Sample Category Title

USDJPY Trades Lower After Cracking 110 Level

The U.S dollar has started to trade lower against the Japanese yen currency, after the FOMC Policy Decision provoked a broad-based sell-off in the U.S dollar index. The USDJPY pair currently trades around the 109.65 level, having previously moved above the 110.00 level, hitting 110.03 on Wednesday. Trading are likely to be increasingly focused on the 110.00 handle, ahead of Friday’s key Non-farm Payrolls job report from the United States economy.

The USDJPY pair retains its intraday bullish bias while trading above the 109.45 level, key resistance is now found at the 110.03 and 110.40 levels.

If the USDJPY pair does move below the 109.45 level, the 109.00 and 108.50 levels offer the strongest form of technical support.

Bitcoin Rises As Goldman Sachs Pushes Forward With Trading Operation

After weeks of pressure, bitcoin reached a low of $6400 in early April. Since then, the cryptocurrency has been gaining, reaching a high of $9630.

Overnight, the BTC/USD pair continued to rally following a report by New York Times that Goldman Sachs is moving ahead with plans to set up a bitcoin trading operation – the first of its kind at a Wall Street bank.

According to the report, Goldman Sachs will be using its own money to trade with clients in contracts linked directly to the price of bitcoin. If they succeed in getting all regulatory approvals, it could perhaps spark a new trend with other banks looking to follow suit.

The bold move by Goldman Sachs is somewhat surprising considering regulation worries and the recent negative press surrounding crypto trading. Lloyd Blankfein, the CEO of Goldman Sachs, was himself a previous crypto critic arguing that currencies might not be around for a long time.

The recent news from Goldman Sachs comes months after a report by Deal Breaker revealed that the company was looking into joining the crypto frenzy. The company’s entry could lead to more demand by institutional investors which could push the price of bitcoin even higher.

Eurozone CPI Data To Make Headlines On Thursday

Thursday will be another active session on the economic calendar, with high-profile data from the Eurozone and United States scheduled to make headlines.

The European data wire begins at 08:00 GMT with a report on Spanish unemployment. The number of people unemployment is forecast to fall by 100,200 in April, according to a median estimate of analysts.

Markit will report on UK services PMI at 08:30 GMT. The monthly indicator is forecast to show a rise of 1.8 points to 53.5 for April.

The European Commission's statistics agency will report on consumer prices at 09:00 GMT. The consumer price index (CPI) for the 19-member Eurozone is forecast to rise 1.3% annually in April, unchanged from the previous month. So-called core inflation, which strips away volatile goods such as food and energy, is expected to come in at 1.2% following a 1% reading the month before.

The Eurozone's producer price index (PPI) will also be released at 09:00 GMT. Factory gate prices are forecast to rise 2.1% annually in March, up from 1.6% the prior month.

In terms of monetary policy, three European Central Bank (ECB) officials are scheduled to deliver speeches on Thursday. They are Peter Praet, Vitor Constancio and Benoit Coeure.

Shifting gears to North America, the US Department of Commerce will release the monthly trade balance report at 12:30 GMT. Washington's deficit is forecast to fall to $50 billion in March from $57.6 billion the month before.

Separately, the Department of Labor will report on initial jobless claims for the week ended 28 April. The number of Americans filing for first time unemployment benefits likely rose by 16,000 to a seasonally adjusted 225,000.

North of the border, the Canadian government will report on international merchandise trade at 12:30 GMT. Canada's trade deficit is forecast to narrow to $2.24 billion in March from $2.69 billion the month before.

EUR/USD

A strong dollar continued to depress the euro on Wednesday, as the EUR/USD exchange rate fell back below 1.2000. At the time of writing, the pair was trading at 1.1951. It now faces immediate support at the 1.1935 level. On the opposite side of the ledger, resistance is likely met at 1.2030.

GBP/USD

Cable's precipitous drop appears to have slowed over the past two days, although the underlying outlook remains firmly entrenched in bearish pressure. GBP/USD is currently trading around 1.3572 having fallen below key levels of support.

USD/CAD

USD/CAD has rallied sharply over the past two weeks. On Wednesday, gains slowed as the currency pair hovered below 1.2900. A bullish US dollar may provide further room for growth in the near term as the loonie continues to shrug off rising oil prices.

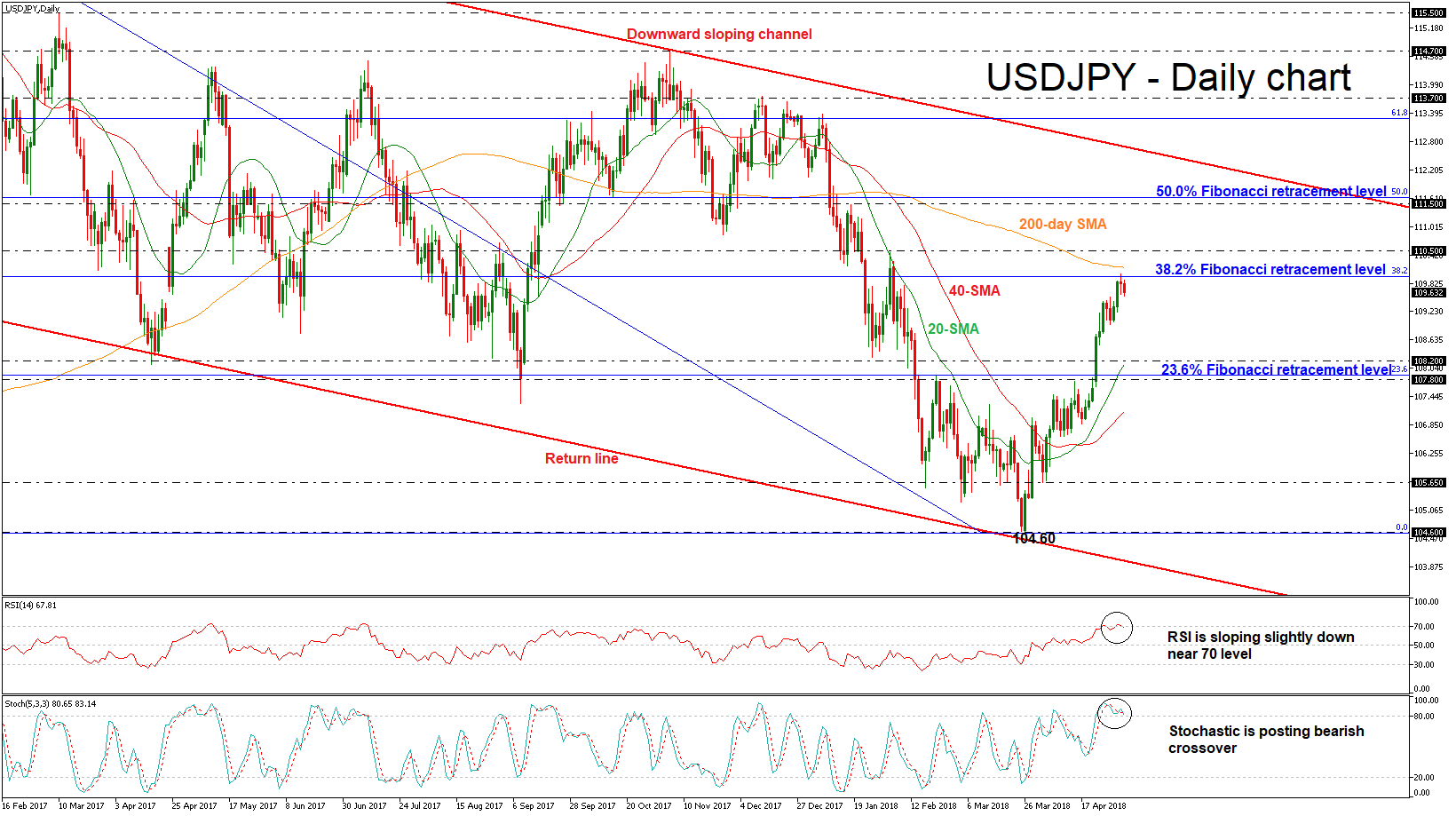

USDJPY Pares Some Gains After Challenging 3-Month High Of 110.00 Key Level

USDJPY has been recording a stunning bullish rally since it hit a 16-month low of 104.60 on March 23. The pair extended its run earlier this week recording a fresh three-month high near the 110.00 psychological level. However, during today’s early session the pair is trading slightly lower paring some gains.

From the technical point of view, the price is approaching the 200-day simple moving average near 110.20, which is acting as strong resistance in the medium-term, while it is developing well above the 20- and 40-SMAs in the short-term. The RSI indicator is running out of steam as it is sloping down around the 70 level, while %K line of the stochastic oscillator is posting a bearish cross with the %D line in the overbought zone, signaling bearish pressure in the price action.

After the bounce off the 38.2% Fibonacci retracement level of 110.00 of the downleg from 118.60 to 104.60, there is a possibility of bearish movement until the next immediate support of 108.20. If the price continues the downward tendency it could open the way towards the 107.80 barrier.

On the flip side, if prices successfully surpass the 38.2% Fibonacci mark could reinforce the bullish move and drive the pair until the 110.50 resistance level taken from the peak on January 18. A jump above the aforementioned obstacle could push the price further up towards 115.50, which holds near the 50.0% Fibonacci.

As a side note, the pair has been consolidating within a downward sloping channel since December 2016 and touched the lower boundary at the end of March, creating a 16-month low of 104.60.

UK Services PMI For April Expected To Rebound And Strengthen

At 08:30 GMT, UK Markit Services PMI (Apr) is expected to come in at 53.5 from 51.7 previously. This data has continued to decline from its 2013 high of 62.5 and had fallen below 53.0 last time out, which had been somewhat of a floor over the past 18 months. The number is expected to move back above 53.0 today, showing modest growth. Failure to do this will put GBP under further pressure.

At 09:00 GMT, Eurozone Consumer Price Index – Core (YoY) (Apr) is expected to be 0.9% against the previous 1.0%. Consumer Price Index (YoY) (Apr) is expected to be unchanged at 1.3%. The recovery in the Euro area is still strong and growing, despite some questionable economic data which may be weather related. CPI is stabilizing around 1.2%/1.3%. EUR crosses may be impacted by this data release.

At 12:30 GMT US Continuing Jobless Claims (Apr 20) is expected to be 1.838M against 1.837M previously. Initial Jobless Claims (Apr 27) is expected to come in at 225K against 209K previously. This data is showing an increase in the number of people who are jobless. Nonfarm Productivity (Q1) is expected to be in at 0.9% against 0.0% previously. Unit Labour Costs (Q1) is expected to be 2.9% against 2.5% prior, showing what has become an expected seasonal increase in this metric, although these costs may be passed onto consumers. Trade Balance (Mar) is expected to be $-50.0B against a previous $-57.6B, reaching levels not seen since 2008. USD crosses may see an increase in volatility from this data release.

At 12:30 GMT, Canadian International Merchandise Trade (Mar) is expected to be $-2.24B against a previous number of $-2.69B. This data is off the low from August 2017 but still shows a negative imbalance. CAD pairs could be moved by this data.

At 13:45 GMT, US Markit Services PMI (Apr) is expected to be unchanged at 54.4. This data is stable at present but a miss today may provoke a market reaction. Markit PMI Composite (Apr) is expected to be 55.2 against 54.8 previously, with consensus pointing to a pick-up in this metric. USD pairs could be moved by this data series.

At 14:00 GMT, US ISM Non – Manufacturing PMI (Apr) is expected to be 58.1 against 58.8 previously. This is still in the upper range of the data releases we have seen over the past seven years but off the highs of above 65.0 reached before the financial crisis. Factory Orders (MoM) (Mar) is expected to be 1.4% from 1.2% prior. This data can be volatile and the expectation is for a positive reading but numbers are expected to remain in the recent range of +3.0% to -3.0%. USD traders will be closely watching this release.

At 16:00 GMT, SNB Chairman Jordan will deliver a speech titled “This is Why the Vollgeld Initiative Harms Switzerland” at the Swiss Institute for Banking and Finance, in Zurich. CHF crosses may be moved by this data.

USD Falls Then Reverses As US Fed Leaves Rates At 1.75%

The US Fed's Monetary Policy Statement and Interest Rate Decision were released yesterday evening, with the rate left unchanged at 1.75%. The market is pricing in two to three hikes in 2018, with a slight bias for three to four that could strengthen the dollar position. The Monetary Policy Statement set a slightly hawkish tone, tempered by the Fed saying it would let inflation run a bit above their 2% target. But the underlying factors in the market soon re-established themselves and the market was caught off-guard as the initial reactionary trade post FOMC reversed. EURUSD initially moved higher from 1.19546 to 1.20252 before creating a new low at 1.19376, while USDCAD initially fell from 1.28570 to 1.28097 before moving to a high of 1.28867. Asian equities are lower again today, as markets worry about US/China trade talks. US Equities have failed to follow European Equity markets higher, as the impact from FX is felt.

UK Construction PMI (Apr) came in at 52.5 v an expected headline number of 50.5, from 47.0 prior. The consensus was for a recovery in the numbers after a softening from the high of 53.1 created in December. The industry had slipped under 50.0 from the high level of 64.6 in 2014, showing a contraction in the index. This data is strong as we head into summer. GBPUSD moved higher from 1.36295 to 1.36655 after this data release.

Eurozone Unemployment Rate (Mar) was as expected, unchanged at 8.5%, a level not previously seen since April 2009. Gross Domestic Product s.a. (QoQ) (Q1) was as expected at 0.4%, from 0.6% previously. Gross Domestic Product s.a. (YoY) (Q1) was also as expected at 2.5%, against 2.7% previously. GDP numbers matched estimates and, although they are down on the previous readings, as these are quarterly figures the decline can be explained somewhat by severe weather in Europe. EURUSD moved up from 1.19932 to 1.20096 following this data release.

US ADP Employment Change (Apr) was 204K versus an expected 200K, against 241K previously, which was revised down to 228K. This data has remained above 200 for the last four months, showing that the US economy is continuing to add jobs. However, this was a decline on the previous month and the smallest monthly increase since November. USDCAD moved higher from 1.28210 to 1.28825 after this data came out.

EURUSD is up 0.30% overnight, trading around 1.19867.

USDJPY is down -0.21% in early session trading at around 109.595.

GBPUSD is up 0.25% this morning, trading around 1.36054.

Gold is up 0.38% in early morning trading at around $1,309.84.

WTI is up 0.16% this morning, trading around $67.76.

Currencies: Fed Brings Balanced Message For The Dollar

Rates: No surprises from the Fed

The Fed kept its policy unchanged and prepared a June rate hike. The US central bank sounded more upbeat in its inflation assessment, but added that the 2% target is symmetric. It suggests no intention to step up the tightening cycle if inflation overshoots the target and probably explains the slight correction lower at the front end of the US yield curve.

Currencies: Fed brings balanced message for the dollar

Yesterday, the dollar remained well bid going into the Fed policy decision. The Fed might allow a slight overshoot of the inflation target. This could be slightly negative for ST US yields and the dollar. However, for now the ‘damage’ for the US currency remains very limited. Tomorrow’s payrolls might decide whether there is room for further USD gains.

The Sunrise Headlines

- US stock markets closed 0.5% to 0.75% lower yesterday. An attempt to gain ground after the Fed statement failed miserably. Asian equity indices lose up to 0.5% with Hong Kong underperforming (-1.5%).

- The Fed kept its monetary policy unchanged, but sounded more confident in the inflation outlook, suggesting more tightening ahead. A reference to its “symmetric” inflation target suggests no speeding up the hiking pace for now.

- A US trade delegation arrived in Beijing for key talks over tariffs, with Chinese state media saying China will stand up to U.S. bullying if needed but that it was still better to hash things out around the negotiating table (Reuters).

- UK PM May is facing a crisis after pro-Brexit ministers paired up with Conservative hardliners to demand a clean break from the EU’s customs system, rejecting her plea for a compromise solution. (BB)

- The UK House of Lords voted 309 to 242 in favour of a change to the government’s EU (Withdrawal) Bill, designed to protect the Irish peace process in another blow to PM May’s government. (BB)

- Trump lawyer Giuliani said the president had repaid his longtime attorney, Cohen, for a $130k payment he made to a former adult film star in October 2016 in exchange for her silence about an alleged sexual encounter. (WSJ)

- Today’s eco calendar contains EMU inflation data, the services PMI (UK) / ISM (US), US weekly jobless claims. The Norges bank holds its policy meeting. Spain & France tap the market and several ECB governors speak.

Currencies: Fed Brings Balanced Message For The Dollar

Fed brings mixed message for the dollar.

The dollar stayed well bid yesterday going into the Fed decision. The Fed left its policy unchanged and signalled more gradual normalization. Powell and Co explicitly said that the 2% inflation target is ‘symmetric’. This suggests it might accept some ST inflation overshoot without taking bolder action. Short-term US yields and the dollar dropped slightly after the Fed statement, but the USD correction was modest and short-lived. EUR/USD closed the session at 1.1951. USD/JPY finished at 109.84.

Asian equities mostly show moderate losses overnight, joining the slightly disappointing reaction of US equities to the Fed statement. The dollar runs into resistance. EUR/USD rebounded to the high 1.19 area. USD/JPY loses a few ticks (currently 109.65area). The Aussie dollar tries a cautious rebound on better than expected foreign trade and housing data. AUD /USD (0.7520 area) dropped temporary below 0.75 earlier this week, touching the lowest level since mid-2017.

The eco calendar is well filled today EMU headline inflation is expected to ease to 1.3% Y/Y. The report might ‘approve’ the cautious ECB approach (slightly euro negative?). The EC updates its economic forecasts. The US calendar contains the non-manufacturing ISM, weekly jobless claims and the trade balance. The ISM is expected to ease slightly to 58.0. We also keep an eye at the prices subseries of the report. The dollar remained well bid yesterday despite a balanced Fed statement. The focus now turns to tomorrow’s US payrolls. EUR/USD came close to the 1.1936 support area (62% retracement), but a real test didn’t occur. USD/JPY tested the 110 big figure. We expect some consolidation on the recent USD rally today. The payrolls will probably have to be solid (including wages) to support further USD gains short-term.

Sterling enjoyed a temporary short-squeeze yesterday supported by a good UK construction PMI. However, the move petered out soon as Pro-Brexit Ministers rejected a middle-of the road solution for the post-Brexit relationship with EMU. EUR/GBP returned to the 0.88 area. The UK services PMI is expected at 53.4 (from 51.7) today. We see a slight asymmetric risk: sterling might be more sensitive to a negative surprise rather than to a small positive surprise. Brexit noise will proably persist and might continue to weigh on sterling.

EUR/USD: dollar rally to slow as Fed maintains balanced approach?

Markets Cautiously Await Outcome Of US Trade Delegation To China

General Trend:

- Asian equity markets are generally lower, in line with US trading session; Participation limited by Japanese holiday

- Australia ASX 200 outperforms on gains in the consumer discretionary and resources sectors

- National Australia Bank (NAB) Q1 profits above ests; noted possible impact of higher short-term funding costs

- Amazon to launch new fulfillment center in Australia

- Hang Seng declines, smartphone maker Xiaomi confirms massive IPO

- Hang Seng Telecom index declines over 1%; US White House reportedly mulling restricting equipment sales by China telecom companies on national security risk grounds (press)

- Hong Kong gaming giant SJM rises over 2% after Q1 earnings

- China/US trade talks expected to begin today, continue on Friday

- Aussie rises after better than expected March Trade Balance and Building Approvals data; little impact seen on bond market

- Analysts continue to push back calls for RBA rate hike: CBA now sees hike in Feb 2019 v Nov 2018 prior

- RBA is expected to release its quarterly statement on monetary policy (SOMP) and forecasts on Friday, May 4th; Gov Lowe suggested no major changes expected

- China and Japan speculated to discuss reopening of currency swap line next week

- USD/JPY trades below ¥110.00 post FOMC

- Japan markets are closed on Friday for holiday

- UK April Services PMI due for release later today

Headlines/Economic Data

Japan

- Nikkei 225 closed for holiday

- Takeda Pharma, 4502.JP There is speculation that the company may receive ¥3.0T loan from a group of banks - Japanese Press

- (JP) Japan and China said to examine plan to revive bilateral currency swap agreement - Japanese Press

Korea

- Kospi opened +0.1%

- 005380.KR Hyundai/Kia Apr China Sales more than doubled y/y - press

- 028260.KR Elliott confirmed taking legal action against the former South Korean administration over its illegal intervention in the merger between Samsung C&T and Cheil Industries in 2015

- Shares of Kepco Plant [051600.KR] have declined by over 14% after Q1 earnings report

- (KR) Bank of Korea (BOK) Apr Minutes: One member noted that the current accomodative policy is desirable as both internal and external uncertainties arise (after the close)

China/Hong Kong

- Hang Seng opened -1%, Shanghai Composite -0.2%

- Hang Seng Property/Construction Index -1.8%, Info Tech -1.4%, Financials -1.4%, Materials -1.4%, Telecom -1.3%

- Esprit Holdings [330.HK] declines over 1%, plans to exit Australia and New Zealand

- (CN) China Environment Ministry: Three northern cities have been ordered to halt approvals related to new polluting projects for 6 months

- (CN) China PBoC Open Market Operation (OMO): Injects CNY50B in 7-day reverse repos v CNY200B prior; Net: drains CNY70B v nil prior

- PBoC: CNY156B in medium-term lending facilities (MLF) to mature in May

- (CN) China PBoC sets yuan reference rate at 6.3732 v 6.3670 prior

- (CN) China State Council: China will further improve its business environment by halving the time required to open a business and start construction projects - Xinhua

- (CN) Study by National Retail Federation (NRF) and the Consumer Technology Association (CTA) finds US tariffs and follow on retaliation by China would reduce US output by ~$3B and nearly 134,000 workers would lose jobs, most of whom are less-skilled workers

- (CN) Since mid-April the PBoC has on various occasions fixed the Yuan (CNY) midpoint weaker than consensus expectations, could suggest concern in China about competing countries in the emerging markets (EM) – financial press

- (RU) Russia doubled its capacity of pipeline exports to China recently as seaborne shipments to Europe have been falling, China on track to replace EU as Russia's top oil customer

- (CN) PBOC announces rules on overseas securities investments by domestic companies: Overseas FX purchase not allowed under RQDII scheme

- (HK) HKMA Chief Chang: Local interest rates should rise along with USD rates; HK$/USD gap attracts carry trade activities

- (HK) Hong Kong HKD 3-month Hibor at 1.66550%, continues to trade at highest level since 2008

Australia/New Zealand

- ASX 200 opened +0.1%, closed +0.8%

- ASX 200 Resources index +1.4%, Telecom +0.9%,Utilities +0.8%, Consumer Discretionary +0.8%, Energy +0.7%, Financials +0.5%; REIT -0.1%

- (AU) AUSTRALIA MAR TRADE BALANCE (A$):1.53B V 865ME (3RD STRAIGHT SURPLUS)

- (NZ) New Zealand April ANZ Job Advertisements M/M: -2.1% v 0.9% prior

- (AU) Australia Apr AIG Performance of Services Index: 55.2 v 56.9 prior

- (AU) Australia Apr CBA PMI Services: 55.2 v 55.6 prior; Composite: 55.3 v 55.4 prior

- (AU) AUSTRALIA MAR BUILDING APPROVALS M/M: 2.6% V 1.0%E; Y/Y: 14.5% V 10.6%E

- NAB.AU Reports H1 (A$) Cash profit 3.29B (ex restructuring costs) v 2.77Be, Net Op Rev 9.1B v 8.87B y/y

- (NZ) New Zealand sells NZ$100M v NZ$100M indicated in Inflation-Indexed Sept 2040 bonds, avg yield 2.1452%

- (NZ) New Zealand PM Ardern urges domestic businesses to show confidence in the government - US financial press

Other Asia

- United overseas bank, UOB.SG Reports Q1 (S$) Net 978M v 807M y/y; Net interest income 1.47B v 1.30B y/y

- (SG) Singapore Fin Min Heng: Singapore should try harder to reach GDP more than 2-3% annually

North America

- US equity markets closed mostly lower: Dow -0.7%, S&P500 -0.7%, Nasdaq -0.4%, Russell 2000 +0.3%

- S&P500 Consumer Staples -2%, Health Care -1.4%

- XRX Reports Q1 $0.68 v $0.15 y/y, Rev $2.44B v $2.45B y/y; Withdraws guidance due to pending nominations

- LOGI Reports Q4 $0.32 v $0.30 y/y, Rev $592.4M v $510.6M y/y, affirms guidance

- XPO Logistics [XPO]: Said to consider up to $8.0B in new deals - FT

- (US) FOMC HOLDS TARGET RATE RANGE AT 1.50-1.75% (AS EXPECTED); INFLATION HAS MOVED CLOSE TO 2% TARGET SINCE MARCH

- (US) President Trump Lawyer Giuliani: Odds are Trump won't be interviewed by Mueller, but does not rule out interview

- (US) DOE CRUDE: +6.2M V +1ME

- Q1 gold demand 973.5T, -7% y/y (weakest Q1 in 10-yrs) - World Gold Council

Europe

- (UK) UK core cabinet said to make no decision on post-Brexit customs during ministers meeting; Hybrid customs union idea appears dead - press

- (UK) House of Lords votes in support of power to prevent a hard border in Ireland; Votes 309-242 to ensure no hard border, defying PM May's position - press

- (EU) ECB's Weidmann (Germany): ECB should not unnecessarily delay its exit from stimulus

- (SA) Saudi Oil Min: producers are monitoring markets and will adjust plans if needed

- Shire [SHP.UK]: There is speculation that Takeda may receive ¥3.0T (~$27.4B) loan from a group of banks - Japanese Press

Levels as of 02:00ET

- Hang Seng -1.4%; Shanghai Composite +0.2%; Kospi -0.5%

- Equity Futures: S&P500 +0.1%; Nasdaq100 +0.0%, Dax +0.2%; FTSE100 +0.2%

- EUR 1.1989-1.1948; JPY 109.88-109.57; AUD 0.7527-0.7485;NZD 0.7012-0.6991

- Jun Gold +0.4% at $1,310/oz; Jun Crude Oil -0.2% at $67.83/brl; Jul Copper +0.4% at $3.08/lb

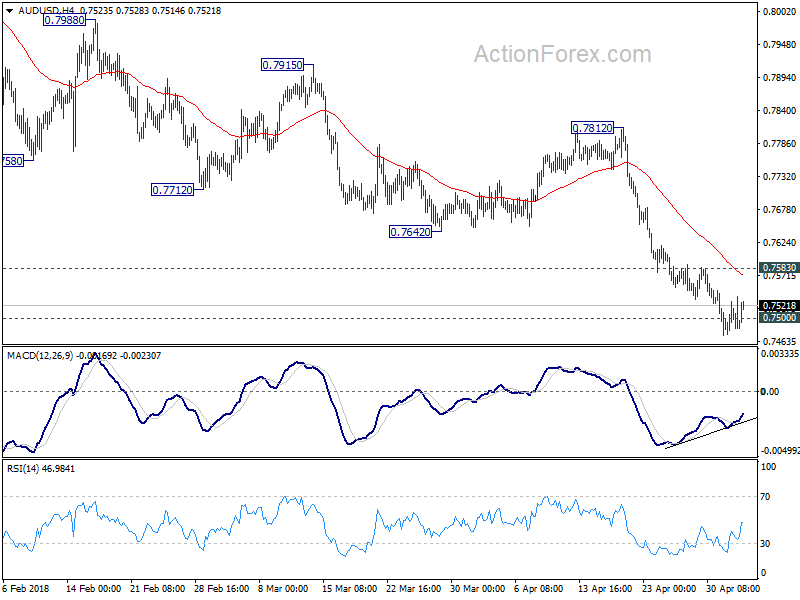

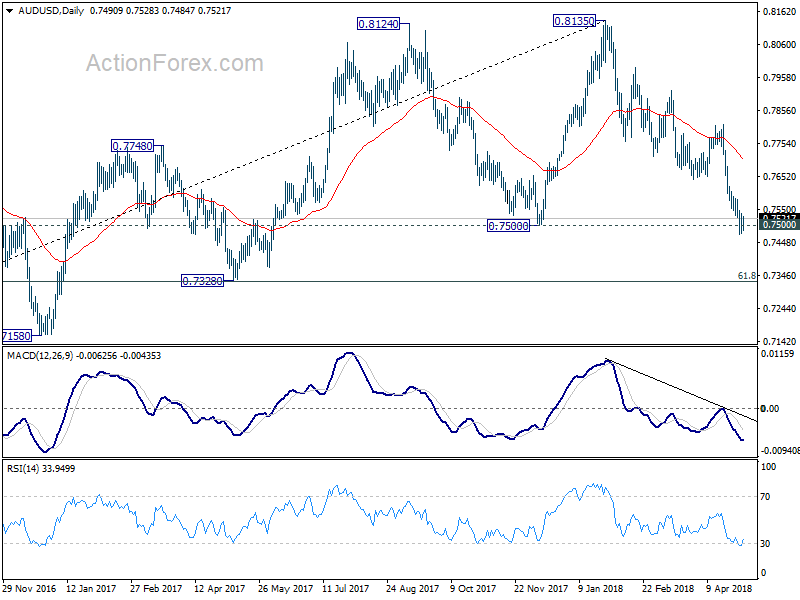

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7465; (P) 0.7501; (R1) 0.7527; More...

AUD/USD continues to lose downside momentum, as seen in 4 hour MACD, as it's drawing support from 0.7500. But with 0.7583 minor resistance intact, further fall is still expected. Sustained break of 0.7500 key support level will indicate medium term reversal and target next support at 0.7328. Nonetheless, break of 0.7583 will suggest short term bottoming. In that case, stronger rebound would be seen back to 0.7642 support turned resistance.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Decisive break of 0.7500 key support will suggest that such correction is completed. In that case, deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

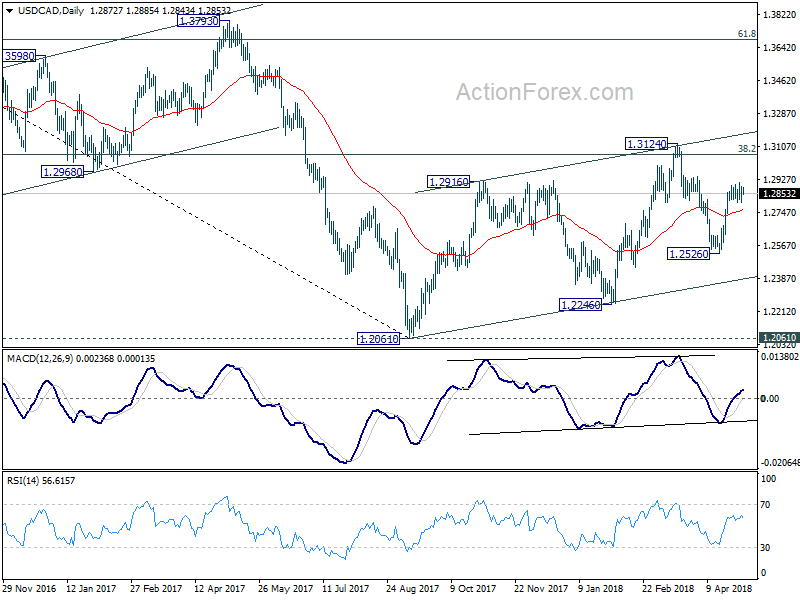

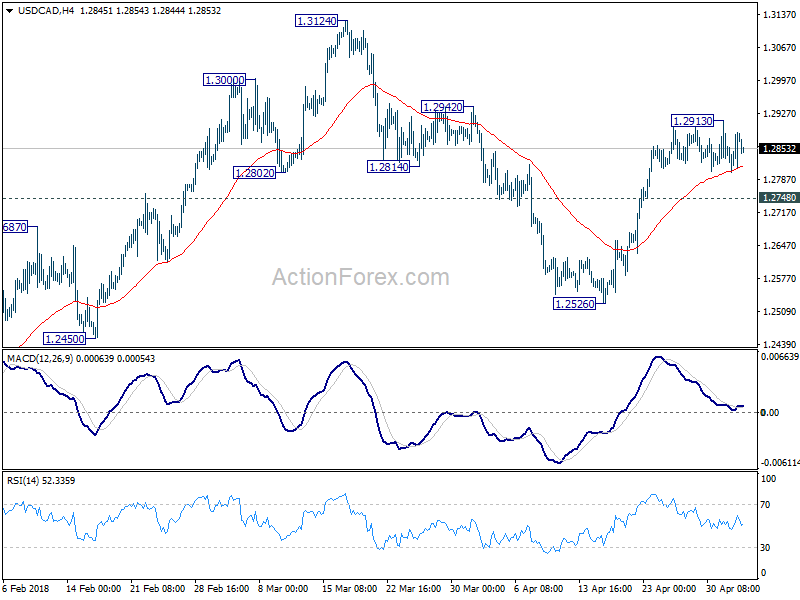

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2827; (P) 1.2857; (R1) 1.2912; More....

Intraday bias in USD/CAD remains neutral for consolidation below 1.2913 temporary top. As long as 1.2748 minor support holds, further rally is expected. Break of 1.2913 will turn bias back to the upside for 1.3124 high. However, break of 1.2748 will turn focus back to 1.2526 support instead.

In the bigger picture, current development suggests that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685.