Sample Category Title

USD/JPY Bounces Off Lower Boundary

The US Dollar has been trading in a narrow channel down against the Japanese Yen since May 2. This channel is being considered as a temporary retracement from the upper border of a dominant pattern.

After reaching the lower boundary of the dominant ascending channel, the currency pair began to appreciate. As a result, the pair has breached the 50.00% Fibonacci retracement level.

The USD/JPY currency exchange rate is likely to continue moving north until it encounters a resistance level set by either the 200– hour SMA or the 100– hour simple moving average.

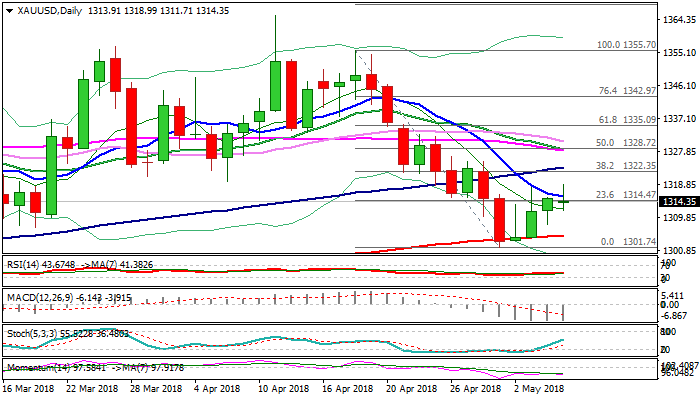

XAU/USD New Pattern Reveals

The XAU/USD pair has broken the previously drawn descending pattern. However, during the first part of Monday's trading session, a new junior ascending channel has been revealed.

By the end of Friday's session, the price commodity has moved past a strong resistance cluster formed by the combination of the 55– and the 100– hour SMAs near the 1310.9 mark. Furthermore, after piercing the 38.20% Fibonacci retracement level, the pair began to decline.

This decline could be stopped either by the 100– hour SMA or the lower boundary of the newly ascending pattern.

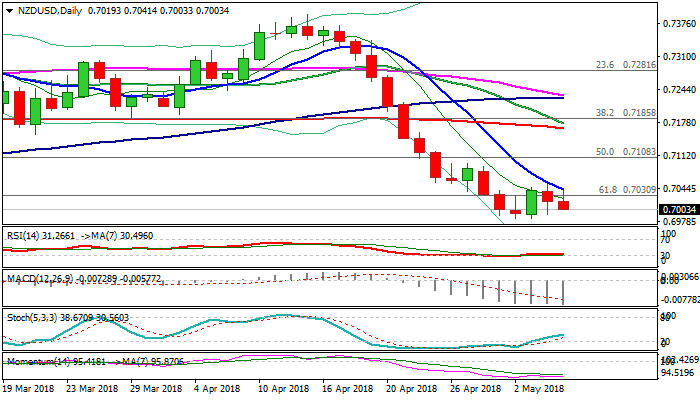

NZDUSD – Rising Downside Pressure After 10SMA Capped Recovery

The Kiwi dollar remains at the back foot on Monday and extends weakness from last Friday’s high at 0.7052, where recovery attempt was capped 10SMA in steep descend.

Brief recovery off 0.6985 base (the lowest in 4 ½ months) where steep bearish acceleration from 0.7394 (13 Apr) found footstep, so far looks like consolidation ahead continuation of larger downtrend.

Fresh weakness on Monday pressures psychological 0.7000 support and looks for attack at 0.6985 base, break of which would generate fresh signal for bearish continuation towards 0.6935/00 (Fibo 76.4% of 0.6780/0.7436 / round-figure support).daily MA’s are in strong bearish setup, however, momentum turned in sideways mode, slow stochastic reversed from oversold territory, while daily RSI is holding around oversold border line, suggesting that consolidation may extend.

Initial bullish signal could be expected on close above 10SMA which would ease downside pressure, but strong overall bears suggest limited recovery.

Res: 0.7042, 0.7052, 0.7081, 0.7140

Sup: 0.6985, 0.6935, 0.6900, 0.6822

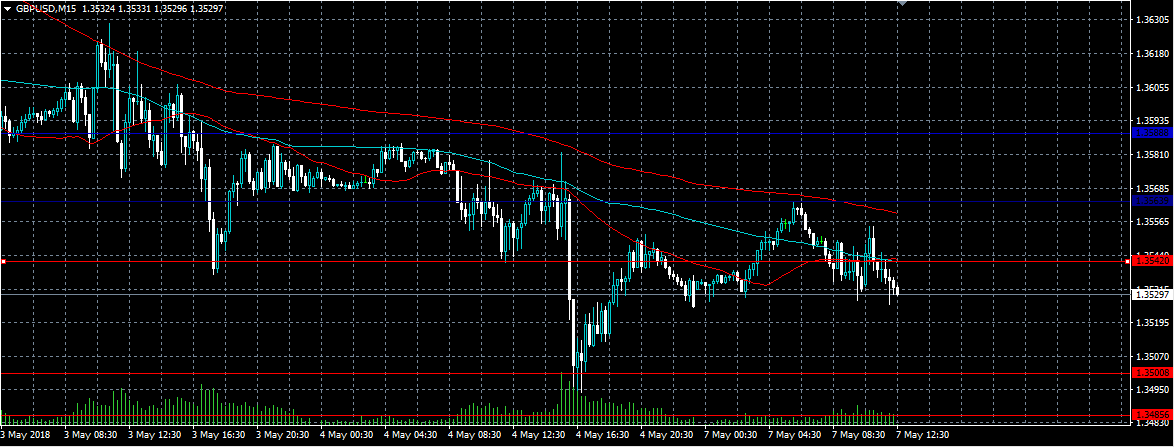

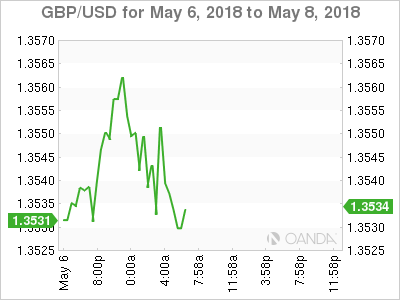

GBPUSD Trading Back Below Key Moving Average

The British pound has started to trade lower against the greenback during the European trading session, as the U.S dollar index continues to move higher. After finding technical resistance from the 1.3563 level this morning, the GBPUSD pair has now fallen back below its key 200-day moving average. Traders are likely to focus on the 1.3500 support level while price trades below the 1.3542 level, which represents the pairs 200-day moving average.

The GBPUSD pair remains strongly bearish while trading below the 1.3542 level, further losses towards 1.3500 and 1.3485 appear likely.

If the GBPUSD pair moves back above the 1.3542 level, buyers may test back towards the 1.3563 and 1.3589 resistance levels.

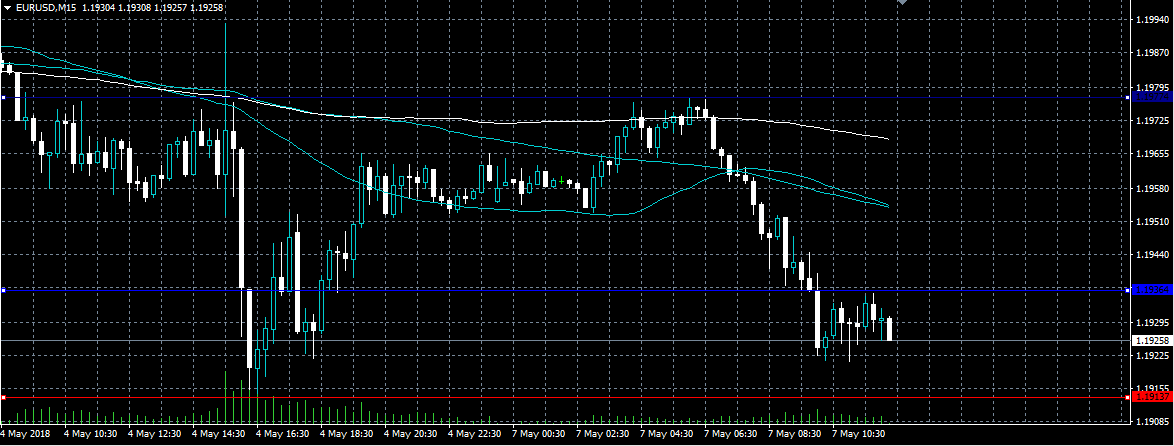

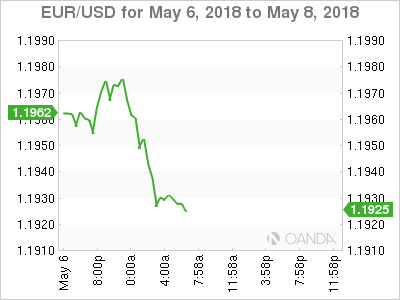

EURO Back Under Pressure After Weak Data

The euro remains under selling pressure against the U.S dollar on Monday, after official data showed German Factory Orders tumbled -0.9 percent during the month of April. The EURUSD pair has been sold aggressively from the 1.1977 level today, with price currently drifting back towards the monthly-low, at 1.1913. Traders now look towards the U.S dollar index and the key 1.1900 level, with EURUSD selling likely to accelerate once the 1.1900 level is broken.

The EURUSD pair remains bearish while trading below the 1.1977 level, key technical support is now found at the 1.1913 and 1.1900 levels.

If the EURUSD pair starts to trade back above the 1.1977 level, buyers may test towards the 1.2000 and 1.2013 resistance levels.

DAX Improves As US Stock Markets End Week On High Note

The DAX index has gained ground in the Monday session. Currently, the DAX is at 12,878 points, up 0.45% on the day. On the release front, eurozone data disappointed. Germany Factory Orders declined 0.9%, missing the estimate of a 0.5% gain. Eurozone Retail PMI dropped to 48.6, marking the first contraction since March 2017. As well, Eurozone Sentix Investor Confidence dipped to 19.2, well short of the forecast of 21.2 points. This marked a fourth straight drop, as investor concern about the health of the eurozone economy is growing.

Is the German locomotive in trouble? On Monday, German Factory Orders posted a second decline in the past three months, pointing to weakness in the manufacturing sector. The markets will be hoping for better news from Industrial Production on Tuesday, with an estimate of 0.8%. The indicator has posted three straight declines. Last week’s PMI reports also disappointed. German Services PMI was the weakest since September 2016, and the eurozone reading also softened compared to March. This points to weaker expansion in services business activity, another indication of weaker eurozone growth in the first quarter of 2018. German numbers are raising concerns about the strength of the eurozone’s largest economy. Manufacturing PMI weakened for a fourth consecutive month in April, and retail sales posted a fourth straight decline.

US employment numbers were mixed on Friday, but US stock markets moved higher, and the positive sentiment has European markets in green territory on Monday. In the US, nonfarm payrolls rebounded with a gain of 164 thousand, although this fell short of the estimate of 190 thousand. Wage growth remained dropped from 0.3% to 0.1%, missing the estimate of 0.2 percent. There was some good news from the unemployment rate, which dropped to 3.9%, beating the estimate of 4.1%. The Fed will likely be pleased that nonfarm payrolls were not red hot, as they April report justifies its policy of gradual rate hikes.

Euro Under Pressure As German Factory Orders Decline

EUR/USD has started the week with losses, continuing the downward trend seen on Friday. In the Monday session, the pair is trading at 1.1926, down 0.30% on the day. On the release front, eurozone data disappointed. Germany Factory Orders declined 0.9%, missing the estimate of a 0.5% gain. Eurozone Retail PMI dropped to 48.6, marking the first contraction since March 2017. As well, Eurozone Sentix Investor Confidence dipped to 19.2, well short of the forecast of 21.2 points. This marked a fourth straight drop. There are no major releases in the US. On Tuesday, Germany releases Industrial Production and Trade Balance, and the US publishes PPI and JOLTS Job Openings. We’ll also hear from Federal Reserve Chair Jerome Powell, who will speak at an event in Zurich.

German numbers are raising concerns about the strength of the eurozone’s largest economy. German Factory Orders posted a second decline in the past three months, pointing to weakness in the manufacturing sector. The markets will be hoping for better news from Industrial Production on Tuesday, with an estimate of 0.8%. The indicator has posted three straight declines. Last week’s PMI reports also disappointed. German Services PMI was the weakest since September 2016, and the eurozone reading also softened compared to March. This points to weaker expansion in services business activity, another indication of weaker eurozone growth in the first quarter of 2018. Manufacturing PMI weakened for a fourth consecutive month in April, and retail sales posted a fourth straight decline.

US employment numbers were mixed on Friday, but the euro was unable to make any headway. In the US, nonfarm payrolls rebounded with a gain of 164 thousand, although this fell short of the estimate of 190 thousand. Wage growth remained dropped from 0.3% to 0.1%, missing the estimate of 0.2 percent. There was some good news from the unemployment rate, which dropped to 3.9%, beating the estimate of 4.1%. The Fed will likely be pleased that nonfarm payrolls were not red hot, as they April report justifies its policy of gradual rate hikes.

U.S Dollar Bulls Take Firm Control

Monday May 7: Five things the markets are talking about

The U.S dollar remains in the ‘black’ ahead of the open stateside, reversing most of its earlier losses in the overnight session. Euro stocks are trading sideways following a muted Asian session, as oil extends its recent gains to new heights.

Note: In Europe, trading volumes remain light due to the May Day Bank holiday in the U.K.

In currencies, the yen weakened as capital markets returned from Golden Week holidays, while the euro was also weaker.

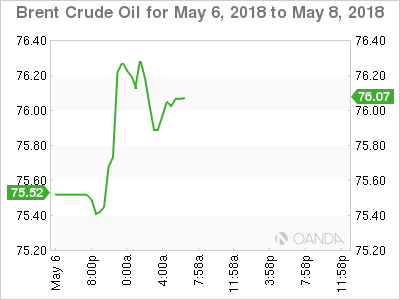

In commodities, WTI crude pushed above the psychological +$70 a barrel for the first time in nearly four years as the market braces for the re-imposition of U.S sanctions on Iran.

Expect geopolitics to remain in focus this week with President Trump expected to decide by May 12 whether the U.S stays in or pulls out of the Iran nuclear deal.

Elsewhere, U.S earnings season continues, and on the economic front, traders will watch out for an expected acceleration in U.S CPI (May 10, 08:30 am EDT).

On Tap this week: Nafta talks resume again in Washington today – it’s a critical period and the U.S is still pushing a hardline. China trade data will be the markets focus on Tuesday, along with Australia’s annual budget. On Thursday, the BoE takes center stage with its rate announcement, while U.S inflation data for April is due the same day.

1. Stocks mixed results, investors looking for substance

In Japan, the Nikkei share average ended flat in choppy trade overnight as hopes that the BoJ would buy ETF’s to offset weakness in financials, which were hit by falling U.S yields. The Nikkei ended little changed, while the broader Topix added +0.1%.

Note: Japanese markets were closed from Wednesday through Friday for Golden Shower week.

Down-under, Aussie shares ended higher on Monday, as a rise in materials stocks pushed the benchmark higher, although gains were capped as financials eased from intraday highs ahead of tomorrow’s 2018 annual budget. The S&P/ASX 200 index rose +0.36% at the close of trade. The benchmark fell -0.6% on Friday. In S. Korea, the Kospi closed out down -1.04%.

In Hong Kong, stocks rallied overnight, as fears of a full-blown Sino-U.S trade war receded ahead of a plethora of Chinese economic data in the coming weeks. The Hang Seng index rose +0.2%, while the China Enterprises Index gained +0.6%.

In China, stocks rebounded sharply on Monday amid optimism about robust April economic data despite lingering trade tensions. The blue-chip CSI300 index rose +1.6%, while the Shanghai Composite Index gained +1.5%.

In Europe, markets have opened flat and trade slightly higher. It’s not surprising to see trading volumes light with the U.K and Ireland closed for a bank holiday. Elsewhere, energy stocks are being supported with WTI topping +$70 a barrel.

U.S stocks are set to open in the ‘black.’

Indices: Stoxx50 flat at 3,548, FTSE closed, DAX +0.3% at 12,860, CAC-40 flat at 5,515; IBEX-35 +0.3% at 10,138, FTSE MIB +0.3% at 24,400, SMI +0.2% at 8922, S&P 500 Futures +0.3%

2. Oil higher on Venezuela and Iran worries

Crude oil prices have rallied +1% overnight to their highest levels since late-2014, pushed up by a deepening economic crisis in Venezuela and a looming decision on whether the U.S will re-impose sanctions against Iran.

Note: President Trump has until May 12 to decide whether to restore the sanctions on Iran that was lifted after an agreement over its disputed nuclear program.

Brent crude oil futures are at +$75.57 per barrel, up +70c, or +0.9%, from Friday’s close. Earlier in the session, they touched their highest since November 2014 at +$75.89 a barrel. U.S West Texas Intermediate (WTI) crude futures rose +70c, or +1% to +$70.42 per barrel.

Note: China’s Shanghai crude oil futures, launched in March, broke their dollar-converted record-high of +$71.32 per barrel by rising as far as $72.54 on Monday. Open interest and traded volumes for Shanghai crude also hit a fresh record overnight.

Nevertheless, helping to cap crude oil prices a tad, is an increase in U.S production – weekly rig counts from Baker Hughes’s – and last week’s U.S inventory reports (EIA and DoE) showed a weekly build up in supplies.

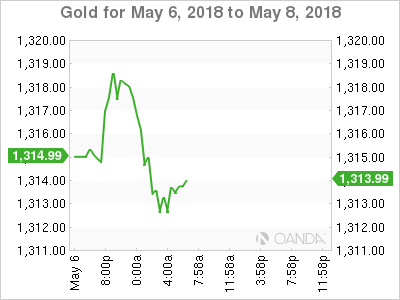

Ahead of the U.S open, gold prices have shed their earlier gains to edge lower, as the ‘big’ dollar holds near its four-month peak, dampening the appeal of bullion. Spot gold is down -0.2% at +$1,311.91 an ounce. U.S gold futures for June delivery slipped -0.2% to +$1,312.60 per ounce.

Note: Earlier in the session, it touched +$1,318.85, its highest since April 30.

3. BoE rate rise expectations collapse

Expectations for a rate increase by the Bank of England (BoE) this Thursday have collapsed (07:00 am EDT) since Governor Carney raised the alarm at the end of April.

Even PM Theresa May’s government has been able to cast some doubt over the timing, as too have U.K rate ‘hawks,’ who suggest that the recent set of soft U.K data also appears to speak against a rate raise anytime soon.

Market consensus believes that the BoE can afford to hold fire to buy time and see how things in consumer credit and retail space play out. However, the outlier remains U.K wage growth that continues to show signs of life, the BoE’s preference might remain for tighter monetary policy, and a hike in August is still a possibility.

The yield on U.S 10-year Treasuries has backed up +1 bps to +2.96%. In Germany, the 10-year Bund yield has dipped -1 bps to +0.53%, while in the U.K, the 10-year Gilt yield has climbed +1 bps to +1.4%.

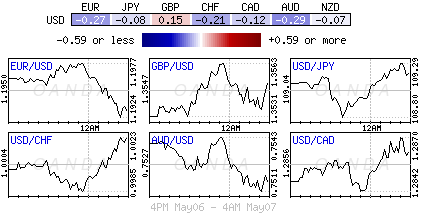

4. Dollars rise to continue

The U.S dollar continues its rise ahead of the open stateside, pushing EUR/USD (€1.1923) to its lowest in nearly four-months. Weaker Euro data (see below) is not helping the ‘single units’ cause.

Despite Friday’s U.S. jobs data miss, dollar ‘bulls’ believe the ‘buck’ still has some catching up to do. The DXY dollar index is up +0.1% at 92.70, close to it’s highest since late 2017.

Note: The DXY has fallen from a peak above 95 in mid-November, however, the market has priced in almost two additional Fed rate rises for 2018 and almost two for 2019.

Sterling traders will be focusing on Thursday’s BoE rate decision and whether it could be a ‘hawkish’ hold, which could help the pound (£1.3526) regain some of its shine.

Emerging market currencies remains weak – Turkey Central Bank (CBRT) has changed its reserve option mechanism to combat recent FX weakness. In Argentina, overnight rates have been aggressively hiked to +40% since last week, to stem the outflow capital from the country.

5. German manufacturing orders drop along with euro confidence

German manufacturing orders dropped for the third consecutive month in March, a further sign of cooling activity in German industry.

Total manufacturing orders fell -0.9% from the month before, which marks the third straight monthly decline. Market expectations had forecasted an increase of +0.5%.

Today’s data add to evidence that Europe’s largest economy has shifted down a gear, following strong growth in Q4, 2017.

Digging deeper, domestic orders for German manufacturing goods rose +1.5% from February, however, foreign demand was down sharply by -2.6%.

Other data this morning showed that the Sentix economic index for the euro zone fell for the fourth consecutive month in May and reached 19.2 points, its lowest level in 18-months. The situation and expectations also both fell slightly.

When is U.S punitive tariffs coming? The decision has not yet been made and it is therefore not surprising that the Sentix economic indices hardly changed in May.

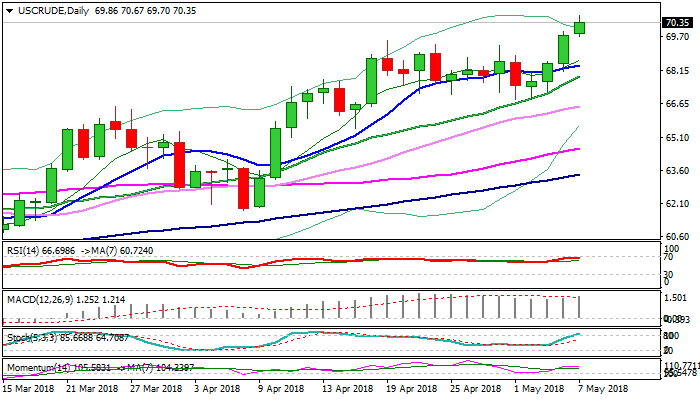

WTI Oil Surges Through Psychological $70 Barrier On Concerns About US/Iran Nuclear Agreement

WTI oil held strong bullish mode at the beginning of the week and surged through psychological $70 barrier, hitting new 3 ½ year high at $70.67 on Monday.

The oil extends steep rally off $66.84 trough in the fourth straight day and generated bullish signal on Friday’s completion of near-term $69.54/$66.84 corrective phase.

Break of psychological $70 barrier was strong bullish signal as the price hesitated under the barrier for two weeks.

Strong bullish sentiment was boosted by rising concerns about the US pulling out the Iran nuclear deal which could cause stronger uncertainty further tightening in global oil market.

President Trump has until 12 May to decide whether the US will pull out of agreement to curb Iran’s nuclear program in return to lifting sanctions on Iran’s oil export.

Eventual close above $70 barrier would generate signal continuation of larger uptrend which eyes targets at $74.94 (04 Oct 2011 low), with possible extension towards $76.35 (Fibo 61.8% of $107.45/$26.04 fall).

Bullish techs and positive sentiment continue to underpin, with rally to be likely interrupted by corrections on overbought studies, with all eyes on President Trump’s decision about nuclear deal with Iran.

Res: 70.67, 71.00, 71.21, 71.60

Sup: 70.00, 69.54, 69.32, 68.75

SPOT GOLD – Recovery Attempts Face Strong Headwinds

Gold price ticked higher on Monday and probed above falling 10SMA to peak at $1318, but gains proved to be short-lived for now.

The yellow metal is attempting to sustain recovery off $1300 zone, where 200SMA contained larger descend from $1355, but recovery attempts face strong headwinds and are on track to be repeatedly capped by falling 10SMA.

Weak momentum studies and overall bearish setup of daily MA’s maintain pressure, as the US dollar remains gold’s key driver and dollar bulls took a breather which resulted recent recovery attempts.

The downside is expected to remain vulnerable while 10SMA caps, keeping risk at $1304/00 pivots (200SMA/psychological support) loss of which could spark fresh bearish acceleration.Close above 10SMA (currently at $1315) is needed to generate bullish signal and open way for recovery extension towards next pivots at $1322/23 (Fibo 38.2% of $1355/$1301/100SMA).

Res: 1315, 1318, 1323, 1328

Sup: 1311, 1308, 1304, 1300