Sample Category Title

EURUSD Intraday Analysis

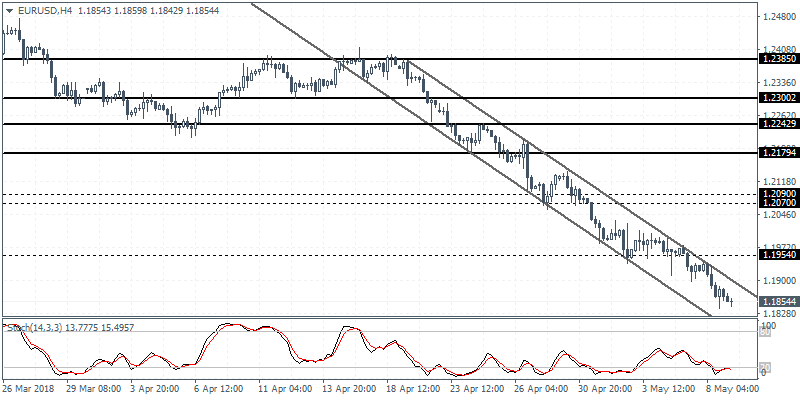

EURUSD (1.1854): The EURUSD extended declines as price action closed below the support level of 1.1920. The declines below this level indicate further losses that could send the EURUSD lower toward the next main support level at 1.1730. Any rebound in prices are likely to be limited to the previous local highs although the main resistance level at 1.1954 will be a key level that could be tested in the near term. As long as the EURUSD remains below 1.1954, we expect to see the downside momentum prevailing.

Trump Withdraws From Iran Deal, RBNZ Meeting In Focus

The newswires were dominated by Trump's decision on Iran nuclear deal which saw oil prices turning volatile on the day. The Trump administration announced that they would be pulling out the Iran nuclear deal. Oil prices reacted little to the news with price already pushing higher in anticipation of the outcome.

On the economic front, retail sales report from Australia showed a flat print and missed estimates of a 0.2% increase. Data from the Eurozone showed a modest improvement in German industrial orders which increased 1.0% compared to estimates of 0.8%. The German trade balance figures are ticked higher to 22 billion compared to estimates of 19.9 billion.

Looking ahead, the U.S. Producer prices index report will be coming out. Economists' polled expect headline PPI to rise 0.2% on the month, a slower pace compared to 0.3% increase previously. Core PPI is also forecast to rise 0.2% on the month.

Later in the day, the RBNZ monetary policy meeting will be a key event to watch for. However, no change to monetary policy is expected at today's meeting.

Markets Tremble As Trump Deserts Iran Nuclear Deal

In a move that dealt a painful blow to global sentiment, President Donald Trump declared on Tuesday that the United States will be pulling out of the 'defective' Iran nuclear deal.

U.S stocks ended mixed on the news while oil prices fluctuated in each direction, as investors considered the potential negative ramifications of Trump’sdecision. The U.S President adopted a very aggressive rhetoric during the announcement and failed to hold back from his view that the 2015 agreement was 'defective' at its core.

While it was widely anticipated that Trump would pull out of the Iran agreement, what is likely to leave a lasting impact on the markets is the threat that he would also penalize those who help Iran. These overall risks are encouraging traders to price in some new geopolitical risk premium, and his threat can potentially be seen as a blow for U.S allies. There is a threat of Trump’s stark tone questioning U.S relations with its European allies, especially given that the likes of France and the United Kingdom had appealed for Trump not to withdraw.

It should also be noted that both China and Russia are also part of the 2015 Iran nuclear agreement. Relations between Trump and both these nations have been questionable in recent weeks. What this all likely means to the financial markets is that anxiety could be heightened over a new round of geopolitical tensions. This will not have been helped by Iran immediately stating that it was preparing to restart uranium enrichment, which is key for making nuclear weapons.

The prospect of heightened geopolitical tensions in the Middle East following Trump’s departure from the nuclear deal is seen as encouragement for risk aversion. A risk-off environment is likely to attract the flight to safety mindset from traders, where both Gold and the Japanese Yen would be seen as potential beneficiaries.

Dollar jumps to fresh 2018 highs

It is shaping up to be another heavily bullish week for the Dollar, which has sprinted above 93.25, its highest level this year against a basket of major currencies.

Thanks to a hawkish Federal Reserve, interest rate differentials are moving in favour of the Dollar. Price action suggests that bulls are back in town, with further upside on the cards amid growing expectations of higher U.S interest rates. Taking a look at the technical picture, the Dollar Index remains firmly bullish on the daily charts. A decisive breakout and daily close above 93.00 could encourage an incline higher towards 93.50.

Commodity spotlight – WTI Crude

Oil bulls entered the scene on Wednesday morning after Trump desertedthe Iran nuclear deal. WTI Crude has scope to venture higher in the near term, as fears of heightened geopolitical tensions in the Middle East fuel concerns of potential supply disruptions.

Taking a look at the technical picture, WTI Crude remains firmly bullish on the daily charts. There have been consistently higher highs and higher lows while the MACD trades to the upside. A solid daily close above the $70.00 level could invite an incline higher towards $71.10. Alternatively, if bulls are unable to keep prices above $70.00, the next key level of interest will be at $69.30.

Gold punished by strengthening Dollar

An aggressively appreciating U.S Dollar is likely to continue punishing Gold this week.

Although the yellow metal was initially boosted by market jitters following Donald Trump’s Iran announcement, gains were later capped by a strengthening Dollar. Gold remains vulnerable to downside losses, especially when considering how Dollar strength remains a dominant market theme.

Taking a look at the technical picture, previous support around $1324 could transform into a dynamic resistance that encourages a decline towards the psychological $1300 support level.

Currencies: USD Rebound Continues. Euro Remains In The Defensive

- Rates: No impact of US’s Iran decision for now; US 10-yr yield again near 3%

The US pulled out of the Iran nuclear deal, but the impact cross markets remained limited apart from a further surge in the oil price. Intraday momentum on bond markets is negative. US eco data remain strong and a 3-yr Note auction went weak. The US 10-yr yield approaches 3% again. Will it be sufficient to lure investor demand at tonight’s 10-yr Note auction? - Currencies: USD rebound continues. Euro remains in the defensive

Yesterday, the dollar extended its gradual rebound. The US withdrawal of the Iran nuclear deal didn’t change this trend. The euro suffers additional headwinds from renewed political uncertainty in Italy. Today, there are no really high profile data to guide USD trading. For now, the complex of higher oil prices, higher US yields and a strong dollar remains in place.

The Sunrise Headlines

- US stock markets ended unchanged even if the US pulled from the JCPOA. Most Asian equity indices trade positive overnight with Japan underperforming.

- The US is exiting the Iranian nuclear accord, President Donald Trump said, dismantling his predecessor’s most prominent foreign-policy initiative and bucking the appeals of some of America’s closest allies. (WSJ)

- US job openings surged to a record high in March, suggesting that a recent slowdown in hiring was probably the result of employers having difficulties finding qualified workers. The quits rate, a measure of job market confidence, rose to 2.3%. (Reuters)

- Japan’s wages rose in March at the fastest pace in years (real wages by 0.8% Y/Y; overall cash earnings by 2.1% Y/Y), a sign that the labor market may finally be fuelling the kind of pay rises the BoJ needs to push inflation higher. (BB)

- The House of Lords inflicted more defeats on May's Brexit bill: one that removes the specific date of Brexit, one that pushes May to keep the UK in EU agencies, one over calls for stronger scrutiny of government lawmaking and one requiring the PM to negotiate to keep the UK in the EU Economic Area. (BB)

- Argentina is seeking IMF aid after a series of drastic interest rates failed to stop the slide of the peso, pushing a country that only recently restored its credibility with investors back towards a financial crisis. (FT)

- Today’s eco calendar only contains US PPI data. The RBNZ is expected to leave rates unchanged. Germany and the US tap the market. Fed Bostic speaks

Currencies: USD Rebound Continues. Euro Remains In The Defensive

USD rebound continues. Euro suffers.

Yesterday, the dollar retained the benefit of the doubt. Markets focused on president Trump’s statement on Iran, but it wasn’t easy to adapt positions on this story. At the same time, the euro remained in the defensive. The threat of new Italian elections provided a good reason for further euro losses. Interest rate differentials were not that important for FX trading yesterday, but the ST spread between the US and Germany widened further. EUR/USD extended its decline and closed the day at 1.1864 (from 1.1922). USD/JPY was little changed at 109.13.

Overnight, Asian equities are trading mixed as investors ponder the impact the US leaving the Iran deal. The oil price (Brent) is reaching the highest level since end 2014. For now, this goes hand in hand with higher US yields and a stronger dollar. USD/JPY did some kind of catching up move this morning and trades currently at 109.50. EUR/USD is trading in the mid 1.18 area, within reach of the correction low.

Today, there are few data in EMU. In the US, the PPI prices will be published. A modest rise of 0.2% M/M is expected. We doubt that this series will provide much additional support for the dollar. Market are looking forward to tomorrow’s US CPI. Also keep an eye at the US 10-y auction. Yesterday, a mediocre 3-y auction supported higher ST yields. In theory, higher yields due to sluggish investors demand is an ambiguous story from a dollar point of view. We look out for the USD reaction in case of another weak auction. For now, the gradual USD uptrend looks well in place. At the same, political and economic headlines are keeping the euro in the defensive. There is no obvious reason to row against the established EUR/USD downtrend. Intermediate support comes in at 1.1789 ahead of the 1.1718 correction low. Also look out whether USD/JPY is able to return to the 110 area.

Yesterday, sterling basically followed the global trends of euro weakness and USD strength. The PM May suffered a new defeat on the Brexit law in the House of Lords, but it isn’t clear to what extent this will change the government’s Brexit strategy. Overnight, BRC retail sales dropped an awful 4.2 % Y/Y. Later today, there are no important data. Investors are looking forward to tomorrow’s BoE policy decision. The BoE is expected to leave the policy rate unchanged, but to keep the door open for an August rate hike. This scenario might be mildly sterling supportive. EUR weakness is a (temporary) negative for EUR/GBP, too

EUR/USD downtrend continues

Oil Moves Higher As Trump Withdraws From Iran Deal

Spot Oil prices are higher overnight after the US withdrew from the Iran Deal yesterday. US WTI bottomed at $67.56 yesterday and is now currently trading at $70.53. US President Trump has long said that the deal was “no good” and part of his election campaign was to end US participation in the agreement. The other signatories of the deal have expressed their willingness to maintain the agreement with Iran in a move that isolates the US. Whether the withdrawal is part of a negotiation tactic by the President remains to be seen and it will depend on the outcome of the Iranian response, with Iran’s Parliamentary Speaker saying that the country has no obligation now to honour the commitments of the agreement.

The Australian Budget was released yesterday. The budget contained a series of tax cuts aimed at lower income taxpayers and forecasted a drop in the deficit from 20.5B to 14.5B. The expectation is for the budget to have a small surplus in 2019/20 of 2.2B. AUDUSD continued to fall from 0.75181 to 0.74352 during this release.

Canadian Housing Starts s.a (YoY) (Apr) were released and came in at 214K against an expected 220K, from a previous 225K last month. This data is performing strongly despite the decline this month. The previous three readings beat expectations but this miss breaks the winning streak. The data showed a drop in single detached dwellings and a rise in multiple unit dwellings. USDCAD dropped from a high of 1.29838 to 1.29633 as a result of this data.

US JOLTS Job Openings (Mar) was released with a headline number of 6.550M against an expected 6.101M, from 6.052M previously, which was revised up to 6.078M. This metric exceeded forecasts and the previous high of 6.31M reached in March, showing job creation is strong and the labour market is dynamic. GBPUSD fell to a low of 1.34843 but turned from there to trade higher for the rest of the day.

EURUSD is down -0.13% overnight, trading around 1.18490.

USDJPY is up 0.36% in early session trading at around 109.514.

GBPUSD is down -0.14% this morning, trading around 1.35275.

USDCAD is up 0.04% overnight, currently trading around 1.29527.

Gold is down -0.25% in early morning trading at around $1,311.10.

WTI is up 0.69% this morning, trading around $70.55.

RBNZ Expected To Leave Rates On Hold At 1.75%

At 12:30 GMT, US Producer Price Index Ex-Food and Energy (YoY) (Apr) is expected to be 2.4% against a previous reading of 2.7%. Producer Price Index (MoM) (Apr) is expected to be 0.2% from 0.3% previously. Producer Price Index Ex-Food and Energy (MoM) (Apr) is expected to be 0.2% against a previous reading of 0.3%. Producer Price Index (YoY) (Apr) is expected to be 2.8% from 3.0% previously. This data is expected to come in lower than expected, with the monthly numbers expected to be slightly softer than the previous readings. The yearly readings are showing bigger percentage declines, indicating a fall in consumer inflation. USD crosses may be affected by this data release.

At 12:30 GMT, Canadian Building Permits (MoM) (Mar) are expected to rise to 2.0% from a previous -2.6%. This shows an anticipated pick-up in the construction industry, although the metric has been showing smaller advances and declines recently compared with historic standards. CAD crosses may be impacted as a result of this data release.

At 14:30 GMT, US EIA Crude Oil Stocks change (May 4) data will be released with an expected draw of -0.719M forecasted, from a build of 6.218M last week. This data surprised to the upside last week, exceeding the expected build of 1.000M. Oil markets are in focus at the moment, after the US withdrew from the Iran Deal yesterday and this data release may add further volatility to the mix.

At 21:00 GMT, The Reserve Bank of New Zealand will release its Rate Statement, Interest Rate Decision and Monetary Policy Statement. The Bank is expected to hold rates at 1.75% and a Press Conference will take place an hour later at 22:00 GMT. NZD crosses will be exposed to additional volatility during this event.

The EU Press Conference On Trade Talks With China

Market movers today

Today is another quiet day in terms of global data releases. The EU press conference on trade talks with China (market access, investment, US tariffs and intellectual property rights) may be interesting given the current focus on global trade policy.

Japanese Prime Minister Shinzo Abe will play host to South Korean President Moon Jae-in and Chinese Premier Li Keqiang.

In the Scandies, focus is on Swedish and Norwegian inflation data for April. In Sweden, we estimate CPIF excluding energy to be 1.2%, 0.2pp below the Riksbank's forecast. In Norway, we estimate CPI core inflation rose to 1.4% y/y in April from 1.2% in March. For more details, see page 2.

Selected market news

Last night, US President Trump announced that the US will withdraw from the Iran nuclear deal from 2015 and reinstate the highest level of economic sanctions on Iran. Trump said that the US will work with its allies to prevent Iran from developing nuclear weapons, but also noted that he is willing to negotiate a deal with Iran. According to a statement from the US Treasury Department, sanctions will be reinstated after 'wind down periods' of 90 or 180 days and thus take full effect after 4 November. See Flash Comment International: US withdraws from Iran nuclear deal , 8 May, for more details.

European leaders have expressed their regrets and concerns over Donald Trump's decision to re-impose US nuclear sanctions on Iran and EU's foreign policy chief, Federica Mogherini, said 'the European Union will remain committed to the continued full and effective implementation of the nuclear deal'.

The market reaction to the announcement from the US was muted overall suggesting that this move from the US was likely to have been priced into the market already, and while the situation should be monitored, this does not change our economic or financial forecasts at this stage. Price actions in the oil market last night underscore that it is unclear whether this will affect Iran's oil exports and thus the oil market, e.g. the US does not import oil from Iran. The oil price rose initially with Brent crude rising USD1/bbl and above USD75/bbl and after a short correction lower, it has continued higher overnight trading at USD76.60/bbl this morning.

In Japan, data released this morning showed that wages rose at the fastest pace since 2003 with regular wages jumping 2.1% y/y in March. Many Japanese companies have struggled to find employees due to a very tight labour market, and the gains in regular wages in March were partly the result of companies hiring more permanent, full-time workers, who generally receive higher pay. Overall, today's wage figures are an encouraging sign for the Bank of Japan, which still struggles to push inflation higher. We still expect the Bank of Japan to keep its monetary policy unchanged in the next 12 months, but we will monitor the development in the labour market and wages closely for any signs that wages may accelerate further.

Elliott Wave View: VOX Calling For A Bounce Soon

Vanguard communication services ETF ticker symbol: VOX short-term Elliott Wave view suggests that the bounce to 88.35 on 4/24/2018 high ended cycle degree wave “b”. Below from there, the cycle degree wave “c” remain in progress as an Impulse Elliott Wave structure looking for more downside extensions.

Down from 88.35 high, Primary wave ((1)) is in progress as Impulsive structure where the internal distribution of each leg down is unfolding in 5 waves structure. Intermediate wave (1) ended in 5 waves structure at 86.93. Above from there, Intermediate wave (2) bounce ended at 88.21 as a Flat structure. Then down from there Intermediate wave (3) ended at 82.51 low. Subdivision of wave (3) unfolded as impulse structure of lesser degree where Minor wave 1 of (3) ended at 85.99, Minor wave 2 of (3) ended at 87.89, Minor wave 3 of (3) ended at 82.91, Minor wave 4 of (3) ended at 84.27, and Minor wave 5 of (3) ended at 82.51 low.

Above from there, the bounce to 84.23 high ended Intermediate wave (4) bounce as a zigzag correction. Intermediate wave (5) of ((1)) remains in progress in another 5 waves structure looking to extend 1 more push lower towards 81.45 – 82.11, which is inverse 123.6%-161.8% Fibonacci extension area of Intermediate wave (4). Afterwards, the instrument is expected to see a bounce in Primary wave ((2)) in 3, 7 or 11 swings to correct cycle from 4/24 high ($88.35) before further downside extension is seen. We don’t like buying it into a proposed bounce.

VOX 1 Hour Elliott Wave Chart

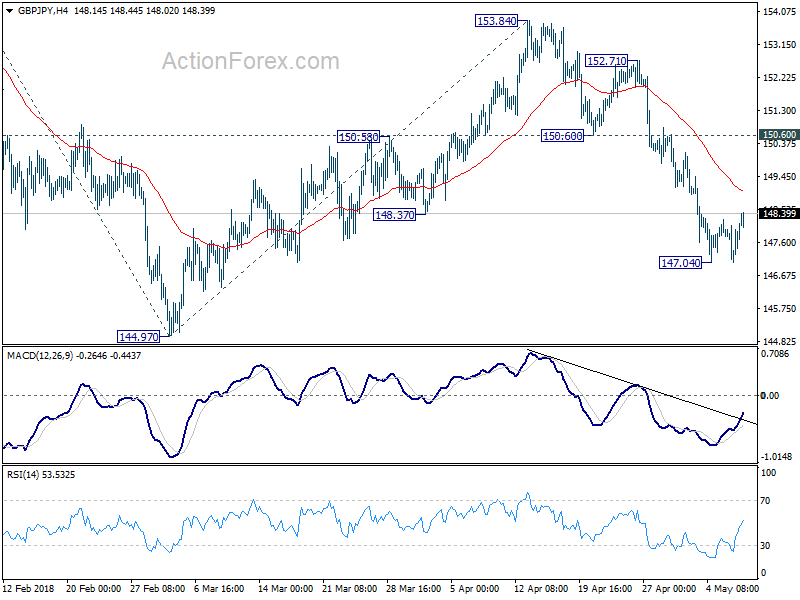

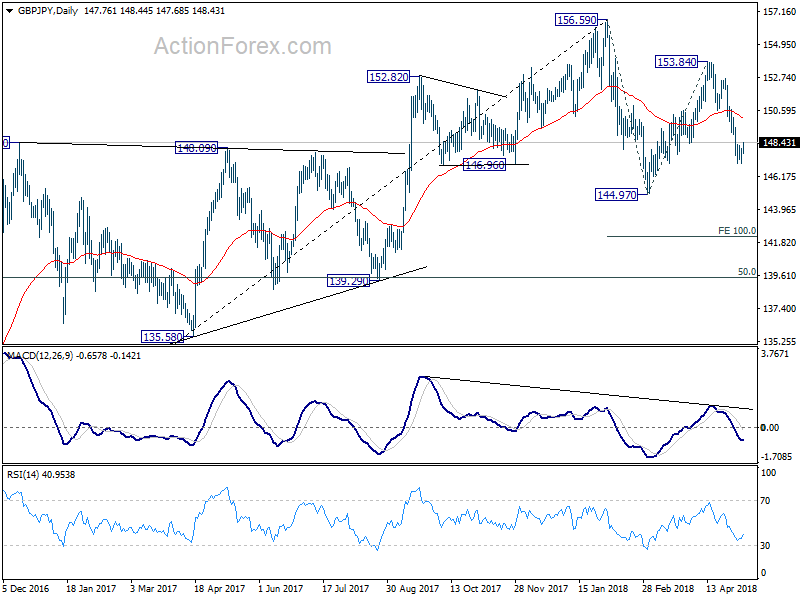

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.23; (P) 147.65; (R1) 148.26; More...

Intraday bias in GBP/JPY remains neutral for consolidation above 147.04 temporary low. Further recovery could be seen to 4 hour 55 EMA (now at 149.03). But upside should be limited below 150.60 support turned resistance to bring another decline. Below 147.04 will target 144.97 first. Break there will resume the fall from 156.59 and target 100% projection of 156.59 to 144.97 from 153.84 at 142.22 next.

In the bigger picture, for now, we're treating price actions from 156.59 as a corrective move. Therefore, while deeper fall is expected, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. There is still prospect of extending the rise from 122.36. However, considering that GBP/JPY failed to sustain above 55 month EMA (now at 153.94), firm break of 139.29 will confirm trend reversal and turn outlook bearish.

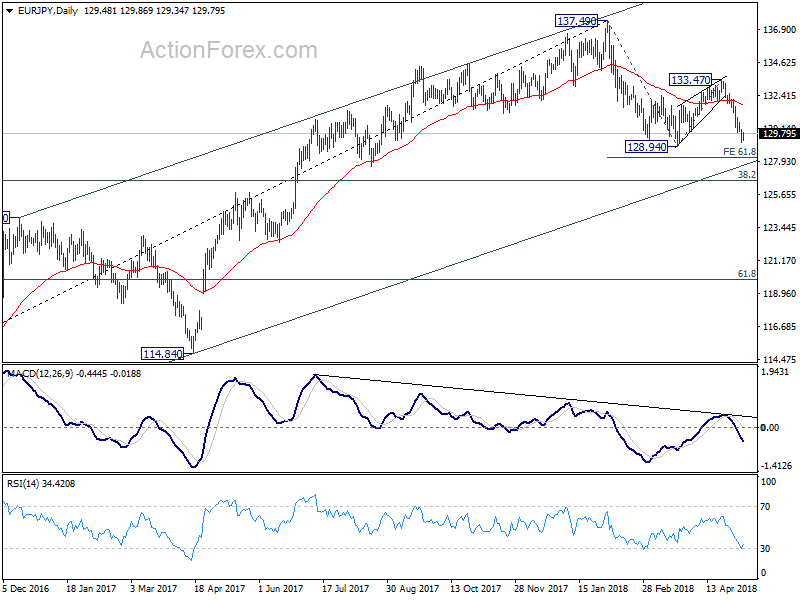

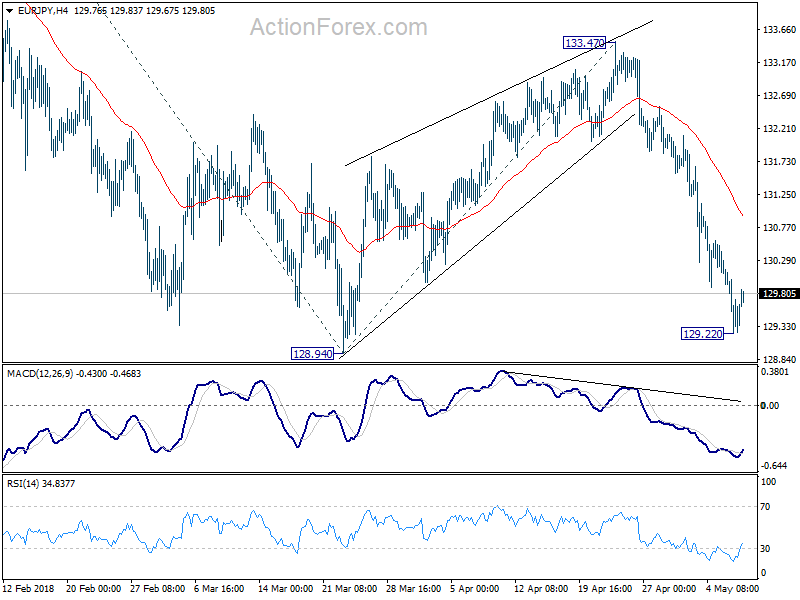

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.09; (P) 129.60; (R1) 129.98; More....

A temporary low is in place at 129.22 in EUR/JPY and intraday bias is turned neutral. Consolidation should be relatively brief as long as 4 hour 55 EMA holds (now at 130.98). Below 129.22 will target 128.94 support. Break will resume whole decline from 137.49 and target 61.8% projection of 137.49 to 128.94 from 133.47 at 128.18 next. Overall, near term outlook will stay bearish as long as 133.47 resistance holds and downside breakout is expected eventually.

In the bigger picture, for now, price actions from 137.49 are viewed as a corrective pattern only. Hence, while, deeper decline would be seen, strong support is expected at 38.2% retracement of 109.03 to 137.49 at 126.61 to contain downside and bring rebound. Up trend from 109.03 (2016 low) is expected to resume afterwards. Though, sustained break of 126.61 will be an important sign of trend reversal and will turn focus to 124.08 resistance turned support.