Sample Category Title

USD/CAD Rectangle Consolidation in Intraday Timeframe

The USD/CAD has been consolidating within the rectangle between W H4 and W L3 levels. Traders need to pay attention to all weekly levels pivot points that are contained in the box. 1.2908 1.2878 and 1.2815. Daily pivot levels are also significant so we need to look at the confluence. We might expect short sellers to sell within 1.2908-20 zone and fresh buyers within the 1.2800-15. Until the consolidation is broken on the USD/CAD, we should see a range play.

- W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

- W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

- W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

- D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

- D L3 – Daily Camarilla Pivot (Daily Support)

- D L4 – Daily H4 Camarilla (Very Strong Daily Support)

- POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

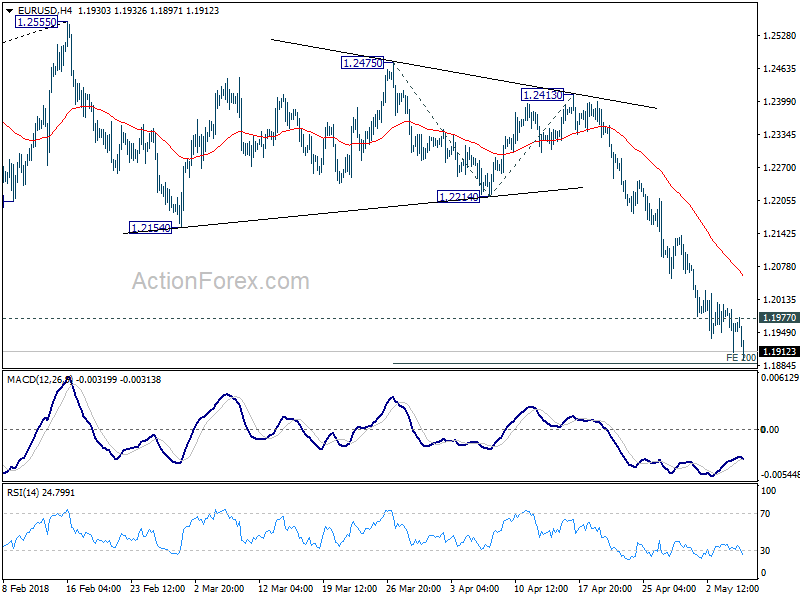

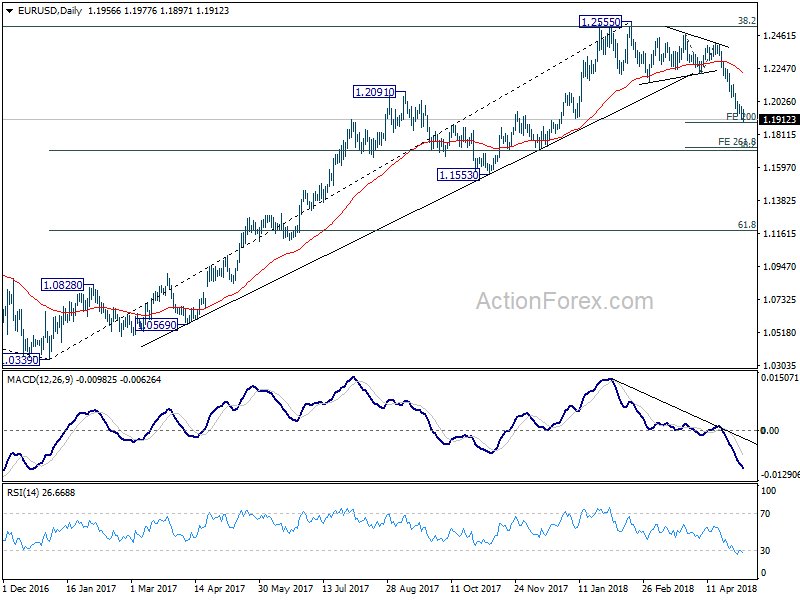

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1914; (P) 1.1955 (R1) 1.1999; More....

EUR/USD reaches as low as 1.1897 so far as recent decline continues. Intraday bias remains on the downside for 200% projection of 1.2475 to 1.2214 from 1.2413 at 1.1891. Firm break will target 261.8% projection at 1.1730. Meanwhile, considering diminishing downside momentum as seen in 4 hour MACD, break of 1.1977 minor resistance will indicate short term bottoming. In that case, intraday bias will be turned to the upside for 4 hour 55 EMA (now at 1.2064) or above for rebound.

In the bigger picture, current decline and firm break of 1.2154 support confirms rejection by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. A medium term top should be in place at 1.2555 and deeper decline would be seen back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. With current downside acceleration, there is prospect of hitting 61.8% retracement at 1.1186 before completing the decline. But still, we'll need to look at the structure to before deciding if it's a corrective or impulsive move.

Dollar Extending Rally against Euro and Swiss Franc as Weak Eurozone Data Weigh

Dollar is extending recent rally against Euro and Swiss Franc in early US session. EUR/USD breached 1.19 handle as it's now trying to get rid of 1.2 firmly. USD/CHF reaches as high as 1.0055 and breached 1.0037 resistance. Weak Eurozone data is a factor weighing on the comment currency, as seen in EUR/GBP too. Nonetheless, the greenback is still held in tight range against Sterling, Aussie and Loonie despite rally attempts. USD/JPY also recovers but struggle to extend through 109.39 yet. 1.3485 in GBP/USD, 0.7472 in AUD/USD and 1.2913 in USD/CAD are the levels to watch to confirm underlying momentum.

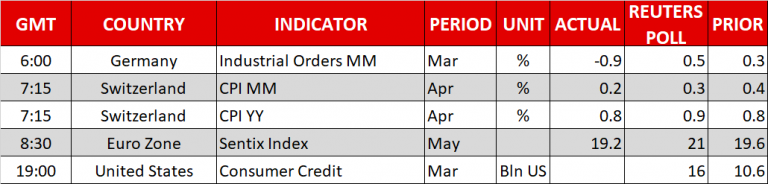

Eurozone Sentix investor confidence dropped to 19.2, lowest since Feb 2017

Eurozone Sentix investor confidence dropped to 19.2 in May, down from 19.6, missed expectation of 21.0. That's the 4th decline in a row, and hit the lowest level since February 2017. Current situation index dropped 0.2 to 42.8, lowest since October 2017. Expectations dropped to -2, lowest since October 2014. Sentix noted that "uncertainties about the introduction of punitive US tariffs and the danger that this could lead to an expansion of protectionist measures are weighing on us."

Eurozone retail PMI at 48.6, Italy sales decline accelerated sharply

Eurozone retail PMI dropped to 48.6 in April, down from 50.1. Weakness was driven by sharp decline in Italy which hit 21 month-low at 42.7. Germany retail PMI dropped to 9-month low at 51.0. France continued to outperform with retail PMI hit 2 month high at 50.1. Markit noted that "the latest data highlighted a disappointing month for the eurozone retail sector. Monthly sales were down for the first time for over a year as signs of restricted consumer demand and increased uncertainty begin to show. This was particularly evident in Italy, where the rate of decline in like-for-like sales accelerated sharply and was the most marked for the better part of two years.

And, "forward-looking indicators add to the dull picture, with falls in purchasing activity and stocks of goods suggesting retailers are taking an increasingly cautious approach to their business operations. The one shining light was a further rise in staffing numbers. That said, without a rebound in customer demand we may see employment slip back into contraction territory in the coming months as well."

Also release in European session, Swiss CPI rose 0.2% mom, 0.8% yoy. Foreign currency reserves rose to CHF 757B

ECB research: Significant increase in protectionism could have material impact on global trade and output

In article titled "Implications of rising trade tensions for the global economy", ECB researcher Lucia Quaglietti warned of the impact of escalation of trade tensions. Based on simulations carried out by ECB staff, in event of a significant increase in protectionism, "the impact on global trade and output could be material." In particular, if US increases tariffs "markedly" on imported goods from all trading partners that "retaliate symmetrically", the outcome for the world economy would be "clearly negative. And, "the impact could be particularly severe in the United States"

For other countries, those with "closest trade relations" with the US would be most negatively affected. And, "only a few open economies with little exposure to the tariff-imposing country may benefit from trade diversion effects, as they would gain competitiveness in third markets."

In addition, the impact of trade tension escalation could be "felt via a number of channels. Higher import prices would lead to higher production costs and lower household purchasing power. Consumption, investment and employment will also be affected. Moreover, there will be economic uncertainty that leads to delay and consumer spending and business investment. Credit supply could be reduced with requirement for higher compensation. And there could be broad spill over to the global financial markets.

China FX reserves dropped to five month low in USD term

According to the latest data from People's Bank of China, the country's foreign exchange reserves dropped to a five month low in April. Reserves dropped USD 17.97B in April from USD 3.143T to USD 3.125T. In SDR terms, Foreign currency reserves rose 11.3 B from 2.162T to 2.173T. Gold reserves was unchanged at 59.24 Million oz. Total reserves dropped from USD 3.240T to USD 3.221T. In SDR terms, total reserves rose from 2.229T to 2.240T.

BoJ March meeting minutes: Not the time to consider stimulus exit yet

In the minutes of March BOJ meeting, some members emphasized the need to have the best communications to the markets. To be more specific, "it was important for the BOJ to thoroughly explain to the public ... that the economy had not yet reached a phase where it should consider the timing and measures of a so-called exit from monetary easing," Also "while normalization, or a gradual reduction in the degree of monetary accommodation, could become a topic for consideration in the future, the BOJ needs to explain to markets that normalization ... would be different from monetary tightening,"

Australia NAB business condition hit record high, but RBA could delay rate hike to 2019

Australia NAB business condition rebounded notably from 15 to 21 in April. That's also a rerecord high since the survey started in March 1997. Business confidence also rebounded from 8 to 10. Alan Oster, NAB Group Chief Economist noted in the release that the results reinforces the evidence of "robust" business activity. Except manufacturing and retail, conditions increased in all industries. And, strength in both business conditions and confidence suggest that "economic growth will strengthen and that over-time".

Meanwhile, falling unemployment rate should "eventually translate into upwards pressure on private sector wages". That would put RBA into a position to "start increasing the current emergency low policy rate:. NAB maintained the forecast for RBA to hike later this year. However, "as hard evidence of a firming in wages growth is yet to appear in the data, and unemployment for the moment stuck at around 5.5%, the risk is that any action by the RBA will be delayed into 2019".

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1914; (P) 1.1955 (R1) 1.1999; More....

EUR/USD reaches as low as 1.1897 so far as recent decline continues. Intraday bias remains on the downside for 200% projection of 1.2475 to 1.2214 from 1.2413 at 1.1891. Firm break will target 261.8% projection at 1.1730. Meanwhile, considering diminishing downside momentum as seen in 4 hour MACD, break of 1.1977 minor resistance will indicate short term bottoming. In that case, intraday bias will be turned to the upside for 4 hour 55 EMA (now at 1.2064) or above for rebound.

In the bigger picture, current decline and firm break of 1.2154 support confirms rejection by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. A medium term top should be in place at 1.2555 and deeper decline would be seen back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. With current downside acceleration, there is prospect of hitting 61.8% retracement at 1.1186 before completing the decline. But still, we'll need to look at the structure to before deciding if it's a corrective or impulsive move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Minutes | ||||

| 1:30 | AUD | NAB Business Conditions Apr | 21 | 14 | 15 | |

| 1:30 | AUD | NAB Business Confidence Apr | 10 | 7 | 8 | |

| 6:00 | EUR | German Factory Orders M/M Mar | -0.90% | 0.50% | 0.30% | |

| 7:00 | CHF | Foreign Currency Reserves (CHF) Apr | 757B | 738B | ||

| 7:15 | CHF | CPI M/M Apr | 0.20% | 0.30% | 0.40% | |

| 7:15 | CHF | CPI Y/Y Apr | 0.80% | 0.90% | 0.80% | |

| 8:10 | EUR | Eurozone Retail PMI Apr | 48.6 | 50.1 | ||

| 8:30 | EUR | Eurozone Sentix Investor Confidence May | 19.2 | 21 | 19.6 |

Canadian Dollar Dips as Investors Search for Cues

The Canadian dollar has posted slight gains in the Monday session, after trading sideways on Friday. USD/CAD is trading at 1.2878, up 0.24% on the day. It’s a light day on the release front, with no major releases in the US or Canada. On Tuesday, Canada releases Housing Starts and the US publishes PPI and JOLTS Job Openings. We’ll also hear from Federal Reserve Chair Jerome Powell, who will speak at an event in Zurich.

Canadian indicators ended the week on a high note. Ivey PMI jumped to 71.5 points in April, crushing the estimate of 60.2 points. This economic index covers all sections of the Canadian economy, but the positive release failed to boost the Canadian dollar, as USD/CAD was unchanged on Friday. In the US, job numbers were a mixed bag. Nonfarm payrolls rebounded with a gain of 164 thousand, although this fell short of the estimate of 190 thousand. Wage growth dropped from 0.3% to 0.1%, missing the estimate of 0.2 percent. There was some good news from the unemployment rate, which dropped to 3.9%, beating the estimate of 4.1%. The Fed will likely be pleased that nonfarm payrolls were not red hot, as they April report justifies its policy of gradual rate hikes.

The Canadian economy is in good shape and the markets can expect additional rate hikes this year. That was the hawkish message from Bank of Canada Governor Stephen Poloz at an event last week in Yellowknife. Poloz singled out household debt as a significant concern, but said that “since the economy is close to where it belongs, interest rates are headed higher”. The markets are confident that the BoC will press the rate trigger in July, with the odds of a hike currently at 73 percent. Other economic issues that Poloz said are weighing on the Canadian economy include uncertainty over US trade policy and the ongoing NAFTA negotiations. If there is progress to report on the US-China tariff spat or on NAFTA, the Canadian dollar should respond with gains.

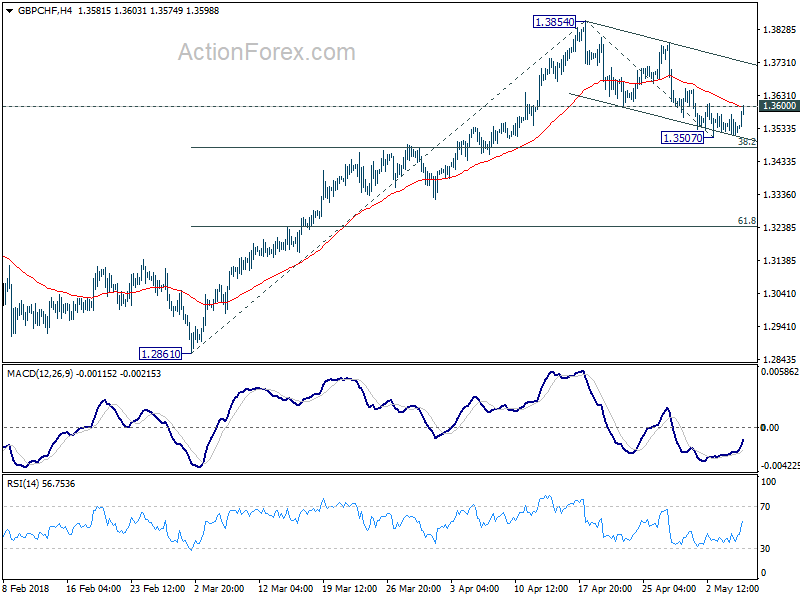

A look at GBP/CHF long opportunity

Heading into US session, GBP and USD are trading as the strongest one for today. CHF franc is the weakest, followed by AUD and then EUR. USD's strength is a bit more convincing as USD/CHF has already took out last week's high as well as key resistance level at 1.0037. EUR/USD has also just breached last week's low. GBP/USD is kept below 1.3588 minor resistance, maintaining near term bearishness.

GBP's strength today is generally seen as corrective in near nature. Except that, EUR/GBP's near term outlook is not overwhelmingly bullish. And, indeed, GBP/CHF is an interest cross to look at. The W row of GBP/CHF action bias showed that it was in a brief up trend. Totally neutral D row (latest 9 bars) indicates that it has been in consolidation. Some 6H red bars indicates that consolidation was in form a a pull back whether sideway trading. But as the 6H bars have turned neutral, downside momentum in the pull back has diminished. And, there are indeed a string of blue H bars, arguing that the correction could be finished and GBP/CHF is ready for rise resumption.

The above could also be seen clearly, in the D, 6H and H Action Bias charts.

Now back to the regular GBP/CHF bar chart. The break of 1.3600 supported turned resistance is the first sign of completion of pull back from 1.3854 at 1.3507. The structure of the fall supports that it's a correction. And it's also held above 38.2% retracement of 1.2861 to 1.3854 at 1.3475, which indicates healthy near term bullishness. Intraday bias is now on the upside for channel resistance (now at 1.3732). Firm break there should confirm this bullish view and send GBP/CHF through 1.3854 high to 61.8% projection from 1.2861 to 1.3854 from 1.3507 at 1.4121 as the first target. Though, break of 1.3507 will invalidate this bullish view and extend the fall from 1.3854 instead.

This is the kind of setup that one can just buy at the current level at around 1.3600, with a stop at 1.3500 (below 1.3507 support), targeting 1.4121. Risk/reward ratio is good enough for position trading.

Euro Under Pressure As Economic Confidence Fades

Here are the latest developments in global markets:

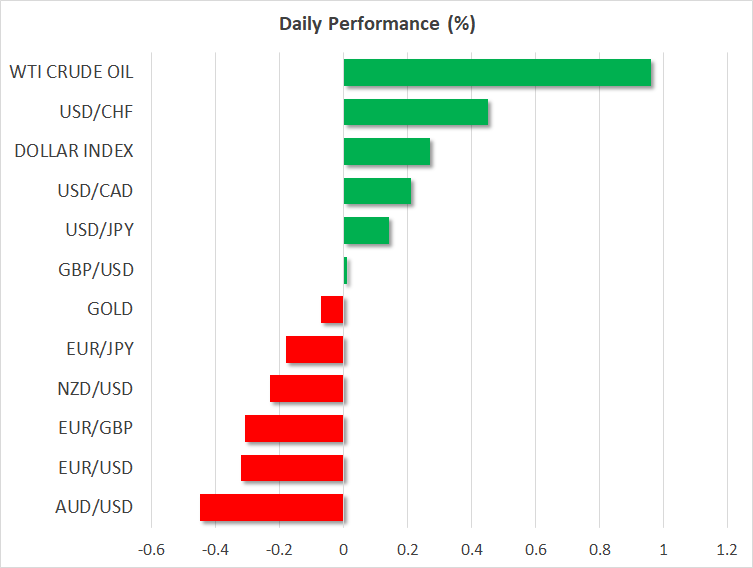

FOREX: The demand for greenback remained strong early in the European session, supported by rising confidence that the Fed, unlike its major counterparts, would keep pace with its stimulus reduction plans despite Friday’s nonfarm payrolls report showing wages growing less than expected. However, risks of a global trade war continued to hang in the background as trade talks between the US and Chinese negotiating teams last week failed to strike a deal. The dollar index rallied to an intra-day high of 92.82 (+0.26%) and dollar/yen reached a peak at 109.32 before it edged down to 109.25 (+0.13%). Euro/dollar extended today’s downfall to 1.1924 (-0.27%) as economic data out of the Eurozone continued to disappoint, with the Eurozone’s Sentix investor confidence index for May falling surprisingly to the lowest since February 2017 on Monday. German factory orders for March also missed forecasts of a growth of 0.5% today, dropping by 0.9% instead, while an ECB researcher warned through an Economic Bulletin article that “In the event of a significant increase in protectionism, the impact on global trade and output could be material.” Pound/dollar erased earlier gains, falling to 1.3534 (+0.02%), while euro/pound was struggling to rebound from 4-day lows, last seen at 0.8800 (-0.33%). In antipodean currencies, aussie/dollar and kiwi/dollar were under pressure in the face of a strengthening dollar, trading lower at 0.7508 (-0.42%) and 0.7000 respectively (-0.21%). Dollar/Lonnie rose to 1.2868 (+0.22%) ahead of the resumption of NAFTA talks today in Washington.

STOCKS: European stocks were mostly positive at 0930 GMT, with the pan-European STOXX 600 and the blue-chip Euro STOXX 50 being 0.15% and 0.01% up. Air France- KLM Group, Europe’s largest air carrier, was the worst performer among companies, with its stocks tumbling by 11.45% after its CEO resigned on Friday following a pay rejection by the staff which spurred strikes in the streets. The French CAC 40 inched up by 0.03%, with gains in the technology sector offsetting losses in telecommunications and financials, the German DAX 30 climbed by 0.36%, while the Italian FTSE MIB rose by 0.31%. UK stock markets were closed for a holiday.

COMMODITIES: Supply concerns lifted oil prices to fresh 3-year highs as hyper-inflated Venezuela headed into default. Analysts were also anticipating the US to pull out of the 2015 Iran nuclear deal on May 12 and reimpose sanctions on Iran as tensions between the two countries were still running high. WTI crude touched a new peak at $70.69/barrel before it fell to $70.41(+1.0%) and Brent hit a new top at $75.89 before it slipped to $75.55 (+0.91%). In precious metals, gold took off one-week highs, retreating to $1,313.90/ounce (-0.08%).

Day Ahead: Quiet day in terms of data; numerous speeches on the agenda

Monday is going to be quiet in terms of economic releases, while market liquidity is expected to be relatively narrower as UK markets are closed for a Bank Holiday today.

The US, the world’s largest economy, will see the release of March consumer credit data at 1900 GMT. Credit is predicted to tick higher by $16.0 billion from $10.6 billion the preceding month.

In terms of public speeches, Atlanta’s Fed President, Raphael Bostic (voting FOMC member in 2018), will be speaking at 1225 GMT, while at 1800 GMT, Richmond’s Fed President, Tom Barkin (voter) and Philadelphia’s Fed chief Patrick Harker (non-voter) will be making comments as well. A bit later, at 1930 GMT, the focus will turn to speeches made by the Dallas Fed President, Robert Kaplan, and the Chicago Fed President Charles Evans (both non-voters).

Early tomorrow, Australia will see the release of retail sales numbers at 0030 GMT; aussie pairs would be eyed. Month-on-month, sales are expected to expand by 0.3% in March versus 0.6% the prior month.

In equities, Walt Disney and Nvidia are two of the companies releasing results this week, on Tuesday and Thursday respectively. Equity market sentiment could be also driven by developments in global trade, as NAFTA talks are resuming today in Washington and US-China discussions seem to have provided no tangible outcome last week.

May 12th Iran Deadline Carries Risks Beyond Price Of Oil

Persistent fears that President Trump will pull out of the Iran nuclear deal later this week have played a pivotal role behind the price of US Oil rising above $70 for the first time since November 2014during early morning trading. Recent price action suggests that investors have not yet concluded pricing in further risk premium as we edge closer to the May 12th deadline Trump has set himself to decide whether the US will remain in the 2015 Iran nuclear deal, and any comments Trump makes in the lead up to the event have the potential to encourage fireworks in the oil markets.

With Trump having referred to the Iran agreement in the past as “the worst deal ever” it is not difficult to understand why investors seem to be expecting the worst on May 12th. The only problem with pricing in the current worst-case scenario is that investors are going to be at risk of being on the complete wrong side of the trade, if any headlines come out in the meantime that Trump could delay his decision on whether to pull out of the Iran deal.

It does also need to be remembered that despite much of the risk premium heading into May 12thbeing focused on how the price of oil might react,there is going to be a threat of wider implications than oil supplies, if Trump does abandon the 2015 nuclear deal. Iranian President Hassan Rouhani has already warned that the US would regret its decision to exit the nuclear deal, and concerns over how Iran might react to the United States pulling out do not appear to have been factored into other asset classes.

One of the most difficult questions to answer is what impact the United States pulling out of the deal might meanfor politics in the Middle East.There have been underlying concerns for some time that Iran is having a growing influence on the region. We are not just talking about a return to strained relations between the US and Iran if Trump pulls out of the deal, but we also need to look at the risk of what impact this could have on regional markets within the Middle East

Uncertainty could also play a role in investor sentiment for wider risk appetite, meaning a period of uncertainty could expose emerging market assets and currencies to downside risks in an environment where investors are already maintaining a cautious stance ahead of geopolitical tensions elsewhere. We are in a trading period where emerging market currencies are already in the midst of sudden weakness, due to the unexpected turnaround in the fortunes of the US Dollar and there is a risk of buying momentum for emerging market currencies taking additional punishment if tensions around Iran surge.

There is a threat that the uncertainty will play a role in how global stocks perform overthe coming days, while it should also not be understated that higher-yielding currencies like the South African Rand, Russian Ruble and Turkish Lira, to name just a few, are highly reliant on investors being attracted towards taking on risk.

I am concerned heading that all of the market focus heading into May 12thseems to have been dictated on how the price of oil might react, without looking at the connotations that the United States pulling out might have on other asset classes.

ECB research: Significant increase in protectionism could have material impact on global trade and output

In article titled "Implications of rising trade tensions for the global economy", ECB researcher Lucia Quaglietti warned of the impact of escalation of trade tensions.

Based on simulations carried out by ECB staff, in event of a significant increase in protectionism, "the impact on global trade and output could be material." In particular, if US increases tariffs "markedly" on imported goods from all trading partners that "retaliate symmetrically", the outcome for the world economy would be "clearly negative. And, "the impact could be particularly severe in the United States"

For other countries, those with "closest trade relations" with the US would be most negatively affected. And, "only a few open economies with little exposure to the tariff-imposing country may benefit from trade diversion effects, as they would gain competitiveness in third markets."

In addition, the impact of trade tension escalation could be "felt via a number of channels. Higher import prices would lead to higher production costs and lower household purchasing power. Consumption, investment and employment will also be affected. Moreover, there will be economic uncertainty that leads to delay and consumer spending and business investment. Credit supply could be reduced with requirement for higher compensation. And there could be broad spill over to the global financial markets.

EUR/USD Breakout Expected

Downside risk continues to prevail in the market as of Friday's session. The bearish movement for the EUR/USD currency pair was temporary stopped after the pair reached the lower boundary of a dominant channel.

The exchange rate has been guided lower by the 55– hour simple moving average since April 19. The first part of Monday's trading session was relatively calm as the currency pair was trading with low volatility.

Everything being equal, a breakout through the upper boundary could be expected during the next 24hrs

GBP/USD Restricted By SMA

Following unsuccessful attempt to breach the 55– hour simple moving average and the weekly pivot point at 1.35 on Friday, the bearish momentum started to lead the Pound Sterling down. As a result, the GBP/USD exchange rate reaches a five-month low level.

Given that the 55– hour SMA has been providing a strong resistance for the currency pair during the last two consecutive trading session, it seems that an upside move might hardly come by today.

Meanwhile, technical indicators suggests that bears are likely to grow stronger within this session.