Sample Category Title

Eurozone Sentix investor confidence dropped to 19.2, lowest since Feb 2017

Eurozone Sentix investor confidence dropped to 19.2 in May, down from 19.6, missed expectation of 21.0. That's the 4th decline in a row, and hit the lowest level since February 2017. Current situation index dropped 0.2 to 42.8, lowest since October 2017. Expectations dropped to -2, lowest since October 2014.

Quotes from the release:

"Uncertainties about the introduction of punitive US tariffs and the danger that this could lead to an expansion of protectionist measures are weighing on us."

Overall Germany investor confidence index dropped 0.9 to 24.4, lowest since September 2016. Current situation index dropped 2.2 to 59.8, lowest since April 2017. Expectation index was unchanged at -7.8.

Eurozone retail PMI at 48.6, Italy sales decline accelerated sharply

Eurozone retail PMI dropped to 48.6 in April, down from 50.1. Weakness was driven by sharp decline in Italy which hit 21 month-low at 42.7. Germany retail PMI dropped to 9-month low at 51.0. France continued to outperform with retail PMI hit 2 month high at 50.1.

Quotes from Alex Gill, economist at IHS Markit:

"The latest data highlighted a disappointing month for the eurozone retail sector. Monthly sales were down for the first time for over a year as signs of restricted consumer demand and increased uncertainty begin to show. This was particularly evident in Italy, where the rate of decline in like-for-like sales accelerated sharply and was the most marked for the better part of two years.

"Forward-looking indicators add to the dull picture, with falls in purchasing activity and stocks of goods suggesting retailers are taking an increasingly cautious approach to their business operations. The one shining light was a further rise in staffing numbers. That said, without a rebound in customer demand we may see employment slip back into contraction territory in the coming months as well."

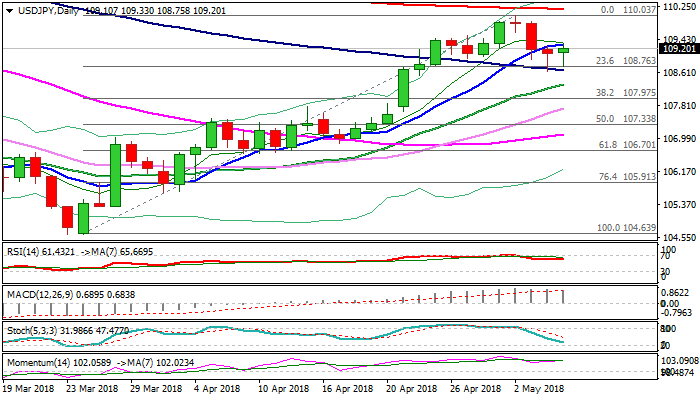

USDJPY – Break Above 10SMA Needed To Generate Bullish Signal And Sideline Existing Downside Risk

The pair bounced back above 109 handle in early European trading on Monday and tests again pivotal barrier at 109.30 (10SMA), following repeated downside rejection at strong 108.70 zone (Fibo 38.2% of 104.63/110.03, reinforced by falling 100SMA).

This sidelines immediate risk of deeper correction from 110 zone, where broader bulls have been capped, as overall structure is still bullish and would keep hopes of fresh attempts towards 110 zone while 108.70 zone supports hold.

Such scenario requires eventual break above 10SMA to open way towards key barriers at 110.03/17 (02 May three-month high / 200SMA).

Basing attempts at 108.70 zone support the notion, however, the downside is expected to remain vulnerable while 10SMA caps.

Bearish scenario requires firm break below 108.70 to open rising 20SMA (108.33) and risk extension towards key supports at 107.97/93 (Fibo 38.2% of 104.63/110.03 / daily cloud top).

Res: 109.30, 109.53, 109.88, 110.03

Sup: 108.76, 108.67, 108.33, 107.93

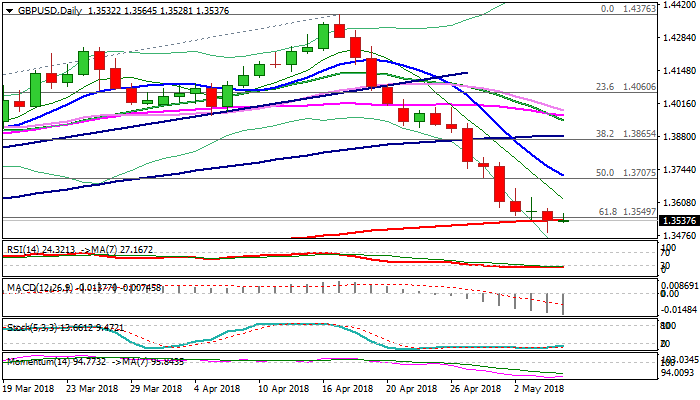

GBPUSD – 200SMA Is Key, Firm Break Lower To Signal Bearish Continuation And Neutralize Risk Of Bounce

Cable probes again through cracked 200SMA (1.3537) in early European session on Monday, after overnight’s recovery attempts were short-lived.

Despite spike below 1.35 on Friday, the pair failed to clearly break below 200SMA and generate bearish signal (Friday’s close was at 200SMA at 1.3535) and repeated failure at 200SMA today could increase risk of bounce.

Oversold daily RSI / slow stochastic and momentum turning higher, support scenario, which also needs close above broken Fibo support at 1.3550 (61.8% of 1.3038/1.4376) to generate further positive signal.

Recovery action could extend towards strong barrier at 1.3718 (falling 10SMA).

Conversely, close below 200SMA would risk retest of Friday’s spike low at 1.3486 and extension towards next pivotal support at 1.3442 (Fibo 38.2% of entire post-Brexit 1.1930/1.4376 recovery phase).

Res: 1.3564, 1.3585, 1.3629, 1.3665

Sup: 1.3528, 1.3486, 1.3442, 1.3400

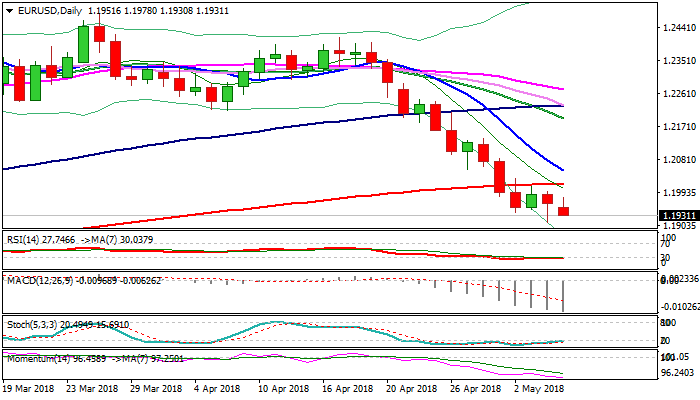

EURUSD – Negative Outlook Below 200SMA, Close Below 1.1936 Fibo Support To Confirm

The Euro stands at the back foot at the beginning of the week and probes through cracked Fibo support at 1.1936 (61.8% of 1.1553/1.2555 ascend) which held the consolidation in past few sessions.

Recovery attempts in Asia were capped under 1.20 barrier, keeping intact key barrier at 1.2016 (200SMA).

Negative near-term outlook is expected to persist while 200SMA caps and keep in focus target at 1.1910 (Friday’s spike low / new 2018 low), with stronger bearish acceleration capable of travelling towards 1.1790 (Fibo 76.4% of 1.1553/1.2555).

Eventual close below 1.1936 is seen as initial requirement for bearish continuation.

Meanwhile, the pair may hold within extended consolidation between 1.1936 and 200SMA, on conflicting daily studies (slow stochastic is reversing from oversold zone while 14-d momentum continues to trend lower.

Bullish scenario requires close above 200SMA to sideline immediate downside risk and signal recovery.

Res: 1.1978, 1.2000, 1.2016, 1.2053

Sup: 1.1910, 1.1893, 1.1854, 1.1816

Currencies: EUR/USD Test Of 1.1915/35 Continues Despite Mixed Payrolls

Rates: Neutral start to the trading week?

Rising oil prices helped erase initial core bond gains after a mixed US payrolls report. Core bonds eventually closed flat. Today's eco calendar only contains second tier eco data while volumes could be low with UK markets closed. Speeches by Fed governors and developments on the geopolitical scene are a wildcard for trading.

Currencies: EUR/USD test of 1.1915/35 continues despite mixed payrolls

On Friday, the dollar showed good resilience even as the payrolls didn't fully meet market expectations. EUR/USD tested the 1.1915/35 support and is still holding near that area this morning. We consider current context as USD neutral, but underlying euro softness still might keep EUR/USD near recent lows.

The Sunrise Headlines

- US stock markets closed the week on a strong note, ending more than 1% higher. Most Asian equity markets trade positive this morning with China outperforming and Japan underperforming.

- Iran, faced with a possible restoration of US sanctions, came out against higher oil prices, signaling a split with fellow OPEC member Saudi Arabia, which is showing a willingness to keep tightening crude markets. (BB)

- President Donald Trump's legal team is striking a more combative tone with Robert Mueller, suggesting publicly that the president may decline to cooperate with the special counsel's prosecutors. (WSJ)

- Conservative tensions over Brexit erupted again as a Business Secretary Clark fuelled speculation that May may be planning to revive a customs plan rejected by eurosceptic members of the government last week. (BB)

- The leader of Italy's anti-establishment 5-Star Movement, Di Maio, made a last-ditch offer to the far-right League in a bid to break a political deadlock that has dragged on for more than two months. (Reuters)

- Atlanta Fed Bostic and SF Fed Williams, voting FOMC members, argued in favour of 2 more hikes this year, but said they were keeping an open mind on the total number of interest rate rises needed.

- Today's eco calendar contains several Fed speakers, but only second tier eco data. UK markets are closed for Early May Bank Holiday

Currencies: EUR/USD Test Of 1.1915/35 Continues Despite Mixed Payrolls

Test of EUR/USD 1.1915/35 support continues

On Friday, US payrolls were mixed. The unemployment rate declined to an ‘impressive' 3.9%, but job growth and AHE were mediocre. However, the dollar showed remarkable resilience and jumped even temporary to a new ST reaction top (against the euro and in the trade-weighted dollar). EUR/USD even tested the 1.1915/35 area. The USD rebound eased later in the session. EUR/USD closed the session at 1.1960 (from 1.1988). USD/JPY finished little changed (109.12). So, the impact of the payrolls on the dollar was modest. At the same time, US yields and the dollar could have ‘suffered' more on the report. Regarding EUR/USD some underlying euro softness was probably still at play.

Overnight, Asian equities reversed initial softness. Most indices now show decent gains, with Japan underperforming. Geopolitical risk (Iran deal) remains a source off uncertainty, but for now markets still ponder what weight to give to the issue. Oil extends its rebound with Brent trading north of $75 p/b and WTI clearing the $70 barrier. Despite the rise in oil, the dollar is also holding up well. EUR/USD trades in the 1.1950 area. USD/JPY dropped temporary below 109 this morning, but also reversed this initial decline. So, global markets show somewhat of a diffuse picture this morning.

Today, there are few important eco data in the US or in Europe. Several Fed MPC members will speak. The will probably elaborate on the issue of ‘symmetrical' US inflation target. As such, we consider this as the Fed at least temporary moving to a more wait-and-see policy stance. However, for now it has no noticeable negative impact on the dollar. Geological issues remain also wild card. We see the current context as rather neutral for the dollar. Even so, EUR/USD is holding near the 1.1915/35 support area. Ongoing euro softness still might help for investors to try a new downside test in EUR/USD. The case for a higher USD/JPY looks for less convincing.

On Friday, EUR/GBP hovered in the lower half of the 0.88 big figure. There were no important eco data. The internal rift within the UK Conservative Party on ‘ the nature of Brexit' continued. This was still the case this weekend as UK Business Secretary Greg Clark indicated that a compromise on a customs union was still on the table. EUR/GBP is drifting back south this morning. We expect more sideways trading going into Thursday's BoE policy meeting

EUR/USD: test of 1.1935/15 support continues despite mixed payrolls

Dollar Climbs After Jobs Data, Trade Developments Eyed

Here are the latest developments in global markets:

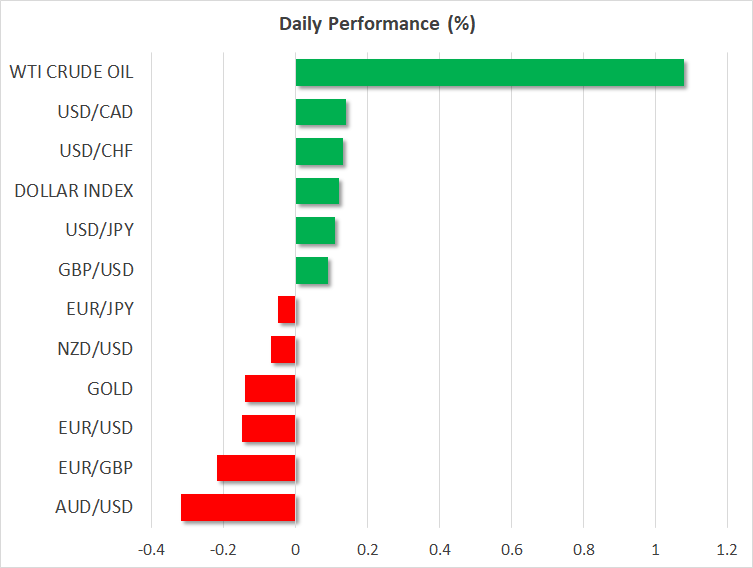

FOREX: The US dollar index is 0.1% higher on Monday, extending the gains it posted on Friday in the aftermath of the US employment report for April. The US unemployment rate touched a 17-year low, likely enhancing speculation that an ever-tightening labor market is set to push wages higher in the coming months – labor force participation did fall as well though.

STOCKS: Wall Street closed higher on Friday, paring some early losses posted after the US employment report to rally into the close. The Nasdaq Composite climbed by 1.71%. Meanwhile, the Dow Jones and the S&P 500 gained 1.39% and 1.29% respectively, with both of these indices surging after they found support near their 200-day moving averages. The gains were partly fueled by Apple Inc (+3.92%), which closed at a record high following news that Warren Buffet's Berkshire Hathaway increased its stake in the company even further. As for today, futures tracking the Dow, S&P, and Nasdaq 100 are all flashing green, pointing to a higher open. In Asia, Japan was mixed with the Nikkei 225 falling by 0.025% but the Topix rising 0.09%, while in Hong Kong, the Hang Seng was down by 0.16%. In Europe, futures tracking all the major indices were in the green, with the only exception being France's CAC 40.

COMMODITIES: Oil prices surged on Friday and are also higher this week. WTI and Brent are up by 1.1% and 1.0% respectively on Monday, both benchmarks touching fresh highs last seen in 2014. Energy markets largely overlooked another rise in the Baker Hughes oil rig count on Friday, which increased by 9 rigs, and instead focused on the prospect of fresh sanctions on Iran. This story is likely to get a lot more attention this week, as the self-imposed US deadline on making a decision about Iran is May 12. Worries around Venezuelan oil production falling even further likely aided the rally. In precious metals, gold is nearly 0.2% lower today, currently trading near the $1,313/ounce mark. The dollar-denominated metal has been on the decline for three consecutive weeks now, as the rebound in the dollar is weighing on demand.

Major movers: Dollar goes into a spin, but closes higher after jobs data

The US employment report released on Friday was mixed, sending the dollar into a spin, though the currency managed to finish the day higher overall. Nonfarm payrolls and wage growth were disappointing, both coming in lower than their respective forecasts. NFP came at 164k in April, missing the consensus for 192k, while average hourly earnings clocked in at 2.6% year-on-year, below the forecast of 2.7%. Last month's print was revised lower to 2.6%. As a result, the knee-jerk reaction in the dollar at the release was negative.

The dip was short-lived though, with the greenback managing to recover all its losses and trade even higher in the following hours, as markets digested the data and focused on the other aspect of the report; the unemployment rate. It fell to 3.9% from 4.1% previously, beating the forecast for a smaller decline to 4.0%. This was the lowest rate recorded in nearly two decades. Although part of the decline may be owed to a similar fall in the labor force participation rate, this still managed to ignite speculation for a more hawkish Fed down the road. The unemployment rate is now notably below full employment levels, which implies that wage growth may be set to pick up speed in the coming months, leading to a more aggressive Fed. Both euro/dollar and sterling/dollar touched fresh four-month lows in the aftermath.

On the trade front, the US-China talks in Beijing that concluded on Friday appear to have yielded no material results, with the two sides simply agreeing to continue negotiating.

In the energy market, oil prices hit their highest levels since November 2014 amid speculation that this week will bring fresh sanctions against Iran, thereby removing a significant chunk of oil supply from the market. The US is set to decide by Saturday, though any comments from the US administration on the subject could move oil prices even before then.

In emerging markets, the Turkish lira posted a new all-time low against the US dollar on Friday, as a combination of high inflation and a large current account deficit continued to apply downward pressure on the currency. In Argentina, the central bank raised interest rates to 40%, in an attempt to stem further declines in the peso and reign in inflation.

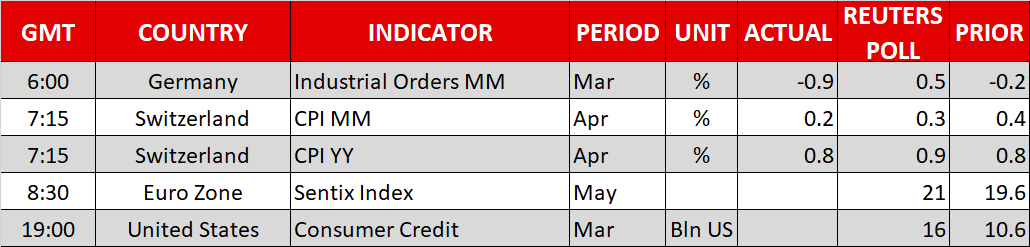

Day ahead: Light calendar with eurozone's Sentix index and US consumer credit data on the agenda; trade issues could take center stage

Monday is a light day in terms of economic releases, with the calendar featuring the Sentix index, which gauges investor confidence in the eurozone, and consumer credit data out of the US.

At 0830 GMT, the Sentix index will be made public. Eurozone investor morale in May is anticipated to edge higher after declining in the three preceding months. Worries about easing expansion in international markets and global trade tensions – most notably between the US and China – were seen as factors leading to the measure's decline earlier in the year.

The US will be on the receiving end of consumer credit data at 1900 GMT. Credit is projected to have risen by $16.0 billion in March. This compares to February's $10.6bn.

In equities, this will be another busy week in term of corporate earnings, with Walt Disney (Tuesday) and Nvidia (Thursday) being two of the companies releasing results as the week unfolds. Equity market sentiment could be driven by developments on global trade though, as NAFTA talks are resuming today in Washington. Meanwhile, discussions between the US and China last week seem to have produced little progress and any updates on this front will be closely watched as well – beyond stock markets, trade developments also have the capacity to affect other markets, such as currency and fixed income ones.

Regional Fed Presidents Raphael Bostic (1225 GMT – voting FOMC member in 2018), Tom Barkin (1800 GMT – voter), Patrick Harker (1800 GMT – non-voter), Robert Kaplan and Charles Evans (both non-voters and both at the same venue at 1930 GMT) will be making appearances today.

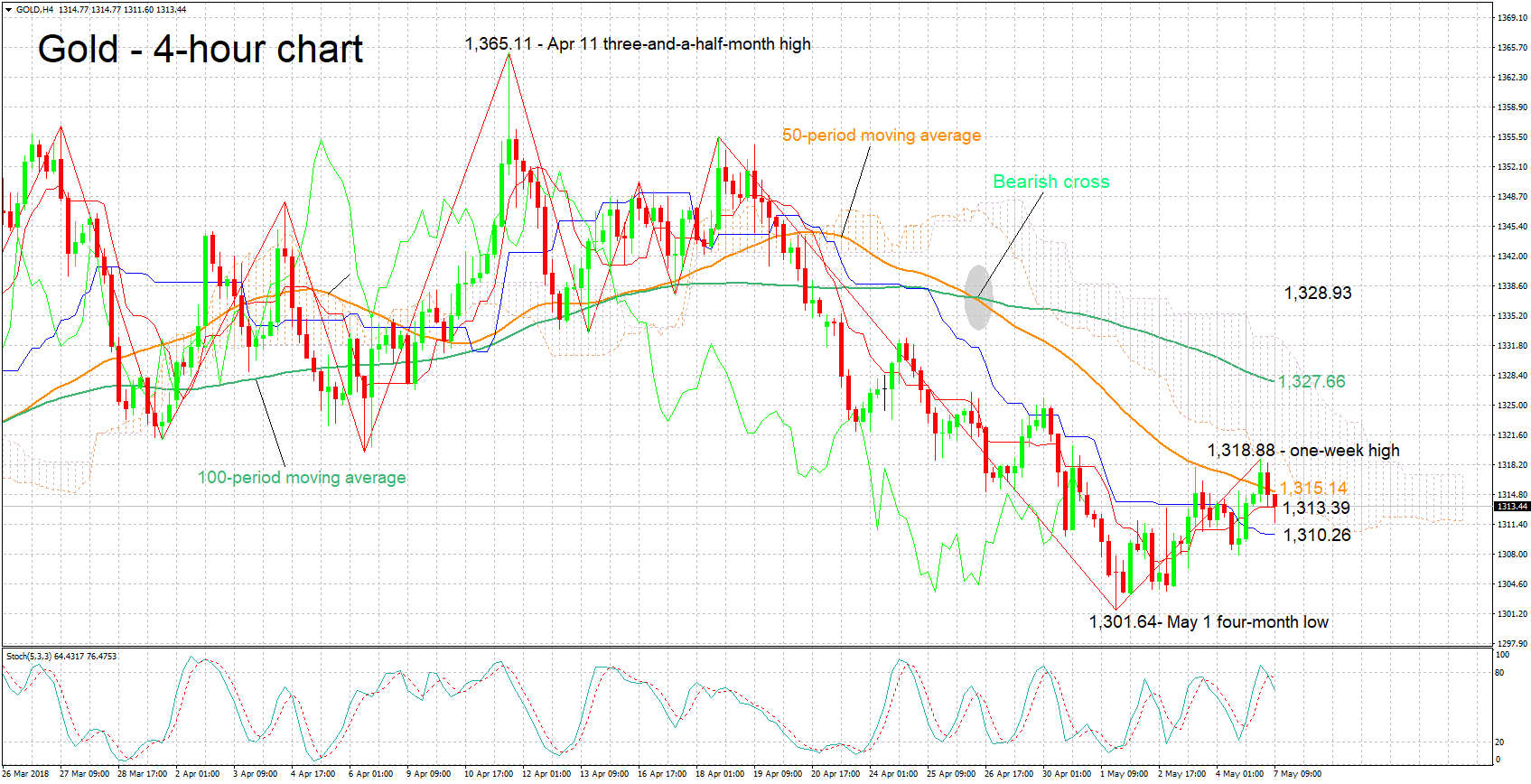

Technical Analysis: Gold retreats after hitting 1-week high; bearish signal by stochastics in very short-term

Gold posted a one-week high of 1,318.88 earlier on Monday before retreating a bit. The Tenkan- and Kijun-sen lines are positively aligned in support of a bullish short-term picture. Notice, though, that the two have flatlined; bullish momentum may be easing. Moreover, the stochastics are giving a bearish signal in the very short-term: the %K line has crossed below the slow %D one.

Rising global trade tensions might support the safe-haven perceived asset. Resistance to advances could come around the current level of the 50-day moving average at 1,315.14 and further above from the area around the Ichimoku cloud bottom at 1,319.65 (this also encapsulates today's one-week high of 1,318.88).

Receding trade worries on the other hand might divert funds out of gold and into riskier assets. The yellow metal could be finding support around the current level of the Tenkan-sen at 1,313.39 at the moment, with steeper declines turning the attention to the Kijun-sen at 1,310.26. Further below, the focus would increasingly start to shift to the four-month low of 1,301.64 from May 1.

A rising US currency could also exert pressure on the dollar-denominated metal, and vice versa.

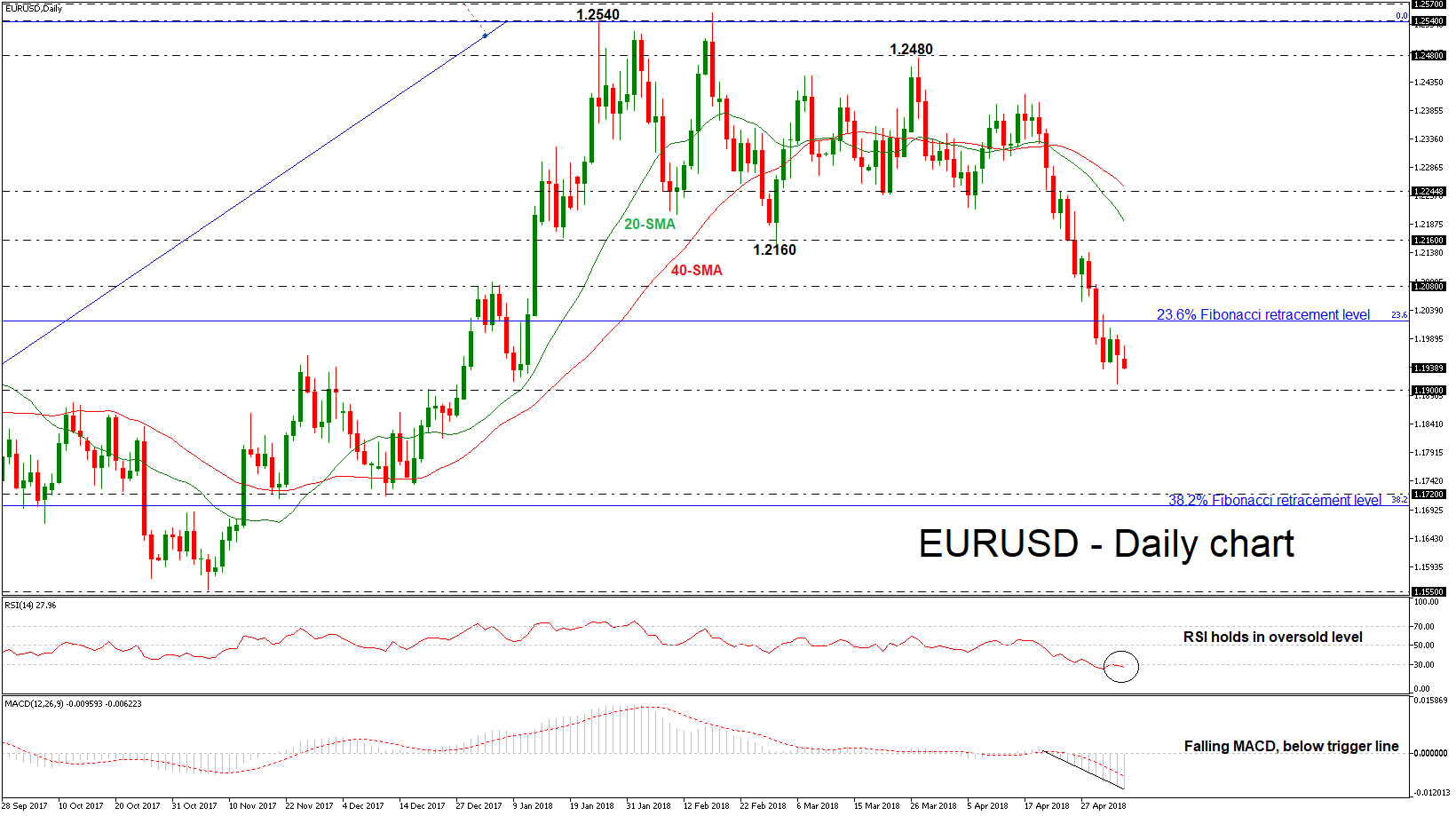

EURUSD Remains Under Pressure, Maintains Short-Term Bearish Bias

EURUSD remains under pressure and risk is still to the downside as prices continue to drift lower from the 23.6% Fibonacci retracement level of 1.2020 of the upleg from 1.0340 to 1.2540, which is acting as strong resistance level for the bulls. The short-term technical indicators are bearish and point to more weakness in the market.

Looking at the daily timeframe, the Relative Strength Index (RSI) is holding in oversold levels but is flattening, while the MACD oscillator is falling with strong momentum below the trigger and zero lines, signaling further losses. Also, the 20- and 40-simple moving averages (SMA) are moving lower following the price action.

The next target to the downside is the December 2017 high of the 1.1900 strong psychological level. At this stage, the market would likely see a resumption of the downtrend and re-challenge the 1.1720 support level, which stands near the 38.2% Fibonacci mark.

Upsides moves are likely to find resistance at the 23.6% Fibonacci of 1.2020. Rising above this area would help shift the focus to the upside towards the 1.2080 resistance barrier. Breaking this level could see a re-test of the 1.2160 hurdle and turn the bias to bullish.

In the short-term, the bearish phase remains in play especially if prices continue to trade below the 23.6% Fibonacci mark. In the bigger picture, the pair posted three negative weekly sessions and is in the process to turn the bullish outlook to bearish.

Gold Edges Lower After Touching 1319 Resistance Level, Holds In Trading Range In Medium Term

Gold has been edging sharply lower during today’s European session after the pullback on the 1319 resistance level. It is worth mentioning that the price has been developing within a trading range since January 2 with the 1365 resistance level being the upper boundary and the 1303 support level the lower boundary, while it lacks a clear trend.

Technically, in the 4-hour chart, the RSI indicator is sloping to the downside and is approaching the negative territory, while the stochastic oscillator posted a bearish cross within the %K line and the %D line, signaling further downside pressure in the positive area.

In the wake of negative pressures and a drop below the 20-simple moving average (SMA) in the near-term, the market could meet the 1303 strong support barrier. A successful close below this level could see a break of the consolidation zone and drive the precious metal lower towards 1289 taken from the high on December 2017.

However, if prices are able to break above the 20-SMA near 1313 in the next few sessions, the risk would shift to the upside, specifically towards the 1319 resistance level. A jump above this level could push the precious metal higher until the 1325.75 resistance barrier.

What To Watch In The Week Ahead?

U.S. equities rallied sharply at the end of last week as did the dollar, despite the NFP disappointment.

The headline number for the rise in jobs came short of analysts’ expectations, “164K vs. 193K forecast”, but the previous month’s figure was revised up by 32K. Average hourly earnings also came in below expectations, growing by 2.6% YoY. The bright spot was the unemployment rate which dropped to an 18-year low at 3.9%.

Overall the labor market remains solid, and with rising inflation the Federal Reserve will persevere with monetary policy normalization. However, there isn’t enough indication yet of the economy overheating, suggesting that two more rate hikes for 2018 will remain the base case scenario.

With the U.S. earning season coming closer to an end, politics are likely to dominate again. Here’s what to watch for the week ahead.

Decision on China, Nafta talks

The first round of negotiations between China and the U.S. ended on Friday with no breakthrough. Although China said some progress was made in trade talks, there weren’t any tangible results. The U.S. demanded China cut the trade deficit by at least $200 billion by the end of 2020, which to many economists seems a mission impossible. The ongoing negotiations might have bought some time and eased tensions in the short-run, but investors will remain alert for another round of trade threats. Markets will closely scrutinize any statement from President Trump on this front.

The negotiation skills of team Trump will be tested again next week, as Nafta talks resume. According to U.S. Trade Representative, Robert Lighthizer, failure to complete trade negotiations with Canada and Mexico in the next two weeks could put the agreement in jeopardy. The Canadian dollar and Mexican peso would be hit hard if a deal doesn’t come through.

Iran Nuclear deal

With oil trading at its highest levels in more than three years, investors are in “wait-and-see” mode on whether to push prices to new highs or start taking some profit. Over the past few weeks, Trump has been criticizing the Iranian nuclear deal and is set to withdraw from it on 12 May, unless his European allies agree to fix the deal. Although oil prices have benefited from tighter supplies, a lot of risk premium has been priced in due to Trump’s threat. However, it's challenging to know the magnitude of reimposing sanctions on oil exports from Iran. That’s why analysts’ expectations varied widely on this front. Whether exports will be hit by 100 thousand or 1 million depends on the nature of the new sanctions. How will Europe react? Will sanctions hit banks and businesses dealing with Iran? How will Iran respond? What about the impact on Middle East politics? Until we get answers to these questions, it’s difficult to estimate the impact on Iranian oil exports. However, prices may remain elevated and even reach $80 in the short run.

Bank of England

A couple of weeks ago, it looked certain that the Bank of England would be hiking rates by 25 basis points, during its May policy meeting. This was before a round of disappointing UK economic data and BoE Governor Carney seemingly backtracking once again from his previous tone that the markets should prepare for an interest rate rise. It is now expected that the BoE will look to raise interest rates gradually and is conscious that there are other meetings over the course of 2018 to raise UK interest rates. As a result, the pound plunged by more than 800 pips from its 17 April peak. While a rate hike is off the table for now, forward guidance may lend the GBP some support, especially if new voices were added to Michael Saunders and Ian McCafferty, who voted for a rate hike in the last meeting.