined following some lackluster data out of the Eurozone.

STOCKS: US markets closed higher yesterday. The tech-heavy Nasdaq Composite climbed by 0.77%, while the Dow Jones and S&P 500 advanced by 0.39% and 0.35% respectively. It should be noted, though, that all these indices gave back some of their early gains yesterday following a tweet from US President Trump that he will announce his decision on the fate of the Iran nuclear deal today, at 1800 GMT. Futures tracking the S&P, Dow, and Nasdaq 100 are all currently in positive territory, albeit marginally so. In Asia, most of the major benchmarks were in the green. In Japan, the Nikkei 225 and the Topix gained 0.18% and 0.37% correspondingly, while in Hong Kong, the Hang Seng surged 1.28%. In Europe, futures tracking the major indices were a sea of red, pointing to a lower open today.

COMMODITIES: Oil prices pulled back from their recent highs, with WTI declining by 0.8% and Brent by 0.7%, ahead of a decision by US President Trump today at 1800 GMT on whether the US will withdraw from the Iranian nuclear deal. Oil prices are likely to move according to the result; higher in case the US leaves and lower in case it doesn't. It should be noted though, that markets seem positioned for the US to exit, so risks surrounding oil prices may be asymmetrical. A decision to stay in could generate a larger downside reaction than the corresponding upside one in case the US leaves, as it would probably come as a surprise (see below). In precious metals, gold prices are lower today, but by less than 0.1%. The yellow metal could also respond to the US announcement on Iran today, to the extent that such a decision increases or decreases geopolitical uncertainty in the Middle East.

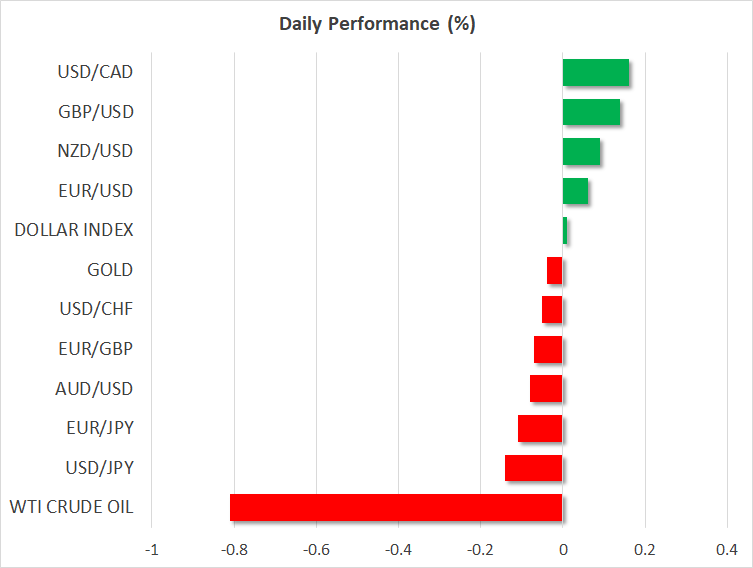

Major movers: Oil eases off highs ahead of Iran announcement; euro loses ground

The US dollar continued to climb yesterday, touching a fresh five-month high before retreating somewhat. Euro/dollar declined notably, briefly breaking below the 1.1900 handle following some disappointing data out of the Eurozone. The Sentix investors' sentiment index for May came lower than expected, likely amplifying the narrative that the bloc's economy is slowing down, as the ECB alluded to at its latest policy meeting. Euro/yen and euro/pound experienced similar retreats.

Today, all eyes will be on the US, where President Trump is expected to announce his decision on the Iran nuclear deal, at 1800 GMT. Under this deal, Iran agreed to limit its nuclear research in exchange for the easing of sanctions on its economy, and if the US pulls out of the accord today, that would likely involve re-imposing sanctions. Oil prices have rallied significantly in recent weeks on speculation for such an outcome, as new sanctions on Iran could remove a substantial amount of oil supply from the market.

Should the US indeed leave the deal, then prices could spike higher on the announcement. That said though, one must also sound a note of caution. Oil has already rallied substantially, which suggests that most of the “sanctions” narrative is already priced in. Thus, while an official confirmation could push prices a little higher from current levels, anything other than that may come as a surprise and hence, trigger a much sharper negative reaction in prices. For instance, if the US decides to give Iran another chance, or if the sanctions are watered down and are smaller than previously, then it wouldn't be a surprise to see a “sell the fact” reaction in oil, since investors already “bought the rumor”.

Besides oil, this decision could impact broader market sentiment as well, perhaps triggering reactions in safe haven assets. A potential imposition of additional sanctions on Iran could lead the nation to threaten restarting its nuclear program, thereby raising geopolitical uncertainty in the Middle East. In this sense, a US withdrawal from the accord could prove beneficial for the likes of gold and the Japanese yen, and vice versa.

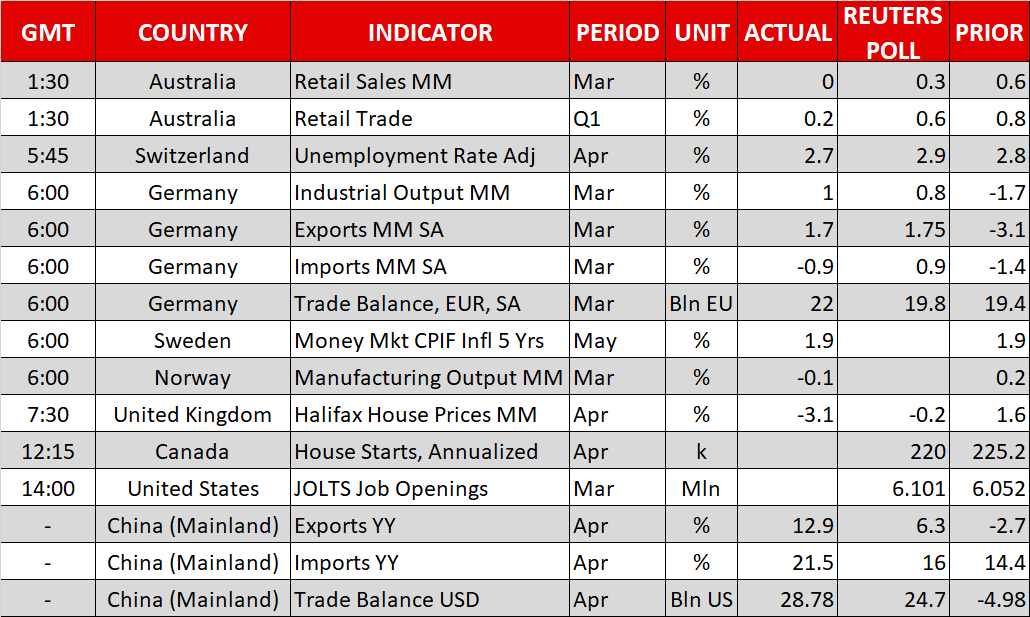

Day ahead: US JOLTS job openings and Canadian housing starts due, with Trump's take on Iran nuclear deal in focus

US JOLTS job openings and housing starts data out of Canada are some of the releases attracting attention out of Tuesday's calendar. However, geopolitics – the US administration's stance on the Iran nuclear deal – seem more likely to drive positioning during today's trading.

The Swedish central bank will be publishing the minutes from its latest monetary policy meeting at 0730 GMT, while the Bank's Deputy Governor Per Jansson will be talking on the economy and monetary policy one hour later. In this respect, krona pairs will be in focus.

Also at 0730 GMT, house price data for April will be made public out of the UK. The Halifax House Price Index is expected to show a 0.2% m/m decline in prices, after a 1.5% gain in March, which constituted the fastest growth in prices since August.

Canadian housing starts data for the month of April are scheduled for release at 1215 GMT, while the US will see the release of JOLTS job openings figures for March at 1400 GMT. The number of openings is anticipated to come in at 6.1 million, roughly 50k more than in February.

With oil prices trading around their highest since late 2014, the API's weekly report on crude oil stocks will be watched when it hits the markets at 2030 GMT. Of more importance though, will be President Trump's decision on the Iran nuclear deal – whether to withdraw from the deal and impose fresh sanctions on Iran. In a tweet yesterday, the US President said he will make an announcement on the issue today after 1800 GMT.

In equities, Walt Disney is among companies releasing quarterly results today. It should be kept in mind though that besides corporate earnings, the Trump administration's decision on Iran can also act as a major driver of equity market sentiment.

Fed Chair Jerome Powell is participating in a panel discussion on “Monetary Policy Influences” hosted by the Swiss National Bank and the IMF. The discussion has started at 0715 GMT.

In US politics, the outcome of primary election battles in Indiana, North Carolina, Ohio and West Virginia will be known by Tuesday night. These will determine those individuals running for the midterm elections in November; President Trump has favored certain candidates.

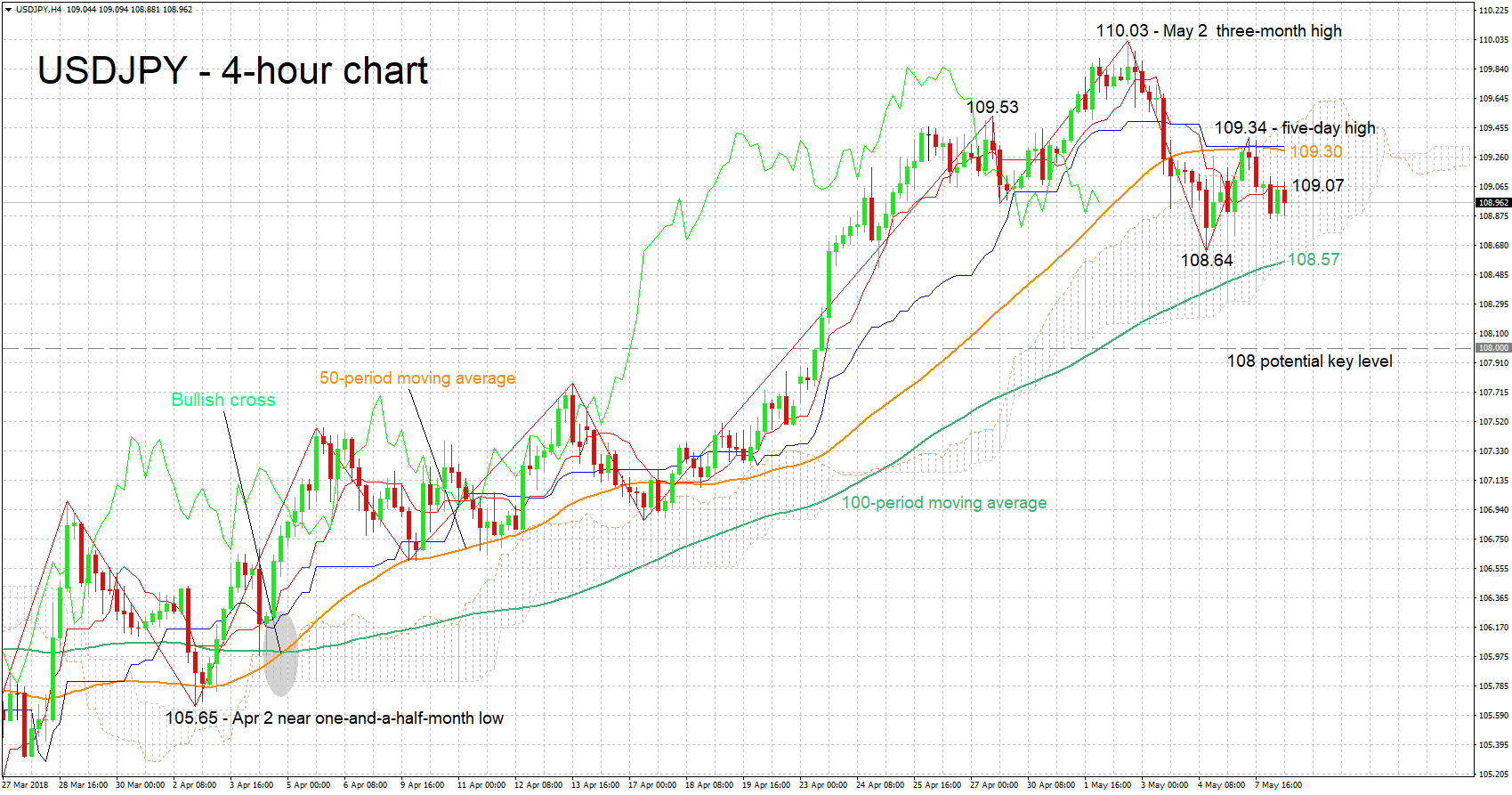

Technical Analysis: USDJPY looking bearish-to-neutral in the short-term

USDJPY has retreated a bit after recording a five-day high of 109.34 during Monday's trading. The Tenkan- and Kijun-sen lines are negatively aligned in support of a bearish short-term picture. Notice though that the two have flatlined as well, overall pointing to a bearish-to-neutral market bias.

Rising geopolitical uncertainty in the aftermath of the US administration's decision on the Iran nuclear deal could divert funds into the safe-haven perceived yen, pushing USDJPY lower. Support to declines could come around the current level of the 100-period moving average at 108.57 which coincides with the Ichimoku cloud bottom; the area around this level encapsulates a previous bottom at 108.64 as well. Steeper losses would increasingly turn the attention to the 108 round figure.

On the upside and in case uncertainty is seen as easing, the pair might propel higher. Immediate resistance could be coming around the Tenkan-sen at 109.07 (including the 109 handle). Stronger bullish movement might meet a barrier around the 50-period MA at 109.30; the region around this includes yesterday's high (109.34), the Kijun-sen (109.33) and the Ichimoku cloud top (109.46).

US releases due later on Tuesday can also spur positioning on the pair.

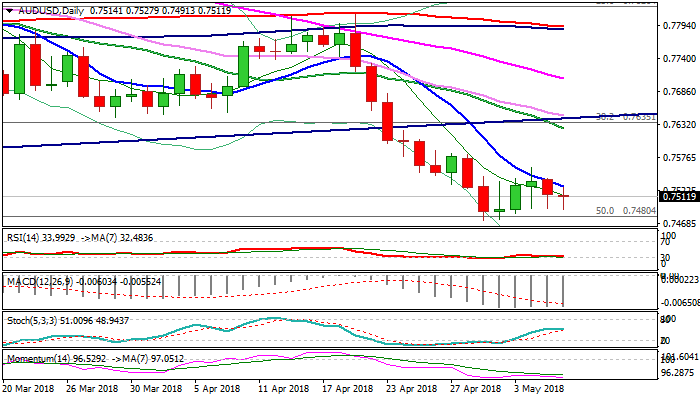

AUDUSD Remains At The Back Foot After Upbeat Chinese Data Partially Offset Impact From Negative Australian Figures

The pair remains in red for the second straight day on Tuesday, following recovery rejection at 0.7560 last Friday.

Aussie was down in Asia on weaker than expected Australian retail sales data but managed to recover a part of losses after upbeat Chinese data (exports and imports strongly overshot forecasts in Apr while trade surplus widened).

Near-term outlook remains negative as falling 10SMA (currently at 0.7529) continues to cap and maintain pressure, together with falling thick 4-hr cloud and weakening momentum studies. Fresh weakness repeatedly probed below 0.75 psychological support (without firm break so far) keeping recent low at 0.7472 in focus.

Break here would generate strong signal for continuation of larger downtrend from 0.8135 (2018 high) and expose next support at 0.7370.

Markets are focusing on one of the key events this week, President Trump’s decision on whether to pull out from nuclear agreement with Iran, as US withdrawal from the deal would increase global uncertainty that could bring the greenback under pressure.

Break and close above 10SMA would be initial positive signal for AUDUSD, while lift above Friday’s recovery high at 0.7560 is needed to spark stronger recovery and open pivotal barrier at 0.7602 (Fibo 38.2% of 0.7812/0.7472 downleg).

Res: 0.7529, 0.7560, 0.7583, 0.7602

Sup: 0.7491, 0.7472, 0.7456, 0.7420

USD/JPY Indecisive Price Action Between 109 And 110

The USD/JPY is at key zone that could determine whether price will build a larger bearish correction or continue the bullish trend. Price would need to break above the previous top at 110 to confirm the uptrend whereas a break below the support trend lines (blue) near 109 indicate that a larger bearish correction within wave X (pink) becomes more likelytowards 108 and 107.50 support levels. A bullish breakout above the 110 resistance level could indicate an extension of the wave W (pink) towards the 50% Fib at 111.50.

The USD/JPY could perhaps be building a larger ABC (blue) zigzag correction but a break above the 100% Fibonacci level and resistance zone at 110 invalidates this wave pattern. A break below the support trend line (blue) is needed before such an ABC becomes more likely, otherwise the currency pair is in a difficult spot at the moment.

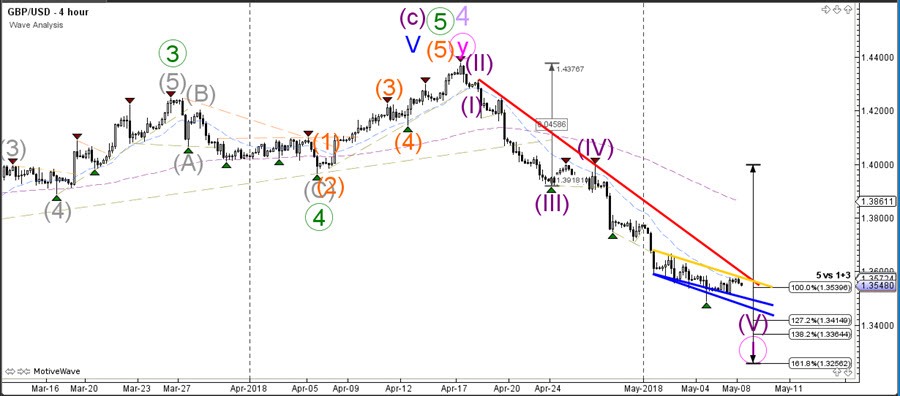

GBP/USD Downtrend Prepares For Bearish Breakout Below 1.35 Support

The GBP/USD bearish momentum is slightly weakening but price action remains solidly in downtrend. A bearish breakout below the 1.35 support zone could see price fall towards the Fibonacci targets of wave 5 (purple). Price action remains bearish as long as price stays below the resistance trend line (red) but a bullish break above that resistance would indicate the completion of wave 1 (pink) and the start of wave 2.

The GBP/USD could have completed a bullish retracement to the Fibonacci levels of wave 4 (green) which could act as a reversal zone for a downtrend continuation. A break above the 61.8% Fibonacci retracement level could indicate the potential end of the downtrend whereas a break below the support trend line (green) could indicate a downtrend continuation towards the Fibonacci targets of wave 5 (green).

Currencies: USD Rally Slows As Markets Await US Decision On Iran Deal

Rates: Trump’s verdict on JCPOA throws shadow over trading

Core bonds traded sideways yesterday and that could remain so today. Heavy supply is negative, but could be balanced by uncertainty on the outcome of tonight’s verdict by US President Trump on the Iranian nuclear accord. Rumours suggest he’ll extend the negotiation period, but Trump has proven in the past that nothing can be taken for granted.

Currencies: USD rally slows as markets await US decision on Iran deal

The dollar maintained a cautiously positive momentum yesterday, especially against the euro. Today’s eco calendar is thin. (FX) Markets await the US decision on the Iran deal. Several options are possible, but we assume that the outcome might leave the USD positive momentum intact.

The Sunrise Headlines

- US stock markets gained around 0.35% with Nasdaq outperforming (+1%) led by Apple. Asian stock markets trade positive as well this morning with China profiting (+1%) from strong trade data.

- US President Trump said he would announce today his decision on the landmark Iran nuclear accord that he has repeatedly condemned. Some European officials suggest he would leave more time for negotiations. (WSJ)

- Richmond Fed Barkin, 2018 voter, says US monetary policy is still accommodative and “it is hard to argue that accommodation is appropriate when unemployment is low and inflation is effectively at our target.” (BB)

- The ECB is likely to move over the summer to gradually phase out its bond-buying program, perhaps announcing a decision after its July 26 policy meeting, ECB Smets said. (WSJ)

- China's exports rebounded more strongly than expected in April (12.9% Y/Y), suggesting global demand remains relatively resilient and providing a cushion to the economy amid a heated trade dispute with the US. (Reuters

- Australian retail sales were unchanged and below consensus (0.2% M/M) in March as a rise for food sales was offset by falls in other industries. AUD/USD slid back below the 0.75 mark. (FT)

- Today’s eco calendar contains US NFIB Small Business Optimism and German industrial production data. Fed Powell and ECB Liikanen speak. The Netherlands, Austria, Germany and the US tap the bond market

Currencies: USD Rally Slows As Markets Await US Decision On Iran Deal

USD rally slows as markets await US Iran decision

In line with end last week, some ‘by default USD buying’ continued yesterday. EUR/USD dropped below the 1.1915/35 support and filled bids near 1.19, but there were no sustained follow-through gains. Dollar strength prevailed, but the news flow was also tentatively euro negative (disappointing German factory orders; risk of new elections in Italy). USD/JPY rebounded to the 109.40 area, but eased later in the session. EUR/USD closed the day at 1.1922. USD/JPY finished at 109.09. In the end, there was too little news to inspire a clear direction move.

Overnight, Asian equities mostly show solid gains. Chinese foreign trade data were strong (a big rise both in imports and exports). The politically sensitive surplus with the US also widened sharply. For now, we see little direct impact on FX. Oil stabilizes off recent highs as markets await US president Trump’s decision on the nuclear deal with Iran. The impact from the oil price on the dollar remains modest for now. The Aussie dollar fell back to AUD/USD 0.75 on disappointing Australian retail sales.

Today, the eco calendar again only contains second tier eco data in the US and in Europe. Markets might give some more attention to the German production after recent poor EMU data. More disappointing news might weigh on the euro. Yesterday, Fed comments tilted to the hawkish side, but with no big impact on the dollar. Markets will look forward to decision of President Trump on the nuclear deal with Iran. Several options area open (from the US leaving the deal to some kind of ‘kicking the can down the road’ scenario). The recent rise of the oil price suggests that, at least the oil market already discounts quite a hawkish US approach. We hold the working hypotheses that the US Iran decision won’t derail USD positive momentum. If EUR/USD breaks below 1.19, next high profile support comes in in the low 1.17 area. USD/JPY underperforms USD/EUR and this might continue to be the case.

Yesterday, EUR/GBP declined off Friday’s correction top, mostly on euro weakness. The pair closed the session at 0.8794. Today, the UK eco calendar is also thin. The UK political debate on Brexit continues (Vote in the House of Lords). Markets are also couting down to the BoE policy decision on Thursday. The ‘bad news’ (no rate hike this week) is probably discounted. Even with no rate hike, the BoE might maintain a moderately hawkish tone. If so, it might be a (temporary) supportive for sterling. Combined with euro softness. EUR/GBP might drift a bit further south in the 0.87 big figure going into the BoE policy decission

EUR/USD downside pressure persists