Sample Category Title

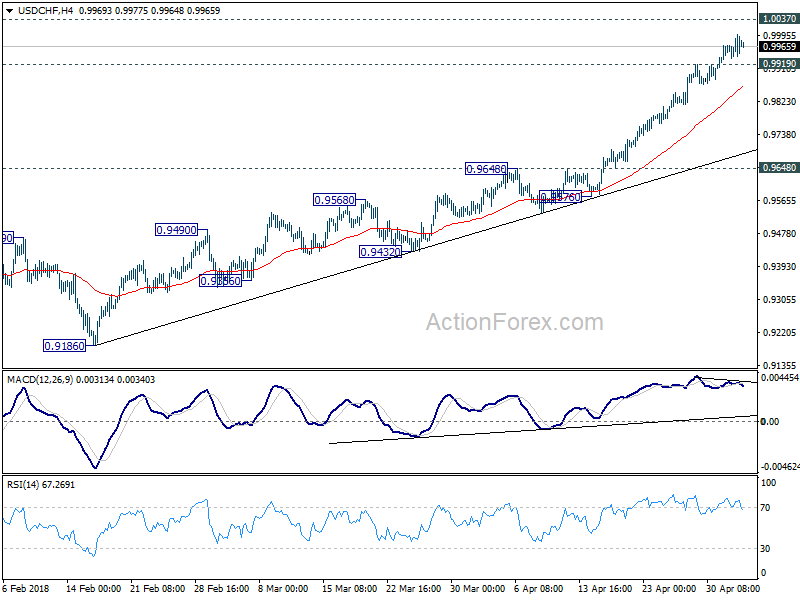

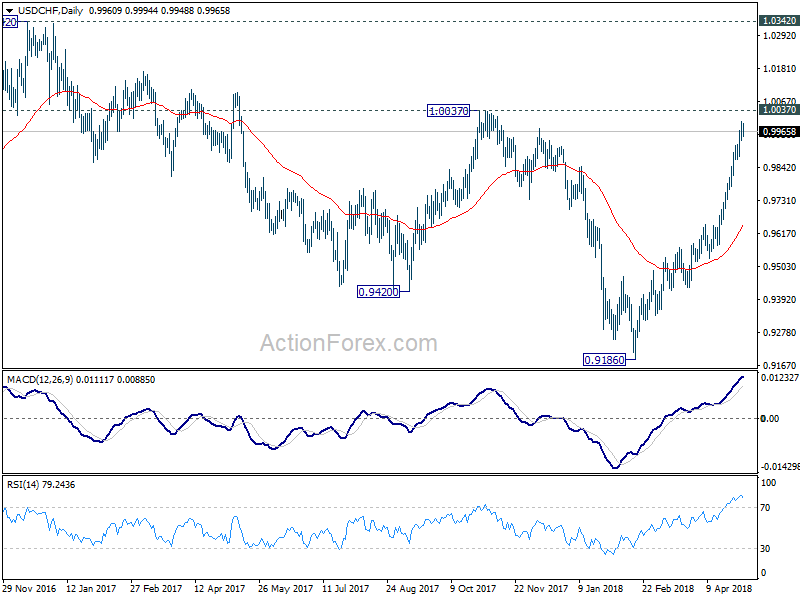

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9952; (P) 0.9976; (R1) 1.0017; More...

USD/CHF is losing some upside momentum as seen in 4 hour MACD, But intraday bias remains on the upside for 1.0037 resistance. Decisive break there will extend the whole rally from 0.9186 towards 1.0342 key resistance On the downside, though, below 0.9919 will indicate short term topping. And, in that case, lengthier consolidation would be seen before another rally.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 0.9648 resistance turned support holds, even in case of pull back.

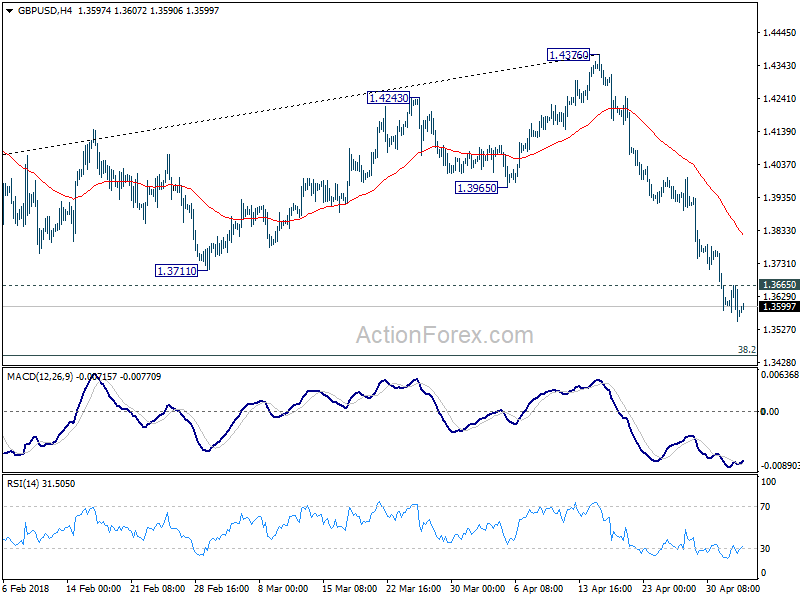

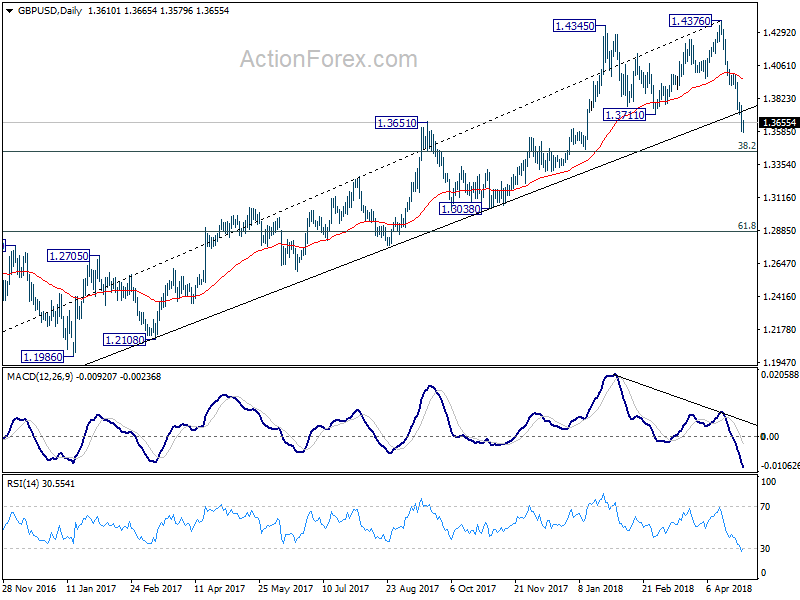

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3528; (P) 1.3597; (R1) 1.3639; More...

GBP/USD's decline resumed after brief consolidation and intraday bias is back on the downside. Current fall from 1.4376 is in progress for 1.3448 fibonacci level next. On the upside, above 1.3665 will argue that a short term bottom is formed. In that case, lengthier consolidation could be seen before another decline.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4248). Deeper decline should be seen to 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 first. Break will target 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3955) holds, even in case of strong rebound.

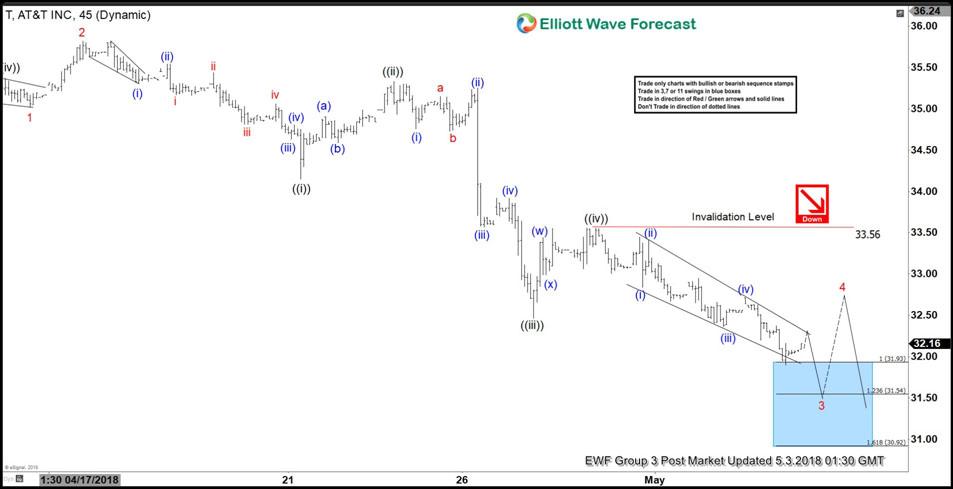

Elliott Wave View: AT&T Calling For 3 Wave Bounce

AT&T ticker symbol $T short-term Elliott Wave view suggests that the decline from 4/10 peak is unfolding as an Impulse Elliott Wave structure. In the impulsive structure, wave 1, 3, and 5 should show 5 waves internal subdivision.

Down from 4/10 peak ($36.39), Minor wave 1 ended in 5 waves structure at 35.02 low. Minor wave 2 bounce ended at 35.82 and Minor wave 3 is in progress with subdivision of 5 waves impulsive structure in the lesser degree. Down from 35.82, Minute wave ((i)) of 3 ended at 34.15, Minute wave ((ii)) of 3 ended at 35.33, Minute wave ((iii)) of 3 ended at 32.47, and Minute wave ((iv)) of 3 ended at 33.56 high.

Below from there, Minute wave ((v)) of 3 remains in progress. Minor wave 3 has reached the minimum number of swings and target, although a marginal low still can’t be ruled out towards $31.54 – $30.92. This is the 123.6%-161.8% Fibonacci extension area of ((v))=((i)). Afterwards, AT&T should end the 5 waves structure in Minor wave 3 and see a Minor wave 4 bounce in 3, 7 or 11 swings against 35.82 high before further downside resumes. We don’t like buying into the proposed bounce.

AT&T 1 Hour Elliott Wave Chart

EUR/USD Is Broadly Unchanged

Market movers today

In Scandi, today's Norges Banks monetary policy meeting is not expected to bring new signals, see preview. It is one of the ‘small meetings' and we expect Norges Bank to repeat the message from March of a forthcoming hike in September, see Scandi section next page.

Main event on the global front is the Euro flash inflation for April. We expect it to remain at the 1.3% level from March and we project core inflation will decline back to 0.9%, due to Easter base effects from 2017 becoming a drag on services prices. A temporary increase in headline inflat ion in coming months is likely because of energy price inflat ion, although we expect the underlying price pressure remains subdued going forward.

Also keep an eye on any news from the US-China trade negotiations taking place Thursday and Friday in Beijing. Any failure to reach some agreement could lead to a re-escalat ion of the trade conflict , see also Flash Comment: Trump holding fire as negotiations with China begin, 25 April 2018.

We also get UK PMI services for April, which may be decisive for Bank of England's rate decision next week. It fell sharply to 51.7 in March, which was much more than suggested by other confidence indicators. We est imate a rebound to 53 in April.

US ISM non-manufacturing for April may fall further as an increasing amount of data points to some softening in demand growth – not least retail sales and durable goods orders.

Selected market news

As expected, the Fed maintained the target range at 1.50-1.75% at its May meeting, which ended yesterday. As it was one of the smaller meet ings, there was only the statement to look for new signals. Usually it does not change much from meet ing to meeting, which was also the case this t ime, but we still believe there was a couple of important changes. Firstly, the Fed now says that inflat ion is running near the ‘symmetric' 2% inflation target meaning that it will allow inflation to move slightly above 2% (as it projected back in March). Secondly, it no longer says that it is monitoring inflation closely. In our view, despite the market reaction, we think it was slightly hawkish increasing the probability of three additional hikes this year.

US 2-year yields fell 3bp after statement and US stocks saw a small lift . However, US stocks retreated again into the close finishing down close to 1%. EUR/USD is broadly unchanged.

Markets now await the US employment report tomorrow and the results of the US-China trade negot iat ions also planned to finish tomorrow.

ECB's Governing Council member Jens Weidman (hawk) said yesterday that market expectat ions of a first rate hike in mid-2019 is ‘not wholly unrealistic'.

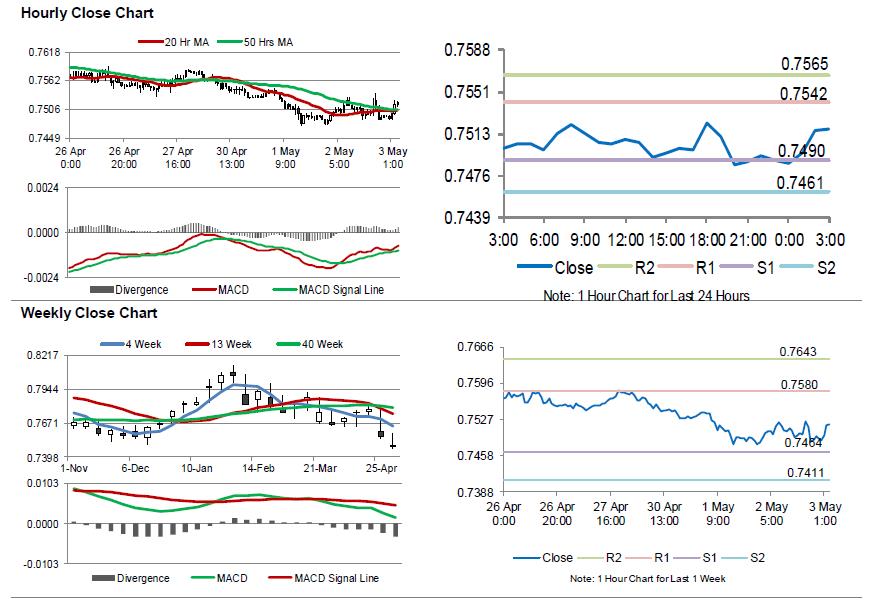

Australia’s Trade Surplus Surprisingly Widened To A Nearly 1 Year High In March

For the 24 hours to 23:00 GMT, the AUD rose 0.05% against the USD and closed at 0.749.

LME Copper prices rose 0.11% or $7.5/MT to $6785.0/MT. Aluminium prices rose 0.49% or $11.0/MT to $2269.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7518, with the AUD trading 0.37% higher against the USD from yesterday's close, following a pair of upbeat economic releases in Australia.

Data showed that Australia's seasonally adjusted trade surplus unexpectedly widened to A$1527.0 million in March, surging to its highest level in almost a year. compared to a revised surplus of A$1349.0 million in the previous month, while markets were expecting for a surplus of A$865.0 million. Moreover, the nation's seasonally adjusted building approvals rebounded 2.6% on a monthly basis in March, topping market expectations for a rise of 1.0%. Building approvals had fallen by a revised 4.2% in the previous month.

On the other hand, the nation's AiG performance of services index declined to a level of 55.2 in April, compared to a level of 56.9 in the prior month.

The pair is expected to find support at 0.7490, and a fall through could take it to the next support level of 0.7461. The pair is expected to find its first resistance at 0.7542, and a rise through could take it to the next resistance level of 0.7565.

Going ahead, the Reserve Bank of Australia's (RBA) statement on monetary policy, due to be released overnight, will be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Economic Growth Cooled As Expected In 1Q 2018

For the 24 hours to 23:00 GMT, the EUR declined 0.28% against the USD and closed at 1.1956, after the latest data revealed that Euro-bloc's economic growth slowed at the start of the new year.

The Euro-zone's seasonally adjusted preliminary gross domestic product (GDP) advanced 0.4% on a quarterly basis in the first quarter of 2018, meeting market expectations. In the previous quarter, GDP had risen 0.7%. Additionally, the region's unemployment rate remained steady at 8.5% in March, in line with market anticipations.

In other economic news, the Euro-zone's final Markit manufacturing PMI fell less than initially estimated to a level of 56.2 in April, while the preliminary figures had indicated a fall to a level of 56.0. The PMI had registered a reading of 56.6 in the prior month.

Separately, Germany's final Markit manufacturing PMI eased to a level of 58.1 in April, confirming the flash reading and following a level of 58.2 in the previous month.

The US Dollar advanced against a basket of major currencies, after the US Federal Reserve (Fed), expressed growing confidence that inflation is inching closer to its goal.

The Fed, at its May monetary policy meeting, unanimously decided to keep the benchmark interest rate unchanged at a target range of 1.50% to 1.75%, meeting market expectations. Further, the central bank expressed more confidence in its inflation outlook, stating that annual inflation is expected to run near the central bank's 2.0% target over the medium term.

On the macro front, ADP private sector employment in the US climbed more-than-anticipated by 204.0K in April, compared to market anticipations for a rise of 198.0K. However, it was the smallest increase since November 2017. The private sector employment had registered a revised gain of 228.0K in the prior month. Meanwhile, the nation's MBA mortgage applications declined 2.5% in the week ended 27 April, compared to a drop of 0.2% in the previous week.

In the Asian session, at GMT0300, the pair is trading at 1.1978, with the EUR trading 0.18% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1933, and a fall through could take it to the next support level of 1.1889. The pair is expected to find its first resistance at 1.2027, and a rise through could take it to the next resistance level of 1.2077.

Looking forward, traders would focus on the Euro-zone's flash inflation figures for April, scheduled to release in a few hours. Additionally, the US initial jobless claims and the ISM manufacturing PMI for April along with trade balance, final durable goods orders and factory orders data, all for March, will keep investors on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

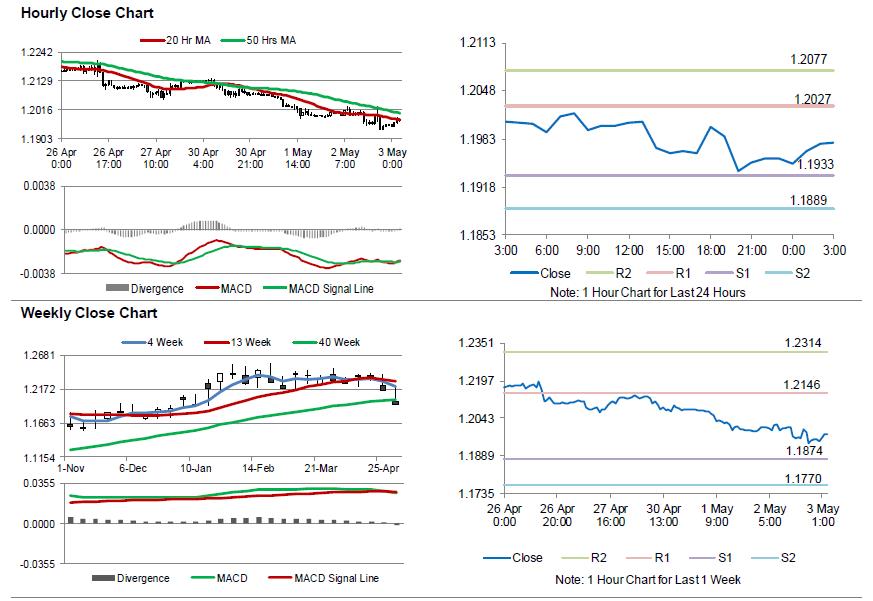

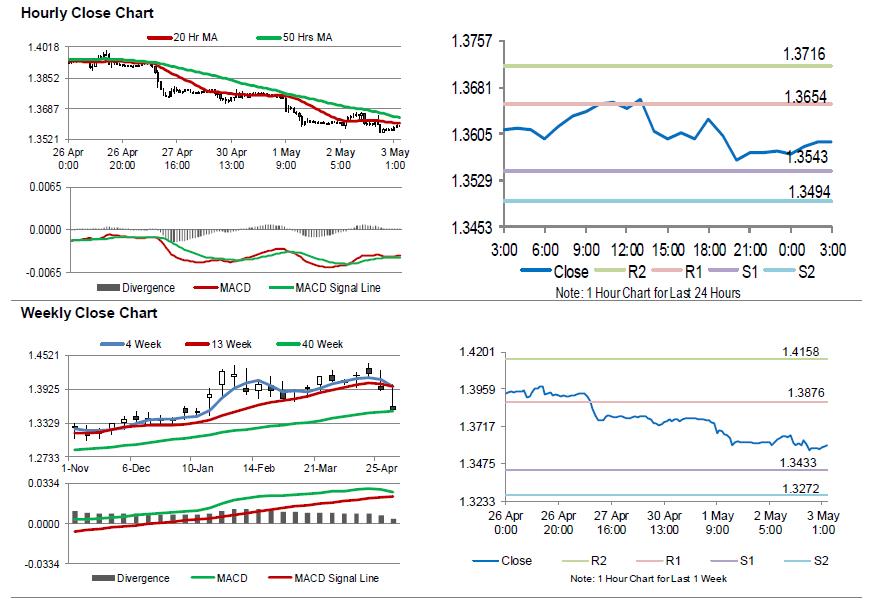

UK’s Construction Sector Bounced Back Into Expansion Territory In April

For the 24 hours to 23:00 GMT, the GBP declined 0.24% against the USD and closed at 1.3576, despite robust British construction sector data.

On the economic front, UK's Markit construction PMI rose more-than-estimated to a level of 52.5 in April, jumping back into the expansion territory and notching its highest level in 5 months. Market expectation was for the PMI to advance to a level of 50.5, after recording a level of 47.0 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.3593, with the GBP trading 0.13% higher against the USD from yesterday's close.

The pair is expected to find support at 1.3543, and a fall through could take it to the next support level of 1.3494. The pair is expected to find its first resistance at 1.3654, and a rise through could take it to the next resistance level of 1.3716.

Going ahead, investors would closely monitor UK's Markit services PMI for April, due to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1914; (P) 1.1973 (R1) 1.2008; More....

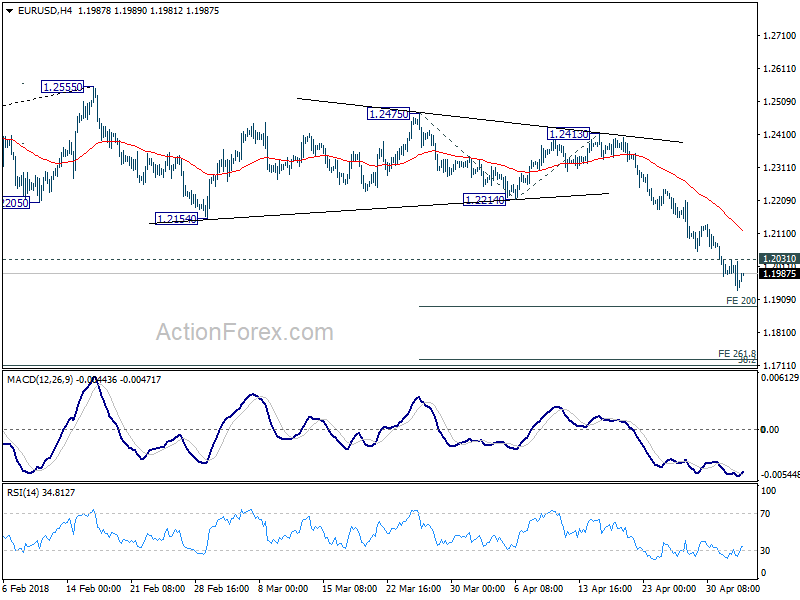

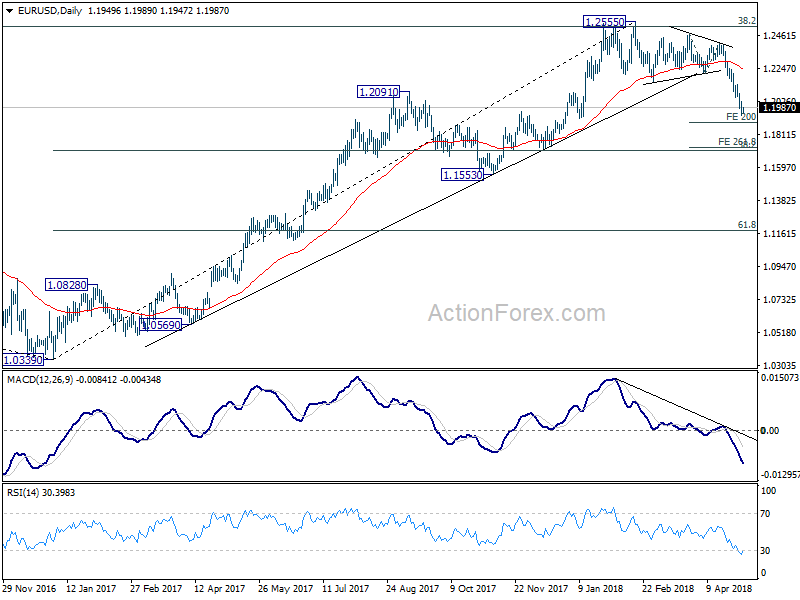

EUR/USD dipped further to as low as 1.1937 but started to lose downside momentum on oversold condition in 4 hour RSI. For the moment, intraday bias stays on the downside with 1.2031 minor resistance intact. Next target is 200% projection of 1.2475 to 1.2214 from 1.2413 at 1.1891. Break will target 261.8% projection at 1.1730. On the upside, though, break of 1.2031 will indicate short term bottoming and bring lengthier consolidation before staging another fall.

In the bigger picture, current decline and firm break of 1.2154 support confirms rejection by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. A medium term top should be in place at 1.2555 and deeper decline would be seen back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. With current downside acceleration, there is prospect of hitting 61.8% retracement at 1.1186 before completing the decline. But still, we'll need to look at the structure to before deciding if it's a corrective or impulsive move.

Dollar Retreats after FOMC; US, Eurozone and UK Data Awaited

Dollar trades generally lower in Asian session as it has turned into correction mode. While slightly more hawkish than expected, the FOMC statement released overnight provided little inspiration to the markets. Major US equity indices ended in red, with DOW dropped -0.72%, S&P 500 down -0.72% and NASDAQ lost -0.42%. 10 year yield also closed slightly lower by -0.012 to 2.964. In the currency markets, Dollar is staying as the strongest one for the week, followed by Canadian Dollar and Japanese Yen. The markets will looks into today's data from US, Eurozone and UK for more guidance.

Fed stands pat, more comfortable on inflation

As widely anticipated FOMC left the Fed funds rate target at 1.5-1.75% overnight. The accompanying statement also came in largely in line with our expectations – shrugging off moderation in first quarter growth and getting more confident in the inflation outlook. The central bank indicated that "both overall inflation and inflation for items other than food and energy have moved close to 2%", while in March, they noted that those barometers "have continued to run below 2%". Meanwhile, the members judged that "Inflation on a 12-month basis is expected to run near the Committee's symmetric 2% objective over the medium- term". A rate hike in June appears a done deal. The updated economic projections and the median dot plot would also be released in the June meeting. The market would be closely watching if the members have raised their rate hike expectations to four times from three. More in FOMC More Hawkish on Inflation, June Rate Hike a Done Deal

And more on FOMC:

- Fed Keeping Things Gradual with Steady Decision and Balanced Statement

- Amid Rising Inflation, The Fed Remains on Course

- Fed Stands Pat But Appears Ready to Hike More Given its Newfound Comfort with Inflation

Mnuchin arrives in Beijing as China warns to stand up to US bullying

US Treasury Secretary Steven Mnuchin arrives in Beijing today and is set to kick start trade negotiation with Chinese Vice-Premier Liu He. Mnuchin told reporter he's "thrilled to be here" upon arriving his hotel. The delegation planned to leave Friday evening.

Ahead of the meeting, the official China Daily said in a editorial that it will "stand up to the US' bullying as necessary". And "as a champion of globalisation, free trade and multilateralism, it will have strong support from the international community". It warned that "the US wants greater access to China's market, but it should not use trade actions as a battering ram to force China to open its doors."

Trump still claimed he always has a good relationship with Chinese President Xi in his tweet ahead of the meeting. He said that "Our great financial team is in China trying to negotiate a level playing field on trade! I look forward to being with President Xi in the not too distant future. We will always have a good (great) relationship!"

Australian Dollar lifted by large trade surplus and surge in building approvals

AUD trades broadly higher today as supported by solid economic data. Australia trade surplus came in at AUD 1.53B in March, widened from AUD 1.35B in February. That's also much larger than expectation of AUD 0.68B. Exports jumped 1% to AUD 34.84B, with strong 8% growth in n non-monetary gold to AUD 131m. Imports rose 1% to AUD 33.31B,. Non-monetary gold imports jumped 28% to AUD 232m.

Building approvals rose 2.6% mom in Mach, much higher than expectation of 1.0% mom. Justin Lokhorst, Director of Construction Statistics at the ABS noted that "the strength in the total dwellings series is being driven by approvals for private sector houses, which have now risen for 13 consecutive months." And, "private sector house approvals are now at their highest level since 2003, in trend terms."

Sterling and Euro to face more data tests

While Sterling and Euro survived yesterday's tests from economic data, they're both facing another day of event risks. From UK, PMI services is expected to climbed back from 51.7 to 53.5 in April. The data should show how well the economy is rebounded after "bad weather" in Q1. Eurozone will release CPI which is expected to be unchanged at 1.3% yoy in April. European Commission will also release new economic forecasts. Later in the day Canada will release trade balance. US will release trade balance, jobless claims, ISM services and factory orders.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1914; (P) 1.1973 (R1) 1.2008; More....

EUR/USD dipped further to as low as 1.1937 but started to lose downside momentum on oversold condition in 4 hour RSI. For the moment, intraday bias stays on the downside with 1.2031 minor resistance intact. Next target is 200% projection of 1.2475 to 1.2214 from 1.2413 at 1.1891. Break will target 261.8% projection at 1.1730. On the upside, though, break of 1.2031 will indicate short term bottoming and bring lengthier consolidation before staging another fall.

In the bigger picture, current decline and firm break of 1.2154 support confirms rejection by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. A medium term top should be in place at 1.2555 and deeper decline would be seen back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. With current downside acceleration, there is prospect of hitting 61.8% retracement at 1.1186 before completing the decline. But still, we'll need to look at the structure to before deciding if it's a corrective or impulsive move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | Trade Balance Mar | 1.53B | 0.68B | 0.83B | 1.35B |

| 1:30 | AUD | Building Approvals M/M Mar | 2.60% | 1.00% | -6.20% | -4.20% |

| 8:30 | GBP | Services PMI Apr | 53.5 | 51.7 | ||

| 9:00 | EUR | Eurozone PPI M/M Mar | 0.10% | 0.10% | ||

| 9:00 | EUR | Eurozone PPI Y/Y Mar | 2.10% | 1.60% | ||

| 9:00 | EUR | Eurozone CPI Estimate Y/Y Apr | 1.30% | 1.30% | ||

| 9:00 | EUR | Eurozone CPI Core Y/Y Apr A | 0.90% | 1.00% | ||

| 9:00 | EUR | European Commission Economic Forecasts | ||||

| 11:30 | USD | Challenger Job Cuts Y/Y Apr | 39.40% | |||

| 12:30 | CAD | International Merchandise Trade (CAD) Mar | -2.0B | -2.7B | ||

| 12:30 | USD | Nonfarm Productivity Q1 P | 1.00% | 0.00% | ||

| 12:30 | USD | Unit Labor Costs Q1 P | 3.00% | 2.50% | ||

| 12:30 | USD | Initial Jobless Claims (APR 28) | 225K | 209K | ||

| 12:30 | USD | Trade Balance Mar | -55.6B | -57.6B | ||

| 13:45 | USD | US Services PMI Apr F | 54.4 | 54.4 | ||

| 14:00 | USD | ISM Non-Manufacturing/Services Composite Apr | 58.1 | 58.8 | ||

| 14:00 | USD | Factory Orders Mar | 1.40% | 1.20% | ||

| 14:30 | USD | Natural Gas Storage | -18B |

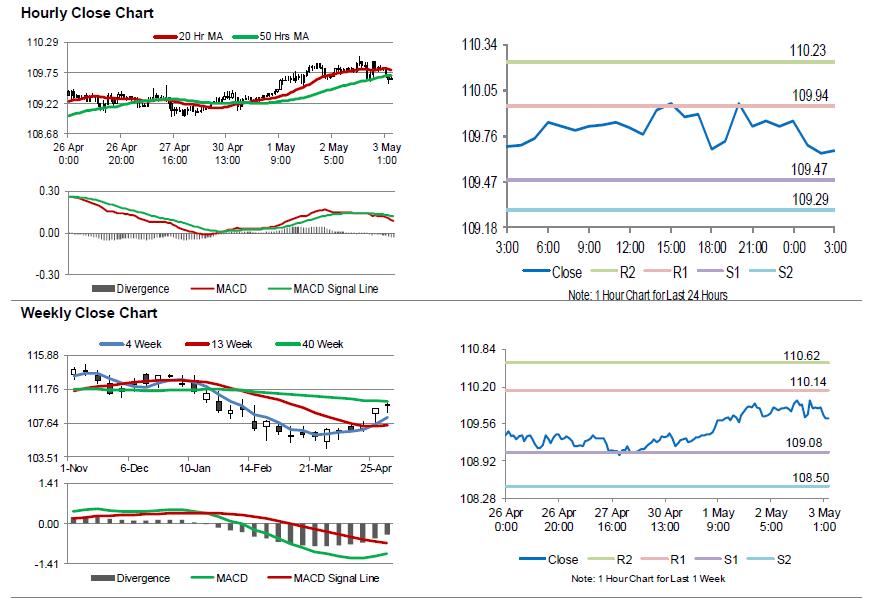

Japanese Yen Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.08% against the JPY and closed at 109.82.

In economic news, Japan’s consumer confidence index unexpectedly fell to a level of 43.6 in April, compared to a reading of 44.3 in the previous month and defying market consensus for a rise to a level of 44.5.

In the Asian session, at GMT0300, the pair is trading at 109.66, with the USD trading 0.15% lower against the JPY from yesterday’s close.

The pair is expected to find support at 109.47, and a fall through could take it to the next support level of 109.29. The pair is expected to find its first resistance at 109.94, and a rise through could take it to the next resistance level of 110.23.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.