Sample Category Title

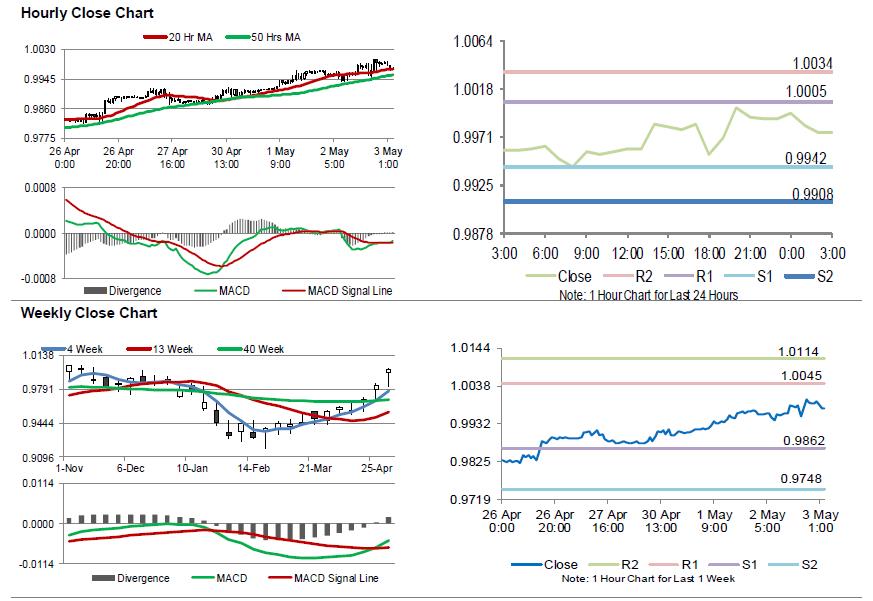

Swiss Real Retail Sales Fell In March, SVME PMI Surprised On The Upside In April

For the 24 hours to 23:00 GMT, the USD rose 0.22% against the CHF and closed at 0.9989.

Macroeconomic data revealed that Switzerland’s real retail sales declined 1.8% on an annual basis in March, after recording a drop of 0.2% in the previous month.

On the contrary, the nation’s SVME manufacturing PMI unexpectedly climbed to a level of 63.6 in April, confounding market expectations for a fall to a level of 59.8. The PMI had recorded a reading of 60.3 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 0.9976, with the USD trading 0.13% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9942, and a fall through could take it to the next support level of 0.9908. The pair is expected to find its first resistance at 1.0005, and a rise through could take it to the next resistance level of 1.0034.

Later today, a speech by the SNB Chairman, Thomas Jordan, will be eyed by market participants.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

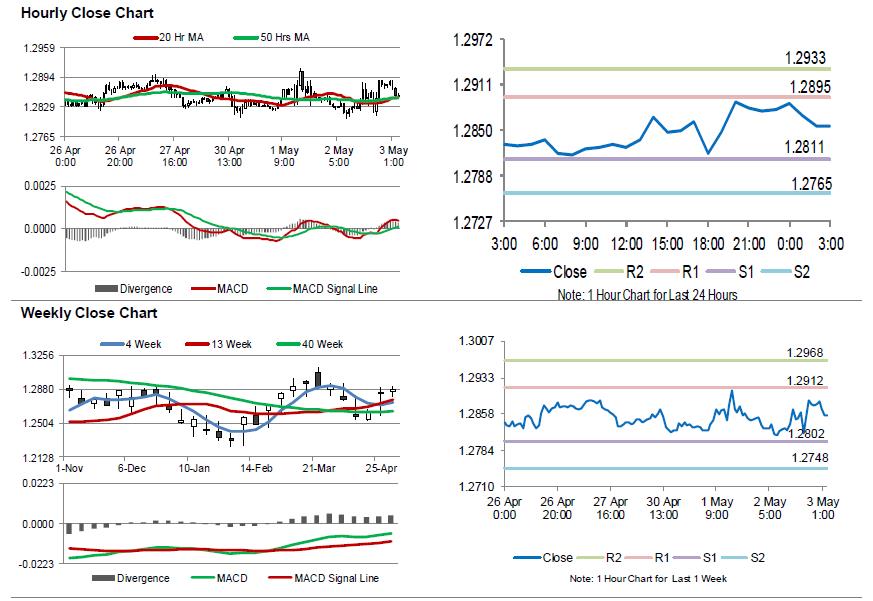

Loonie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.24% against the CAD and closed at 1.2878.

In the Asian session, at GMT0300, the pair is trading at 1.2856, with the USD trading 0.17% lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2811, and a fall through could take it to the next support level of 1.2765. The pair is expected to find its first resistance at 1.2895, and a rise through could take it to the next resistance level of 1.2933.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

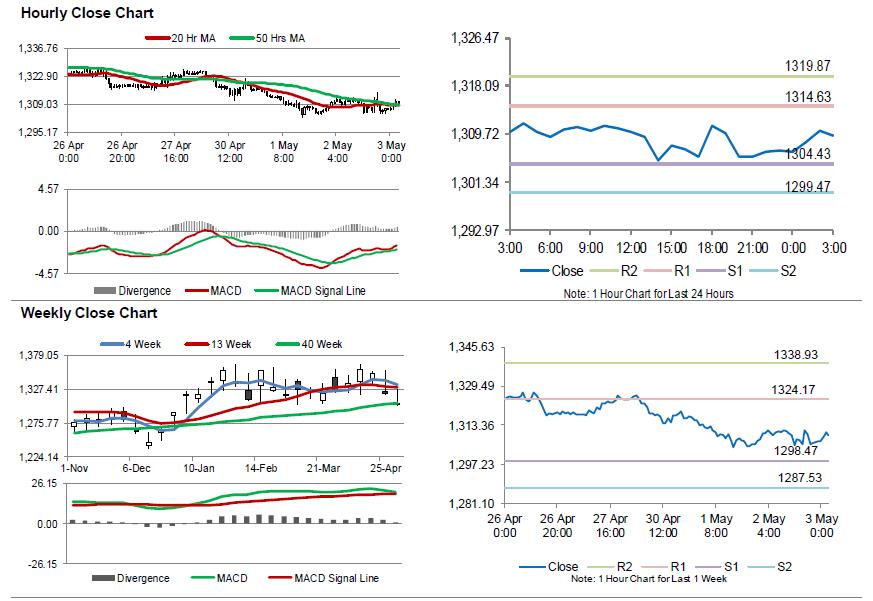

Gold: Yellow Metal Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, Gold rose 0.07% against the USD and closed at USD1306.60 per ounce, after the Fed reiterated that interest rates would rise only gradually.

In the Asian session, at GMT0300, the pair is trading at 1309.40, with gold trading 0.21% higher against the USD from yesterday’s close.

The pair is expected to find support at 1304.43, and a fall through could take it to the next support level of 1299.47. The pair is expected to find its first resistance at 1314.63, and a rise through could take it to the next resistance level of 1319.87.

The yellow metal is showing convergence with its 20 Hr and 50 Hr moving averages.

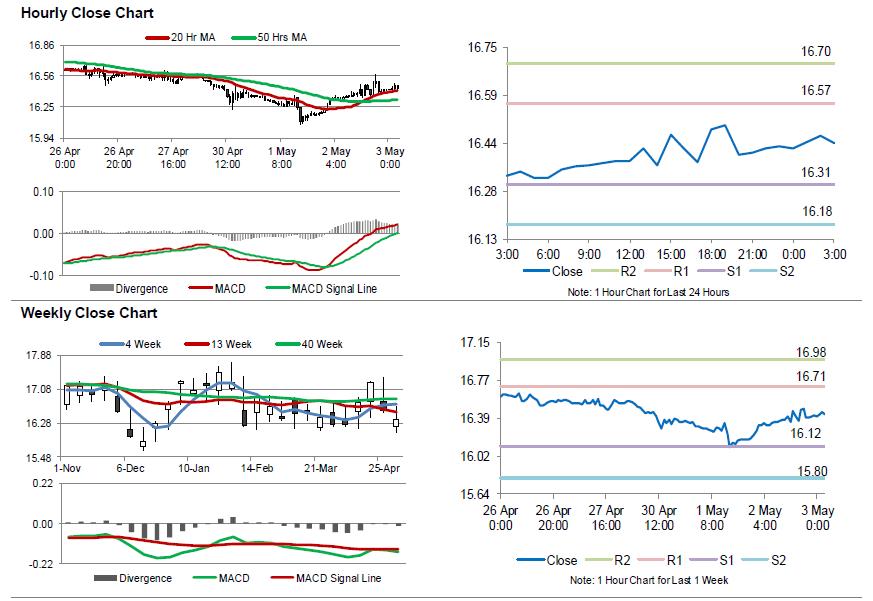

Silver: White Metal Extends Its Gains In The Morning Session

For the 24 hours to 23:00 GMT, Silver rose 1.42% against the USD and closed at USD16.43 per ounce, tracking gains in gold prices.

In the Asian session, at GMT0300, the pair is trading at 16.44, with silver trading 0.06% higher against the USD from yesterday’s close.

The pair is expected to find support at 16.31, and a fall through could take it to the next support level of 16.18. The pair is expected to find its first resistance at 16.57, and a rise through could take it to the next resistance level of 16.70.

The white metal is trading above its 20 Hr and 50 Hr moving averages.

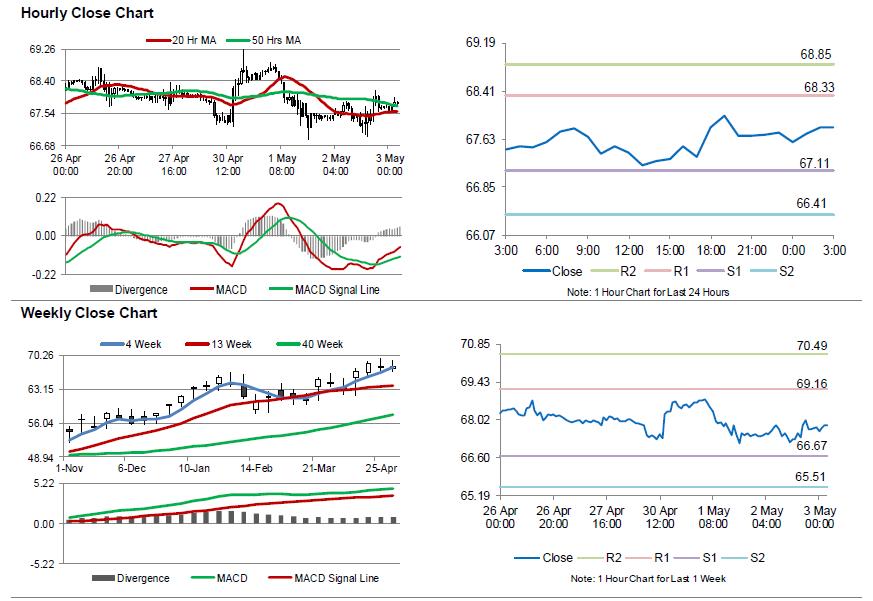

Crude Oil: Oil Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, Crude Oil rose 0.43% against the USD and closed at USD67.73 per barrel, pushed up by persistent concerns that the US may reimpose sanctions on major OPEC member, Iran. Moreover, the International Monetary Fund threatened to expel Venezuela, raising concerns over the nation's crude production.

Separately, the Energy Information Administration (EIA) indicated that US crude oil stockpiles jumped by 6.2 million barrels to 435.96 million barrels in the week ended 27 April.

In the Asian session, at GMT0300, the pair is trading at 67.82, with oil trading 0.13% higher against the USD from yesterday's close.

The pair is expected to find support at 67.11, and a fall through could take it to the next support level of 66.41. The pair is expected to find its first resistance at 68.33, and a rise through could take it to the next resistance level of 68.85.

Crude oil is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Mnuchin arrives in Beijing as China warns to stand up to US bullying

US Treasury Secretary Steven Mnuchin arrives in Beijing today and is set to kick start trade negotiation with Chinese Vice-Premier Liu He. Mnuchin told reporter he's "thrilled to be here" upon arriving his hotel. The delegation planned to leave Friday evening.

Ahead of the meeting, the official China Daily said in a editorial that it will "stand up to the US' bullying as necessary". And "as a champion of globalisation, free trade and multilateralism, it will have strong support from the international community". It warned that "the US wants greater access to China's market, but it should not use trade actions as a battering ram to force China to open its doors."

Trump still claimed he always has a good relationship with Chinese President Xi in his tweet ahead of the meeting.

https://twitter.com/realDonaldTrump/status/991886413686861824?ref_src=twsrc%5Egoogle%7Ctwcamp%5Eserp%7Ctwgr%5Etweet

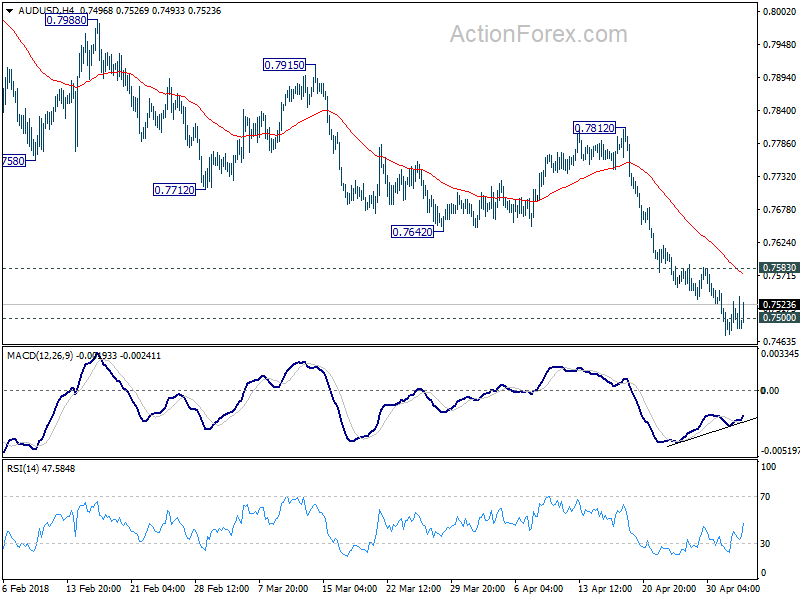

Australian Dollar lifted by large trade surplus and surge in building approvals

AUD trades broadly higher today and it's still extending the rally at the time of writing. Solid economic data provide some support. Technically, though, AUD remains in down trend against USD and CAD despite the rebound.

Australia trade surplus came in at AUD 1.53B in March, widened from AUD 1.35B in February. That's also much larger than expectation of AUD 0.68B. Exports jumped 1% to AUD 34.84B, with strong 8% growth in n non-monetary gold to AUD 131m. Imports rose 1% to AUD 33.31B,. Non-monetary gold imports jumped 28% to AUD 232m.

Building approvals rose 2.6% mom in Mach, much higher than expectation of 1.0% mom. Justin Lokhorst, Director of Construction Statistics at the ABS noted that "the strength in the total dwellings series is being driven by approvals for private sector houses, which have now risen for 13 consecutive months." And, "private sector house approvals are now at their highest level since 2003, in trend terms."

AUD/USD is trying to draw support from 0.7500 key level for the moment. While it's firm elsewhere, AUD/USD needs to break through 0.7583 minor resistance to confirm short term bottoming. Otherwise, near term outlook will remain bearish.

DOW and 10 year yield still heading down after FOMC

Major US equity indices closed lower overnight. DOW lose -174.07 pts or -0.72% to 23924.98. S&P 500 dropped -19.13 pts or -0.72% to 2635.67. NASDAQ closed down -29.8 pts or -0.42% at 7100.90. Long term treasury yields also closed lower, with 30-year yield down -0.002 at 3.135. 10-year yield lost -0.012 to 2.964.

The reactions, falling stocks and falling yield, argue that markets didn't bother much with the FOMC announcement.

Overall development in DOW is still in-line with our bearish view. The rebound since late last week we limited by 55 day EMA, the triangle pattern from 23360.29 still holds. Price actions from 2330.29 is seen as the second leg of the corrective pattern from 26617.71. It could extend for a while. But eventual downside breakout is expected. The correction from 26617.71 would extend to 38.2% retracement of 15450.56 to 26616.71 at 23351.24 before completion.

Outlook in 10 year yield is also unchanged. The correction from 3.035 short term top should extend lower to 55 day EMA (now at 2.837), which is also close to channel support. If it's corrective whole five wave rally from 2.033, there is prospect of touching 2.717 support or 38.2% retracement of 2.033 to 3.035 at 2.652 before completion. That is, It will take a while before TNX would have another take of 3.036 key resistance (2013 high).

Market Morning Briefing: Euro Saw A Low Of 1.1938

STOCKS

As the FED kept rates unchanged not much of movement was expected but it seems the stock markets are reacting rather negatively. News states that the introduction of the word “symmetric” in the statement to define the inflation goals could be taken in a way to understand that the FED would let inflation overshoot its target. Surprisingly the Dow (23924.98, -0.72%) is down about 174 points, but closed above 23750. While that holds, the index is likely to remain ranged. The falling momentum if continues could take it lower towards 23500-23250 in the near term.

Dax (12802.25, +1.51%) broke out sharply above 12600-12700 region while the Euro (1.1978) declined from levels above 1.21. The Euro looks weak for the coming sessions and while the Euro weakens, Dax could continue to hit fresh highs in the current rally targeting 13000-13200 on the upside.

Nikkei (22472.78, -0.16%) is down slightly. Note immediate resistance near 22600 and while that holds, a short dip towards 22200 or lower is possible in the near term. Outlook is bearish for the coming sessions.

Shanghai (3064.44, -0.54%) is stuck in the 3150-3050 region and may remain so this week. A break on either side is necessary to see any major movement in the coming sessions.

Nifty (10718.05, -0.20%) is likely to remain stable for the coming sessions with the upside capped at 10800. Trade within 10600-10800 region is likely to be seen in the coming sessions.

Sensex (35176.42, +0.046%) has some scope of rising towards 36000.

COMMODITIES

Some stability could be expected in the crude prices for some sessions. Brent (73.18) and Nymex WTI (67.81) are almost stable for now. Brent could be trading in the broad 76-72 region for sometime while WTI tests resistance near 70 and could come off towards 66-65 levels in the near term.

Gold (1309.40, +0.29%) almost tested 1300 on the downside and may now start to move up in the coming sessions towards 1320 again. Near term likely to be bullish while above 1300.

Copper (3.0615) is held by the support on the 3-day candle chart and while that holds, copper could move up to test 3.15 again in the coming sessions.

FOREX

Dollar index (92.58) saw a high near 92.8 yesterday as the US Fed predictably maintained status quo, while at the same time acknowledging that inflation is moving higher. This hawkish component of the Fed’s stance might have pushed Dollar Index towards 92.8 but it is again trading near 92.5-92.6 currently. In the near term, there could be a dip back towards 92.0-91.5 after which it should again resume its uptrend. The next target on the upside in the medium term could be 94-95 (which corresponds to the 5th wave starting point of the downmove since Dec ’16). It is also seen on daily line chart as resistance on trendline coming down from Jan ’17 and could be tested in the next 2-3 weeks.

Euro (1.1973) saw a low of 1.1938 yesterday as the Dollar Index simultaneously strengthened, possibly due to the Fed’s positivity about future inflation. It could move up towards 1.20 in the coming 1-2 sessions. If it moves further up above 1.20, then levels near 1.21 could again be tested in the near term. However, after that, it is likely to again start moving down towards its medium term target, which would be levels near 1.16-1.17 (which is the 5th wave starting point of the Euro’s upmove since Dec ’16). This downside target is also seen as support on trendline in the daily line chart.

Dollar Yen (109.68) : Dollar Yen continued moving up further in the upward channel on 3 day candles and saw a high near 110. Our predicted dip towards 109 hasn’t taken place yet, but it could well happen in the coming sessions. The current uptrend looks capped till 110.0-110.5 in the medium term, after which Dollar Yen could dip.

Euro Yen (131.35) : As mentioned yesterday, support near 131 on weekly candles for Euro Yen might well give it support in this week. Lower support is present near 130 which would be tested when Dollar Yen moves down towards 109 and Euro simultaneously moves below 1.195. For this week, our targets of 1.200-1.205 on Euro and 109.5-109.0 on the Dollar Yen give a range of 131.95-130.80 for the Euro Yen.

Pound (1.359), after having broken below crucial long term support level near 1.385 on weekly line chart, is slated to turn very bearish in the medium term. As mentioned yesterday, it is moving down towards its next downside target of 1.35 (seen on daily candles), which could possibly be tested by early next week.

Dollar Rupee (66.66): Dollar Rupee to trade sideways in the 66.60-66.80 region today. A break above 66.80 could take it higher towards 67.00-67.20.

INTEREST RATES

The Fed maintained status quo yesterday but expressed positivity regarding rising inflation. This hawkish component did take the US 10 year yield towards 2.99% but the yield has again dipped a bit. Medium term targets in our Apr ’18 US Treasury report (available on demand) are as follows:

3.2%-3.3% (10 Year), 3.4%-3.5% (30 Year), 3.15% (5 Year) and 2.75% (2 Year). A breach of the 3% level by the 10 year yield would be vital for these targets to be achieved by June. A rate hike is expected in the June Fed meeting, which might start getting factored later this month and could henceforth lead to a rally in yields towards these medium term targets. We also expect some more yield curve flattening in the next month followed by steepening after that, as yields bounce from long term supports.

US 10 Yr Yield (2.97%), 30 Yr (3.15%), 5 Yr (2.80%), 2 Yr (2.49%):

Repeating yesterday’s comment:The US 2 year yield (2.5) has tested the psychologically important 2.5% level and could now see a short term correction towards 2.45%.

The 10 Year yield (2.97%) couldn’t rise above 3% inspite of the FOMC’s hawkish stance. A rise back above 3% could happen later this month as the June Fed rate hike starts getting factored by traders.

US Crude Oil Inventory Increased Much More Than Expected

The report from the US Energy Information Administration (EIA) shows that total crude oil and petroleum products stocks jumped +5.36 mmb (consensus: +0.74 mmb) to 1187.73 mmb in the week ended April 27. Crude oil inventory soared +6.22 mmb to 435.96 mmb, amidst increases in 3 out of 5 PADDs. PADD 5 (a region that includes the western states of California, Arizona, Nevada, Oregon, Washington, Alaska, and Hawaii) alone saw inventory gain of +4.88 mmb. Cushing stock gained +0.42 mmb to 35.78 mmb. Utilization rate increased +0.3% to 91.1%. Meanwhile, crude production increased +0.03M bpd to 10.62M bpd for the week.

For refined oil products, gasoline inventory increased +1.17 mmb to 237.98 mmb although demand added +0.08% to 9.09M bpd. This was compared with consensus of a -0.59 mmb drop. Production rose +1.61% to 10.05M bpd while imports gained +3.01% to 0.92M bpd during the week. Distillate inventory fell -3.18 mmb to 118.83 mmb although demand jumped +19.63% to 4.49M bpd. The market had anticipated a -0.59 mmb draw. Production added +0.36% to 5M bpd while imports plunged -38.21% to 0.08M bpd during the week.

Released after market close on Tuesday, the industry- sponsored API estimated that crude oil inventory gained +3.43 mmb during the week. For refined oil products, gasoline distillate added +1.6 mmb while distillate fell -4.08 mmb.