Sample Category Title

(FED) FOMC Statement May 2, 2018

Information received since the Federal Open Market Committee met in March indicates that the labor market has continued to strengthen and that economic activity has been rising at a moderate rate. Job gains have been strong, on average, in recent months, and the unemployment rate has stayed low. Recent data suggest that growth of household spending moderated from its strong fourth-quarter pace, while business fixed investment continued to grow strongly. On a 12-month basis, both overall inflation and inflation for items other than food and energy have moved close to 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with further gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace in the medium term and labor market conditions will remain strong. Inflation on a 12-month basis is expected to run near the Committee's symmetric 2 percent objective over the medium term. Risks to the economic outlook appear roughly balanced.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 1-1/2 to 1-3/4 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant further gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

Voting for the FOMC monetary policy action were Jerome H. Powell, Chairman; William C. Dudley, Vice Chairman; Thomas I. Barkin; Raphael W. Bostic; Lael Brainard; Loretta J. Mester; Randal K. Quarles; and John C. Williams.

Gold Edges Higher, Investors Looking For Rate Hints From Fed

Gold prices have steadied on Wednesday, following two straight losing sessions. In North American trade, the spot price for an ounce of gold is $1305.56, up 0.12% on the day. On the release front, ADP Nonfarm Payrolls dropped to 204 thousand, compared to 241 thousand a month earlier. Still, this beat the estimate of 200 thousand. Later in the day, the Federal Reserve will set the benchmark interest rate and issue a rate statement. On Thursday, the US will release two key indicators – unemployment claims and ISM Non-Manufacturing PMI.

All eyes are on the Federal Reserve, which will release a rate statement on Wednesday. Policymakers are expected to maintain the benchmark rate at a range between 1.50% and 1.75%, and analysts will be keeping a close eye on the rate statement for clues about future rate hikes. Although the Fed is currently projecting three rate hikes in 2018, there is growing sentiment that the Fed will bump this up to four increases. The Fed last raised rates in March, and some analysts see the Fed raising rates once each quarter – in June, September and December. Higher inflation has raised speculation that the Fed will consider raising its rate hike forecast. The Fed’s preferred inflation gauge, the Personal Consumption Expenditures price index, hit the Fed’s target of 2% inflation for the first time in a

The US dollar continues to gain ground, and that has been bad news for gold prices. Gold has plunged 3.4% since April 16 and is likely to fall below the symbolic $1300 level, for the first time since late December. There are a number of factors weighing on gold prices. Investor risk appetite remains strong, as tensions in the Korean peninsula have dropped rapidly. The leaders of North and South Korea met last week for a historic meeting, and US President Trump is scheduled to meet with North Korean leader Kim in the near future. On the domestic front, the US economy continues to perform well and inflation is moving higher. This has raised expectations that the Federal Reserve will raise rates four times in 2018, which is bullish for the US dollar.

Bundesbank Weidmann: Worries of slowdown are exaggerated

Bundesbank head Jens Weidmann tried to talk down worries over Eurozone growth slow down. He said "some observers already see evidence of an approaching end to the upswing in the recent economic slowdown:". He added "however, I think such worries are exaggerated."

He also said expectations of an ECB hike towards mid-2019 remain realistic.

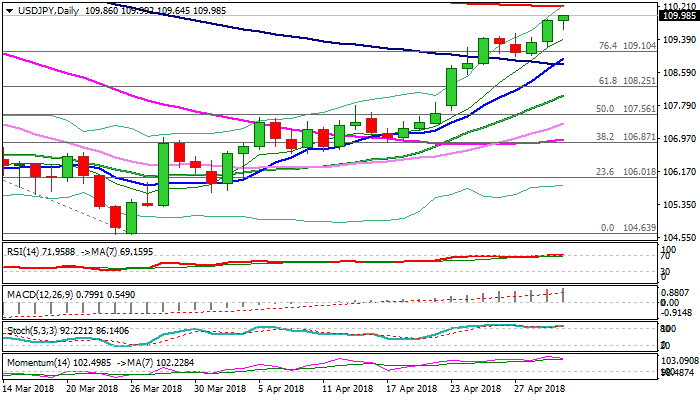

USDJPY Pressure 110 Barrier Again; Fed Policy Decision in Focus

The USDJPY pair is pressuring again 110.00 barrier after greenback accelerated higher in the US session, driven by better than expected US private sector employment data.

Bulls are on track to resume rally, after today’s shallow dip to 109.65 was contained by previous barrier (Fibo 50% of 114.73/104.62 fall).

Break through pivots at 110.00 (psychological) and 110.22 (200SMA) is needed to generate fresh bullish signal for test of next strong barrier at 110.48 (02 Feb high) and open way for possible extension towards 110.87 Fibo 61.8% of 114.73/104.62).

Fed’s policy decision, due later today, is expected to provide fresh signals, as hawkish tone would boost the greenback for eventual break through 110.00/22.

Softer tone from the US central bank may slow bulls and signal extended consolidation before bulls continue.

Dips would face strong supports at 108.90 zone (rising 10SMA / top of 4-hr cloud).

Res: 110.00; 110.22; 110.48; 110.87

Sup: 109.65; 109.23; 108.90; 108.65

Pound Stems Slide as Construction PMI Beats Estimate

The pound has steadied in the Wednesday session, after recording sharp losses in the Wednesday session. In North American trade, GBP/USD is trading at 1.3603, down 0.07% on the day. On the release front, British Construction PMI improved to 52.5, above the estimate of 50.5 points. Over in the US, ADP Nonfarm Payrolls dropped to 204 thousand, compared to 241 thousand a month earlier. Still, this beat the estimate of 200 thousand. Later in the day, the Federal Reserve will set the benchmark interest rate and issue a rate statement. On Thursday, Britain releases Services PMI, and the US will publish two key indicators – unemployment claims and ISM Non-Manufacturing PMI.

The pound’s woes continue, as the US dollar flexes its muscles against its major rivals. The pound dropped below the 1.36 line on Tuesday, the first time that has happened since early January. Investors have not taken kindly to soft British numbers. GBP/USD dropped sharply on Friday after GDP posted a negligible gain of 0.1%, and there was a repeat performance on Tuesday, as Manufacturing PMI missed the estimate and dropped for a fifth straight month. The poor performance of the economy in the first quarter has dampened expectations that the BoE will raise rates at next week’s rate meeting, with the odds of a hike plunging to 20%, compared to 90% at the beginning of April. Most analysts expect the BoE to delay a rate hike until the second half of the year, with August or November being the most likely months for a rate hike.

What can we expect from the Federal Reserve? At the March policy meeting, policymakers raised rates for the first time in 2018, and are expected to remain on the sidelines at today’s meeting. Analysts will be keeping a close eye on the rate statement for clues about future rate hikes. Although the Fed is currently projecting three rate hikes in 2018, there is growing sentiment that the Fed will bump this up to four increases. The CME Group has priced in a quarter-point hike in June at 93% and one scenario is that the Fed will keep raising rates once each quarter – in June, September and December. Higher inflation has raised speculation that the Fed will consider raising its rate hike forecast. The Fed’s preferred inflation gauge, the Personal Consumption Expenditures price index, hit the Fed’s target of 2% inflation for the first time in a year in March.

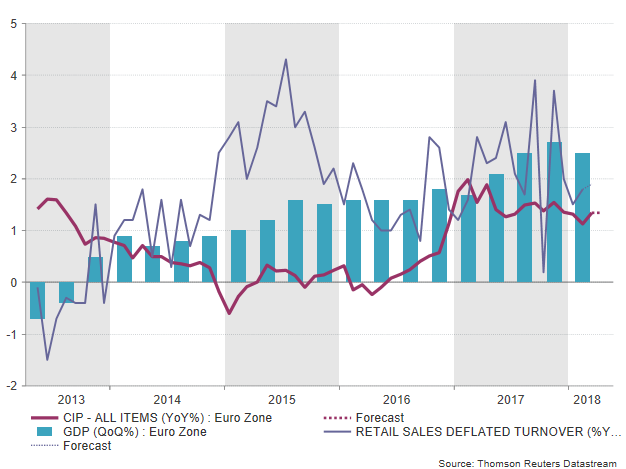

Eurozone Flash CPI to Lack Momentum in April

Eurozone flash inflation readings will be available for review on Thursday at 0900 GMT and forecasts suggest that price growth in the monetary union will continue to lack momentum needed to reach the European Central Bank’s (ECB) inflation target, justifying the central bank’s patience in removing stimulus.

On an annual basis, the headline Harmonized Consumer Price Index (HICP) is said to have increased by 1.3% as in March, while the core equivalent which trims volatility, is seen marginally lower at 1.2% y/y compared to 1.3% in the previous month. This would not be a surprise as preliminary HCPI figures published separately in Germany, France, and Italy a couple of days ago, – the three largest EU economies – failed to pick up speed in April, remaining around March levels. Therefore, with the bloc’s inflation gauges showing no signs of an upward trend towards the ECB’s ideal price growth of 2.0%, policymakers are unlikely to make any changes to their accommodative monetary strategy. Instead, they will probably hold asset purchases to run until their expiration date in September or even beyond if key indicators appear softer in the coming months, with the announcement probably coming in June. The hint could also come in July if the data miss is significant. A rate hike is also expected to come well after the quantitative easing program matures, making markets wondering whether the central bank will be able to catch up with its counterparts before the next recession hits. It is also worth noting that the ECB’s survey of 58 professional forecasters conducted in early April showed that inflation could reach 1.6% in 2017 and 1.7% in 2020; 0.1 percentage points lower than estimates three months ago.

The start of 2018 was a gloomy one for the bloc as business surveys surprisingly moderated and preliminary GDP growth figures for the first quarter of the year slowed down as expected. In the coming months, trade risks could translate into even weaker business confidence if the EU and the US fail to reach an agreement on steel and aluminum import tariffs. This in return could boost prices of imported goods and under softer competition domestic producers could find the opportunity to raise their own prices as well, leading inflation higher as policymakers wish for. However, the ECB will likely refrain from winding down stimulus under this scenario in which economic growth is narrowing on the back of trade inefficiency. Still, this seems not to be the case for now as Trump’s decision to extend temporary tariff exceptions for the EU, Canada, and Mexico showed that the US President is not in the mood to start a global trade war.

The start of 2018 was a gloomy one for the bloc as business surveys surprisingly moderated and preliminary GDP growth figures for the first quarter of the year slowed down as expected. In the coming months, trade risks could translate into even weaker business confidence if the EU and the US fail to reach an agreement on steel and aluminum import tariffs. This in return could boost prices of imported goods and under softer competition domestic producers could find the opportunity to raise their own prices as well, leading inflation higher as policymakers wish for. However, the ECB will likely refrain from winding down stimulus under this scenario in which economic growth is narrowing on the back of trade inefficiency. Still, this seems not to be the case for now as Trump’s decision to extend temporary tariff exceptions for the EU, Canada, and Mexico showed that the US President is not in the mood to start a global trade war.

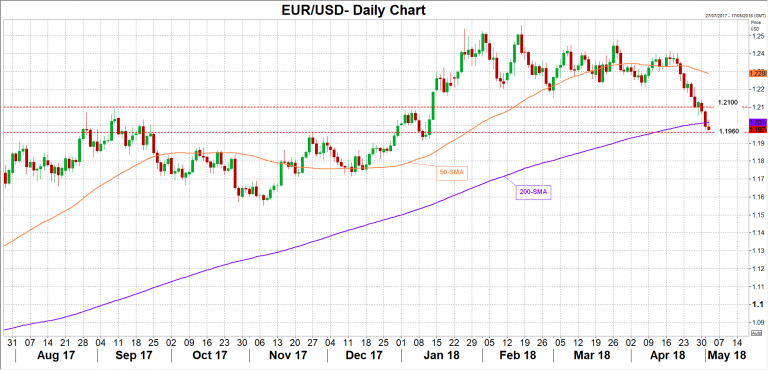

Turning to forex markets, euro/dollar could experience further pressure if Thursday’s CPI readings disappoint, meeting immediate support at the November’s low of 1.1960 before the focus shifts down to the 1.1900 psychological level. On the other hand, if CPI beats expectations, the price could break above the 200-day simple moving average which currently stands 1.2014 to find resistance at the 1.2100 handle.

On Friday, Eurozone retail sales for the month of March could add volatility to euro/dollar as well. Unlike CPI forecasts, projections for retail sales are optimistic, with analysts predicting an expansion of 0.5% m/m compared to 0.1% seen in February, the highest since January. On a yearly basis, the measure is said to rise by 0.1 percentage points to 1.9%.

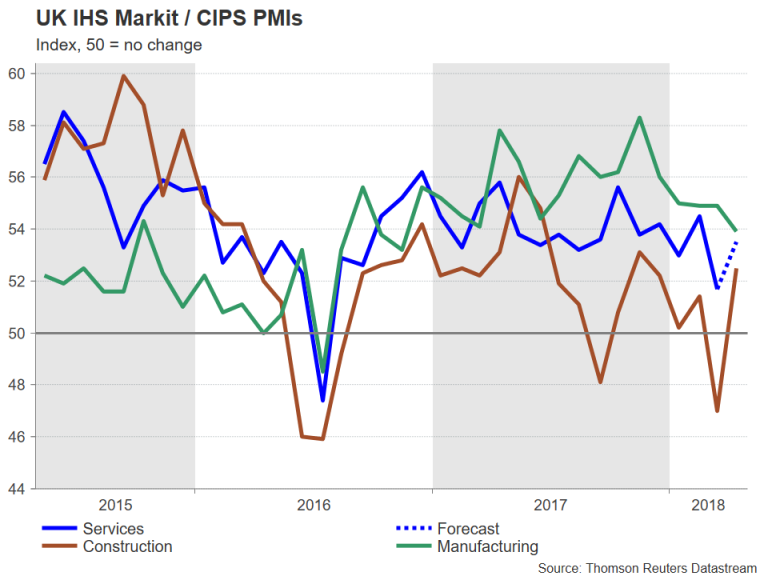

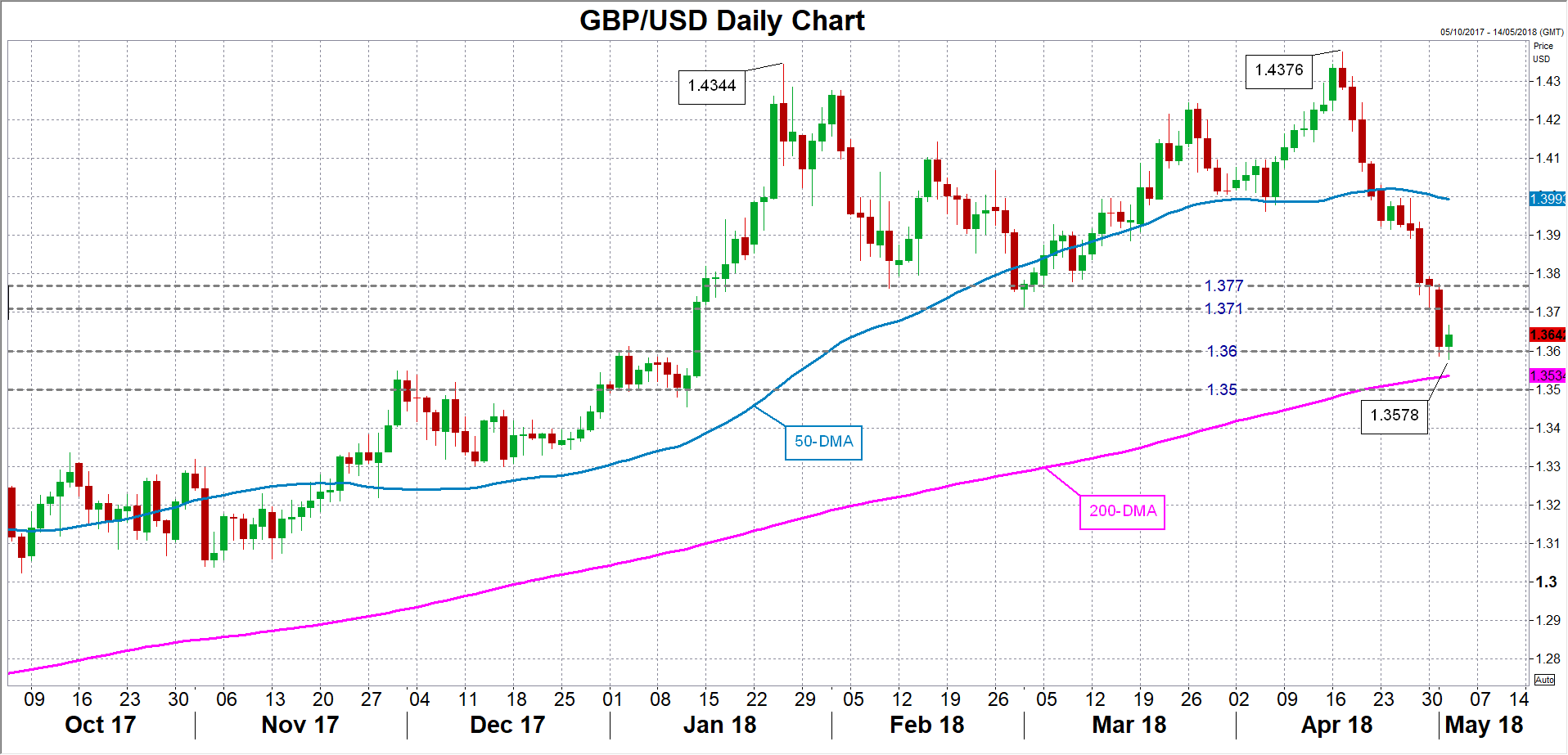

Could UK Services PMI Resurrect Hopes for May Rate Hike?

Market odds of an interest rate rise by the Bank of England in May have fallen dramatically over the past month from over 90% to less than 20% after a run of weak UK data. BoE chief, Mark Carney, also cast doubt about the prospect of a May move in recent remarks. However, after strongly signalling a rate increase earlier in the year, the Bank may have cornered itself into raising rates as it risks losing credibility if it doesn’t hike at its next meeting on May 10. The April services PMI on Thursday could provide the BoE’s hawks with enough reason to push for a rate hike.

The British economy grew by just 0.1% quarter-on-quarter in the three months to March, slower than the consensus forecasts of 0.3%. In addition, the inflation overshoot caused by the pound’s depreciation after the Brexit referendum is subsiding much more quickly than anticipated, with headline CPI falling to 2.5% in March. The labour market remains a bright spot but it’s too early to bet on wage growth being on a sustained path upwards.

While the Bank of England expected some softness in the economy at the start of the year, policymakers may now be worried that growth is too weak to withstand a tightening in monetary policy so soon after the November hike. The slowdown is not limited to the UK, however, as across the continent, the Eurozone economy also lost some steam in the first quarter. Faltering demand in Europe does not bode well for UK manufacturers, which export almost half of their goods to the European Union.

Manufacturing activity declined to a 17-month low in April according to the Purchasing Managers’ Index by IHS Markit/CIPS. In contrast, construction output picked up more than expected in April, but the more important services PMI, due on Thursday, could be the determining factor for the BoE.

The services PMI deteriorated sharply in March, falling to its lowest since July 2016 in the immediate aftermath of the Brexit referendum. During the first quarter, bad weather, as well as the squeeze on households’ incomes from falling real wages weighed on consumer spending, which is a key driver of the services sector as well as the wider economy. But with the income squeeze now starting to ease as inflation moves lower, and as the effects of the cold weather recede, consumer confidence could rebound strongly in April.

The PMI gauge for services is forecast to increase to 53.5 in April from 51.7 in March. A bigger-than-expected increase could propel the pound higher, which is rebounding from a near 4-month low of $1.3578 ploughed earlier today. An upside surprise in the data could bring the $1.37 handle back into view, with the March low of $1.3710 potentially acting as resistance. A stronger rally could meet resistance around the recently congested area of $1.3770.

Another negative reading though on Thursday could cut today’s recovery short, driving sterling back below the $1.36 level. This week’s low of $1.3578 would likely act as immediate support in such a scenario, while deeper losses would raise the prospect of the pound losing its grip on the $1.35 level for the first time since January.

Sunset Market Commentary

Markets:

The German Bund opened lower in a catch-up move following yesterday’s German Labour Day Holiday. Lackluster trading characterized the European session with markets mainly counting down to tonight’s FOMC verdict and ignoring Q1 EMU GDP data (in line with forecasts). The US Note future started outperforming despite a strong ADP labour market report and despite the US Treasury’s quarterly refinancing announcement. The latter, as expected, showed another increase in debt sales stemming from the giant fiscal stimulus package. The argument favours higher long term US yield in the longer run though, especially since it is accompanied by the Fed’s balance sheet reduction. Today’s intraday move suggests some final, technically insignificant, positioning into the Fed. The US central bank will probably label soft Q1 GDP as transitory while sharpening its inflation rhetoric and preparing a June rate hike. The short term market reaction might be muted, but this scenario suggests higher US rates in the medium term through an increased probability of 2 (FOMC median) instead of 3 additional rate hikes this year. The German yield curve bear steepens at the time of writing with yields 1 bp (2-yr) to 2 bps (30-yr) higher. Changes on the US yield curve are limited to 1 bp. 10-yr yield spread changes vs Germany are close to unchanged with Italy outperforming (-4 bps) after Italian president Mattarella ruled out rumours of a snap election in June.

There were several interesting data in the EMU and in the US today. However, this time, they weren’t able to kick-start a new intraday trading dynamics in the major USD cross rates. EMU Q1 GDP was reported exactly in line with expectations. The US private sector added 204k jobs according to the ADP labour report. This report was also close to forecasts. Investors have shifted into wait-and-see modus ahead of this evening’s Fed policy statement. EUR/USD hovers near the 1.20 big figure. USD/JPY is holding in the 109.75 area. The Fed is largely expected to keep its policy unchanged. However, if the Fed upgrades its assessment on inflation and the market would gradually tilt further to three additional Fed rate hikes rather than two, the dollar might remain well supported.

The most recent sterling correction slowed today. EUR/GBP struggled to extend its rebound north of 0.88 this morning. Cable also showed some tentative signs of bottoming out. Mid-morning, the UK April construction PMI rebounded from 47.0 to 52.5 (only 50.5 was expected). In the global picture of the UK economy, the construction PMI isn’t the most important pointer to assess the cyclical momentum in the UK economy. However, after last week’s sterling sell-off, it was enough for some sterling shorts to reduce exposure. EUR/GBP trades currently just below the 0.88 big figure. Cable hovers in the mid 1.36 area. For now we don’t anticipate a sustained comeback of sterling yet. The internal debate with PM May’s conservative party on what kind of Brexit the UK should aim for, is again heating op. At the same time, the market has now largely rejected the idea of a May BoE rate hike.

News Headlines:

Eurozone unemployment stabilized at 8.5% while growth in 1Q 2018 slowed down to 0.4% MoM (2.5% YoY). Both figures came in as expected, suggesting some natural rolling over from an extraordinary 2017.

The US labour market remains robust. The ADP report showed that private employers added 204 000 jobs in April, beating 198 000 consensus and recording a >200 000 increase for a sixth month running.

The US Treasury Department will boost the amount of long-term debt it sells to $73 bn this quarter as President Trump’s administration seeks to finance budget deficits set to widen further because of tax cuts and higher spending.

Germany’s debt to GDP ratio will likely drop below 60% in 2019, FM Scholz said at a news conference in Berlin presenting government’s budget plans. The plan foresees no net supply through 2022.

EURUSD Returns Below 200SMA on Solid US Jobs Data; FOMC Verdict Eyed for Fresh Signals

The Euro eased in early US trading on Wednesday and returned below 200SMA and 1.20 handle after better than expected US ADP private jobs data (204K in Apr vs 200K f/c) offered fresh support to the greenback, deflating Euro's recovery attempts. Fed is due to release its policy decision later today and focus turns towards the announcement, which is expected to provide fresh signal. The central bank is widely expected to keep interest rates unchanged today, but traders will be looking for signals of the future Fed's action. Hawkish tone, which would signal more aggressive approach and three hikes this year, would offer fresh boost to already bullish dollar, while softer tone would provide Euro bears further breather and signal stronger correction of 1.2413/1.1981 fall. Bearish scenario is expected to confirm break through 200SMA and 1.20 support and open way for extension towards 1.1936 (Fibo 61.8% of 1.1553/1.22555) and 1.1900 (round-figure) in extension. Dovish tone from Fed would allow for stronger recovery and expose initial barriers at 1.2083 (Tuesday's high) and 1.2100 (round-figure).

Res: 1.2012; 1.2031; 1.2055; 1.2083

Sup: 1.1981; 1.1936; 1.1915; 1.1900

Japanese Yen Subdued in Thin Holiday Trade

With Japanese markets closed for Constitution Day, the yen is having a quiet day. In the North American session, USD/JPY is trading at 109.91, up 0.05% on the day. On the release front, Japanese Consumer Confidence fell to 43.6 points, missing the estimate of 44.6 points. In the US, ADP Nonfarm Payrolls dropped to 204 thousand, compared to 241 thousand a month earlier. Still, this beat the estimate of 200 thousand. Later in the day, the Federal Reserve will set the benchmark interest rate and issue a rate statement. On Thursday, the US releases two key indicators – unemployment claims and ISM Non-Manufacturing PMI.

What can we expect from the Federal Reserve? At the March policy meeting, policymakers raised rates for the first time in 2018, and are expected to remain on the sidelines at today’s meeting. Analysts will be keeping a close eye on the rate statement for clues about future rate hikes. Although the Fed is currently projecting three rate hikes in 2018, there is growing sentiment that the Fed will bump this up to four increases. The CME Group has priced in a quarter-point hike in June at 93% and one scenario is that the Fed will keep raising rates once each quarter – in June, September and December. Higher inflation has raised speculation that the Fed will consider raising its rate hike forecast. The Fed’s preferred inflation gauge, the Personal Consumption Expenditures price index, hit the Fed’s target of 2% inflation for the first time in a year in March.

Like many other industrialized countries, Japan’s economy experienced a slowdown in the first quarter of 2018. Annualized growth in Q4 stood at 1.6% but stands to drop sharply in Q1, with an estimate of just 0.5%. One factor in the slowdown is a significant drop in exports, due to the stronger Japanese currency. The yen has gained about 3% against the dollar in 2018, hurting the competitiveness of Japanese exports. Still, the economic recovery has been impressive, as the economy has expanded for eight consecutive quarters, its longest streak since the 1980s. The Japanese consumer, however, remains pessimistic, and the April reading of 43.6 marked an 8-month low.