Sample Category Title

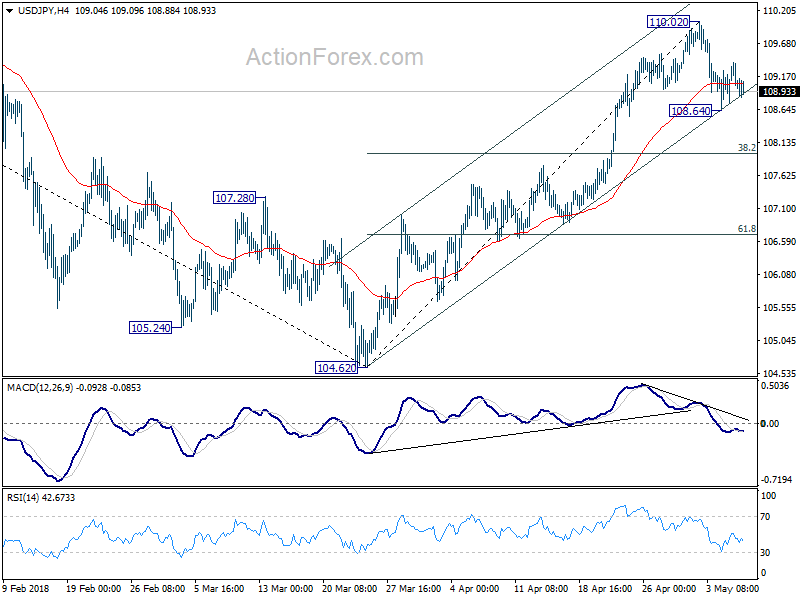

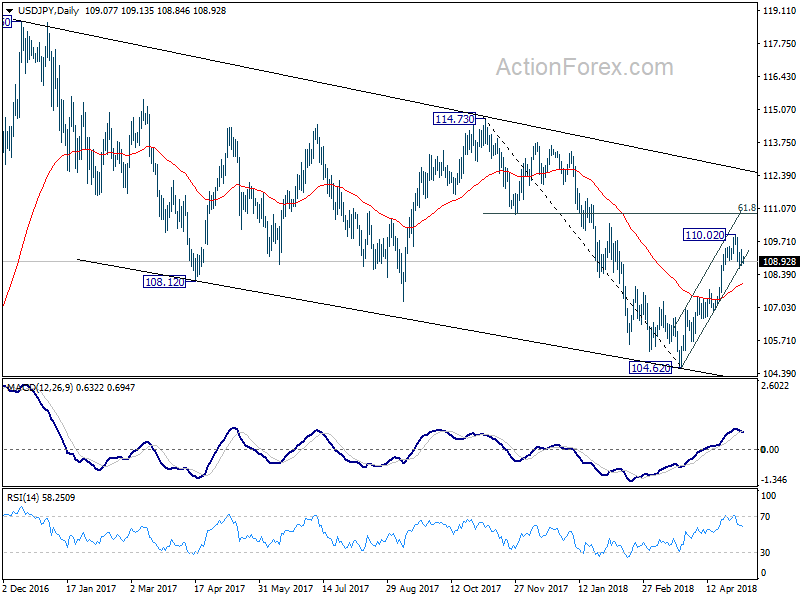

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.76; (P) 109.07; (R1) 109.40; More...

Intraday bias in USD/JPY remains neutral for consolidation below 110.02 short term top. Below 108.64 minor will bring deeper pull back. But downside should be contained by 38.2% retracement of 104.62 to 110.02 at 107.95 to bring rebound. On the upside, break of 110.02 will resume the rise from 104.62 to t 61.8% retracement of 114.73 to 104.62 at 110.86 next.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 55 day EMA (now at 107.95) holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above. However, sustained break of 55 day EMA will dampen this bullish view and turn focus back to 104.62 low instead.

China Trade Surplus with US Highest This Year; No Deal from Trade Talk but Not Yet Hopeless

China recorded a trade surplus of US$ 28.8B in April, beating consensus of US$ 27.5B. In March, China reported a deficit of US$ 5B due to seasonal factor. Compared with the same period last year, trade surplus narrowed by -23.1%. The +12.9% y/y increase in exports was overshadowed by a +21.5% jump in imports. Specifically, its trade surplus with the US expanded to US$ 22.2B, up from US$15.4B a month ago. In the first four months of the year, China's trade surplus with the US reached US$ 80.4B. The data failed to do any help to soothe the recent trade tensions between the world’s two biggest economies.

No Breakthrough in First Trade Talk

The US-China trade talk on May 3-4 ended a joint statement, let alone a deal. Media reported that the White House demands to reduce US trade deficit with China by US$ 200B by the end of 2020, from 2018 levels. Furthering the effort to reduce trade deficit, China’s purchases of US goods should represent at least 75% of a commitment to a US$ 100B increase in purchases of US exports for the 12 months beginning June 1 2018, and at least 50% of China’s commitment to an additional US$ 100B increase in purchases of US exports in the 12 months beginning June 1, 2019. The US has also lain down requests on the protection on the US tech industry and intellectual property, restrictions on Chinese investment in “sensitive US technology sectors or sectors critical to US national security”, China’s opening up of markets for US investment.

On China’s side, it requests the US to remove the trade restrictions announced over the past two months. For instance, the US should stop imposing 25% additional tariffs on Chinese products, adjust the export ban on ZTE and lift bans on exports of integrated circuits to China. China also demands the US not to initiate any Section 301 investigation against China, which has been scheduled on May 15.

Trade War is Still Not Our Base Case

Little has been agreed upon after the meeting last week While this signals that the US may impose US$ 50B of tariffs on 1 300 Chinese imports when its public comment period on the proposed sanctions ends on May 22, we remain hopeful of an eventual deal would be reached. Liu He, the vice premier of the Chinese Communist Party (CCP) as well as the top economic official, will arrive Washington next week to continue the discussions with US president Donald Trump's economic team. We notice that the Chinese government has softened its tone over trade issues. The editorial (http://www.xinhuanet.com/mrdx/2018-05/06/c_137158886.htm) of Xinhua news, CCP’s mouthpiece, over the weekend described the trade talk as frank, highly- effectively and constructive. It noted that the talk itself has set a positive beginning for avoiding further escalation of trade tensions. Meanwhile, a news report by Economic Information Daily (http://www.jjckb.cn/2018-05/07/c_137160241.htm) revealed that China’s Commerce Department has begun studying the possibility of lowering tariffs of vehicles and some daily necessities.

Oil At Four-Year High Ahead Of US President’s Iran Deal Announcement

During yesterday's trading session Crude Oil WTI rose above $70 for the first time since 2014, as US President Trump announced that he would reveal his decision on the Iran Deal today at 18:00 GMT. The indications are that he will withdraw from the agreement, calling it one of the “worst deals ever made”. This is despite strong pressure from European allies to stay the course and make amendments if necessary. The price is up 10% over the last month due to this concern so it is possible that there is a “buy the rumour sell the fact” trade taking place, as the price has dropped back from yesterday's high.

Swiss Consumer Price Index (YoY) (Apr) came in at 0.8% against an expected 0.9%, from the previous 0.8%. Inflation has been rising since it bottomed in 2015, with the current level not seen since 2011. Increases in fuel prices are among the main contributors to the higher readings. USDCHF moved higher from 1.00233 to 1.00294 following this data release.

US Consumer Credit Change (Mar) came in at $11.62B v an expected $16.00B, against a previous $10.60B, which was revised up to $13.64B. This data release shows a continued decline in consumer credit, with the data down from last month when the higher revision is taken into account. The data missed its consensus by a wide margin and the metric has more than halved since the January high of $28.05B. Credit card debt fell by the largest amount in more than five years, down $2.6B. GBPUSD fell from 1.35664 to 1.35541 after this data release.

Australian Retail Sales (MoM) (Mar) fell to 0.0% against a consensus of 0.3%, from 0.6% previously. The lower number suggests that the RBA will have to continue its policy of holding rates steady for some time. This came after the beat last month, with the AUD reacting badly to the data release, falling from 0.75212 to 0.74918.

EURUSD is down -0.05% overnight, trading around 1.19163.

USDJPY is down -0.02% in early session trading at around 109.075.

GBPUSD is down -0.03% this morning, trading around 1.35523.

USDCAD is up 0.21% overnight, currently trading around 1.29085.

Gold is down 0.15% in early morning trading at around $1,312.10.

WTI is down -0.03% this morning, trading around $69.93.

Focus Shifts To Trump Iran Deal Announcement

At 07:15 GMT, US Fed Chairman Powell is due to deliver a speech titled “Monetary Policy Influences on Global Financial Conditions and International Capital Flows” at the High Level Conference on the International Monetary System, hosted jointly by the Swiss National Bank and International Monetary Fund, in Zurich. Comments made could result in moves in USD crosses.

At 09:30 GMT, The Australian Budget Release will take place. This annual event outlines the government’s spending and income levels for the year ahead, including planned investment and borrowing. AUD crosses may be impacted by the by this release.

At 12:15 GMT, Canadian Housing Starts s.a (YoY) (Apr) will be released with an expected number of 220K from a previous 225K last month. This data is showing strong performance, despite indicators that the headline number will decline this month. The previous three readings beat expectations. CAD pairs could see an increase in price movement from this data.

At 14:00 GMT, US JOLTS Job Openings (Mar) will be released with the headline number expected to be 6.020M from 6.052M previously. This metric reached a high of 6.31M in March, showing job creation is strong and the labour market is dynamic. USD pairs may react to this data.

At 18:00 GMT, US President Trump is expected to speak about the Iran Deal from Washington D.C. He has spoken about scrapping the deal in the past and re-imposing sanctions against the country. This event could impact global markets, especially USD and Middle Eastern Currencies.uni

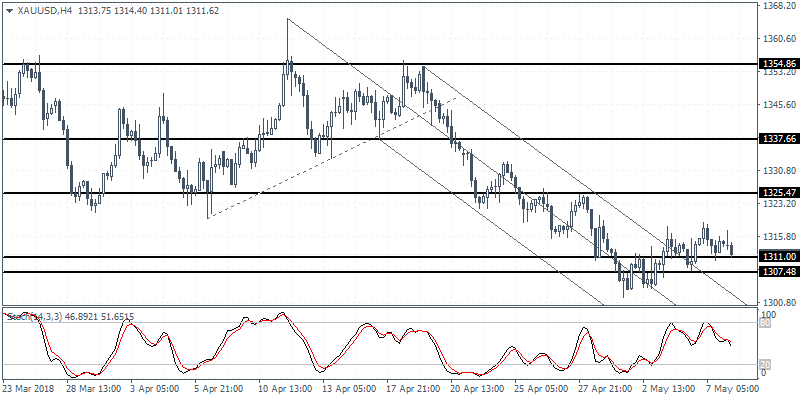

XAUUSD Intraday Analysis

XAUUSD (1311.62): Gold prices gave up the modest gains logged in the previous day as price action was seen falling back to the support level of 1311 - 1307 region. We expect prices to remain consolidating at this support level. A rebound in gold prices could signal a possible move to the upside. The resistance level at 1325 is likely to be the upside target, unless gold prices breach the current support. A break down below the support level could send gold prices falling toward the 1300 level.

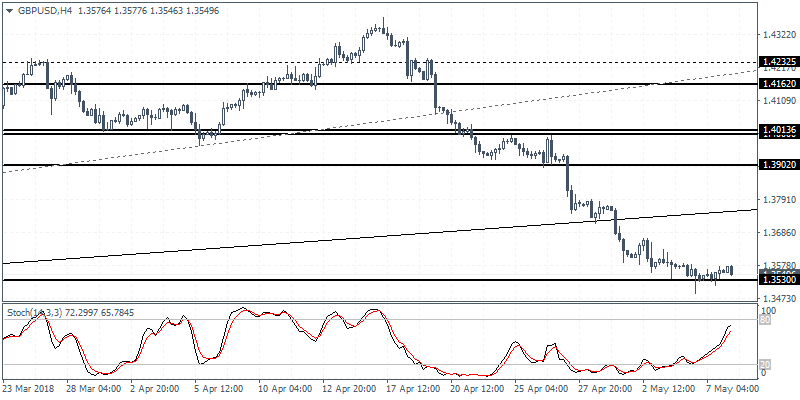

GBPUSD Intraday Analysis

GBPUSD (1.3549): The British pound was seen consolidating near the support level for the past few days. We expect this sideways price action to remain in place heading into this Thursday's BoE meeting. With the Stochastics showing a hidden bearish divergence, there is a strong possibility for GBPUSD to break down below the support level at 1.3530. In this case, further declines could push the GBPUSD lower to the 1.3000 round number support. To the upside, a close above the previous highs of 1.3580 is required in order to support any upside move.

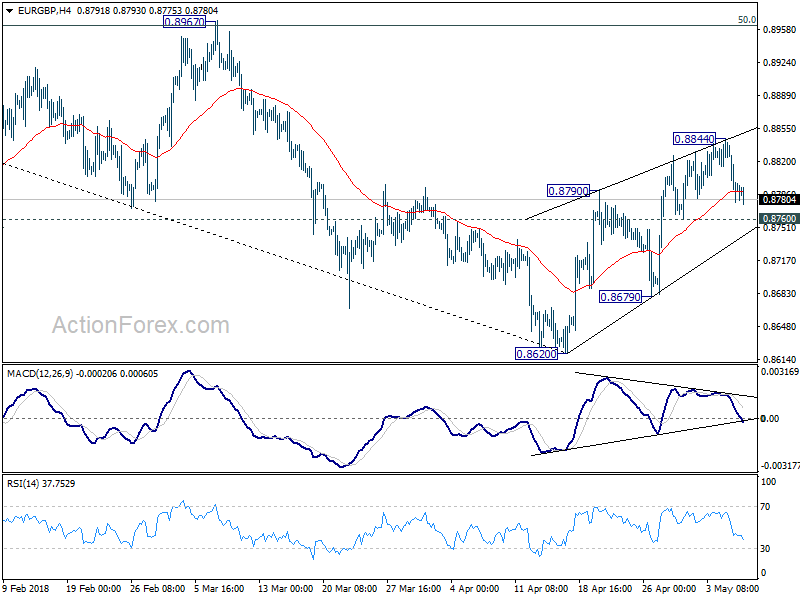

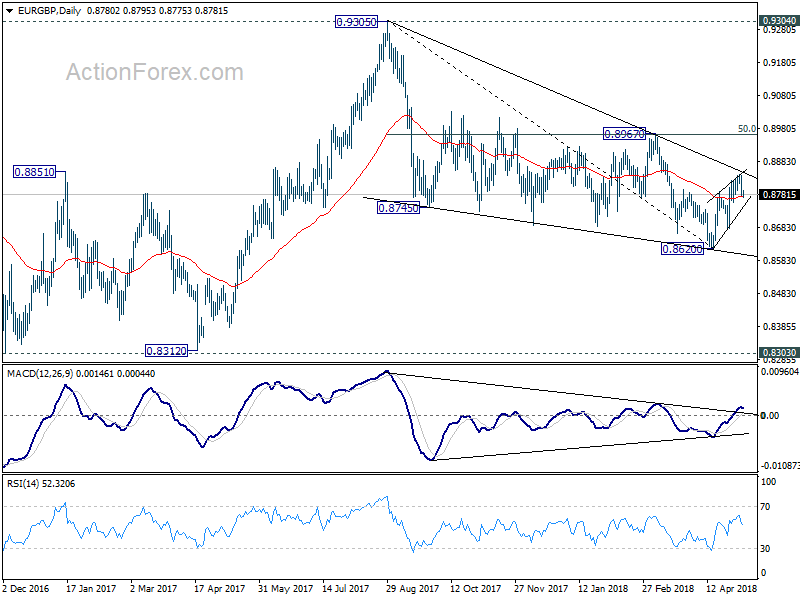

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8769; (P) 0.8803; (R1) 0.8828; More...

Intraday bias in EUR/GBP remains neutral for the moment. Loss of momentum as seen in 4 hour MACD and the steep retreat from 0.8844 argues that rebound from 0.8620 might be completed. Break of 0.8760 minor support will turn bias to the downside for 0.8679. Break there will likely resume whole decline from 0.9305 through 0.8620 low. On the upside, above 0.8844 will revive near term bullishness for 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963).

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

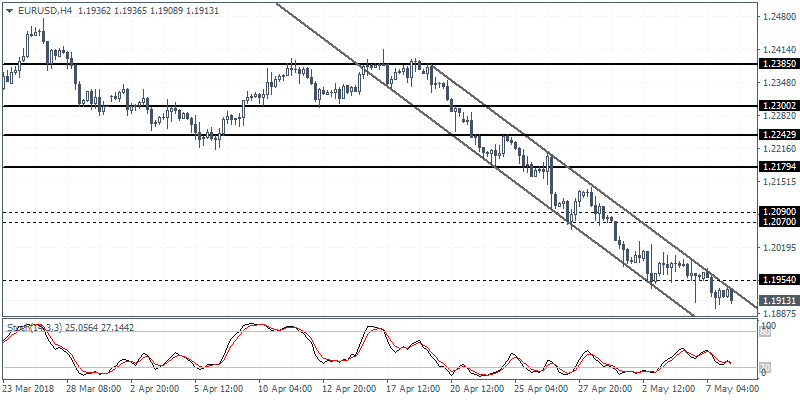

EURUSD Intraday Analysis

EURUSD (1.1931): The EURUSD was seen continuing to trade weaker but with price action trading in the support zone of 1.1960 - 1.1920, we could expect to see a reversal at this level. In the event that price action breaks below this support level, then we expect the declines to push lower toward the next main support level at 1.1730. Alternately, with the Stochastics currently showing a higher low against the lower low in price, we could expect a rebound. This can be confirmed on a daily close above 1.1954 level.

Fed Powell Speech, Trump To Decide On Iran Sanctions Today

The markets were seen trading subdued on the day with price action staying rather flat. Economic data on Monday was quiet with only the Fed member speeches from Bostic and Barkin.

The Eurozone Sentix investor confidence was seen easing back for the fourth consecutive month, while the German factory orders report showed another month of decline at 0.9%. The previous month’s data was seen to be revised higher.

Looking ahead, the economic calendar for the day will see the release of the Swiss unemployment figures. Forecasts show no change to the Swiss unemployment rate which is expected to remain steady at 2.9%.

The German industrial production figures will be coming out later today with expectations pointing to a 0.8% increase on the month following a 1.6% decline the month before. German trade balance numbers are also expected during the day.

The Fed Chair, Jerome Powell is expected to speak early in the day. Powell will be speaking at a conference in Zurich. His speaking engagement comes a week after the Federal Reserve left interest rates unchanged.

Australia's annual budget release is expected later although it is unlikely to be a major market moving event. In the U.S. President Trump announced that his administration would announce its decision whether or not to pull out of the Iran nuclear deal. Oil prices have risen steadily in anticipation of a U.S. pullout from the deal.

Trump Will Announce His Stance On The Iranian Nuclear Deal

Market movers today

Today at 20:00 CEST, US President Trump will announce his stance on the Iranian nuclear deal. This is particularly important for the oil market as there is a risk of Iran's oil exports being hit by new sanct ions.

Today is another quiet day in terms of economic data releases. In Sweden, we have multiple releases including the Prospera survey and the Riksbank minutes (see page 2).

In the US, we have tier 2 items including NFIB small business optimism and JOLTS job data. Fed Chair Jerome Powell is due to speak this morning, but he is unlikely to provide more information on a Fed bent on delivering two-three more hikes this year.

Selected market news

Geopolitics is set to take centre stage amidst a light economic schedule, as US President Trump is due to reveal his stance on the Iranian nuclear deal at 20:00 CEST. Worries over Iran sent WTI oil punching through USD70 a barrel for the first time since November 2014.

Robust demand and OPEC-curtailed supply have left the oil market tight and vulnerable to event shocks. Event risk revolves around Trump init iat ing sanctions on Iran , as the US waiver on sanctions is due to expire on the 12 May. Meanwhile, the Venezuelan economy cont inues to be beset by turmoil.

We see a tail risk of sanct ions hitt ing Iranian oil supply or a Venezuelan meltdown, which could send Brent to USD80-85 per barrel. we conduct a sensitivity analysis of the implications of such an oil price spike in the currency domain. Depending on the currency pair, we find both upside and downside risk.