Sample Category Title

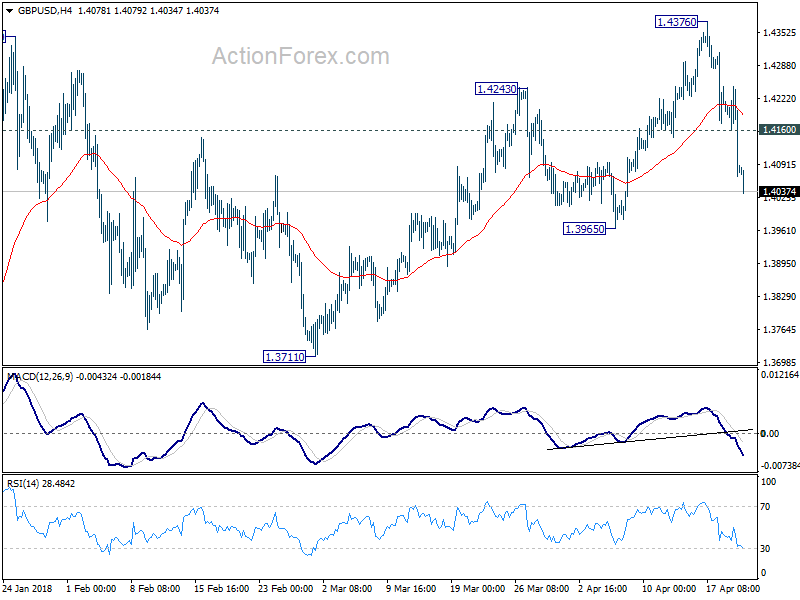

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4016; (P) 1.4131; (R1) 1.4195; More...

GBP/USD's fall from 1.4376 accelerates to as low as 1.4039 so far. The strong break of 1.4144 firstly indicate short term topping. And considering bearish divergence condition in daily MACD, it's also an early sign of medium term topping. Intraday bias is turned to the downside for 1.3965 support first. Break will pave the way to retest 1.3711 key support level On the upside, above 1.4160 minor resistance will turn focus back to 1.4376 instead.

In the bigger picture, rise from 1.1946 (2016 low) is still in progress . It is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. We'd continue to favor this medium term bullish view as long as 1.3711 support holds, even in case of deep pull back.

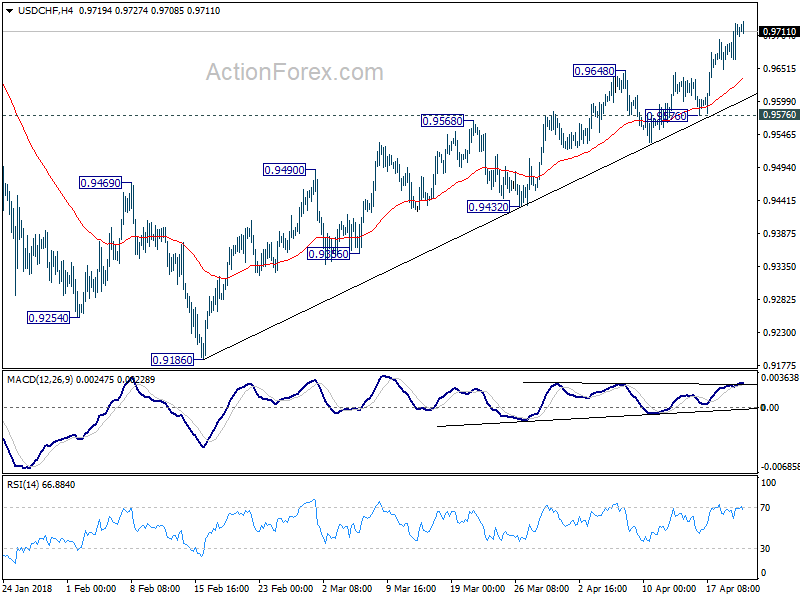

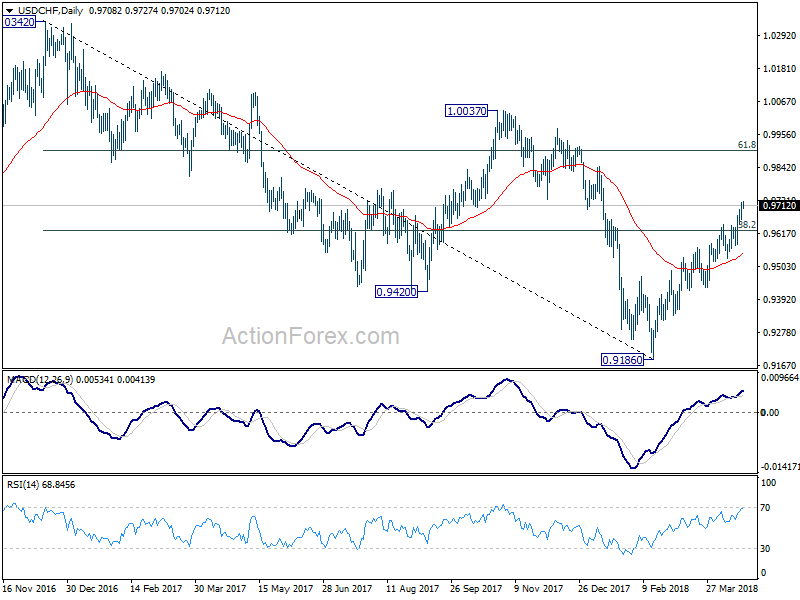

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9677; (P) 0.9700; (R1) 0.9735; More...

USD/CHF's rally resumed after brief retreat and intraday bias is back on the upside. Current rise 0.9186 is expected to target 0.9900 fibonacci level next. On the downside, break of 0.9576 support is needed to indicate short term topping. Otherwise, outlook will remain bullish even in case of retreat.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next.

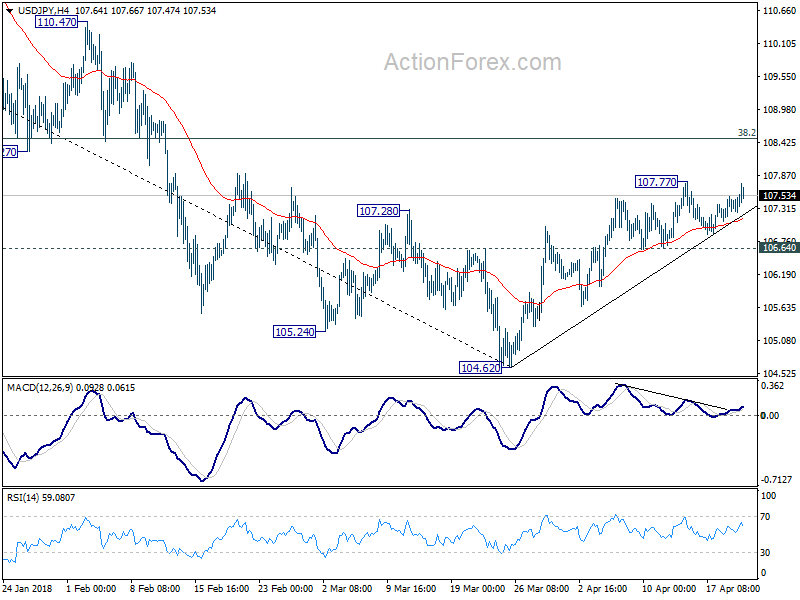

USD/JPY Daily Outlook

Daily Pivots: (S1) 107.17; (P) 107.34; (R1) 107.53; More...

Intraday bias in USD/JPY remains neutral at this point. Break of 107.77 will target 38.2% retracement of 114.73 to 104.62 at 108.48 which is close to 108.12. This level is crucial in determining the medium outlook. On the downside, break of 106.64, however, will indicate the rebound from 104.62 has completed. And in that case, bias will be turned back to the downside for retesting 104.62.

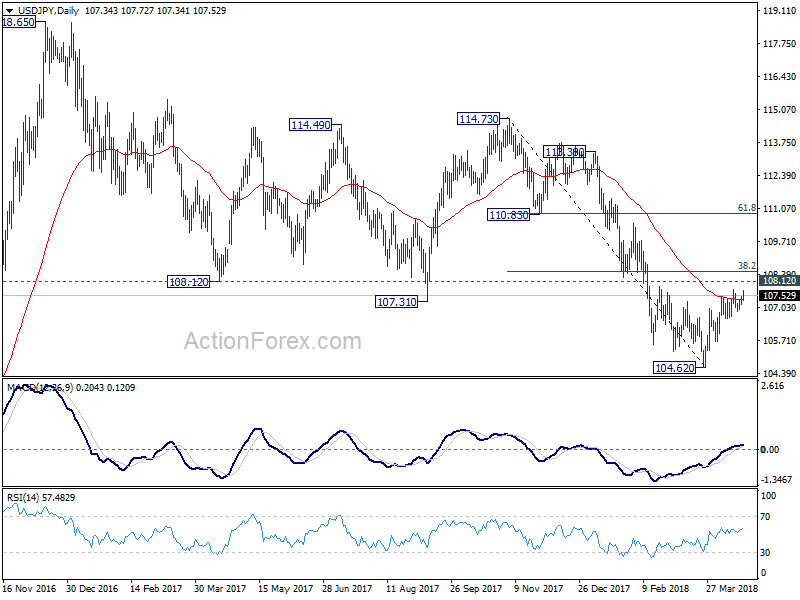

In the bigger picture, as long as 108.12 support turned resistance holds, the medium term down trend from 118.65 (2016 high) should still continue lower, at least to retest 98.97 (2016 low). However, sustained break of 108.12 will be an early sign of medium term reversal. In that case, further rise would be seen to 114.73 resistance to confirm completion of the fall from 118.65.

In the bigger picture, as long as 108.12 support turned resistance holds, the medium term down trend from 118.65 (2016 high) should still continue lower, at least to retest 98.97 (2016 low). However, sustained break of 108.12 will be an early sign of medium term reversal. In that case, further rise would be seen to 114.73 resistance to confirm completion of the fall from 118.65.

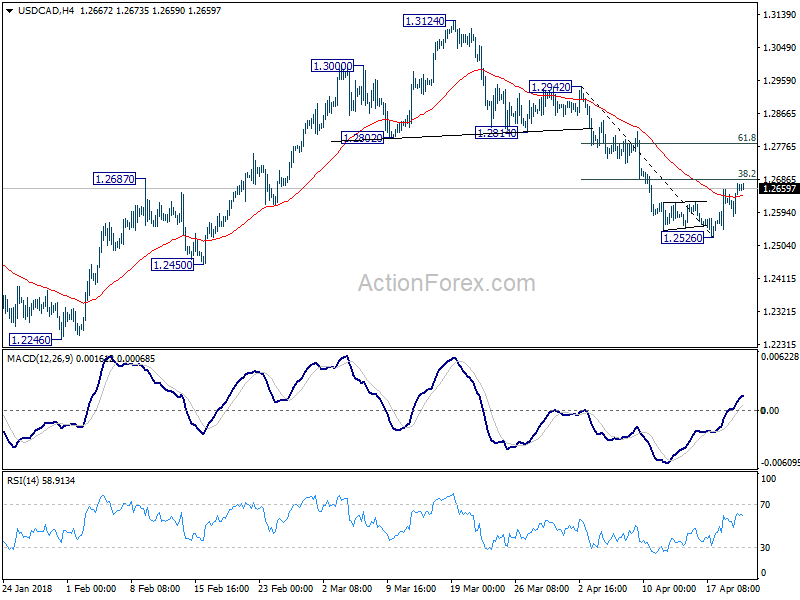

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2611; (P) 1.2643; (R1) 1.2702; More....

Intraday bias in USD/CAD remains mildly on the upside. Rebound from 1.2526 short term bottom should extend to 38.2% retracement of 1.2942 to 1.2526 at 1.2685, or even further to 55 day EMA (now at 1.2725). But upside should be limited well below 1.2814 support turned resistance and bring fall resumption. We'd expect decline from 1.3124 to extend later to 1.2061/2246 support zone.

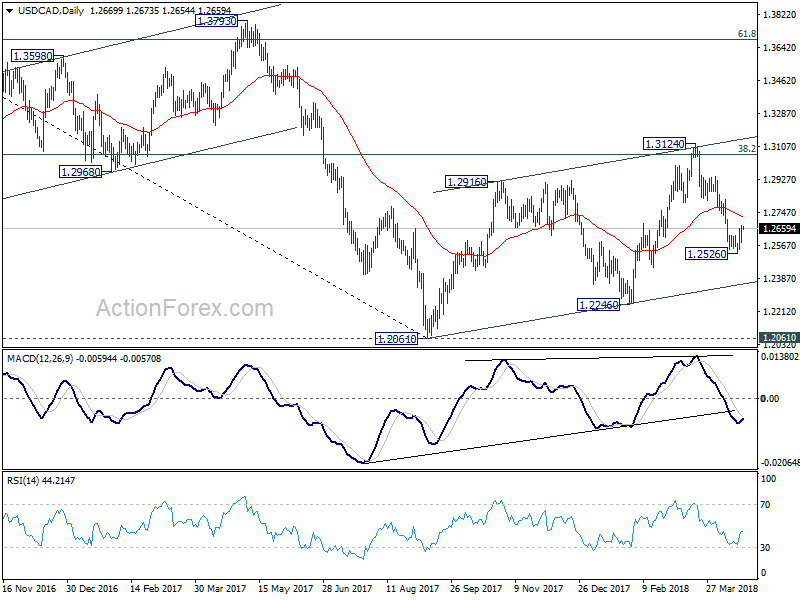

In the bigger picture, current development turns favors to the case that rise from 1.2061 is a corrective three wave pattern. It could have completed at 1.3124 after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Focus is now back on 1.2061 and 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Decisive break there will resume larger down trend from 1.4689 (2016 high) to 61.8% retracement of 0.9406 to 1.4689 at 1.1424.

In the bigger picture, current development turns favors to the case that rise from 1.2061 is a corrective three wave pattern. It could have completed at 1.3124 after hitting 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Focus is now back on 1.2061 and 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Decisive break there will resume larger down trend from 1.4689 (2016 high) to 61.8% retracement of 0.9406 to 1.4689 at 1.1424.

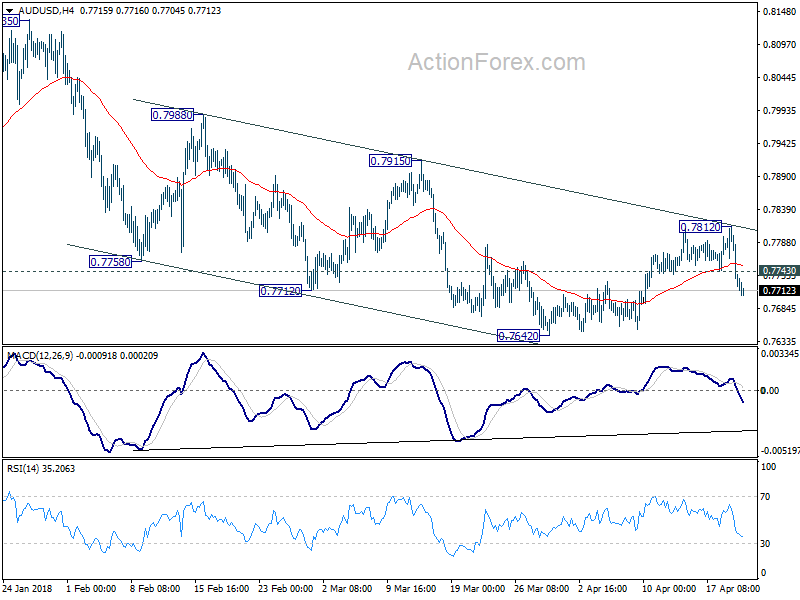

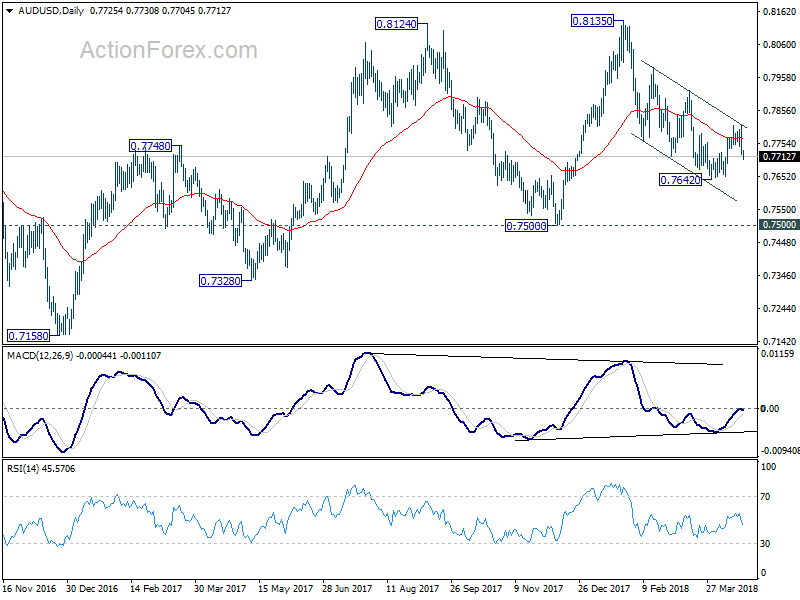

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7693; (P) 0.7753; (R1) 0.7787; More...

AUD/USD faced strong rejection from near term falling channel resistance. Break of 0.7743 indicates that rebound from 0.7642 has completed at 0.7812. And larger fall from 0.8135 might be resuming. Intraday bias is turned back to the downside for 0.7642 first. Break will target 0.7500 key support level.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

BOE Governor Carney Sends GBP Tumbling With Rate Hike Comments

Bank of England Governor, Mark Carney, was interviewed by the BBC yesterday, where he made the comment that he didn’t want to get too focused on the precise timing of the next hike and that it’s more about the general path. He went on to say that the market should prepare for a few interest rate rises over the next few years, that economic data has been mixed and any rate hikes would be gradual and could be delayed by Brexit. He also noted that uncertainty around Brexit had prevented what would have been a surge of investment and that productivity is not increasing, which would limit the rate at which wages could pick up. The comments sent shockwaves through GBP pairs, with GBPUSD falling from 1.41989 to 1.40799 in only one hour. GBPJPY fell from 152.421 to a session low of 151.078, while EURGBP jumped from 0.86921 to 0.87699.

The US Bond market also a point of concern, with the 10-year approaching the 3.0% level once again. This played a part in dragging equity markets lower, as the yield curve steepened. EURUSD fell to the lowest levels of the day in yesterday’s trading, down from 1.23815 to 1.23279 as a result.

UK Retail Sales (YoY) (Mar) was 1.1% v an expected 2.0%, from 1.5% previously. Retail Sales (MoM) (Mar) was -1.2% v an expected -0.5%, against a prior 0.8%. Retail Sales Ex-Fuel (YoY) (Mar) was 1.1% v an expected 1.4%, from 1.1% previously, which was revised up to 1.2%. Retail Sales Ex-Fuel (MoM) (Mar) was -0.5% v an expected -0.4%, against a prior 0.6%, which was revised down to 0.4%. Retail sales numbers on all metrics missed expectations and fell in yesterday’s data release. This was impacted by the unusually cold weather conditions during March, which prevented shoppers getting out, meaning that it is likely a temporary drop that traders can explain away. EURGBP fell from 0.87320 to 0.87173 following this data release.

FOMC Member Brainard spoke about regulatory reform at the Global Finance Forum, in Washington DC. She made the following comments: It is too early to revisit bank capital rules. She added that it may be appropriate to require banks to build a counter-cyclical capital buffer. She warned of growing pro-cyclical pressures, including rising asset prices and leverage. She also said that inflation is well anchored by some signs of imbalances.

US Continuing Jobless Claims (Apr 6) was 1.863M v an expected 1.848M, against a previous 1.871M, which was revised up to 1.878M. Initial Jobless Claims (Apr 13) was 232K v an expected 230K, from 233K previously. Philadelphia Fed Manufacturing Survey (Mar) was 23.2 v an expected 20.1, against 22.3 previously. The data showed a slight increase in unemployment for the third month in a row, coming in above expectations. USDJPY fell from 107.391 to 107.322 following this data.

FOMC Member Mester spoke about the economic outlook and monetary policy at the University of Pittsburgh’s Joseph M. Katz Graduate School of Business. Audience questions followed and she made the following comments: Further rate hikes are appropriate this year and next and she said gradual rate hikes would help avoid overheating and financial stability risks. She sees more than 2.5% GDP growth this year. She said that financial market volatility, trade and geopolitics pose risks but have not caused a change in the outlook. She said that monetary policy and financial conditions were still accommodative. She added that the U.S. is 'slightly beyond” full employment. She sees inflation moving up to 2% over the next 1-2 years.

Japanese National Consumer Price Index (YoY) (Mar) was as expected at 1.1%, against a prior 1.5%. National Consumer Price Index Ex-Fresh Food (YoY) (Mar) was also as expected, at 0.9%, against a prior 1.0%. National Consumer Price Index Ex Food and Energy (YoY) (Mar) also came in as expected, unchanged at 0.5%. USDJPY moved higher from 107.379 to 107.728 after this data release.

EURUSD is down -0.02% overnight, trading around 1.23432.

USDJPY is up 0.25% in early session trading at around 107.625.

GBPUSD is down -0.08% this morning, trading around 1.40691.

USDCAD is down -0.04%, trading around 1.26655.

Gold is down -0.19% in early morning trading at around $1,342.90.

WTI is down -0.06% this morning, trading around $68.14.

Canadian Retail Sales And CPI Data On The Agenda Today

At 09:30 GMT, UK MPC Member Saunders is due to speak at the University of Strathclyde’s Fraser of Allander Institute, in Glasgow. Comments made may affect GBP pairs.

At 11:30 GMT, German Buba President Weidmann is due to participate in a press conference at the International Monetary Fund’s Spring Meeting, in Washington DC. EUR pairs may be impacted by any comments made.

At 12:30 GMT, Canadian Consumer Price Index (MoM) (Mar) is expected to be 0.4% against 0.6% previously. BOC Consumer Price Index Core (YoY) (Mar) is expected to be unchanged at 1.5%. BOC Consumer Price Index Core (MoM) (Mar) is expected at 0.2% v a prior 0.7%. Consumer Price Index (YoY) (Mar) is expected to be 2.4% against 2.2% previously. Consumer Price Index – Core (MoM) (Mar) came in at 0.2% previously. Retail Sales Ex-Autos (MoM) (Feb) is expected to be 0.3% against 0.9% previously. Retail Sales (MoM) (Feb) is expected to be unchanged at 0.3%. There is a very mixed forecast expected across these data points, which may result in a choppy reaction from the markets, as the data paints an uncertain picture. However, any clear assumption that can be extracted from the data will give traders something to run with. Retail sales are expected to have a stronger showing after missing expectations over last two months but Core Retail Sales are forecasted to show a drop. CAD crosses may be affected by this release, especially if the data deviates from expectations.

At 15:15 GMT, FOMC Member Williams is due to speak at a fireside chat hosted by the Fisher Center for Real Estate and Urban Economics, in California. USD pairs may be impacted by any comments made.

At 17:00 GMT, the Baker Hughes US Oil Rig Count will be released. The prior number last Friday showed that there were 815 oil rigs in operation, up from 808 the previous week. With oil currently at the highest levels in recent times, on the back of a bigger than expected draw in inventories on Wednesday, this data may set the tone for traders as they look to the week ahead.

Currencies: EUR/USD Rebound To Slow Post-Fed Minutes

Rates: Bund ends consolidation phase

Core bonds lost ground yesterday with Bunds underperforming US Treasuries. The move suggests an end of the consolidation phase for the Bund which started end March. Rising inflation expectations can send the German yield further up. The US 10-yr yield approaches the upper bound of the 2.7%-2.95% trading band.

Currencies: BoE's Carney blocks sterling rebound as he questions May rate hike

Yesterday, the dollar got the benefit of the doubt even as interest rate differentials moved in favour of the euro. Today, the eco calendar is thin. Even so, some further repositioning in favour of the dollar might be on the cards. Sterling finally tumbled sharply lower as BoE's Carney indicated that the BoE hasn't decided on the timing of a next rate hike.

The Sunrise Headlines

- US stock markets lost 0.35% to 0.78% yesterday with Nasdaq underperforming on a disappointing outlook from Apple's main chip supplier. Asian bourses trade negative as well with China underperforming (> -1%).

- BoE Carney indicated that financial markets were wrong to believe an interest rate rise in May was a foregone conclusion. Sterling lost ground with EUR/GBP north of 0.8750 and GBP/USD below 1.41.

- EU officials are set to reject a potential UK solution to the crucial issue of what happens to the Irish border after Brexit (maintaining an invisible border to the whole of the UK), deepening the stalemate in negotiations. (BB)

- The Trump administration is considering declaring a national economic emergency to impose new restrictions on Chinese investment as part of a trade crackdown on Beijing, according to a senior US Treasury official. (FT)

- Japanese inflation slowed for the first time since July 2016. The key national CPI ex fresh food rose by 0.9% Y/Y, from 1% Y/Y in February, providing the BoJ with a fair enough reason to maintain its stimulus.

- German economic growth could slow slightly in the first quarter, but the upswing in Europe's largest economy remains robust and broad-based thanks to strong domestic and foreign demand, the finance ministry said. (Reuters)

- Today's eco calendar contains German PPI data and EMU consumer confidence. Chicago Fed Evans is scheduled to speak.

Currencies: EUR/USD Rebound To Slow Post-Fed Minutes

Carney blocks sterling rebound

There was initially again no clear guide for USD-trading yesterday. EUR/USD held a tight range in the upper half of the 1.23 big figure. The dollar finally captured a better bid later in the session. We didn't see any high profile news. The move coincided with a slight decline in the oil price and with a correction on US equity markets. The dollar maybe played some kind of temporary safe haven role. EUR/USD close the session at 1.2345. USD/JPY finished little changed at 107.37.

Asian equities remain in the defensive overnight. Technology shares take the lead in the decline. China underperforms again. Japanese March inflation data remain soft, but were in line with expectations (0.9% Y/Y for the measure ex Fresh food). The moves in the major USD cross rates are modest. Even so, the USD currency is holding up well given the volatility/uncertainty in several other markets.

There are hardly any important data in EMU or in the US today. We aren't convinced that this will be a guarantee for calm trading. Yesterday's moves in core bonds suggest that investors are adapting positions. The dollar held up well in this process even as the interest rates moved in favour of the euro. We look out whether this pattern persists. A further catching up move with European bonds underperforming Treasuries is not per se a positive for the euro. We also keep an eye at the gyrations in commodities and equities. The jury is still out, but in a short-term perspective, we have the impression that a renewed rise in volatility might benefit the dollar rather than euro.

Sterling (EUR/GBP) initially held near the levels after Wednesday's soft inflation data. March UK retail sales disappointed again. However, poor weather conditions were to blame. The market assumed that soft data wouldn't question a May rate hike anymore. Sterling even rebound with EUR/GBP returning to the 0.87 area. BoE's Carney created doubts after the European close by indicating that the BoE hasn't decided on the timing of a next rate hike yet. Sterling was hammered. EUR/GBP jumped to the 0.8765/70 area. There are no UK eco data today. Yesterday's comments of BoE Carney broke the sterling positive momentum. The extensive test of the 0.8650 range bottom is rejected. Short-term, some further unwinding of sterling longs ahead of the BoE meeting might be on the cards. Brexit noise might also resurface.

USD (tradeweighted): USD to trend higher in the range?

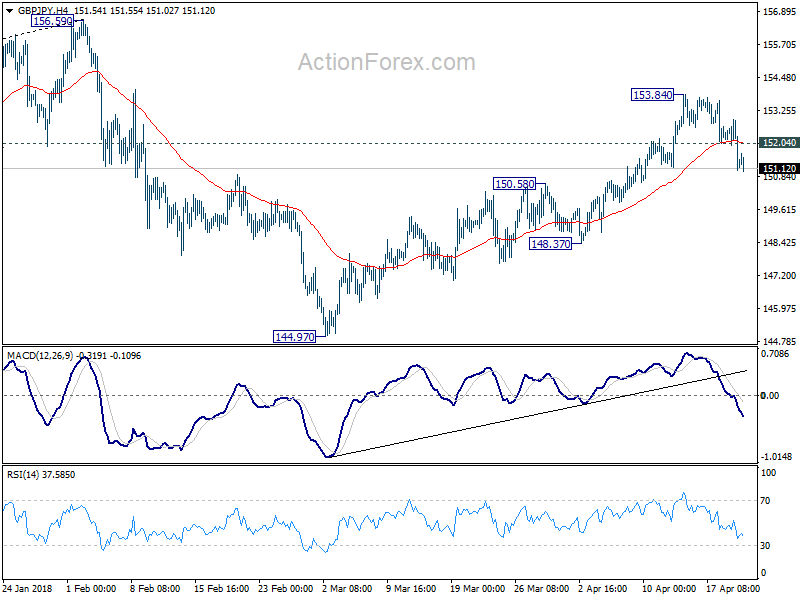

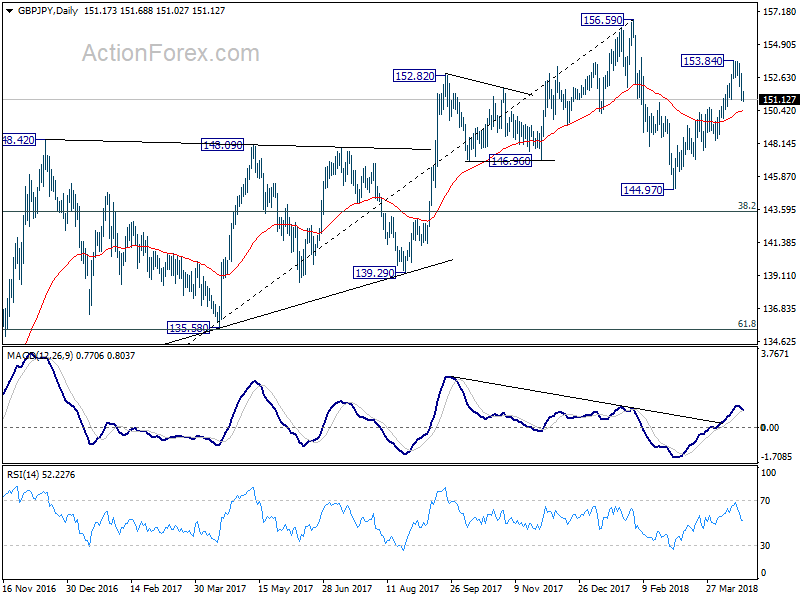

GBP/JPY Daily Outlook

Daily Pivots: (S1) 150.52; (P) 151.73; (R1) 152.39; More...

GBP/JPY's fall from 153.84 continues today and breach of 151.15 minor support now suggests that rebound from 144.97 has completed. Intraday bias is turned to the downside for 148.37 support first. Break will pave the way for retesting 144.97 low. On the upside, above 152.04 minor resistance will turn focus back to 153.84 instead.

In the bigger picture, price actions from 156.59 are viewed as a corrective pattern. For now, we'd expect at least one more fall for 38.2% retracement of 122.36 to 156.59 at 143.51 before the consolidation completed. Though, firm break of 156.59 will resume whole up trend from 122.36 (2016 low) to 50% retracement of 195.86 (2015high) to 122.36 at 159.11 next.

In the bigger picture, price actions from 156.59 are viewed as a corrective pattern. For now, we'd expect at least one more fall for 38.2% retracement of 122.36 to 156.59 at 143.51 before the consolidation completed. Though, firm break of 156.59 will resume whole up trend from 122.36 (2016 low) to 50% retracement of 195.86 (2015high) to 122.36 at 159.11 next.

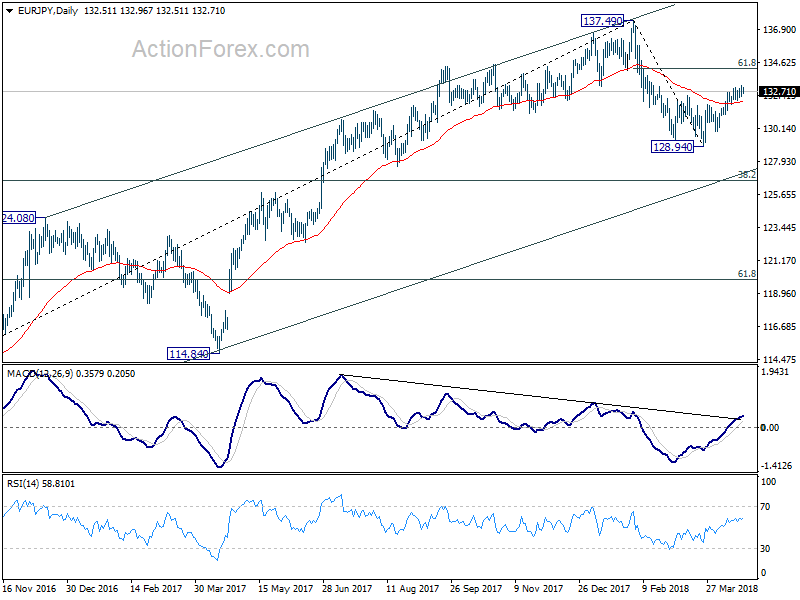

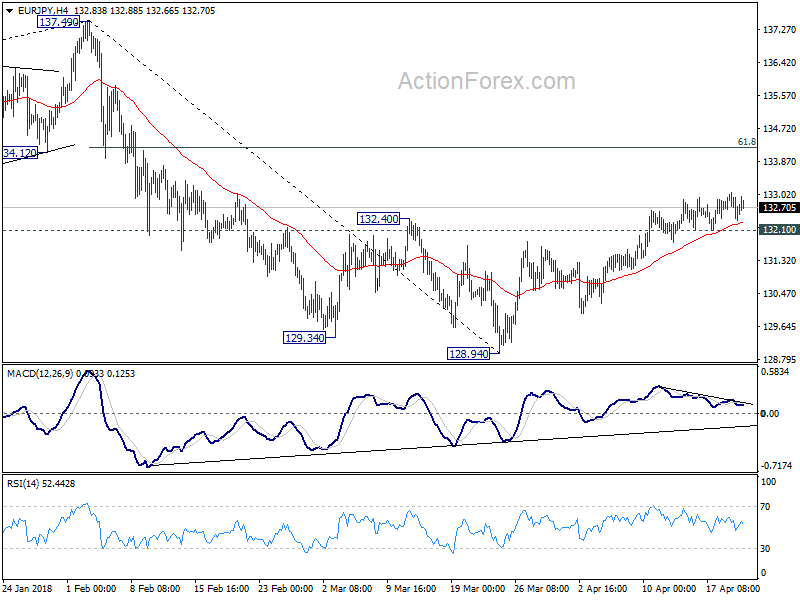

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.23; (P) 132.65; (R1) 132.96; More....

EUR/JPY continues to lose upside momentum as seen in 4 hour MACD. But with 132.10 minor support intact, further rise could be seen. Nonetheless, upside will now likely be limited by 61.8% retracement of 137.49 to 128.94 at 134.22 and below. On the downside, below 132.10 minor support will suggests that the rebound from 128.94 might have completed. And, intraday bias will be turned back to the downside for retesting 128.94 low.

In the bigger picture, price action from 137.49 medium term top are developing into a corrective pattern. Strong support from 55 week EMA (now at 129.91) suggests that the first leg has completed at 128.94 already. Nonetheless, break of 137.49 is needed to confirm resumption of the rise from 109.03 (2016 low). Otherwise, we'd expect more corrective range trading, with risk of another fall to 38.2% retracement of 109.03 to 137.49 at 126.61 before completion.

In the bigger picture, price action from 137.49 medium term top are developing into a corrective pattern. Strong support from 55 week EMA (now at 129.91) suggests that the first leg has completed at 128.94 already. Nonetheless, break of 137.49 is needed to confirm resumption of the rise from 109.03 (2016 low). Otherwise, we'd expect more corrective range trading, with risk of another fall to 38.2% retracement of 109.03 to 137.49 at 126.61 before completion.