Sample Category Title

Canadian Dollar Trading Sideways, Fed Announcement Next

The Canadian dollar continues to trade quietly this week. In the Wednesday session, USD/CAD is trading at 1.2837, down 0.10% on the day. On the release front, there are no Canadian events on the schedule. In the US, ADP Nonfarm Payrolls are expected to slide to 200 thousand. As well, the Federal Reserve will set the benchmark interest rate and issue a rate statement. On Thursday, the US releases unemployment claims and ISM Non-Manufacturing PMI, and Canada will release Trade Balance.

Canada’s economy grew by 0.4% in February, above the estimate of 0.3%. This was a welcome rebound from January, when GDP contracted 0.1%. The economy has endured a sluggish first quarter, and unless March GDP is outstanding, growth in the first quarter will fall under 2%.

All eyes are on the Federal Reserve, which will release a rate statement on Wednesday. Policymakers are expected to maintain the benchmark rate at a range between 1.50% and 1.75%, and analysts will be keeping a close eye on the rate statement for clues about future rate hikes. Although the Fed is currently projecting three rate hikes in 2018, there is growing sentiment that the Fed will bump this up to four increases. The Fed last raised rates in March, and some analysts see the Fed raising rates once each quarter – in June, September and December. Higher inflation has raised speculation that the Fed will consider raising its rate hike forecast. The Fed’s preferred inflation gauge, the Personal Consumption Expenditures price index, hit the Fed’s target of 2% inflation for the first time in a year in March.

US President Trump made waves when he imposed tariffs on steel and aluminum imports earlier in the year. However, Trump announced this week that he had extended exemptions on the tariffs for Canada and Mexico for another 30 days. The exemptions come at a sensitive time, with the US, Canada and Mexico neck deep in negotiations over a new NAFTA trade agreement. The talks have made significant progress, but the critical auto pact remains a stumbling block. It is likely that a tentative agreement will be hammered out, perhaps later this month. The Bank of Canada has dropped strong hints that it plans to raise interest rates later this year, but policymakers would like the NAFTA issue to be resolved before the next rate hike.

Dollar Steady ahead of FOMC while Gold Inches Up

The mighty Dollar was the main talking point across financial markets this week, after rallying to a four-month high above 92.50 against a basket of major currencies.

Today’s main event risk for the Dollar, and potential market shaker, will be the outcome of the Federal Reserve’s meeting, which is widely expected to conclude with monetary policy left unchanged. Although May’s FOMC meeting will not include a press conference or fresh economic projections, investors should not be quick to expect the meeting to be a “non-event”. Much of the attention will be directed towards the policy statement, which could offer fresh insight into the central bank’s views on inflation and the US economy. With robust US data boosting sentiment towards the economy, and rising inflation expectations supporting the prospect of higher interest rates, the Dollar remains heavily supported. A hawkish Fed statement is likely to inject Dollar bulls with enough inspiration to elevate the Dollar Index to fresh yearly highs.

Prior to the FOMC’s decision, the ADP private jobs data report will be in the spotlight, with economists forecasting a 200k rise in the month of April. A figure that meets or exceeds this forecast could boost buying sentiment towards the Greenback.

Speaking of the Dollar, the currency held steady against its major counterparts on Wednesday. The Dollar Index has broken above the 200 Daily Simple Moving Average while the MACD has crossed to the upside. A breakout and daily close above 92.50 could encourage an incline higher towards 93.00 and 93.30, respectively. A failure for bulls to secure a close above 92.50 could encourage a decline back towards 92.00.

Sterling higher after Construction PMI rebounds

Sterling edged slightly higher on Wednesday, following the better-than-expected UK Construction PMI figures.

The UK’s construction industry bounced back to life in April, as the PMI climbed to a score of 52.5, up from March’s score of 47.00 and exceeding the 50.5 market expectation. Regardless of positive construction figures, sentiment towards the British Pound remains bearish. Sterling is likely to find itself depressed and bruised as expectations continue to fade over the Bank of England raising interest rates in May. With the local elections in England on Thursday dishing out some short-term political risk and uncertainty, Sterling remains vulnerable to further losses.

From a technical standpoint, the GBPUSD is bearish on the daily charts, as there have been consistently lower lows and lower highs, while the MACD trades to the downside. The breach below the 1.3640 level could invite a decline towards 1.3580 and 1.3540, respectively.

Commodity spotlight – Gold

Commodity spotlight – Gold

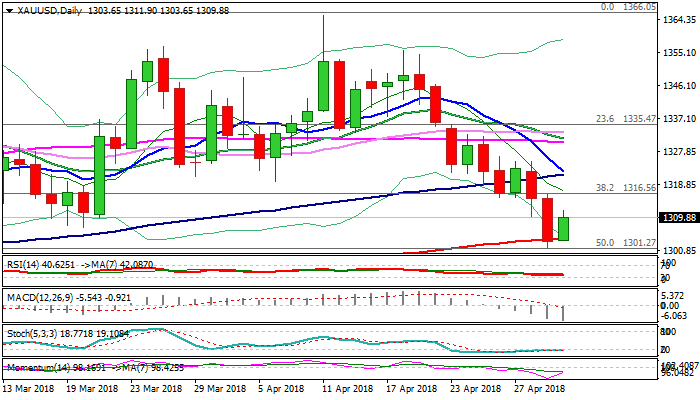

Gold has inched higher today, with prices venturing towards $1309 as of writing. With the fundamental drivers punishing the yellow metal still firmly intact, the current rebound could be nothing more than a technical move. An appreciating Dollar, coupled with expectations of higher US interest rates, is likely to continue pressuring the yellow metal. Bears remain in firm control below $1324 with the next key levels of interest at $1300 and $1260, respectively.

Heading into US session, a look at USD, EUR & GBP

It's a big day for USD and EUR, and slightly less so far GBP today. Let's have a look at how the three are performing after events from Eurozone and UK.

From USD heatmap, it's clear that the main trend is up as seen in the W and M row. Except that, USD cannot overwhelm CAD. D row, all in red, suggests some weakness today. But light red means it's more in consolidation then reversal. This is affirmed by 4H row which shows US up against all but EUR and GBP. Hence, USD is in consolidation as we await ADP employment, FOMC, and ISM services and NFP later in the week.

EUR remains rather weak. Outlook versus Sterling is a bit mixed. 4H row shows EUR is recovering against others, but there is no follow through buying. While in-line with expectation GDP growth figure stabilized the selloff, there is no momentum for a solid rebound yet.

Comparing to EUR, GBP's movement today is much more convincing. It's up against all as seen in the D row. And strengthen at the moment remains strong too with 4H row all in deep blue. It's still in decline for the month. And is in deep red against USD, JPY, CHF and CAD for the week. So, while the rebound is strong, it's much more likely a correction than a reversal. But for counter trend strategies, GBP is a much better choice to bet on than EUR.

SPOT GOLD Bounces As Traders Took Profit Ahead Of Fed

Gold price bounces on Wednesday after hitting four-month low at $1301 on Tuesday's bearish acceleration which also cracked strong support provided by 200SMA at $1303.

The yellow metal recovers on weaker dollar ahead of FOMC, as traders are booked profits on recent strong rally.

Oversold conditions signal corrective action, however, strong bearish sentiment on firm greenback and significantly reduced safe-haven demand, keeps gold price under strong pressure and suggests limited recovery.

Broken Fibo 38.2% support / yesterday's high, mark initial barrier at $1316, while stronger upticks are expected to stall under 100SMA ($1321), as resistance is reinforced by falling 10SMA, which attempts to form bear-cross.

Bearish scenario requires break below psychological $1300 support to open way towards $1285 (Fibo 61.8% of $1236/$1366 rally).

Only break and close above 100/10 SMA's would sideline downside risk and signal stronger correction of $1355/$1301 fall.

Res: 1311, 1316, 1321, 1323

Sup: 1303, 1300, 1289, 1285

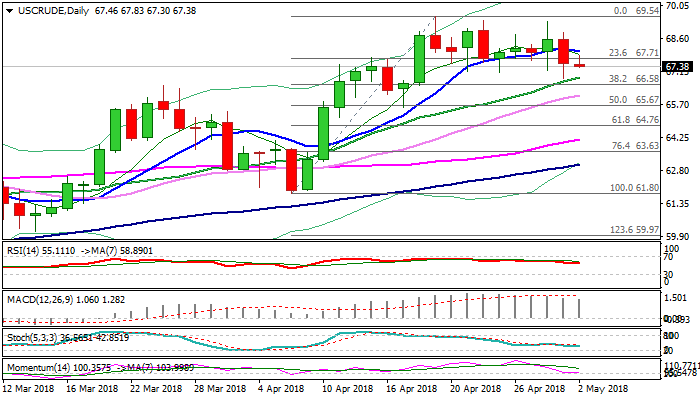

WTI Oil – Limited Recovery Keep Oil Price At The Back Foot, EIA Crude Stocks Report In Focus

WTI oil stand at the back foot in the mid-European session and moved lower after recovery attempts from Tuesday's low at $66.84 were capped by the base of 4-hr cloud (spanned between $67.55 and $68.02).

Fresh attempts to extend Tuesday's strong fall (oil price was around $2 down) and pressures cracked floor of recent $67.10/$69.54 congestion.

Eventual close below 10SMA on Tuesday was negative signal, reinforced by significant loss of momentum, keeping near-term risk at the downside.

Break below $67.10 and next pivots at $66.88 (rising 10SMA) and $66.58 (Fibo 38.2% of $61.80/$69.54) is needed to generate stronger bearish signal and trigger deeper correction of $61.80/$69.54 upleg.

US API crude stocks data, released on Tuesday, showed strong build in crude inventories (3.42 million barrels) while focus turns on today's release of EIA weekly crude stocks data, which are forecasted for 0.73 million barrels build, following last week's unexpected build of 2.17 million barrels.

Another negative figure from crude inventories report could put oil price under fresh pressure which could result in reversal signal and sideline broader bulls for deeper correction.

Bearish scenario on loss of $67.10/$66.58 pivots would open targets at $66.09 (rising 30SMA) and $65.67 (daily Kijun-sen).

Conversely, oil price may remain within extended consolidation range while pivotal supports hold.

Broken 10SMA marks initial resistance at $68.03 and sustained break here would sideline persisting downside risk and shift near-term focus higher.

Res: 67.83, 68.03, 68.87, 69.32

Sup: 67.10, 66.88, 66.58, 66.09

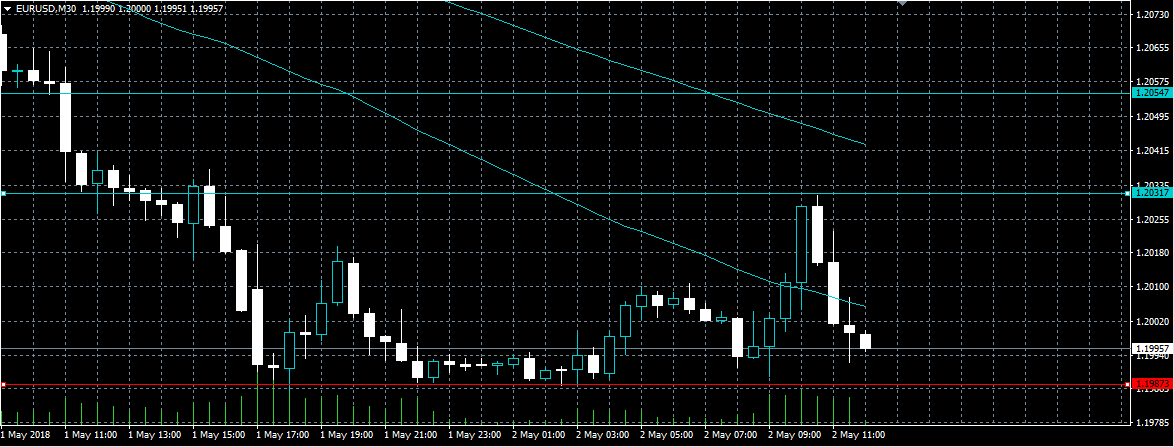

Strong Technical Rejection Weighing On Euro

The euro currency has fallen back below the 1.2000 level against the US dollar after the pair was aggressively sold from the 1.2031 level during today’s European trading session. The EURUSD pair currently trades close to the lows of the day, as sellers looked past better than expected eurozone GDP numbers. Moving into the U.S session, the euro’s 200-day moving average, at 1.2010, and the FOMC Policy Decision later today remain the key focus points for traders.

The EURUSD pair is strongly bearish while trading below the 1.2010 level, key support is found at the 1.1955 and 1.1930 levels.

If the EURUSD pair trades back above the 1.2010 level, key intraday resistance is found at the 1.2031 and 1.2054 levels.

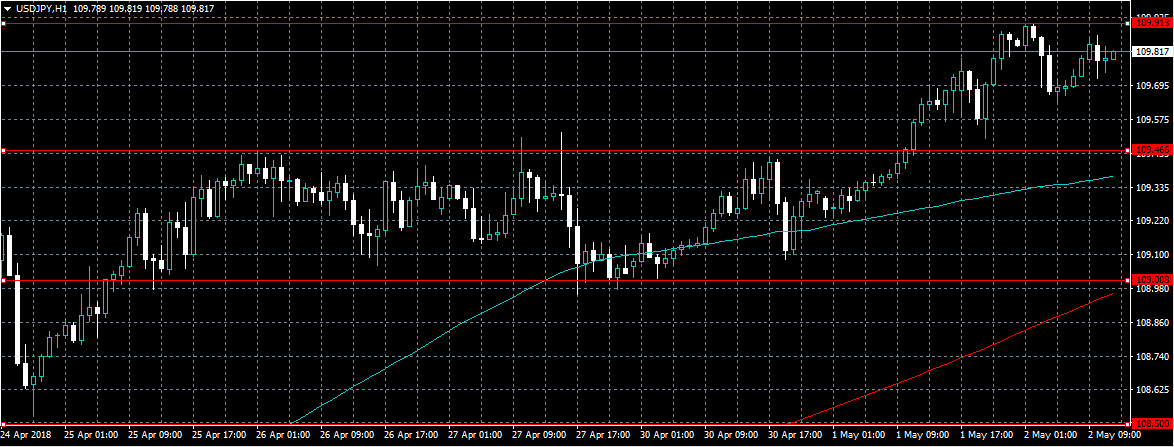

USDJPY Targeting 110 Handle Ahead Of FOMC

The U.S dollar has moved to a fresh eleven-week trading-high against the greenback, hitting 109.91, following another round of strong buying in the U.S dollar index. The USDJPY pair currently trades around the 109.80 level, with buyers looking to build momentum for a push higher towards the psychological 110.00 level. Traders are likely to focus on high-impact data from the United States today, and the key 92.00 handle of the U.S dollar index.

The USDJPY pair remains bullish while trading above the pivotal 109.45 level, upside resistance is now found at the 110.10 and 110.40 levels.

If the USDJPY pair moves below the 109.45 level, the 109.00 and 108.50 levels remain the strongest forms of downside resistance.

Dollar Treads Water Ahead Of FOMC Rate Decision, European Stocks Up

Here are the latest developments in global markets:

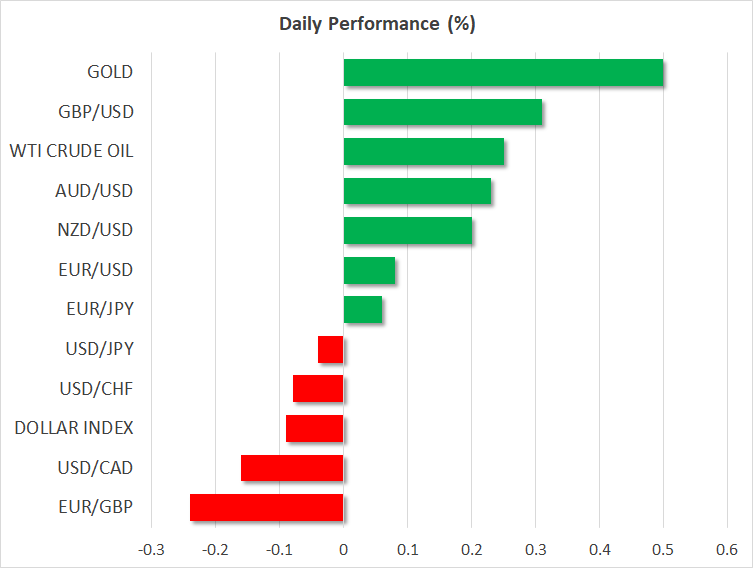

FOREX: The US dollar managed to pare some losses against the Japanese yen made after it touched a 3-month high of 109.91 earlier in the day, rising to 109.83 (-0.02%). The dollar index, which gauges the greenback’s strength versus six major currencies, managed to hit a 4-month high of 92.56 on Tuesday, peaking above the 200-day moving average for the first time in a year but today the index was slightly lower at 92.36 (-0.09%). Pound/dollar rose by 0.28% on Wednesday snapping five straight negative daily sessions, as better-than-expected UK construction PMI data calmed investors concerned about a sharp economic slowdown. Eurozone’s GDP flash reading for the first quarter eased to 2.5% y/y as expected, while the bloc’s final Markit manufacturing PMI was surprisingly revised higher, with euro/dollar moving marginally higher by 0.09% to touch 1.2000. In antipodean currencies, aussie/dollar and kiwi/dollar were in a bullish mode, both rising by 0.29%, recovering some of the extraordinary losses they posted in recent days. Dollar/loonie was down by 0.18% but within the range developed last week.

STOCKS: European stocks gained in Europe as many investors returned from holidays in contrast to their Asian counterparts which were on the back foot. The benchmark European STOXX 600 rose by 0.69% at 0944 GMT led by tech stocks and basic materials, while the blue-chip Euro STOXX 50 was up by 0.53%, being in the green for the fifth day in a row. The German DAX 30 surged by 1.30% hitting a fresh three-month high and the French CAC 40 moved higher by 0.25%. Also, the British FTSE 100 jumped by 0.66%. In the US, even though the S&P, Dow Jones were mixed on Tuesday, futures tracking these indices are currently in the green, pointing to a higher open today.

COMMODITIES: Oil prices were mixed, with WTI crude trading higher by 0.25% at $67.43 per barrel and Brent trading lower by 0.26% at $72.94. Fears on whether the US will reimpose sanctions to Iran continued to support oil prices, while worries over rising US production continued to limit gains. In precious metals, silver surged by 1.51% and gold gained 0.58%.

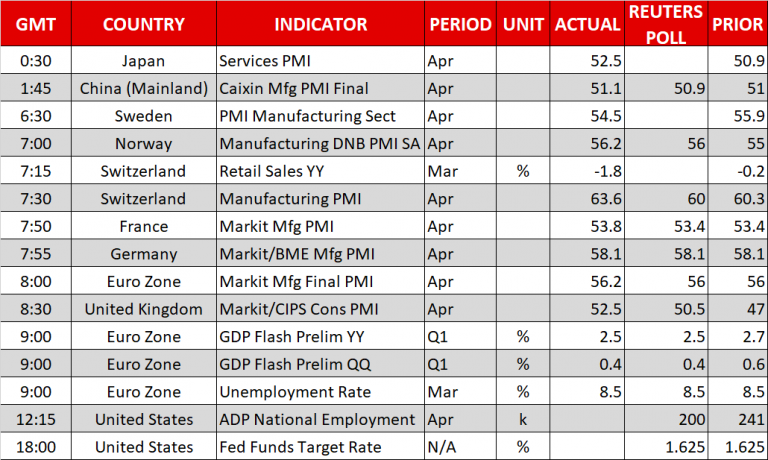

Day ahead: Eyes on FOMC rate decision; ADP employment report in focus

The FOMC rate decision will be the highlight event later in the day. Analysts are currently fully pricing in two more rate hikes this year and have started to bet on a third one, but this time they are widely expecting rates to remain unchanged at 1.75% as no press conference is scheduled to follow the rate announcement. However, analysts will be focused to identify any hawkish tweaks to the language expressed in the FOMC monetary statement as a series of data published recently proved that the US economy is gaining momentum. Should policymakers acknowledge encouraging economic trends, the dollar could stretch higher. Still, comments underlying the uncertainties in the trade front could limit greenback’s gains. Yet, Trump’s decision to extend negotiations on steel and aluminum import tariffs on Tuesday after temporary exceptions expired on May 1 showed that the US President is not currently in the mood to start a global trade war. The rate announcement and the FOMC rate statement are due at 1800 GMT.

Before the FOMC reveals its decision, investors will take a close eye on the ADP nonfarm employment report (1215 GMT) to finalize their projections for the more comprehensive nonfarm payrolls report delivered by the government on Friday. According to forecasts, the ADP numbers which track employment changes in the private sector are anticipated to show that job positions increased by 200,000 in April compared to a rise of 241,000 in the preceding month. An upward surprise in the data could hint that Friday’s NFP job numbers could also beat analyst forecasts.

Meanwhile, in oil markets, investors will be waiting for the EIA weekly update on US crude oil stocks to come into view at 1430 GMT.

In equities, Tesla is among companies releasing quarterly results on Wednesday; the carmaker will be reporting after the US market close.

Any headlines on the Brexit front are likely to attract attention as well, as the Cabinet Brexit sub-committee of senior ministers is gathering today to discuss the UK’s future customs partnership with the EU.

USD Pares Gains Ahead Of Fed Decision

- Traders Look For Fourth Rate Hike Hint From Statement;

- USD Takes a Breather After Strong Rally;

- GBP Pares Considerable Losses After Better PMI.

'With expectations on the rise, there's plenty more room for a fourth hike to be priced in, as well as a faster pace of tightening further down the line'

US futures are treading water ahead of the open on Wednesday, as investors await the monetary policy announcement from the Federal Reserve and earnings from 49 US companies.

The interest rate decision from the Fed is expected later in the session on Wednesday and while no change is expected at this meeting, traders will be paying very close attention to the accompanying statement for clues on the number of rate hikes this year. The chances are, the Fed won't stray too far from previous messaging and, if it decides to warn of the possibility of a fourth hike this year, it will probably do so in the economic projections next month.

Still, with the central bank having previously projected three this year with an additional next, even a slight hawkish shift in the statement could convince traders that a fourth is more likely. As it stands, a fourth rate hike is around 50% priced in, having been around half that only a few weeks ago. With expectations on the rise, there's plenty more room for a fourth hike to be priced in, as well as a faster pace of tightening further down the line.

'the near-term could be favourable for the greenback as it attempts to claw back some of the losses incurred over the last 16 months'

The data is certainly supporting the case for faster tightening with even the Fed's preferred inflation measure – the core personal consumption expenditure price index – almost at target. Tax reforms will likely continue to boost the economy in the near-term also and influence the Fed's view on tightening with it.

The US dollar has seen something of a resurgence in recent weeks as well, with the slight increase in interest rate expectations in the US having coming at the same time as a softening in the tightening case for other central banks as well as some very strong earnings reports from US corporates. With the 2-year yield now at its highest since 2008 and the 10-year above 3%, after seriously struggling to breach this threshold for months, the near-term could be favourable for the greenback as it attempts to claw back some of the losses incurred over the last 16 months.

'At one time, a hike looked an almost certainty due to the language from the central bank in recent months but that has changed recently'

The pound is having a torrid time in comparison to and, particularly, against the greenback having fallen more than 5% over the last couple of weeks. The move has come as rate hike expectations for the Bank of England this month have fallen from around 70% to less than 20% at the time of writing. At one time, a hike looked an almost certainty due to the language from the central bank in recent months but that has changed recently with Governor Mark Carney claiming that there are other meetings this year at which they could raise interest rates.

This comes as the economic data has turned sour with the economy barely growing in the first quarter, inflation falling in recent months closer to target and confidence in the outlook being less positive. While the construction PMI saw a stronger than expected bounce back in April, having suffered as a result of the bad weather in March, the manufacturing PMI was not so good having fallen again while the services PMI is expected to rebound slightly but point continue the trend of falling optimism.

Still to come today we'll get the ADP non-farm employment number, which traders will be eyeing ahead of Friday's jobs report, 49 S&P 500 companies report on the fourth quarter and we'll also get oil inventory data.

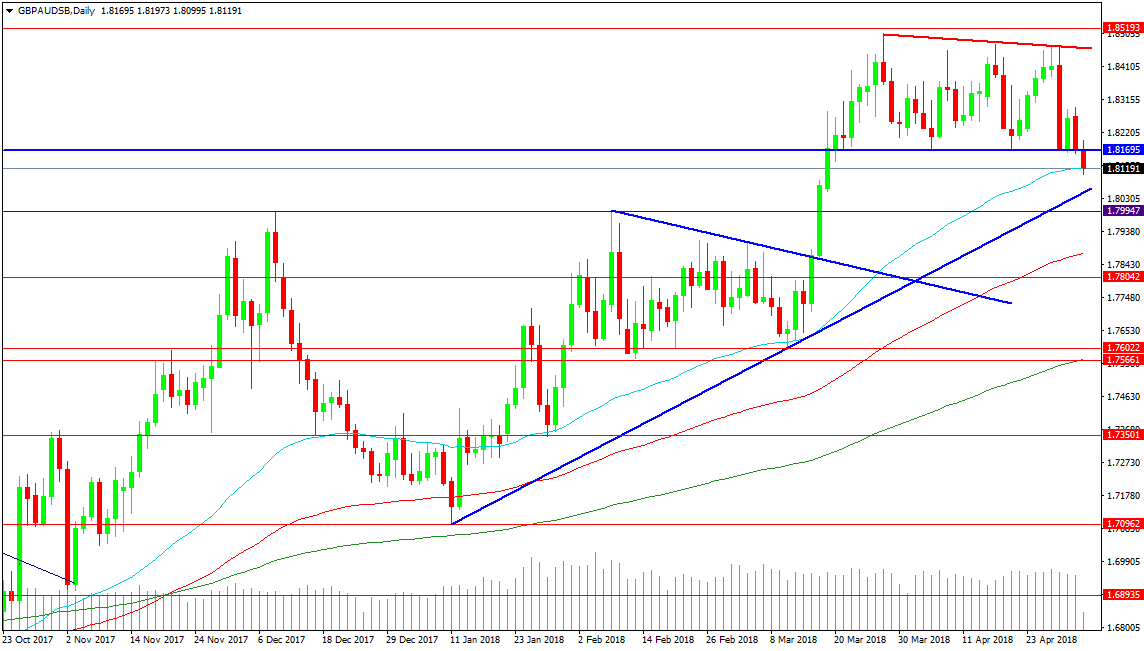

Forex Analysis: GBPAUD And NZDUSD

The price action on this chart shows that the GBPAUD pair has been consolidating sideways after a breakout above 1.80000. The pair has spent most of April in this consolidation, with resistance at 1.85000 and support at 1.81695. Today’s drop below this support level puts the pair on the back foot. Resistance on a break higher comes in at 1.85193, followed by 1.86000 and 1.86715. There was a large drop due to Brexit and this makes finding resistance difficult. The 1.88850 level has featured in the past, with 1.90000 a major level to contend with.

The trend has been rising steadily and the supporting blue trend line can be seen at 1.80435, with the 50 DMA at 1.81219 currently holding price from falling further. The 1.79950 level has been used as resistance in December and February and can be supportive now. A fall under this area targets light support at 1.78042 and the 100 DMA at 1.78700. There is a supportive zone at 1.76025 down to 1.75660 that is being reinforced by the 200 DMA, which could prevent the price from reaching lower levels. A break under this zone targets 1.73500, 1.70962 and 1.68935.

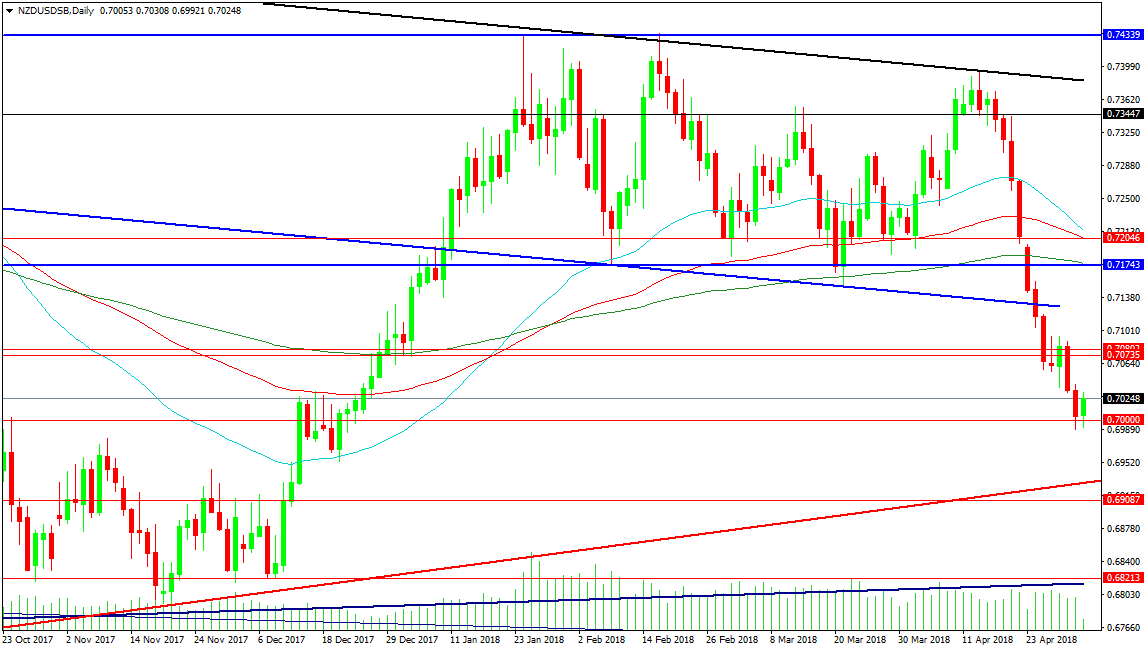

NZDUSD

The NZDUSD pair has broken its pattern and has been steadily declining since the high at 0.73944 on the 13th of April. On this daily chart, the moving averages are starting to turn lower, with price setting new lows for 2018. Support comes in at 0.70000 and we have bounced from this area today. Stronger support can be found at the rising red trend line at 0.69256 and the nearby 0.69087 support level. A fall to the blue trend line at 0.68138 may see buyers stepping in.

Resistance is now positioned at the 0.70735/0.70802 zone, where price consolidated over the last number of days. A retest of this area will decide direction but a break above this zone leaves long positions with a hill still to climb. The falling blue trend line is resistive at 0.71250, with the 0.71743 level reinforced by the 200 DMA. The 0.72046 level has the 100 DMA backing it with the 50 DMA about to start a rapid chase lower to catch the price. Further on, resistance levels are seen at 0.73447 and 0.74339.