Sample Category Title

It’s Number 3 Again!

Number 3 has been of crucial significance in 2018. Trump has been predicting that his policies would bring an increase in annual growth to over than 3% a year. The Federal Reserve is expected to raise interest rates 3 times in 2018. However, investors and traders are most concerned about U.S. 10-year Treasury Yields breaking 3%. At the time of writing U.S. 10-year yields are less than 3 basis points to breaching the 3%, a level it hasn't topped since 2014, so what happens when this level is breached?

Looking back on February, when interest rates started rising along with concerns over trade tensions, U.S. equities fell sharply with all major U.S. indices entering a correction territory. Higher interest rates mean higher borrowing cost for corporates, and another sharp spike would eat away a significant element of their profitability by increasing interest expense. Investors will also readjust their required cost of capital as risk-free rates rise, which could make equities less attractive. Many consumers will find their disposable income fall, as they have to pay more for their mortgages. So, unless the growth in the economy, wages, and companies' profitability offsets the rise in interest rates, there may be bad times ahead, especially for equities.

Dollar bulls were the most excited by the rallying yields as they found it to be an excellent opportunity to take long positions. The DXY stood at two weeks high early Monday trading above 90.40. Bulls are probably awaiting confirmation from the bond markets before considering their next move, where a break above 3% could encourage more investors to join the long trade.

Oil prices are another thing to keep an eye on. President Trump last week accused OPEC of keeping oil prices artificially high. His intervention came after reports on Wednesday showed that Saudi Arabia would be happy to see crude rise to $80 or even $100 a barrel, a sign that OPEC and friends will not alter the supply cut deal anytime soon. Although Trump's tweet may have encouraged profit taking, it will not have a long-lasting effect. What OPEC should be worried about is how higher oil prices will impact inflation and thus, interest rates. Although inflation is what many economies are lacking at the moment, a steep rise in prices would add further pressure on global economy which is already showing signs of weakness. That's what could put a ceiling on oil prices.

Today's release of Flash Manufacturing and Service PMIs from France and Germany could remind some that Europe has lost momentum in 2018. ECB's President, Mario Draghi warned on Friday that Eurozone growth cycle may have peaked, so any signs of further slowdown will likely delay any plans for tightening. That's why I do not expect any policy change when the ECB meets on Thursday, not even a sign of the end of quantitative easing, which is likely to add some pressure on the Euro.

Currencies: Dollar Profits From Higher Yields, At Least For Now

Rates: US Treasuries remain under pressure, Bunds temporary saved by ECB?

The US 10-yr yield reached a new 2018 high, paving the way for a move towards key resistance at 3.05%/3.08%. The new upleg in European yields could be hampered by the ECB meeting. Today's PMI's could confirm Draghi's view that the European growth cycle might have peaked even if momentum remains strong.

Currencies: Dollar profits from higher yields, at least for now

The USD rebound accelerated on Friday. Core bond yields rose across the board, but the dollar profited more than the euro. FX traders will keep an eye at the EMU PMI's today. Markets might prepare for a rather soft tone at Thursday's ECB meeting. At the same time, the USD enjoys a constructive flow. The post-Carney correction of sterling might slow

The Sunrise Headlines

- US stock markets ended the final trading session of last week 0.85% to 1.3% lower with Nasdaq again underperforming. Asian risk sentiment is more mixed this morning with China slightly lagging behind.

- ECB policy makers see scope to wait until their July meeting to announce how they'll end their bond-buying program, according to euro-area officials familiar with the matter (Bloomberg).

- President Trump will urge North Korea to act quickly to dismantle its nuclear arsenal when he meets Kim Jong Un and isn't willing to grant substantial sanctions relief in return for a freeze of its nuclear tests, officials said. (WSJ)

- Brussels plans to shift tens of billions in EU funding away for central and eastern Europe, diverting money from countries such as Poland and Hungary to those hit hard by the financial crisis such as Spain and Greece. (FT)

- ECB President Draghi said that the EMU growth momentum is expected to continue, but warned that the latest economic indicators suggest that the growth cycle may have peaked.

- US Treasury Secretary Mnuchin said he may travel to China, a move that could ease tensions between the two countries, as international policymakers acknowledged Beijing needs to change its trade practices. (Reuters).

- Today's eco calendar contains EMU April PMI's and US existing home sales. Belgium taps the bond market and ECB Coeuré speaks in Frankfurt

Currencies: Dollar Profits From Higher Yields, At Least For Now

Dollar profits from higher yields, at least for now.

On Friday, the USD rebound accelerated. Interest rates/interest rate differentials weren't the only driver behind rise of the US currency. However, US yields nearing key levels (e.g. 3% for the US 10-y yield) probably added to the USD positive sentiment. EUR/USD dropped below the 1.23 mark and closed the session at 1.2288. USD/JPY trended higher in the 107 big figure even as US equities came under pressure. The pair finished the day at 107.66.

Overnight, Asian equities are trading mixed. However, the regional equity performance is not too bad given to losses in the US on Friday. US yields continue drifting higher. The (trade weighted) dollar is moving toward the top of this year's consolidation pattern. USD/JPY (107.80 area) is gaining a few ticks. EUR/USD hovers in the 1.2275 area.

Today, the US PMI's and existing home sales will be published. Markets will also keep a close eye at the first estimate of the April EMU PMI's. The EMU composite PMI dropped substantially in February and March. A further easing from 55.2 to 54.8 is expected. We see a chance of the deceleration in the PMI/growth momentum to ease. However, a new negative surprise might weigh on the euro. At the IMF meeting, ECB's Draghi said that the EMU growth cycle might have peaked, but at the same time that confidence in the inflation outlook increased. Still markets might prepare for a rather soft ECB at Thursday's policy meeting. So, the news flow might be mixed for the euro while the dollar is holding a positive ST momentum. EUR/USD 1.2215 is first support ahead of the key 1.2155 area. We see a good chance of EUR/USD testing thiss range bottom as US yields are keeping an upward bias. On Friday, sterling was looking for a new equilibrium as the repositioning after Thursday's soft comments from BoE governor Carney petered out. EUR/GBP reversed an early up-tick and settled in the mid 0.87 area. BoE Sauders in a speech indicated that further gradually policy normalization might continue. There are no important eco data in the UK today. EUR/GBP 0.88 is a first relevant resistance area. We look out whether last week's post-Carney correction has run its course. Some relative euro softness might also hamper the EUR/GBP topside.

USD (trade weighted): nearing 90.50/91 range top area

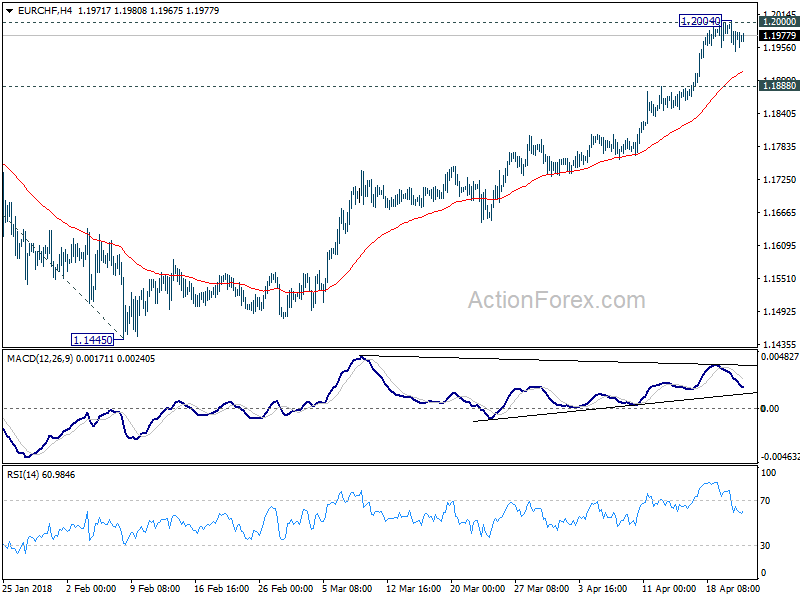

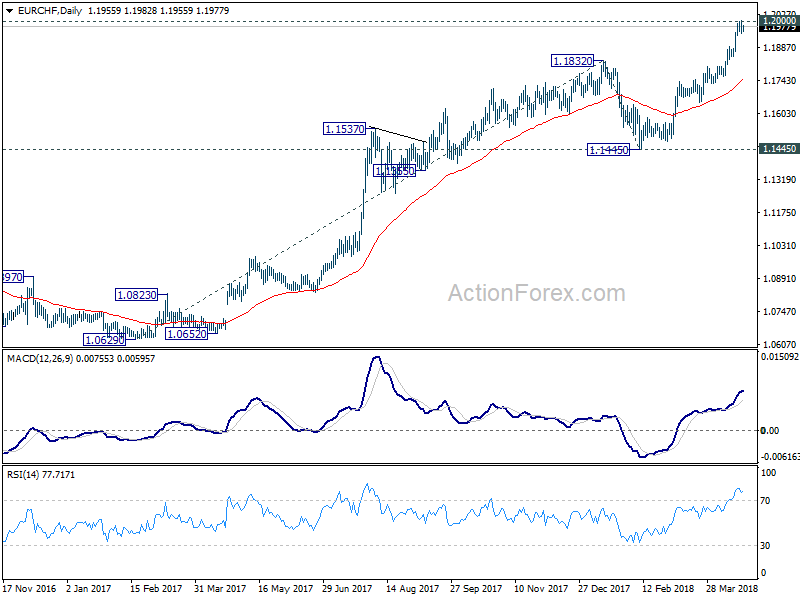

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1948; (P) 1.1976; (R1) 1.2004; More...

Intraday bias in EUR/CHF stays neutral with focus on 1.2 key resistance. Further rally is expected as long as 1.1888 minor support holds. Firm break of 1.2 will pave the way to 61.8% projection of 1.0629 to 1.1832 from 1.1445 at 1.2188. However, consider bearish divergence condition in 4 hour MACD, break of 1.1888 will indicate short term topping. In that case, deeper pull back would be seen back to 1.1445/1832 support zone.

In the bigger picture, long term up trend in EUR/CHF is still in progress. Prior SNB imposed floor at 1.2003 was already met but there is no sign of reversal yet. As long as 1.1445 support holds, we'd expect the up trend to extend to 2013 high at 1.2649 next.

Equities Cautious Despite N. Korea Stopping Nuclear Program

General Trend:

- Asian equity markets trade cautiously after pledge by North Korea, rise in interest rates

- US equity futures pare opening gains

- Banks rise with increase in 10-yr yields

- China Unicom rises over 3% after reporting Q1 results

- Display companies decline after Apple dropped over 4% on Friday

- Chinese tech companies Lenovo and BoE Technology decline amid US sanction concerns

- Asia 10-yr bond yields track rise in US interest rates

- Japan Chief Cabinet Sec commented on declining poll numbers

- Australia Q1 CPI data due on Tuesday’s session, trimmed mean (CPI) expected to remain below RBA’s 2-3% target

- North Korea/South Korea summit expected to begin on Friday

- Bank of Japan (BoJ) to hold policy meeting on April 26-27th (Thursday-Friday)

Headlines/Economic Data

Japan

- Nikkei 225 opened flat; closed -0.3%

- TOPIX Electric Appliances index -0.4%; Iron & Steel index +1.1%, Securities +0.7%

- Megabanks rise over 1%

- (JP) Japan PM Abe cabinet approval rating falls 3pts to 39% - Yomiuri; Mainichi poll falls 3pts to 30%; ANN poll falls to 29% (lowest level since 2012)

- (JP) Japan Chief Cabinet Sec Suga: Approval ratings show Abe government is under scrutiny from people

- (JP) Thus far in April, the BoJ has purchased equity ETFs only 1 time when the Topix declined more than 0.2% during morning trading – Japanese Press

- (JP) Japan Apr Prelim PMI Manufacturing: 53.3 v 53.1 prior

- (JP) BOJ Gov Kuroda: Japan needs strong accommodative monetary policy for some time; reiterates long way to 2% inflation target

- Toshiba, 6502.JP Denies reports it will cancel sale of chip unit if China doesn't approve it

Korea

- Kospi opened -0.1%

- (KR) North Korea announces it will stop nuclear and ICBM testing effective April 21st, and will begin to dismantle a nuclear testing site in the northern part of the country – press (over the weekend)

- (KR) Korean press looks at North Korea's decision to end nuclear testing; noting Kim needed to make the announcement in order to justify talks with the US to the North Korean people

- (KR) North Korea leader Kim has accepted US inspection of nuclear test site - Korean press

- (KR) According to KITA, South Korean washer exports to the United States -45.4% y/y after US implemented restrictions - Korean press

- (KR) South Korea Fin Min Kim and US Mnuchin agreed on side lines of G20 to strengthen their policy coordination - Korean press

- (KR) Bank of Korea (BoK) Gov Lee conducting research on adding employment to mandate – US financial press

- (KR) South Korea Apr 1-20 Exports y/y: +8.3% v 9.3% prior; Imports y/y: +20.8% v 5.8% prior

- (KR) Bank of Korea (BOK) sells 1-yr monetary stabilization bonds (MSB), avg yield 1.89%

- (KR) South Korea sells KRW800B in 20-yr bonds, avg yield 2.74%

- (KR) South Korea Central Bank sells KRW1.0T v KRW 1.0T indicated in 3-month Monetary Stabilization; Yield: 1.57% v 1.58% prior Bonds (MSB)

China/Hong Kong

- Hang Seng opened -0.3%, Shanghai Composite -0.3%

- Hang Seng Industrial Goods index -1.4%, Info Tech -1.3%, Energy -1.1%, Utilities -0.7%, Consumer Goods -0.9%, Property/Construction -0.8%; Financials +0.2%

- (CN) PBOC Gov Yi Gang: China's financial sector has remained sound with risks "broadly contained" – Xinhua

- (CN) China MOFCOM: China has received information that the US Treasury Sec Mnuchin wishes to make a trip to China to negotiate economic and trade issues - Xinhua

- (CN) US Treasury Sec Mnuchin: continuing dialogue with China on trade; cautiously optimistic we can reach an agreement; Considering a trip to China

- (CN) China PBoC sets yuan reference rate at 6.3034 v 6.2897 prior

- (CN) China PBoC Open Market Operation (OMO): Injects CNY80B in 7-day reverse repos v skips prior; Net: injects CNY0B

- HK$ rises to 7.8433 (1-month high)

- (CN) Analysts discuss PBOC RRR targeted rate cut last week, noting it is a move to target shadow banking – press

- (CN) There is CNY520B expected to mature this week related to PBoC monetary policy tools – US financial press

- (CN) China Foreign Ministry: Notes 'major' transportation accident in North Korea involving Chinese tourists, sees 'large' number of casualties

- (HK) Hong Kong 1-month HK$ HIBOR 1.04714% (highest level since Jan 4th)

Australia/New Zealand

- ASX 200 opened flat

- ASX 200 Financials index +0.8%, Resources +0.6%; Energy -0.6%, Utilities -0.7%

- Macquarie Infrastructure , MIG.AU Group of US based shareholders calling for the board to be sacked and company liquidated - AFR

- iSelect [-52%], ISU.AU Cuts FY18 (A$) Underlying EBIT 8.0-12.0M (guided 26-29M prior); Names Brodie Arnhold as acting-CEO, replacing Scott Wilson

- (AU) Australia buys back A$500M v A$500M indicated in Oct 2019 and April 2020 bonds

- (AU) Australia sells A$500M v A$500M indicated in 3.25% April 2029 bonds, avg yield 2.8843% v 2.6337% prior, bid to cover 5.88x v 3.47x prior

North America

- (US) US 10 year Treasury yield hits 2.968%, highest since Jan 2014

- Tencent, 700.HK There is renewed speculation that Music Entertainment unit is planning a US IPO in H2 2018 - US financial press

Other Asia

- (ID) Bank of Indonesia Dep Gov Waluyo: Reiterates central bank will be in market to maintain stability of Rupiah currency (IDR)

- (PH) Philippines Central Bank (BSP) Gov Espenilla: Premature to sat there is a trade war

Europe

- (MX) Mexico sign free trade agreement (FTA) with EU over the weekend, expanding prior agreement to cover finance, e-commerce and agriculture (prior was only basic goods and machinery)

- (EU) ECB said to have no plans to slow normalization plans despite recently slower data - financial press

- Deutsche Bank, DBK.DE HNA Group cuts stake to 7.9% (prior 8.8%)

- EU said to be considering a deeper cartel investigation into Daimler, BMW and VW - German press

Levels as of 02:00ET

- Hang Seng -0.4%; Shanghai Composite -0.4%; Kospi -0.2%; ASX 200 +0.4%

- Equity Futures: S&P500 +0.3%; Nasdaq100 +0.3%, Dax +0.3%; FTSE100 +0.1%

- EUR 1.2288-1.2265; JPY 107.89-107.61; AUD 0.7682-0.7658;NZD 0.7218-0.7199

- Jun Gold -0.1% at $1,336/oz; Jun Crude Oil -0.1% at $68.36/brl; May Copper +0.5% at $3.15/lb

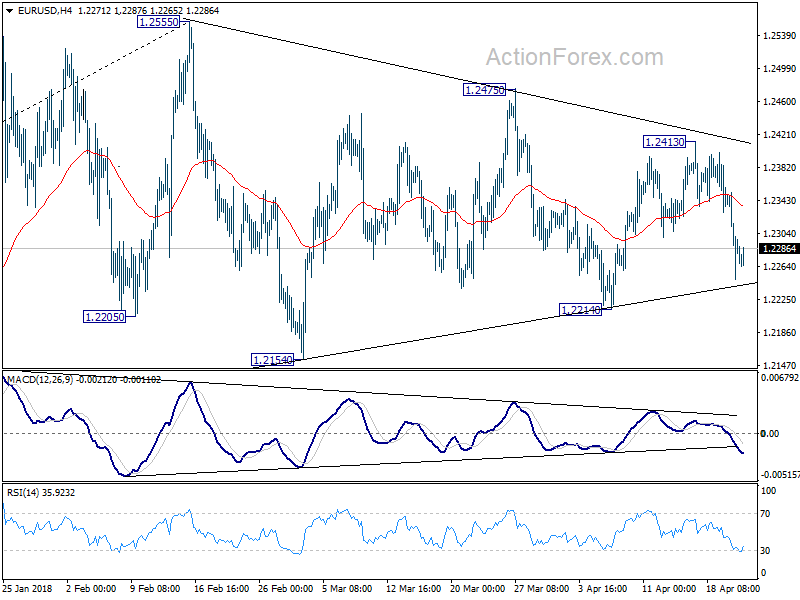

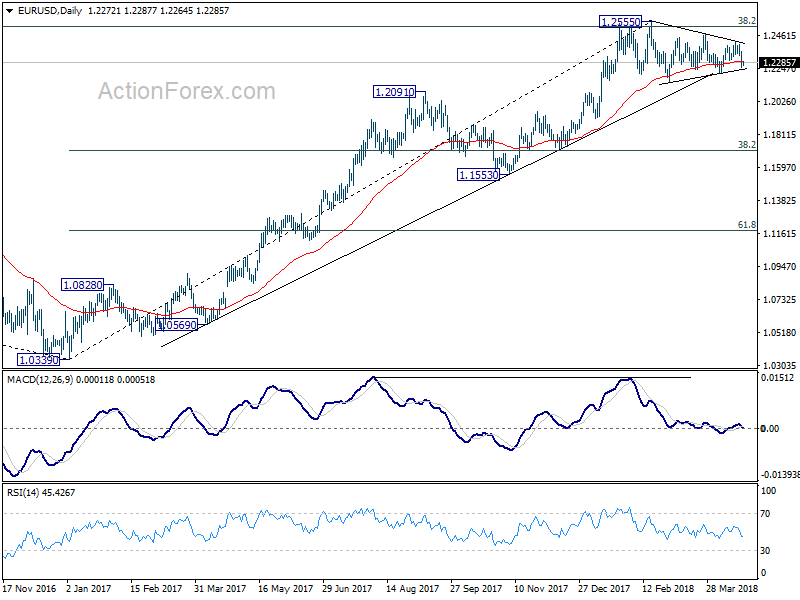

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2239; (P) 1.2296 (R1) 1.2342; More....

Focus remains on 1.2214 support in EUR/USD. Decisive break there will revive the case of medium term reversal. In that case, deeper fall would be seen to 1.2154 first. Firm break there will confirm and target 38.2% retracement of 1.0339 to 1.2555 at 1.1708 next. On the upside, break of 1.2413 will turn focus back to 1.2555 high instead.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

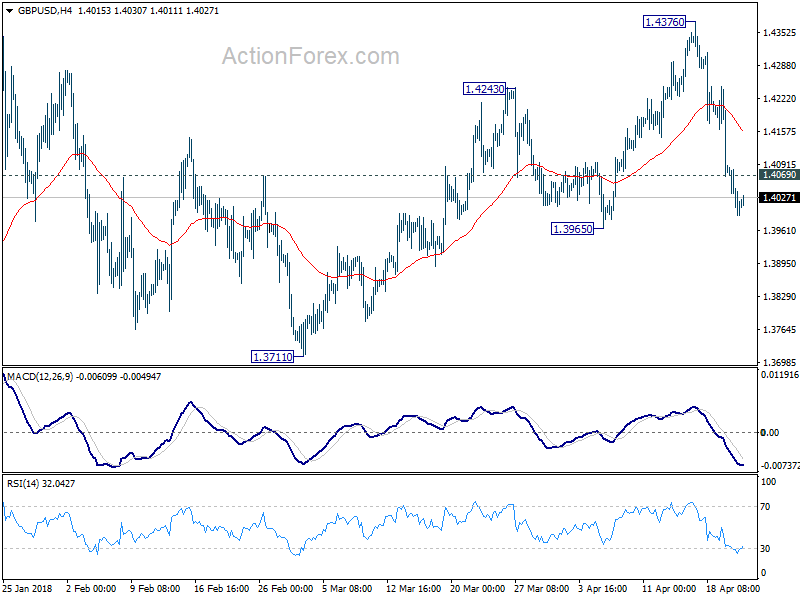

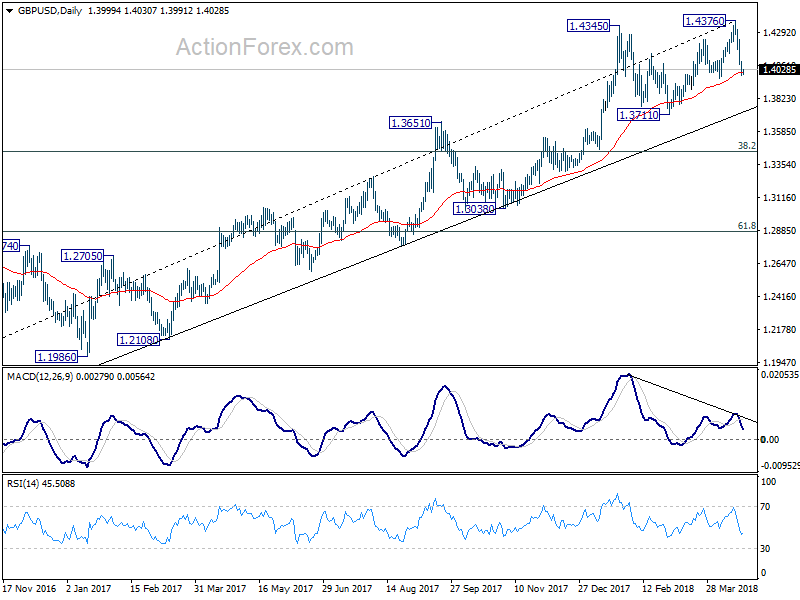

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3968; (P) 1.4029; (R1) 1.4060; More...

GBP/USD recovers mildly but with 1.4069 minor resistance intact, intraday bias stays on the downside for 1.3965 support. Break there will pave the way to 1.3711 key support level. On the upside, above 1.4069 minor resistance will turn intraday bias neutral and bring consolidations. But for now, near term risk will stay on the downside as long as 4 hour 55 EMA (now at 1.4157 holds).

In the bigger picture, bearish divergence condition in daily MACD is raising the chance of medium term reversal. Also, note that GBP/USD has just failed to sustain above 55 month EMA (now at 1.4257). Focus is back on 1.3711 support. Firm break there will confirm medium term reversal and target 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 first. Break will target 61.8% retracement at 1.2874 and below. For now, sustained break of 55 month EMA is needed to confirm medium term upside momentum. Otherwise, we won't turn bullish even in case of strong rebound.

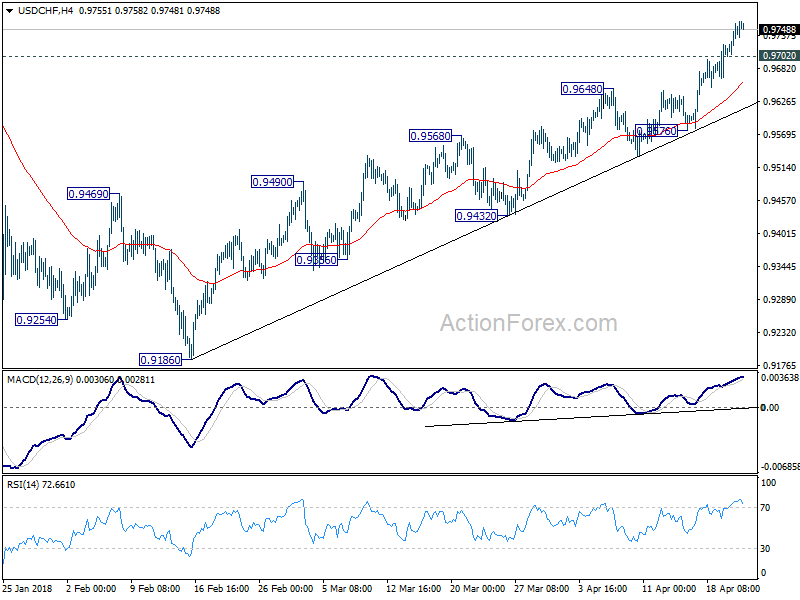

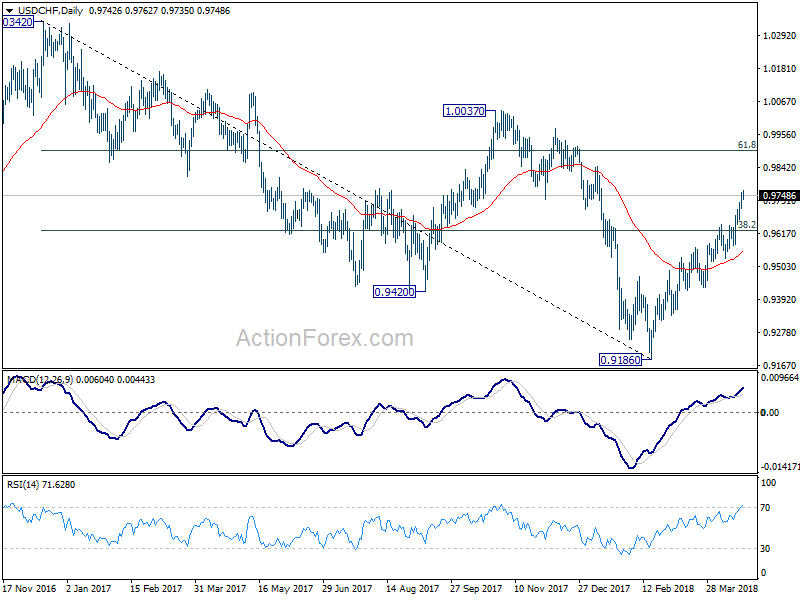

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9711; (P) 0.9735; (R1) 0.9770; More...

Intraday bias in USD/CHF remains on the upside for the moment. Current rise from 0.9186 should target 0.9900 fibonacci level next. On the downside, below 0.9702 minor support will turn bias neutral and bring consolidations. But outlook will stay bullish as long as 0.9576 support holds.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next. This will now be the preferred case as long as 0.9576 support holds.

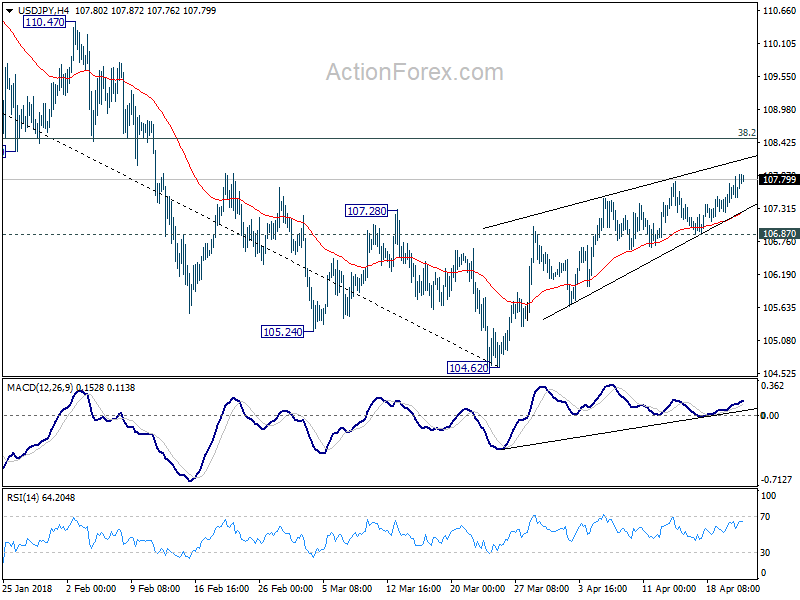

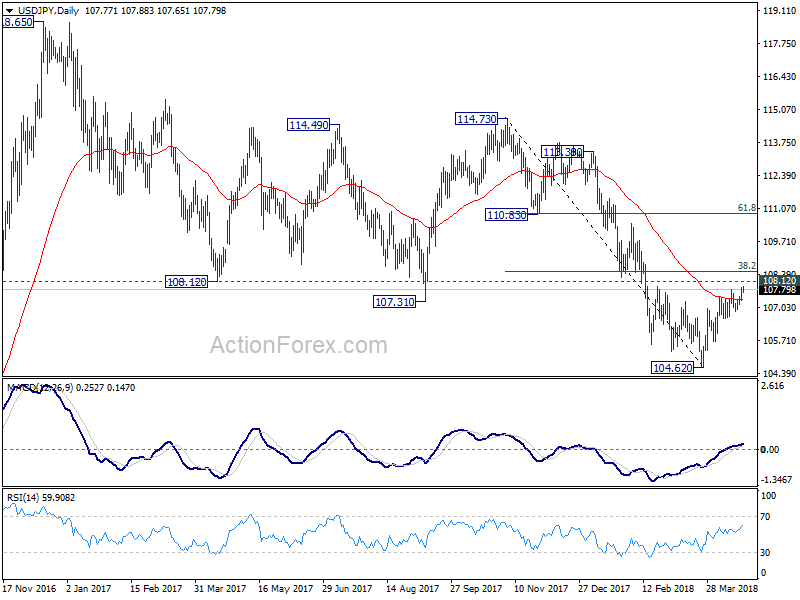

USD/JPY Daily Outlook

Daily Pivots: (S1) 107.36; (P) 107.61; (R1) 107.86; More...

Intraday bias in USD/JPY remains on the upside and rebound from 104.62 is extending to 38.2% retracement of 114.73 to 104.62 at 108.48 9 which is close to 108.12. This resistance zone will be crucial in determining the medium outlook. On the downside, break of 106.64, however, will indicate the rebound from 104.62 has completed. And in that case, bias will be turned back to the downside for retesting 104.62.

In the bigger picture, as long as 108.12 support turned resistance holds, the medium term down trend from 118.65 (2016 high) should still continue lower, at least to retest 98.97 (2016 low). However, sustained break of 108.12 will be an early sign of medium term reversal. In that case, further rise would be seen to 114.73 resistance to confirm completion of the fall from 118.65.

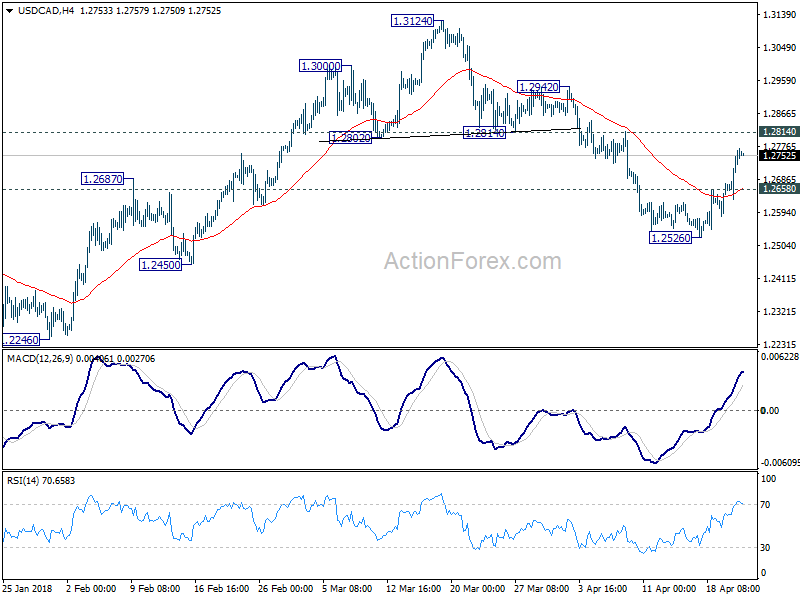

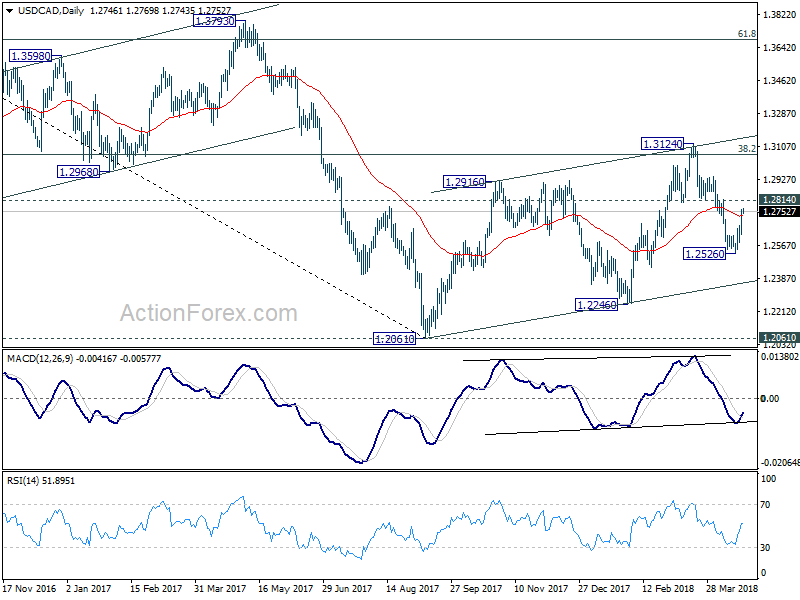

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2673; (P) 1.2718; (R1) 1.2806; More....

Intraday bias in USD/CAD remains on the upside for further rebound. However, we're holding on to the view that rebound from 1.2061 has completed with three waves up to 1.3124. Hence, we'd expect strong resistance below 1.2814 support turned resistance to limit upside and bring another fall. On the downside, below 1.2658 minor support will turn bias back to the downside for 1.2526. However, firm break of 1.2814 will invalidate our view and bring stronger rally to retest 1.3124 instead.

In the bigger picture, for now, we're slightly favoring the view that rise from 1.2061 is a corrective three wave pattern that's completed at 1.3124, after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. And, fall from 1.3124 is resuming larger down trend from 1.4689 (2015 high). However, break of 1.3124 will revive the case of bullish reversal. That is, the down trend from 1.4689 has completed at 1.2061 already.

Asian Stock Markets Are Trading On A Mixed Note This Morning

Market movers today

We start out the week with a lot of preliminary activity indicators for April, before attention later this week turns to the ECB meeting on Thursday as well as the US preliminary GDP numbers for Q1.

In the euro area, the PMI figures will be released today. Manufacturing PMI declined throughout Q1 18, from 60.6 in December 2017 to 56.6 in March 2018. We believe a further decline to 55.5 is pending for April. Several survey indicators have pointed to lower optimism, fear of a trade war and the euro appreciation last year is starting to show its impact on activity. Similarly, Service PMI declined to 54.9 in March since peaking at 58.0 in January. We believe Service PMI is set for a further decline to 54.3 in April.

In the US, Markit PMIs are due for release on Monday. Empire regional PMIs fell in March which points to a slowdown in manufacturing sector. The gap between ISM and Markit PMI manufacturing remains a mystery, although we consider ISM to have come in at a too high level. We believe both indices will fall over the coming months. Markit service PMI fell in February but we estimate it increased slight ly in March from 54 up to 55.

Selected market news

Asian stock markets are trading on a mixed note this morning. In Japan, the manufacturing PMI rebounded slightly to 53.3 after declining in Q1 as the Japanese manufacturing sector has shown some weakness recently as a stronger yen has weighed on exporters.

On Friday, North Korean leader Kim Jong-un pledged to suspend further missile and nuclear testing ahead of a summit between North and South Korea at the end of April , which is likely to be followed by a meeting between US President Trump and the North Korean leader in June. President Trump initially hailed the North Korean pledge to suspend its missile tes ing as ‘big progress' but tempered his enthusiasm yesterday, re-inject ing a note of caution.

Over the weekend, the IMF communique pointed to global leaders expressing concerns about the high level of debt globally and trade frictions . At the meetings, the US came under criticism from other member countries for its latest trade measures. However, US finance Minister Steven Mnuchin hit back, calling for the IMF to step up efforts to reduce global imbalances, in particular surplus countries like Germnay and China. Furthermore, Mnuchin revealed that he is planning to visit China in the near term to discuss trade and other economic issues.