Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.61; (P) 109.82; (R1) 110.05; More...

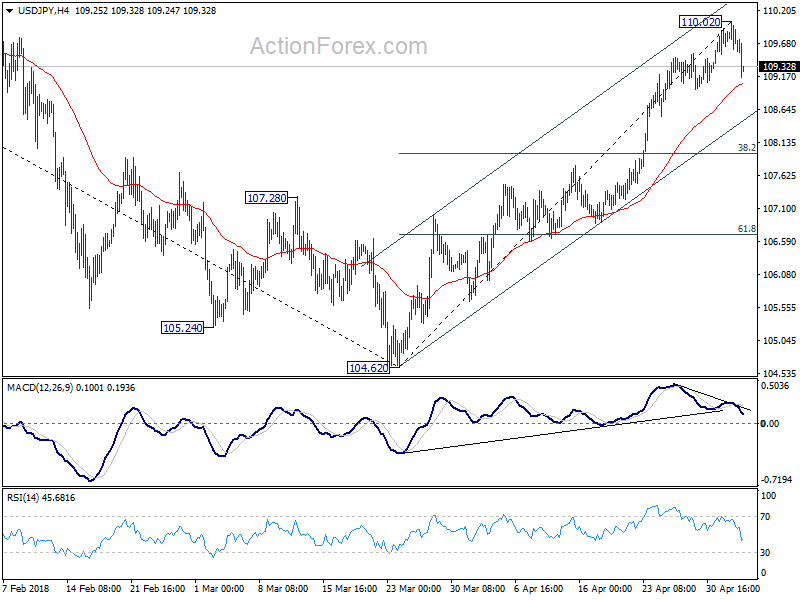

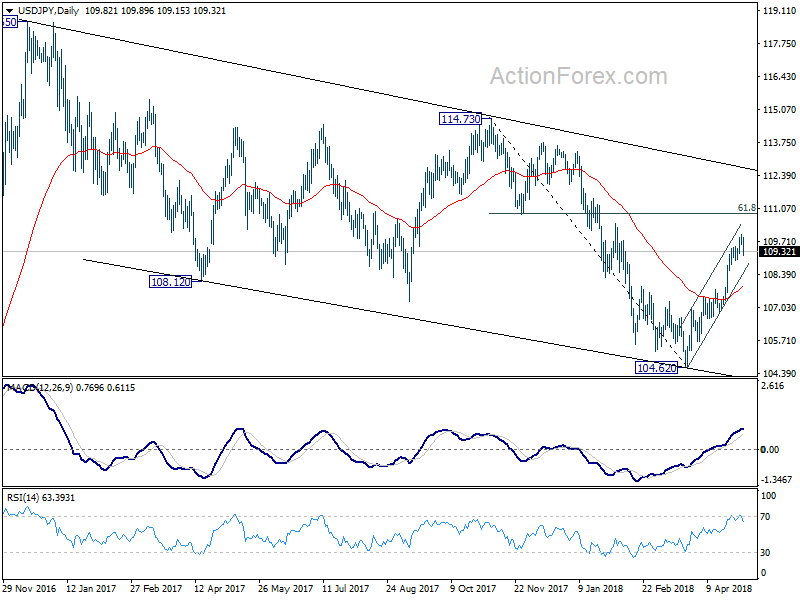

USD/JPY's sharp decline and break of 109.50 minor support indicates short term topping at 110.02, on bearish divergence condition in 4 hour MACD. Intraday bias is turned to the downside for deeper retreat to near term channel support (now at 108.48). But we'd expect strong support from 38.2% retracement of 104.62 to 110.02 at 107.95 to contain downside and bring rebound. Break of 110.02 will resume the rise from 104.62 to t 61.8% retracement of 114.73 to 104.62 at 110.86 next.

In the bigger picture, break of 108.12 support turned resistance now suggests that corrective fall from 118.65 (2016 high) has completed with three waves down to 104.62. And, rise from 98.97 (2016 low) could be resuming. Focus is back on 114.73 resistance and break there will pave the way to 118.65 and above. This will now be the preferred case as long as USD/JPY stays above 55 day EMA (now at 107.97).

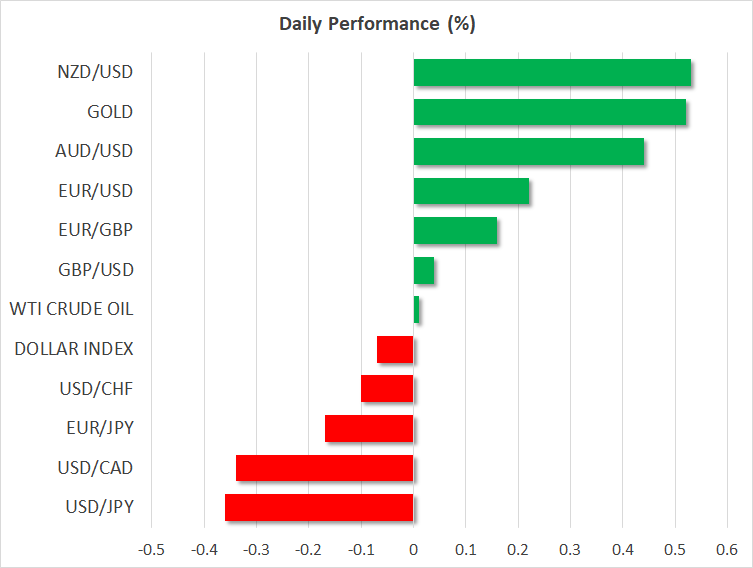

Yen Stealing the Show as Dollar Consolidates, Euro and Sterling Tumble on Weak Data

Dollar is trading with a soft tone today as traders are cautiously waiting for tomorrow's job report. And just like how it was in recent months, wage growth will be more important than the headline number. For now, Yen and New Zealand Dollar have stolen the spotlight as both surge strongly. In particular, Yen is taking advantage of data disappointment in Eurozone and UK and jumps sharply higher against Euro and Sterling. Risk aversion could also be a factor as US stocks are set to open lower. Gold also manages to bounce back to 1315, partly thanks to Dollar's consolidation.

US trade deficit narrowed in general, but widened against China

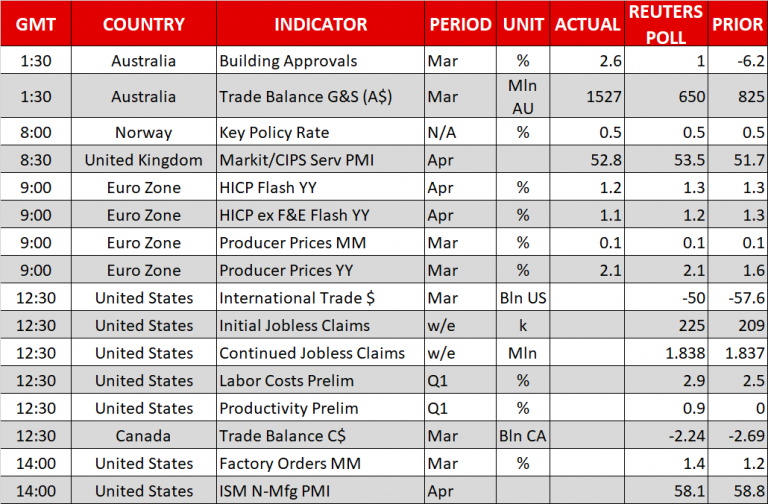

US trade deficit narrowed to USD -49.0B in March, down USD -8.8B from USD -57.7B in February. That's also the lowest monthly deficit in six months. March exports rose USD 4.2b to USD 208.5b. Imports dropped USD 4.6b to USD 257.5B.

Trade deficit with China, however, rose USD 0.7B to USD 35.4B in March. Exports to China rose USD 1.6B to USD 12.4B. But imports increased more by USD 2.3B to USD 47.7B. Also, it should be noted that year-to-date, trade deficit widened USD -25.5B, or up 18.5%, from the same period in 2017.

Initial jobless claims rose 2k to 211k in the week ended April 28, below expectation of 225k. The four week moving average dropped 7.75k to 221.5k. Continuing claims dropped -77k to 1.756m in the week ended April 28, lowest since December 8, 1973.

Also released, US nonfarm productivity rose 0.7% in Q1 while unit labor costs rose 2.7%. Canada trade deficit widened to CAD -4.1B in March.

UK PMIs take BoE fingers firmly off rate hike trigger

UK PMI services rose to 52.8 in April, up from 51.7 but missed consensus of 53.5. Markit's key findings are not too encouraging for the UK. It noted that business activity rises at subdued pace in April. There is the weakest upturn in employment since March 2017 and inflationary pressures are moderate.

Chris Williamson, Chief Business Economist at IHS Markit, noted that the three PMI surveys collectively showed "only a muted rebound in business activity" after the heavy snow in March. And failing to regain February's growth pace suggested deterioration in underlying performance. The surveys pointed to GDP growth at around 2% at the start of Q2. And, "the disappointing services data will add to expectations that the MPC will take its finger firmly off the rate hike trigger. Any further slowing will also raise questions as to whether the November rate hike may have been ill-timed."

Eurozone CPI missed, ECB Praet sounded cautious

Eurozone flash CPI slowed to 1.2% yoy in April, down from 1.3% yoy and missed expectation of 1.3% yoy. CPI core performed even worse, dropped to 0.7% yoy, down from 1.0% yoy and missed expectation of 0.9% yoy. ECB chief economist Peter Praet said two hours after the CPI release that while the central bank cannot yet declare "mission accomplished" on inflation, "we have made substantial progress on the path towards a sustained adjustment in inflation."

But Praet also acknowledged that "the latest economic data and survey results have generally surprised to the downside, suggesting some loss of momentum in economic activity." But he pointed out that "temporary factors may also be at work". He emphasized that "we will also need to monitor whether, and if so, to what extent, these developments reflect a more durable softening in demand."

Australian Dollar lifted by large trade surplus and surge in building approvals

AUD trades broadly higher today as supported by solid economic data. Australia trade surplus came in at AUD 1.53B in March, widened from AUD 1.35B in February. That's also much larger than expectation of AUD 0.68B. Exports jumped 1% to AUD 34.84B, with strong 8% growth in n non-monetary gold to AUD 131m. Imports rose 1% to AUD 33.31B,. Non-monetary gold imports jumped 28% to AUD 232m.

Building approvals rose 2.6% mom in Mach, much higher than expectation of 1.0% mom. Justin Lokhorst, Director of Construction Statistics at the ABS noted that "the strength in the total dwellings series is being driven by approvals for private sector houses, which have now risen for 13 consecutive months." And, "private sector house approvals are now at their highest level since 2003, in trend terms."

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.61; (P) 109.82; (R1) 110.05; More...

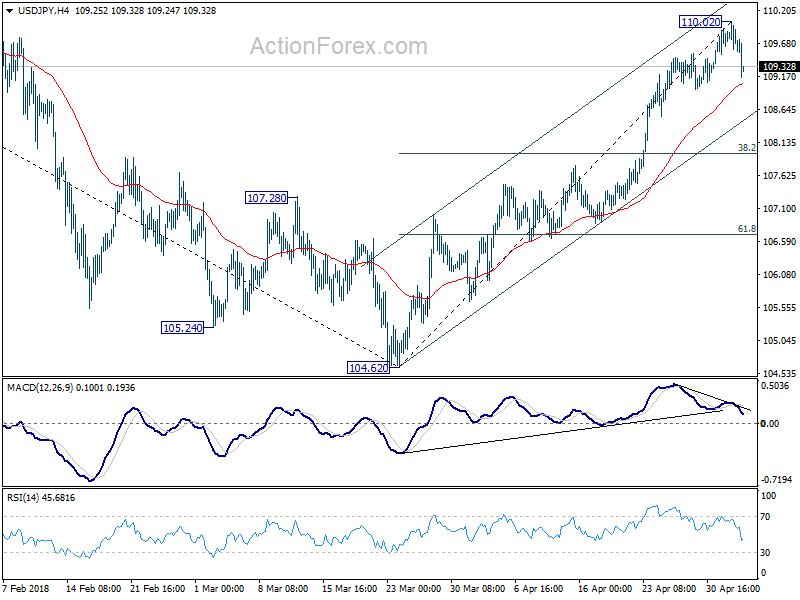

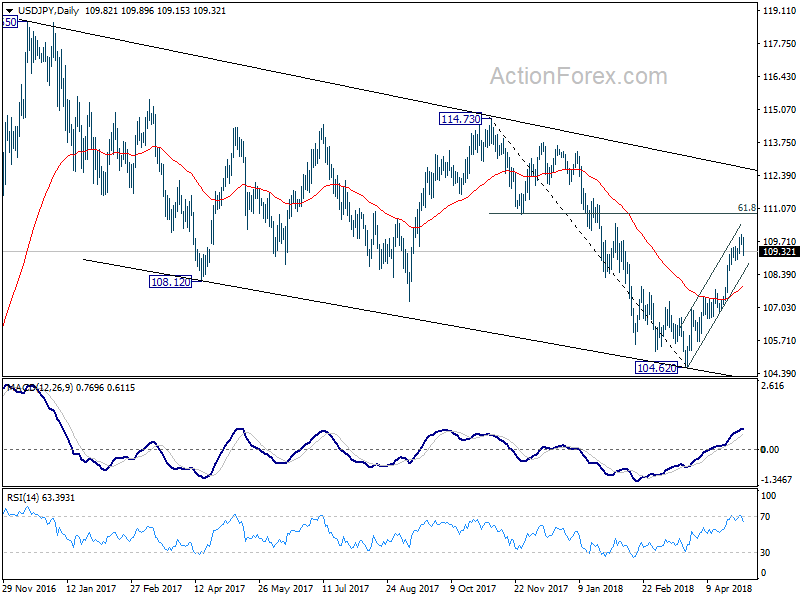

USD/JPY's sharp decline and break of 109.50 minor support indicates short term topping at 110.02, on bearish divergence condition in 4 hour MACD. Intraday bias is turned to the downside for deeper retreat to near term channel support (now at 108.48). But we'd expect strong support from 38.2% retracement of 104.62 to 110.02 at 107.95 to contain downside and bring rebound. Break of 110.02 will resume the rise from 104.62 to t 61.8% retracement of 114.73 to 104.62 at 110.86 next.

In the bigger picture, break of 108.12 support turned resistance now suggests that corrective fall from 118.65 (2016 high) has completed with three waves down to 104.62. And, rise from 98.97 (2016 low) could be resuming. Focus is back on 114.73 resistance and break there will pave the way to 118.65 and above. This will now be the preferred case as long as USD/JPY stays above 55 day EMA (now at 107.97).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance Mar | 1.53B | 0.68B | 0.83B | 1.35B |

| 01:30 | AUD | Building Approvals M/M Mar | 2.60% | 1.00% | -6.20% | -4.20% |

| 08:30 | GBP | Services PMI Apr | 52.8 | 53.5 | 51.7 | |

| 09:00 | EUR | Eurozone PPI M/M Mar | 0.10% | 0.10% | 0.10% | |

| 09:00 | EUR | Eurozone PPI Y/Y Mar | 2.10% | 2.10% | 1.60% | |

| 09:00 | EUR | Eurozone CPI Estimate Y/Y Apr | 1.20% | 1.30% | 1.30% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr A | 0.70% | 0.90% | 1.00% | |

| 09:00 | EUR | European Commission Economic Forecasts | ||||

| 11:30 | USD | Challenger Job Cuts Y/Y Apr | -1.40% | 39.40% | ||

| 12:30 | CAD | International Merchandise Trade (CAD) Mar | -4.1B | -2.0B | -2.7B | -2.93B |

| 12:30 | USD | Nonfarm Productivity Q1 P | 0.70% | 1.00% | 0.00% | |

| 12:30 | USD | Unit Labor Costs Q1 P | 2.70% | 3.00% | 2.50% | |

| 12:30 | USD | Initial Jobless Claims (APR 28) | 211K | 225K | 209K | |

| 12:30 | USD | Trade Balance Mar | -49.0B | -55.6B | -57.6B | -57.7B |

| 13:45 | USD | US Services PMI Apr F | 54.4 | 54.4 | ||

| 14:00 | USD | ISM Non-Manufacturing/Services Composite Apr | 58.1 | 58.8 | ||

| 14:00 | USD | Factory Orders Mar | 1.40% | 1.20% | ||

| 14:30 | USD | Natural Gas Storage | -18B |

US trade deficit narrowed in March, continuing jobless claims dropped to lowest since 1973

USD continues to trade with a soft tone in early US session. But it's staying in yesterday's range except versus JPY and NZD, which are both strong today.

US trade deficit narrowed to USD -49.0B in March, down USD -8.8B from USD -57.7B in February. That's also the lowest monthly deficit in six months. March exports rose USD 4.2b to USD 208.5b. Imports dropped USD 4.6b to USD 257.5B.

Trade deficit with China, however, rose USD 0.7B to USD 35.4B in March. Exports to China rose USD 1.6B to USD 12.4B. But imports increased more by USD 2.3B to USD 47.7B.

Also, it should be noted that year-to-date, trade deficit widened USD -25.5B, or 18.5%, from the same period in 2017.

Initial jobless claims rose 2k to 211k in the week ended April 28, below expectation of 225k. The four week moving average dropped 7.75k to 221.5k. Continuing claims dropped -77k to 1.756m in the week ended April 28, lowest since December 8, 1973.

Also released, US nonfarm productivity rose 0.7% in Q1 while unit labor costs rose 2.7%.

Canada trade deficit widened to CAD -4.1B in March.

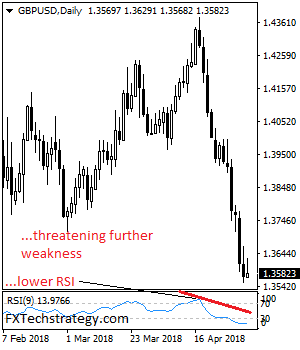

GBPUSD: Remains Weak And Vulnerable On Bear Pressure

GBPUSD: The pair faces further downside pressure. Support lies at the 1.3550 level where a break will turn attention to the 1.3500 level. Further down, support lies at the 1.3450 level. Below here will set the stage for more weakness towards the 1.3400 level. Conversely, resistance stands at the 1.3650 levels with a turn above here allowing more strength to build up towards the 1.3700 level. Further out, resistance resides at the 1.3750 level followed by the 1.3800 level. On the whole, GBPUSD remains biased to downside short term.

DAX Dips as Eurozone CPI Misses Forecast

The DAX index has lost ground in the Wednesday session. Currently, the DAX is at 12,753 points, down 0.37% on the day. On the release front, Eurozone CPI Flash Estimate dropped to 1.2%, shy of the estimate of 1.3%. Core CPI Flash Estimate followed a similar trend, dipping to 0.7%, short of the forecast of 0.9%. On Friday, Germany and the eurozone release Services PMI and the eurozone will publish retail sales.

Eurozone annual inflation is expected to dip to 1.2%, down from 1.3% in March, according to Eurostat. As well, Core annual inflation is forecast to edge lower to 0.9%, after three straight readings of 1.0%. These readings point to sluggish inflation, well short of the ECB target of around 2 percent. The weak inflation numbers are not surprising, as eurozone growth has softened in the first quarter. This is also reflected in manufacturing data, as German and eurozone manufacturing PMIs dropped for a fourth consecutive month.

The Federal Reserve maintained the benchmark rate at a target of 1.5% to 1.75% on Wednesday. The markets were looking for some discussion about inflation and were not disappointed. The rate statement was significant, with policymakers noting that “overall inflation has moved closer to 2 percent”. This was more hawkish than the March statement, in which the rate statement said that inflation indicators “have continued to run below 2 percent”. With inflation moving closer to the Fed target of 2 percent, there is a stronger likelihood that the Fed will upgrade its rate projection from three to four hikes in 2018. The odds of a fourth rate hike this year stand at 50%. The Fed rate statement also noted that “market-based measures of inflation compensation remain low”, a reference to soft wage growth, which is at 2.7%, lower than the 3% rate that the Fed would like to see.

Into US session: JPY surges against Europeans

Yen surges broadly as markets enter into US session. The rally is particularly steep against European majors. Both EUR and GBP are troubled by weaker than expected data. The limited movement in EUR/USD and GBP/USD is just a reflection that USD is consolidating after recent gains. And USD is awaiting tomorrow's NFP. They are not indications that EUR and GBP are not affected by the releases.

The JPY Action Bias table show that for now, only AUD and NZD escape from JPY's intraday pressure. For short to medium term, European majors are suffering.

EURJPY 6H Action Bias chart shows clear persistent downside momentum in the cross ever since breaking 132.5 handle. It's on course for 128.94 low.

Similarly, GBPJPY 6H Action Bias chart also displays persistent downside momentum after taking out 151. 144.97 will be the next target after taking out 148.37 support.

Euro, Pound Lose Momentum After Data Misses

Here are the latest developments in global markets:

FOREX: The US dollar continued to move lower during the early European session, deviating further below the 3-month high of 110.02 versus the yen reached during Wednesday’s European trading. Specifically, dollar/yen retreated to 109.49 (-0.32%), a day after the FOMC left interest rates unchanged. The accompanying statement acknowledged that inflation is close to target, signaling that policymakers would accept inflation surpassing the 2.0% target. However, a drop of a statement highlighting the continued expansion of the economy made the statement look somewhat dovish, pushing the dollar lower. With the Fed’s meeting out of the way now, the focus is shifting to US jobs data due on Friday for further indication of the strength of the economy and inflationary pressures. The dollar index, which gauges the greenback’s strength versus six major currencies, eased by 0.04% to 92.47 after hitting a 4-month high of 92.63 on Wednesday. Pound/dollar edged down from 1.3628 to 1.3593 in the wake of worse-than-expected UK Services PMI, remaining 0.03% up on the day. Euro/dollar pared some of its earlier gains after Eurozone’s CPI figures appeared slightly weaker than expected, slipping from 1.2000 to 1.1980 (+0.25%). The antipodean currencies erased yesterday’s losses, with aussie/dollar and kiwi/dollar advancing by 0.53% and 0.59% respectively. Dollar/loonie was on the back foot today but remained within a narrow range over the last daily sessions, trading at 1.2929 (-0.40%). The Norwegian krone surged against the dollar and the euro after Norway’s central bank kept rates steady as expected, reiterating that the first rate hike would come after the summer.

STOCKS: European stocks were in the red at 1000 GMT on Thursday as the euro managed to bounce up. Disappointing earnings releases weighed on equities as well. The benchmark European STOXX 600 dived by 0.27%, while the blue-chip Euro STOXX 50 was down by 0.32%. The German DAX 30 fell by 0.29% after a strong bullish day. The French CAC 40 and the Spanish IBEX 35 were down by 0.27%, while the British FTSE 100 declined by 0.07%. In Asia, Japan’s Nikkei 225 and Topix closed marginally lower by 0.16% and 0.15% respectively. In the US, even though the S&P, Dow Jones, and the Nasdaq all retreated yesterday, futures tracking these indices are currently in the green, pointing to a higher open today.

COMMODITIES: Oil prices were moving higher as speculation that the US could reimpose sanctions to Iran overshadowed fears over a rising US production. West Texas Intermediate crude rose by 0.29% to $68.18 a barrel and Brent jumped by 0.20% to $73.59 a barrel. Gold price gained for the second session in a row, last seen at $1,311.80 per ounce (+0.56%) ahead of US-China trade talks.

Day ahead: US trade balance & ISM Services PMI feature on the calendar

Investors will keep a close eye on the dollar and the loonie later in the day as the US and Canada are scheduled to update a number of economic measures.

At 1230 GMT, the US international trade deficit for the month of March is expected to narrow to $50.0 billion after reaching a 9 ½-year high of $57.6bn in the previous month. Investors will also monitor the bilateral trade figures given Trump’s dissatisfaction on trade deals particularly with the EU, Japan, and China. Canada and Mexico, on the other hand, are said to be within reach of an agreement with the US on NAFTA, with the deal probably coming before the Mexican presidential elections in July and the US mid-term elections in November. Recall that Trump decided to extend import tariff negotiations on steel and aluminum until June 1 after temporary exceptions expired on May 1, signaling that maybe a global trade war is not a desirable option. Moreover, the US trade delegation led by the Treasury Secretary Steven Mnuchin has arrived in China on Thursday for two days to start two-day tariff negotiation with the Chinese team.

At the same time, the US Department of Labor will issue its weekly report on initial jobless claims, with analysts anticipating the number of people applying for unemployment benefits for the first time to rise to 225k in the week ending April 27 compared to 209k seen in the preceding week. Labor costs and productivity for the first quarter will be published along with the above data, while Canadian trade numbers will be also under review at 1230 GMT.

Later, at 1400 GMT, the US will see the release of factory orders for the month of March and April’s ISM services PMI, with the former anticipated to rise by 1.4% m/m, faster than the 1.2% expansion in February, and the latter projected to slow down by 0.7 points to 58 but remain above the growth threshold of 50.

In politics, local government elections are taking place in the UK today. The outcome could work against the UK Prime Minister, Theresa May, as the markets believe that the opposition parties could see their council seats increasing, especially in London, given May’s controversial Brexit plans. A defeat for May could shed a dark light on her leadership and her efforts to achieve a clear exit from the EU’s customs union. The first results will arrive by midnight. No local votes will take place in Scotland, Wales and Northern Ireland.

In equity markets, the earnings season continues, with Activision Blizzard and Xerox being among companies releasing quarterly results on Thursday; both corporations will be reporting after today’s US market close.

Turning to public appearances, ECB Vice President Vitor Constancio and ECB Executive Board member Benoit Coeure will be talking about fostering a banking and capital markets union within the eurozone at 1200 GMT and 1230 GMT respectively.

Pound Softens On PMI Disappointment, Oil Shaky

Investors who were looking for a quick opportunity to attack the Pound were given the green light on Thursday after Britain’s service sector rebounded less than expected last month.

The UK Services PMI rose to 52.8 in April, up from March’s score of 51.7 but below the 53.5 market forecast. The sluggish services data is likely to weigh on sentiment and fuel concerns over economic growth remaining subdued. Expectations over the Bank of England raising interest rates next week have deteriorated further following today’s disappointing PMI report with the GBPUSD dipping towards 1.3573 at time of writing. Sterling could be poised for further pain as the combination of Brexit uncertainty and fading UK rate hike expectations expose the currency to downside risks. The increasing divergence in monetary policy between the BoE and Fed could instil bears with enough inspiration to send the GBPUSD to levels not seen since December 2017 - around 1.3400.

From a technical standpoint, the GBPUSD remains heavily bearish on the daily charts. There have been consistently lower lows and lower highs while the MACD has crossed to the downside. The breakdown below 1.3640 could encourage a decline towards 1.3580 and 1.3500, respectively.

Commodity spotlight – WTI Oil

Oil prices edged higher on Thursday as investors overlooked the surging U.S crude inventories, but focused on OPEC supply cuts and developments around the Iran nuclear deal.

Price action continues to suggest that WTI bulls remain heavily reliant on geopolitical tensions and fears of supply shortages to sustain the current upside. While oil could appreciate further if the U.S withdraws from the 2015 Iran nuclear deal, gains are likely to remain limited by robust production from U.S Shale. Oil remains shaky and an appreciating Dollar has the ability to accelerate the downside. From a technical standpoint, WTI bulls are displaying early signs of exhaustion on the daily charts with resistance found at $69.00. A failure for bulls to keep above the $67.50 level could result in a decline towards $67.00 and $66.00, respectively.

ECB Praet: Data suggested some loss of momentum in economic activity

ECB chief economist Peter Praet said while the central bank cannot yet declare "mission accomplished" on inflation, " we have made substantial progress on the path towards a sustained adjustment in inflation."

Praet acknowledged that "the latest economic data and survey results have generally surprised to the downside, suggesting some loss of momentum in economic activity." But he pointed out that "temporary factors may also be at work". He emphasized that "we will also need to monitor whether, and if so, to what extent, these developments reflect a more durable softening in demand."

Europe Continues To Suffer From Disappointing Data

Notes/Observations

- Euro Zone Apr advance CPI data misses expectations and heightens recent ECB caution on outlook

- UK Apr PMI Services missed expectations and continued to fuel speculation that the Q1 GDP miss was due to more than just weather

- Norway Central Bank statement less dovish than expected after recent spat of weak data; still sees its 1st potential rate hike after summer

Asia:

- PBOC announced rules on overseas securities investments by domestic companies: Overseas FX purchase were not allowed under RQDII scheme

- Australia Mar Trade Balance registered its 3rd straight surplus (A$1.5B v0.8Be)

Europe:

- ECB's Weidmann (Germany): ECB should not unnecessarily delay its exit from stimulus. ECB hasn't corrected or committed to market expectation for first rate hike before end of reinvestment; reiterated view that market expectation for first rate hike around mid-2019 was not unrealistic

- House of Lords voted in support of power to prevent a hard border in Ireland. Vote was 309-242 to ensure no hard border, defying PM May's position. This is the 10th vote to go against the govt on proposed amendments to the EU Withdrawal Bill

- PM May said to have conceded that her plans for a customs partnership with the EU were “dead” after senior Cabinet ministers turned on her during a crunch Brexit meeting

Americas:

- FOMC left its Target Rate Range unchanged at 1.50-1.75% (as expected); inflation near goal; risks to the outlook appear roughly balanced, removing a prior reference to “near-term risks”

- Venezuela said to be poised to miss a May 8th deadline for a $275M debt installment; Brazil govt could be on the hook due to its guarantee. President Temer canceled a trip to Asia this week to supervise the episode - White House spokesperson Walters: President Trump said to be considering re-imposing steel, aluminum tariffs on Brazil

Economic Data:

- (IE) Ireland Apr Services PMI: 58.4 v 56.5 prior, Composite PMI: 57.6 v 53.7 prior

- (RU) Russia Apr Manufacturing PMI: 51.3 v 50.5e (21st month of expansion)

- (TR) Turkey Apr CPI M/M: 1.9% v 1.5%e; Y/Y: 10.9% v 10.5%e; CPI Core Index Y/Y: 12.2% v 11.5%e

- (TR) Turkey Apr PPI M/M: 2.6%e v 1.5% prior; Y/Y: 16.4% v 14.3% prior

- (HU) Hungary Mar PPI M/M: 0.0% v 0.8% prior; Y/Y: 3.5% v 3.9% prior

- (HU) Hungary Feb Final Trade Balance: €0.8B v €0.8B prelim

- (NO) Norway Central Bank (Norges) left the Deposit Rates unchanged at 0.50%; as expected

- (BR) Brazil Apr FIPE CPI (Sao Paulo): 0.0% v 0.0%e

- (UK) Apr Services PMI: 52.8 v 53.5e, Composite PMI: 53.2 v 53.7e

- (HK) Hong Kong Mar Retail Sales Value Y/Y: 11.4% v 10.9%e; Retail Sales Volume Y/Y: 10.0% v 8.6%e

- (EU) Euro Zone Apr Advance CPI Estimate Y/Y: 1.2% v 1.3%e; CPI Core Y/Y: 0.7% v 0.9%e

- (EU) Euro Zone Mar PPI M/M: 0.1% v 0.1%e; Y/Y: 2.1% v 2.1%e

Fixed Income Issuance:

- (ES) Spain Debt Agency (Tesoro) sold total €3.81B vs. €3.5-4.5B indicated range in 2021, 2028 and 2066 Bonds

- Sold €1.39B in 0.05% Jan 2021 SPGB; Avg yield: -0.145% v -0.232% prior, Bid-to-cover: 2.66x v 3.08x prior

- Sold €1.32B in 1.40% Apr 2028 SPGB; Avg yield: 1.288% v 1.235% prior, Bid-to-cover: 2.01x v 1.30x prior

- Sold €1.10B in 3.45% July 2066 SPGB; Yield: 2.664% v 3.192% prior; Bid-to-cover: 2.09x v 1.54x prior

- (ES) Spain Debt Agency (Tesoro) sold €690M vs. €0.5-1.0B indicated range in 0.30% Nov I/L 2021 bonds (SPGBei;Bonoei); Real Yield: -1.578% v -1.183% prior; Bid-to-cover: x v 2.67x prior (Dec 7th 2017)

- (FR) France Debt Agency (AFT) sold total €8.488B vs. €7.5-8.5B indicated range in 2026, 2028, 2034 and 2048 Oats

- Sold €2.071B in 0.50% May 2026 Oat; Avg Yield: 0.53% v 0.61% prior; Bid-to-cover: 1.89x v 1.78x prior

- Sold €3.611B in 0.75% May 2028 Oat; Avg Yield: 0.81% v 0.74% prior; Bid-to-cover: 1.88x v 1.94x prior

- Sold €955M in 1.25% May 2034 Oat; Avg Yield: 1.22% v 1.14% prior; Bid-to-cover: 2.11x v 1.80x prior

- Sold €1.851B in 2.00% May 2048 Oat; Avg Yield: 1.65% v 1.58% prior, Bid-to-cover: 1.35x v 1.85x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.1% at 387.1, FTSE +0.1% at 7550, DAX +0.1% at 12792, CAC-40 -0.1% at 5523, IBEX-35 +0.1% at 10093, FTSE MIB -0.3% at 24206, SMI +0.1% at 8922, S&P 500 Futures +0.3%]

- Market Focal Points/Key Themes: European Indices trade mixed following weakness in the US overnight, but positive futures this morning on busy morning for corporate earnings. Major German Dax components Bayer, Adidas and Infineon reported this morning with Bayer trading little changed following mixed result, affirming currency adjusted forecast, Adidas lower after a revenue miss and Infineon trades higher after a profit beat. In France Veolia trades up after a beat on the top and bottom line, Thales also trades higher after a Revenue beat. In other movers Smith and Nephew trades lower after guidance cut, with Fingerpint Cards, Fresenius Medical and Trinity Mirror also lower after earnings.

Movers

- Consumer Discretionary [Trinity Mirror [TNI.UK] -0.9% (Trading update), Adidas [ADS.DE] -0.9% (Earnings)]

- Industrials [Rolls Royce [RR.UK] -0.9% (AGM Statement), Thales [HO.FR] +2.2% (Earnings), Gerberit [GEBN.CH] +3.1% (Earnings)]

- Technology [Infineon [IFX.DE] +0.9% (Earnings), Fingerprint Cards [FINGB.SE] -11% (Earnings)]

- Financials [ Victoria Park [VICP.SE] +9% (To be acquired) ]

- Healthcare [Fresenius Medical [FME.DE] -1.8% (Earnings), Solvay [SOLB.BE] -2.0% (Earnings), Smith and Nephew [SN.UK] -6.5% (Earnings, outlook)]

Speakers

- ECB's Villeroy (France) Not surprised by slower Q1 GDP growth in France. French corporate debt levels required vigilance

- ECB’s Hansson (Estonia): Latest Euro Area developments were positive and had allowed a moderate exit from loose policies

- ECB's Constancio (Portugal), term expires in May): Euro Zone wasting the benefits of currency union

- Norway Central Bank (Norges) policy statement noted that the decision was unanimous to keep policy steady. The overall outlook was unchanged compared the March meeting. Underlying inflation was low, but rising capacity utilization was expected to push up price and wage inflation further out . Reiterated view that interest rates would most likely to be raised after summer

- Sweden Central Bank (Riksbank) Gov Ingves: Rate path was a forecast not a promise. Needed to be vigilant and keep inflation expectations high

- Sweden Central Bank (Riksbank) Dep Gov Skingsley: Not at the point where rate hike could begin. Did not want to risk what has been achieved

- EU's Moscovici: Inflation should increase slowly in Europe

- UK Brexit Min Davis: No surprise that it take time to decide on future customs arrangement with the EU. Reiterates govt stance that the that UK had to leave the customs union. Both options on the table had drawbacks

- Taiwan Central Bank (CBC) Mar Minutes: MPC notes the domestic economy faced uncertainty. One member noted that a rate hike would boost the TWD currency. TWD currency appreciation would affect company investment plans

- China State Chancellor Wang stated that the Chinese govt supported the end of war on the Korean Peninsula

Currencies

- USD saw similar price action to Wed’s session as it saw initial gains evaporate then recover in early US trade.

- EUR/USD was back below the 1.20 level ahead of the US morning. after soft advance CPI data.. The data reinforced recent ECB cautiousness on the moderation in growth and inflation.

- GBP/USD initially moved back above the pivotal 1.36 level before another disappoint ingdata release. Apr PMI Services missed expectations and continued to fuel speculation that the Q1 GDP miss was due to more than just weather. The UK govt possible customs union plan with the EU had been put under question, moving the Irish border issue back on top of the political agenda.

- EUR/NOK cross was lower after the Norway Central Bank policy statement was deemed less dovish than expected after recent spat of weak data. Norges still saw the 1st potential rate hike after summer. Cross trading below 9.70 ahead of the NY morning.

Fixed Income

- Bund Futures trade 13 ticks higher at 158.74 as Euro Zone Apr Advance CPI data remains subdued. Upside targets 159.75, while a return lower targets the 157.25 level.

- Gilt futures trade at 122.00 higher by 10 ticks, after UK Services disappoints, but does rebound from the 20-month low in March. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Thursday’s liquidity report showed Wednesday's excess liquidity rose to €1.901T from €1.859T prior. Use of the marginal lending facility increased from €20M to €47M.

Looking Ahead

- (UK) Last Day of Commons Session Before May Recess

- (IT) Italy Democratic Party (PD) debate whether to join Five Star in coalition govt

- (UK) EU-UK officials meet in Brexit negotiations

- (CN) US delegation in China for trade talks

- (RU) Russia Apr Sovereign Wealth Funds: Wellbeing Fund: $B v $65.9B prior

- 05:30 (NO) Norway Central Bank (Norges) Gov Olsen post rate decision press conference

- 05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month bills

- 05:30 (UK) DMO to sell £3.0B in 0.75% July 2023 Gilts;

- 06:00 (IE) Ireland Apr Live Registry Monthly Change: No est v -2.2K prior; Liver Registry Level: No est v 233.1K prior

- 06:45 (US) Daily Libor Fixing

- 07:00 (CZ) Czech Central Bank (CNB) Interest Rate Decision: Expected to leave Repurchase Rate unchanged at 0.75%

- 07:00 (ZA) South Africa Mar Electricity Consumption Y/Y: No est v 0.4% prior; Electricity Production Y/Y: No est v 2.0% prior

- 07:30 (US) Apr Challenger Job Cuts: No est v 60.4K prior; Y/Y: No est v 39.4% prior

- 08:00 (BR) Brazil CONAB Crop Report

- 08:00 (BR) Brazil Mar Industrial Production M/M: 0.5%e v 0.2% prior; Y/Y: 3.0%e v 2.8% prior

- 08:00 (CL) Chile Mar Retail Sales Y/Y: 4.7%e v 4.0% prior; Commercial Activity Y/Y: No est v 5.9% prior

- 08:00 (PT) ECB’s Constancio (Portugal, outgoing) in Frankfurt

- 08:05 (UK) Baltic Dry Bulk Index

- 08:15 (CZ) Czech Central Bank Gov Rusnok to hold post Rate Decision press conference (with staff updates)

- 08:30 (US) Initial Jobless Claims: 225Ke v 209K prior; Continuing Claims: 1.84Me v 1.837M prior

- 08:30 (US) Q1 Preliminary Nonfarm Productivity: 0.9%e v 0.0% prior; Unit Labor Costs: 3.0%e v 2.5% prior

- 08:30 (US) Mar Trade Balance: -$50.0Be v -$57.6B prior

- 08:30 (CA) Canada Mar Int'l Merchandise Trade (CAD): -2.3Be v -2.7B prior

- 08:30 (US) Weekly USDA Net Export Sales - 08:30 (FR) ECB’s Coeure (France) in Frankfurt

- 09:00 (RU) Russia Gold and Forex Reserve w/e Apr 27th: No est v $463.8B prior

- 09:00 (MX) Mexico Mar Leading Indicators M/M: No est v 0.00 prior

- 09:45 (US) Apr Final Markit Services PMI: 54.4e v 54.4 prelim, Composite PMI: 54.8 prelim

- 10:00 (US) Apr ISM Non-Manufacturing Composite: 58.0e v 58.8 prior

- 10:00 (US) Mar Factory Orders: 1.4%e v 1.2% prior; Factory Orders (ex-transportation): No est v 0.1% pror

- 10:00 (US) Mar Final Durable Goods Orders: No est v 2.6% prelim; Durables Ex Transportation: No est v 0.0% prelim, Capital Goods Orders (Non-defense/ex-aircraft): No est v -0.1% prelim, Capital Goods Shipment (Non-defense/ex-aircraft): No est v -0.7% prelim

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 12:00 (CH) SNB's Jordan in Zurich

- 17:00 (CL) Chile Central Bank (BCCH) Interest Rate Decision: Expected to leave Overnight Rate Target unchanged at 2.50%