Sample Category Title

Canadian Dollar Drifting Ahead Of CPI, Retail Sales

The Canadian dollar is showing little movement in the Friday session. Currently, USD/CAD is trading at 1.2655, down 0.13% on the day. On the release front, Canada releases key consumer data. CPI is expected to dip to 0.4%. Core Retail Sales and Retail Sales are also forecast to post gains of 0.4%. There are no US data releases on the schedule.

There were no surprises from the Bank of Canada on Wednesday, as the bank maintained the benchmark rate at 1.25 percent. The BoC was in cautious mode in the rate statement, noting that growth in the first quarter was weaker than the bank had forecast, but that it expected better news in the second quarter. The bank has some egg on its face, as in January it predicted growth of 2.5% for the first quarter, but has now revised the forecast to just 1.3% growth. Speaking after the statement, BoC Governor Stephen Poloz said that “the economy is in a good place,” but added that “interest rates are very low”. This is a clear signal that the BoC plans to raise rates in the near future, and many analysts are predicting a rate hike in July. Canada’s employment picture has been a bright spot, underscored by an excellent ADP nonfarm payrolls report on Thursday. As well, inflation has moved closer to the BoC’s target of 2 percent, making a rate hike likely in the next few months.

Continuing uncertainty over the future of the NAFTA trade agreement remains a major headache for the Bank of Canada. The protectionist US administration has reopened the NAFTA agreement, threatening to walk away if its demands for major concessions in favor of the US are not met. NAFTA is a crucial component of the Canadian economy, and the loss of NAFTA would be a nightmare for Canada. Ideally, the bank would prefer to hold off on a rate hike until the NAFTA issue is resolved. At the same time, the Federal Reserve is expected to raise rates at least twice more in 2018, and if the BoC does not increase rates, the Canadian dollar could fall sharply against a US currency that would be more attractive to investors.

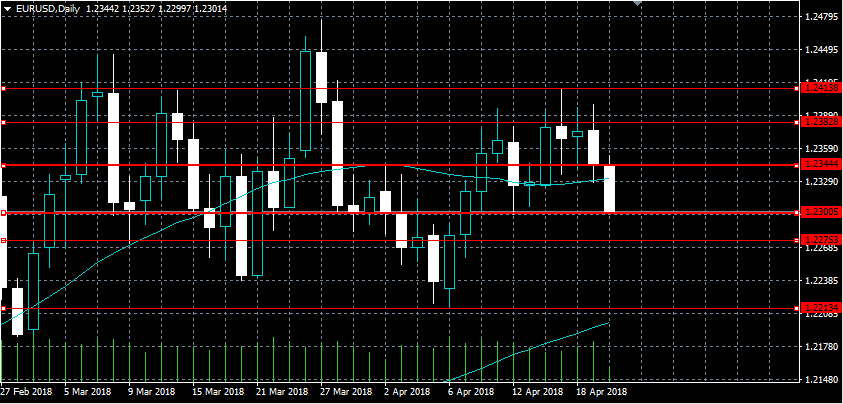

EURUSD Now Testing Critical Support

The euro has continued to weaken against the greenback during the European trading session, as weaker German PPI inflation data and a rise in the value of the U.S dollar index weigh on the single currency. The EURUSD is currently testing the 1.2300 support level, with the pair now looking set for a second day of heavy trading losses. Traders now look to the releases of U.S Consumer Confidence data during the U.S trading session, with EURUSD sellers looking for a bearish weekly close below the 1.2300 level.

The EURUSD is intraday bearish while trading below the 1.2344 level, sellers may test towards the 1.2275 and 1.2213 levels.

Should the EURUSD pair move back above the 1.2344 level, buyers may be encouraged to test back towards the 1.2382 and 1.2413 levels.

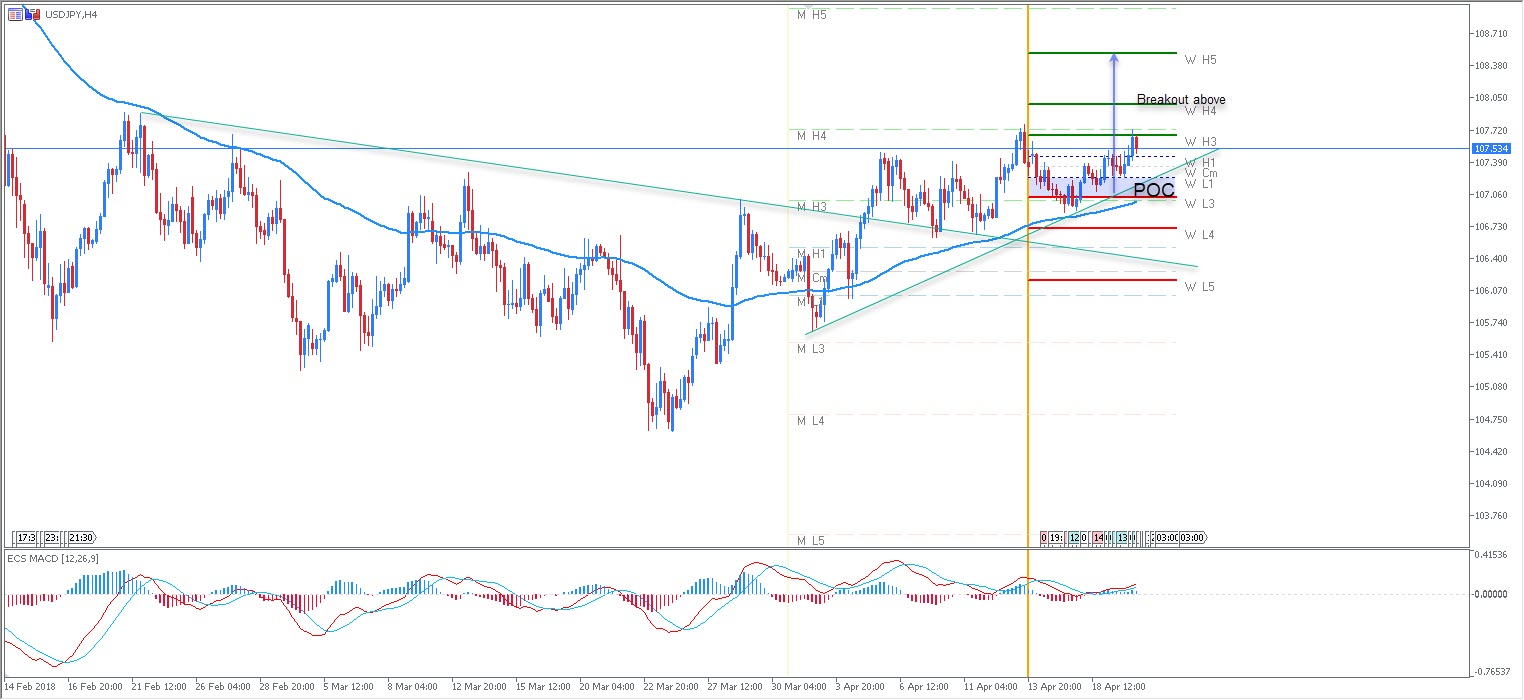

USDJPY Testing Key Upside Resistance

The U.S dollar has moved towards the upper-end of its recent medium-term trading range against the Japanese yen, as the U.S dollar index strengthens over rising U.S treasury bond-yields. The USDJPY pair currently trades around the 107.60 level, after finding interim daily resistance from the 107.72 level. Traders now look towards the February monthly price-high at 107.92, as it forms the strongest area of technical resistance before the 108.00 handle.

The USDJPY pair remains intraday bullish while trading above the 107.30 level, key resistance is now found at the 107.92 and 108.43 levels.

Should price-action on the USDJPY pair decline below 107.30 level, sellers will likely test towards the 107.00 and 106.60 support levels.

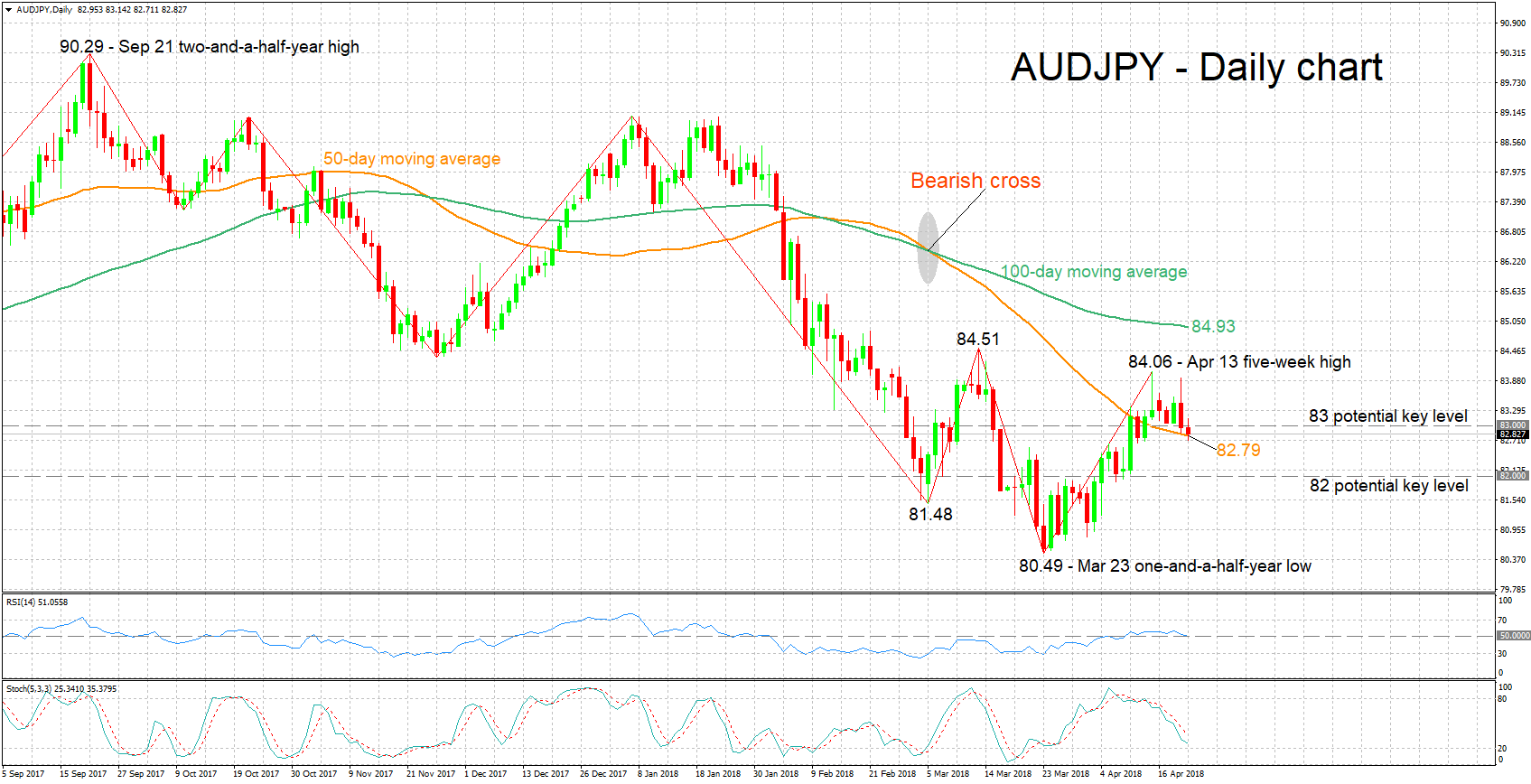

AUDJPY Posts 8-Day Low, Stochastics Paint Negative Picture In Very Short-Term

AUDJPY has retreated a bit after reaching a five-week high of 84.06 last week. Earlier on Friday, the pair hit an eight-day low of 82.71.

The RSI has been largely moving sideways in recent days, pointing to the absence of short-term momentum in either the upside or the downside. The stochastics, however, are projecting a negative picture in the very short-term: the %K line remains below the slow %D one, with both lines heading lower.

Immediate support could be taking place around the current level of the 50-day moving average line at 82.79; the 50-day MA itself was briefly violated earlier in the day. Support to additional declines might come around the 82 round figure that may be of psychological significance, with steeper losses starting to increasingly turn the attention to the one-and-a-half-year low of 80.49 from late March.

On the upside and in case of advances, the range around the 83 handle might act as a first line of resistance, before the focus turns to last week’s five-week high of 84.06 – the area around this peak also encapsulates the 84 mark that could also hold psychological importance.

The medium-term outlook is looking mostly bearish, with the pair being in a downtrend, recording lower highs and lower lows. A bearish cross has also been in place since early March when the 50-day MA moved below the 100-day one. A decisive move above the 50-day MA though, which is where price action is taking place at the moment, would set a more neutral medium-term picture for the pair.

Overall, the short-term bias is looking mostly neutral (with bearish signals in the very short-term) and the medium-term outlook appears predominantly negative.

USD/JPY Bullish Trend Line Cross Targets Higher Levels

The USD/JPY has broken through a trend line boosted by rising 10 year US yields. The US 10-year yields were up and we can see the USD/JPY going up too. Leaned bullish W pattern and X cross of two trend lines are technically suggesting upside continuation. 107.05-20 is the POC zone and the pair could spike to the upside targeting 108.00. 4h candle close above 108.00 should give another boost to USD/JPY and the target is 108.50. Today is Friday so pay attention to profit taking later in the day.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

M H4 - Monthly Camarilla Pivot (Very Strong Monthly Resistance)

M L3 – Monthly Camarilla Pivot (Monthly Support)

M L4 – Monthly H4 Camarilla (Very Strong Monthly Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

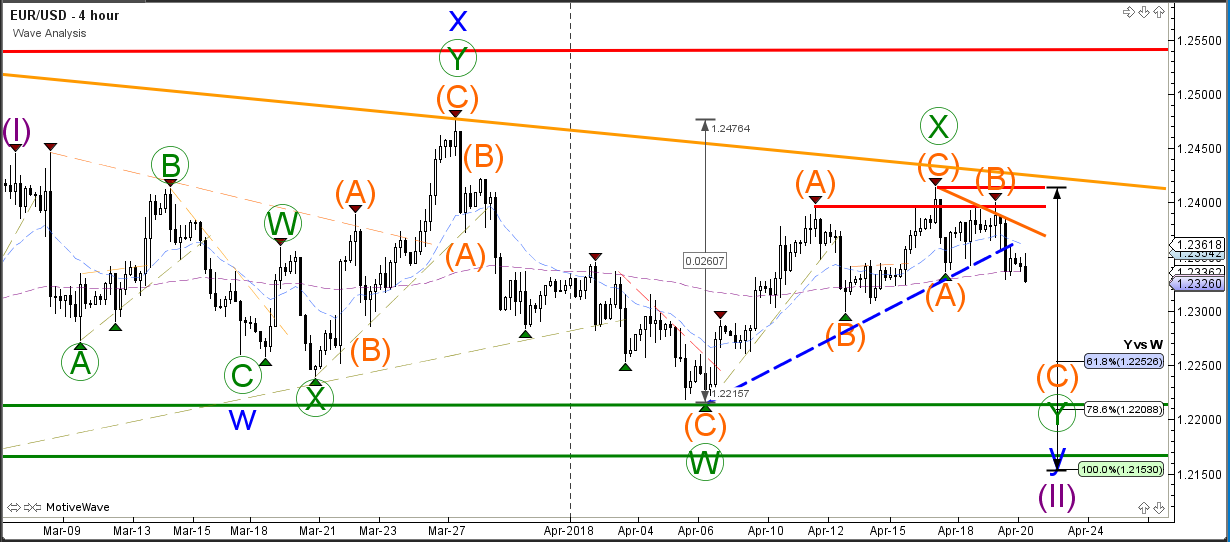

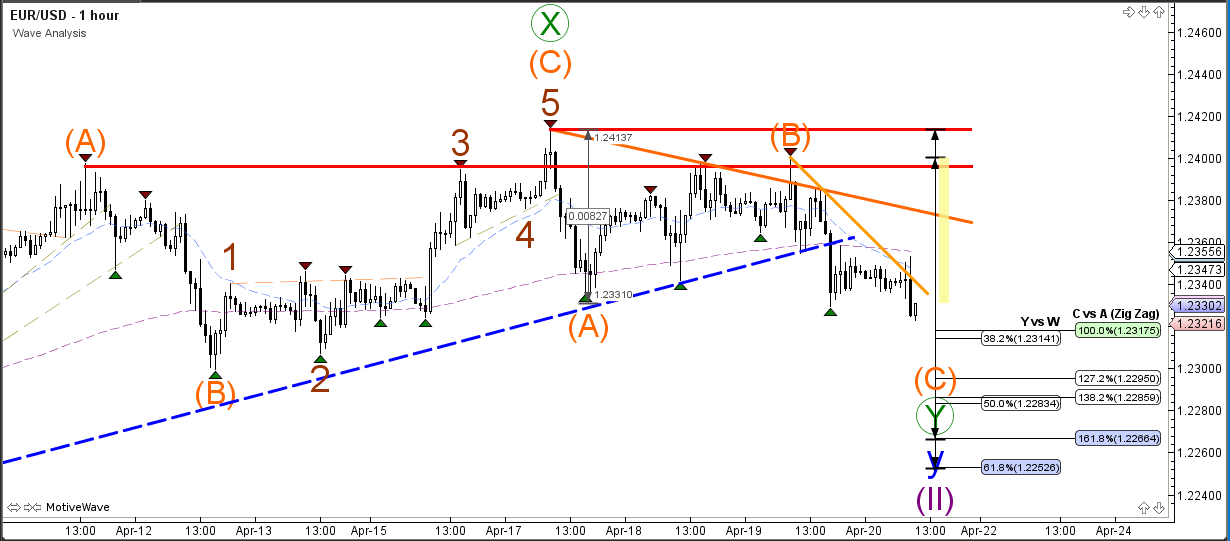

EUR/USD Breaks Support Line For Bearish Wave C Break

The EUR/USD is breaking below the support trend line (dotted blue) which is creating a larger bearish wave structure and expanding the bearish correction. Price is probably building a bearish ABC (brown) correction and could fall to test the Fibonacci targets of wave Y vs W.

The EUR/USD broke below the chart pattern and is likely to make the short-term trend bearish. A bullish breakout is expected to face a strong support zone at 1.2325, 1.2250 and 1.22.

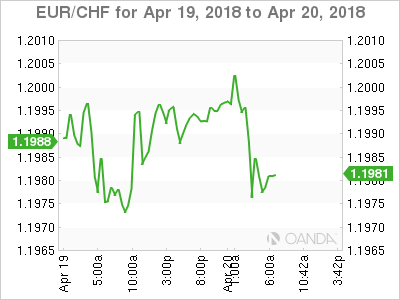

EUR/CHF – Swiss National Bank Deja Vu

Global equities are closing out the week on the back foot, stressed mostly by technology stocks coming under earnings-related pressure. U.S Treasury yields are holding above the psychological +2.90% as German Bunds steadied and U.K gilts pared yesterday's losses.

In FX the 'big' dollar has managed to extend this week's advance, while in commodities, crude oil prices have eased a tad, as the rally in metals has stumbled.

Bank of England's (BoE) Governor Carney comments on Thursday managed to send the sterling to a two-week low of £1.4045 – he said that “due to softer economic data, the BoE may consider not raising interest rates in May, as most were expecting.”

Note: Both U.K inflation and retail sales data this week were both lower than in the previous periods and below market expectations. The odds for a May hike have dropped to +50%, earlier this week futures traders were looking at +80% possibility.

On Tap: Canadian retail sales and inflation data due at 08:30 am EDT.

1. Stocks slip on tech pressure

In Japan, the Nikkei share average edged lower overnight as worries about slower smartphone demand hit technology shares, while financial stocks found support on the back of higher U.S yields. The Nikkei gave up -0.1% – the index has rallied +1.8% for the week, its fourth consecutive week of gains. The broader Topix rallied +0.1%.

Down-under, Aussie shares snap five sessions of gains, as the recent commodity prices rally paused for breath. The S&P/ASX 200 index fell -0.1%, but managed to close out the week higher for the consecutive time. In S. Korea, the Kospi fell -0.3%.

In Hong Kong, stocks end lower on a slump in energy shares prices from their two-month high print Thursday. The Hang Seng index ended down -0.9%, while the China Enterprises Index closed -1.5% lower.

In China, stocks post their worst week in a month on trade war concerns. The blue-chip CSI300 index closed down -1.3%, while the Shanghai Composite Index dropped -1.5%.

In Europe, regional indices are trading mixed, – materials and energy stocks are under pressure following retracement in commodities and oil. In the U.K, Brexit negotiation concerns are weighing on sentiment.

In the U.S, stocks are expected to open in the 'black (-0.2%).

Indices: Stoxx50 +0.1% at 3,487, FTSE +0.3% at 7,367, DAX -0.2% at 12,545, CAC-40 -0.1% at 5,388; IBEX-35 +0.1% at 9,877, FTSE MIB -0.1% at 23,760, SMI -0.4% at 8,798, S&P 500 Futures -0.2%

2. Oil dips, but trades atop of its four year highs, gold higher

Ahead of the U.S open, crude oil prices trade near their three-year highs, supported by ongoing OPEC led supply cuts and strong global demand drawing down excess supplies.

Brent crude oil futures are at +$73.74 per barrel, down -4 cents from Thursday's close, while U.S West Texas Intermediate (WTI) crude futures are down -13c at +$68.16 a barrel.

Note: Both Brent and WTI hit their highest levels since November 2014 on Thursday, at $74.75 and $69.56 per barrel respectively. WTI is set for its second weekly gain, climbing more than +1% this week, while Brent is also poised to rise for a second week, adding around +1.5%.

Beyond OPEC and company's supply management, crude prices have also been supported by market expectations that the U.S will re-introduce sanctions on OPEC-member Iran.

Gold prices have inched a tad lower ahead of the U.S open and are headed for the first weekly decline in three-weeks on expectations of higher U.S rates and easing political tensions on the Korean Peninsula and Syria weighing on demand for the safe-haven metal. Spot gold is down -0.1% at +$1,344.10 an ounce, while U.S gold futures have fallen -0.2% to +$1,346.30 per ounce. Spot gold is on the cusp of falling -0.2% on the week.

3. Sovereign yields back up

With the inflationary implications of commodity prices gaining strongly this week, and geopolitical risks fading, has supported global sovereign bond yields to back up.

Stateside, the U.S 10 year Treasury yield has suddenly spiked above +2.90% and to levels not seen since the FOMC rate hike in March.

The speed of this week's rise has allowed the U.S yield curve to steepen slightly. The 2's/10's spread has pushed out from +43 bps earlier this week up to +47bps, and this in turn has helped the dollar find a bid.

Elsewhere, in Germany, the 10-year Bund yields are unchanged at +0.60%. In the U.K, the 10-year Gilt yield has dipped -4 bps to +1.5%, while in Japan, the 10-year JGB yield has climbed +2 bps to +0.06%, the highest in seven-weeks.

4. EUR/CHF deja vu

EUR/CHF has rallied back above the infamous €1.2000 handle, again this morning, reaching €1.2008, its highest since the Swiss National Bank (SNB) ended its policy of keeping a €1.20 EUR/CHF floor in early 2015.

However, for now, it has failed to stay, last trading down -0.1% at €1.1974. Expect the market to remain cautious following the pair's rapid appreciation.

Note: EUR/CHF has rallied from €1.15 early March to today's €1.20+ handle.

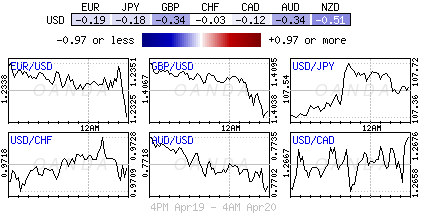

GBP/USD (£1.4066) has continued its soft tone in the aftermath of Governor Carney's comments yesterday that seems to doubt on a BoE rate hike next month. He emphasized yesterday that markets should “not get overly focused on the exact timing of hikes but attuned to the general path of rates.”

With the mild inflation data throughout Europe in recent weeks could get ECB's Draghi to verbally push back on EUR strength. ECB rhetoric of late has been all about 'patience' and dealers and investors seem to believe that any change in guidance would come in June rather at next week's ECB meeting (April 26).

Higher U.S yields is supporting USD/JPY as its move above the psychological ¥107.50 to ¥107.66. The Bank of Japan (BoJ) also meets next week.

5. German producer prices rise

German data this morning showed that in March the index of producer prices for industrial products rose by +1.9% y/y.

In February the annual rate of change all over had been +1.8%.

Digging deeper, the March price indices of all main industrial groups increased compared with the previous year – energy prices were up +2.4%, while prices of electricity increased by +5.5%, whereas prices of petroleum products were up +1.3% and prices of natural gas (distribution) rose by +0.2%.

The overall index, disregarding energy, was +1.7% up on March 2017 and +0.1% compared with February.

Futures Edge Lower In Calm End To The Week

- Stocks Benefiting From Lack of Escalation on Global Issues;

- Sterling Slides as Carney Backtracks on May Hike;

- Saunders Maintains Hawkish View as BoE Split Becomes Clear.

'A slight down day on Thursday and marginal losses in futures ahead of the open today shouldn’t take anything away from what has been a decent week for equity markets”

We could be in for a relatively calm end to the week, which investors may welcome given how beneficial it has been over the course of the week.

A slight down day on Thursday and marginal losses in futures ahead of the open today shouldn’t take anything away from what has been a decent week for equity markets, which have benefited greatly from the lack of noise around Syria or trade wars. The gradual improvement in sentiment has accompanied the lack of escalation on both these issues, something that will only be sustainable as long as it continues.

Earnings season in the US is also helping matters with the financial sector in particular having reported some strong numbers for the first quarter. It’s likely to be a strong season of growth for earnings, aided considerably by Donald Trump’s tax reforms, the question now is whether other sectors can live up to or surpass the hefty expectations.

'The numbers we’ve seen when combined with the uncertain outlook certainly warranted a rethink from policy makers at the BoE”

The pound is slipping again this morning, after having suffered sizeable losses late on Thursday in response to Bank of England Governor Mark Carney’s rather dovish comments. While Carney didn’t deviate from the view that gradual rate hikes are going to be necessary, he did cast doubt on whether the next will come in May, which was heavily being priced in earlier this week.

It’s actually been quite a bad week for the pound, which peaked close to 1.44 against the dollar on Tuesday before falling more than 2% in response to a series of disappointing data releases. The numbers we’ve seen when combined with the uncertain outlook certainly warranted a rethink from policy makers at the BoE but until now, I wasn’t convinced they would actually reconsider having spent months laying the groundwork for a May rate hike.

'The question is what camp the other policy makers sit in, Carney’s or Saunders’”

While a hike is by no means off the table, the comments from Carney are a clear and deliberate warning to markets that the Monetary Policy Committee could delay the move by a few months, at which point the data may be less sketchy and the outlook more clear. Market expectations have since fallen to around 45% for a rate hike and could fall further if fellow policy makers join Carney is playing down an increase in a few weeks.

One policy maker that won’t be joining him is Michael Saunders – voted for a hike at the last meeting - who spoke this morning about the need to raise interest rates at a 'gradual” not 'glacial” pace and questioned the significance of first quarter data due to the weather. He also claimed labour market inflation pressures are greater than forecast in February so I wouldn’t expect his vote to change next month. The question is what camp the other policy makers sit in, Carney’s or Saunders’.

DAX Steady, Investors Eye Eurozone Consumer Confidence

The DAX index is steady in the Friday session. Currently, the DAX is trading at 12,574 points, up 0.06% on the day. On the release front, there are no major events. German PPI improved to 0.1%, but this fell short of the estimate of 0.2%. Later in the day, the eurozone releases consumer confidence, which is expected to remain at zero for a third straight month.

Years of massive stimulus from the ECB have stimulated the eurozone economy, but inflation has not kept up. This was underscored by March inflation numbers. German PPI improved from -0.1% to 0.1%, but missed the estimate of 0.2%. Final CPI came in at 1.3%, up from 1.1% a month earlier. Still, the reading fell short of the estimate of 1.4%. With inflation well below the ECB inflation target of around 2%, there is little pressure on the ECB to tighten its accommodative monetary policy. The ECB’s stimulus program is scheduled to wind up in September, but an increase in interest rates is unlikely before 2019.

The markets are keeping a close eye on the ECB, which meets next week for a policy meeting. Despite stronger economic conditions in the eurozone, the ECB has been in cautious mode. At the March meeting, policymakers took a small step, dropping a pledge to increase stimulus if needed. Will we see additional ‘baby’ steps at the April meeting? The markets are not expecting any change in forward guidance, and concerns over recent trade disputes could mean a dovish statement from ECB President Mario Draghi. Traders shouldn’t expect any dramatic moves next week, as the bank will likely continue to preach patience and prudence.

Euro Under Pressure As German Inflation Misses Estimate

EUR/USD has lost ground in the Friday session. Currently, the pair is trading at 1.2299, down 0.40% on the day. On the release front, there are no major events. German PPI improved to 0.1%, but this fell short of the estimate of 0.2%. Later in the day, the eurozone releases consumer confidence, which is expected to remain at zero for a third straight month.

The German and eurozone economies have been performing well in 2018, but inflation levels remained low in March. German PPI improved from -0.1% to 0.1%, but missed the estimate of 0.2%. Final CPI came in at 1.3%, up from 1.1% a month earlier. Still, the reading fell short of the estimate of 1.4%. With inflation well below the ECB inflation target of around 2%, there is little pressure on the ECB to tighten its accommodative monetary policy. The ECB’s stimulus program is scheduled to wind up in September, but an increase in interest rates is unlikely before 2019.

Investors are keeping a close eye on the ECB, which meets next week for a policy meeting. Despite stronger economic conditions in the eurozone, the ECB has been in cautious mode. At the March meeting, policymakers took a small step, dropping a pledge to increase stimulus if needed. Will we see additional ‘baby’ steps at the April meeting? The markets are not expecting any change in forward guidance, and concerns over recent trade disputes could mean a dovish statement from ECB President Mario Draghi. Traders shouldn’t expect any dramatic moves next week, as the bank will likely continue to preach patience and prudence.