Sample Category Title

Japan, South Korea and China in first trilateral talk since 2015

Japanese Prime Minister Shinzo Abe, South Korean President Moon Jae-in and Chinese Premier Li Keqiang are meeting in Tokyo today for the first trilateral summit since 2015. As the host of the meeting, Abe said that "for our three nations, building future-oriented cooperative relations is extremely important for the region as a whole." And he urged the three nations to "stay in close touch with international society and demand that North Korea take concrete moves" on denuclearization.

China's Li expressed the willingness to "work with Japan and South Korea to jointly maintain regional stability and push forward the development of the three countries." Separately, China is set to sign a currency swap agreement with Japan, and grant the country a quota of Renminbi Qualified Foreign Institutional Investors (RQFII) for investments.

WTI oil above 70, 10 year yield at 2.99, JPY weakens after Trump’s Iran deal withdrawal

Reactions to Trump's pull out of the Iran deal were rather muted. DOW ended up 0.01% at 24360, S&P 500 down -0.03%, NASDAQ up 0.02%. WTI crude oil reversed initial loss and is back above 70.5. 10 year jumped together with oil and is back at 2.99. Yen is thus, under some pressure and trades broadly lower in Asian session.

Elsewhere in the currency markets, Canadian Dollar recovers broadly, follow oil price. Dollar is supported by rebound in yields while NZD is trading higher ahead of tomorrow's RBNZ rate decision.

Market Morning Briefing: Trump’s Withdrawal From The Iran Deal

STOCKS

Dow (24360.21, +0.012%) is almost stable and is trading just below immediate trend resistance near 24500. While that holds, the index could again come off towards 23750-23500. A break above 24500 is needed to indicate some bullishness in the medium term.

Dax (12912.21, -0.28%) looks bullish and could target 13200-13400 in the medium term. Near term trend is up.

Nikkei (22400.50, -0.48%) is stuck at same levels for the last 4-5 sessions unable to decide which direction to move. Immediate resistance near 22600 continues to hold for now. It would be important to watch price action at current levels. A rejection would take it down to 22000 and lower while a break above 22600, if seen could turn bullish for the medium term.

Shanghai (3154.06, -0.24%) has moved up and may attempt to test 3200 in the near term. While above 3150, near term trend is up.

Nifty (10717.80, +0.021%) is trading below 10800. It would be important to see if the index is able to break above 10800 in the coming sessions. A rejection from 10800 could drag the index down to 10600-10500 levels again but a break above 10800, if seen would be bullish for the coming weeks.

COMMODITIES

Trump announced the withdrawal of the US-Iran 2015 nuclear deal. The Crude prices started to move up after the much awaited Iran decision. Brent (76.69) is trading higher after testing intra-day lows of 73.10 yesterday. Similarly Nymex WTI (70.63) is up from 67.64. While the rising momentum is strong Brent could head towards 78 in the near term while WTI could head towards 71-72 levels. Note there are immediate resistances just above current levels and we could soon see some dip by the early next week.

Gold (1310.81) is down to 1310. Lack of bull strength is visible just now and the price could eventually move down to test 1300 or even 1280 in the near to medium term.

Copper (3.056) could come down to test 3.0 in the next couple of sessions. Near term looks bearish.

FOREX

Dollar index (93.18), against our expectation, didn't see a dip towards 92.4-92.5 yesterday; instead it rose to a high near 93.28 and is currently trading near 93.2. Looking at the 1 hour chart, the Dollar Index could be in the last leg of its 5 wave upmove from 89.23 (17th Apr onwards). This last leg could possibly end near 93.70-94.50. Our projection of the Dollar Index coming close to its medium term target of 94-95 in the next 1-2 weeks might well come out to be true. (the level 94-95 corresponds to the 5th wave starting point of the downmove since Dec '16).

Euro (1.1852), against our expectation, did not rise towards 1.1950-1.1975 yesterday; instead it saw a low of 1.1838 and is currently trading near 1.185. Corresponding to the Dollar Index's upmove towards 93.70-94.50, the Euro could have its current downmove restricted till 1.1775-1.1655, after which it could again start rising. If the Dollar Index tests 95, Euro could simultaneously test 1.160-1.158.

Dollar Yen (109.54), in line with our expectation, has risen after testing support on the upward trendline on daily candles near 108.76. This current upmove could now take it higher towards 110.0-110.5-110.75 in the near term. The broader uptrend looks capped till 110.50-110.75 in the medium term, after which Dollar Yen could turn bearish.

Euro Yen (129.83) tested support (on weekly candles) near 129.3 (earlier mentioned as 129.75) yesterday. It could respect this support for a few days, but is then likely to break it when the Dollar Yen turns bearish after testing 110.00-110.75 and the Euro continues its downmove till 1.16.

Pound (1.3534): As we had predicted, Pound did rise to 1.359 yesterday but has again dipped after that. If it again rises above 1.354-1.355, it might possibly see some further near term upmove till 1.36 (even 1.37). However, if it moves down to 1.35, the current downmove might well extend till 1.325.

Dollar Rupee (67.0825): Immediate Support at 67.00. May see test of 67.30-35. Medium term Support at 66.80-50.

INTEREST RATES

Trump's withdrawal from the Iran deal could possibly take crude prices higher in the near term. This in turn could lead to a rally in yields as well (the 10 Year has already risen from 2.95% to 2.99%). This development is yet another reason why bearishness in global bonds is likely to continue this year. The Fed last week had also expressed some hawkishness in its stance. In the near term, we are expecting US yields to start rising towards their medium term targets (see below) as the June Fed meeting comes closer (where a rate hike is widely expected).

The medium term targets for US yields in our Apr '18 US Treasury report (available on demand) are as follows: 3.2%-3.3% (10 Year), 3.4%-3.5% (30 Year), 3.15% (5 Year) and 2.75% (2 Year). A breach of the 3% level by the 10 year yield would be vital for these targets to be achieved by June. A rate hike is expected in the June Fed meeting, which might start getting factored later this month and could henceforth lead to a rally in yields towards these medium term targets. We also expect some more yield curve flattening in the next month followed by steepening after that, as yields bounce from long term supports.

US 10 Yr Yield (2.99%), 30 Yr (3.14%), 5 Yr (2.82%), 2 Yr (2.52%):

The US 30 year yield (3.14%) didn't dip towards support on short term chart near 3.08% but has risen and could now move up towards its important resistance level of 3.2% .

The 2 year yield didn't dip to 2.45% as we had been expecting and has continued to rise above 2.5% to 2.52%. Our medium target of 2.75% could be tested later this month or in min June.

UK, Germany and France urged US not to obstruct JCPoA Iran deal implementation

Below is the full joint statement of the UK, Germany and France.

Joint statement from Prime Minister Theresa May, Chancellor Angela Merkel and President Emmanuel Macron following President Trump’s statement on Iran.

It is with regret and concern that we, the Leaders of France, Germany and the United Kingdom take note of President Trump’s decision to withdraw the United States of America from the Joint Comprehensive Plan of Action.

Together, we emphasise our continuing commitment to the JCPoA. This agreement remains important for our shared security. We recall that the JCPoA was unanimously endorsed by the UN Security Council in resolution 2231. This resolution remains the binding international legal framework for the resolution of the dispute about the Iranian nuclear programme. We urge all sides to remain committed to its full implementation and to act in a spirit of responsibility.

According to the IAEA, Iran continues to abide by the restrictions set out by the JCPoA, in line with its obligations under the Treaty on the Non-Proliferation of Nuclear Weapons. The world is a safer place as a result. Therefore we, the E3, will remain parties to the JCPoA. Our governments remain committed to ensuring the agreement is upheld, and will work with all the remaining parties to the deal to ensure this remains the case including through ensuring the continuing economic benefits to the Iranian people that are linked to the agreement.

We urge the US to ensure that the structures of the JCPoA can remain intact, and to avoid taking action which obstructs its full implementation by all other parties to the deal. After engaging with the US Administration in a thorough manner over the past months, we call on the US to do everything possible to preserve the gains for nuclear non-proliferation brought about by the JCPoA, by allowing for a continued enforcement of its main elements.

We encourage Iran to show restraint in response to the decision by the US; Iran must continue to meet its own obligations under the deal, cooperating fully and in a timely manner with IAEA inspection requirements. The IAEA must be able to continue to carry out its long-term verification and monitoring programme without restriction or hindrance. In turn, Iran should continue to receive the sanctions relief it is entitled to whilst it remains in compliance with the terms of the deal.

There must be no doubt: Iran’s nuclear program must always remain peaceful and civilian. While taking the JCPOA as a base, we also agree that other major issues of concern need to be addressed. A long-term framework for Iran’s nuclear programme after some of the provisions of the JCPOA expire, after 2025, will have to be defined. Because our commitment to the security of our allies and partners in the region is unwavering, we must also address in a meaningful way shared concerns about Iran’s ballistic missile programme and its destabilising regional activities, especially in Syria, Iraq and Yemen. We have already started constructive and mutually beneficial discussions on these issues, and the E3 is committed to continuing them with key partners and concerned states across the region.

We and our Foreign Ministers will reach out to all parties to the JCPoA to seek a positive way forward.

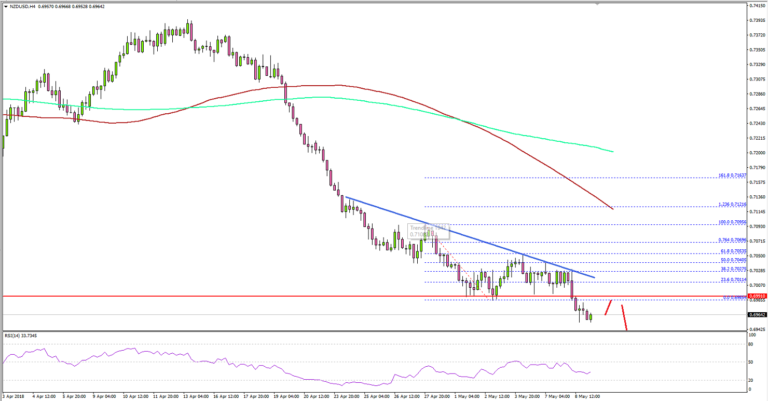

NZD/USD Accelerating Declines Below 0.7000

Key Highlights

- The New Zealand Dollar declined sharply and moved below the 0.7000 support against the US Dollar.

- There is a major bearish trend line forming with resistance at 0.7020 on the 4-hour chart of NZD/USD.

- The pair may decline further towards the 0.6900 support in the near term.

- Today, the US Producer Price Index for April 2018 will be released, which is forecasted to increase by 0.2% (MoM).

NZDUSD Technical Analysis

The New Zealand Dollar remained in a major downtrend and broke the 0.7000 support against the US Dollar. The NZD/USD pair could accelerate declines as long as it is below 0.7020.

Looking at the 4-hours chart, the pair faced a lot of selling interest from the 0.7050 swing high. It declined sharply and settled below a major support at 0.7000-0.6990. Before collapsing below 0.6990, there was an upside correction towards 0.7040.

However, the upside move was capped by the 50% Fib retracement level of the last drop from the 0.7095 high to 0.6985 low. Moreover, there is a major bearish trend line forming with resistance at 0.7020 on the 4-hour chart of NZD/USD.

The pair is currently struggling to recover and is trading well below the 100 (red) and 200 (green) simple moving averages. If the current trend remains intact, the pair could test the 0.6900 level in the near term.

On the upside, resistances are seen at 0.6990, 0.7000 and 0.7020. Only a close above 0.7020 and the highlighted bearish trend line could start a substantial recovery.

Looking at the other major pairs such as EUR/USD and GBP/USD, there was a lot of bearish pressure as both pairs declined heavily. On the other hand, it seems like USD/JPY may extend gains towards the 110.00 level in the near term.

Economic Releases to Watch Today

- US Wholesale Inventories for March 2018 – Forecast +0.5%, versus +0.5% previous.

- US Producer Price Index April 2018 (MoM) – Forecast +0.2%, versus +0.3% previous.

- US Producer Price Index April 2018 (YoY) – Forecast +2.8%, versus +3.0% previous.

- US Producer Price Index Ex Food and Energy April 2018 (MoM) – Forecast +0.2%, versus +0.3% previous.

- US Producer Price Index Ex Food and Energy April 2018 (YoY) – Forecast +2.4%, versus +2.7% previous.

Trump Quits Iran Deal

Donald Trump fulfilled a campaign promise by announcing the US departure from the Iran nuclear deal in a move thatwas largely expected but still sent oil traders for a ride. The Swiss franc was the top performer while the commodity currencies lagged. The latest Premium Video signals which trades Ashraf will be taking, featuring the 6-week curse trade.

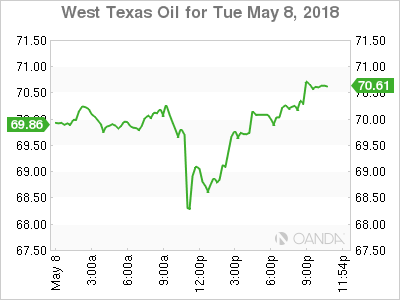

After weeks of speculation and international lobbying, Trump opted to quit the Iran deal, formally known as JCPOA. Throughout the day Tuesday, rumors and denials bounced WTI crude oil prices around. From as high as $70.40 to as low as $67.63 before ultimately finishing close to unchanged and near $70. Monday's high of $70.76 will be a key level to watch in the days ahead.

Other markets also fluctuated out of genuine fear or elation. One reason for the largely-muted market reaction suggested there is still room for negotiation. The sanctions have mandatory 90-day and 180-day notice periods to give companies a chance to tidy up so nothing has been imposed yet. In his announcement, Trump invited Iran back to the negotiating table at any future point.

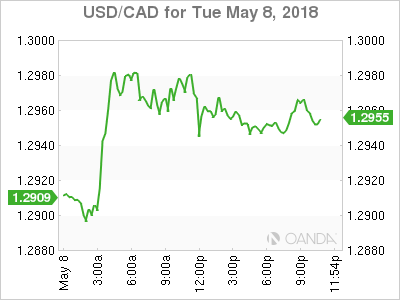

Another interesting move was in USD/CAD as the pair rallied to 1.2998 as oil dropped to the lows of the day. The inability to break above followed by a slide down to 1.2948 suggests firm resistance ahead of the big figure.

More Volatility On The Way!!

More Volatility on the Way!!

The US administration Iran deal exit announcement rolled out in typical President Trump spectacular fashion, but at the end of the day, the market's response was somewhat unenthusiastic with few substantive changes in Gold, Yields or equities.

But that belies the squally interlay moves on WTI which had been down as much as 4.4% earlier amid nervousness ahead of the official announcement.

Currency Markets

In FX, positioning unwinds on the EUR has allowed for more sizable USD gains which have particularly intensified in the EM space. While the weaker links in the chain, Turkey and Argentina have been under the gun all week. The market is growing deeply concerned about the immediate USD liquidity crunches are raising obvious concerns that once the US recommences with interest normalisation and importantly, starts moving forward with the first experimental phase of QE reduction, EM will be in for some significant pain.

Fed Chair Powell's earlier speech in London may have a lot to do with the pain in EM. Specifically, the Fed Chair's comments on EM being able to navigate US policy exit were very notable implying that its Fed policy first and the rest of the world second. Get ready for higher US rates and the long-awaited draining of the QE punch bowl.

This year EM has been able to weather higher US Yields and wobbly equity markets, but it appears that this recent bout of EUR weakness vis a via the USD dollar seems to be the driving factor behind the recent capitulation. If this holds true, it's probably best to wait for the EUR to bottom before reengaging Asia EMfx exposures. At this stage, the USD dollar doesn't appear to be running out of charge anytime soon.

Equity Markets

Given the singular market focus on the US Iran waiver, US equity market, for the most part, parroted movements on oil prices but ended up finish flat on the day.

But indeed, some attention should be given to global FX markets that are reeling at the prospects of a stronger USD dollar and higher US rates which could accelerate the pace of capital outflow from Asian markets.

Oil Markets

Oil markets had an extremely volatile session, and predictably volumes soared causing clearing delays. So, what's next? More volatility of course !!

Given the unilateral move by the US, much of the movement on oil prices had been factored in. But now we are back to the delicate supply balance narrative which is part and parcel of OPEC/NON-OPEC accord, robust global demand dynamics and Venezuelan adversity as its reasonably safe to say that the supply cushion is deflated. Suggesting that even without Iran sanctions Oil prices will remain firm. While Venezuela will arguably be the most prominent tailwind for oil prices over the near term, there is growing OPEC friction bubbling. Saudi Arabia, which wants oil prices even higher, and Iran, which says a reasonable oil price is between US$60-65 a barrel which will make for some exciting headlines as we near the cartel meeting on June 22. And of course, state-owned oil companies in Russia will be asked to turn back the clock as they want to boost production at these current levels.

Gold

Gold prices received a fillip for the unilateral Iran sanctions as the markets worst fears, of course, will be Iran reaction which has promised to be vigorous. But with Treasury Secretary Mnuchin leaving the door ajar to further discussions, gains could be initially capped given the focus could shift back the strong USD, which is showing little signs of running out of charge.

EMFX Asia

The local whipping boy these days is the IDR, and you need to look no further than yesterday local bond auction for guidance with a dreadful bid to cover ratio with foreign accounts side-lined while others continue to look for the exits.

MYR sees presidential elections Wednesday. BN is broadly expected to win, although there is some uncertainty over the margin of victory and therein lies the risk.

USD/CAD Canadian Dollar Lower Despite Oil Rise After US Pulls Out of Iran Deal

The Canadian dollar was lower on Tuesday after the US currency rose on the back of the uncertainty surrounding the United States participation in the Iran deal. The greenback rose as investors looked to the currency as a safe haven. US President Donald Trump announced that the US would be pulling out of the 2015 nuclear agreement and would reimpose economic sanctions on Iranian exports. The move was not unexpected as the Trump administration had criticized the deal but allies were hoping the US would remain, as it stands there are still 5 nations who are backing the deal. The United Kingdom, France, China , Russia and Germany remained committed to the deal where Iran will receive no sanctions as long as it complies with stopping its uranium enrichment program.

- US pulling out of deal a blow to allies and increases Middle East tensions

- Oil price uncertainty higher as geopolitics a main driver

- Iran is the Organization of the Petroleum Exporting Countries (OPEC) 2nd largest producer

Loonie Falters as End of Iran Deal Could Influence NAFTA

The USD/CAD gained 0.56 percent on Tuesday. The currency pair is trading at 1.2953 after the US pulled out of the Iran nuclear deal. The loonie fell to a seven week low. The Canadian currency is heavily correlated with oil prices, but in this instance the announcement from President Trump triggered a flight to safety favouring the USD. Contradictory reports ahead of the final decision sparked volatility in the market. CNN published a piece that gave hope the US would remain in the Iran deal. A New York Times report had a source say that Trump had already told French President Emmanuel Macron that he would exit the agreement. The French president denied those details but eventually that was exactly what came to pass. European leaders were in talks with Iranian leaders and issued a statement where they condemned the decision by the US president.

The price of oil rose, but given the geopolitics it was the US dollar that appreciated against the CAD. Taking into consideration another agreement, NAFTA is still under renegotiation and the manner in which Trump ended the Iran nuclear deal there is some pessimism about the trade deal. Canadian, Mexican and US officials have been in meetings this week trying to bring the deal to a successful conclusion after months of slow moving negotiations. Shale provided the edge needed for the US to move to the top of the energy production chain and given that other major producers agreed to limit their output this is not something that will change in the short term.

Oil Rises After US Ends Iran Deal Participation

West Texas Intermediate is trading at $69.71 after the US pulled out of the Iran deal. The landmark nuclear deal that lifted economic sanctions against Iran in exchange for reducing the enrichment of uranium in 2015 will continue with the other 5 signatories but prices are rising as the Organization of the Petroleum Exporting Countries (OPEC) second largest producer could face heavy sanctions from the US. The fact that the European leaders assured Iran of their commitment to the deal should limit the impact on oil supply but as more details emerge on US sanctions energy prices will react accordingly.

The announcement today from President Trump kicks off a 180 day grace period so that American companies can wind down any oil related activities. The sanctions from 2015 will be reapplied with the main target being Iranian oil exports and the US has already warned purchasers that reducing their consumption volume is advised to avoid secondary sanctions.

Oil prices had attained stability after the Organization of the Petroleum Exporting Countries (OPEC) and other major producers agreed to limit production last year. Geopolitical events, specially those that directly impacted oil supplies had slowly pushed prices higher. The uncertainty about the Iran deal put crude prices at levels not seen since November 2014.

Weekly US crude inventories will be released tomorrow at 10:30 am EDT with a drawdown expected after a huge buildup last week. Energy prices have been stable as the OPEC and allies have cut down supply, but the US has not ramped up supply as first thought. While the speed of the move has not been as forecasted the direction of the trend continues to be up. Drilling has quietly been increased as current prices make shale operations profitable.

Market events to watch this week:

Wednesday, May 9

8:30am USD PPI m/m

10:30am USD Crude Oil Inventories

5:00pm NZD Official Cash Rate

5:00pm NZD RBNZ Monetary Policy Statement

6:00pm NZD RBNZ Press Conference

9:10pm NZD RBNZ Gov Orr Speaks

Thursday, May 10

4:30am GBP Manufacturing Production m/m

7:00am GBP BOE Inflation Report

7:00am GBP MPC Official Bank Rate Votes

7:00am GBP Monetary Policy Summary

7:00am GBP Official Bank Rate

8:30am USD CPI m/m

Friday, May 11

8:30am CAD Employment Change

9:15am EUR ECB President Draghi Speaks

Eco Data 5/9/18

[php_everywhere instance="1"]

Muted reaction to Trump’s withdrawal from Iran deal. USD, CHF, JPY stay in pole position

Trump announced to withdraw from the Iran deal. Market reactions are relative limited as it seems like it's all expected. DOW turns from initial loss to slight gain. But technically, it still has to overcome 55 day EMA (now sitting at 24442). The currency markets are also relatively steady. Dollar, Swiss and Yen are staying in pole positions.