Sample Category Title

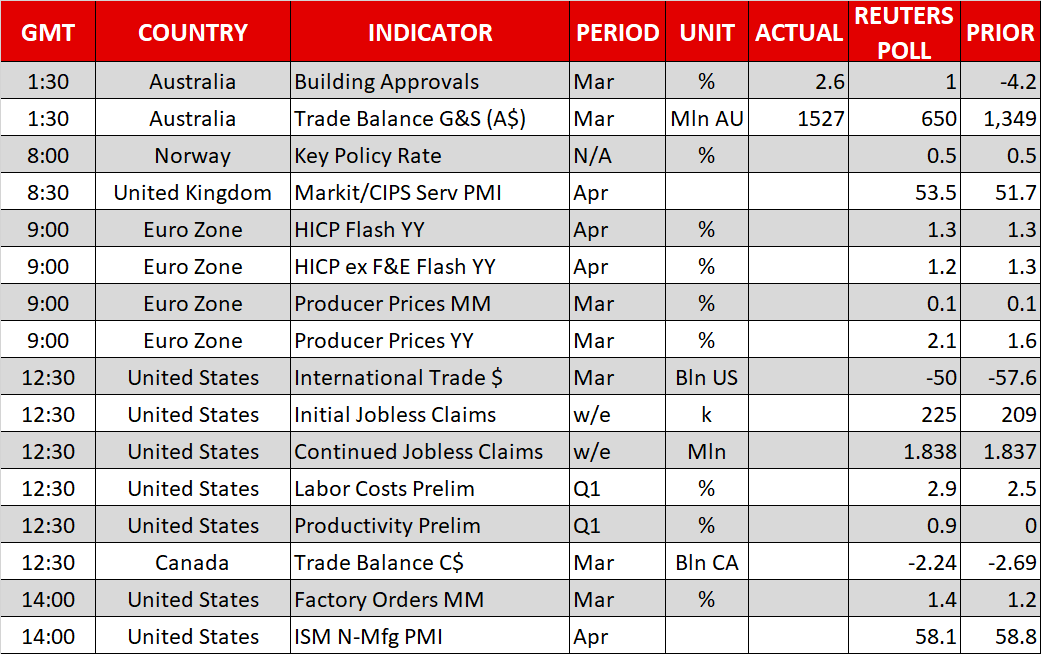

UK PMI services rose to 52.8 vs exp 53.5, rate of economic growth remained disappointingly subdued

UK PMI services missed market expectations, but GBP is steadily in range against USD, EUR and JPY so far.

PMI services rose to 52.8 in April, up from 51.7 but missed consensus of 53.5. Markit's key findings are not too encouraging for the UK. It noted that business activity rises at subdued pace in April. There is the weakest upturn in employment since March 2017 and inflationary pressures are moderate.

Comments from Chris Williamson, Chief Business Economist at IHS Markit:

"The services survey adds to signs that the rate of economic growth remained disappointingly subdued at the start of the second quarter. The three PMI surveys collectively showed only a muted rebound in business activity after being disrupted by heavy snowfall in March, failing to regain February's pace of growth to suggest that the underlying performance of the economy has continued to deteriorate.

"The overall expansion signalled by the three surveys in April was the second-weakest since the Brexit vote, pointing to a quarterly rate of GDP growth of around 0.2% at the start of the second quarter.

"Jobs growth across services, manufacturing and construction has also slowed to its weakest since the referendum and inflationary pressures have eased.

"The surveys have indicated that sales, investment and hiring are being hit by uncertainty about the economic outlook as well as sluggish domestic demand, notably among consumers.

"The disappointing services data will add to expectations that the MPC will take its finger firmly off the rate hike trigger. Any further slowing will also raise questions as to whether the November rate hike may have been ill-timed."

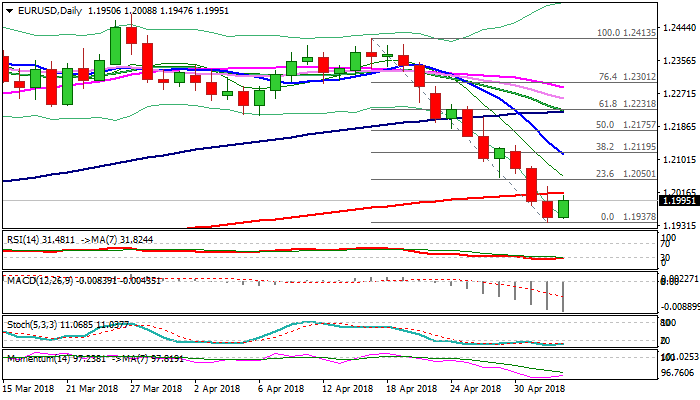

EURUSD – Bears Are Taking A Breather Above Strong Fibo Support At 1.1936

The Euro bounced from new multi-month low at 1.1938 on Thursday, but recovery attempts so far remain under key barriers at 1.2000/14 (psychological barrier/200SMA).

Steep fall off 1.2413 (17 Apr high) found footstep just above key Fibo support at 1.1936 (61.8% of 1.1553/1.2555 rally), signaling consolidative/corrective action before broader bears resume.

Daily RSI is emerging from oversold territory, while deeply oversold slow stochastic is turning higher and 14-d momentum is reversing, supporting the notion. US Federal Reserve kept interest rates unchanged as expected, but pointed that inflation is moving higher and moving close to its 2% target, economic outlook is balanced and jobs sector is strengthening, keeping positive environment for the dollar.

Profit-taking on strong bearish acceleration in past two weeks would push the price higher, which could be seen as positioning for fresh weakness.

While 200SMA caps, immediate focus will remain at the downside, with break through 1.1936 to generate bearish signal for fresh bearish acceleration which could stretch towards 1.1790 (Fibo 76.4% of 1.1553/1.2555 ascend.

On the other side, break and close above 200SMA would signal stronger corrective action which should be capped under 1.2120 zone (falling 10SMA/Fibo 38.2% of 1.2413/1.1938 descend), to keep larger bears intact.

EU inflation data (Apr f/c 1.3% vs 1.3% prev) is the key event of the European session, while batch of US data are due later today and eyed for fresh signals

Res: 1.2000, 1.2014, 1.2050, 1.2083

Sup: 1.1936, 1.1915, 1.1900, 1.1854

Dollar Trades Like A Rollercoaster After Fed, Eurozone Inflation Coming Up

Here are the latest developments in global markets:

FOREX: The US dollar index, which gauges the greenback’s strength against a basket of six major currencies, was practically unchanged on Thursday after it touched its highest level in 2018 yesterday, in the aftermath of the Fed’s policy meeting.

STOCKS: US markets closed lower yesterday, following the FOMC meeting. Although stock indices spiked higher immediately on the decision, that sentiment quickly turned around and equities edged lower to finish in the red. The S&P 500 and Dow Jones both fell by 0.72%, while the Nasdaq Composite declined by 0.42%. Futures tracking the S&P, Dow, and Nasdaq 100 are currently in positive territory, albeit marginally so. In Asia, Japanese markets remained closed for a public holiday, while in Hong Kong, the Hang Seng tumbled by 1.4%. In Europe, futures tracking the major indices were a sea of red, pointing to a lower open for these benchmarks today.

COMMODITIES: Both WTI and Brent are down on Thursday, but by less than 0.1%. Prices responded little to a surprisingly large build in US inventories yesterday. Another interesting point is that oil has remained elevated lately even despite a resurgent US dollar, which typically exerts downward pressure on the precious liquid. The obvious conclusion is that expectations around fresh sanctions being imposed on Iran soon are currently strong enough to offset both signals that US production is soaring and the recovery in the dollar. In precious metals, gold is trading 0.4% higher today, last seen near the $1,308 per ounce mark. The safe haven traded like a rollercoaster yesterday after the FOMC decision, initially surging and then quickly giving those gains back, overall moving in opposite directions with the dollar.

Major movers: Dollar drops after Fed but quickly recovers to touch 2018 high

The Fed kept borrowing costs unchanged yesterday, as was widely anticipated. There were three noteworthy changes in the accompanying statement. Starting with the dovish ones, policymakers removed a sentence that previously stated the economic outlook had strengthened, signaling that economic data have begun to moderate. In addition, the Fed included the word “symmetric” when describing its 2% inflation target. This was interpreted as a hint it may be comfortable allowing inflation to run above 2% without raising rates for a while, since it was running below it for so long. The result was a sharp drop in the dollar immediately following the decision.

However, the tumble was short-lived, and the greenback recovered all its losses to trade higher in the following hours, as the dust settled and market participants digested the hawkish signals in the statement as well. The Fed also erased a sentence that previously indicated “the Committee is monitoring inflation developments closely”, which is likely a hint that officials are becoming more confident inflation will rise, and that downside risks have dissipated. The dollar index surged to reach a fresh high for 2018 in the aftermath.

Overall, the key takeaway was that the Fed is becoming a little more cautious about the economy’s performance, but considerably more optimistic on the inflation outlook. As for the dollar, all eyes will now turn to tomorrow’s employment report, which should provide some direction – particularly if there are any surprises in the wage figures. Lastly, the greenback may also be impacted by fresh signals on trade. Note that US Treasury Secretary Mnuchin arrived in China for negotiations today, so we may see some market attention fall back on trade issues.

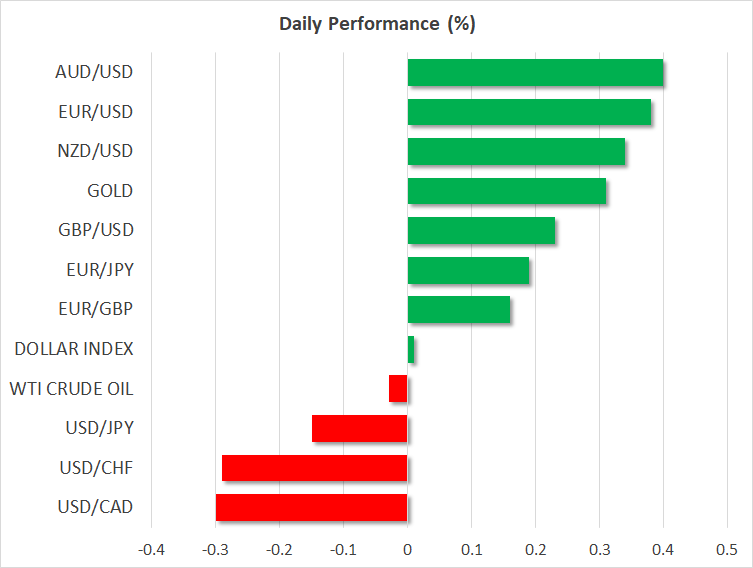

In the antipodean currencies, aussie/dollar and kiwi/dollar are higher by 0.4% and 0.35% respectively today, catching their breath following roughly two weeks of continued declines for both.

Day ahead: Eurozone inflation, UK services PMI, US trade data & services PMI on the agenda

Thursday’s calendar features a number of important releases, including flash inflation figures for April out of the eurozone.

At 0800 GMT, the Norges Bank’s decision on interest rates will be made public. No change in rates is expected though the Bank’s communication could well lead to positioning in Nokkie pairs. At the same time, the Swedish central bank will be holding an open hearing with Governor Stefan Ingves on the report “Account of Monetary Policy 2017”. In this respect, Swedish krona pairs will also be monitored.

Attention will next turn to the UK which will be on the receiving end of PMI data for the all-important services sector, which contributes around 80% of the nation’s GDP; an acceleration in activity is expected. In the two preceding days, the respective PMI readings for the manufacturing and construction sectors surprised to the downside and delivered a beat correspondingly.

Politics are also in focus in the UK which holds local elections today. PM May’s Conservatives Party is projected to lose council seats. Should the number of lost seats exceed expectations, then a leadership challenge could be put back on the table, further complicating things and leading to additional losses for sterling pairs. Meanwhile, Brexit uncertainty looms large with an ongoing debate on whether the nation should remain within a customs union with the EU after it officially exits the bloc.

Preliminary inflation figures for the month of April are due out of the eurozone at 0900 GMT. Headline inflation, as gauged by the Harmonised Index of Consumer Prices (HICP) that uses a common methodology across EU countries, is anticipated to grow at 1.3% y/y, the same as in March. This compares to the ECB’s target for annual inflation of close to but below 2%. Core inflation, that excludes volatile food and energy items, will also be watched. Euro area producer price data for March are scheduled for release at the same time.

Trade data out of the US will be in focus at 1230 GMT, with the country’s trade deficit expected to narrow in March after rising to a nine-and-a-half-year high in February. The numbers pertaining to the bilateral trade deficit with China will also be closely monitored amid ongoing trade tensions – which have eased somewhat lately – between the world’s two largest economies. Weekly jobless claims data, as well as numbers on Q1 labor costs and productivity will hit the markets at the same time, while Canada will also be seeing the release of March trade data at 1230 GMT.

Later in the day (1400 GMT), factory orders for March and April’s ISM services PMI will be generating attention out of the US. On an annual basis, factory orders are forecast to grow at a faster pace compared to the month that preceded, while service sector activity as gauged by the ISM’s PMI is anticipated to ease, though still comfortably remain in expansion territory (above the 50 threshold).

Activision Blizzard and Xerox are among companies releasing quarterly results on Thursday; both corporations will be reporting after today’s US market close.

Policymakers making appearances include ECB Vice President Vitor Constancio and ECB Executive Board member Benoit Coeure, who will be talking on fostering a banking and capital markets union within the eurozone at 1200 GMT and 1230 GMT respectively.

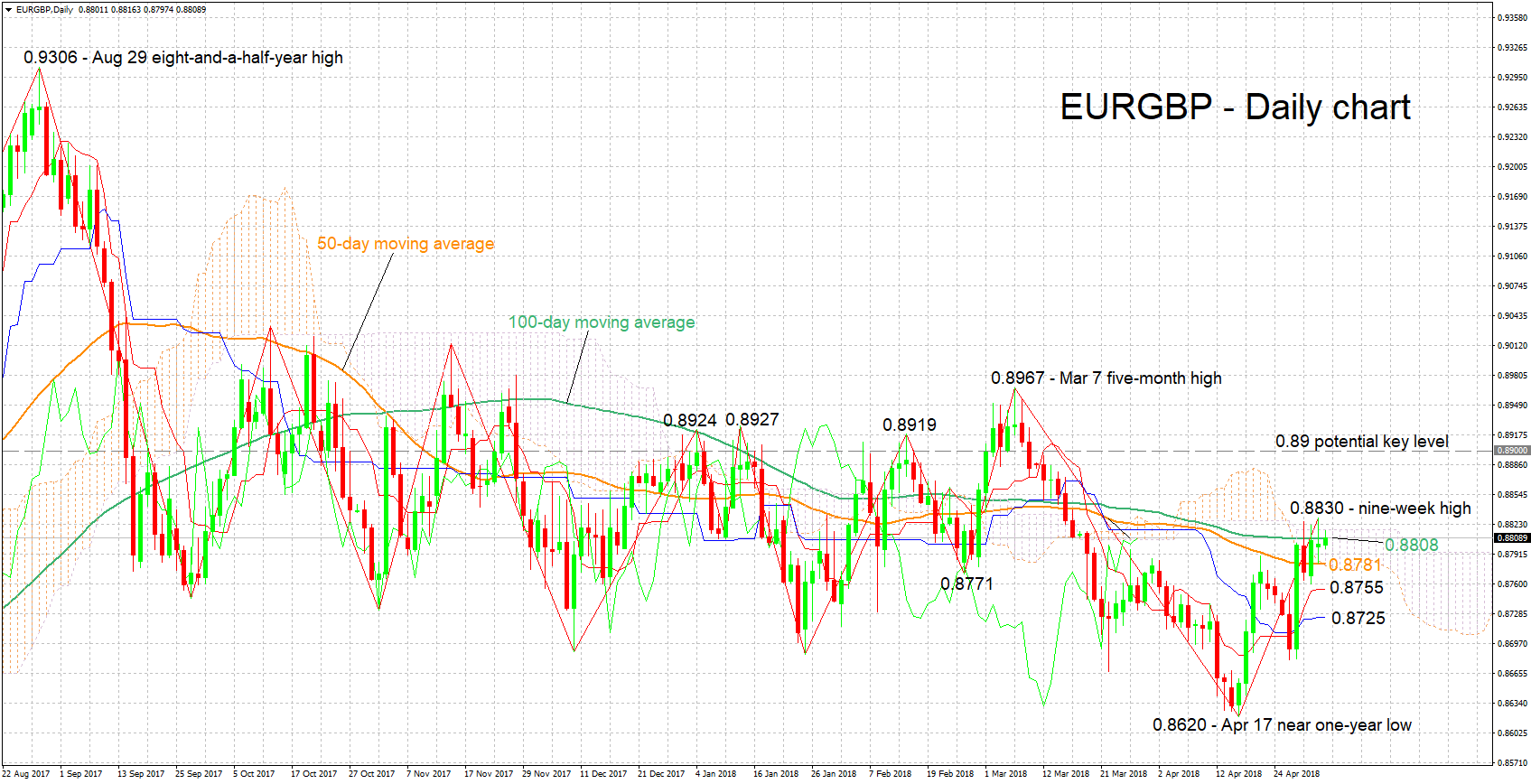

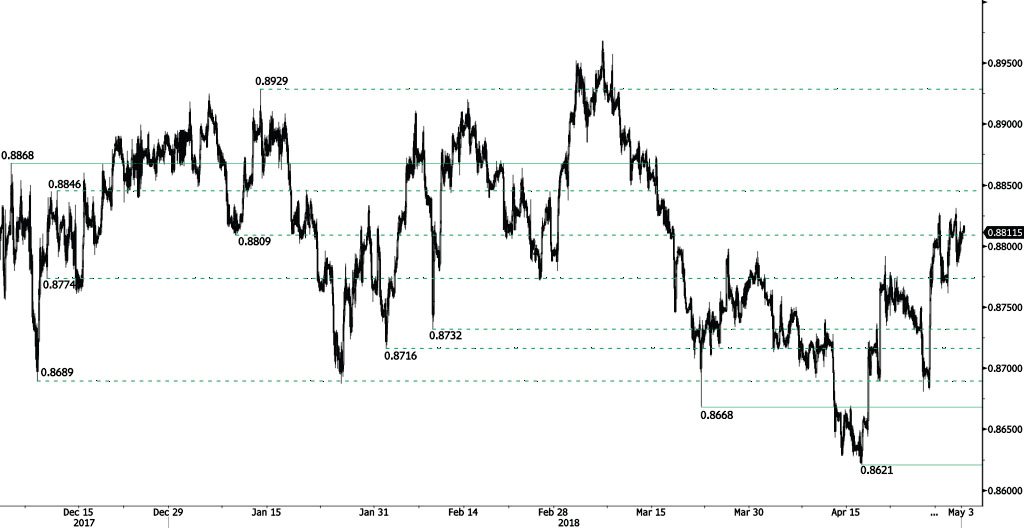

Technical Analysis: EURGBP short-term bullish, trades not far below 9-week high

EURGBP advanced considerably after hitting a near one-year low of 0.8620 on April 17, eventually posting a nine-week high of 0.8830 during Wednesday’s trading. The Tenkan- and Kijun-sen lines are positively aligned in support of a bullish bias. Notice though that the two have flatlined, this being a sign of easing positive momentum in the short-term.

Stronger-than anticipated inflation figures out of the eurozone are likely to refuel the positive momentum, pushing the pair higher. EURGBP is currently marginally above the 100-day moving average located at 0.8808, but could still be meeting resistance around it (the region around this MA also includes the Ichimoku cloud top at 0.8817). Further above, additional resistance could come around yesterday’s high of 0.8830, with attention next turning to the 0.89 round figure.

On the downside and in case of weaker eurozone data, support could come around the current level of the 50-day MA at 0.8781 (including the Ichimoku cloud bottom at 0.8779), and further below from the Tenkan-sen (0.8755) and Kijun-sen (0.8725) lines.

UK data and related developments can also move the pair during today’s trading.

Bitcoin Strengthening

Bitcoin rise started in mid-April starts back, currently trading above 9200 and heading along the 9300 range. Bitcoin bearish pattern started in March 2018 weakens. The pair is contained between hourly support and resistance given at 6306 (13/11/2017 low) and 10232 (01/02/2018 high). The technical structure suggests further short-term increase.

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 7'000 - 12'000 in 2018. Bitcoin is trading slightly above its 200 DMA (8200 range)

CRUDE OIL Continued Weakness

Crude oil weakness continues, trading below 68 and heading along the 67.50 range. Crude Oil is currently trading at December 2014 levels. The bullish pattern started in mid-February 2017 is maintained. Hourly support and resistance are given at 65.56 (17/04/2018 low) and 69.54 (12/01/2014 high). The technical structure suggests short-term downward moves.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

SILVER Continued Strength

Silver recovery phase from 16.06 (01/05/2018 low) continues, trading above 16.40 and heading along the 16.50 range. Hourly support and resistance are given at 16.03 (05/12/2017 low) and 16.87 (06/03/2018 high). The technical structure suggests further short-term increase.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. The pair is trading below its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Heading Higher

Gold is bouncing off from 1304 low, trading along 1310 and approaching the 1313 range. Hourly support and resistance are given at 1300 (29/12/2017 low) and 1329 (08/03/2018 high). The technical structure suggests short-term increase.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1'392 (17/03/2014) is required to confirm it. A major support can be found at 1'045 (05/02/2010 low).

EUR/CHF Maintained At The 1.1950 Range

EUR/CHF is maintained at the 1.1950 range, trading sideways. Strong resistance at 1.20 remains. Hourly support given at 1.1842 (11/04/2018 low) is distanced. The short-term technical structure suggests further short-term sideways trading moves.

In the longer term, the technical structure has reversed. Strong resistance at 1.20 (level before the unpeg) is now at reach. The ECB's slowing QE program is likely to cause buying pressures on the euro, which should weigh in favour of the EUR/CHF. Support and resistance can be found at 1.0624 (24/06/2016 low) and 1.2097 (18/12/2014 high).

EUR/GBP Trading Above 0.88

EUR/GBP is bouncing off from 0.8783 (02/05/2018 low), heading along the 0.8817 range. EUR/GBP bearish pattern started in March is weakening. Hourly support and resistance are given at 0.8668 (22/03/2018 low) and 0.8868 (05/12/2017 high). The technical structure suggests short-term upward moves.

In the long-term, the pair has largely recovered from 2015 lows. The technical structure suggests further upside pressure. Strong resistance can be found at 0.9500 (psychological level) while support remains at 0.8304 (05/12/2016 low). The pair is trading below its 200 DMA.

AUD/USD Bouncing Off

AUD/USD bearish pattern from 0.7813 (19/04/2018) pauses, the pair recovery phase from 0.7473 (01/05/2018 low) continues, approaching the 0.7530 range. Hourly resistance 0.7879 (28/02/2018 high) remains. The technical structure suggests short-term increase.

In the long-term, the upward trend slows down after failing to reach key resistance at 0.8164 (14/05/2015 low). Key support stands at 0.6009 (31/10/2008 low). A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.