Sample Category Title

GBP/USD Continued Weakness

GBP/USD strong decline from 1.4377 high continues, trading at end March high and heading along the 1.4055 range. Hourly support and resistance are given at 1.3905 (23/02/2018 low) and 1.4377 (17/04/2018 high). The technical structure suggests further short-term decline.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high)

EUR/USD Pausing

EUR/USD sideways trading continues at the 1.2340 range. The pair is currently maintained between hourly support and resistance given at 1.2165 (17/01/2018 low) and 1.2506 (25/01/2018 high). The technical structure suggests further short-term sideways trading moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

BoE’s Carney Slams The Pound, Canadian Inflation & Retail Sales Eyed

Here are the latest developments in global markets:

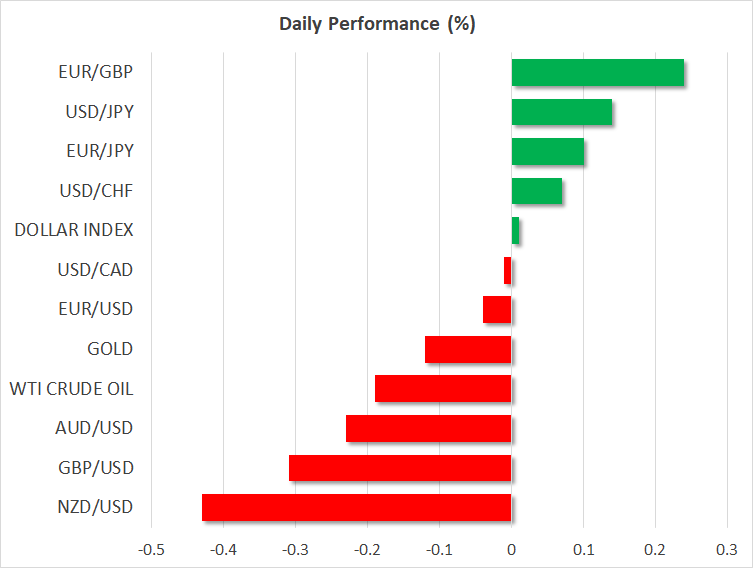

FOREX: The US dollar index is practically unchanged on Friday, after it posted solid gains earlier on Thursday on the back of rising US Treasury yields. Sterling/dollar was 0.3% lower, with the British pound extending the losses it posted yesterday, after BoE Governor Mark Carney hinted that a rate hike in May is not actually a done-deal.

STOCKS: US markets closed lower, pressured by a notable rise in longer-term US bond yields, something that usually curbs demand for stocks. The Nasdaq Composite led the way down on the back of concerns that the handset boom is taking a breather (Apple was a notable decliner), falling by 0.78%, while the S&P 500 and the Dow Jones dropped by 0.57% and 0.34% respectively. The slide looks set to continue today, as futures tracking the Dow, S&P, and Nasdaq 100 are all currently pointing to a slightly lower open. Asian markets were lower on Friday as well, for the most part. In Hong Kong, the Hang Seng fell 0.68%, while Japan was mixed, with the Nikkei 225 falling by 0.13% but the Topix managing to close 0.05% higher. In Europe, futures tracking almost all the major indices were flashing green. The exceptions were the Euro STOXX 50, the German DAX and the Italian FTSE MIB.

COMMODITIES: Oil prices are slightly lower on Friday, with both WTI and Brent down by 0.2%. That said, both benchmarks touched fresh highs last seen in 2014 yesterday, and despite the latest pullback, they remain elevated. Speculation that Saudi Arabia is aiming for prices closer to $100 was the key trigger for the recent surge, with surprising drawdowns in inventories enhancing the bullish sentiment. Today, the focus will turn to the Baker Hughes rig count, for a fresh indication on US production. In precious metals, gold is 0.1% lower, last seen near $1342 per ounce, extending losses from yesterday. The yellow metal's underperformance is likely owed to the recovery in the greenback. Since gold is denominated in dollars, an appreciation in the currency makes the metal less attractive for investors using foreign currencies, weighing on its demand.

Major movers: Pound slammed as BoE's Carney puts May hike into doubt; dollar climbs alongside US yields

It's turning out to be a bad week for the British pound. While sterling/dollar touched fresh two-year highs earlier in the week, the pair has since collapsed following a flurry of disappointing UK economic data and some remarks from BoE Governor Carney yesterday that brought the prospect of a May rate hike into doubt.

The BoE chief noted that the precise timing of the next hike is not that important, and that what matters is the general path in rates. He also made reference to recent “mixed” data, Brexit uncertainties weighing on investment, and stagnant productivity. Overall, his tone was cautious, not resembling a central banker that is about to raise interest rates, thus disappointing sterling-bulls looking for signals that a hike is imminent. The implied probability for a May hike fell to 44% from 67% prior to Carney's speech, according to UK OIS.

The US dollar climbed yesterday, boosted by a surge in longer-term US Treasury yields. The 10-year yield currently hovers near 2.91%, just below its February high of 2.95%. While the greenback initially remained unfazed by the surge in yields, it eventually caught up and enjoyed some demand, with the dollar index reaching a 10-day high. Meanwhile, US stocks underperformed. Rising bond yields are typically considered harmful for stocks, which become less attractive to hold in an environment where bonds begin to offer a higher and “safer” return.

The yen was on the back foot today, declining by 0.15% and 0.1% against the dollar and euro respectively. Overnight, data showed that Japanese inflation slowed in March, as expected, confirming once again that there is no pressure on the BoJ to begin considering a stimulus-exit.

Elsewhere, the antipodean currencies underperformed, with aussie/dollar and kiwi/dollar falling by 0.2% and 0.4% correspondingly, both extending the significant losses they posted yesterday as the dollar regained its footing.

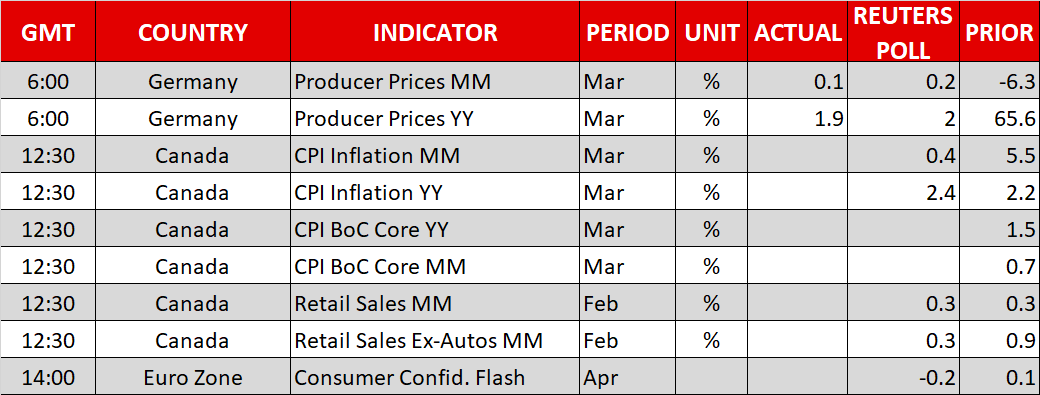

Day ahead: Canadian CPI & retail sales figures in focus; eurozone consumer confidence also due

In a relatively light day in terms of releases, most attention will be falling on Canadian inflation & retail sales figures, with data on eurozone consumer confidence also attracting some interest.

Canadian CPI figures for the month of March will be made public at 1230 GMT. Headline inflation is expected to accelerate to 2.4% y/y from February's 2.2%. An upside surprise in likely to help the Canadian dollar, though maybe not as much as would have otherwise been the case. This is owed to the Bank of Canada downplaying the significance of rising inflation, attributing it to transitory factors, in its latest meeting earlier this week. Month-on-month, headline CPI is anticipated to rise by 0.4%, a slower pace compared to February's 0.6%. Core CPI, as well as the measures of inflation utilized by the BoC in its policy-making, will also be watched by market participants.

Retail sales for February out of Canada will also be made public at 1230 GMT. Those are expected to grow at the same 0.3% rate as in January. Core retail sales, the measure that excludes automobiles, are projected to slow down to 0.3% from January's 0.9%.

The European Commission's Directorate General for Economic and Financial Affairs will release its flash estimate of eurozone consumer confidence for the month of April at 1400 GMT. Further deterioration in consumer morale is expected, with the measure expected to return to negative territory at -0.20, recording its lowest reading since October.

General Electric and Honeywell International are among companies releasing quarterly results on Friday; they will both be reporting before the US market open.

In energy markets, the US Baker Hughes oil rig count due out at 1700 GMT will be generating attention, especially in light of the recent surge in oil prices.

Regional Fed Presidents Charles Evans (non-voting FOMC member in 2018) and John Williams (voter) are among policymakers sharing remarks today. They will be speaking at 1340 GMT and 1515 GMT respectively. Meanwhile, the IMF and World Bank Spring Summit is underway, with finance ministers and central bank heads from around the world, including ECB and BoE chiefs Mario Draghi and Mark Carney attending the event.

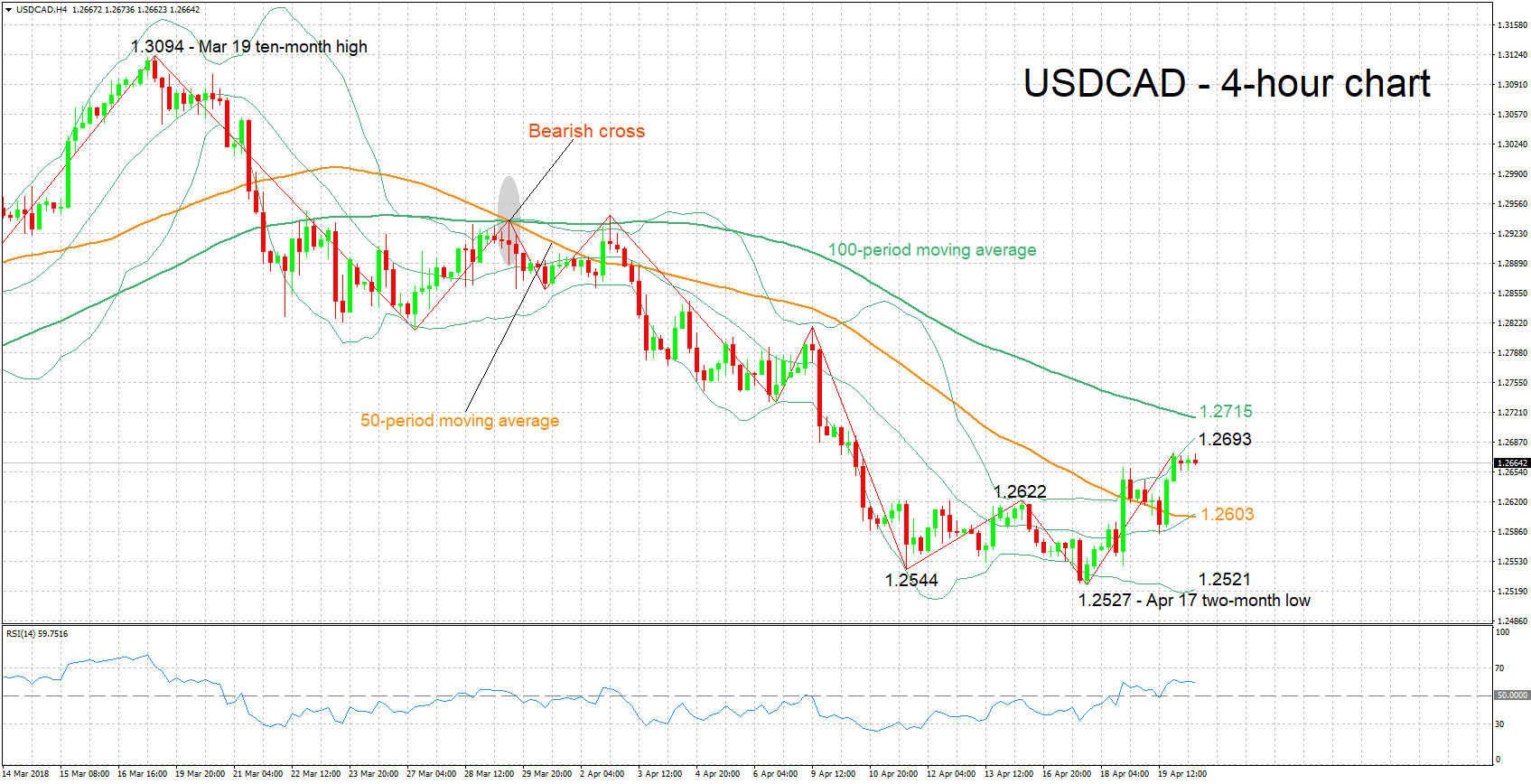

Technical Analysis: USDCAD records 10-day high; bullish momentum may be fading

USDCAD posted a 10-day high of 1.2675 on Thursday, while it is trading only a few pips below the aforementioned peak at the moment. The RSI has been rising overall in recent days, though it is currently moving sideways. This could be an early sign of easing positive momentum and a more neutral picture in the near-term.

Upbeat Canadian data later in the day are likely to support the loonie, pushing USDCAD lower. Support to declines could come around 1.2622 – a previous peak – and the current level of the 50-period moving average at 1.2603 (this is where the middle Bollinger line roughly lies as well).

Disappointing data on the other hand could push the pair higher. Resistance to advances might be met around the upper Bollinger band at 1.2693 and the 100-period MA at 1.2715.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

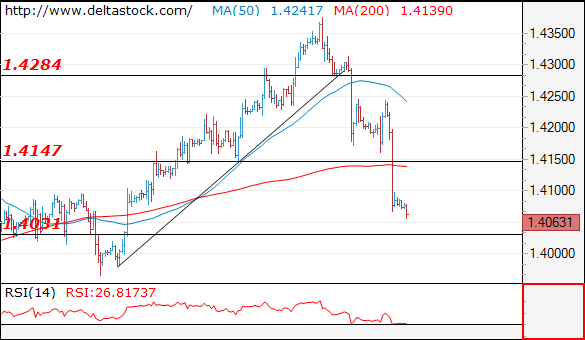

EUR/USD

Current level - 1.2339

The intraday bias is negative below 1.2360, with a risk of a slide towards 1.2280 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2360 | 1.2560 | 1.2300 | 1.2160 |

| 1.2470 | 1.2560 | 1.2260 | 1.2090 |

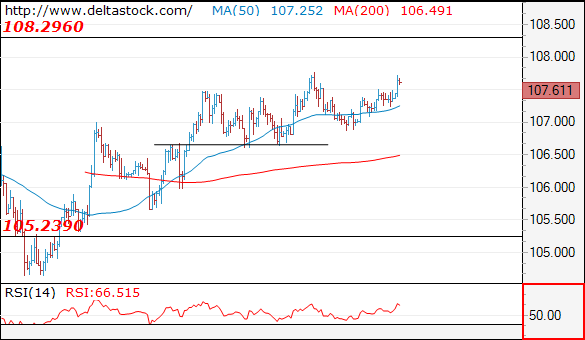

USD/JPY

USD/JPY

Current level - 107.61

The intraday bias is positive above 107.50, for a rise towards 108.30. Crucial is 107.25 low.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 107.77 | 108.30 | 107.25 | 105.20 |

| 108.30 | 110.40 | 106.60 | 104.60 |

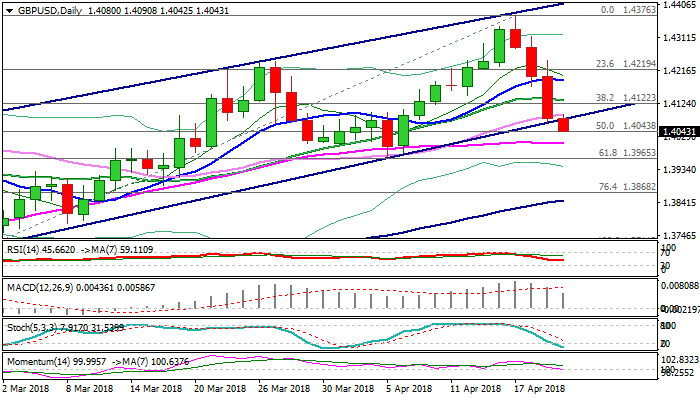

GBP/USD

GBP/USD

Current level - 1..4063

The massive sell-off has been renewed after the corrective pattern below 1.4250 and the bias is still bearish, for 1.4030 and 1.3960. Crucial on the lower frames is 1.4100 peak.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4100 | 1.4150 | 1.4030 | 1.3960 |

| 1.4150 | 1.4280 | 1.3960 | 1.3710 |

ECB Preview – Not On Draghi’s Watch

New ECB call: We expect a first rate hike of 20bp in December 2019, i.e. after Mario Draghi's reign ends (October 2019). Previously we expected 10bp in June 2019.

We postpone our estimate of the ECB's first rate hike due to increased downside risks to growth and inflation and we believe the ECB will revise its growth forecast down in its next staff projection in June.

Our key takeaway from the March ECB meeting is that the ECB will be reactive and not proactive. This was reflected in the accounts, which six times mentioned 'patience and persistence' regarding monetary policy. Added to this stance is an inflation profile that continues to be subdued and, consequently, we expect ECB to prefer taking a cautious stance.

The still-solid growth dynamics and no deflation risk support ending QE in 2018...but, in our view, a rate hike will come only once inflation is on a self-sustained path towards the target of 'below, but close to, 2%over the medium term'.

Our updated inflation expectations, which also include 2020, are 1.4%, 1.4% and 1.5% for 2018, 2019 and 2020, respectively. We expect core inflation to be 1.5%in December 2019.

Our view on next week's meeting

We expect the meeting to be relatively uneventful in terms of new information.

We expect Draghi to acknowledge the FX, trade war risks and downside risks to the ECB's growth forecasts on the back of the moderation in data as the main risks to the downside.

In particular, we expect a softer tone in the ECB's assessment on growth, which in March was 'strong and broad-based' and 'projected to expand in the near term at a somewhat faster pace'.

We present a 'buzzword bingo' at the end of this preview, which includes our view on potential change for next week.

Fixed income: The 10Y German yield has been characterised by range trading. Our tactical trading recommendation is Buy Bunds if the yield is close to 0.8% and sell them if it is close to 0.4%. Buy the Bund spread close to 40bp and sell when it is above 50bp.

FX: A hesitant ECB in April should help EUR/USD slide within the recent range, helped by a relatively cyclical outlook and stretched positioning. We are tactically short the cross for a 1-3M dip. However, medium term, we still project EUR/USD upside on a 6-12Mhorizon. We remain strategically long the cross via options (December 2018 expiry).

GBPUSD Holds In Red For The Fourth Straight Day, Dovish BoE Carney Dampened Hopes For Rate Hike In May

Cable hit new two-week low at 1.4044 on Friday, in extension strong fall from Thursday, when pound was hit by comments from BoE Governor Carney. The pair remains firmly in red for the fourth consecutive day and puts broader bulls under increased pressure, as today’s fresh extension lower broke below the lower boundary of bull-channel from 1.3711 and so far retraced 50% of 1.3711/1.4376 upleg.

Daily techs weakened as 10/20/30MA’s turned to bearish setup and falling 14-d momentum is attempting into negative territory.

The pair is also on track for strong bearish weekly close which is seen as negative signal.

Series of downbeat key data from UK this week (wages, CPI, retail sales) increased pressure on sterling as initial expectations for BoE rate hike in the next meeting in May faded.

Additional pressure came from BoE Governor Carney who dampened wide rate hike expectations on Thursday, saying that there were other CB meetings this year, signaling that BoE wouldn’t act in May.

Pound spiraled in late Thursday’s trading after Carney’s comments and holds firmly in red at the beginning of European trading on Friday.

Fibo 61.8% of 1.3711/1.4376 ascend).

Oversold slow stochastic on daily chart signals bear may take a breather before resuming. Broken channel support line marks initial resistance at 1.4079, reinforced by 30SMA (1.4092), with extended upticks to be capped by strong barriers at 1.4030 zone (20SMA / base of thick 4-hr cloud).

Res: 1.4076, 1.4092, 1.4130, 1.4189

Sup: 1.4010, 1.4000, 1.3965, 1.3944

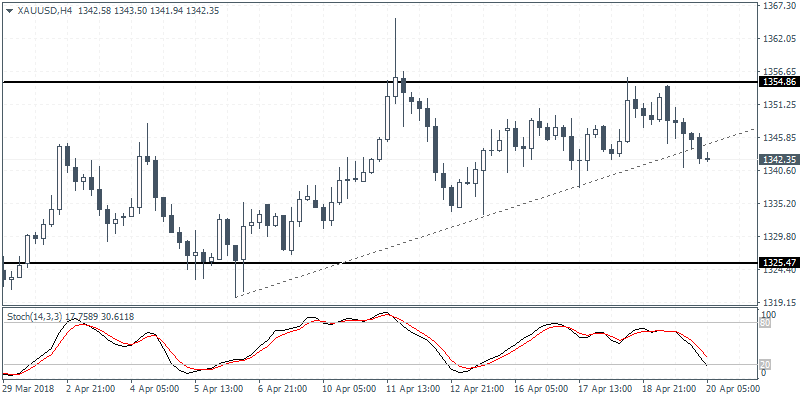

XAUUSD Intraday Analysis

XAUUSD (1342.35): Gold prices were trading weak yesterday as the intraday rally to test the resistance level at 1354 failed. On the 4-hour chart, the rising trend is currently being breached. A convincing close below the minor rising trend line could signal a move to the downside. Gold prices could be seen testing the lower main support at 1325 level. However, given the ranging conditions in the markets, we expect to see some consolidating taking place. To the upside, further gains can be expected only on a breakout above 1354 level of resistance.

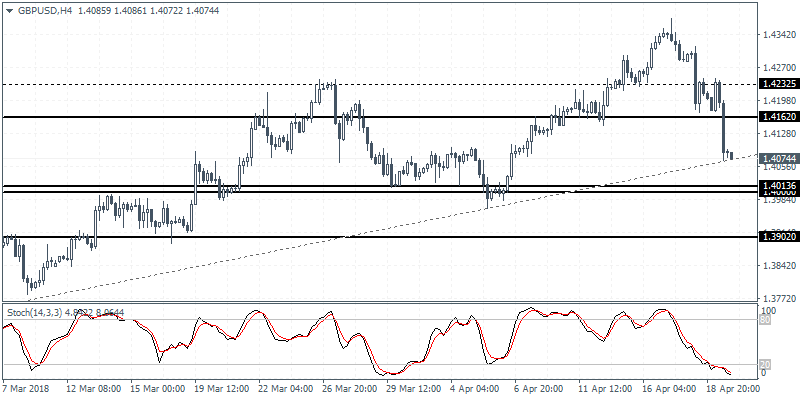

GBPUSD Intraday Analysis

GBPUSD (1.4074): The British pound briefly consolidated below the 1.4232 and 1.4162 levels before giving up the gains. Price action was seen closing strongly below the main support at 1.4162. We expect the bearish trend to push prices lower towards testing the support level at 1.4013 - 1.4000 level. In the near term, any reversals are likely to be a pullback to the decline. There is a possibility for GBPUSD to retrace the losses to test the price level at 1.4162. With prices at the rising trend line, we expect to see a modest rebound in the near term with the downside bias holding strong.

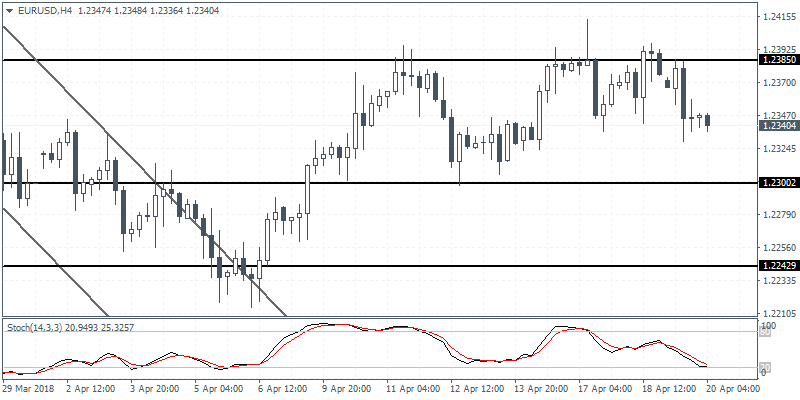

EURUSD Intraday Analysis

EURUSD (1.2340): The EURUSD was seen giving up the gains after another test to 1.2385 failing to push prices higher. The euro currency gave up the gains and is seen pushing lower in the near term. The support level at 1.2300 is likely to be the downside target. However, in the medium term, EURUSD could remain range bound within the current price levels. To the downside, a breakdown below 1.2300 could signal further losses.

USD Bounces Back, Canada Inflation Awaited

The UK's retail sales data showed a larger than expected decline. Retail sales in March fell sharply 1.2% on the month. This was larger than the expected decline of 0.5% that was forecast by economists. The declines also reversed the 0.8% increase from the previous month.

Data from the U.S. showed that the Philly Fed manufacturing index of 23.2. This was weaker than the expected forecast of 20.8 and higher than the previous month's increase of 22.3.

Looking ahead, the economic calendar will see the release of the Canadian inflation data. Forecasts point 0.4% increase on the month. This was slower than the 0.6% increase compared to the previous month. Retail sales data is also expected to be released today. Economists forecast that retail sales rose at a slower pace of 0.4% compared to 0.9% increase compared to the month before.

Later in the day, the FOMC Member, Williams is also expected to speak.