Sample Category Title

Limited Market Movements Ahead Of NFP And Wage Data

With the Non-farm payrolls and wage data set to dominate the session today, the overnight picture shows small ranges in markets after Indices sold-off but recovered yesterday. The AUD moved up to 0.75600 in reaction to the RBA Monetary Policy Statement, as the bank upgraded its core inflation outlook for the year and set the tone for higher rates “to be appropriate at some point”. But this move has since reversed, moving below 75420, the level price traded at when the statement was released. Elsewhere, there is no news on the US/Chinese trade talks in Beijing, as the US delegation delivered a list of requests on trade, to their counterparts.

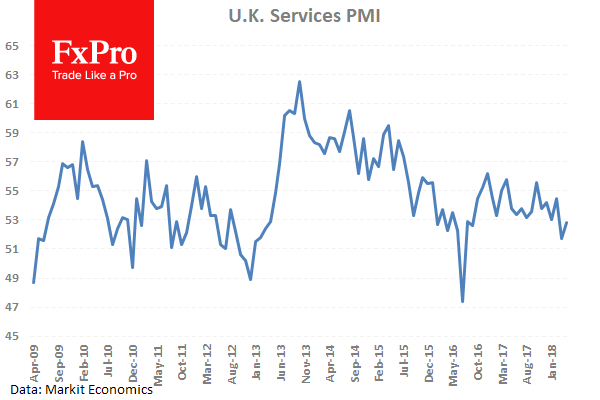

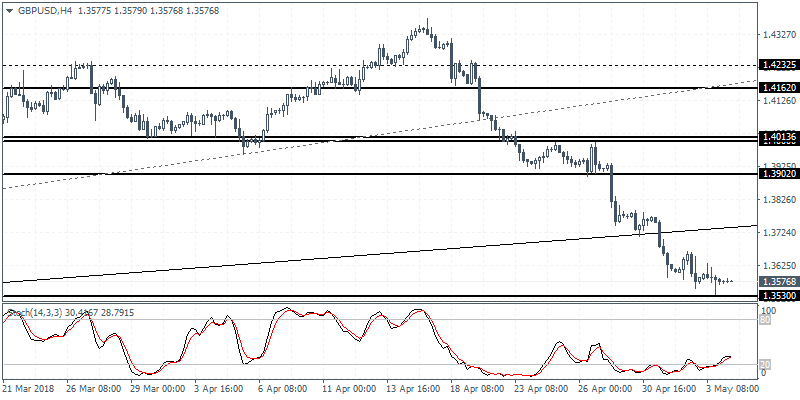

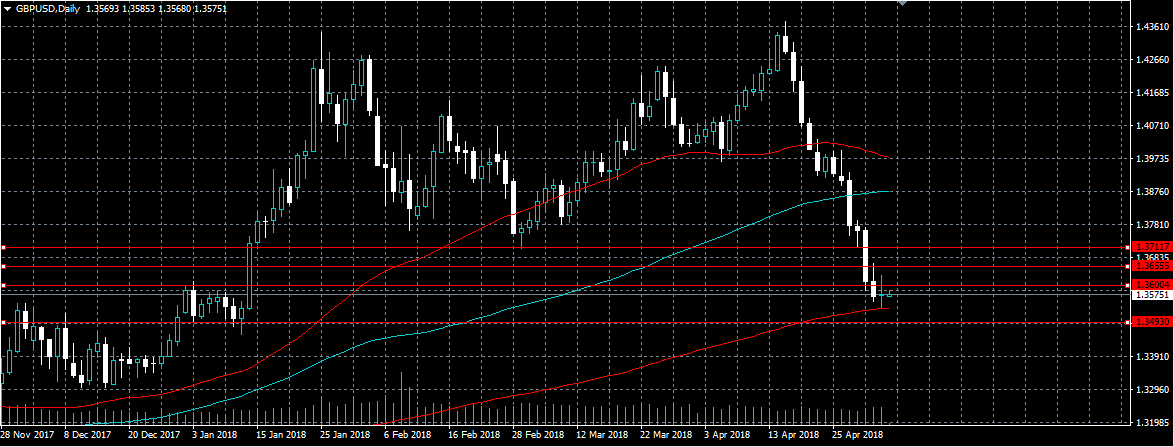

UK Markit Services PMI (Apr) came in at 52.8 against an expected 53.5, from 51.7 previously. This data is continuing to decline from its 2013 high of 62.5 and had fallen below 53.0, which had been somewhat of a floor over the last 18 months. The number disappointed yesterday, as it failed to move back above 53.0. GBPUSD moved down from 1.36191 to 1.35736 as a result.

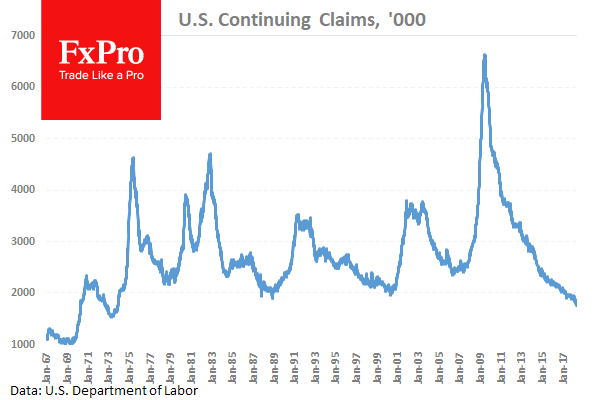

US Continuing Jobless Claims (Apr 20) came in at 1.756M versus an expected 1.838M, against 1.837M previously, which was revised down to 1.833M. Initial Jobless Claims (Apr 27) was 211K versus an expected 225K, against 209K previously. This data is showing mixed results, with an increase failing to materialise, generating a miss on expectations but a slight uptick in Initial claims. Nonfarm Productivity (Q1) came in at 0.7% versus an expected 0.9%, against 0.0% previously, which was revised up to 0.3%. This shows efficiency slipping and ultimately upward pressure on inflation. Unit Labour Costs (Q1) was 2.7% versus an expected 2.9%, against 2.5% prior, which was revised down to 2.1%. This shows an increase in this metric despite the miss, with these costs eventually being passed onto consumers, raising inflation. The Trade Balance (Mar) was $-49.0B versus an expected $-50.0B, against a previous $-57.6B, which was revised down to $-57.7B. This data has recovered after reaching levels not seen since 2008 last month. GBPUSD tested up above 1.36000 initially but fell to 1.35377 after this data release.

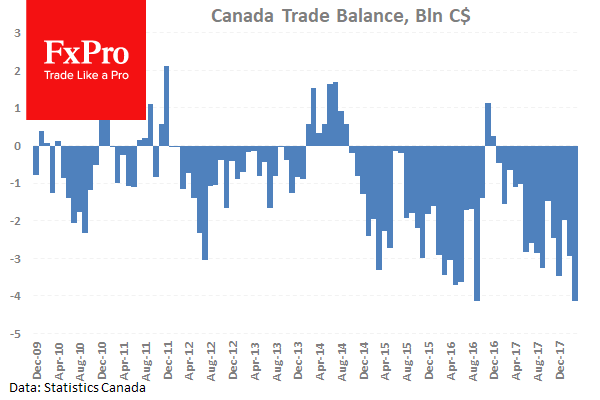

Canadian International Merchandise Trade (Mar) was $-4.14B versus an expected $-2.24B, against a previous number of $-2.69B, which was revised down to $-2.93B. This data has fallen dramatically to match the low of November 2016. USDCAD tested higher to 1.28739 before reversing lower to 1.28431 following this data release.

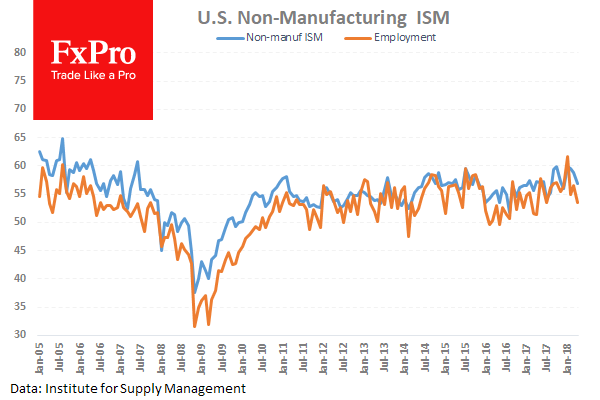

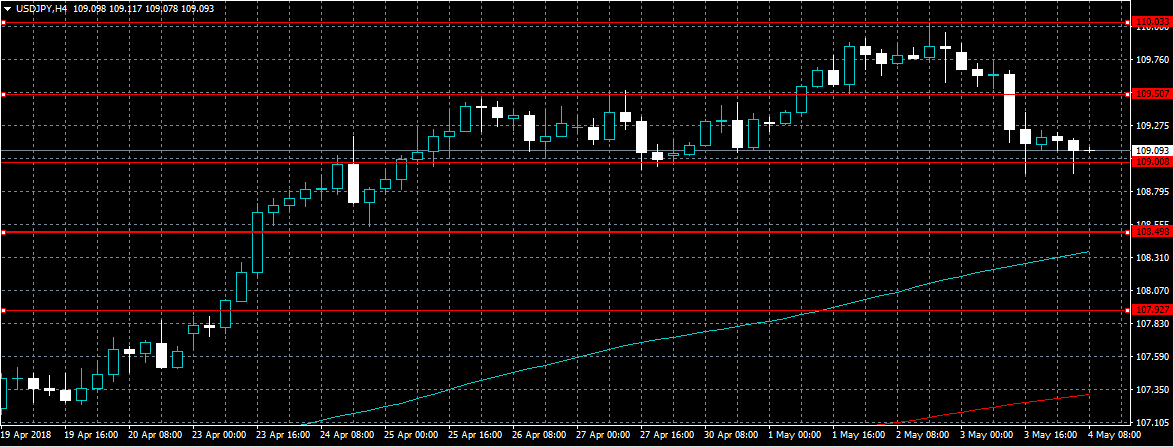

US ISM Non – Manufacturing PMI (Apr) came in at 56.8 versus an expected 58.1, against 58.8 previously. This is still in the upper range of the data releases we have seen over the past seven years but off the highs of above 65.0 reached before the financial crisis. Factory Orders (MoM) (Mar) was 1.6% against an expected 1.4%, from 1.2% prior, which was revised up to 1.6%. USDJPY fell from 109.353 to 108.925 following this data release.

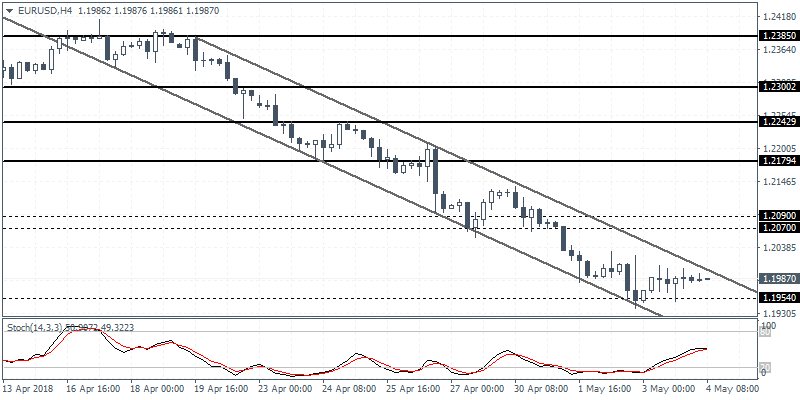

EURUSD is down -0.04% overnight, trading around 1.19833.

USDJPY is down -0.08% in early session trading at around 109.093.

GBPUSD is up 0.04% this morning, trading around 1.35774.

Gold is up 0.05% in early morning trading at around $1,312.63.

WTI is down -0.09% this morning, trading around $68.39.

US Non-Farm Payrolls And Wage Data Dominate Calendar

At 07:55 GMT, German Markit Services PMI (Apr) is expected to be unchanged at 54.1. After reaching a multi-year high of 57.3 in February, this data has come back into its range under 56.0. German Markit PMI Composite (Apr) is also expected to be unchanged at 55.3. Traders will be watching for the numbers to deviate from expectations and create volatility in EUR pairs.

At 08:00 GMT, Eurozone Markit Services PMI (Apr) is expected to be unchanged at 55. This figure had fallen last month, after hitting a high of 58.0 in February. Markit PMI Composite (Mar) is also expected to be unchanged at 55.2. EUR crosses may be impacted by this data release.

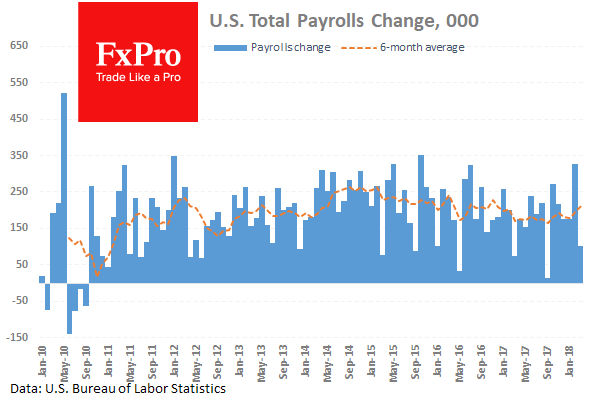

At 12:30 GMT, US Non-Farm Payrolls (Apr) is expected at 192K v a prior 103K. This measures the change in the number of employed people in April. The Unemployment Rate (Apr) is expected at 4.0% with a prior of 4.1%. This measures the percentage of the total workforce unemployed and actively seeking employment during April. Average Hourly Earnings (YoY) (Apr) is expected to be unchanged at 2.7%. Average Hourly Earnings (MoM) (Apr) is expected to be 0.2% against 0.3% previously. Average Weekly Hours (Apr) is expected to be unchanged at 34.5. Labour Force Participation Rate (Apr) is expected to be unchanged at 62.9%. This data may have a large impact on the financial markets, as the tight labour market has yet to lead to an increase in earnings. This would lead to an increase in inflation, which markets have reacted negatively to recently. USD crosses may experience volatility around these data releases.

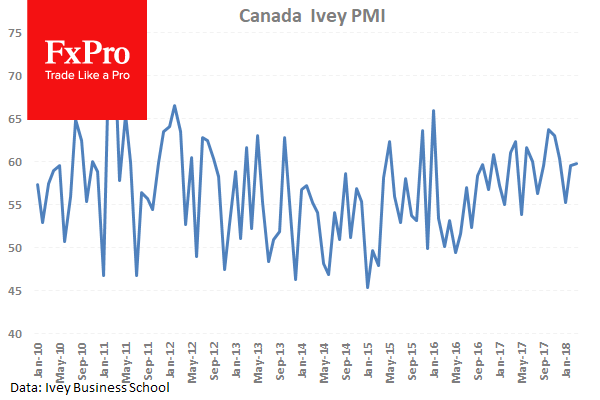

At 14:00 GMT, Canadian Ivey Purchasing Managers Index s.a. (Apr) is expected to be 60.2 against a previous 59.8. Ivey Purchasing Managers Index (Apr) was 64.7 previously. This data is showing robust growth, continuing one of the longest positive runs, having remained above 50.0 for over 20 months. CAD crosses may be moved by this data release.

At 16:00 GMT, US FOMC Member Dudley is due to discuss financial turmoil and the challenges ahead in an interview conducted by Matthew Winkler with Bloomberg News. This event may result in moves in USD crosses.

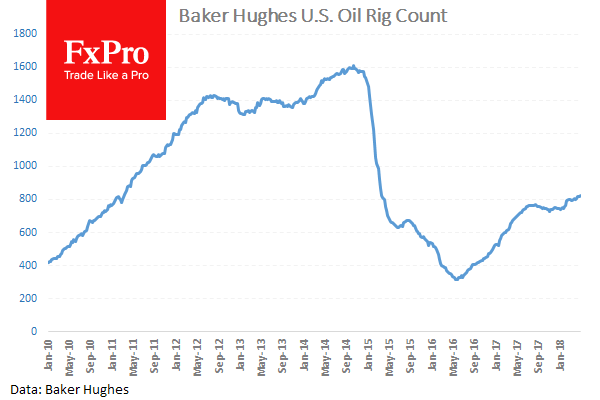

At 17:00 GMT, Baker Hughes US Oil Rig Counts is due to be released with a headline number from last week of 825. WTI Oil may become volatile around this data release and will be in traders’ minds when trading resumes on Monday.

At 19:00 GMT, US FOMC Member Williams is due to deliver brief remarks at the Hoover Institute’s Monetary Policy Conference, hosted by Stanford University. This event could result in moves in USD crosses.

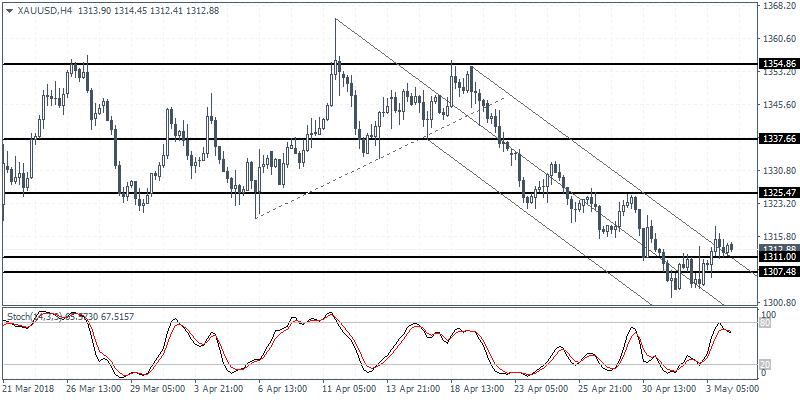

XAUUSD Intraday Analysis

XAUUSD (1312.88): Gold prices managed to breakout above the price level of 1311 - 1307. A close above this support level now suggests a potential upside move in prices. The resistance level of 1325.50 remains a key level for price action to test. In the near term, we expect gold prices to remain range bound within the current levels. The support at 1311 - 1307 is likely to hold the declines in the near term. However, if this support level gives way, we could expect gold prices to drop toward the 1300 level of round number support.

GBPUSD Intraday Analysis

GBPUSD (1.3576): The British pound continued its decline although price action remains supported above the price level of 1.3530. The weaker services PMI data cast doubts on whether the BoE would be able to hike rates next week. This led to the GBPUSD posting declines. From a technical outlook, we expect to see the currency pair consolidating near the current levels of support. A rebound off this price level could signal a potential move to the upside. The breached trend line remains a key dynamic resistance level if there is a correction.

EURUSD Intraday Analysis

EURUSD (1.1987): The EURUSD was seen closing weaker on the day as price action fell to a fresh 4month low at 1.1954. The decline to this support level coincided with the support level that was established in late November 2017. Price action has remained slightly volatile after slipping to this level. In the near term, we expect to see the EURUSD consolidate around this level of support before possibly posting a rebound. The resistance level at 1.2090 - 1.2070 remains as a key level to the upside and therefore, the EURUSD could remain range bound within these levels.

Traders Look To Payrolls Report

The U.S. dollar was seen holding ground on Thursday albeit trading mixed. Economic data on the day included the UK's services PMI. Data showed that services sector activity increased modestly from March's 51.7 to 52.8.

In the Eurozone, the flash inflation estimates showed that headline inflation rebounded to 1.2% but this was below forecasts of a 1.3% increase. Core inflation rate eased further to 0.7%.

The ISM's non-manufacturing PMI data showed that the index eased to 56.8 missing forecasts and down from March's reading of 58.8

Looking ahead, the economic data for the day will see the nonfarm payrolls report standing out. Median forecast point to the U.S. unemployment rate potentially easing to 4.0% in the month of April. The number of jobs added during the month is expected to rebound from March's 103k to 189k. Wage growth which also remains a key component is expected to show a 0.2% increase on a month over month basis. A better than expected report could potentially renew hawkish bets on the U.S. dollar.

Elsewhere, the Canadian Ivey PMI data is due to be released today. A number of Fed speeches are also lined up including Dudley, Williams and Quarles.

GBPUSD Bounces From 200-Day Moving Average

The British pound has recovered upside momentum against the U.S dollar, after sterling dip-buyers stepped in just before the pairs key 200-day moving average. The GBPUSD pair currently trades around the 1.3575 level, after finding strong demand from 1.3537 level, which was only slightly above its 200-day moving average, at 1.3532. Traders now look towards the U.S Non-farm Payrolls job report, with the monthly headline number and monthly wage earnings data strongly in focus.

The GBPUSD pair is intraday bearish while trading below the 1.3600 level, further losses towards 1.3532 and 1.3493 levels remain possible.

If the GBPUSD pair moves back above the 1.3600 level, buyers may test towards the 1.3665 and 1.3710 levels.

USDJPY Lower After Breaking Key Support

The U.S dollar has tumbled lower against the Japanese yen, hitting, as falling equity markets prompted traders to move into the perceived safety of the yen currency. The USDJPY pair currently trades around the 109.00 level, after crashing below the 109.50 support level on Thursday, as U.S stock price tumbled. Traders look towards the European stock market reaction and the 109.00 level for directional guidance, ahead of today’s Non-farm Payrolls job report.

The USDJPY pair is now bearish while trading below the 109.50 level, support is now found at the 108.49 and 107.92 levels.

If the USDJPY pair starts to trade back above the key 109.50 level, buyers may test towards the 110.03 and 110.40 levels.

Friday Is Nonfarm Payrolls Day

A deluge of economic data will make its way through the financial markets on Friday, but none are more important than the US nonfarm payrolls release, which is scheduled to come at 12:30 GMT. The US jobs report is arguably the most anticipated release of the month, as it gives investors insights into the health of the world's largest economy.

In terms of economic data, the first major release of the day comes at 06:45 GMT when the French government reports on international trade. Paris is forecast to post a trade deficit of €4.9 billion for March, down from €5.2 billion the month before.

IHS Markit will release euro-wide PMI data beginning at 07:15 GMT. PMI reports covering services and composite indices are scheduled for Spain, Italy, France, Germany and the 19-member Eurozone. The Eurozone composite PMI is forecast to come in at 55.2.

The European Commission's statistical agency will report on retail sales at 09:00 GMT. Receipts at retail stores are forecast to rise 0.5% in March after a 0.1% uptick the month before. In annualized terms, this translates to growth of 1.9%.

Shifting gears to North America, the Labor Department is expected to show the creation of 192,000 nonfarm jobs in April. That would mark a significant improvement over the March growth rate of just 103,000. The jobless rate is forecast to fall to 4% from 4.1% the previous month.

Average hourly earnings, a proxy for inflation, likely rose 0.2% month-on-month and 2.7% annually.

Also on Friday, Federal Reserve officials William Dudley and John Williams will deliver speeches at 16:00 GMT and 19:00 GMT, respectively. Williams is a member of this year's Federal Open Market Committee (FOMC), which recently voted to keep interest rates on hold.

Energy traders will also be keeping a close eye on the weekly rig counts courtesy of Baker Hughes Inc.

EUR/USD

Europe's common currency continues to hold below 1.2000 as traders turn their attention to nonfarm payrolls. EUR/USD was last seen trading around 1.1990. where it faces immediate support at 1.1937 and resistance at 1.2000.

GBP/USD

Cable continues to hold at the lower end of its three-week range, with prices firmly capped below 1.3600. At the time of writing, GBP/USD was valued at 1.3583, where it had gained 0.1% from the previous close. The pair faces a psychological hurdle at 1.3700. On the downside, support is located around 1.3570.

USD/CAD

The North American currency pair has established a choppy trading range over the past week, with prices bouncing around between 1.2820 and 1.2900. USD/CAD was last valued at 1.2840, where it was little changed. Nonfarm payrolls will likely provide the next major catalyst for this pair, which appears to have shrugged off rising oil prices.

Currencies: Dollar Probably Needs Excellent Payrolls To Extend Rebound

Rates: Payrolls strong enough to overrule Fed?

Core bonds proved to be more resilient of late as the ECB and Fed respectively signaled no haste to start the normalization process and to step up the gradual rate hike cycle. US payrolls are expected to match or beat consensus today, but will they be strong enough to overrule the recent cautious rhetoric?

Currencies: Dollar probably needs excellent payrolls to extend rebound

Yesterday, the dollar took a breather as the Fed indicated that it is in no hurry to step up the pace of rate hikes. Today’s US payrolls might clarify whether there is room for additional USD gains. For that to happen a combination of good payrolls growth and solid wages is probably needed. EUR/USD 1.1915/35 is the next important technical reference.

The Sunrise Headlines

- US stock markets ended between flat and 0.25% lower. Losses on Asian equity markets tend to be slightly bigger overnight.

- Argentina raised interest rates for the 2nd time in a week (to 33.25%) after more than $5bn of central bank intervention failed to stop a steep fall in the peso, highlighting the intensifying pressure on EM currencies in recent weeks. (FT)

- The April Caixin services PMI unexpectedly picked up from 52.3 to 52.9 as new business and employment grew at a faster rate, signalling a solid rise in a sector that Beijing is counting on to maintain economic growth. (Reuters)

- A US trade delegation in China has been having very good conversations, US Treasury Secretary Mnuchin said, as he heads into the second and likely last day of talks in Beijing. A breakthrough deal is viewed as highly unlikely. (Reuters)

- North Korea said to have agreed in principle with US for “complete” denuclearization by 2020, South Korea’s Dong-A Ilbo newspaper reports, citing unidentified intelligence sources. (BB)

- UK PM May's Conservative Party avoided a wipeout in London local elections and eked out gains in Brexit-supporting regions elsewhere, early results showed, although her Labour opponents gained ground in the capital. (Reuters)

- Today’s eco calendar contains US payrolls, unemployment rate and average hourly earnings. EMU retail sales and the final services PMI feature on the agenda as well. Several ECB & Fed governors speak

Currencies: Dollar Probably Needs Excellent Payrolls To Extend Rebound

Payrolls strong enough for further USD gains?

EUR/USD faced conflicting signals yesterday. The dollar rally slowed as the Fed suggested that it won’t immediately react to a limited overshoot of the inflation target. This blocked the rise in US yields and the USD. On the euro side of the story, EMU April inflation again missed the consensus by quite a big margin (1.2% Y/Y). Both conflicting stories kept EUR/USD in a tight range mostly in the upper half of the 1.19 big figure. Uncertainty the high level US-Chinese trade talks caused some caution in global risk sentiment. The impact on the major FX cross rates stayed modest but the yen developed a tentative rebound. USD/JPY drifted south off the 110 area. EUR/JPY showed a sharp intraday setback.

Overnight, Asian equities continued the recent lacklustre performance. Investors are monitoring the China-US trade talks and are looking forward to the US payrolls. The (trade weighted) USD is holding slightly off the recent peak. EUR/USD hovers just below 1.20. USD/JPY struggles not to fall below the 1.09 handle. The Reserve bank of Australia sees good growth in 2018/2019 (3 % +), but expects inflation to stay in the lower part of the 2-3% target band. The Aussie dollar rebounded a few more ticks and trades again in the AUD/USD 75.50 area.

Today, the final EMU services PMI’s will be published. Markets will look out whether the recent easing in the EMU economic momentum might bottom. However, the focus is on the US payrolls report. US April job growth is expected to return to its recent trend close to 200k. Earnings growth (0.2% M/M and 2.7% Y/Y expected) will also be key for the market reaction. After Wednesday’s balanced Fed communication, we assume that the dollar needs a positive surprise to extend its recent rally. In that case, we look out whether EUR/USD will be able to break the 1.1915/36 support area. Given yesterday’s post-Fed reaction, this might not be that easy. Of course there is still the euro side of the story. For USD/JPY the 110 area is the next topside reference.

Yesterday, sterling traded with a negative bias. The political stalemate on Brexit within the Conservative party remains an underlying negative for sterling. The UK services PMI also disappointed, indicating ongoing slow growth the start of Q2 and further reducing the chances of a May BoE rate hike. Today, there are no important data in the UK. EUR/GBP tries to sustain north of 0.88. Negative news might push the pair higher to the 0.8868/0.9033 resistance ahead of next week’s BoE meeting.

D: will payrolls be strong enough for USD to rally below 1.1936/15 support?