Sample Category Title

Eurozone PMIs Poised to Show Further Loss of Momentum ahead of ECB Meeting

The Eurozone will see the release of its preliminary PMI prints for April on Monday, at 0800 GMT. Forecasts point to further cooling of economic activity, something likely to be discouraging news for ECB policymakers, who will announce their monetary policy decision on Thursday.

In April, Eurozone’s Markit manufacturing PMI is forecast to decline to 56.1, from 56.6 in March, while the services index is anticipated to dip to 54.6, from 54.9 previously. The composite figure – which blends the two measures – is expected to follow suit, drifting lower for the third consecutive month.

Despite the projected declines, all figures are expected to remain safely above the critical 50 line that separates expansion from contraction, signaling the bloc’s economy is still growing, albeit at a slower pace than previously. If so, this would further confirm the European Central Bank’s (ECB) concerns – that after a very strong start to the year, the economy is now losing momentum.

Coming on top of worries around protectionism, a stronger euro, and still-subdued inflation, fresh signals that the bloc is slowing down would likely amplify speculation that the ECB may adopt a more cautious, “wait-and-see” stance with regards to policy. The Bank is widely anticipated to begin scaling back its asset purchase (QE) program later this year, but continued disappointing data could lead policymakers to appear more conservative, perhaps noting that all options are on the table and that nothing is pre-set.

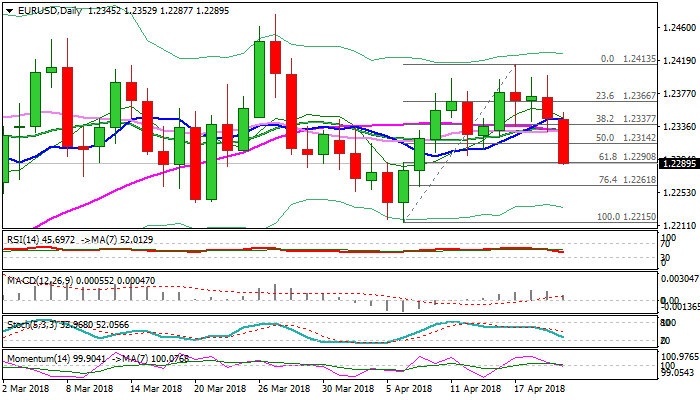

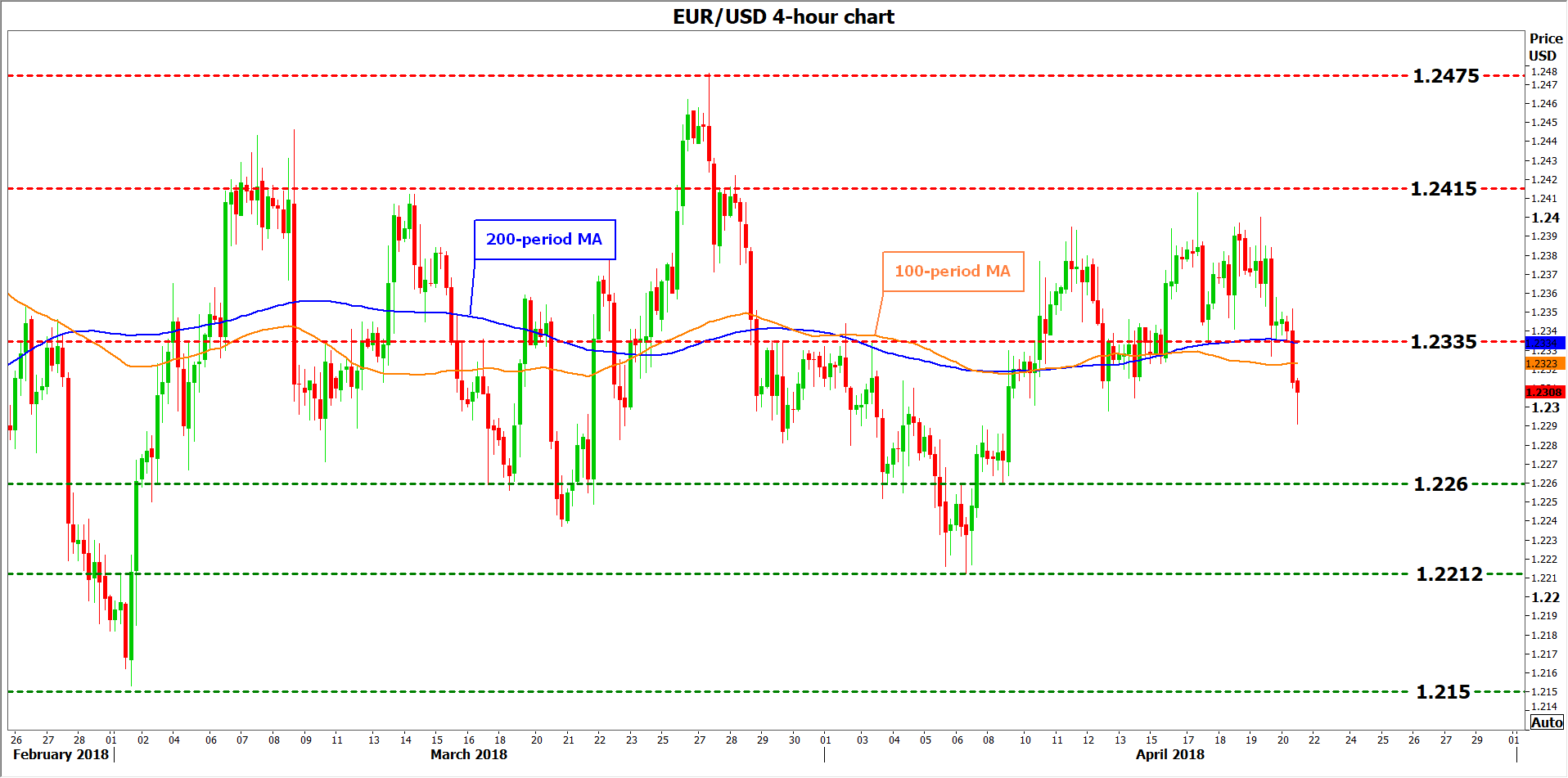

In case the PMIs decline by even more than expected, that could enhance expectations for a more dovish tone by President Draghi and other ECB policymakers when the Bank meets again on Thursday, thereby weighing on the common currency. Euro/dollar could edge lower and challenge the 1.2260 zone – the range around this level was congested recently. A break below this support would initially bring the 1.2212 area into play, defined by the April 6 low, with even steeper declines aiming for 1.2150, the March 1 trough.

In case the PMIs decline by even more than expected, that could enhance expectations for a more dovish tone by President Draghi and other ECB policymakers when the Bank meets again on Thursday, thereby weighing on the common currency. Euro/dollar could edge lower and challenge the 1.2260 zone – the range around this level was congested recently. A break below this support would initially bring the 1.2212 area into play, defined by the April 6 low, with even steeper declines aiming for 1.2150, the March 1 trough.

On the upside, and in case of a positive surprise in the data, euro/dollar could spike higher for a test of the 1.2335 hurdle, marked by the inside swing low on April 17. Notice that the 100-period and 200-period moving averages on the 4-hour chart are not far off this point, at 1.2323 and 1.2334 respectively. An upside break of this territory would initially bring into scope the 1.2415 level, identified by the peaks of April 17, and subsequently the March 27 top at 1.2475.

Finally, note that the corresponding French and German PMIs for April will also be released on Monday ahead of Eurozone’s prints, at 0700 GMT and 0730 GMT respectively. Any major surprises in these figures may trigger a market reaction even before the bloc’s overall data are made public.

Chicago Fed Evans discussed overheating and monetary policy

Chicago Fed President Charles Evans delivered a speech at the University of Wisconsin today. There he laid down "three possibilities concerning low inflation and low unemployment and their implications for monetary policy".

The first one being the "overheating story" and said that the "risks are not particularly high". Evans pointed out that the so called "Phillips curve" is much "flatter" than it was. And, adding to that "inflation expectations low and well anchored, and a lack of fuel from strong wage growth", there is no "outsized risk of a breakout in inflation".

The second scenario is that "inflation is low because the sustainable rate of unemployment is actually much lower than the FOMC's 4-1/2 percent estimate". Therefore, "unemployment rate really isn't putting any pressure on labor markets." In this case, "the risks of overheating would be lower, and perhaps interest rate adjustments could be smaller."

In the third scenario, "unemployment running below its natural rate, u*, without rising inflation is due to labor market inefficiencies that are outside the purview of monetary policy." He added that

"let's consider the possibility that unemployment remains low and some structural problem keeps wages and prices from rising to attract workers. Is this really a problem that monetary policy is suited to address? I think the answer is no."

Finally, Evans also noted that Fed is facing "low inflation trends and low inflation expectations". And, " some cyclical upturn in inflation is actually welcome because it should help solidify expectations symmetrically around our 2 percent objective. This is necessary for achieving our inflation target on a sustainable basis."

His full speech Overheating and Monetary Policy: How Does Low Inflation Affect the Policy Narrative?

Canadian Retail Sales Rise 0.4% in February

Highlights:

- Retail sales rose 0.4% in the month that was in line with market expectations and up from a downwardly revised gain in January of 0.1% (0.3% previously). Retail sales are up 3.5% from a year ago.

- E-commerce sales, which represents 2.7% of overall retail sales, are up 14.6% relative to a year ago levels though this is down from a recently quarterly peak of 35% in the second quarter of last year.

Our Take:

Nominal retail sales rose 0.4% in February which represented an improvement from a downwardly revised gain of only 0.1% in January (0.3% previously). This rebound in large part reflected a recovery in auto sales of 1.9% after a disappointing drop in January. Excluding this component, sales were disappointingly flat with declines in a number of key components including clothing (-1.4%), furniture (-2.0%) and, unexpectedly, gasoline stations (-0.9%). Eliminating the impact of higher prices, the volume of retail sales rose 0.3% in February. This more than reversed the 0.2% drop in January.

The volume of retail sales to date in the first quarter is up a modest 1.2% relative to year ago levels. This reflects a relatively sharp slowing from a recent peak in the second quarter of last year of 7.4%. Our expectation is that in the face of rising interest rates, consumer spending growth will continue to slow through 2018. Last year’s strong increase in consumption was the key contributor to the Canadian economy currently pushing up against capacity limits. So the slowing isn’t unwanted because it will prevent the economy from running too hot and dampens the risk of a pickup in inflationary pressures. To keep growth at a sustainable but non-inflationary pace, our expectation is that the central bank will continue to reduce current highly stimulative monetary conditions. Though the Bank of Canada opted to hold the overnight rate unchanged at 1.25% at this week’s policy meeting, it acknowledged that interest rates will eventually need to move higher. As to the pace of tightening, the best guide offered by the central bank was that it would be “data dependent.”

Canadian underlying inflation trends still generally firm in March

Highlights:

- Year-over-year headline CPI growth rose to 2.3% from 2.2% in February — although that was below market expectations for a 2.4% gain.

- Ex-food & energy price growth strengthened to 1.9% from 1.8% on a year-over-year basis.

- The Bank of Canada’s preferred ‘core’ measures held at a 2.0% average in March although CPI-trim ticked down to 2.0% from 2.1% in February.

Our Take:

The tick higher in the headline CPI rate to 2.3% in March was softer than expected — although with little sign of softening in underlying trends that are still running around a 2% rate or higher. Energy prices rose about as expected given higher gasoline prices. Ex-food & energy price growth also ticked higher — albeit not quite as much as we expected — rising to 1.9% year-over-year from 1.8%. More recent trends have still been stronger than the latest year-over-year rates imply. Month-over-month gains in ex -food & energy prices have averaged 2.9% at an annualized rate over the last 6 months. That’s the highest in 15 years. The Bank of Canada’s measures of ’core’ inflation still averaged right at the central bank’s inflation objective at 2.0%, even with a small tick lower in the CPI-trim to 2.0% from 2.1%. More recent growth trends for those measures have also generally been firm at a slightly above-2% rate.

To be sure, economic growth has softened from the (unsustainable) 4% rate of growth a year ago. Nonetheless, for a ‘data-dependent’ Bank of Canada, the economy still looks to be operating around its long-run capacity limits, wages and inflation have firmed, and underlying economic activity still seems to be improving at a slightly ‘above-potential’ rate once looking through transitory near-term wiggles in the GDP data. Yet the overnight interest rate is still 175 basis points below its assumed long-run ’neutral’ level. Looking through monthly/quarterly volatility, we think the economic data will continue to improve enough to justify further modest removal of what is still a significant amount of monetary policy stimulus in place at this point in the economic cycle.

Comment on Yesterday’s FI Sell-off

Today's key points

- We argue that the combination of a weakening business cycle and central banks sticking to a dovish rhetoric should cap the upside for yields in Q2.

- The risk factor for global FI markets is further spikes in commodity prices, especially if the Trump administration engages in a tougher stance towards Iran.

Global yields have seen upward pressure over the past 24 hours. In our view, there were no obvious drivers for the sell-off but a combination of renewed focus on commodity prices and supply from France and Spain probably drew yields higher in the European market. The negative sentiment was carried over to the US, where 10Y US treasury yields rose 5bp to 2.92% and 2s10s and 5s30s steepened after flattening significantly over the past couple of weeks. 10Y US breakeven inflation expectations rose once again, underlining the impact of higher commodity prices.

However, we doubt we are in for a significant new jump in yields as in January and February, where 10Y Germany rose 35bp over six weeks.

1. The business cycle is weakening

Yesterday, we published a research paper where we looked at the global business cycle. Research: Global business cycle moving lower.

Here, we argue that there are clear signs that the global business cycle peaked in early 2018. Furthermore, our MacroScope models point to a further deceleration over the coming quarters. Declining PMI levels across regions tend to cause some anxiety about the strength of the recovery and would normally put a cap on bond yields.

2. Central banks are not turning more hawkish in Q2

Hence, if global yields are to see further strong upward pressure, the driver needs to be a new spike in commodity prices or change in rhetoric from central banks. We doubt the latter will be the case if the global business cycle is weakening. In that respect, see ECB Preview – Not on Draghi's watch from today, in which we forecast that the ECB will not hike before December 2019. Regarding central bank rhetoric, note also that BoE Governor Mark Carney struck a dovish tone in an interview last night, stating that a few rate hikes may be warranted over the next few years, thus essentially questioning whether a May hike is a done deal after all. Carney came after the close of the Gilt market and Gilts are higher this morning. We also expect a soft stance from the Riksbank next week, as we expect the Riksbank to postpone the first rate hike to 2019.

Commodity prices are the risk factor for global FI markets

In our view, the main risk factor for global FI markets here in Q2 is the global commodity market. The sanctions against Russia could still push some metal prices higher even after aluminium and nickel have jumped recently. In the oil market, it is noteworthy that the supply and demand balance has improved this year (lower stocks). However, especially oil prices could be pushed higher if the Trump administration decides to take a tougher stance on Iran. However, it would be a supply-driven oil price, which the ECB should be less eager to react on.

Bottom line: the risk of a more pronounced fixed income sell-off here in Q2 should be modest, in our view.

Sunset Market Commentary

Markets:

Yesterday’s core bond sell-off slowed today. The US Note future underperformed a flat-trading Bund, but there were no strong trading themes. The eco/event calendar provided no impetus. Declining stock and oil markets suggested a better performance of core bonds. After yesterday’s repositioning lower, we might have entered calmer trading conditions ahead of next week’s ECB meeting. The US yield curve bear steepens with yields 1.3 bps (2-yr) to 2.5 bps (30-yr) higher. The US 10-yr yield (2.93%) approaches this year’s high (2.95%) which is first important resistance. Changes on the German yield curve are modest, varying between -0.5 bps (5-yr) and +1.1 bp (30-yr). 10-yr yield spreads vs Germany are close to unchanged.

Yesterday afternoon’s dollar rebound continued and even accelerated without obvious trigger. There is no one-on-one link between the dollar and interest rate differentials with other majors like the euro. That said, the absolute interest rate differential at the short end of the curve is becoming huge, making it expensive to hold dollar shorts (2y US yield at 2.44%, 2y US/German interest differential touching 3%!). In the same context, the market is ever more shifting in the direction of three additional Fed rate hikes this year, despite recent global uncertainty. Other factors like a topping out pattern in the oil price maybe helped some further USD gains. Whatever the reason, USD momentum is clearly improving. EUR/USD dropped below the 1.23 barrier. USD/JPY is also holding up well even as the equity rally is losing steam. USD/JPY is trending higher in the 107 big figure.

Sterling was looking for a new equilibrium today after BoE’s Carney yesterday gave an interview that made markets question the scenario of a May BoE rate hike. Sterling remained under pressure early in the session as interest markets discount only a probability of about 50% for a May rate hike, compared to 80% before the Carney comments. EUR/GBP rebounded to the high 0.87 area. However, the sterling decline gradually eased. BoE Sauders in a speech agreed that any further policy normalization should develop in a gradual way. Even so, he maintained his call for an ‘early’ rate hike as he saw a capacity constraints building in the UK economy. The immediate reaction of sterling was limited an short-lived. EUR/GBP hovers in the mid 0.87 area. Cable is holding a relatively tight sideways range in the mid 1.40 area.

News Headlines:

BoE Saunders is sticking to his guns, arguing for further interest-rate increases the day after Governor Carney came out with a surprisingly cautious outlook. “We do not need to set policy in a way that will create rising spare capacity or higher unemployment. But our foot no longer needs to be so firmly on the accelerator.”

US President Trump has blasted the oil producer group Opec for driving oil prices to the highest level since 2014, saying that crude prices have been driven “artificially” high. Brent crude declined from $74/barrel to the $73/barrel area.

Canadian eco data disappointed. Core retail sales stabilized on a monthly basis in February (vs +0.4% M/M increase expected). Headline inflation hit the highest level in three year (2.3% Y/Y), but fell short of expectations (2.4% Y/Y). The Canadian dollar continued the correction lower which started after Wednesday’s BoC meeting. USD/CAD cruised above 1.27.

Canada: Retail Sales Volumes Slightly Higher in February

Retail sales advanced 0.4% in February. The increase was almost entirely due to volumes, which rose 0.3%. However, volumes were revised down notably in the prior three months.

Higher sales at motor vehicle and parts dealers was the main driver behind February's gain (+1.4%), with sales excluding this category flat in the month. Still, sales were higher at general merchandise stores (+2.0%) and miscellaneous retailers (0.4%). On the opposite end of the spectrum, sales dropped in most other categories, with notable declines in furniture, home furnishing and electronics (-2.0%), gasoline stations (-0.9%) and clothing and clothing accessories stores (-1.4%).

Sales were higher in seven of ten provinces, though the majority of the gain was concentrated in Ontario. There were also relatively large gains in Nova Scotia (+3.2%), Saskatchewan (0.6%), and Quebec (0.5%). Conversely, sales dropped in Manitoba (-1.9%) and Alberta (-0.3%), while dipping slightly in Newfoundland and Labrador (0.1%).

Key Implications

Though volumes increased in February, downward revisions to earlier months imply weaker spending momentum early in 2018 than previously thought. So far in the first quarter, volumes are down 1.5% compared to Q4's average, pointing to softer consumer spending in Q1.

That said, we still expect consumer spending to contribute to economic growth in 2018, buoyed by a healthy labour market. However, some easing is expected from 2017's turbocharged rate, as spending is dampened by weaker housing market activity and rising interest rates.

February's gain in volumes puts real GDP on track for increase of 1.6% in Q1, not far from the Bank of Canada's recently revised estimate of 1.3%. As such, today's report likely does little to alter current outlook at the Bank, with policymakers likely to continue a gradual pace of normalization, with the next hike expected this summer.

Canadian Inflation Edges Up in March

Consumer prices rose 2.3% year-on-year (year-on-year) in Canada in March, a hair below the consensus estimate of 2.4%, but up from 2.2% in January. Price growth edged down on a month-on-month basis (seasonally adjusted), rising 0.1% (from 0.2% in February).

Energy prices (+7.5 y/y) and gasoline (+17.1% ) in particular were a key contributor to the headline gain in inflation. Elsewhere it was a pretty mixed bag. Year-on-year inflation accelerated for half of the major categories and decelerated for the other half. The same story was true month-on-month price growth, with declining prices for clothing and footwear (-0.6%, seasonally adjusted) and household operations (-0.2%) offsetting decent gains for health and personal care (+0.7%), recreation and education (+0.6%), and tobacco and alcohol (+0.9%)

The Bank of Canada's core price measures were largely unchanged, with only CPI-trim edging down to 2.0% (from 2.1%), while CPI-median remained unchanged at 2.1% and CPI-common at 1.9%.

Key Implications

After some excitement at the move higher in inflation in February, price pressures appear to have settled down a touch in March. Outside of energy prices, which will continue to put upward pressure on inflation given recent gains in oil prices, price growth was tepid in March.

With the Bank of Canada upgrading its outlook for inflation and noting temporary factors as the reason for near-term strength, there is a high bar for inflation to jump over to get the central bank to move faster on raising interest rates. Still, one more hike is likely on tap this year, consistent with the improved outlook for future economic growth, both globally and domestically.

USDCAD Extends Recovery after Weak Canadian Data

The pair extends recovery into third straight day on Friday and broke through 100SMA (1.2678) as loonie was hit by weak Canadian data (CPI 0.3% Mar vs 0.4% f/c and 0.6% Feb / core retail sales 0.0% Feb vs 0.3% f/c and 1.0% Jan). Recovery leg of 1.2527 (17 Apr low) extends and pressures falling 20SMA (1.2731), eyeing pivotal barrier at 1.2755 (Fibo 38.2% of 1.3124/1.2527 descend, reinforced by 55SMA). Firm break here is needed to signal stronger correction of 1.3124/1.2527 fall, which could extend towards next key barrier at 1.2846 (daily cloud top). Caution of possible recovery stall as slow stochastic is overbought on daily chart and momentum studies remain weak. Broken 100SMA now acts as initial support, guarding strong support at 1.2621 (converged 200/10SMA's), loss of which will be bearish.

Res: 1.2731; 1.2755; 1.2813; 1.2846

Sup: 1.2678; 1.2621; 1.2585; 1.2545

EURUSD – Bears Could Extend to Daily Cloud Base on Acceleration Through 1.2290 Fibo Support

The Euro extended weakness on Friday and tested support zone at 1.2299/90, driven by stronger dollar and hedging for option expiries.

The pair holds just above new daily low at the beginning of the US session, with strengthening negative near-term sentiment, seeing risk of deeper fall.

Weekly close below 1.2290 pivot (Fibo 61.8% of 1.2215/1.2413 upleg) would generate stronger bearish signal for further weakness towards key supports at 1.2235 (daily cloud base) and 1.2215 (06 Apr low).

Strong barrier at 1.2329 (converged 20/30/55SMA’s) is expected to keep the upside protected.

Res: 1.2314; 1.2329; 1.2350; 1.2400

Sup: 1.2261; 1.2235; 1.2215; 1.2200