Sample Category Title

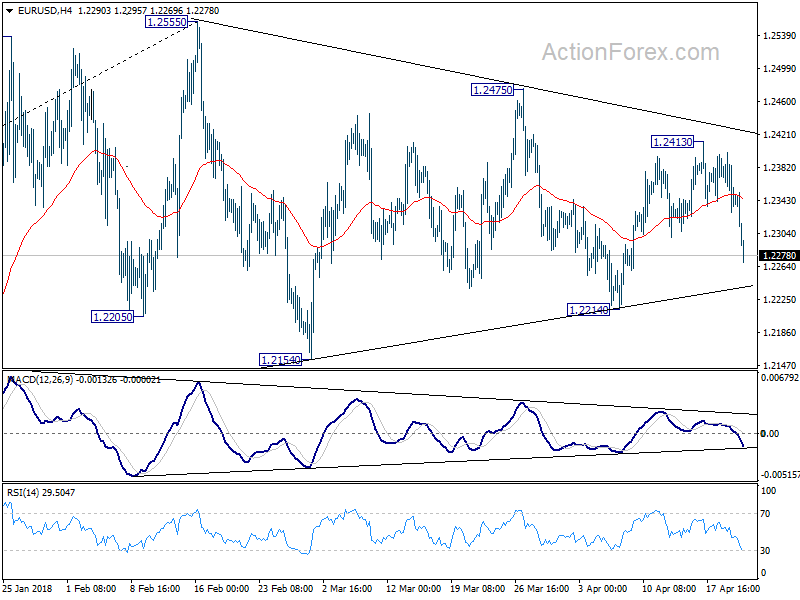

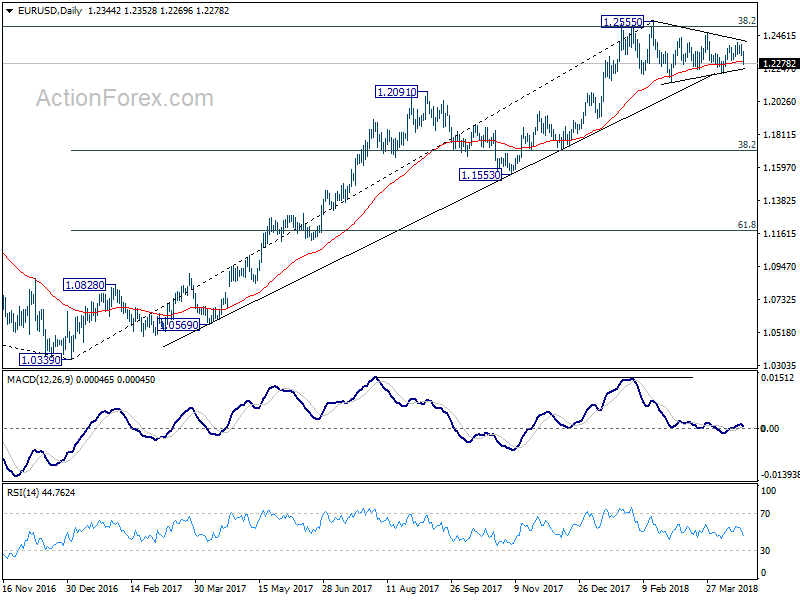

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2315; (P) 1.2358 (R1) 1.2386; More....

EUR/USD's sharp decline today now put 1.2214 support in focus. Decisive break there will revive the case of trend reversal, after rejection by 1.2516 key fibonacci resistance. In that case, outlook will be turned bearish for 1.2154 support and below.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

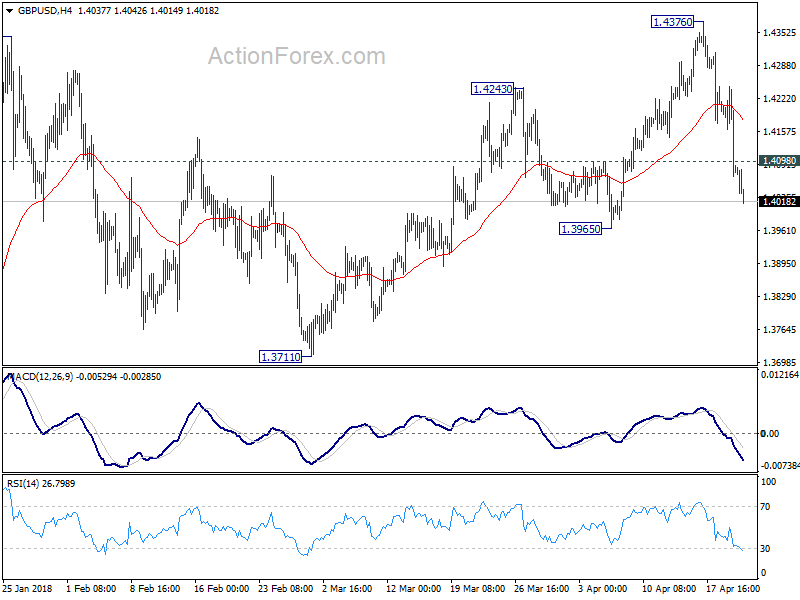

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4016; (P) 1.4131; (R1) 1.4195; More...

GBP/USD decline extends to as low as 1.4018 so far. Intraday bias stays on the downside for 1.3965 support. Considering bearish divergence condition in daily MACD, a medium term could be in place at 1.4376 already. Break of 1.3965 will pave the way to retest 1.3711 key support level. On the upside, above 1.4098 minor resistance will turn intraday bias neutral first.

In the bigger picture, rise from 1.1946 (2016 low) could be still in progress . It is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. We'd continue to favor this medium term bullish view as long as 1.3711 support holds, even in case of deep pull back.

In the bigger picture, rise from 1.1946 (2016 low) could be still in progress . It is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. We'd continue to favor this medium term bullish view as long as 1.3711 support holds, even in case of deep pull back.

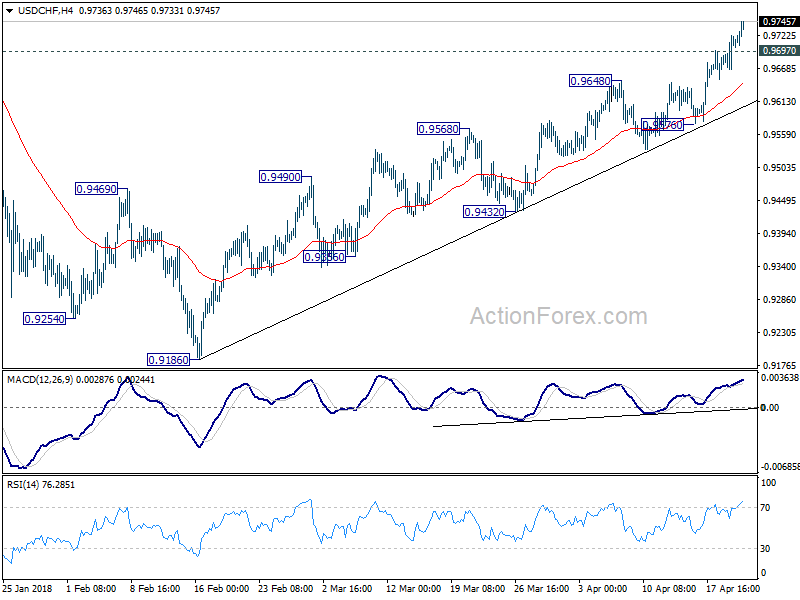

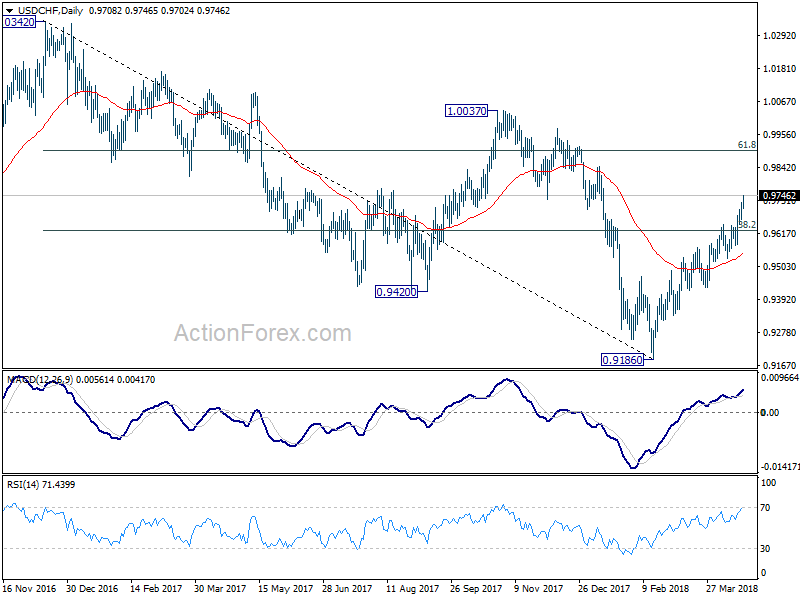

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9677; (P) 0.9700; (R1) 0.9735; More...

USD/CHF reaches as high as 0.9745 so far and intraday bias remains on the upside. Current rise from 0.9186 is expected to target 0.9900 fibonacci level next. On the downside, below 0.9697 minor support will turn bias neutral and bring consolidations. But outlook will stay bullish as long as 0.9576 support holds.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next.

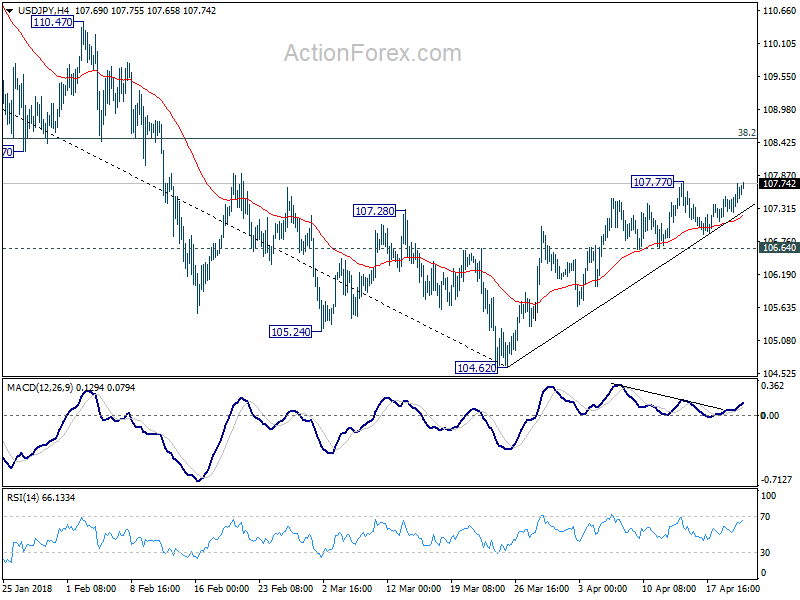

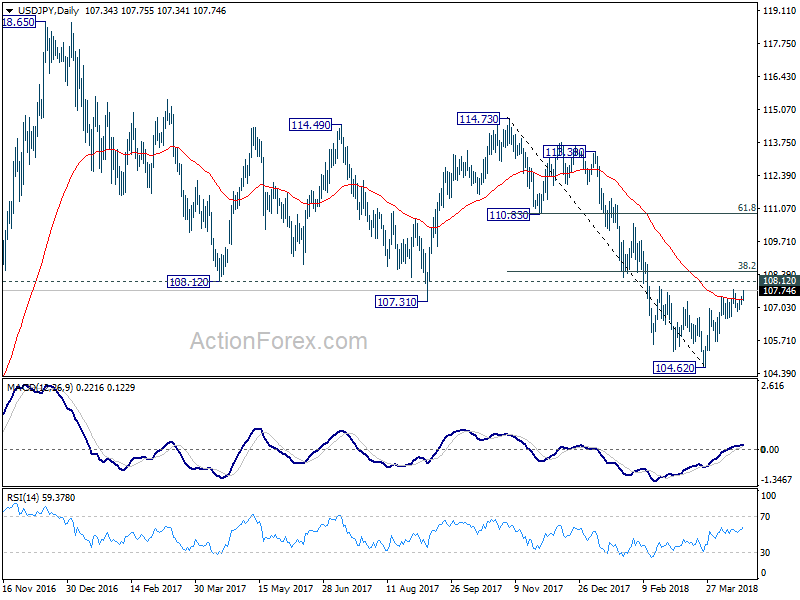

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 107.17; (P) 107.34; (R1) 107.53; More...

At this point, USD/JPY is still held below 107.77 and intraday bias remains neutral first. Break of 107.77 will target 38.2% retracement of 114.73 to 104.62 at 108.48 which is close to 108.12. This level is crucial in determining the medium outlook. On the downside, break of 106.64, however, will indicate the rebound from 104.62 has completed. And in that case, bias will be turned back to the downside for retesting 104.62.

In the bigger picture, as long as 108.12 support turned resistance holds, the medium term down trend from 118.65 (2016 high) should still continue lower, at least to retest 98.97 (2016 low). However, sustained break of 108.12 will be an early sign of medium term reversal. In that case, further rise would be seen to 114.73 resistance to confirm completion of the fall from 118.65.

In the bigger picture, as long as 108.12 support turned resistance holds, the medium term down trend from 118.65 (2016 high) should still continue lower, at least to retest 98.97 (2016 low). However, sustained break of 108.12 will be an early sign of medium term reversal. In that case, further rise would be seen to 114.73 resistance to confirm completion of the fall from 118.65.

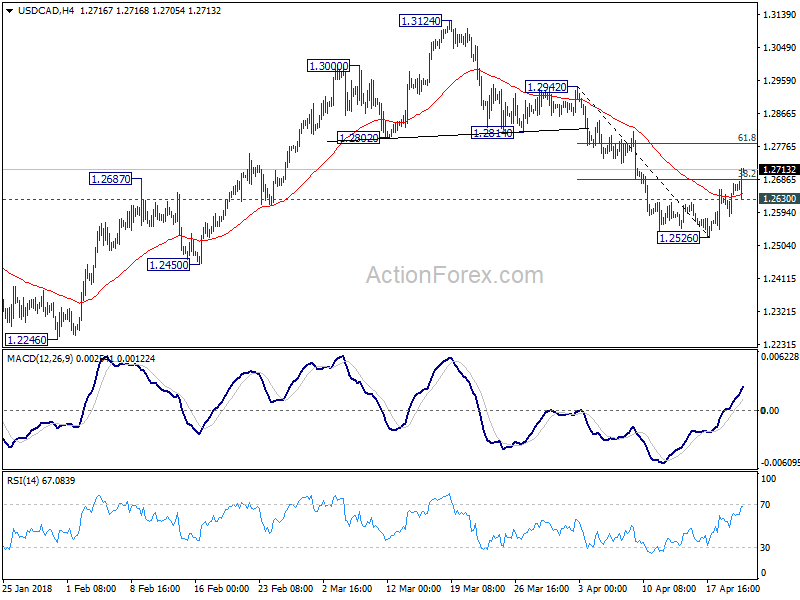

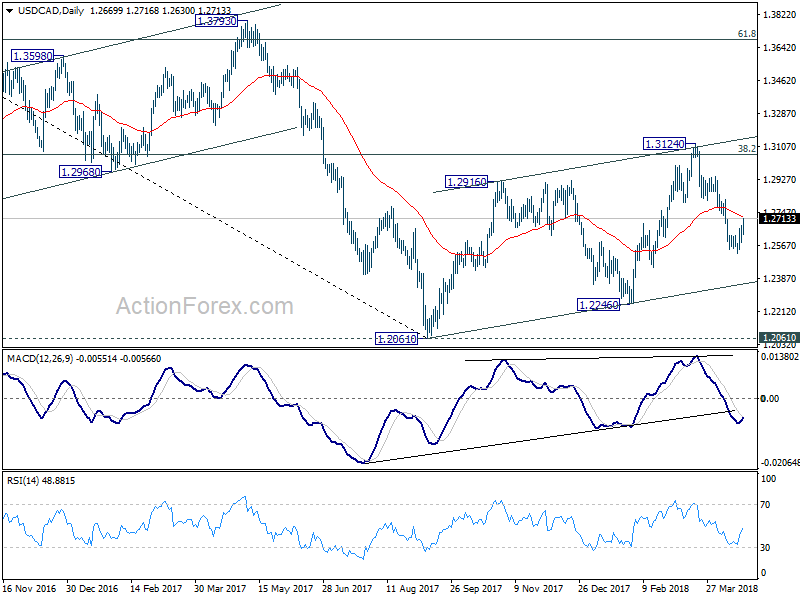

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2611; (P) 1.2643; (R1) 1.2702; More....

USD/CAD's rebound from 1.2526 extends to as high as 1.2716 so far, breaking 38.2% retracement of 1.2942 to 1.2526 at 1.2685. Intraday bias stays on the upside for 55 day EMA (now at 1.2725) and above. For now, such recovery is seen as a correction. Hence, we'd expect strong resistance below 1.2814 support turned resistance and bring fall resumption. Below 1.2630 minor support will turn bias back to the downside for 1.2526. However, sustained break of 1.2814 will turn focus back to 1.3124 instead.

In the bigger picture, current development turns favors to the case that rise from 1.2061 is a corrective three wave pattern. It could have completed at 1.3124 after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Focus is now back on 1.2061 and 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Decisive break there will resume larger down trend from 1.4689 (2016 high) to 61.8% retracement of 0.9406 to 1.4689 at 1.1424.

Canadian Dollar Selloff Extends after CPI and Retail Sales Misses, Dollar Rally Accelerating

Dollar's broad based rally continues today and is showing sign of acceleration. In particular, while Euro has been rather resilient, EUR/USD is starting to be dragged down by others as it dips through 1.23. While there is still some way to go, focus is now back o 1.2214 support and a break there could prompt further rally in the greenback. Meanwhile, Japanese Yen seems to be relatively immune against Dollar as USD/JPY is still bounded in range below 107.77. As the current rally in Dollar is more driven by surging treasury yields than anything else, development in both will be the main focus before the week closes.

Loonie selloff resumes after data misses

Canadian Dollar is suffering another selloff after disappointing economic data. Headline retail sales rose 0.4% mom in February, below expectation of 0.5% mom. Ex-auto sales was even worse, flat mom, versus expectation of 0.5% mom rise. Headline CPI rose 0.3% mom, 2.3% yoy in March, below expectation of 0.4% mom, 2.4% yoy. February's figure was 0.6% mom, 2.2% yoy. Core CPI common was unchanged at 1.9% yoy, below expectation of 2.0% yoy. Core CPI median was unchanged at 2.1% yoy, below expectation of 2.2% yoy. Core CPI trim slowed to 2.1% yoy, down from expectation of 2.1% yoy and missed expectation of 2.1% yoy.

The Loonie has been under some much selling pressure after BoC left no indication of a near term rate hike earlier this week in its rate decision statement. BoC also revised down 2018 growth forecasts and sounded cautious on a number of uncertainties, including NAFTA renegotiation and geopolitical tension. NAFTA talks are carrying on in Washington today. As Canadian Foreign Minister Chrystia Freeland noted yesterday, there were "good progress". But she didn't indicate on a timeline to finish it, just saying "we'll work as long as it takes to get a great deal".

Sterling stays week as BoE May hike is far from certain

Sterling turned a bit mixed today but not because it's stabilizing. The Pound remains under pressure against Dollar and Euro. There was also sign of acceleration in the selloff. But for today, Pound selling is overwhelmed by selling in commodity currencies instead. Sterling is so far the second weakest for the week, just after New Zealand Dollar.

Sterling was initial quite resilient after triple data misses this week. But BoE Mark Carney's comments somehow closed the case for it. The key takeaway from Carney's comment is that he tried to tone down the chance of a May hike. He said "we have had some mixed data … We'll sit down calmly and look at it all in the round." He added that "there will be some differences of view but it is a view we will take in early May, conscious that there are other meetings over the course of this year."

A BoE May hike is now far from being certain.

EUR/CHF still struggling to overcome 1.2

EUR/CHF is another major focus of today as it breached 1.2 handle to 1.2004 but quickly dipped back. The reaction to this 1.2 handle is worth some attention, not just for it's being a historical floor set by SNB. But also, rejection from 1.2 could prompt a pull back in Euro elsewhere. And as a chain reaction, deeper selloff in EUR/USD could push up the greenback elsewhere.

At this special moment, SNB Chairman Thomas said in an interview that the depreciation of the Swiss Franc is in the "right direction". Nonetheless, the currency as a safe haven is prone to change and the situation is "fragile". So the SNB will "remain very prudent". Jordan added that "there's no need to do anything regarding monetary policy at this moment", as "we are convinced that the current monetary policy is still necessary."

Japan core inflation slowed in March, BoJ Kuroda warned on protectionism

Japan national CPI core slipped back to 0.9% yoy in March, down from February's 1.0% yoy, meeting market expectations. It will take a few more months to see if it's only a blip or a change in trend. Core inflation had an impressive up this year but momentum has been slowing. It's already looking a be challenging for inflation to meet BoJ's own media projection of 1.4% in the current fiscal year. And BoJ might need to delay the timing for hitting 2% target again, if the slowdown in inflation persists.

Separately, BoJ Governor Haruhiko Kuroda stepped up his warning on protectionism, as he arrived at the G20 summit of finance ministers and central bankers. He said there will be "quite comprehensive" debate on trade during the meeting. And he emphasized that "many countries share the view they benefit greatly from free trade, so I don't think protectionism will spread and lead to a decline in global growth. But the risk is there." He added that "protectionism isn't having a huge impact on Japan's economy yet. But the risk is right in front of us, so we need to carefully watch how developments unfold."

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2611; (P) 1.2643; (R1) 1.2702; More....

USD/CAD's rebound from 1.2526 extends to as high as 1.2716 so far, breaking 38.2% retracement of 1.2942 to 1.2526 at 1.2685. Intraday bias stays on the upside for 55 day EMA (now at 1.2725) and above. For now, such recovery is seen as a correction. Hence, we'd expect strong resistance below 1.2814 support turned resistance and bring fall resumption. Below 1.2630 minor support will turn bias back to the downside for 1.2526. However, sustained break of 1.2814 will turn focus back to 1.3124 instead.

In the bigger picture, current development turns favors to the case that rise from 1.2061 is a corrective three wave pattern. It could have completed at 1.3124 after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Focus is now back on 1.2061 and 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Decisive break there will resume larger down trend from 1.4689 (2016 high) to 61.8% retracement of 0.9406 to 1.4689 at 1.1424.

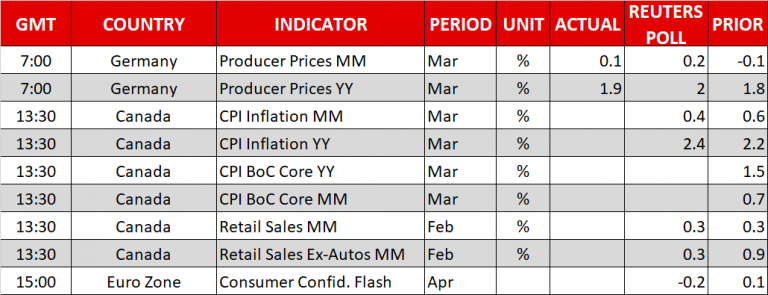

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Mar | 0.90% | 0.90% | 1.00% | |

| 04:30 | JPY | Tertiary Industry Index M/M Feb | 0.00% | 0.00% | -0.60% | -0.40% |

| 06:00 | EUR | German PPI M/M Mar | 0.10% | 0.20% | -0.10% | |

| 06:00 | EUR | German PPI Y/Y Mar | 1.90% | 2.00% | 1.80% | |

| 12:30 | CAD | Retail Sales M/M Feb | 0.40% | 0.50% | 0.30% | 0.10% |

| 12:30 | CAD | Retail Sales Ex Auto M/M Feb | 0.00% | 0.50% | 0.90% | 1.00% |

| 12:30 | CAD | CPI M/M Mar | 0.30% | 0.40% | 0.60% | |

| 12:30 | CAD | CPI Y/Y Mar | 2.30% | 2.40% | 2.20% | |

| 12:30 | CAD | CPI Core - Common Y/Y Mar | 1.90% | 2.00% | 1.90% | |

| 12:30 | CAD | CPI Core - Median Y/Y Mar | 2.10% | 2.20% | 2.10% | |

| 12:30 | CAD | CPI Core - Trim Y/Y Mar | 2.00% | 2.10% | 2.10% | |

| 14:00 | EUR | Eurozone Consumer Confidence Apr A | -0.1 | 0.1 |

CAD selloff resumes as CPI and retail sales missed expectations

CAD's selloff resumes after disappointing data from Canada.

Headline retail sales rose 0.4% mom in February, below expectation of 0.5% mom.

Ex-auto sales was even worse, flat mom, versus expectation of 0.5% mom rise.

Headline CPI rose 0.3% mom, 2.3% yoy in March, below expectation of 0.4% mom, 2.4% yoy. February's figure was 0.6% mom, 2.2% yoy.

Core CPI common was unchanged at 1.9% yoy, below expectation of 2.0% yoy.

Core CPI median was unchanged at 2.1% yoy, below expectation of 2.2% yoy.

Core CPI trim slowed to 2.1% yoy, down from expectation of 2.1% yoy and missed expectation of 2.1% yoy.

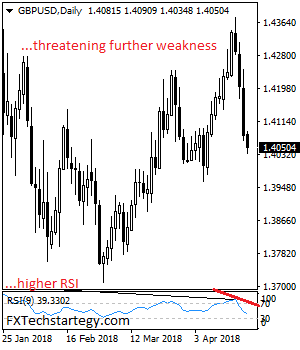

GBPUSD: Weakens Further On Bear Pressure

GBPUSD: The pair weakened further on Thursday and followed through on Friday leaving risk lower in the days ahead. Support lies at the 1.4000 level where a break will turn attention to the 1.3950 level. Further down, support lies at the 1.3900 level. Below here will set the stage for more weakness towards the 1.3850 level. Conversely, resistance stands at the 1.4100 levels with a turn above here allowing more strength to build up towards the 1.4150 level. Further out, resistance resides at the 1.4200 level followed by the 1.4250 level. On the whole, GBPUSD remains biased to downside.

Carney Strikes Down Hawks, Lira Trades Sideways

Buying sentiment towards the British Pound deteriorated sharply yesterday, after dovish comments from Bank of England’s Governor Mark Carney heavily diluted expectations of an interest rate hike in May.

Carney’s cautious tone and his acknowledgement of recent “mixed” economic data, planted a seed of doubt among investors that the central bank will take action next month. With inflation cooling, retail sales disappointing and a dovish Carney entering the scene, Sterling bulls could be in trouble. The probability of a rate hike in May plunged to below 50% (down from 70% before Carney spoke) and this continues to punish the currency. Sensitivity to monetary policy speculation is likely to remain a key fundamental theme impacting the British Pound. If market expectations continue to deteriorate over higher U.K interest rates, Sterling could be exposed to further downside risks.

Taking a look at the technical picture, this has been a terribly bearish week for the GBPUSD, with prices trading around 1.4060 as of writing. Previous support at 1.4100 could transform into a dynamic resistance that encourages a decline lower towards 1.4000. If bulls are able to push prices back above 1.4100, the next key level of interest will be 1.4230.

Turkish Lira takes a breather

It has certainly been a positive trading week for the Lira, as a surprise announcement of snap elections in Turkey boosted appetite for the currency.

President Tayyip Erdogan called an early election for 24 June, creating a sense of optimism among investors that political stability would increase. The main risk event for the Lira next week will be the Central Bank of the Republic of Turkey’s (CBRT) monetary policy meeting. There is speculation over a potential rate hike in April, following Erdogan’s call for early presidential and parliamentary polls. The Lira could receive further support if the CBRT raises interest rates.

From a technical standpoint, the USDTRY remains under pressure on the daily charts, with prices trading around 4.05 as of writing. A failure of bulls to secure a daily close above 4.05 could result in a decline towards the 4.00 level. Alternatively, a weekly close above 4.05 could inspire bulls to challenge 4.10.

Commodity spotlight – Gold

Gold depreciated on Friday as easing geopolitical tensions and hopes of higher U.S interest rates dented appetite for the yellow metal.

The yellow metal continues to be driven by conflicting fundamental themes and this is reflected in the price action witnessed over recent weeks. While bulls remain inspired by geopolitics, lingering trade war fears and U.S political risk, bears have found support in the form of rising U.S rate hike expectations.

Gold is likely to remain a battleground for bulls and bears until a fresh directional catalyst is brought into the picture. Taking a look at the technical picture, prices could challenge $1360 if bulls are able to keep above $1340. Alternatively, a breakdown below $1340 may result in a decline towards $1324.

Euro Under Pressure; Canadian CPI Pending

Here are the latest developments in global markets:

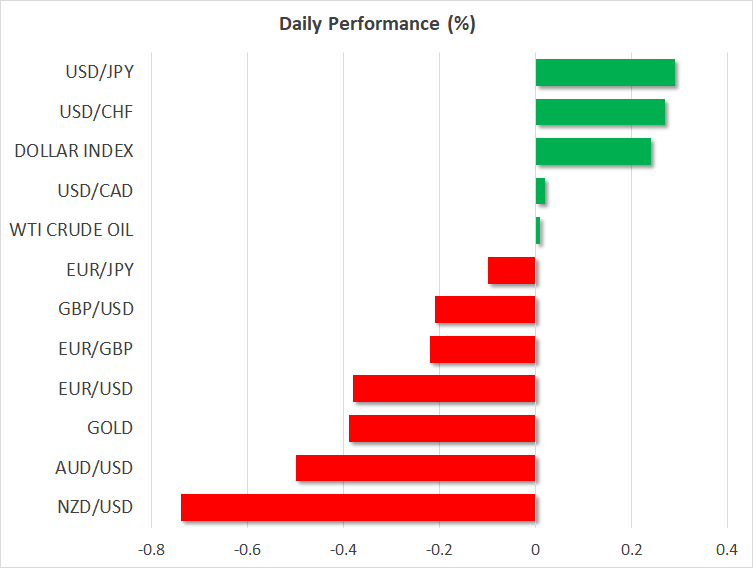

FOREX: The dollar index, which gauges the greenback’s strength versus six major currencies, was up, standing at 90.14 (+0.22%). Dollar/yen managed to pick up speed, rising to 107.66 (+0.28%), boosted by the strong rally in US treasury yields. Pound/dollar was flirting with two-week lows, last seen at 1.4060 (-0.20%) following a deep fall yesterday immediately after the BoE Governor, Mark Carney, signaled that the central bank may not rush to raise interest rates in May showing concern on this week’s discouraging economic numbers. Euro/dollar fell by 0.34% ahead of the European Central Bank meeting next week, where policymakers might give some clues on their plans to remove monetary stimulus. However, analysts believe that the central bank could hold a cautious stance on the face of this week’s disappointing data out of the Eurozone. Dollar/loonie was in a range on Friday after completing two bullish days, moving marginally higher by 0.02% before the release of the Canadian CPI later today. Antipodean currencies were trading significantly lower, with aussie/dollar and kiwi/dollar being down at 0.7692 (-0.45%) and 0.7216 (-0.76%) respectively. Euro/Swiss franc turned lower to 1.1978 (-0.07%) after touching a fresh three-year high of 1.2004 during the Asian session.

STOCKS: European markets were mixed at 0933 GMT. The pan-European STOXX 600 was weaker by 0.12%, while the blue-chip Euro STOXX 50 was slightly up by 0.15%. The German DAX 30 fell by 0.07%, the French CAC 40 lost 0.08%, the Italian FTSE MIB traded higher by 0.30% and the UK’s FTSE 100 climbed by 0.37%. Asian equities closed lower except the Japanese Topix which finished the session up by 0.05%. US stocks dropped for the first time in three days yesterday, as technology shares came under pressure from trade and earnings concerns. Futures tracking US indices are poised to open lower today.

COMMODITIES: Oil managed to recover part of yesterday’s losses, with WTI bouncing up to $68.33 (+0.06%) and Brent crawling up to $73.89 (+0.15%) a barrel respectively. Gold traded lower by 0.37% at $1,340.2 per ounce.

Day ahead: Canada reports on inflation and retail sales; Eurozone consumer confidence in focus

Day ahead: Canada reports on inflation and retail sales; Eurozone consumer confidence in focus

In terms of data, Canadian consumer prices and retail sales, as well as Eurozone’s preliminary figures on consumer confidence will attract the most attention later today. Brexit developments could also be in the spotlight as the latest headlines showed that the Irish border issue remains a sticking point in Brexit negotiations.

At 1230 GMT, Canada will see the release of the March CPI, with analysts projecting headline inflation to pick up by 2.4% year-on-year compared to 2.2% growth in February but the rise could be due to temporary factors such as increases in oil prices and higher minimum wages according to the Bank of Canada. On a monthly basis, consumer prices are expected to ease by 0.2 percentage points to 0.4%. Core measures, which are closely watched by the BoC, could be in focus as well, leading the loonie higher if they appear to be heading upwards towards the mid-point of the central bank’s target range of 1-3.0% (no analyst estimates are available for these indices). At the same time, the loonie could face additional volatility from retail sales if the numbers deviate from forecasts. According to analysts, consumer spending could expand by 0.3% m/m in February as in January.

In the Eurozone, April’s initial estimates on consumer confidence will come under review at 1500 GMT. The index returned to positive territory in November for the first time in almost two decades, giving a boost to the euro, but first estimates are now for the gauge to post negative marks again, falling by 0.2% in April. Should the confidence index decline more than anticipated, the euro could extend today’s losses.

In oil markets, investors will be waiting for the Baker Hughes oil rig count to come out at 1700 GMT after both the American Petroleum Institute and the Energy Information Administration indicated a surprising decline in US oil inventories, lifting crude prices to three-year highs. In case Baker Hughes shows a smaller number of active US oil rigs, oil prices could reach fresh peaks.

Meanwhile in the UK, optimism on Brexit was in doubt after reports that the EU is set to reject May’s proposals to avoid a hard border in the Northern Ireland after UK’s departure from the bloc. While the UK has not made any formal announcement on its plans on the issue yet, some officials said that a border should be applied to the whole of the UK, with the no part of the country remaining in the customs union and the single market. This, however, contradicts the EU preferences which want a border only in Northern Ireland, questioning whether progress in Brexit talks could continue.

As for today’s public appearances, Chicago Fed President, Charles Evans (non-voting FOMC member in 2018), and San Francisco Fed Governor, John Williams (voter), will be talking at 1340 GMT and 1515 GMT respectively. A news conference by the G20 Finance ministers will attract interest at 1645 GMT as finance ministers and central bankers from around the world are meeting in Washington this week for meetings of the International Monetary Fund and World Bank.