Sample Category Title

Which Currencies are More Sensitive to Oil Price Shock?

- The waiver on US nuclear-related sanctions on Iran expires on 12 May - we see a tail risk of Iran's oil exports being hit by sanctions and Brent rising to USD80-85/bl.

- This creates upside risks for EUR/TRY, EUR/JPY and EUR/CHF and downside risks for EUR/CAD, EUR/NOK and EUR/RUB.

Oil event risk on the increase - focus turns to Iran

Oil prices rallying to the highest level since 2014 is due partly to rising event risk in the oil market (Chart 1). We highlight the tense geopolitical situation in the Middle East and the deteriorating economic situation in Venezuela as two hotspots for a sudden oil supply disruption, which could send the oil price higher and affect FX markets. Focus is now on Iran, as the waiver on US sanctions related to the 2015 nuclear deal expires on 12 May. US President Donald Trump has argued against a continuation of the current nuclear deal and we see a tail risk where sanctions related to Iran's oil exports are reinstated (Chart 2) and the price of Brent jumps to USD80-85/bl. If the deal continuesd, oil prices could fall to around USD72-73/bl from the current level.

In terms of the FX impact, shown in Table 1 below, we map the sensitivity to oil price changes of different major and emerging market currencies vis-à-vis the EUR. We measure on (1) relative net exports to eurozone net exports, (2) the current beta on changes in the oil price and (3) how the currency pair was affected when oil prices fell close to 10% following the 2015 Iran nuclear deal (Chart 3). Based on a cross-check of Table 1, there is upside risk to EUR/TRY, EUR/JPY, EUR/CHF and EUR/INR from the extreme case scenario outlined above and downside risk to EUR/CAD, EUR/NOK and EUR/RUB. Notably, EUR/USD maintains a minuscule sensitivity to oil, which means that an oil spike should not be able to derail the current negative momentum in the cross.

Pound Edges Higher in Thin Holiday Trade

The British pound has posted slight gains on Monday, erasing the losses seen on Friday. In North American trade, GBP/USD is trading at 1.3571, up 0.29% on the day. British banks are closed for May Day, and there are no British releases. It’s a quiet day in the US, with no major events. On Tuesday, the US releases PPI and JOLTS Job Openings. We’ll also hear from Federal Reserve Chair Jerome Powell, who will speak at an event in Zurich.

It has been a rough run for the British pound, which posted a third consecutive losing week. The pound has slid 4.9% since mid-April, and GBP/USD dropped below the 1.35 line on Friday for the first time since early January. In addition to a broadly stronger US dollar, recent weak British numbers have soured sentiment towards the pound. Preliminary GDP for the first quarter missed the forecast with a negligible gain of 0.1%, and Manufacturing and Services PMIs also fell short of their estimates. The soft data has also drastically lowered expectations that the Bank of England will raise interest rates on Thursday. Most analysts expect the BoE to delay a hike until the second half of the year, with August or November being the most likely months for a rate hike.

In the US, job numbers were a mixed bag on Friday. Nonfarm payrolls rebounded with a gain of 164 thousand, although this fell short of the estimate of 190 thousand. Wage growth dropped from 0.3% to 0.1%, missing the estimate of 0.2 percent. There was some good news from the unemployment rate, which dropped to 3.9%, beating the estimate of 4.1%. The Fed will likely be pleased that nonfarm payrolls were not red hot, as they April report justifies its policy of gradual rate hikes.

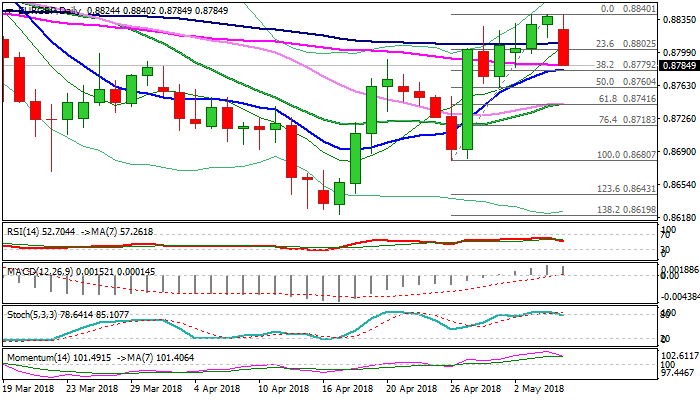

EURGBP – On Track to Complete Reversal Pattern

The cross accelerated lower on Monday and penetrated daily cloud (0.8817/0.8775), on trach to complete reversal pattern on daily chart after Friday’s action ended in Hanging Man.

Fresh weakness eyes key support zone between 0.8785 and 0.8775 (consisting of converged 55/10SMA’s; Fibo 38.2% of 0.8680/0.8840 and daily cloud base).

Firm break here is needed to confirm reversal and open way for further retracement of two-legged recovery from 0.8620 (17 Apr low).

Daily slow stochastic emerged from overbought zone, while RSI and momentum turned south, supporting the notion.

Broken 100SMA marks initial resistance (0.8808) which is expected to limit the upside and keep upper pivots at 0.8840 (04 May high) and 0.8876 (200SMA) intact.

Res: 0.8808; 0.8840; 0.8876; 0.8900

Sup: 0.8775; 0.8756; 0.8742; 0.8718

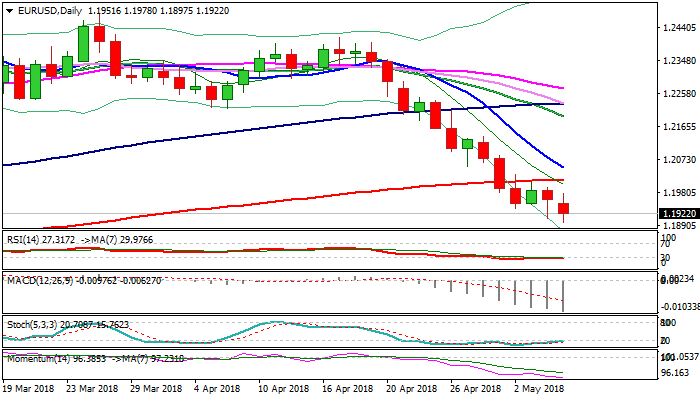

EURUSD Cracks 1.19 Support in Fresh Extension Lower, Helped by Downbeat German/EU Data

The Euro dented round-figure support at 1.19 in extension of fresh weakness which commenced in late Asian session and accelerated after downbeat German/EU data.

German factory orders fell 0.9% in Mar vs forecasted rise of 0.5%, while Eurozone’s investor confidence fell below expectations in May (19.2 vs 21.2 f/c). The pair maintains firm bearish tone which strengthened further after narrow consolidation in past couple of sessions kept key barrier provided by 200SMA (1.2016) intact.

Falling 10SMA is approaching 200SMA in attempt to form death-cross and generate fresh bearish signal, while negative outlook is also reinforced by firmly bearish momentum studies.

The pair is on track for daily close below 1.1936 (Fibo 61.8% of 1.1553/1.2555 ascend) which would offer another bearish signal.

Continuation of downtrend from 1.2413 (17 Apr high) could extend to 1.1790 (Fibo 76.4%), with weekly cloud top (1.1681) expected to come in focus on stronger bearish acceleration.

Meanwhile, bears could be interrupted as daily studies are oversold and bullish divergence is forming on slow stochastic.

Bearish outlook is expected to remain intact while corrective upticks stay capped under 200SMA.

Res: 1.1940; 1.1978; 1.2016; 1.2052

Sup: 1.1897; 1.1846; 1.1816; 1.1790

Japanese Yen Trading Sideway, Shrugs Off Upbeat Minutes

The Japanese yen is showing little movement in the Monday session. In North American trade, USD/JPY is trading at 109.27, up 0.10% on the day. On the release front, the Bank of Japan released its minutes from the April policy meeting. Later in the day, Japan releases Household Spending, which is expected to rebound with a strong gain of 1.2%. There are no major US releases on the schedule. On Tuesday, the US releases PPI and JOLTS Job Openings. We’ll also hear from Federal Reserve Chair Jerome Powell, who will speak at an event in Zurich.

The Bank of Japan minutes from the March meeting were upbeat. The minutes said that the economy, as well as inflation, are likely to continue on an upward trend. The bank has long sought to reach an inflation target of around 2 percent, and if policymakers are correct and this goal is on its way to being achieved, the BoJ will be able to contemplate a reduction in its stimulus program, a move which could have a substantial impact on the yen. However, the cautious BoJ is likely to stick to current policy well into 2019, even if economic conditions improve and inflation moves closer to target.

In the US, job numbers were a mixed bag on Friday. Nonfarm payrolls rebounded with a gain of 164 thousand, although this fell short of the estimate of 190 thousand. Wage growth dropped from 0.3% to 0.1%, missing the estimate of 0.2 percent. There was some good news from the unemployment rate, which dropped to 3.9%, beating the estimate of 4.1%. The Fed will likely be pleased that nonfarm payrolls were not red hot, as they April report justifies its policy of gradual rate hikes.

Sunsent Market Commentary

Markets

Trading in core US and European bonds took a slow start for the new trading week. Volumes were light with UK markets closed. There were also no really important data. The US yields were little changed (unchanged for 2y; -0.5 bp for 10 & 30y yield). German bond yields currently decline up to 1 bp (5-year). 10y intra-EMU-spread changes versus Germany range between unchanged and +2bp. For now, there is no meaningful underperformance of Italian bonds, despite press headlines on the possibility of new elections in July if current attempts to form a new government would fail.

There was also no really dominant story to guide USD trading, but the swings in the dollar were a bit more pronounced than in yield markets. End last week some ‘by default USD buying’ prevailed even as the US payrolls painted a mixed picture. This cautiously USD positive momentum continued today. USD/JPY tried to sustain well north of the 109 handle. EUR/USD filled bids at around the 1.19 big figure. So, it looks that the 1.1915/35 support area might be breached. For now, the further rise of the oil price had hardly any negative impact on the dollar. Dollar strength prevailed, but the news flow was also tentatively euro negative. German March factory orders disappointed again (-0.9% M/M vs 0.5% expected). Euro selling also accelerated slightly on headlines that the political deadlock in Italy might lead to new elections, maybe as early as July. EUR/USD currently trades in the low 1.19 area. USD/JPY hovers in the 109.30 area. We look out how long higher oil prices and a strong dollar will go hand in hand. From a data point of view, the US price data on Wednesday (PPI) and on Thursday (CPI) are probably the next important reference for US yields and for the dollar.

Sterling was better bid compared to last week. Cable didn’t go anywhere, hovering in the mid 1.35 area. This was a reasonably good performance given overall dollar strength. EUR/GBP dropped back to the 0.88 area, pressured by overall euro softness. For now, it remains unclear whether UK PM May will be able to reach a compromise within her Conservative Party on the future relationship with the EU post Brexit. However, for now, this causes no additional sterling losses anymore. Sterling investors are also looking forward to Thursday’s BoE meeting. A rate hike is now almost completely price out. Maybe some investors are turning a bit less negative on sterling as the BoE might keep the door open for a rate hike later this year.

News Headlines

German industrial orders (-0.9% M/M, 3.1% Y/Y) unexpectedly dropped for the third month running in March due to weak foreign demand, data showed, suggesting that factories in Europe's largest economy are facing headwinds from rising protectionism. (Reuters)

Italy’s two biggest political forces rejected the idea of a government of technocrats in talks with President Mattarella, increasing the chances of new elections as early as July to overcome a two-month deadlock. (BB)

China's foreign exchange reserves in April fell more than expected, to a five-month low, as the US dollar rebounded and on growing signs that Chinese regulators are less worried about capital flight. Reserves fell $17.97 bn in April to $3.125 tn - the lowest since November 2017, compared with a rise of $8.34 bn in March. (Reuters).

BoC Lane: Still a significant degree of uncertainty around the trade situation

Bank of Canada (BoC) Deputy Governor Timothy Lane said earlier today there are still a significant degree of uncertainty around the trade situation. While news on steel has changed a lot in the last few days, it's still a fluid situation, not a situation of calling all clear. And even though BoC doesn't need to stay on hold until there is more clarity, the lack of clarity has dampening effect on outlook.

Lane also noted that during rate decision discussion, trade uncertainty is definitely a risk to outlook, but that's just one of a number of factors. And for BoC, one of the reasons to be on hold is that policymakers are very cautious to make sure there is adequate taking stock of what rates are doing to households.

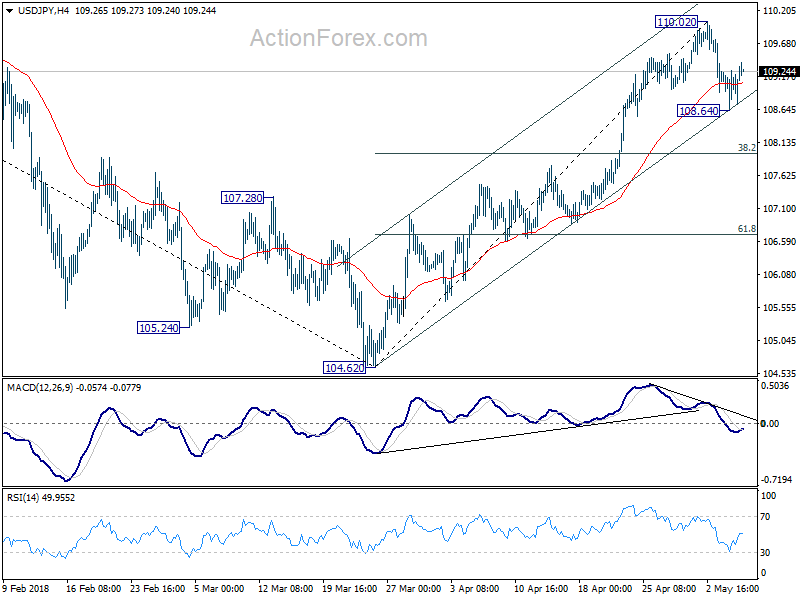

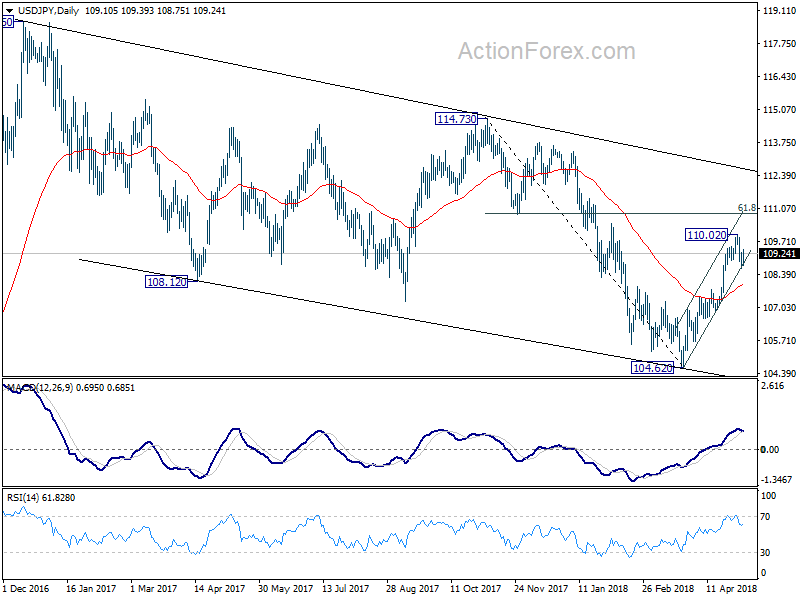

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.69; (P) 108.98; (R1) 109.32; More...

USD/JPY is staying in consolidation below 110.02 short term top and intraday bias remains neutral Another fall cannot be ruled out. Below 108.64 will bring deeper pull back to 38.2% retracement of 104.62 to 110.02 at 107.95. In that case, we'd expect strong support fro 107.95 to contain downside and bring rebound. On the upside, break of 110.02 will resume the rise from 104.62 to t 61.8% retracement of 114.73 to 104.62 at 110.86 next.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 55 day EMA (now at 107.95) holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above. However, sustained break of 55 day EMA will dampen this bullish view and turn focus back to 104.62 low instead.

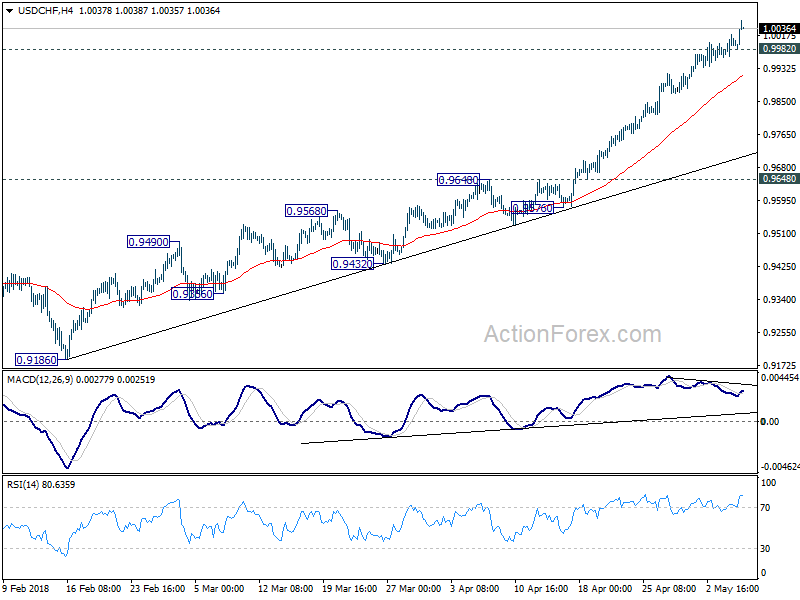

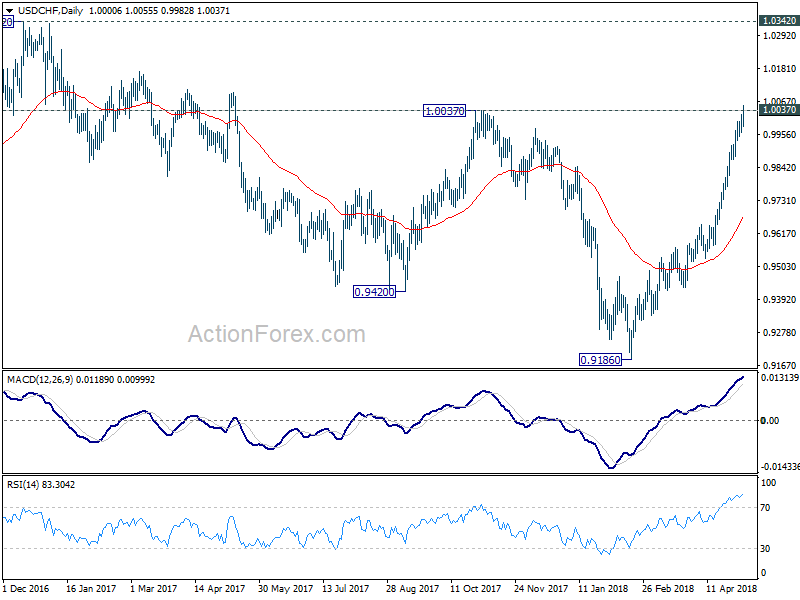

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9965; (P) 0.9994; (R1) 1.0025; More...

USD/CHF's rally continues today and reaches as high as 1.0055 so far. Intraday bias stays on the upside. Sustained trading above 1.0037 will pave the way to 1.0342 key resistance next. On the downside, though, below 0.9982 minor support will indicate short term topping. And, in that case, deeper retreat could be seen to 4 hour 55 EMA (now at 0.9918) and below before staging another rise.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 0.9648 resistance turned support holds, even in case of pull back.

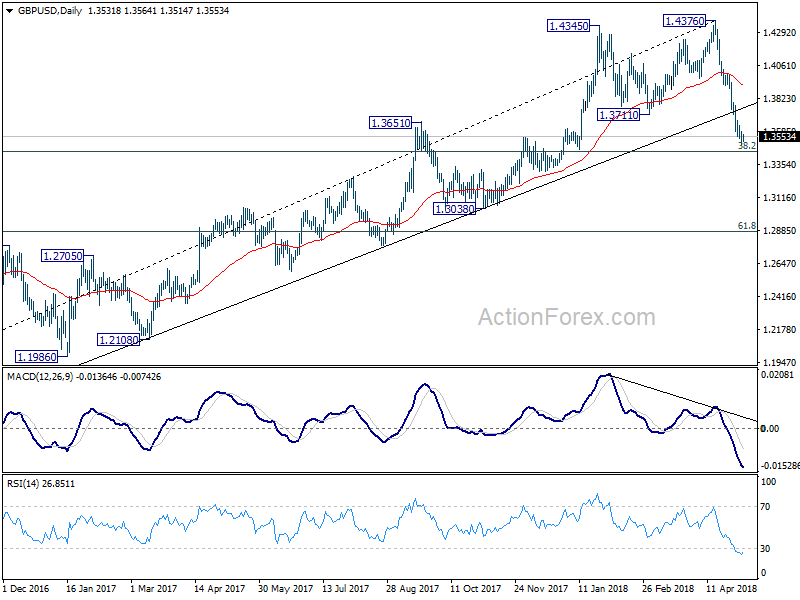

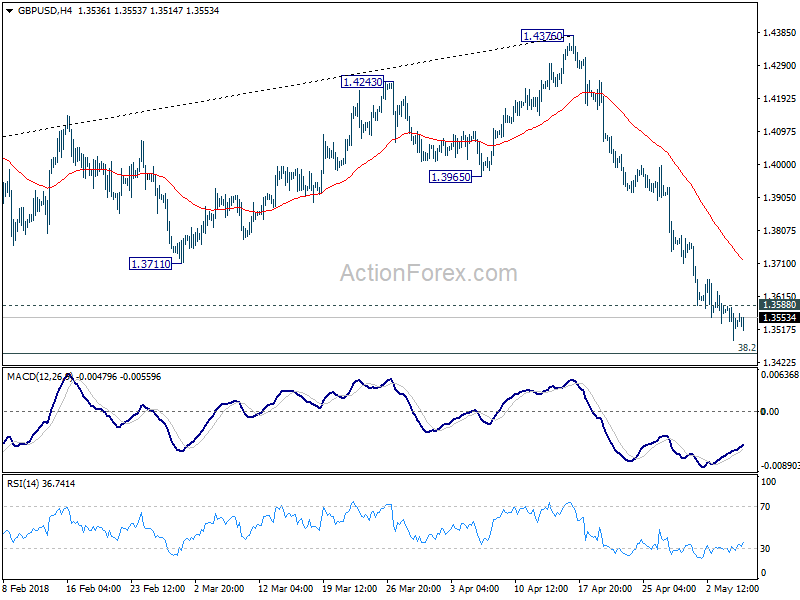

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3478; (P) 1.3532; (R1) 1.3578; More...

No change in GBP/USD's outlook. Intraday bias remains on the downside for 1.3448 fibonacci level next. On the upside, above 1.3588 minor resistance will argue that a short term bottom is formed. In that case, stronger recovery could be seen back to 4 hour 55 EMA (now at 1.3719) and above before staging another fall.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). Deeper decline should be seen to 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 first. Break will target 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3925) holds, even in case of strong rebound.