Dollar is trading with a soft tone today as traders are cautiously waiting for tomorrow’s job report. And just like how it was in recent months, wage growth will be more important than the headline number. For now, Yen and New Zealand Dollar have stolen the spotlight as both surge strongly. In particular, Yen is taking advantage of data disappointment in Eurozone and UK and jumps sharply higher against Euro and Sterling. Risk aversion could also be a factor as US stocks are set to open lower. Gold also manages to bounce back to 1315, partly thanks to Dollar’s consolidation.

US trade deficit narrowed in general, but widened against China

US trade deficit narrowed to USD -49.0B in March, down USD -8.8B from USD -57.7B in February. That’s also the lowest monthly deficit in six months. March exports rose USD 4.2b to USD 208.5b. Imports dropped USD 4.6b to USD 257.5B.

Trade deficit with China, however, rose USD 0.7B to USD 35.4B in March. Exports to China rose USD 1.6B to USD 12.4B. But imports increased more by USD 2.3B to USD 47.7B. Also, it should be noted that year-to-date, trade deficit widened USD -25.5B, or up 18.5%, from the same period in 2017.

Initial jobless claims rose 2k to 211k in the week ended April 28, below expectation of 225k. The four week moving average dropped 7.75k to 221.5k. Continuing claims dropped -77k to 1.756m in the week ended April 28, lowest since December 8, 1973.

Also released, US nonfarm productivity rose 0.7% in Q1 while unit labor costs rose 2.7%. Canada trade deficit widened to CAD -4.1B in March.

UK PMIs take BoE fingers firmly off rate hike trigger

UK PMI services rose to 52.8 in April, up from 51.7 but missed consensus of 53.5. Markit’s key findings are not too encouraging for the UK. It noted that business activity rises at subdued pace in April. There is the weakest upturn in employment since March 2017 and inflationary pressures are moderate.

Chris Williamson, Chief Business Economist at IHS Markit, noted that the three PMI surveys collectively showed “only a muted rebound in business activity” after the heavy snow in March. And failing to regain February’s growth pace suggested deterioration in underlying performance. The surveys pointed to GDP growth at around 2% at the start of Q2. And, “the disappointing services data will add to expectations that the MPC will take its finger firmly off the rate hike trigger. Any further slowing will also raise questions as to whether the November rate hike may have been ill-timed.”

Eurozone CPI missed, ECB Praet sounded cautious

Eurozone flash CPI slowed to 1.2% yoy in April, down from 1.3% yoy and missed expectation of 1.3% yoy. CPI core performed even worse, dropped to 0.7% yoy, down from 1.0% yoy and missed expectation of 0.9% yoy. ECB chief economist Peter Praet said two hours after the CPI release that while the central bank cannot yet declare “mission accomplished” on inflation, “we have made substantial progress on the path towards a sustained adjustment in inflation.”

But Praet also acknowledged that “the latest economic data and survey results have generally surprised to the downside, suggesting some loss of momentum in economic activity.” But he pointed out that “temporary factors may also be at work”. He emphasized that “we will also need to monitor whether, and if so, to what extent, these developments reflect a more durable softening in demand.”

Australian Dollar lifted by large trade surplus and surge in building approvals

AUD trades broadly higher today as supported by solid economic data. Australia trade surplus came in at AUD 1.53B in March, widened from AUD 1.35B in February. That’s also much larger than expectation of AUD 0.68B. Exports jumped 1% to AUD 34.84B, with strong 8% growth in n non-monetary gold to AUD 131m. Imports rose 1% to AUD 33.31B,. Non-monetary gold imports jumped 28% to AUD 232m.

Building approvals rose 2.6% mom in Mach, much higher than expectation of 1.0% mom. Justin Lokhorst, Director of Construction Statistics at the ABS noted that “the strength in the total dwellings series is being driven by approvals for private sector houses, which have now risen for 13 consecutive months.” And, “private sector house approvals are now at their highest level since 2003, in trend terms.”

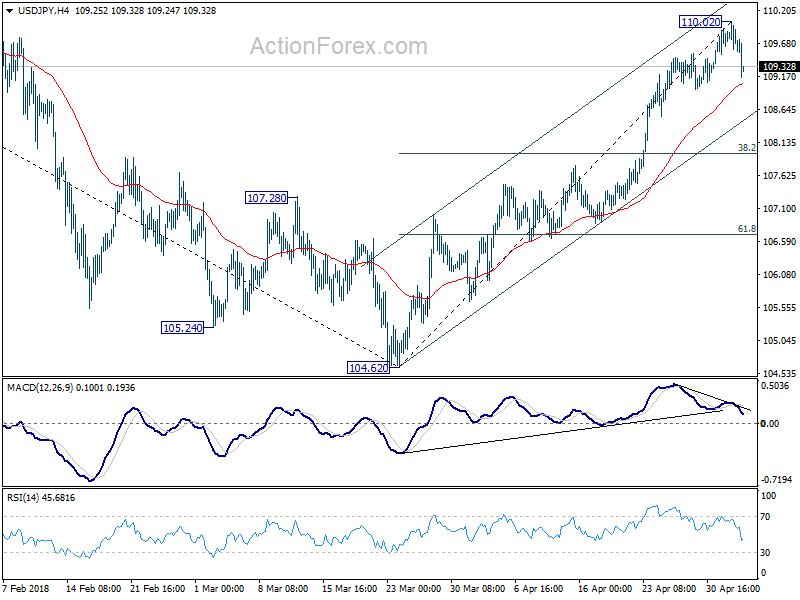

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.61; (P) 109.82; (R1) 110.05; More…

USD/JPY’s sharp decline and break of 109.50 minor support indicates short term topping at 110.02, on bearish divergence condition in 4 hour MACD. Intraday bias is turned to the downside for deeper retreat to near term channel support (now at 108.48). But we’d expect strong support from 38.2% retracement of 104.62 to 110.02 at 107.95 to contain downside and bring rebound. Break of 110.02 will resume the rise from 104.62 to t 61.8% retracement of 114.73 to 104.62 at 110.86 next.

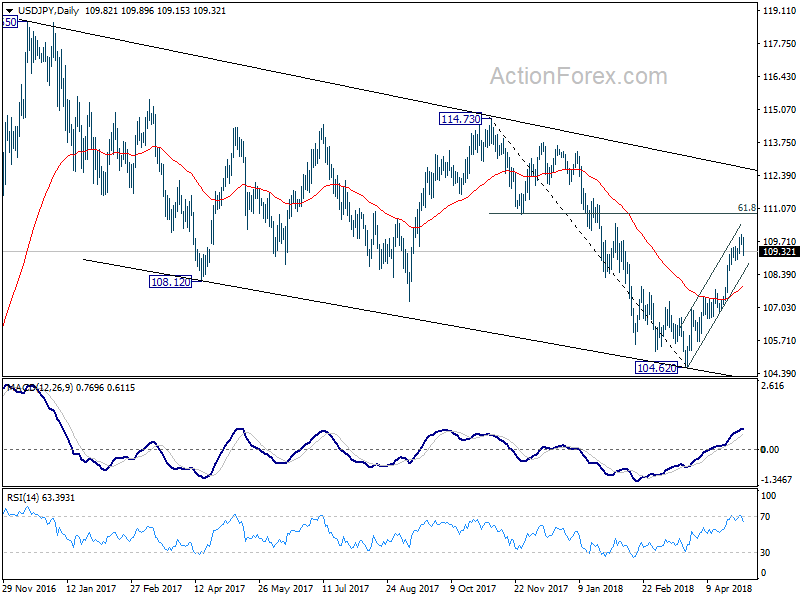

In the bigger picture, break of 108.12 support turned resistance now suggests that corrective fall from 118.65 (2016 high) has completed with three waves down to 104.62. And, rise from 98.97 (2016 low) could be resuming. Focus is back on 114.73 resistance and break there will pave the way to 118.65 and above. This will now be the preferred case as long as USD/JPY stays above 55 day EMA (now at 107.97).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance Mar | 1.53B | 0.68B | 0.83B | 1.35B |

| 01:30 | AUD | Building Approvals M/M Mar | 2.60% | 1.00% | -6.20% | -4.20% |

| 08:30 | GBP | Services PMI Apr | 52.8 | 53.5 | 51.7 | |

| 09:00 | EUR | Eurozone PPI M/M Mar | 0.10% | 0.10% | 0.10% | |

| 09:00 | EUR | Eurozone PPI Y/Y Mar | 2.10% | 2.10% | 1.60% | |

| 09:00 | EUR | Eurozone CPI Estimate Y/Y Apr | 1.20% | 1.30% | 1.30% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr A | 0.70% | 0.90% | 1.00% | |

| 09:00 | EUR | European Commission Economic Forecasts | ||||

| 11:30 | USD | Challenger Job Cuts Y/Y Apr | -1.40% | 39.40% | ||

| 12:30 | CAD | International Merchandise Trade (CAD) Mar | -4.1B | -2.0B | -2.7B | -2.93B |

| 12:30 | USD | Nonfarm Productivity Q1 P | 0.70% | 1.00% | 0.00% | |

| 12:30 | USD | Unit Labor Costs Q1 P | 2.70% | 3.00% | 2.50% | |

| 12:30 | USD | Initial Jobless Claims (APR 28) | 211K | 225K | 209K | |

| 12:30 | USD | Trade Balance Mar | -49.0B | -55.6B | -57.6B | -57.7B |

| 13:45 | USD | US Services PMI Apr F | 54.4 | 54.4 | ||

| 14:00 | USD | ISM Non-Manufacturing/Services Composite Apr | 58.1 | 58.8 | ||

| 14:00 | USD | Factory Orders Mar | 1.40% | 1.20% | ||

| 14:30 | USD | Natural Gas Storage | -18B |

{kind=link}