Sample Category Title

Dollar Mildly Firmer in Quiet Markets, USD/JPY Pressing Channel Support

The forex markets open the week rather quietly today. Dollar is trading mildly firmer in tight range against other major currencies. Aussie is so far the weakest one today, getting no support from positive business condition and confidence data. Markets could remain quiet today with UK on holiday. The economic calendar is also relatively light.

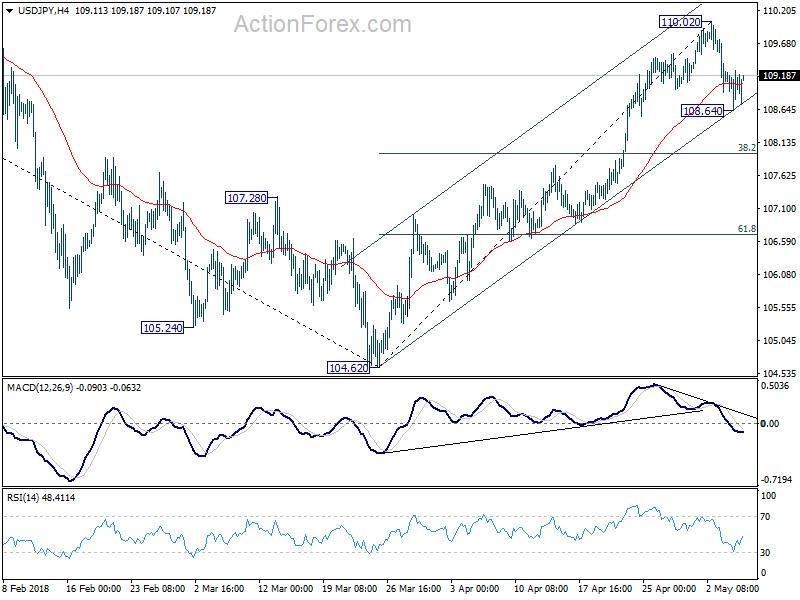

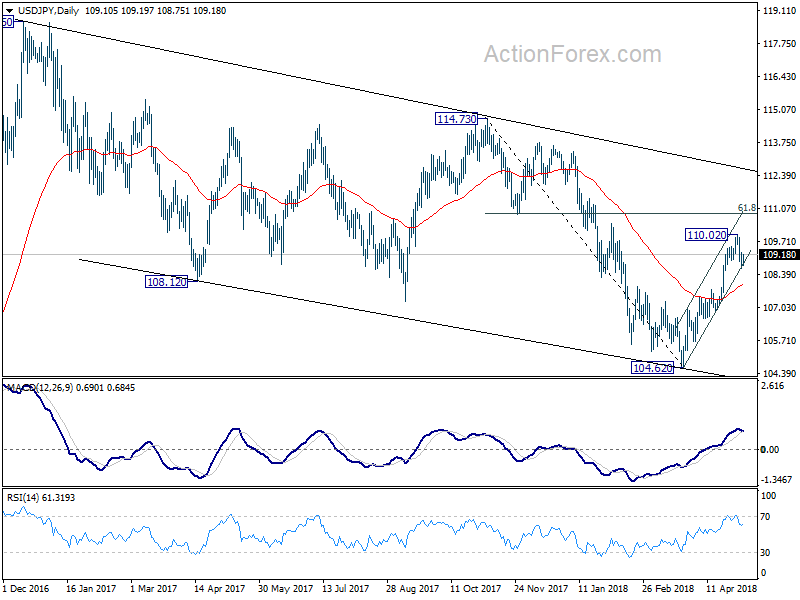

Technically, with near term minor support levels intact, the greenback is expected to rise further against all, except Yen. While USD/JPY's decline slowed after hitting 108.64 last week, the pull back from 110.02 could still extend deeper. The depth of which will depend on how much support USD/JPY would get from channel line (now at 108.72).

BoJ March meeting minutes: Not the time to consider stimulus exit yet

In the minutes of March BOJ meeting, some members emphasized the need to have the best communications to the markets. To be more specific, "it was important for the BOJ to thoroughly explain to the public ... that the economy had not yet reached a phase where it should consider the timing and measures of a so-called exit from monetary easing," Also "while normalization, or a gradual reduction in the degree of monetary accommodation, could become a topic for consideration in the future, the BOJ needs to explain to markets that normalization ... would be different from monetary tightening,"

Australia NAB business condition hit record high, but RBA could delay rate hike to 2019

Australia NAB business condition rebounded notably from 15 to 21 in April. That's also a rerecord high since the survey started in March 1997. Business confidence also rebounded from 8 to 10. Alan Oster, NAB Group Chief Economist noted in the release that the results reinforces the evidence of "robust" business activity. Except manufacturing and retail, conditions increased in all industries. And, strength in both business conditions and confidence suggest that "economic growth will strengthen and that over-time".

Meanwhile, falling unemployment rate should "eventually translate into upwards pressure on private sector wages". That would put RBA into a position to "start increasing the current emergency low policy rate:. NAB maintained the forecast for RBA to hike later this year. However, "as hard evidence of a firming in wages growth is yet to appear in the data, and unemployment for the moment stuck at around 5.5%, the risk is that any action by the RBA will be delayed into 2019".

RBNZ to stand pat this week, likely throughout 2018 too

Two central banks will meet this week. RBNZ is expected to keep the official cash rate unchanged at 1.75%. There is little chance of a surprise given the CPI slowed deeply to 1.1% yoy in Q1. RBNZ Governor Adrian Orr also said after the release that "very benign inflation going forward without doubt, as we've forecast." According to a Reuters poll, all 16 economists surveyed expected RBNZ to stand pat this week. 14 economists expected RBNZ to hold throughout 2018. 8 forecasts RBNZ to hike by the end of Q3 2019.

BoE to stand pat, eyes on new forecasts and voting

BoE is widely expected to keep bank rate unchanged at 0.50%. Asset purchase target will also be maintained at GBP 435B. The expectation of a May hike waned after recent batch of weak data. UK CPI grew merely 0.1% qoq in Q1. April PMIs showed that rebound at the start of Q2 was weak. And, UK CPI also slowed more than expected to 2.5% yoy in March, giving BoE less pressure to hike immediately.

It's now seen that BoE would delay the gradual tightening of of monetary policy. But interest rates are still on the path of going up. Markets are pricing in around 50% chance of hike by August. But we'd argue that November is a better timing until there is a drastic turn in momentum in the latter half of Q2.

But such market expectations could shift drastically. Firstly, BoE will release the quarterly Inflation Report and we'll see how the data released in the past three months affect the growth and inflation projections. Secondly, it would be interesting to see if the two known hawks, Ian McCafferty and Michael Saunders, would change their mind and refrain from voting for rate hike again. And turn in the two could trigger steep selloff in the Pound.

The week ahead

In addition to the two central bank meetings there are a number of economic data to watch too. US CPI will be the most important one. Also, there will be Australia retail sales, China trade balance, ECB monthly bulletin, UK productions and Canada employment. Here are some highlights for the week:

- Monday: German factory orders; Swiss foreign currency reserves, CPI; Eurozone retail PMI, Sentix investor confidence

- Tuesday: Japan household spending; Australia retail sales; China trade balance; Swiss unemployment rate; German industrial production, trade balance; Canada housing starts

- Wednesday: Japan leading indicators, labor cash earnings; Australia Westpac consumer sentiment; Canada building permits; US PPI

- Thursday: RBNZ rate decision; BoJ summary of opinions; China CPI and PPI; ECB monthly bulletin; BoE rate decision, UK productions, trade balance; US CPI, jobless claims; Canada New housing price index

- Friday: New Zealand BusinessNZ manufacturing index; Australia home loans; Canada employment; US import prices, U of Michigan consumer sentiment

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.69; (P) 108.98; (R1) 109.32; More...

Intraday bias in USD/JPY remains neutral for the moment. The pull back from 110.02 short term top halted after drawing support from near term channel. But break of 110.02 is needed to confirm resumption of rise from 104.62. Otherwise, more consolidation could be seen. And below 108.64 will bring deeper fall to 38.2% retracement of 104.62 to 110.02 at 107.95. In that case, we'd expect strong support fro 107.95 to contain downside and bring rebound. On the upside, break of 110.02 will resume the rise from 104.62 to t 61.8% retracement of 114.73 to 104.62 at 110.86 next.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 55 day EMA (now at 107.95) holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above. However, sustained break of 55 day EMA will dampen this bullish view and turn focus back to 104.62 low instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Minutes | ||||

| 1:30 | AUD | NAB Business Conditions Apr | 21 | 14 | 15 | |

| 1:30 | AUD | NAB Business Confidence Apr | 10 | 7 | 8 | |

| 6:00 | EUR | German Factory Orders M/M Mar | 0.50% | 0.30% | ||

| 7:00 | CHF | Foreign Currency Reserves (CHF) Apr | 738B | |||

| 7:15 | CHF | CPI M/M Apr | 0.30% | 0.40% | ||

| 7:15 | CHF | CPI Y/Y Apr | 0.90% | 0.80% | ||

| 8:10 | EUR | Eurozone Retail PMI Apr | 50.1 | |||

| 8:30 | EUR | Eurozone Sentix Investor Confidence May | 21 | 19.6 |

BoE to stand pat, eyes on new forecasts and voting

BoE is widely expected to keep bank rate unchanged at 0.50%. Asset purchase target will also be maintained at GBP 435B. The expectation of a May hike waned after recent batch of weak data. UK CPI grew merely 0.1% qoq in Q1. April PMIs showed that rebound at the start of Q2 was weak. And, UK CPI also slowed more than expected to 2.5% yoy in March, giving BoE less pressure to hike immediately.

It's now seen that BoE would delay the gradual tightening of of monetary policy. But interest rates are still on the path of going up. Markets are pricing in around 50% chance of hike by August. But we'd argue that November is a better timing until there is a drastic turn in momentum in the latter half of Q2.

But such market expectations could shift drastically. Firstly, BoE will release the quarterly Inflation Report and we'll see how the data released in the past three months affect the growth and inflation projections. Secondly, it would be interesting to see if the two known hawks, Ian McCafferty and Michael Saunders, would change their mind and refrain from voting for rate hike again. And turn in the two could trigger steep selloff in the Pound.

BoE Could be More Dovish than “Hawkish Hold”

BOE is almost certain to keep the Bank rate unchanged at 0.5% in the May meeting. Weakness in PMI data released last week aggravated concerns that recent the moderation in economic activities might persist. Doubts have arisen that whether the slowdown in 1Q18 is only driven by transitory factors or indeed by some underlying reasons. While the market continues to expect the BOE to maintain the so-called “hawkish hold” in May – members voting 7-2 to leave rate at 0.5% and maintaining the rhetoric that “an ongoing tightening of monetary policy over the forecast period would be appropriate”, we actually believe it is possible for the central bank to turn more dovish, e.g. revising lower GDP growth and inflation forecasts. The market has now priced in only 50/50 chance of an August hike. Indeed, the possibility of an unchanged monetary policy throughout the year has increased.

Released last week, Markit’s PMI report indicated weakness in UK economic activities might extend from the first quarter to the second quarter. Services PMI recovered slightly, by +1.1 points to 52.8 in April. Yet, this missed consensus of 53.5. The improvement from March’s 20-month low of 51.7 was just mild and marked the second weakest rate of growth since September 2016. Manufacturing PMI dropped -1.2 points to a 17-month low of 53.9, missing expectations of 54.8. The sub-indices of output, new orders and employment also displayed slowdown in growth. As Markit noted “while adverse weather was partly to blame in February and March, there are no excuses for April’s disappointing performance, making the chances of a near term hike in interest rates by the Bank of England look increasingly remote”. It added that “the sector is unlikely to see any improvement on the near-stagnant performance signaled by the opening quarter’s GDP numbers” and “the trend in manufacturing production is likely to remain subdued”. Construction PMI improved to 52.5 from 47. This beat consensus of 50.5. While the rebound appeared strong, it was after the weather-related disruption in March. Underlying demand across the construction sector remained subdued, with total new work rising only marginally in April.

In the previous report (https://www.actionforex.com/action-insight/special-topics/90825-brexit-uncertainty-remains-key-determinant-of-boes-rate-hike-path/), we suggested that the government, and probably BOE officials, might have seen the disappointing GDP growth in 1Q18 as driven by adverse weather, temporary factor that should not continue in coming months. However, the weakness in PMI reports are probably first hints that the slowdown might have persisted in the second quarter. That is something worth monitoring.

The ease in inflation has also made a rate hike less imminent. Back in November, BOE’s rate hike was driven by the fact that inflation has overshot +3%, significantly higher than the +3% target, for months. Governor Mark Carney noted at the November meeting that inflation is “unlikely to return to the 2% target” without a rate hike.

Back then, the governor had since September prepared the market for the November rate hike. In February this year, Carney hinted at earlier and larger rate increases with the meeting minutes indicating that “monetary policy would need to be tightened somewhat earlier and by a somewhat greater extent over the forecast period than anticipated at the time of the November report”. It was interpreted as a hint for the May hike. However, the central bank has changed course over the month. Carney noticeable turned more dovish at his BBC interview on April 19. While affirming a rate hike is “likely” this year, he emphasized that any increase would be “gradual”. The Governor attempted to downplay the chance of a May rate hike. As he noted, “I am sure there will be some differences of view but it is a view we will take in early May, conscious that there are other meetings over the course of this year”. He suggested that there was a lot of data to consider before the decision in May, adding that “we have had some mixed data… On the softer side some of the business surveys have come off. Retail sales have been a bit softer – we are all aware of the squeeze that is going on in the high street”. The language, together with recent soft economic data, suggest that the chance for a May rate hike in May is remote.

RBNZ to stand pat this week, likely throughout 2018 too

RBNZ is expected to keep the official cash rate unchanged at 1.75%.

According to a Reuters poll, all 16 economists surveyed expected RBNZ to stand pat this week. 14 economists expected RBNZ to hold throughout 2018. 8 forecasts RBNZ to hike by the end of Q3 2019.

Sluggish inflation is a key factor giving RBNZ room for not acting. CPI slowed deeply to 1.1% yoy in Q1, sitting near the lower end of the target band.

RBNZ Governor Adrian Orr also said after the release that "very benign inflation going forward without doubt, as we've forecast."

He added that “what really matters is the confidence and expectation and belief that we are aiming for that midpoint of 2 percent all of the time.” And he pledged that “we are doggedly determined to aim for two percent, but the accuracy around…that is very limited.”

BoJ March meeting minutes: Not the time to consider stimulus exit yet

In the minutes of March BOJ meeting, some members emphasized the need to have the best communications to the markets.

To be more specific:

- "It was important for the BOJ to thoroughly explain to the public ... that the economy had not yet reached a phase where it should consider the timing and measures of a so-called exit from monetary easing,"

- "While normalization, or a gradual reduction in the degree of monetary accommodation, could become a topic for consideration in the future, the BOJ needs to explain to markets that normalization ... would be different from monetary tightening,"

One member warned of the risk of prolonging ultra loose monetary policy, on financial institutions:

- "There was a risk financial intermediation would be pulled back if the low-yield environment was further prolonged,"

And, one member expressed the concern of weakness in consumption recovery.

Market Morning Briefing: Euro Yen Had Broken Below Support Near 131

STOCKS

Dow (24262.51, +1.39%) has moved up from support levels near 23500 and while that holds, there is scope for the index to rise towards 24400 in the coming sessions. Overall broad range of 24400-23500 is likely to hold for the medium term.

Dax (12819.60, +1.02%) has moved up a bit and could gradually rise towards 12900-13000 levels in the near term. View remains bullish while above 12700.

Japan was in a holiday mood since 3rd May and the stock index has opened today on a negative note, trading below the resistance at 22600. Nikkei (22372.14, -0.45%) could dip from current resistance levels and head towards 22200 or lower in the coming sessions. Only on a sustained break above 22600, we may expect a sharp rise towards 23000; else the index is likely to remain bearish.

Shanghai (3116.66, +0.83%) needs to break above 3150 in the coming sessions to be able to move higher towards 3200 or above. For now while below 3150, the index is likely to remain trapped in the 3150-3050 region.

Nifty (10618.25, -0.57%) has been coming off from levels near 10800 as expected and while that holds, the fall could continue targeting 10500 in the near term.

COMMODITIES

Crude oil trades higher as the deadline of Iran sanctions (May 12th) nears. Brent (75.22) is ready to test the previous high near 75.60 and looks bullish just now. Brent could continue to move up to make fresh highs in the current rally this week.

Nymex WTI (70.18) is up as well and could head towards 71-72 levels soon. Near term looks bullish. Note that 72 is an important resistance which may hold in the medium term.

Gold (1317.66) is stuck in the 1310-1325 region and is unable to decide which direction to take. While the metal price remains above 1300-1310, eventual rise towards 1350 is possible.

Copper (3.0834) is likely to trade sideways in the 3.05-3.15 region for the coming sessions.

FOREX

Dollar index (92.474) saw a low of 92.35 on Friday but has risen from there once again. While it stays below 92.5, there are chances of it ranging between 92.5-92.3 for some time; if it goes below 92.3, it could test 92.0-91.50 as well. A breach of 92.5 could take it higher towards its medium term target of 94-95 (which corresponds to the 5th wave starting point of the downmove since Dec '16).

Euro (1.1971) couldn't move up past 1.20 on Friday. There are still some chances for it to rise towards 1.20. If it moves above 1.202 (earlier mentioned as 1.201), it could then go up till 1.205-1.210 before resuming its downtrend again in the medium term. A dip below 1.193 would make it bearish towards its medium term target near 1.16-1.17 (which is the 5th wave starting point of the Euro's upmove since Dec '16).

Dollar Yen (108.98) had dipped to 109 after testing highs near 110.04 last week. It has support on daily candles near 108.75-108.90 from where it could again move higher towards 110.5-110.75 in the near term. The broader uptrend looks capped till 110.50-110.75 in the medium term, after which Dollar Yen could turn bearish.

Euro Yen (130.47) had broken below support near 131 on weekly candles last week. Lower support on weekly candles near 130.00-129.75 is expected to give it support this week since both Dollar Yen and Euro could rise towards 110 and 1.20 respectively.

Pound (1.3554) turned very bearish last week after breaking below crucial long term support level near 1.385 on weekly line chart. It is continuing to move down towards its next downside target of 1.35-1.345 (seen on daily candles), which could possibly be tested this week.

Dollar Rupee (66.885) tested previous high near 66.91 on Friday, but did not break above it. The market closed relatively strong on Friday (rather than relatively weak) and as such there can be chances of further extension on the upside to 67.00-20 in the near term. Avoidance of the upside will need a fall/ break below 66.50 at least. For the time being, the trend still points upwards.

INTEREST RATES

The Fed maintained status quo in its May meeting last week but expressed positivity regarding rising inflation. This hawkish component had taken the US 10 year yield towards 2.99% but the yield has continued to stay below 3% after that. The yields could start rising again as the June Fed meeting comes closer (where a rate hike is widely expected).

The medium term targets for US yields in our Apr '18 US Treasury report (available on demand) are as follows: 3.2%-3.3% (10 Year), 3.4%-3.5% (30 Year), 3.15% (5 Year) and 2.75% (2 Year). A breach of the 3% level by the 10 year yield would be vital for these targets to be achieved by June. A rate hike is expected in the June Fed meeting, which might start getting factored later this month and could henceforth lead to a rally in yields towards these medium term targets. We also expect some more yield curve flattening in the next month followed by steepening after that, as yields bounce from long term supports.

US 10 Yr Yield (2.95%), 30 Yr (3.12%), 5 Yr (2.79%), 2 Yr (2.49%):

The US 30 year yield (3.12%) could dip more towards support on short term chart near 3.08% before rising again.

The 10 Year yield (2.95%) is near support on the short term chart. We are expecting this support to hold, in which case, it should again start moving up towards 3%. As mentioned above, a rise back above 3% could happen later this month as the June Fed rate hike starts getting factored by traders.

Australia NAB business condition hit record high, but RBA could delay rate hike to 2019

Australia NAB business condition rebounded notably from 15 to 21 in April. That's also a rerecord high since the survey started in March 1997. Business confidence also rebounded from 8 to 10.

Quote from the release by Alan Oster, NAB Group Chief Economist:

- "The record high in the business conditions index in the April Survey simply reinforces what has been evident since the middle of last year, that business activity in Australia is robust."

- "Conditions increased in all industries except for manufacturing and retail and, in trend terms, are strongest in mining.

- "Of some concern is that retail conditions turned negative for the first time this year"

- "On a more positive note, concerns that retail weakness might be spreading to retail & personal services have been alleviated by a significant improvement in conditions in that industry over the last two months, particularly in April."

- "The improvement in the employment index was particularly welcome in the light of the ABS reporting a slowdown in jobs growth in recent months. Historically, the NAB Survey does a good job at looking through short-term cycles in the ABS data and so we think the labour market continues to improve."

- "While forward orders fell, on a trend basis they increased and point to a positive outlook for the non-mining economy, including employment and investment growth."

- "The Survey results for March are consistent with our outlook for the Australian economy. The strength in business conditions and leading indicators suggest economic growth will strengthen and that over-time we should see strong jobs growth and falls in the unemployment rate. Falling unemployment should eventually translate into upwards pressure on private sector wages, at which point the RBA will be in a position to start increasing the current emergency low policy rate. Our current call is for the first move by the RBA to be late this year, but as hard evidence of a firming in wages growth is yet to appear in the data, and unemployment for the moment stuck at around 5.5%, the risk is that any action by the RBA will be delayed into 2019"

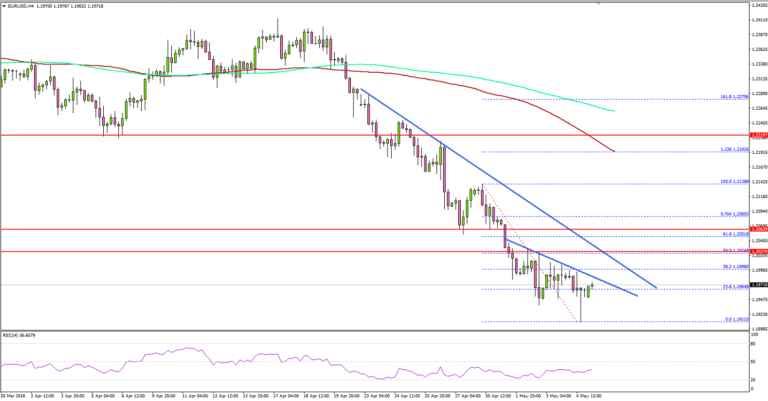

EUR/USD Settled Below Key Support Levels

Key Highlights

- The Euro declined heavily this past week and broke the 1.2000 support against the US Dollar.

- There is a major bearish trend line formed with resistance at 1.2010 on the 4-hour chart of EUR/USD.

- The US nonfarm payrolls in April 2018 came in at 164K, less than the forecast of 192K.

- The US unemployment rate dipped from 4.1% to 3.9%.

EURUSD Technical Analysis

The Euro came under a lot of pressure this past week and declined below the 1.2000 support against the US Dollar. The EUR/USD pair traded as low as 1.1911 before buyers appeared.

Looking at the 4-hours chart, there was a major decline initiated from the 1.2400 area. The pair seems to be under a lot of bearish pressure and it may continue to decline or consolidate losses in the near term.

It recently tested the 23.6% Fib retracement level of the last decline from the 1.2138 high to 1.1911 low. However, there are many hurdles on the upside near the 1.2000-1.2040 zone.

There is also a major bearish trend line formed with resistance at 1.2010 on the same chart. Moreover, the 50% Fib retracement level of the last decline from the 1.2138 high to 1.1911 low is close to the 1.2025 level.

Therefore, the pair will most likely face a strong selling interest near 1.2010 and 1.2025. On the downside, the 1.1920 level is a major support, followed by 1.1850.

This past Friday, the US nonfarm payrolls report for April 2018 was released by the US Department of Labor. The market was looking for a reading of around 190K, compared with the last 103K.

The actual result was on the lower side as the US NFP in April 2018 came in at 164K. However, the last reading was revised up to 135K. More importantly, the US unemployment rate dipped from 4.1% to 3.9%.

The report added:

Among the major worker groups, the unemployment rate for adult women decreased to3.5 percent in April. The jobless rates for adult men (3.7 percent), teenagers (12.9 percent), Whites (3.6 percent), Blacks (6.6 percent), Asians (2.8 percent), and Hispanics (4.8 percent) showed little or no change over the month.

Overall, the US Dollar may perhaps extend gains versus the Euro, British Pound and the Japanese Yen in the near term.

Economic Releases to Watch Today

- German Factory Orders for March 2018 (MoM) – Forecast +0.7%, versus +0.3% previous.

- Swiss CPI for April 2018 (YoY) – Forecast +0.8%, versus +0.8% previous.

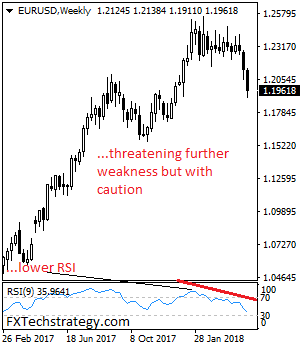

EURUSD – Remains Vulnerable But With Caution

EURUSD - The pair closed lower the past week with more decline envisaged. However, a move higher on correction is envisaged. On the upside, resistance comes in at 1.2000 level with a cut through here opening the door for more upside towards the 1.2050 level. Further up, resistance lies at the 1.2100 level where a break will expose the 1.2150 level. Conversely, support lies at the 1.1900 level where a violation will aim at the 1.1850 level. A break of here will aim at the 1.1800 level. Below here will open the door for more weakness towards the 1.1750. All in all, EURUSD faces further downside threats.

Traders were Bearish on Precious Metals While Stayed Mixed on Energy

Speculators were mixed over the energy complex in the week ended May 1. Net LENGTH for crude oil futures plunged -21 696 contracts from a week ago to 690 727. NET LENGTH of heating oil rose +4 341 contracts to 26 997 while net LENGTH for gasoline dropped -1 940 contracts to 83 027. Net SHORT for natural gas decreased -1 378 contracts to 94 849 for the week.

Speculators were bearish over the precious metal complex last week. Net LENGTH for gold slumped -29 867 contracts to 106 779. Silver reverted to Net SHORT of 7 196 contracts for the week. For PGMs, net LENGTH for platinum slumped -7 068 contracts to 10 764 while that for palladium slipped -196 contracts to 10 765.