Sample Category Title

Quiet Start to a Week of Guaranteed Volatility, on Yields, Central Banks, Data and Politics

The financial markets are pretty quiet as another week starts. Despite positive news regarding Korean peninsula, major Asian indices are trading slightly lower. At the time of writing, Nikkei is down -0.28%, HK HSI is down -0.66%. In the currency markets, major pairs and crosses are bounded in Friday's range, which are, admittedly quite wide. Sterling is recovering some losses and is broadly higher. Yen is trading in red in general.

The week ahead, nonetheless, almost certainly guarantees more volatility. In the financial markets, US Treasury yields is one that will catch much attention. Eyes will be on whether 10 year yield could break through 3% handle, and the subsequent reactions in stocks and Dollar.

Regarding central banks, ECB and BoJ will announce rate decisions. There is little expectation on BoJ as usual. But markets are still keen to get hints on what ECB would do when the asset purchase program ends in September. On economic data front, there will be Q1 GDP from US and UK, Eurozone PMIs and German Ifo, Australia inflation, New Zealand trade balance.

On Geopolitics, South Korean President Moon Jae-in will make another big step in peace of the Korean Peninsula by having the first high level summit with North Korean Leader Kim. Moon has already made tremendous progress in denuclearization of North Korea. Also, the May 1 deadline of US 232 steel and aluminum tariff exemption is approaching. And it's so far uncertain on who will get their exemptions made permanent.

As for today, technically, EUR/CHF at 1.2 will be something that every currency trader look at, even if they don't trade it. EUR/JPY will have its focus on 132.10 minor support. GBP/USD and AUD/USD will be pressing key near term support at 1.3965 and 0.7642 respectively. 1.2214 support in EUR will also be watched even though there is still a bit of distance from there.

Japan PMI manufacturing: Stronger yen begins to impact price competitiveness

Japan PMI manufacturing rose to 53.3 in April, up from 53.1 but missed expectation of 53.4. Joe Hayes, Economist at IHS Markit, noted in the release that the survey data depicted a positive backdrop in the Japanese manufacturing sector during April. And the improvements in the headline number was "underpinned by stronger rates of growth in output, new orders and employment." Business confidence also "strengthened". On the other hand, new export orders dropped for the first time since August 2016 as "stronger yen begins to impact price competitiveness". But rise in total new business inflows also indicated "stronger domestic demand".

BoJ Kuroda: Inflation to meet target in fiscal 2019, but risks are skewed to the downside

BoJ Governor Haruhiko Kuroda repeated his usual rhetoric that the central bank "must continue very strong accommodative monetary policy for some time" in order to reach the 2% inflation target. He pointed out that "if you exclude energy items, then inflation rate is only about 0.5 percent." And, there is "still a long way to go to achieve the 2 percent inflation target." Kuroda is still expecting inflation to hit target in fiscal 2019 but "risks are skewed to the downside,"

Moon Jae-in scored another point as North Korea suspected nuclear tests, abolished nuclear site

South Korea announced to stop broadcasting its propaganda along the border with North Korea, as a gesture of goodwill ahead of the highly anticipated Inter-Korean Summit at the border truce village of Panmunjom on Friday.

South Korean President Moon Jae-in has made tremendous progress in solving the Korea crisis by continuously seeking dialogue. The meeting between high level officials of the two countries earlier this year was the turning point. And, the limited, yet successful, joint participation in recent Winter Olympic in the South created a crucial diplomatic window for the relationship.

It's only the third top level summit between the two countries, with the two previous meetings held back in 2000 and 2007. Ahead of the meeting, North Korea has announced to suspend nuclear and missile tests effective immediately. Its northern nuclear test site will also be abolished. And now, a formal end to the Korean War is also on agenda in the meeting between Moon and North Korean leader Kim Jong-un.

Considering that South Korea was in a mess when Moon took office last May. His predecessor was impeached for corruption. The achievements domestically and diplomatically deserved much recognition. And that's a main reason Moon is chosen as the 4th of the World's 50 Great Leaders by Fortune as announced last week.

Looking ahead

Euro has been rather resilient against Dollar and Yen this week. But it will be facing tests from sentiment indicators as well as ECB rate decision and press conference. Eurozone PMIs and German Ifo could add to evidence that Eurozone is slowing down from stellar growth. And more importantly, ECB could continue to sound cautious and noncommittal to ending asset purchase program after September. These would be factors in triggering a downside breakout in EUR/USD.

US and UK GDP will also be closely watched. BoE Governor Mark Carney clearly indicated last week that a May BoE hike is not a certainty. Sterling's selloff could accelerate if Q1 GDP disappoints again. Dollar, on the other hand, will look into Q1 GDP, along with developments in treasury yield, to solidify recent upside momentum.

Other than those events, Australia CPI, New Zealand trade balance will also be watched. BoJ rate decision, on the other hand, will likely be a non-event.

Here are some highlights for the week ahead

- Monday: Eurozone PMIs; Canada wholesale sales; US PMIs, existing home sales

- Tuesday: Japan services PPI; Australia CPI; Swiss trade balance; German Ifo; UK public sector net borrowing; US house price indices, new home sales, consumer confidence

- Wednesday: Japan all industry index

- Thursday: Australia import prices; German Gfk consumer sentiment; UK BBA mortgage approvals, CBI realized sales; ECB rate decision; US durable goods orders, jobless claims, trade balance, wholesale inventories

- Friday: New Zealand trade balance; UK consumer confidence; Japan Tokyo CPI, unemployment rate, industrial production retail sales, housing starts BoJ rate decision; Australia PPI; French GDP, German import price, unemployment; UK GDP; US GDP, employment cost index

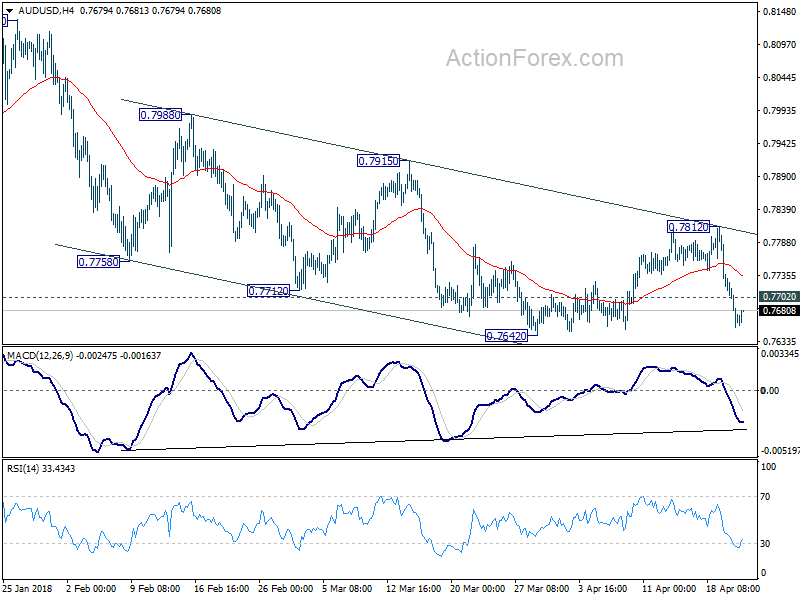

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7639; (P) 0.7685; (R1) 0.7715; More...

AUD/USD recovers mildly today but intraday bias remains on the downside with 0.7702 minor resistance intact. Break of 0.7642 support will resume the whole decline from 0.8135 and target 0.7500 key support level next. Break there will indicate medium term reversal. On the upside, above 0.7702 minor resistance will turn intraday bias neutral and bring consolidations. But recovery should be limited below 0.7812 resistance to bring fall resumption.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | JPY | PMI Manufacturing Apr P | 53.3 | 53.4 | 53.1 | |

| 7:00 | EUR | France Manufacturing PMI Apr P | 53.5 | 53.7 | ||

| 7:00 | EUR | France Services PMI Apr P | 56.5 | 56.9 | ||

| 7:30 | EUR | Germany Manufacturing PMI Apr P | 57.5 | 58.2 | ||

| 7:30 | EUR | Germany Services PMI Apr P | 53.7 | 53.9 | ||

| 8:00 | EUR | Eurozone Manufacturing PMI Apr P | 56.1 | 56.6 | ||

| 8:00 | EUR | Eurozone Services PMI Apr P | 54.6 | 54.9 | ||

| 12:30 | CAD | Wholesale Trade Sales M/M Feb | 0.80% | 0.10% | ||

| 12:30 | USD | Chicago Fed Nat Activity Index Mar | 0.27 | 0.88 | ||

| 13:45 | USD | US Manufacturing PMI Apr P | 55.2 | 55.6 | ||

| 13:45 | USD | US Services PMI Apr P | 54.1 | 54 | ||

| 14:00 | USD | Existing Home Sales Mar | 5.55M | 5.54M |

Market Morning Briefing: Euro Yen Seems To Be Breaking Support

STOCKS

Almost major indices have immediate resistances on the upside and could either remain stable or dip over the next couple of sessions.

Dow (24462.94, -0.82%) came off on Friday but while the index remains above 24250, there could be chances of a rise back to levels near 25000. A break below 24250, if seen could trigger a fall towards 24000 or lower.

Dax (12540.50, -0.21%) is down slightly. As mentioned last week, the resistance near 12600-12650 is important and while that holds, a dip back towards 12400 is possible.

Nikkei (22092.24, -0.32%) rose in the last few sessions as expected but could limit its upside to 22500-22550 levels in the near term. A dip towards 21800 could be seen if the resistance near 22550 holds strong.

Shanghai (3061.28, -0.33%) is stuck in the 3050-3150 region and may remain stable for a few sessions before deciding on further direction. A break below 3050 could open up chances of a fall towards 2900. Watch crucial levels near 3050.

Nifty (10564.05, -0.012%) is stable below 10600. Either the index may remain stable for a few more sessions or come off to test 10450.

COMMODITIES

Brent (73.94) looks poised just now but has some chances of moving higher towards 75-76 which is an important resistance zone. A fall thereafter could be seen targeting 72-71 in the medium term.

Nymex WTI (68.19) also has some scope of moving up towards 69.0-69.5 in the next few sessions before coming off sharply from there.

Gold (1336) came of below 1340 after almost a week and if the price continues to remain below 1340, Gold could be vulnerable to a fall towards 1320-1300 soon.

Copper (3.1485) has weekly resistance near 3.20-3.22 and which if holds could push the prices down again towards 3.10 or lower. The price may trade within 3.22-3.13 region for sometime before a dip towards 3.10 or lower is seen in the longer run.

FOREX

Dollar index (90.372), as per expectation, is now testing resistance on 3 day candles near 90.25-90.50 (earlier mentioned as 90.00-90.25) and also on daily line chart. The 90.5-91.0 zone could be a crucial resistance zone, whose breach could imply a bullish Dollar in the medium term. As per our Apr ’18 Euro report, we currently prefer Dollar bearishness till May/Jun, after which it could turn bullish. Whether the downmove from 103 since Dec ’16 ends immediately, or later in this quarter, would have to be seen.

Euro (1.2276): Against our expectation, Euro broke below support near 1.23 (on daily line chart) to see a low near 1.225. The 1.225-1.215 region is a crucial support zone for the Euro and a break past this zone could imply medium term bearishness. Our Apr ’18 Euro report prefers some bullishness for the Euro till May/Jun and bearishness after that. The upmove from 1.045 since Dec ’16 could start seeing a correction in this quarter.

Dollar Yen (107.80) as expected, has moved up and is now very close to its previous high of 107.78 (also seen as resistance on daily candles). Both possibilities are equally likely now: a breach past 107.8 to target 21 week moving average near 108.88 or a bearish turn (breaking support on daily candles) towards 106.5 and lower.

Euro Yen (132.33) seems to be breaking support on daily candles near current levels and is near resistance on weekly candles, which increases the likelihood of a dip. There is support near 131 on weekly candles which could be tested if Euro dips towards 1.215 while the Dollar Yen stays near 108.

Pound (1.4021) saw 4 consecutive sessions of downmoves last week from 1.4377 towards 1.40 (support on daily candles). It has already broken support on daily line chart near 1.408 and is likely to dip further to test crucial long term support level near 1.38-39 on weekly line chart. If this support also breaks, Pound could turn very bearish in the medium term.

Dollar Rupee (66.125): May test 66.40-50 this week. See some profit-taking from there.

INTEREST RATES

Last week saw US yields rising towards record highs due to improving US economy indicators and rising commodity prices. In the last 2 weeks the following releases had all indicated a growing US economy: Industrial Production, Capacity Utilization, US Retail Sales data, unemployment claims data and the Fed minutes. In addition, Crude’s rise towards 74 has increased inflation expectations and is fuelling the rise in US yields.

US 10 Yr Yield (2.96%), 30 Yr (3.145%), 5 Yr (2.81%), 2 Yr (2.46%):

Repeating Friday's comment, the US 2 year yield has reached its highest levels since 2008 and could rise higher in May. Upside could be restricted to 2.5% in the near term.

The 10 Year yield (2.96%) is has breached resistance near 2.92% on medium term chart. If it doesn’t dip back towards 2.85%-2.825%, it could soon target the psychologically crucial 3% level soon. However, our preference is for the yield to dip soon.

The 30 yr yield as we expected, has moved up further towards 3.15%. We expect it to dip along with the 10 Year yield after testing levels near 3.2%

Moon Jae-in scored another point as North Korea suspended nuclear tests, abolished nuclear site

South Korea announced to stop broadcasting its propaganda along the border with North Korea, as a gesture of goodwill ahead of the highly anticipated Inter-Korean Summit at the border truce village of Panmunjom on Friday.

South Korean President Moon Jae-in has made tremendous progress in solving the Korea crisis by continuously seeking dialogue. The meeting between high level officials of the two countries earlier this year was the turning point. And, the limited, yet successful, joint participation in recent Winter Olympic in the South created a crucial diplomatic window for the relationship.

It's only the third top level summit between the two countries, with the two previous meetings held back in 2000 and 2007. Ahead of the meeting, North Korea has announced to suspend nuclear and missile tests effective immediately. Its northern nuclear test site will also be abolished. And now, a formal end to the Korean War is also on agenda in the meeting between Moon and North Korean leader Kim Jong-un.

Considering that South Korea was in a mess when Moon took office last May. His predecessor was impeached for corruption. The achievements domestically and diplomatically deserved much recognition. And that's a main reason Moon is chosen as the 4th of the World's 50 Greatest Leaders by Fortune as announced last week.

Trader were Largely Bullish on Energy and Precious Metals

Speculators were bullish over the energy complex in the week ended April 17. Net LENGTH for crude oil futures jumped +21 051 contracts from a week ago to 728 131. NET LENGTH of heating oil rose +8 258 contracts to 22 989 while net LENGTH for gasoline gained +4 245 contracts to 75 154. Net SHORT for natural gas decreased -8 976 contracts to 89 297 for the week.

with the exception of platinum, speculators were bullish over the precious metal complex last week. Net LENGTH for gold increased +7 697 contracts to 163 069. Net SHORT for silver slumped -14 746 contracts to 87 for the week. For PGMs, net LENGTH for platinum fell -1 353 contracts to 17 647 while that for palladium added +2 388 contracts to 10 548.

Japan PMI manufacturing: Stronger yen begins to impact price competitiveness

Japan PMI manufacturing rose to 53.3 in April, up from 53.1 but missed expectation of 53.4.

Comments in the release by Joe Hayes, Economist at IHS Markit:

"Survey data depicted a positive backdrop in the Japanese manufacturing sector during April. The improvement in the headline PMI was underpinned by stronger rates of growth in output, new orders and employment. Furthermore, business confidence strengthened, while output prices were hiked to a stronger degree, signalling optimism in demand conditions.

"Although new export orders declined for the first time since August 2016, as the stronger yen begins to impact price competitiveness, the rise in total new business inflows signals stronger domestic demand."

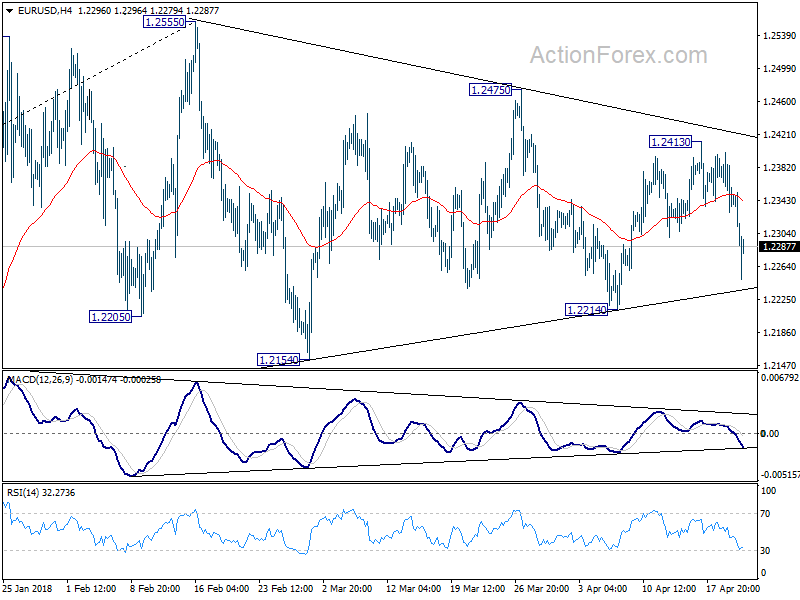

EUR/USD Turned Bearish Below 1.2360

Key Highlights

The Euro failed to move above 1.2420 and declined sharply against the US Dollar.

There was a break below a major bullish trend line with support at 1.2365 on the 4-hours chart of EUR/USD.

The Euro Zone Manufacturing PMI for April 2018 (Prelim) will be released today, which is forecasted to remain at 56.6.

The US Existing Home Sales report for March 2018 (MoM) will be released today, which is forecasted to increase by 1.3%.

EURUSD Technical Analysis

This past week, the Euro made many attempts to break the 1.2400 and 1.2420 resistance levels against the US Dollar. The EUR/USD pair failed to settle above 1.2400, which resulted in a sharp downward move.

During the decline, there was a break below a major bullish trend line with support at 1.2365 on the 4-hours chart. The pair also broke the 50% Fib retracement level of the last wave from the 1.2215 low to 1.2413 high.

Moreover, there was a close below the 100 (red) simple moving average (4-hours) and the 200 (green) simple moving average (4-hours). These are negative signs and suggests that EUR/USD moved into a bearish zone below 1.2360.

On the downside, a close below the 76.4% Fib retracement level of the last wave from the 1.2215 low to 1.2413 high could result in further losses. The next support is near the last swing low of 1.2215, followed by 1.2200.

If the pair corrects higher from the current levels, it may perhaps face resistances near 1.2320, the 100 (red) simple moving average (4-hours) and the 200 (green) simple moving average (4-hours).

Economic Releases to Watch Today

- Germany's Manufacturing PMI for April 2018 (Preliminary) – Forecast 57.6, versus 58.2 previous.

- Germany's Services PMI for April 2018 (Preliminary) – Forecast 53.8, versus 53.9 previous.

- Euro Zone Manufacturing PMI April 2018 (Preliminary) – Forecast 56.6, versus 56.6 previous.

- Euro Zone Services PMI for April 2018 (Preliminary) – Forecast 55.0, versus 54.9 previous.

- US Manufacturing PMI for April 2018 (Preliminary) – Forecast 55.0, versus 55.6 previous.

- US Services PMI for April 2018 (Preliminary) – Forecast 54.0, versus 54.0 previous.

- US Existing Home Sales for March 2018 (MoM) – Forecast +1.3%, versus +3.0% previous.

Oil Prices And US Yields To Dictate The Pace This Week

Oil prices and the US Yields to dictate the pace this week

While geopolitical tensions remain bubbling under the surface, rising oil prices and higher US yields suggest investors are likely to deal with increased volatility as a broad range of political, economic and financial events unfolds

US Core PCE, GDP price index, personal consumption data are expected to set the tone this week. Nevertheless, politics will stay on the radar, as we should be in for a plethora of opinions during the build-up to the USA historical meeting with North Korea in May, even more so with North Korea announcing they are suspending missile and nuclear tests.

While everyone will be keying on the PCE, don’t overlook Fridays advance Q1 real GDP report which will cornerstone near-term expectations for growth and could be the most impactful data of the week.

Three central banks: the ECB, the BoJ and the Riksbank take to the stage, but all three are expected to remain on hold. The markets are now of the view global central banks l will kick the policy can further down the road in an attempt to stall for more time to access the global fallout worsening economic data – the press conferences should be reasonably quiet.

The recent downturn in global economic data is suggesting we are moving from a state of global synchronised growth to a synchronised slowdown. Partially explaining why global central bankers are applying a heavy coat of dovish wax to their policy guidance these days.

Oil Markets

Traders will be intently monitoring rumours suggesting an attempted coup was underway in Saudi Arabia. Any hint of a coup will add a considerable element of uncertainty in the region, as the Riyadh is currently dealing with a threat of Yemeni rebels so any indication of destabilisation within the areas top exporter should send risk premiums through the roof and oil prices surging higher.But it appears yesterday Palace rukus was much ado about nothing as it was later confirmed an unauthorised drone was shot down over the Royal Palace in Riyadh. With Yemen tension running high, Saudia Arabia will act vigilantly in these situations as Shiite rebels and their allies in Yemen have been known to use drones against the Saudi -led coalition in the past.

Post Jeddah oil meetings, OPEC and Russia compliance remains high and solidly committed to reigning in oversupply which should continue to support prices. But involuntary supply cut’s and production outages in Venezuela will also continue to support even more so after the falls in US inventories last week. Moreover, all the while Oil Traders are playing the waiting game for probably oil sanctions against Iran, which could push oil prices up as much as $3-7 per barrel. Also, factor in last weeks Saudi jawboning targetting $80 or $ 100 per barrel it suggests prices will remain firm for the foreseeable future and should continue to gravitate higher.

While Oil traders docket is obviously full this week with tangible narratives, but none the less after getting caught off guard after President Trump tweeted that he found OPEC driving up prices artificially was unacceptable they will be keeping a closer eye on the Presidents twitter account. While not clear what type of reprisal the administration could take, it has traders again looking over their shoulder for more Whitehouse bluster.

Oil Prices and Yield Curve

Besides rising oil prices and the inflationary impact on the US yield curve, the Bond market sell-off is as much a factor of supply concerns at this stage, so even with yields moving higher if auction cover ratios remain tepid, it should not be USD supportive. None the less high US yields will have negative implications for on EM currencies especially if the higher US yields continue to provide a fillip to the USD. We could see a break in Oil prices traditional slightly negative correlation with the USD in this environment.

Gold Markets

Rising US Bond Yields and a firming US dollar will present the most obvious risk for Gold this week. With little to no stirring on the geopolitical front and trade tensions abating, Gold may lose its lustre near term, and we could see a further culling of long positions on dwindling appetite, more so if the USD extends last week bullish momentum.

Currency Markets

An unusual amount of USD housekeeping taking place on a very “squeezy” Friday as several supportive dollar themes start to take shape which should influence trading decisions this week. A big selloff in global fixed income has provided the USD with a solid foundation.

Higher US yields have played a role in supporting the USD as surging oil prices make for a compelling inflationary storyline.

With both the BoE and BoC waxing dovish, the markets are betting that ECB will kick the policy can further down the road in an attempt to stall for more time stall for more time – the press conferences should be reasonably quite also.

There has been a reduction in the Trump USD dollar risk premium after Deputy Attorney General Rod Rosenstein told President Donald Trump last week that he is not a target of any part of Special Counsel Robert Mueller’s investigation or the probe into his long-time lawyer, Michael Cohen, according to several people familiar with the matter.

The improving geopolitical landscape in Korea and no further escalation in Syria has removed some geopolitical risk premia from the Dollar.

There been increasing maker chatter about an economic slowdown in China which is being viewed USD positive on the surface as Chinese authorities may shift towards weaker yuan policy to buffer the negative growth( Q2 GDP) impact from deleveraging and trade wars with the US.

G-10

The Euro

Softer EU economic data and with the ECB likely to kick the can down the road on the policy front, the Euro prints below 1.2300. While a reasonably significant sell-off, it was in line with the broader USD rally last week.

The British Pound

What a difference a week makes and how things can turn entirely upside down in FX markets in a mere 48 hours. With GBP extended long positions running at the highest in several years, GBP bulls were dealt a blow by soggy data Wage Inflation, UK CPI but the coup de gras was another bout of Carney Carnage as the BOE chief flip-flopped on policy once again. At 1.40 positioning feels much more balanced so traders will be taking their cue from Brexit: Specifically, the House of Commons, where a cross-party selection of MPs is trying to force a meaningful debate and vote on the delicate subject of the UK’s future relationship with the EU customs union.

The Japanese Yen

We could have a busy week on the Yen post as the markets continue to focus on US yields, but the popularity of Japanese Prime Minister Abe is expected to weigh on investor sentiment.

EM ASIA FX

The Malaysian Ringgit

Despite surging energy prices, the USDMYR has remained mired in a very tight trading range as traders are dealing with some shifting narratives. Higher oil prices usually play favourably for the Ringgit, but with US 10 year yields approaching 3 % and a broadly firmer US dollar, local note dealers are waiting for more favourable levels to by the Ringgit. So with the market not shifting attention from trade and geopolitical angst to higher US yields MYR sentiment will remain weak over the short term, especially when factoring in the election risk premium, as slight as that may be.

Over the longer term, however, medium-term macro conditions and low domestic inflation should make MGS attractive and support the Ringgit over time.

North Korea

We have run the gamut when it comes to North Korea headlines this year, from WW3 to flat out pessimism to cautious optimism and a now outright disbelief that North Korea will suspend nuclear and missile testing.

This fantastic development should set an enjoyable tone for the Trump -Kim peace treaty summit. However, it only clears the lowest barrier, as President Trump will loosen the screws when there is a clear-cut Nuclear Non-Proliferation and Disarmament Policy agreement on the table along with international access to the nuclear facilities to ensure full compliance.

However, make no mistake; this is a cooperative effort between Japan, South Korea, China and USA. With this economic weight, never mind military might staring you down. I suspect Kim Jong Un sees the writing on the wall and is ready to play ball.

It should be viewed very positively as geopolitical risk is the main reason why Korean markets (equity) trade at a discount relative to the regional exporter powerhouses. One thing we need to be cognizant however the other side of this trade, the USD is. For the past year, the Trump Risk Premium has weighed down the beleaguered USD. So better news in North Korea has not only removed some of the geopolitical risk premia from the dollar but also has lowered the Trump risk premium on the dollar. Moreover, probably one of the leading reason the USD got stronger towards the end of the last week.

However, the door is wide open to adding some KRW risk on this preliminary step for North Korea to move away from a more military driven economy and will hopefully make the shift to a more free market economy. Although these are baby steps, it could lead North Korea to open up its economy, which will be extremely positive for the Kospi given the immense opportunity for telcos and utilities in the North.

Trade war uncertainty and tech sector woes are keeping KRW positions light, however, but indeed, the reduction in Korean Peninsula tensions will provide a longer-term boost to the Korean markets.

Trade War Front

Definite overtone continues to be expressed by the US administration with US Treasury Secretary Mnunchin leading the weekend news parade as backroom negotiations continue, stating ” the US remains cautiously optimistic we can reach an agreement.”

Eco Data 4/23/18

[php_everywhere instance="1"]

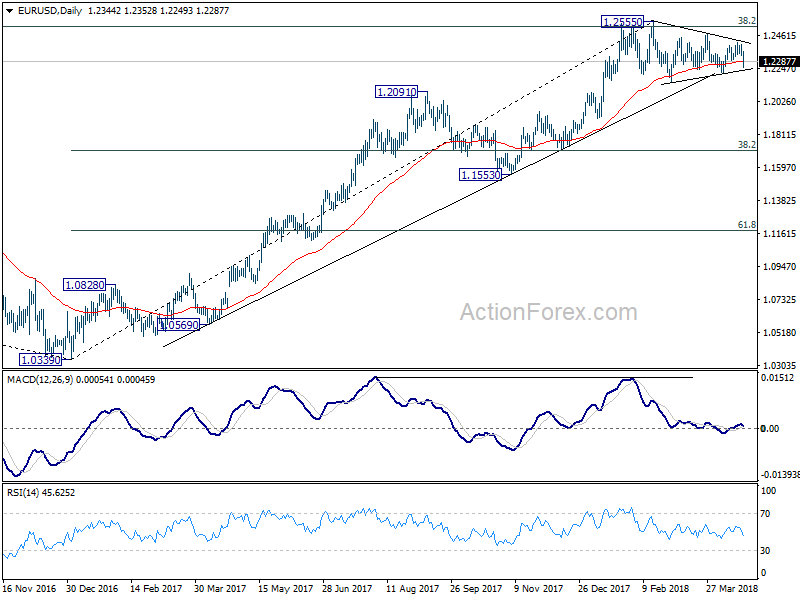

EUR/USD Weekly Outlook

EUR/USD edged higher to 1.2413 last week but reversed well ahead of near term falling trend line. Initial bias is now on 1.2214 support his week. Decisive break there will revive the case of medium term reversal. In that case, deeper fall would be seen to 1.2154 first. Firm break there will confirm and target 38.2% retracement of 1.0339 to 1.2555 at 1.1708 next. On the upside, break of 1.2413 will turn focus back to 1.2555 high.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

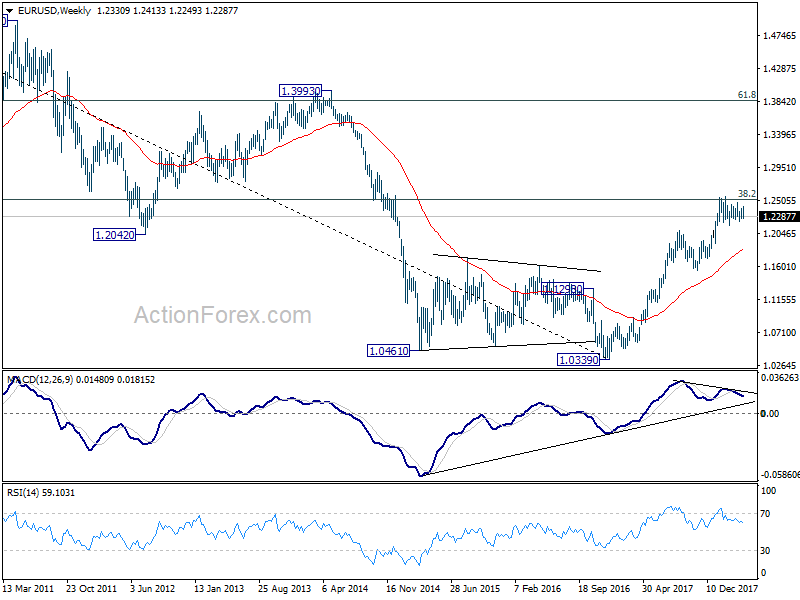

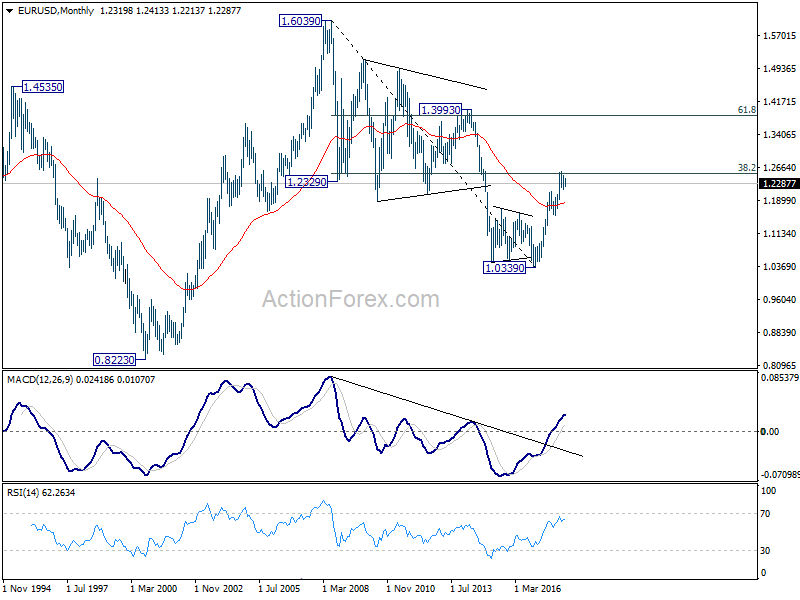

In the long term picture, 1.0339 is seen as an important bottom as the down trend from 1.6039 (2008 high) could have completed. It's still early to decide whether price action from 1.0339 is developing into a corrective or impulsive pattern. Reaction to 38.2% retracement of 1.6039 to 1.0339 at 1.2516 will give important clue to the underlying momentum.

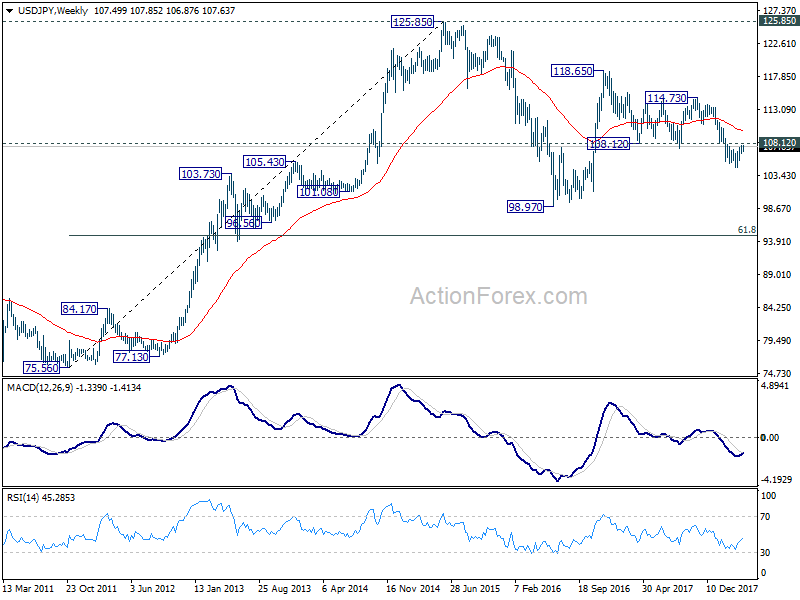

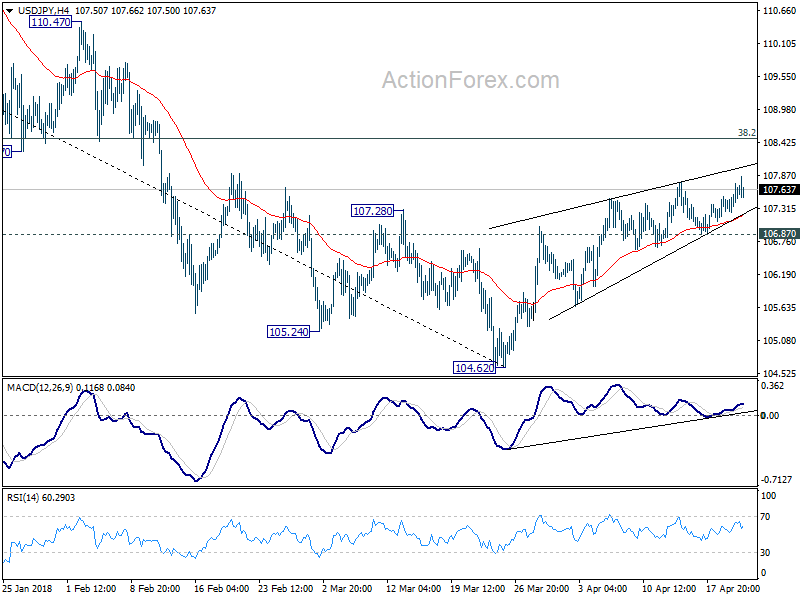

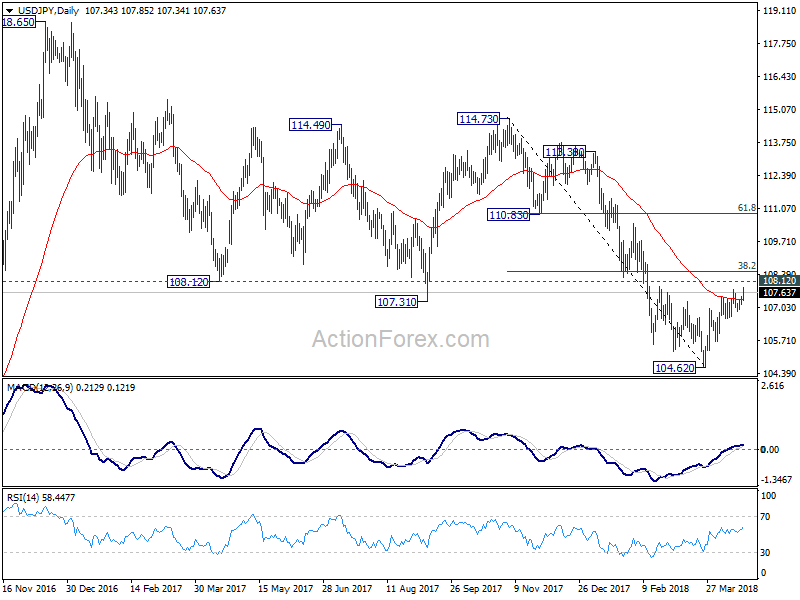

USD/JPY Weekly Outlook

USD/JPY's rebound from 104.62 extended last week with very weak upside momentum. Further rise could be seen this week to 38.2% retracement of 114.73 to 104.62 at 108.48 9 which is close to 108.12. This resistance zone will be crucial in determining the medium outlook. On the downside, break of 106.64, however, will indicate the rebound from 104.62 has completed. And in that case, bias will be turned back to the downside for retesting 104.62.

In the bigger picture, as long as 108.12 support turned resistance holds, the medium term down trend from 118.65 (2016 high) should still continue lower, at least to retest 98.97 (2016 low). However, sustained break of 108.12 will be an early sign of medium term reversal. In that case, further rise would be seen to 114.73 resistance to confirm completion of the fall from 118.65.

In the long term picture, the rise from 75.56 (2011 low) long term bottom to 125.85 top is viewed as an impulsive move, no change in this view. Price actions from 125.85 are seen as a corrective move which could still extend. In case of deeper fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77. Up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.