Sample Category Title

Friday Is Nonfarm Payrolls Day

A deluge of economic data will make its way through the financial markets on Friday, but none are more important than the US nonfarm payrolls release, which is scheduled to come at 12:30 GMT. The US jobs report is arguably the most anticipated release of the month, as it gives investors insights into the health of the world's largest economy.

In terms of economic data, the first major release of the day comes at 06:45 GMT when the French government reports on international trade. Paris is forecast to post a trade deficit of €4.9 billion for March, down from €5.2 billion the month before.

IHS Markit will release euro-wide PMI data beginning at 07:15 GMT. PMI reports covering services and composite indices are scheduled for Spain, Italy, France, Germany and the 19-member Eurozone. The Eurozone composite PMI is forecast to come in at 55.2.

The European Commission's statistical agency will report on retail sales at 09:00 GMT. Receipts at retail stores are forecast to rise 0.5% in March after a 0.1% uptick the month before. In annualized terms, this translates to growth of 1.9%.

Shifting gears to North America, the Labor Department is expected to show the creation of 192,000 nonfarm jobs in April. That would mark a significant improvement over the March growth rate of just 103,000. The jobless rate is forecast to fall to 4% from 4.1% the previous month.

Average hourly earnings, a proxy for inflation, likely rose 0.2% month-on-month and 2.7% annually.

Also on Friday, Federal Reserve officials William Dudley and John Williams will deliver speeches at 16:00 GMT and 19:00 GMT, respectively. Williams is a member of this year's Federal Open Market Committee (FOMC), which recently voted to keep interest rates on hold.

Energy traders will also be keeping a close eye on the weekly rig counts courtesy of Baker Hughes Inc.

EUR/USD

Europe's common currency continues to hold below 1.2000 as traders turn their attention to nonfarm payrolls. EUR/USD was last seen trading around 1.1990. where it faces immediate support at 1.1937 and resistance at 1.2000.

GBP/USD

Cable continues to hold at the lower end of its three-week range, with prices firmly capped below 1.3600. At the time of writing, GBP/USD was valued at 1.3583, where it had gained 0.1% from the previous close. The pair faces a psychological hurdle at 1.3700. On the downside, support is located around 1.3570.

USD/CAD

The North American currency pair has established a choppy trading range over the past week, with prices bouncing around between 1.2820 and 1.2900. USD/CAD was last valued at 1.2840, where it was little changed. Nonfarm payrolls will likely provide the next major catalyst for this pair, which appears to have shrugged off rising oil prices.

Currencies: Dollar Probably Needs Excellent Payrolls To Extend Rebound

Rates: Payrolls strong enough to overrule Fed?

Core bonds proved to be more resilient of late as the ECB and Fed respectively signaled no haste to start the normalization process and to step up the gradual rate hike cycle. US payrolls are expected to match or beat consensus today, but will they be strong enough to overrule the recent cautious rhetoric?

Currencies: Dollar probably needs excellent payrolls to extend rebound

Yesterday, the dollar took a breather as the Fed indicated that it is in no hurry to step up the pace of rate hikes. Today’s US payrolls might clarify whether there is room for additional USD gains. For that to happen a combination of good payrolls growth and solid wages is probably needed. EUR/USD 1.1915/35 is the next important technical reference.

The Sunrise Headlines

- US stock markets ended between flat and 0.25% lower. Losses on Asian equity markets tend to be slightly bigger overnight.

- Argentina raised interest rates for the 2nd time in a week (to 33.25%) after more than $5bn of central bank intervention failed to stop a steep fall in the peso, highlighting the intensifying pressure on EM currencies in recent weeks. (FT)

- The April Caixin services PMI unexpectedly picked up from 52.3 to 52.9 as new business and employment grew at a faster rate, signalling a solid rise in a sector that Beijing is counting on to maintain economic growth. (Reuters)

- A US trade delegation in China has been having very good conversations, US Treasury Secretary Mnuchin said, as he heads into the second and likely last day of talks in Beijing. A breakthrough deal is viewed as highly unlikely. (Reuters)

- North Korea said to have agreed in principle with US for “complete” denuclearization by 2020, South Korea’s Dong-A Ilbo newspaper reports, citing unidentified intelligence sources. (BB)

- UK PM May's Conservative Party avoided a wipeout in London local elections and eked out gains in Brexit-supporting regions elsewhere, early results showed, although her Labour opponents gained ground in the capital. (Reuters)

- Today’s eco calendar contains US payrolls, unemployment rate and average hourly earnings. EMU retail sales and the final services PMI feature on the agenda as well. Several ECB & Fed governors speak

Currencies: Dollar Probably Needs Excellent Payrolls To Extend Rebound

Payrolls strong enough for further USD gains?

EUR/USD faced conflicting signals yesterday. The dollar rally slowed as the Fed suggested that it won’t immediately react to a limited overshoot of the inflation target. This blocked the rise in US yields and the USD. On the euro side of the story, EMU April inflation again missed the consensus by quite a big margin (1.2% Y/Y). Both conflicting stories kept EUR/USD in a tight range mostly in the upper half of the 1.19 big figure. Uncertainty the high level US-Chinese trade talks caused some caution in global risk sentiment. The impact on the major FX cross rates stayed modest but the yen developed a tentative rebound. USD/JPY drifted south off the 110 area. EUR/JPY showed a sharp intraday setback.

Overnight, Asian equities continued the recent lacklustre performance. Investors are monitoring the China-US trade talks and are looking forward to the US payrolls. The (trade weighted) USD is holding slightly off the recent peak. EUR/USD hovers just below 1.20. USD/JPY struggles not to fall below the 1.09 handle. The Reserve bank of Australia sees good growth in 2018/2019 (3 % +), but expects inflation to stay in the lower part of the 2-3% target band. The Aussie dollar rebounded a few more ticks and trades again in the AUD/USD 75.50 area.

Today, the final EMU services PMI’s will be published. Markets will look out whether the recent easing in the EMU economic momentum might bottom. However, the focus is on the US payrolls report. US April job growth is expected to return to its recent trend close to 200k. Earnings growth (0.2% M/M and 2.7% Y/Y expected) will also be key for the market reaction. After Wednesday’s balanced Fed communication, we assume that the dollar needs a positive surprise to extend its recent rally. In that case, we look out whether EUR/USD will be able to break the 1.1915/36 support area. Given yesterday’s post-Fed reaction, this might not be that easy. Of course there is still the euro side of the story. For USD/JPY the 110 area is the next topside reference.

Yesterday, sterling traded with a negative bias. The political stalemate on Brexit within the Conservative party remains an underlying negative for sterling. The UK services PMI also disappointed, indicating ongoing slow growth the start of Q2 and further reducing the chances of a May BoE rate hike. Today, there are no important data in the UK. EUR/GBP tries to sustain north of 0.88. Negative news might push the pair higher to the 0.8868/0.9033 resistance ahead of next week’s BoE meeting.

D: will payrolls be strong enough for USD to rally below 1.1936/15 support?

Markets Focusing On China/US Trade Talks, Upcoming US Employment Data

General Trend:

- Asian equities trade generally lower, in line with US session; Japan closed for holiday

- Banks in focus: HSBC and Australia’s Macquarie report better than expected earnings

- China/US trade talks are continuing

- Reserve Bank of Australia (RBA) sees ‘solid’ Q1 growth, notes impact of higher funding costs on banks

- China April Caixin Services PMI beats ests

- Philippines Central Bank Chief says closer to rate hike than before; April CPI remained above target

- Malaysia exports to China declined again in March

- South Korea bonds decline

- South Korea said the US refuted an earlier report which said that US President Trump was said to have ordered the Pentagon to consider cutting troops in South Korea.

- China Dalian iron ore futures are now open to foreign traders as of today

- Next week, Japan PM Abe and China Premier Li are expected to hold a summit in Tokyo

Headlines/Economic Data

Australia/New Zealand

- ASX 200 opened flat, closed -0.5%

- (AU) RESERVE BANK OF AUSTRALIA (RBA) QUARTERLY STATEMENT ON MONETARY POLICY (SOMP): RAISES DEC 2018 CORE INFLATION FORECAST BY 25BPS TO 2.00%; If the economy improves as expected, higher rates likely to be appropriate at some point.

- (AU) Australia sells A$600M v A$600M indicated in 2.75% Nov 2029 bonds, avg yield 2.8181% v 2.8600% prior, bid to cover: 3.57x

- (NZ) RBNZ and FMA to seek assurances that New Zealand banks are behaving ethically

China/Hong Kong

- Shanghai Composite opened -0.3%, Hang Seng flat

- (CN) CHINA APR CAIXIN PMI SERVICES: 52.9 V 52.3E; COMPOSITE: 52.3 V 51.8 PRIOR

- (CN) US Treasury Sec Mnuchin comments from China: US and China are having very good conversation

- (CN) China said to expand checks of certain US fruit imports - financial press

- CN) China Banking Insurance Commission Chairman Guo Shuqing said domestic economic risks remain controllable - Chinese Press

- (CN) For the week, PBoC drained a net of CNY110B in open market operations v CNY270B net drain w/w

- (CN) China PBoC sets yuan reference rate: 6.3521 v 6.3732 prior

- (CN) The Governor of China Hainan pledged to limit property speculation – US financial press

- (HK) Hong Kong Apr PMI: 49.1 v 50.6 prior (1.5 year low)

- (HK) HKMA Chan said the Hong Kong dollar (HKD) may again decline to weak end of trading band – Local Media

- (HK) Hong Kong Exchange CEO: Sees substantial autumn for IPOs in Hong Kong

Japan

- Nikkei closed for holiday

- (JP) Japan, China and South Korea Finance leaders meeting statement: Notes risks posed by rising trade protectionism

- (CN) China: Premier Li’s visit to Japan to promote bilateral ties

Korea

- Kospi opened flat

- Samsung Electronics resumes trading after stock split

- (KR) US President Trump said to order Pentagon to consider cutting troops in South Korea - NYT

- (KR) North Korea said to agree to full denuclearization by 2020 - South Korean Press [Reminder: On Apr 18th Reports circulated that the US was seeking to denuclearize North Korea by 2020]

- (KR) Insurance companies in South Korea said to delay foreign investments due to rise in hedging costs – US financial press

- (KR) South Korea Apr Foreign Reserves: $398.4B (record high) v $396.8B prior

- (KR) South Korea Mar BoP Current Account Balance: $5.2B v $4.0B prior; BoP Goods Balance: $9.9B v $6.0B prior

Other

- (PH) Philippines Apr CPI M/M: 0.5% v 0.4%e; Y/Y: 4.5% v 4.5%e

- (SG) Singapore Apr PMI: 55.6 v 53.7 prior

- (TW) Manufacturers of capacitors in Taiwan may raise prices following move by Aihua Group – Taiwanese Press

North America

- US equity markets closed mostly lower: Dow flat, S&P500 -0.2%, Nasdaq -0.2%, Russell 2000 -0.5%

- S&P500 -0.9%, Financials -0.9%

- (US) White House economist Calabria: First day of talks with China have been pretty positive; -Will ask China to lower tariff rates to match US levels; has discreetly given China a list of asks

- Apple [AAPL]: Buffett's Berkshire said to have purchased 75M Apple shares in Q1 - CNBC

Europe

- (UK) UK may not be able to leave customs union until 2023; Civil servants briefing ministers this week told them that the UK may take 5 years to implement the technological Irish border fix ('max-fac') that cabinet Brexiters favor. - UK press

- (UK) UK PM May Conservative Party said to hold on to overall control of London’s Wandsworth council in local government elections – financial press

- (UK) NIESR cuts UK 2018 growth forecast to 1.5% (from 1.9% prior forecast) - Telegraph

- Axa [CS.FR]: Reports Q1 Rev €30.8B v €31.6B y/y

Levels as of 02:00ET

- Hang Seng -0.5%; Shanghai Composite -0.1%; Kospi -0.6%

- Equity Futures: S&P500 flat; Nasdaq100 -0.1%, Dax -0.1%; FTSE100 -0.3%

- EUR 1.1979-1.1996 ; JPY 108.93-109.25 ; AUD 0.7526-0.7562 ;NZD 0.7021-0.7053

- Jun Gold +0.1% at $1,314/oz; May Crude Oil +0.2% at $68.53/brl; May Copper +0.4% at $3.104/lb

Eurozone PMI composite at 55.1. Marked, broadbased fading of growth spurt

Eurozone PMI services was finalized at 54.7 in April, revised down from 55.0. Prior month's reading was 54.9.

Eurozone PMI composite was finalized at 55.1, revised down from 55.2. Prior month's reading was 55.2.

German PMI composite dropped to 19-month low at 54.6. Italy PMI composite dropped to 15-month low at 52.9.

On the other hand, France PMI composite rose to 2 month high at 56.9. Ireland PMI composite rose to 3 month high at 57.6.

Quote from Chris Williamson, Chief Business Economist at IHS:

Quote from Chris Williamson, Chief Business Economist at IHS:

"The final PMI numbers confirm the marked, broadbased fading of the eurozone's growth spurt so far this year. The headline index has fallen from an eleven-and-a-half year peak in January to a 15- month low in April. Despite the drop, the PMI is not yet at a worryingly low level, but the survey details hint at further easing in the coming months.

"While the expansion signalled by April's PMI is disappointing relative to the elevated levels seen at the start of the year, the survey remains indicative of the eurozone economy growing at a robust quarterly rate of approximately 0.5-0.6%. Employment growth is also still booming, with the rate of job creation in the service sector at its highest for over a decade.

"Employment is a lagging indicator, however, and two reliable leading indicators have turned down, suggesting that both output and hiring trends will weaken further, at least into May. First, backlogs of uncompleted orders grew at the slowest rate for eight months. Second, companies' expectations about future output hit a five-month low. Any further deterioration could herald new concerns among policymakers regarding the economic outlook."

US “detailed list of asks” to China leaked

While there is no official communications regarding the so-called trade "negotiation" between US and China, WSJ reported the "detailed list of asks" that the US delegates gave to China during the meeting in Beijing.

In short, US asks China to:

- narrow trade surplus by US 200B by 2020

- reduce trade imbalance immediately

- halt subsidies for advanced tech

- cut tariffs on all products to levels no higher than that of US

- refrain from targeting US farmers and agricultural products

- refrain from retaliating against US restrictions on investments from China

It's unsure what the US has offered on the table.

When you ask for something without offering anything, that's not really negotiation. From there, it's unsure how seriously the US is taking the so called trade negotiation.

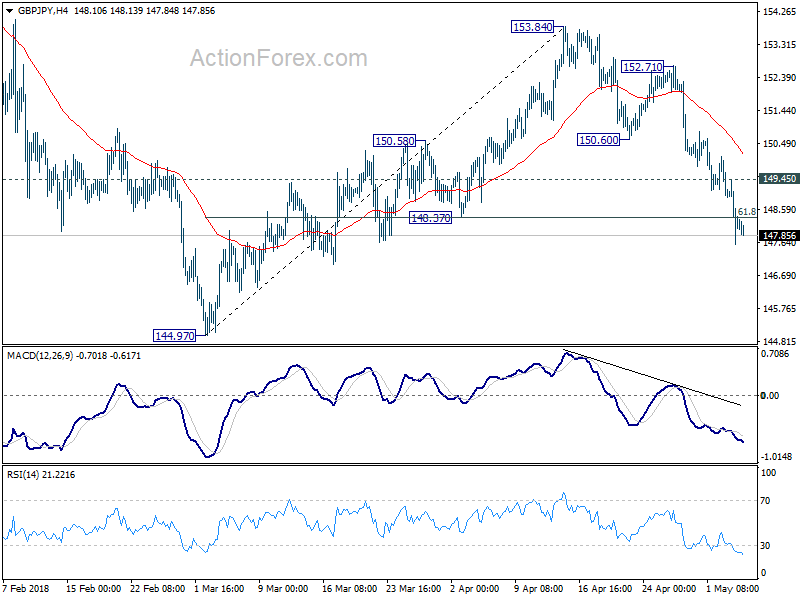

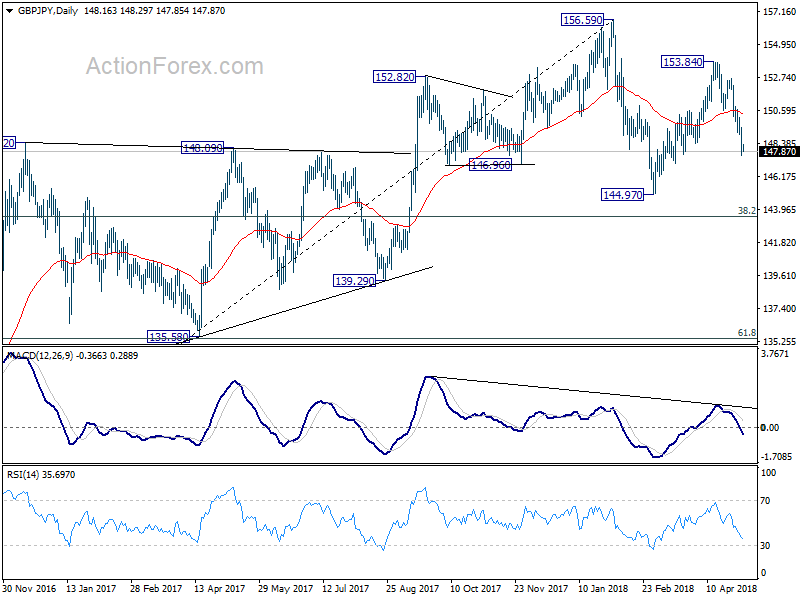

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.39; (P) 148.42; (R1) 149.26; More...

Intraday bias in GBP/JPY remains on the downside for the moment. With 148.37 support taken out, fall from 153.84 should extend to 144.97 low first. Break there will target 143.51 fibonacci level. On the upside, above 149.45 minor resistance will turn intraday bias neutral and bring recovery. But upside should be limited well below 152.71 resistance to bring another decline.

In the bigger picture, price actions from 156.59 are viewed as a corrective pattern. For now, we'd expect at least one more fall for 38.2% retracement of 122.36 to 156.59 at 143.51 before the consolidation completed. Though, firm break of 156.59 will resume whole up trend from 122.36 (2016 low) to 50% retracement of 195.86 (2015high) to 122.36 at 159.11 next.

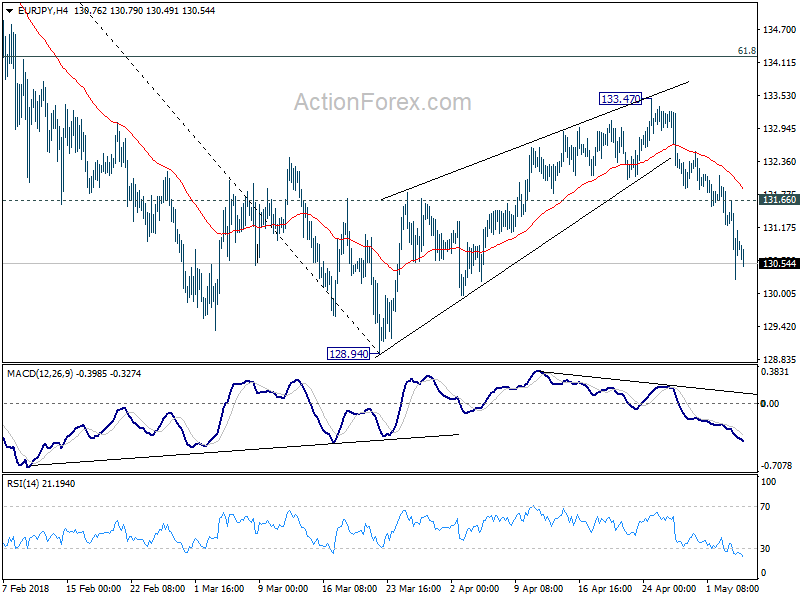

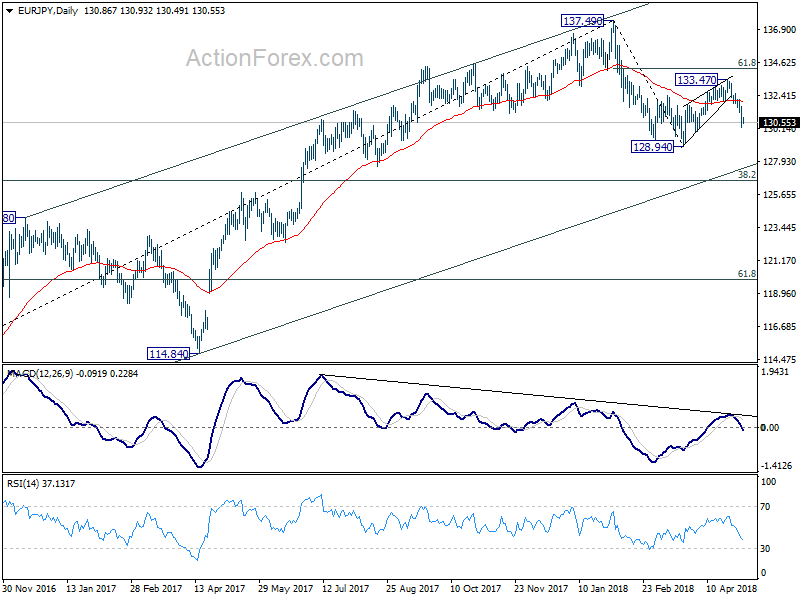

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.23; (P) 130.94; (R1) 131.63; More....

Intraday bias in EUR/JPY remains on the downside as fall from 133.47 should target 128.94 low. Break there will resume whole fall from 137.49 and target 126.61 fibonacci level next. On the upside, above 131.66 minor resistance will turn intraday bias neutral first. But recovery should be limited well below 133.47 resistance to bring another fall.

In the bigger picture, price action from 137.49 medium term top are developing into a corrective pattern. The first leg has completed at 128.94. The second leg might be finished at 133.47 or it might extend. But after all, we'd expect another decline through 128.94 to 38.2% retracement of 109.03 to 137.49 at 126.61 before completing the correction.

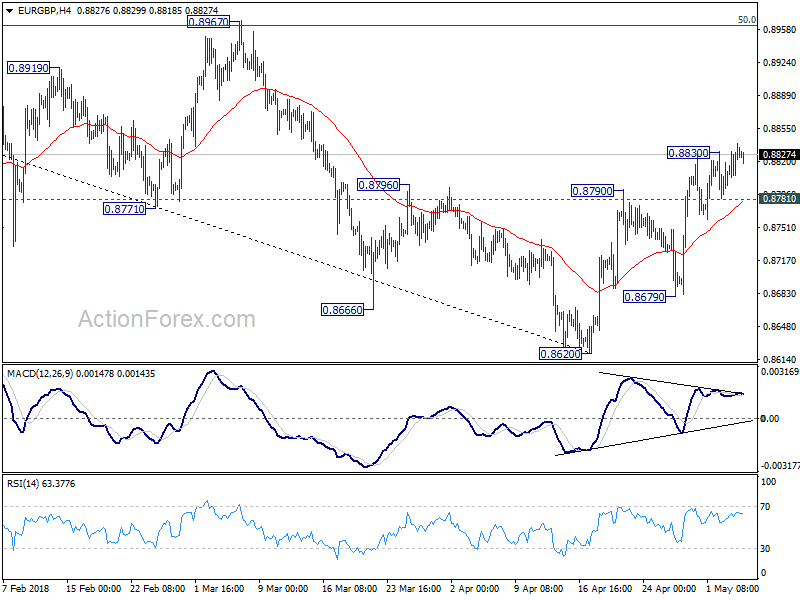

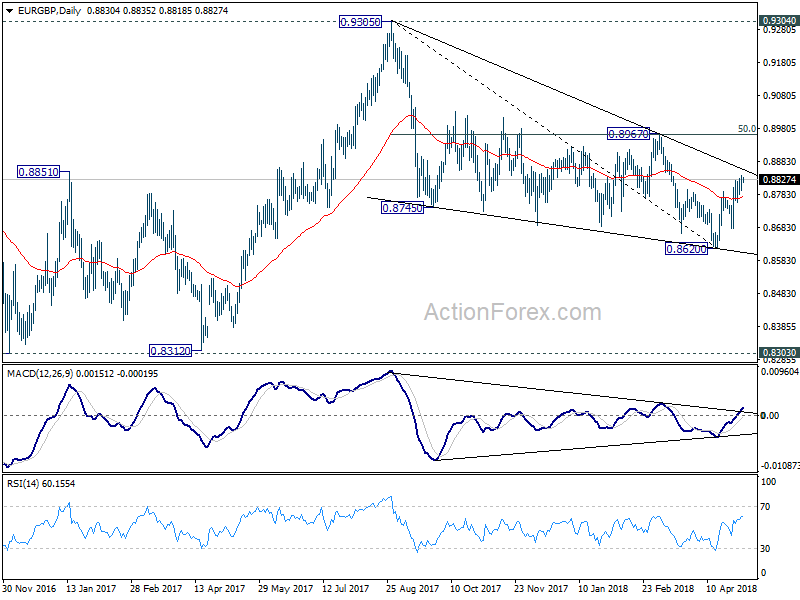

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8805; (P) 0.8823; (R1) 0.8847; More...

Intraday bias in EUR/GBP is back on the upside as rebound from 0.8620 resumes. Further rise would be seen to 0.8967 cluster resistance next (50% retracement of 0.9305 to 0.8620 at 0.8963). Firm break there will confirm neat term reversal. On the downside, below 0.8781 minor support will turn focus back to 0.8679 support. Break there will suggests that larger decline from 0.9305 is resuming.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

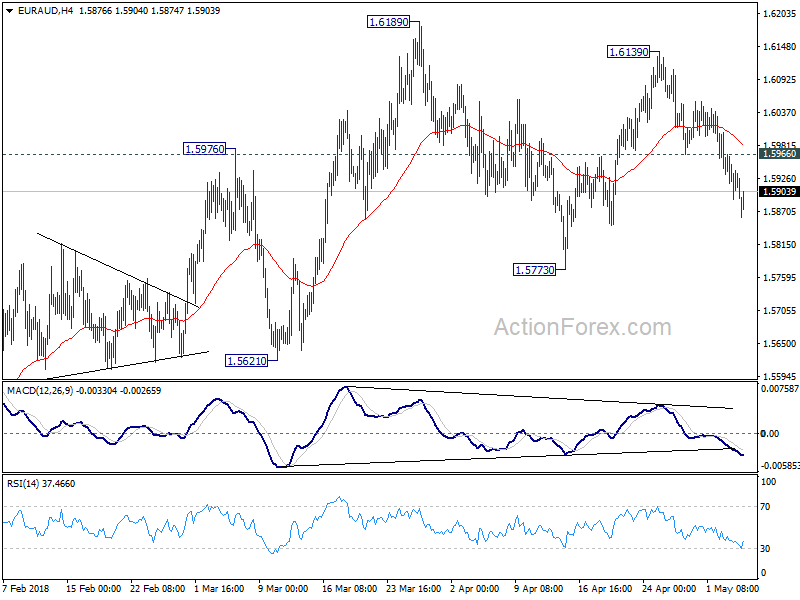

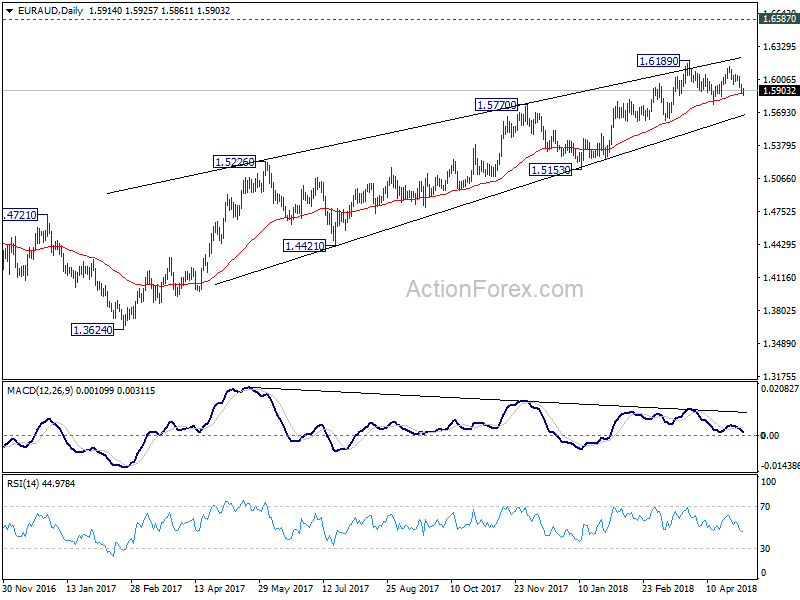

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5881; (P) 1.5924; (R1) 1.5956; More....

Intraday bias in EUR/AUD remains on the downside for 1.5773 support and possibly below. Still, price actions from 1.6189 are seen as a consolidation pattern. Hence, downside should be contained above 1.5621 to bring rise resumption. On the upside, above 1.5966 support turned resistance will turn bias to the upside for 1.6139 and then 1.6189 high.

In the bigger picture, while there is bearish divergence condition in daily MACD, there is no clear sign of reversal yet. EUR/AUD also drew strong support from 55 day EMA and rebounded. Current rally from 1.3624 could still extend to 1.6587 key resistance (2015 high). Nonetheless, we'd expect further loss of upside momentum, and strong resistance from 1.6587 to limit upside and bring reversal. On the downside, sustained break of 1.5621 support should confirm reversal and turn outlook bearish for 1.5153 support and below.

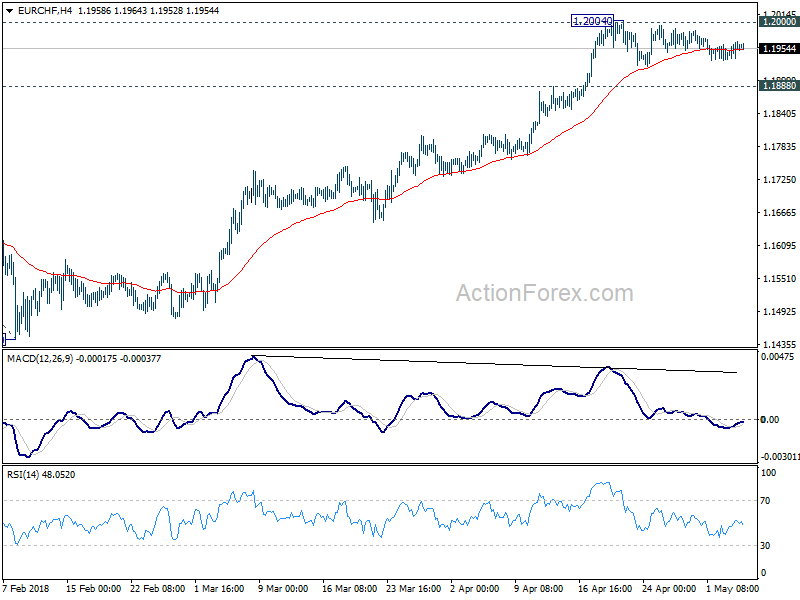

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1940; (P) 1.1954; (R1) 1.1974; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 1.2004 is extending. As long as 1.1888 minor support holds, further rise is expected. On the upside side, decisive break of 1.2 will pave the way to 61.8% projection of 1.0629 to 1.1832 from 1.1445 at 1.2188. However, consider bearish divergence condition in 4 hour MACD, break of 1.1888 will indicate short term topping. In that case, deeper pull back would be seen back to 1.1445/1832 support zone.

In the bigger picture, long term up trend in EUR/CHF is still in progress. Prior SNB imposed floor at 1.2003 was already met but there is no sign of reversal yet. As long as 1.1445 support holds, we'd expect the up trend to extend to 2013 high at 1.2649 next.