Sample Category Title

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2273

The overall bias is still bearish, with a risk of another dip to 1.2230 area, but first we should see a minor rebound to 1.2310 zone. Crucial on the upside is 1.2335.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2310 | 1.2412 | 1.2230 | 1.2160 |

| 1.2335 | 1.2560 | 1.2210 | 1.2090 |

USD/JPY

USD/JPY

Current level - 107.84

The bias remains positive, for a tight test of 108.30 area. Crucial on the downside is 107.25 low.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 107.90 | 108.30 | 107.25 | 105.20 |

| 108.30 | 110.40 | 106.60 | 104.60 |

GBP/USD

Current level - 1..4022

The recent sell-off reached the support zone around 1.3980 and the outlook is already positive, for a corrective rebound towards 1.4010 area. Initial minor resistance lies at 1.4040.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4040 | 1.4280 | 1.3980 | 1.3960 |

| 1.4115 | 1.4280 | 1.3960 | 1.3710 |

Germany PMIs: Solid start to the second quarter.

Germany PMI manufacturing dropped to 58.1, down from 58.2 and beat expectation of 57.5. GErmany PMI services rose to 54.1, up from 53.9 and beat expectation of 53.7. PMI compositive rose to 55.3, up from 55.1.

Comments from Phil Smith, Principal Economist at IHS Markit:

"Growth of Germany's private sector steadied in April, to arrest the loss of momentum seen in February and March. With both manufacturing and services seeing slightly quicker increases in output, the data show the economy making a solid start to the second quarter.

"There was also a welcome pick-up in the rate of private sector job creation in April. Employment levels rose strongly on a broad-based basis by sector, albeit with the rate of hiring among manufacturers easing from the recent elevated levels.

"However, a further slowdown in new order growth to its weakest for over a year-and-a-half does raise some concerns. This seemed to be reflected in the survey's measure of business confidence, which slipped further from the highs seen in 2017."

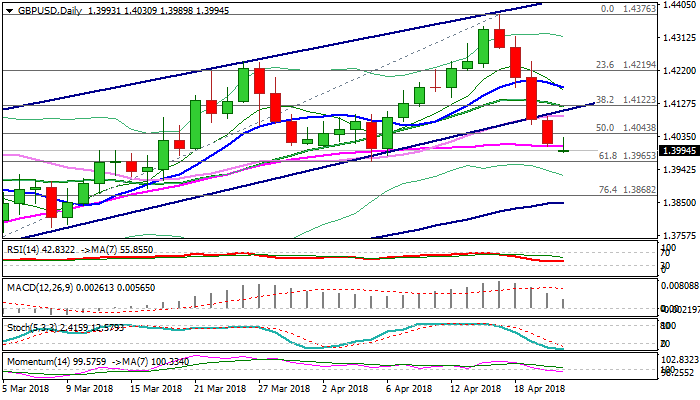

GBPUSD – Bears Cracked Psychological 1.40 Support And Signal Further Weakness

Cable maintains negative tone at the beginning of the week and cracked psychological 1.40 support, in extension of steep four-day fall from last week's peak at 1.4376. Weak releases of key UK data last week and dovish comments from BoE's Governor Carney, sidelined strong hopes for rate hike in May and soured sentiment. Pound spiraled lower in reaction on news, which resulted in the biggest weekly loss since early Feb. Fresh weakness dented larger bulls as repeated rejection of post-Brexit fall's recovery is forming double-top on weekly chart. Also, last week's break below bull-channel support line and violation of psychological 1.40 support (reinforced by 55SMA) are strong bearish signals. Pivotal support at 1.3965 (05 Apr trough/Fibo 61.8% of 1.3711/1.4376 rally) came under pressure and firm break here would confirm reversal and open way for further weakness. Bears may show hesitation on approach to 1.3965 support as slow stochastic is in deep oversold territory on daily chart, with corrective upticks expected to remain below 1.41 zone (30SMA/broken bull-channel support line) to keep bears intact. Negative momentum is building on daily chart and signals further downside, along with bearishly-aligned MA's.

Res: 1.4008, 1.4030, 1.4094, 1.4103

Sup: 1.3989, 1.3965, 1.3931, 1.3901

France PMIs: Private sector remained firmly in expansionary mode

France PMI manufacturing dropped to 53.4 in April, down from 53.7 and missed expectation of 53.5. France PMI services rose to 57.4, up from 56.9, beat expectation of 56.5. PMI composite rose to 56.9, up from 56.3.

Comments from Alex Gill, Economist at IHS Markit:

"The French private sector remained firmly in expansionary mode according to latest flash data. Indeed, at 56.9, the headline composite output figure signalled a sharper rate of growth than in March, and one that remained well above its long-run average (53.9).

"After having shown signs of slowing in recent months, the data will buoy hopes that the renaissance in the French economy has far from run its course. Further encouragement can be garnered from the broad-based nature of the acceleration, with sharper growth evident in both the manufacturing and services sectors, the former on the back of marked moderations in the prior two months."

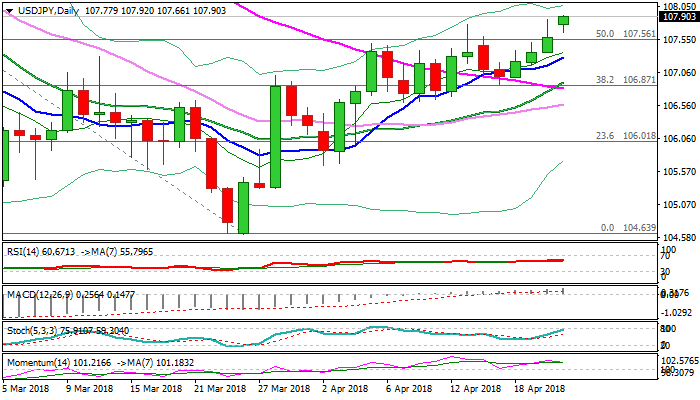

USDJPY Hits Two-Month High On Reduced Safe-Haven Demand, Bulls Pressure Pivotal 108.25 Fibo Barrier

The pair hit new two-month high at 107.90 on Monday in extension of three-day rally from 106.88 trough, as easing concerns over global political risks significantly reduced safe-haven-demand and kept yen under pressure.

Trading on Monday started with gap-higher opening and probe through Friday’s spike-high at 107.85 pressure psychological 108 barrier.

Bulls are on track for eventual close above 107.56 (50% retracement of 110.48/104.63 bear-leg, which repeatedly capped upside attempts in past two months) to generate fresh bullish signal.

Break above 108 handle would open pivotal barrier at 108.25 (Fibo 61.8%), break of which would signal further recovery and bring in focus targets at 109.01/31 (falling 100SMA/top of thick daily cloud).

Bullish daily techs remain supportive, however, bulls may show hesitation at 108 barrier.

Rising 10SMA which tracks the ascend since late Mar marks solid support at 107.27, which is expected to hold dips and keep bullish structure intact.

Res: 108.00, 108.25, 108.77, 109.01

Sup: 107.66, 107.56, 107.27, 106.88

Rising Yields Bolster The Dollar, Eurozone Flash PMIs In Focus

Here are the latest developments in global markets:

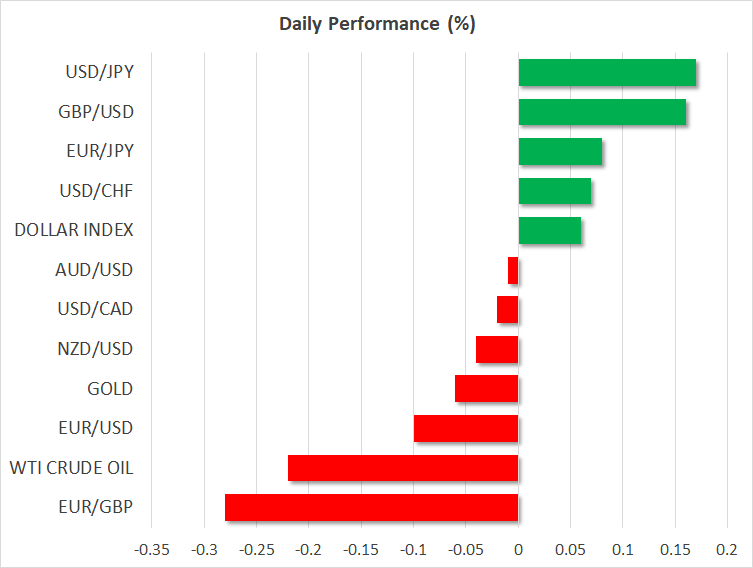

FOREX: The US dollar index traded higher on Monday, though by less than 0.1%, adding to the significant gains it posted on Fridayon the back of rising US Treasury yields. The loonie plunged on Friday after Canada’s CPI data disappointed, while the safe-haven Japanese yen is a touch softer today, amid diminishing risks on the North Korean front.

STOCKS: US markets closed lower on Friday, weighed on by a sustained rise in longer-term US bond yields. Rising bond yields typically weigh on demand for stocks, which become less attractive to hold in an environment where bonds begin to offer a higher and “safer” return. The Nasdaq Composite led the way down, declining by 1.27%, while the S&P 500 and Dow Jones fell by 0.85% and 0.82% respectively. That said, futures tracking the Dow, S&P and Nasdaq 100 are currently flashing green, pointing to a higher open today. In Asia, Japan’s Nikkei 225 dropped 0.33% while the Topix was down only by 0.02%. In Hong Kong, the Hang Seng declined 0.31%. In Europe, futures tracking most major benchmarks were in positive territory, though only marginally so.

COMMODITIES: Oil prices are slightly lower today, with WTI and Brent crude declining by 0.2% and 0.15% respectively. Despite the pullback though, both remain elevated near their respective three-and-a-half year highs. On Friday, US President Trump accused OPEC of keeping prices artificially elevated, while the Baker Hughes oil rig count showed another marked increase in active US rigs, both of which likely tempered the bullish sentiment surrounding the oil market. In precious metals, gold is trading marginally lower today, extending the significant losses it posted on Fridayas the US dollar surged. Since gold is denominated in dollars, an appreciation in the greenback makes the metal less attractive for investors using foreign currencies.

Major movers: Dollar bolstered by rising yields; loonie plunges on disappointing CPIs

The US dollar index surged on Friday, touching its highest level since April 6, buoyed by a sharp rise in longer-term US bond yields. The yield on 10-year US Treasuries touched 2.979% on Monday, a fresh high last seen in 2014, helping to increase the appeal of the greenback.

Besides lingering concerns about US deficits, the recent spike in yields appears to be owed to rising oil prices fueling speculation for higher inflation down the road, as well as trade and geopolitical risks subsiding. In terms of geopolitics, North Korea pledged over the weekend to immediately suspend its nuclear and missiles tests. As for trade, US Treasury Secretary Steven Mnuchin said on Saturday he is considering visiting China for trade negotiations, amplifying speculation that the recent tensions may be resolved through talks, instead of escalating into anything bigger.

The yen started the week on a soft footing, trading 0.15% lower against the dollar and almost 0.1% down versus the euro. The fact that trade and geopolitical risks seem to be fading is diminishing demand for the Japanese currency, which is viewed as a safe-haven asset.

Elsewhere, the loonie plunged on Friday, extending its recent losses. The move came after Canada’s inflation data for March disappointed, diminishing expectations for an imminent rate hike by the Bank of Canada (BoC). BoC Governor Poloz reinforced this narrative over the weekend, indicating he is not worried about inflation being above 2%. He said the Bank has a 1-3% inflation target range, and that a temporary overshoot above 2% does not automatically imply a rate hike. While the BoC appears unlikely to hike in May given the cautious stance it has maintained lately, investors still seem convinced a hike will materialize in July, with the implied probability for such action resting at 76%.

Day ahead: Eurozone PMIs and US existing home sales on the agenda

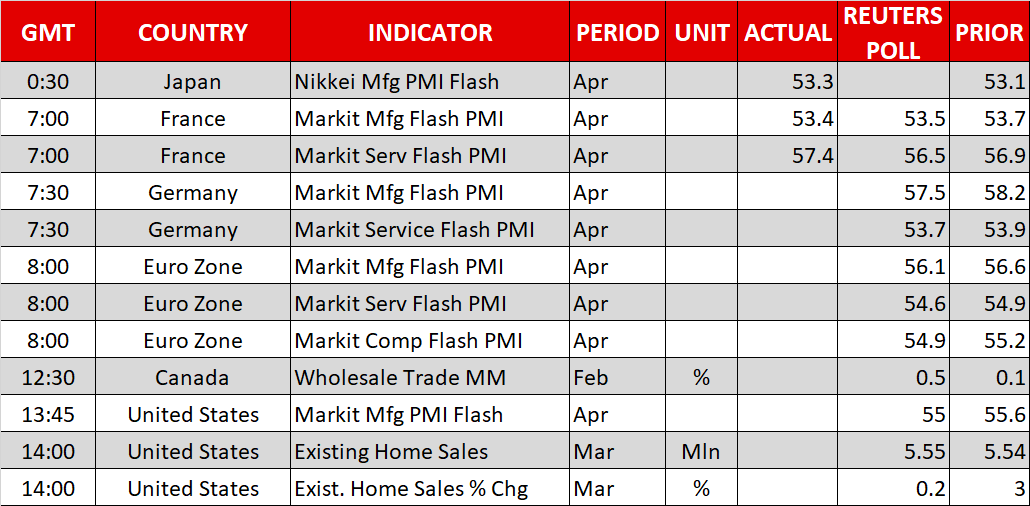

Monday’s economic calendar features a few releases that have the capacity to lead to movements in forex markets. Perhaps most notable of those releases are the eurozone’s flash PMI readings for the month of April, especially in light of the fact that they come only a few days ahead of a European Central Bank meeting.

Eurozone preliminary PMI estimates for the manufacturing and services sectors, as well as the composite measure that blends the two industries, will be made public at 0800 GMT. Projections are for April’s figures to remain above the 50 contraction/expansion territory, though point to further easing of activity after an upbeat start of the year. Such an outcome would support views that economic activity has peaked in the euro area and likely complicate the ECB’s “task” to normalize policy; the Bank is holding a meeting later this week, with a decision on monetary policy scheduled to be made public on Thursday.

The corresponding PMI prints for Germany and France, the eurozone’s two largest economies, are also due today ahead of euro-wide numbers. Germany’s numbers will hit the markets at 0730 GMT, while France’s were released at 0700 GMT (the manufacturing print was marginally below expectations, while the one on services positively surprised; the euro gained as a result).

Turning to North America, Canada will see the release of data on February’s wholesale trade at 1230 GMT, with the focus next turning to the US. Markit’s flash manufacturing PMI for April and figures on March existing home sales will be made public out of the world’s largest economy at 1345 GMT and 1400 GMT respectively. Manufacturing activity is anticipated to cool a bit though still remain in growth territory, and existing home sales are expected to marginally expand relative to February, a month during which they surged –supply-side issues are yet again likely to have affected home sales.

Google parent Alphabet and Halliburton will be releasing quarterly results today; the former after the US market close and the latter before the market’s open.

An appearance before the House of Commons Standing Committee on Finance by Bank of Canada Governor Stephen Poloz and Senior Deputy Governor Carolyn Wilkins at 1930 GMT might be of interest for loonie traders, while ECB Board member Benoit Coeure will be participating in a conference at 1400 GMT.

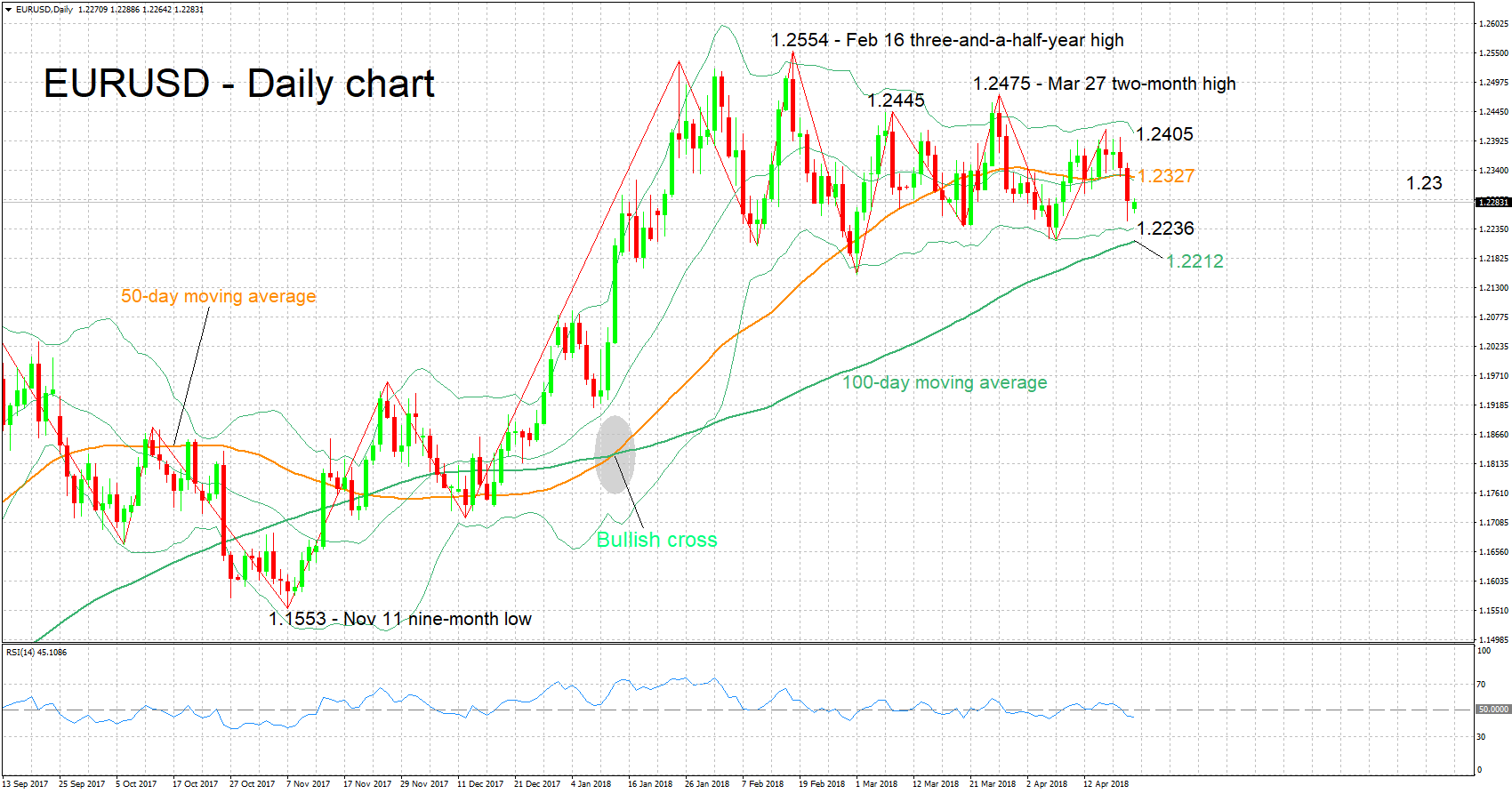

Technical Analysis: EURUSD weak bearish sentiment in the short-term

EURUSD has lost ground after reaching a near four-week high of 1.2413 on Tuesday, eventually recording a two-week low of 1.2249 on Friday; price action is taking place roughly 30 pips above that trough at the moment. The RSI has fallen below its 50 neutral perceived level, supporting a negative short-term picture, though the fact that the indicator is only moderately negatively sloped is an indication that bearish sentiment is not that strong.

Stronger-than-expected eurozone PMI prints later on Monday are likely to boost the pair, with resistance to advances potentially coming around the current level of the 50-day moving average at 1.2327. This is where the middle Bollinger line (a 20-day MA line) roughly lies as well, while the 1.23 round figure not far below might also act as a barrier to gains.

Conversely, weaker than forecasted prints are anticipated to push EURUSD lower. Support in this case might come around the lower Bollinger band at 1.2236; the range around this includes last week’s two-week low of 1.2249, as well as the near eight-week low of 1.2214 hit on April 6. The 100-day MA lies not far below at 1.2212.

US releases later in the day also have the capacity to move the pair.

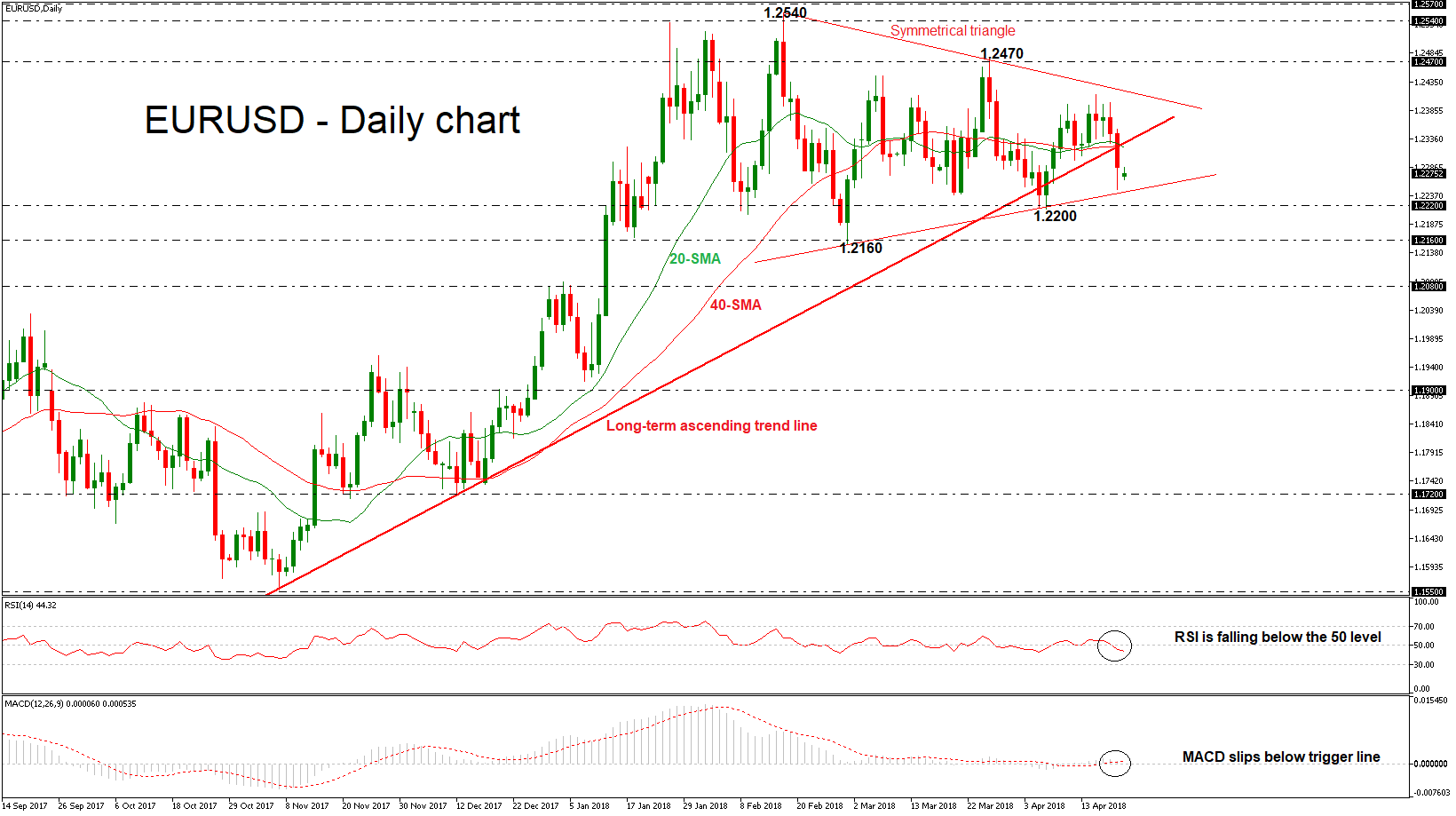

EURUSD Penetrates Long-Term Ascending Trend Line, Still Stands In Symmetrical Triangle In Near-Term

EURUSD has been underperforming in the past two days, breaking below the long-term ascending trend line, which has been holding since March 2017. However, the single currency is still standing in the symmetrical triangle formation against the greenback as it finished the day around the 1.2250 price level, near the lower boundary.

In the daily timeframe, the RSI indicator is currently increasing negative momentum below the threshold of 50, while the MACD oscillator is slowing down in positive zone and created a bearish crossover with its trigger line. Both are hinting that the next move in prices is likely to be on the downside rather than on upside. Also, the pair is developing well below the 20- and 40-simple moving averages.

Should the market extend losses and slip below the triangle pattern, the main bullish trend in the medium term could shift to bearish. Support could be met near the 1.2220 barrier, which holds near the lower band of the triangle. A significant leg below this level could send prices towards the 1.2160 level, taken from the low in March.

Conversely, if the pair bounces up, immediate resistance could be provided by the 20- and 40-SMAs around 1.2320. In case of more advances, the pair could touch the upper band of the pattern near 1.2412, which is near the peak of April 17. A jump above this strong resistance level could open the way towards the 1.2470, taken from the peak on March 27.

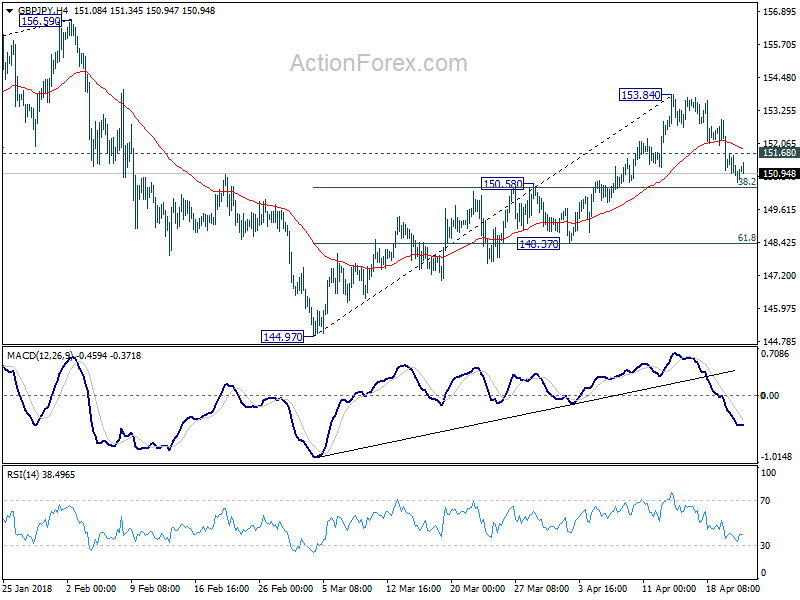

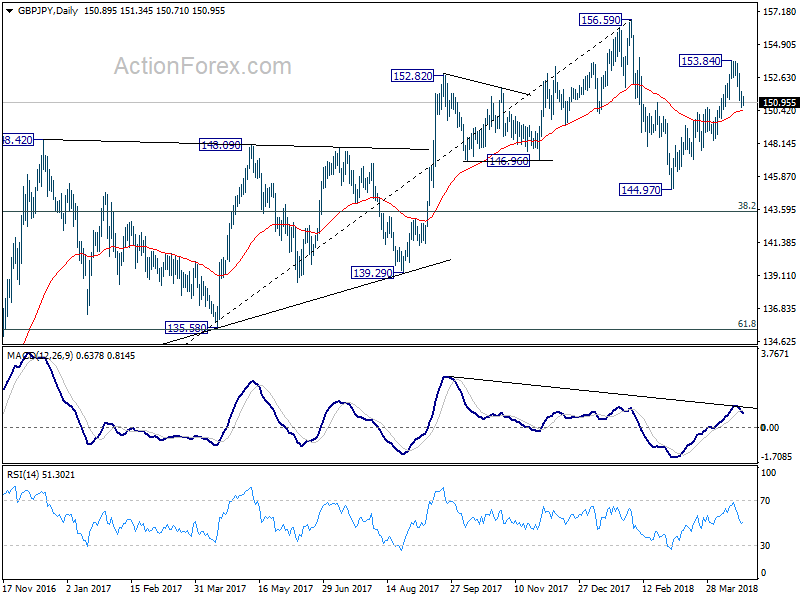

GBP/JPY Daily Outlook

Daily Pivots: (S1) 150.30; (P) 151.00; (R1) 151.34; More...

Intraday bias in GBP/JPY remains on the downside for the moment. As noted before, corrective rise from 144.97 should have completed at 153.84 already. Deeper fall should be seen to 148.37 support first. Break will bring retest of 144.97 low. On the upside, above 151.68 minor resistance will turn intraday bias neutral first. But near term risk will now stay on the downside as long as 153.84 holds.

In the bigger picture, price actions from 156.59 are viewed as a corrective pattern. For now, we'd expect at least one more fall for 38.2% retracement of 122.36 to 156.59 at 143.51 before the consolidation completed. Though, firm break of 156.59 will resume whole up trend from 122.36 (2016 low) to 50% retracement of 195.86 (2015high) to 122.36 at 159.11 next.

European Data Expected To Show Further Weakness Today

At 07:30 GMT, German Markit Manufacturing PMI (Apr) is expected to come in at 57.5 from 58.2 previously. Markit Services PMI (Apr) is expected at 53.7 v 53.9 previously. Markit PMI Composite (Apr) is expected to be 54.8 from 55.1 prior. The expectation is for a slip in these data points, confirming that the December reading was a short-term high. For Manufacturing, it was the highest since before the financial crisis and for service, it was the highest since June 2011. This weakness is a worry for the ECB. EUR traders will be closely following this data release.

At 08:00 GMT, Eurozone Markit Manufacturing PMI (Apr) is expected to come in at 56.1 from 56.6 previously. Markit Services PMI (Apr) is expected at 54.6 v 54.9 previously. Markit PMI Composite (Apr) is expected to be 54.9 from 55.2 prior. This data is also expected to soften once again from the highs in December. EUR crosses may see a spike in volatility should the released data differ from the expected consensus.

At 14:00 GMT, US Existing Home Sales (MoM) (Mar) is expected to be 5.55M against 5.54M previously. After reaching a seven-year high in November at 5.81M, this data point had slipped lower in the following months, signalling a little softness in the sector, however, it recovered somewhat last month. That recovery is expected to continue with this reading. USD crosses may be moved by this data, as analysts try to understand the impact on the economy.

Major data releases for the week:

On Tuesday, at 01:30 GMT, Australian CPI data will be released.

On Thursday, at 11:45 GMT, The ECB will announce its Interest Rate Decision, with a Press Conference and Monetary Policy Statement to follow at 12:30 GMT.

At 23:30 GMT, Japanese CPI data will be released.

On Friday, at 02:00 GMT, The BOJ will announce its Interest Rate Decision and release its Monetary Policy Statement. A Press Conference will follow at an undisclosed time, usually two to three hours later.

At 08:30 GMT, UK Gross Domestic Product data will be released.

At 12:30 GMT, US Gross Domestic Product data will be released, along with Personal Consumption Expenditures.

North And South Korea To Meet On Friday For Historic Talks

The Koreas will hold historic talks on Friday, aimed at formally ending hostilities between them and closing a chapter of their combined history. North Korea pledged to suspend missile and nuclear tests effective immediately, while South Korea has lifted border propaganda broadcasts. USDJPY has moved up to the 107.800 level, with resistance above at 108.000 and a breakout on further good news targeting 109.000. Risk-on is expected to continue in the markets after major indices declined on Friday, but only to retest key breakout supporting levels from the last two weeks. The US500 held the 2660.00 support area and the German30 Index held the 12500.00 area. Indices futures are indicating a higher opening for markets ahead of the European session, despite some weakness in Asia, and if these supporting levels hold it could be a very positive week. Gold has slipped lower, as demand softens and USD finds some strength in early trading that is likely to continue.

Canadian Consumer Price Index (MoM) (Mar) was 0.3% v an expected 0.4%, against 0.6% previously. BOC Consumer Price Index Core (YoY) (Mar) was 1.4% v an expected 1.5%, against 1.5% previously. BOC Consumer Price Index Core (MoM) (Mar) was as expected at 0.2%, from a prior 0.7%. Consumer Price Index (YoY) (Mar) was 2.3% v an expected 2.4%, against 2.2% previously. Consumer Price Index – Core (MoM) (Mar) was 0.0% against 0.2% previously. Canadian Retail Sales Ex-Autos (MoM) (Feb) was 0.0% v an expected 0.3%, against 0.9% previously, which was revised up to 1.0%. Retail Sales (MoM) (Feb) was 0.4% v an expected 0.3%, against 0.3% previously, which was revised down to 0.1%. These data points came in largely as expected, with slight softness in some readings. Retail sales were slightly stronger after missing expectations over the last two months, but last month’s figure was revised down. Retail Sales Ex-Autos showed a drop, but last month’s figure was revised up. The sales data is showing a lot of weakness as a result, with the 3-month average of Sales Ex-Autos at -0.4%, the lowest since 2015. USDCAD moved higher from 1.26328 up to 1.27450 after the release of this data, as the CAD weakened further for the third day.

The Baker Hughes US Rig Count was released with a headline number of 820. The prior number last Friday showed that there were 815 Oil rigs in operation, up from 808 the previous week. With oil at the highest levels in recent years, on the back of a bigger than expected draw in inventories on Wednesday, this data may set the tone for traders as they start the week.

EURUSD is down -0.13% overnight, trading around 1.22700.

USDJPY is up 0.18% in early session trading at around 107.806.

GBPUSD is up 0.11% this morning, trading around 1.40169.

USDCAD is down -0.07%, trading around 1.27553.

Gold is down -0.08% in early morning trading at around $1,334.50.

WTI is up 0.37% this morning, trading around $68.33.