Sample Category Title

Currencies: USD Rally Slows As Markets Await US Decision On Iran Deal

Rates: Trump’s verdict on JCPOA throws shadow over trading

Core bonds traded sideways yesterday and that could remain so today. Heavy supply is negative, but could be balanced by uncertainty on the outcome of tonight’s verdict by US President Trump on the Iranian nuclear accord. Rumours suggest he’ll extend the negotiation period, but Trump has proven in the past that nothing can be taken for granted.

Currencies: USD rally slows as markets await US decision on Iran deal

The dollar maintained a cautiously positive momentum yesterday, especially against the euro. Today’s eco calendar is thin. (FX) Markets await the US decision on the Iran deal. Several options are possible, but we assume that the outcome might leave the USD positive momentum intact.

The Sunrise Headlines

- US stock markets gained around 0.35% with Nasdaq outperforming (+1%) led by Apple. Asian stock markets trade positive as well this morning with China profiting (+1%) from strong trade data.

- US President Trump said he would announce today his decision on the landmark Iran nuclear accord that he has repeatedly condemned. Some European officials suggest he would leave more time for negotiations. (WSJ)

- Richmond Fed Barkin, 2018 voter, says US monetary policy is still accommodative and “it is hard to argue that accommodation is appropriate when unemployment is low and inflation is effectively at our target.” (BB)

- The ECB is likely to move over the summer to gradually phase out its bond-buying program, perhaps announcing a decision after its July 26 policy meeting, ECB Smets said. (WSJ)

- China's exports rebounded more strongly than expected in April (12.9% Y/Y), suggesting global demand remains relatively resilient and providing a cushion to the economy amid a heated trade dispute with the US. (Reuters

- Australian retail sales were unchanged and below consensus (0.2% M/M) in March as a rise for food sales was offset by falls in other industries. AUD/USD slid back below the 0.75 mark. (FT)

- Today’s eco calendar contains US NFIB Small Business Optimism and German industrial production data. Fed Powell and ECB Liikanen speak. The Netherlands, Austria, Germany and the US tap the bond market

Currencies: USD Rally Slows As Markets Await US Decision On Iran Deal

USD rally slows as markets await US Iran decision

In line with end last week, some ‘by default USD buying’ continued yesterday. EUR/USD dropped below the 1.1915/35 support and filled bids near 1.19, but there were no sustained follow-through gains. Dollar strength prevailed, but the news flow was also tentatively euro negative (disappointing German factory orders; risk of new elections in Italy). USD/JPY rebounded to the 109.40 area, but eased later in the session. EUR/USD closed the day at 1.1922. USD/JPY finished at 109.09. In the end, there was too little news to inspire a clear direction move.

Overnight, Asian equities mostly show solid gains. Chinese foreign trade data were strong (a big rise both in imports and exports). The politically sensitive surplus with the US also widened sharply. For now, we see little direct impact on FX. Oil stabilizes off recent highs as markets await US president Trump’s decision on the nuclear deal with Iran. The impact from the oil price on the dollar remains modest for now. The Aussie dollar fell back to AUD/USD 0.75 on disappointing Australian retail sales.

Today, the eco calendar again only contains second tier eco data in the US and in Europe. Markets might give some more attention to the German production after recent poor EMU data. More disappointing news might weigh on the euro. Yesterday, Fed comments tilted to the hawkish side, but with no big impact on the dollar. Markets will look forward to decision of President Trump on the nuclear deal with Iran. Several options area open (from the US leaving the deal to some kind of ‘kicking the can down the road’ scenario). The recent rise of the oil price suggests that, at least the oil market already discounts quite a hawkish US approach. We hold the working hypotheses that the US Iran decision won’t derail USD positive momentum. If EUR/USD breaks below 1.19, next high profile support comes in in the low 1.17 area. USD/JPY underperforms USD/EUR and this might continue to be the case.

Yesterday, EUR/GBP declined off Friday’s correction top, mostly on euro weakness. The pair closed the session at 0.8794. Today, the UK eco calendar is also thin. The UK political debate on Brexit continues (Vote in the House of Lords). Markets are also couting down to the BoE policy decision on Thursday. The ‘bad news’ (no rate hike this week) is probably discounted. Even with no rate hike, the BoE might maintain a moderately hawkish tone. If so, it might be a (temporary) supportive for sterling. Combined with euro softness. EUR/GBP might drift a bit further south in the 0.87 big figure going into the BoE policy decission

EUR/USD downside pressure persists

Pound Heavily Underpriced Heading Into BoE Meeting

Apart from the eagerly anticipated announcement from President Trump on whether the United States will pull out of the 2015 Iran nuclear deal, one of the most highly awaited events in the economic calendar this week will be the latest interest rate decision from the Bank of England (BoE). After sinking 5.5% since 17 April and the GBPUSD nosediving from around 1.44 to 1.35 during this period, it does appear that the financial markets are now heavily underpricing the chances of an upbeat BoE statement later in the week.

The major catalyst behind the aggressive Pound selling from investors has been another reversal in stance from BoE Governor Mark Carney when it comes to his views on UK monetary policy. Carney has been known to backtrack on his monetary policy stance more than once in the past, but his latest change in tone has led to the financial markets completely dismissing any chance of a UK interest rate rise this month.

I would be aware that the Pound is looking heavily oversold heading into the BoE meeting, with investors expecting no action from the Monetary Policy Committee (MPC). Headlines from other voters within the MPC that their ambition remains to see higher UK interest rates should provide the Pound with an opportunity for a revival after a crushing couple of weeks.

Emerging markets hoping for reprieve from stronger Dollar

Signals that the stunning turnaround in fortunes for the US Dollar might pause is going to lead to optimism that the recent pain for emerging market currencies will also take a break.

The emerging market currencies have been guilty of playing catch up with the US Dollar’s strength, after the Greenback powered ahead of developed currencies like the Pound, Euro and Yen in recent weeks, with most emerging market currencies broadly lower against the USD over the past couple of days.

Where the Dollar goes from here could depend on how the markets react to President Trump’s announcement on the Iran nuclear deal later today. President Trump has now announced that he will be informing whether the United States will pull out of the 2015 deal today, after it was previously suggested that the deadline to make a decision would be at the end of the week.

If the announcement does lead to a new round of geopolitical risk being priced into the financial markets, there will be concerns over what impact this will have on risk appetite.

There have been persistent fears for a long time that Trump will pull out of the 2015 nuclear deal and confirmation of this will present a threat to global stocks. Emerging market currencies could also feel the pinch from reduced risk appetite, while the Japanese Yen and Gold would likely benefit from market uncertainty.

Euro hits new 2018 low

The EURUSD has resumed its recent downward spiral this week, by falling below 1.19 for the first time since late 2017.

A new round of weak economic data has exposed further fears that the Euro area is at risk of entering another downturn. I personally feel that this view is a little unfair, considering that the Eurozone outperformed all expectations throughout the previous year. The latest EU data will however provide the ECB with more reason to remain hesitant on raising interest rates, meaning that increasing interest rate differentials between the United States and Europe risk exposing the EURUSD further to the downside.

Ringgit weakens ahead of General Election

Ahead of an extremely busy week for the Malaysian calendar, the Ringgit is showing signs of weakness against the USD.

The intense buying momentum in the USD has probably been the main contributor to the Ringgit fluctuations, but the general election this week will still be seen as a potential event risk. If there is unexpected uncertainty with the election in Malaysia, it can’t be ruled out that the Ringgit could find itself at risk of further selling pressure.

Rupiah weakens as Indonesia GDP disappoints

The Indonesian Rupiah tumbled to its lowest levels since December 2015 at 14,000, after GDP growth in Indonesia showed signs of weakness in the first quarter of 2018. The headline GDP miss has been attributed to weak consumption, and the news failed to help the Rupiah pull away from its recent rut that has seen the currency take the position of the second-worst Asian performer over the past three months.

The slower pace of economic growth is going to make it difficult for Bank Indonesia to raise interest rates, despite calls for the central bank to take action in an effort to prevent the local currency from further weakness.

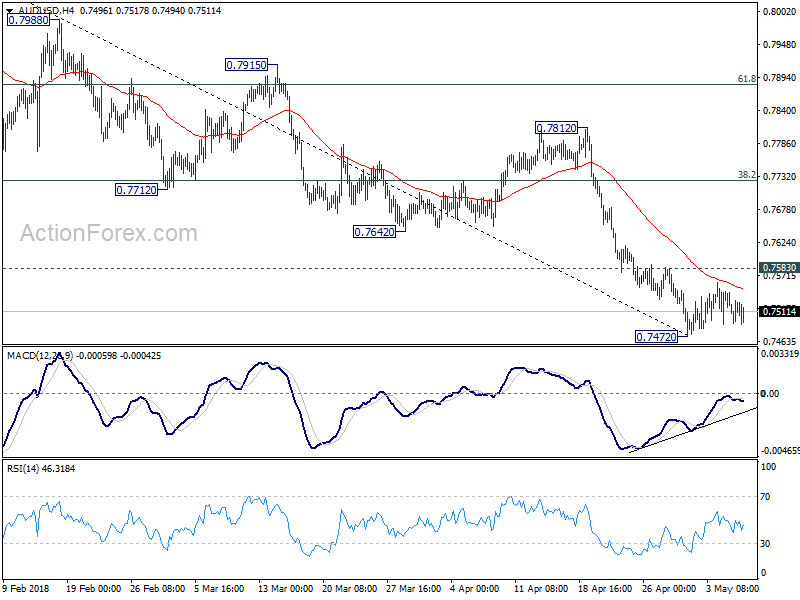

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7492; (P) 0.7517; (R1) 0.7542; More...

AUD/USD is staying in consolidation above 0.7472 temporary low. With 0.7583 minor resistance intact, recent decline should resume sooner rather than later. Below 0.7472 and sustained break of 0.7500 will indicate medium term reversal and target next support at 0.7328. However, break of 0.7583 will indicate short term bottoming, on bullish convergence condition in 4 hour MACD. And stronger rebound could be seen back to 38.2% retracement of 0.8135 to 0.7472 at 0.7725 and possibly above.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Decisive break of 0.7500 key support will suggest that such correction is completed. In that case, deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

China Trade Balance In-Line, Oil Holds Higher Awaiting Iran Outcome

General Trend:

- Asian equity markets trade generally higher, in line with US session

- Australia March and Q1 retail sales miss ests; Australian dollar and 3-year yield decline

- Japan household spending declines for 2nd straight month, leads to questions about whether weakness is temporary

- China April Trade Surplus and Exports beat ests

- China 2018/19 soy imports expected to decline for the first time in over 10 years (CNGOIC)

- US/China trade talks to continue: China's top economic advisor will be in Washington next week

- May 8th deadline for Takeda’s approach for Shire in focus

- US President Trump is expected to make decision on Iran deal later on Tuesday (18:00 GMT); WTI Crude Futures decline in Asia

- Indonesia 2-year bond yields rise over 25ps; tracks recent weakness in Rupiah currency (IDR)

- NZ Shadow Board sees no changes at Thursday’s RBNZ policy meeting

- Australia’s budget due for release later today

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.1%; closed +0.2%

- TOPIX Info & Communications index +0.5%, Electric Appliances +0.2%; Real Estate -0.6%, Retail Trade -0.5%

- Automakers decline ahead of Wednesday’s expected earnings report from Toyota Motors

- (JP) BoJ to explain why it omitted inflation target timing – Japanese Press

- (JP) Japan Govt to set new fiscal reform target that keeps ratio of FY21 deficit to nominal GDP at 3% of below – Japan press

- (JP) Japan Fin Min Aso: No answer on timing of new fiscal reform target yet

- (JP) Japan Mar Household Spending y/y: -0.7% v 1.0%e

- Takeda, 4502.JP Comments on press reports: talks continue with Shire on possible offer, will make announcement if firm offer is made

- (JP) Japan MoF sells ¥2.2T v ¥2.2T indicated in 0.1% (prior 0.1%) 10-yr JGB; avg yield 0.046% v 0.032% prior; bid to cover 4.20x v 4.16x prior

- (CN) China Premier Li: China will grant RQFII quota to Japan; will also sign a currency swap agreement during visit to Japan

Korea

- Kospi opened +0.3%

- (KR) Korea International Trade Association report: South Korea needs more attention to avoid US anti-dumping moves as the bulk of its exports overlaps with already regulated Chinese goods - Korean press

- (KR) Bank of Korea (BoK) sells KRW500B in 6-month monetary stabilization bonds (MSBs); yield 1.72%

- 005380.KR Hyundai/Kia expected to report stronger sales due to recovery in China - Korean press

- (KR) South Korea sells KRW1.70T in 5-year bonds: avg yield 2.59%

- SK Telekom, 017670.KR To pay KRW702B to acquire 55% stake in Siren Holdings which owns 100 percent of ADT Caps; Macquarie Group bought 45% for KRW574B

China/Hong Kong

- Hang Seng opened +0.4%, Shanghai Composite flat

- Hang Seng Info Tech index +2.7%, Financials +1.5%, Consumer Goods +1.4%

- Shanghai Composite Property sub-index rises over 1.5%

- (CN) CHINA APR TRADE BALANCE: $28.8B V $27.8BE; Exports Y/Y: 12.9% v +8.0%e ; Imports Y/Y: 21.5% v 16.0%e

- (CN) CHINA APR TRADE BALANCE (CNY): 182.8B V 189.2BE; Exports Y/Y: 3.7% v +4.0%e ; Imports Y/Y: 11.6% v 10.4%e

- (CN) CHINA APR FOREIGN RESERVES: $3.125T V $3.131TE (2nd monthly decline)

- (CN) China PBoC Open Market Operation (OMO): Skips reverse repo operations for the second consecutive day; Net: CNY0B drain v CNY0B drain prior

- (CN) China PBoC sets yuan reference rate: 6.3674 v 6.3584 prior

- (CN) China may release detailed rules on CDRs in 2-3 months - China Securities Journal

- (CN) China President Xi top economic adviser to visit the US for trade talks

- (CN) PBoC: Reiterates to boost cross-border usage of yuan (CNY); held meeting on yuan cross-border business on May 7th

- (HK) Hong Kong 3-month HKD Hibor continues to trade at highest since 2008; currently near 1.74696%

- (CN) Li Daokui: China unlikely to deprecate yuan for 'trade war'

Australia/New Zealand

- ASX 200 opened +0.1%, closed 0.1%

- ASX 200 Financials index +0.8%, Utilities +0.6%; Energy -1.1%, Resources -0.7%, Telecom -0.5%

- (NZ) New Zealand 9M Budget surplus NZ$910M more than forecasted; Core rev Rev NZ$1.1B more than forecasted

- (NZ) New Zealand Shadow Board: Sees little need for RBNZ to change cash rate

- (AU) Australia sells A$150M v A$150M indicated in 2.50% Sept 2030 indexed bonds, avg yield 0.8357%, bid to cover 3.43x

- (AU) AUSTRALIA MAR RETAIL SALES M/M: 0.0% V 0.2%E

- (AU) AUSTRALIA Q1 RETAIL SALES EX-INFLATION Q/Q: 0.2% V 0.6%E

- (NZ) New Zealand Q2 2-yr Inflation Expectations: 2.01% v 2.11% prior; 1-yr inflation expectations 1.80% v 1.86% prior

Other Asia

- Nanya Technology [2408.TW]: Expects DRAM prices to rise in Q2 - Digitimes

North America

- US equity markets ended higher: Dow +0.4%, S&P500 +0.4%, Nasdaq +0.8%, Russell 2000 +0.9%

- S&P500 Technology +0.7%, Industrials +0.7%, Financials +0.7%

- FOXA Comcast said to be arranging financing with banks for all cash bid for Twenty-First Century Fox - financial press

- QCOM Said to be exploring closing or selling data center business and preparing exit from server chip business - press

- Canadian Natural Resources [CNQ]: Royal Dutch Shell sells 97.6M share stake in Canadian Natural Resources Limited for $3.3B

- (IR) President Trump: I will announce Iran decision tomorrow (Tuesday) at 14:00ET (18:00 GMT)

- (US) Fed's Kaplan (dove, non-voter): base case for 2018 is still three hikes total; 2% is a symmetrical inflation target - Q&A with reporters

- (US) Fed's Barkin (FOMC voter): economic growth is being propelled by unbelievably positive consumer and business confidence

- (US) Senior Trump Administration Official: President Trump to request $15B in spending cuts from Congress

- (US) NY Attorney General Schneiderman to resign amid allegations by multiple women

Europe

- (UK) PM May said to have delayed Cabinet discussion on customs plan - UK press

- (EU) ECB's Praet (Belgium, chief economist): euro area data points to some moderation but remains consistent with a broad-based and solid expansion

- (EU) ECB's Smets (Belgium): recent economic data is consistent with continued robust expansion; ECB may have better understanding of data at June or July meetings; Investors could be correct to push out their forecasts for when ECB might increase rates

- (GR) ESM chief Regling: Greek loan maturities could be extended

- (IT) Italy President Mattarella: confirms there is no possibility of forming a political govt; urges parties to support a "neutral" non-partisan govt

- Virgin Money VM.UK CYBG confirms preliminary approach to acquire Virgin Money; for exchange ratio of 1.1297 new CYBG shares for each Virgin Money share

- Shire [SHP.UK]: Takeda comments on press reports: talks continue with Shire on possible offer, will make announcement if firm offer is made

- Hochtief [HOT.DE]: Reports Q1 op net €106.3M v €93.3M y/y, Rev €5.27B v €5.15B y/y; Affirms FY18 Op €470-520M (prior €470-520M y/y)

- Unicredit [UCG.IT]: Hedge fund Caius Capital alleges that the company misclassified certain capital - FT

Levels as of 02:00ET

- Hang Seng +1.2%; Shanghai Composite +0.7%; Kospi -0.3%

- Equity Futures: S&P500 -0.0%; Nasdaq100 +0.1%, Dax +0.1%; FTSE100 -0.2%

- EUR 1.1938-1.1909; JPY 109.14-108.85; AUD 0.7528-0.7491;NZD 0.7028-0.7009

- Jun Gold -0.1% at $1,312/oz; Jun Crude Oil -1.1% at $69.94/brl; Jul Copper +0.4% at $3.09/lb

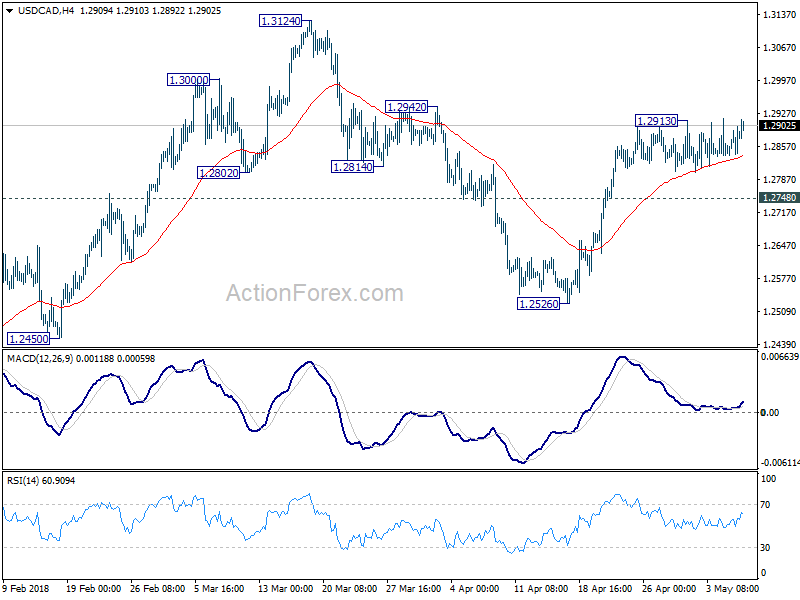

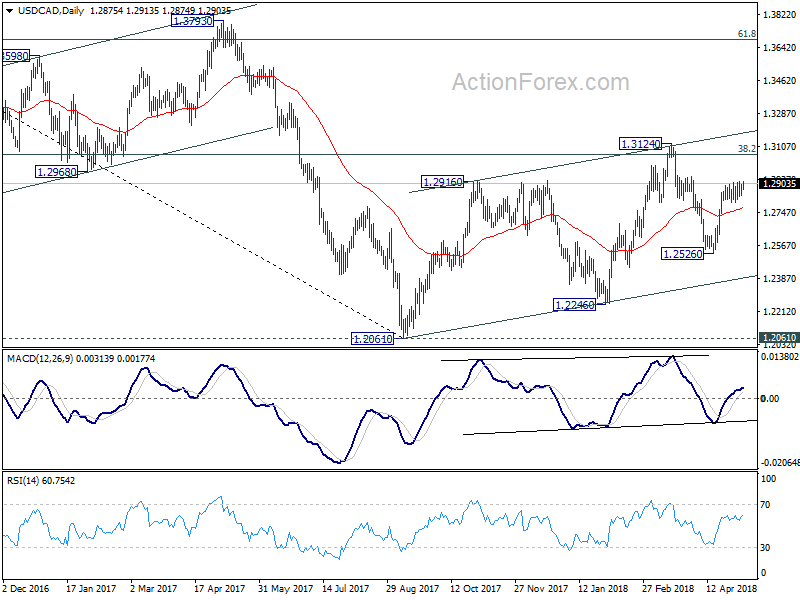

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2847; (P) 1.2872; (R1) 1.2907; More....

USD/CAD is still bounded in range below 1.2913 temporary top and intraday bias stays neutral. As long as 1.2748 minor support holds, further rise is expected. Break of 1.2913 will target a test on 1.3124 high next. Though, break of 1.2748 will turn focus back to 1.2526 support instead.

In the bigger picture, current development suggests that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685.

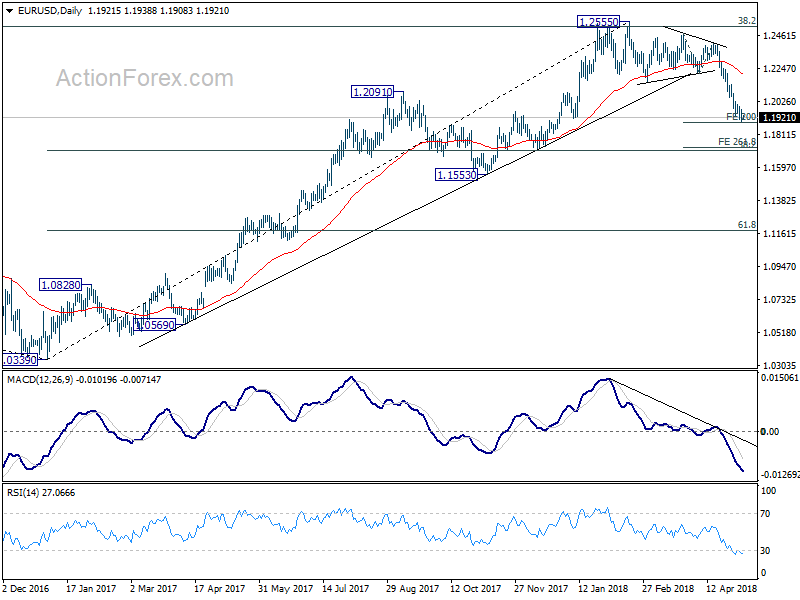

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1887; (P) 1.1933 (R1) 1.1968; More....

Downside momentum in EUR/USD remains unconvincing as seen in 4 hour MACD. But with 1.1977 minor resistance intact, intraday bias remains on the downside. Break of 200% projection of 1.2475 to 1.2214 from 1.2413 at 1.1891 will target 261.8% projection at 1.1730. Though, break of 1.1977 will suggest short term bottoming. In that case, intraday bias will be turned to the upside for 4 hour 55 EMA (now at 1.2036) or above for rebound.

In the bigger picture, current decline and firm break of 1.2154 support confirms rejection by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. A medium term top should be in place at 1.2555 and deeper decline would be seen back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. With current downside acceleration, there is prospect of hitting 61.8% retracement at 1.1186 before completing the decline. But still, we'll need to look at the structure to before deciding if it's a corrective or impulsive move.

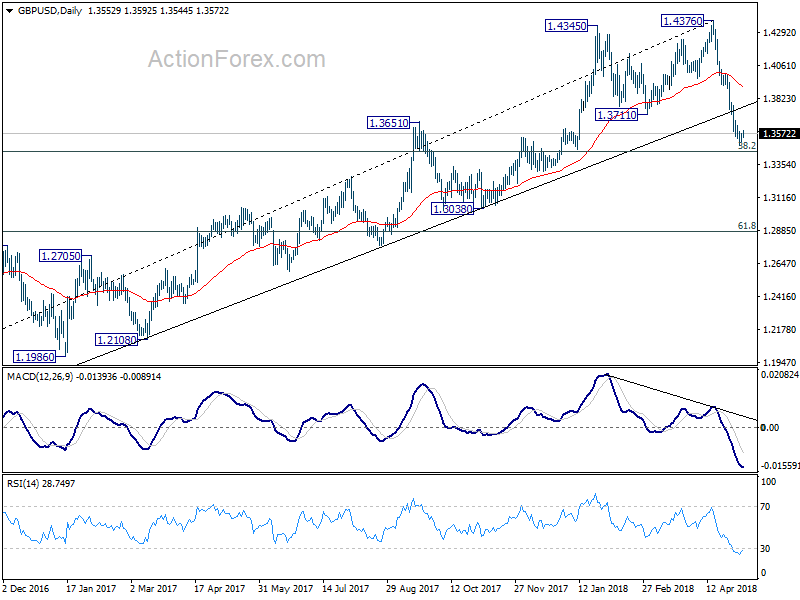

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3522; (P) 1.3548; (R1) 1.3582; More...

A temporary low is in place at 1.3485 in GBP/USD and intraday bias is turned neutral for consolidation. Stronger recovery could be seen back to 4 hour 55 EMA (now at 1.3679) and above. But upside should be limited by 38.2% retracement of 1.4376 to 1.3485 at 1.3825 to bring another decline. Break of 1.3485 will resume the fall from 1.4376 to 1.3448 fibonacci level next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). Deeper decline should be seen to 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 first. Break will target 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3925) holds, even in case of strong rebound.

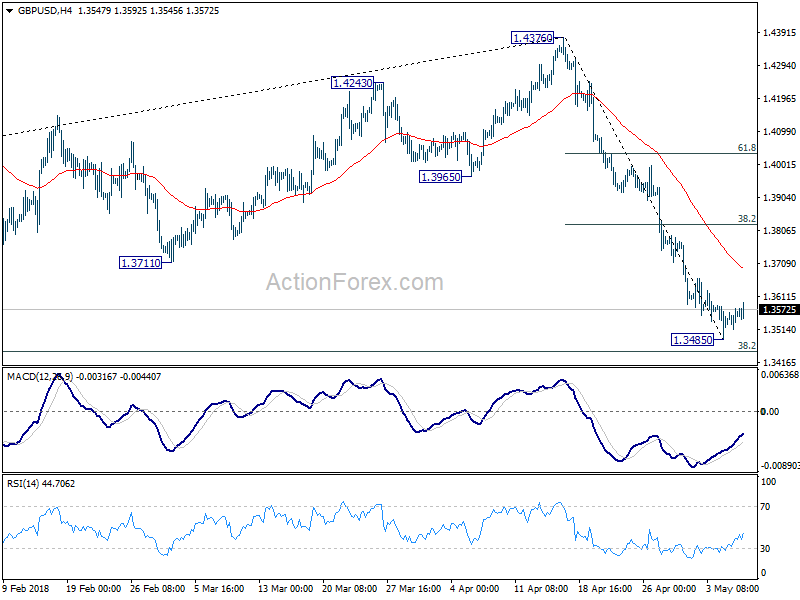

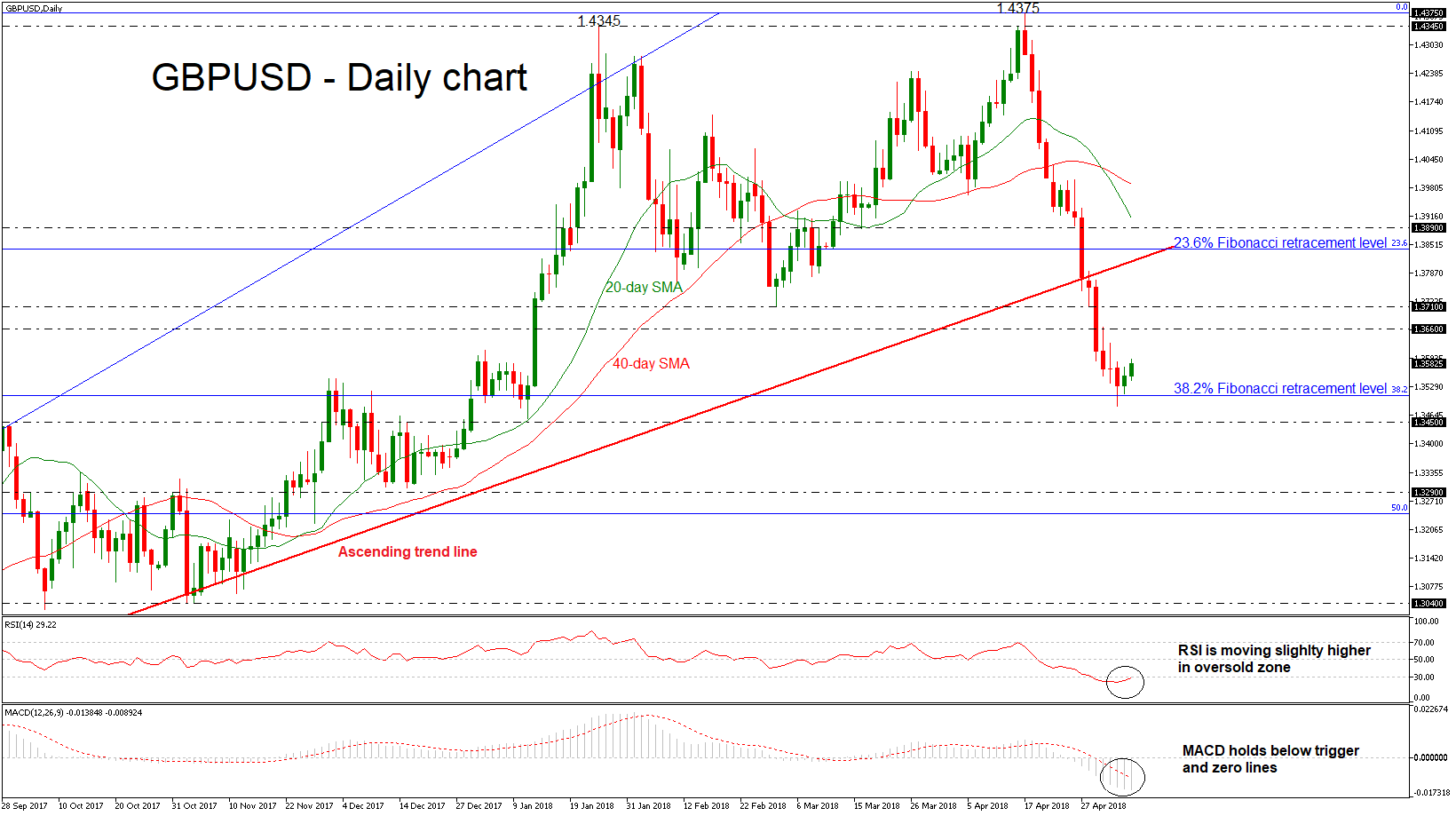

GBPUSD Sell-Off Eases Slightly After Finding Support At 4-Month Low Of 1.3485

GBPUSD has headed sharply lower over the last three weeks after the strong bounce off the 1.4375 resistance level. The pair challenged a fresh almost four-month low of 1.3485 achieved last Friday near the 38.2% Fibonacci retracement level of the upleg from 1.2100 to 1.4375. The pair failed to end a day below the aforementioned obstacle and is paring some of the losses.

From the technical point of view, in the daily timeframe, the Relative Strength Index (RSI) is slightly pointing to the upside but remains in the oversold zone, while the MACD oscillator is losing bearish momentum in the negative territory, indicating that a bullish correction is possible. Additionally, the 20- and 40-simple moving average (SMAs) posted a bearish crossover the preceding week, confirming the bearish pressure.

If price action remains above the 38.2% Fibonacci of 1.3510, there is scope to test the 1.3660 – 1.3710 resistance area. Clearing this key zone would see additional gains towards the 23.6% Fibonacci mark of 1.3840. Rising above it would see prices re-test the 1.3890 barrier.

If 1.3510 support fails, then the focus would turn to the downside again towards the next immediate support of 1.3450. Breaching this region would increase downside risks and bring about a deeper reversal of the medium-term outlook and touching the 1.3290 support hurdle.

Overall, GBPUSD has been negative after the penetration of the ascending trend line, which had been holding since March 2017.

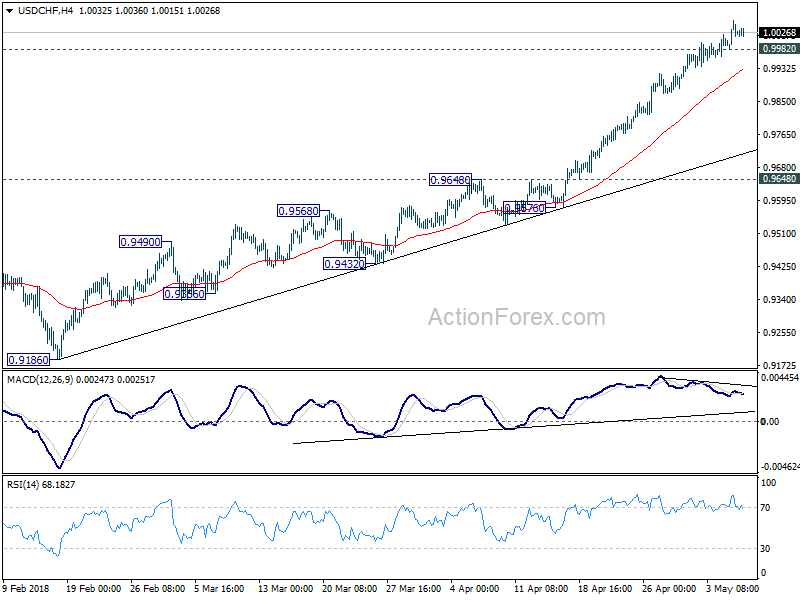

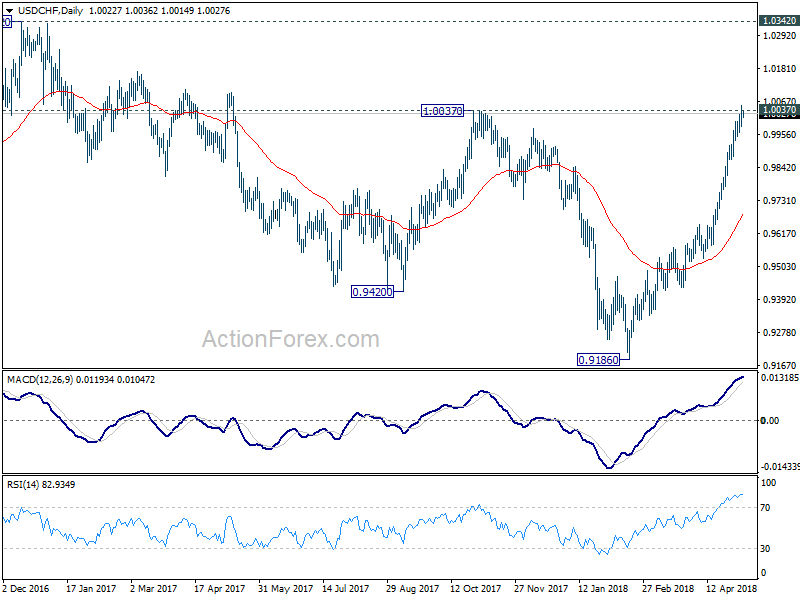

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9987; (P) 1.0022; (R1) 1.0060; More...

Upside momentum remains unconvincing in USD/CHF. But with 0.9982 minor support intact, intraday bias remains on the upside. Sustained trading above 1.0037 will pave the way to 1.0342 key resistance next. On the downside, though, below 0.9982 minor support will indicate short term topping. And, in that case, deeper retreat could be seen to 4 hour 55 EMA (now at 0.9932) and below before staging another rise.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 0.9648 resistance turned support holds, even in case of pull back.

Short-Term Sterling Buying Gaining Momentum

The British pound has started to move higher against the U.S dollar after finding dip-buying from the 1.3514 level, creating a bullish double-bottom pattern above the former weekly trading-low. The GBPUSD pair currently trades around the 1.3550 level, with short-term upside momentum intact while price trades above the key 1.3514 level. Sterling traders may remain cautious over the coming day’s, ahead of Thursday’s key Bank of England interest rate decision.

The GBPUSD pair is intraday bullish while trading above the 1.3514 level, further upside towards 1.3585 and 1.3610 levels seems possible.

If the GBPUSD pair falls below the 1.3514 level, traders will likely test towards the 1.3500 and 1.3485 support levels.