Sample Category Title

As Good As Gold

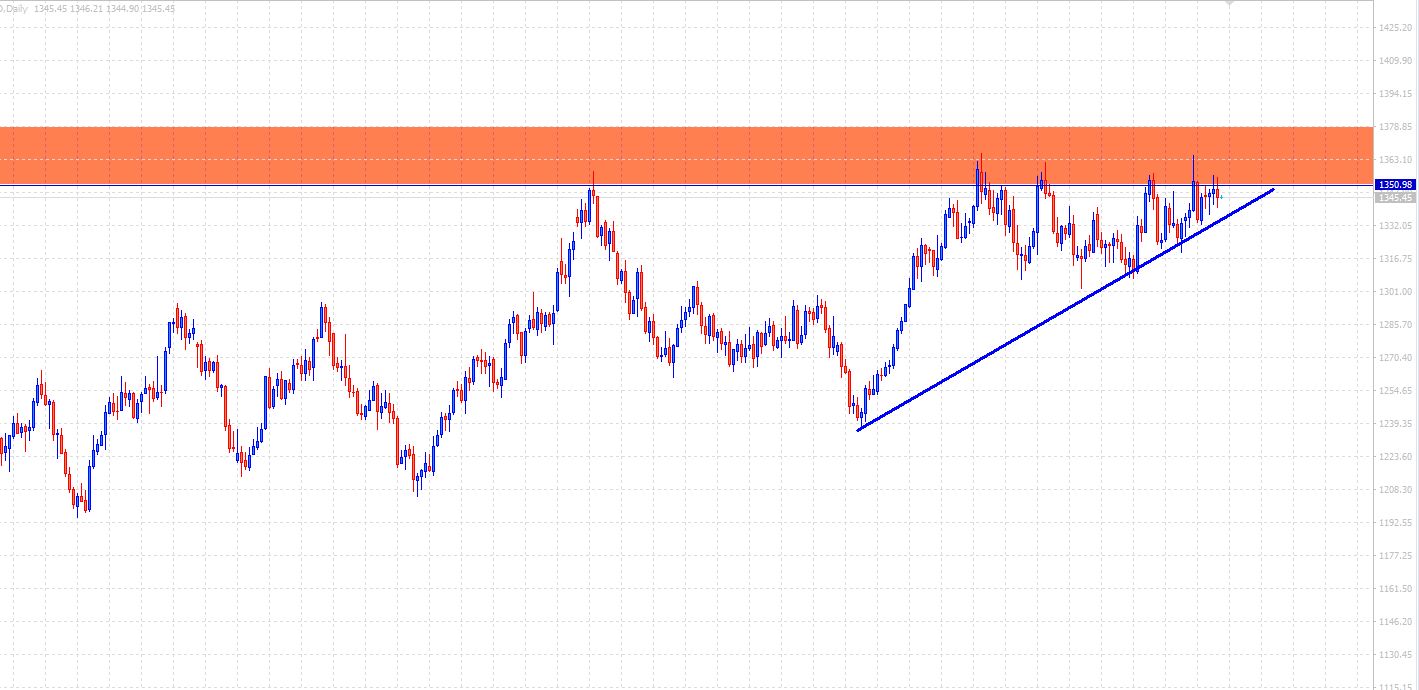

Since then, price has been playing out brilliantly and gold continues to tighten up as shown on the XAUUSD weekly chart below. You can see we're at the point now where price looks coiled to explode to the upside and there's very little resistance overhead until around the 1571 level.

Let's look at it a bit closer on the daily chart.

A convincing break above our red resistance area could indicate the beginning of a significant long term bull trend. There are a couple of ways a trader could play a setup like this. You could buy the breakout, or if you miss that you could potentially buy the retrace of price back to our breakout area.

Either way, always wait for the break or whatever you use for confirmation. To me, this is pretty much as textbook as it gets and i'll continue to watch closely.

Market Morning Briefing: Dollar Yen Has Continued Rising After Testing 107.0-106.9

STOCKS

The daily momentum as seen on the daily line charts indicate that a possible dip is coming up on the Dow (24664.89, -0.34%) in the near term. Currently trading near important levels, it is important to see if the Dow comes off from 25000 or manages to move up in the next few sessions. A rejection from 25000 looks more likely with a possibility of testing 24250 on the downside.

Dax (12567.42, -0.19%) has paused just at the daily resistance near 12600. Being an important levels, a break or dip from here would determine the next course of action. While 12600 holds, the index could come off to test 12400-12200 again; else a rise above 12600 could trigger a medium term uptrend.

22500-22550 is crucial resistance zone for Nikkei (22222.13, +0.14%) which could push the index towards 21800-21600 levels in the coming sessions. Such a dip, if seen in Nikkei could limit the upside for Dollar Yen (107.63) just now.

Shanghai (3091.35, -0.83%) moved up sharply from 3050 and is currently trading just below important levels near 3100-3150. While these levels provide some resistance, Shanghai looks bearish for the medium term. A break above 3150 could indicate some upmove in the next few sessions.

Nifty (10565.30, +0.37%) has not been able to close above the crucial resistance near 10600 and while that holds, a dip back to levels near 10400 looks likely. Sensex (34427.29, +0.28%) also seems to have made a near term top and could now fall a bit towards 34000 or lower in the coming sessions.

COMMODITIES

Brent (73.83) is trading near crucial levels. Although we had mentioned a rise towards 76 yesterday, there is an interim resistance near 74 which is likely to keep the prices stable or push it down towards 72. Near term likely to be stable if not very bearish.

Nymex WTI (68.37) has important weekly resistance near 69 (revised from yesterday’s mentioned 70) which is likely to hold just now, either keeping the WTI price stable or pushing it down towards 67-66 levels. Upside is likely to be limited at 69 just now.

Gold (1344.71) is limiting itself in a narrow range of 1340-1370 for the near term. 1340 is a decent near term support while 1370 is an important resistance which the index is finding difficult to break just now. Some sideways consolidation is possible for a few sessions.

Copper (3.1320) has immediate resistance near 3.15-3.17 and while that holds, Copper is likely to come off towards 3.10-3.07 in the near term. A break above 3.15-3.17 is needed to move higher towards 3.20/25 (less likely).

FOREX

Dollar index (89.95) has risen past 13 days and 21 days moving average lines on daily line chart near 89.8 and could now test higher resistance on 3 day candles near 90.00-90.25, after which it could dip back towards 89.50-89.25.

Euro (1.2340): Euro is testing the 21 moving averages on daily and 3 day line charts near 1.233-1.235 and could dip lower to support near 1.23 on daily candles. A break of 1.23 (if it happens) could be very bearish. Our preference is for the support to hold, leading to a bounce back towards 1.24 and higher.

Dollar Yen (107.65) has continued rising after testing 107.0-106.9 earlier this week and could move up further near previous high of 107.78. It needs to be seen if Dollar Yen turns bearish from its previous high or moves up further towards 109 (seen as 21 week moving average on weekly line chart).

Euro Yen (132.84), as per expectation, has stayed below resistance near 133, being provided by 21 moving average on the weekly line chart and also seen as resistance on daily and 3 day candles. This resistance could be broken if Dollar Yen continues to move up towards 109 and Euro bounces towards 1.24. The maximum upside for Euro Yen in the near term could be 135-138 ( corresponding to 109-110 on Dollar Yen and 1.25-1.26 on Euro); after which it could turn bearish.

Pound (1.408) has dipped very quickly to test support near 1.410 on daily line chart after testing strong resistance near 1.43-1.435 (on 3 day line chart). If it breaks this support, there is lower support near 1.40 on daily candles. Further lower, there is crucial long term support level near 1.38-39 on weekly line chart, whose break could make Pound very bearish. If current support near 1.41-1.40 holds, Pound may attempt a rise towards 1.46 (crucial long term resistance on weekly line chart).

Dollar Rupee (65.795): Target of 66.15 could come earlier than end-April/ early-May also.

INTEREST RATES

In the past few days, US yields have continued rising in response to crucial US economic indicators throwing up improved numbers. Industrial Production, Capacity Utilization, US Retail Sales data, unemployment claims data and the Fed minutes had all indicated a growing US economy. In addition, rising commodity prices (specially, Crude) has increased inflation expectations and is fuelling the rise in US (and even German) yields.

US 10 Yr Yield (2.9173%), 30 Yr (3.1073%), 5 Yr (2.76%), 2 Yr (2.43%):

The US 2 year yield has reached its highest levels since 2008 and could rise higher in May. Upside could be restricted to 2.5% in the near term.

The 10 Year yield (2.9173%) is very close to resistance near 2.92% on medium term chart and could dip towards 2.85%-2.825% from here in the next week. It is likely to creep up towards 2.95% in May as long as crude prices remain elevated.

The 30 yr yield as we expected, has moved up further towards 3.1%. It could move up slightly more towards 3.12% (even 3.15%) and then dip.

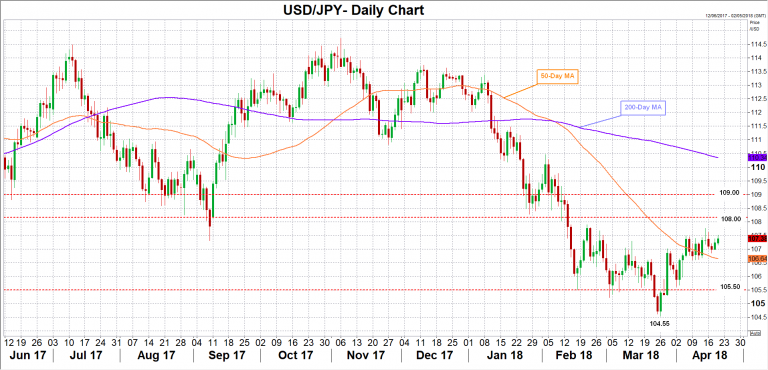

USD/JPY Trading Above Crucial Support At 107.00

Key Highlights

- The US Dollar is trading in a bullish zone above the 107.00 support against the Japanese Yen.

- There are two important bullish trend lines forming with support at 107.00-10 on the 4-hours chart of USD/JPY.

- The US Initial Jobless Claims for the week ending April 14, 2018 declined from 233K to 232K.

- Japan’s National CPI in March 2018 (YoY) increased 1.1%, similar to the forecast.

USDJPY Technical Analysis

This past week, the US Dollar remained well supported above the 106.50 level against the Japanese Yen. This week, the USD/JPY pair is forming a crucial support base above the 107.00 level.

Looking at the 4-hours chart, there are two important bullish trend lines forming with support at 107.00-10. The pair recently traded as high as 107.77 before correcting lower. It declined and tested the 106.90 level along with the bullish trend lines.

Downsides were limited, resulting in an upside move above 107.00. The pair moved above the 50% Fib retracement level of the last drop from the 107.77 high to 106.88 low.

At the moment, the pair is positioned well above the 100 simple moving average (red, 4-hours), which is a positive sign. As long as the pair is above 107.00 and the 100 SMA, it may perhaps continue to move higher.

On the upside, the 107.60-70 area is a key barrier for more gains. Above 107.70, the pair will most likely break the 108.00 level for more upsides.

Recently, the US Initial Jobless Claims report for the week ending April 14, 2018 was released by the US Department of Labor. The market was looking was a decline from the previous reading of 233K to 230K.

However, the result was on the lower side as there was only 1K decline in claims from 233K to 232K.

The report added:

The 4-week moving average was 231,250, an increase of 1,250 from the previous week’s unrevised average of 230,000.

Overall, the market sentiment is favoring the US Dollar and USD/JPY is likely to extend upsides in the near term.

Economic Releases to Watch Today

- Canadian Consumer Price Index March 2018 (MoM) – Forecast +0.4%, versus +0.6% previous.

- Canadian Consumer Price Index March 2018 (YoY) – Forecast +2.4%, versus +2.2% previous.

- Canadian Retail Sales Feb 2018 (MoM) – Forecast +0.3%, versus +0.3% previous.

- Canadian Retail Sales ex Autos Feb 2018 (MoM) – Forecast +0.3%, versus +0.9% previous.

Where Do We Go From Here ?

Where do we go from here?

US stock market had its first loss of the week as technology companies and consumer products went south.

Overall earnings were quite bullish for markets, but there are the usual post earnings pessimism permeating markets that this is about as good as its going to get

But investors should also take note of surging oil prices and the possible inflationary impact they could have on sending the US yield curve higher, which could prove to be the markets undoing.

Oil Prices

Saudi Arabia with OPEC’s support is looking to draw a new line in the sand for Oil prices and added another level of intrigue to the already bullish narrative. Now whether this is merely noise or a valid bullish signal, I expect this debate to continue. But there is a multitude of the domestic reason for Saudi to chase this dream beyond Aramco IPO.

Back in the real world, traders are still revelling in yesterday’s EIA inventories data which were conclusively a bullish signal. While the market is trading off overnight highs it’s more likley a case of traders trimming positions heads of potential weekend headline risk.

The civil war in Syria and threat of Yemeni rebels targeting the region’s top oil exporter Saudi Arabia with rockets has traders paying the geopolitical risk premium which should keep downticks in check. And all the while oil investors are playing the waiting game for probable oil sanctions against Iran.

All this makes for a compelling list of bullish narratives.

Gold Prices

The uncertainty over geopolitical risk and trade war tension has moved to the back burner this week and has made for a less compelling argument in the gold market. Traders are rehashing old topics amidst reasons to stay long into the weekend, but drawing few if any conclusions

Unless unexpected headlines hit the markets, we’re likely to remain within tight trading ranges but perhaps gravitate to the lower end of the spectrum as traders pair back long positions ahead of the weekend

The Euro

A quiet 24 hours for EURUSD, as the EURUSD seems exceptionally fluid on a 1.24 handle but lacking in momentum in either direction.

The Japanese Yen

Trump and Abe have come across as long-lost fraternal bothers and the markets; especially the Nikkei took notice. But despite the abundance of reason to go long USDJPY, the market remains exceptionally defensive knowing that one headline can upset the apple cart

The British Pound

Flip Flop tick tock, BOE Carney walked back all the hawkishness suggesting interest rates will go up over the next few years but gave no specific timeline which caused anyone who was banking on a May rate hike to head for the exits.

The Malaysian Ringgit

$Asia continues to trade on mixed themes, but the Ringgit remains exceptionally muted due to the building election risk. But with currency markets, including G-10 mired in sideways activity it’s unlikely we will see any significant shift in the local note today.

Eco Data 4/20/18

[php_everywhere instance="1"]

Retail Sales Plunge But Pound Unscathed

The British pound has steadied in the Thursday session, after considerable losses on Wednesday. In North American trade, GBP/USD is trading at 1.4205, down 0.01% on the day. On the release front, British Retail Sales plunged 1.2%, worse than the estimate of -0.5%. US unemployment claims ticked lower to 232 thousand, close to the estimate of 230 thousand. As well, the Philly Fed Manufacturing Index improved to 23.2 thousand, easily beating the estimate of 20.8 points.

British consumer data has been soft this week, and this will likely raise concerns about the health of the British economy. On Thursday, Retail Sales declined 1.2%, its weakest reading in three months. However, the sharp drop has been attributed to unusually bad weather in March, as blizzards hampered travel in the UK and kept consumers at home and away from shopping malls. The markets shrugged off the weak release, and the pound is unchanged on Thursday.

The pound lost ground on Wednesday, following the release of weak inflation numbers. CPI in March dropped to 2.5%, after six consecutive readings of around 3.0 percent. The soft reading surprised the markets, and the pound responded with losses. The real producer index and other inflation indicators also missed their estimates. Despite the slowdown in inflation and consumer spending, the markets still expect the Bank of England to raise rates at next month’s policy meeting. Policymakers in favor of a rate hike can point to the fact that inflation still remains well above the BoE target of 2 percent and the labor market remains tight. The pound has jumped more than 5% against the greenback this year, and if the BoE raises rates next month, the pound will likely make further gains.

USD lifted as 10 year yield breaks 2.9, heading to 2018 high at 2.943

Dollar receives some solid buying as the rally in 10 year yield picks up steam to above 2.9 handle.

That's a wake up call to traders that TNX could now be taking on 2.943 high, which is a key near term resistance. Break of which will finally resume the larger up trend, through 3.0 handle, 20 2013 high and 3.036. The correlation of Dollar and yield has somewhat broken down in recent months. But a break above 3% could be the turning point to realign the correlation.

That's a wake up call to traders that TNX could now be taking on 2.943 high, which is a key near term resistance. Break of which will finally resume the larger up trend, through 3.0 handle, 20 2013 high and 3.036. The correlation of Dollar and yield has somewhat broken down in recent months. But a break above 3% could be the turning point to realign the correlation.

Japanese Yen Edges Lower, CPI Report Next

USD/JPY has posted small gains in the Thursday session. In North American trade, USD/JPY is trading at 107.37, up 0.13% on the day. On the release front, US unemployment claims ticked lower to 232 thousand, close to the estimate of 230 thousand. As well, the Philly Fed Manufacturing Index improved to 23.2 thousand, easily beating the estimate of 20.8 points. Later in the day, Japan releases National Core CPI, which is expected to tick lower to 0.9%. On Friday, Japan releases Tertiary Industry Activity, which is forecast to gain 0.1% after two straight declines.

The safe-haven yen often benefits from geopolitical crises, and the escalating tariff between China and the US could be a boon for the Japanese yen, if investors become unnerved by the spat which could hurt the global economy. After a lull in the trade battle between the two economic giants, another shot was fired this week. This time it came from China, which announced a tariff of some 179% on US sorghum crops, which is a livestock feed. China imports about $1 billion of sorghum annually, and if the tariff remains in place, will essentially halt US exports of sorghum to China. The Chinese government has threatened to impose tariffs on US soybean exports, valued at some $12 billion each year. If the US administration decides to retaliate, the specter of an ugly trade war between the US and China could spook investors and send global markets into a tailspin.

With the huge fluctuations that Bitcoin has exhibited in recent months, there has been plenty of press about cryptocurrencies. The proliferation of cryptocurrencies has led to discussions about central bank-issued digital currencies (CBDC), and their effect on the global financial scene. At a banking conference earlier this week, BoJ Deputy Governor Masayoshi Amamiya said that CBDC would have a negative impact on the current financial system, but added that cryptocurrencies could find a role with central banks, such as in payment and settlement transactions. Currently, the BoJ and ECB are involved in a joint initiative, Project Stella, which is examining the use of Blockchain in securities transactions.

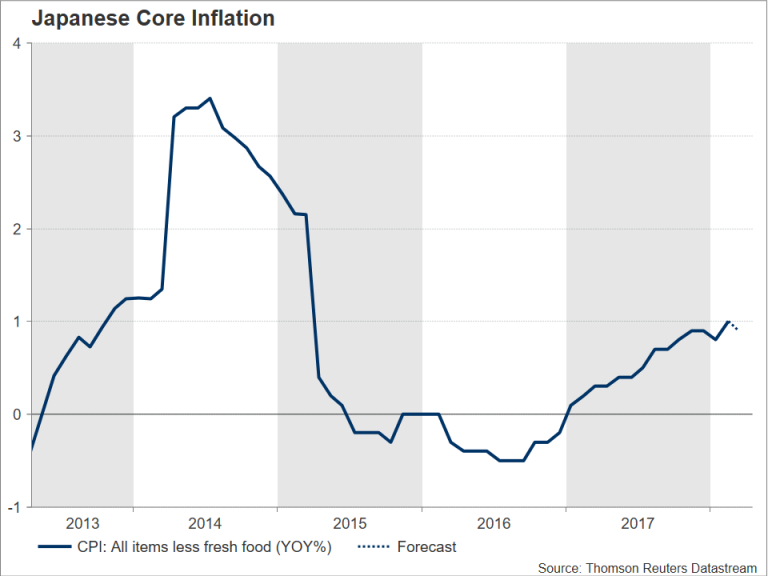

Japanese Inflation to Lose Momentum Keeping BoJ on Stimulus Path

Early on Friday, data out of Japan are expected to show that inflation in the world’s third-largest economy was unable to speed up in March as the winter season was coming to an end, adding more uncertainty as regards the timing the Bank of Japan (BoJ) will start normalizing policy. The figures could also signal that a stronger exchange rate continues to feed deflationary pressures at a time when subdued real wages are undercutting consumers’ purchasing power.

According to forecasts, the core nationwide Consumer Price Index (CPI) for the month of March is said to have eased to 0.9% year-on-year from the 1.0% seen in February, remaining far below the BoJ’s price target of 2.0% and hence supporting policymakers’ current views that the central bank is unlikely to dial back on its ultra-loose monetary policies anytime soon. Instead, the BoJ could maintain its accommodative policy until it convincingly sees inflation approaching its goal on the back of higher wages and consumer spending. But recent evidence supports that this is not happening at the moment. Real wage growth in Japan declined for the third consecutive month in February and household spending in the same month recorded the biggest contraction since April 2017 on yearly terms. Yet, the latter was said to have emerged due to the unusually cold weather which kept consumers at home and lifted vegetable prices. Some good news regarding price pressures though, is that Japanese firms seem to intensely compete for skilled workers, as a survey conducted by Nikkei showed in early April that nonmanufacturing wages reached their highest expansion in two decades this year, overcoming the rise in manufacturing earnings which tend to lead wages in Japan.

On the business front, a stronger yen makes Japanese exports less attractive to foreigners and reduces costs for imports. During March, trade uncertainties linked to Trump’s import tariffs on steel and aluminum which took effect on March 23, drew further demand for the safe-haven yen which usually benefits from rising risk aversion. During the first quarter, the yen gained 5.8% versus the greenback, while it also currently remains at elevated levels relative to the US currency. This was also evident from the latest BoJ Tankan survey for large manufacturers which found that businesses turned cautious on their future plans amid an appreciating exchange rate, US trade politics and the fall in stock markets. Moreover, export growth in March came in almost half of what analysts expected on the face of a stronger yen; still, the rise was larger than in February. Imports faced a downfall for the first time since January 2017, increasing the country’s trade surplus to the highest since May 2016.

On the business front, a stronger yen makes Japanese exports less attractive to foreigners and reduces costs for imports. During March, trade uncertainties linked to Trump’s import tariffs on steel and aluminum which took effect on March 23, drew further demand for the safe-haven yen which usually benefits from rising risk aversion. During the first quarter, the yen gained 5.8% versus the greenback, while it also currently remains at elevated levels relative to the US currency. This was also evident from the latest BoJ Tankan survey for large manufacturers which found that businesses turned cautious on their future plans amid an appreciating exchange rate, US trade politics and the fall in stock markets. Moreover, export growth in March came in almost half of what analysts expected on the face of a stronger yen; still, the rise was larger than in February. Imports faced a downfall for the first time since January 2017, increasing the country’s trade surplus to the highest since May 2016.

Even though the Japanese yen is not as data-sensitive compared to other currencies, a negative surprise in CPI numbers could pressure the yen especially to the extent it is seen as pushing further back in time a tightening cycle by the BoJ, giving chance to the dollar to bounce up to the two-month high of 107.77 reached on April 13. A bigger unexpected drop in data, which could raise doubts on whether the BoJ’s current ultra-easy monetary policy is enough to lift inflation, could offer steeper increases to dollar/yen, driving the pair even higher towards the 108 and 109 key levels. On the flip side, an upbeat report could provide evidence that the BoJ’s strategy is reaping rewards, pushing dollar/yen down to the 50-day simple moving average which currently stands at 106.64. A break below this level could open the way towards the area around 105.50 as well before the focus shifts to the 17-month low of 104.55 recorded in late March.

Sunset Market Commentary

Markets

Of late, European/German buods stayed resilient, outperforming US Treasuries as US yields trended again cautiously higher. Today, European yields finally started a catching up move. We didn’t see one specific reason. Several smaller factors might have been at work. A new up-leg in oil prices (and to a lesser extent in some other commodities) might have stoked inflation fears among investors in European bonds. Supply in Spain and France were also a bond negative in a daily perspective. From a technical point of view, the Bund finally dropped below Monday’s correction low, leaving a MT consolidation pattern. This break probably triggered some stop-loss repositioning on the March Bund rally. Also worth mentioning, the flatting trend on the US yields curve has halted. At the time of writing, the US yield curve bear steepens with 2-year yield little changed and the 30-year yields rising 3.7bp. German bonds show a similar move, but underperforming US Treasuries with 2-year yields rising 1.2bp and the 10-y yield rising 5 bp. Intra-EMU spread changes remain very limited across different countries with Spain slightly underperforming (+2bp).

As was the case earlier this week, there was again no clear driver for USD trading. EUR/USD again tested the 1.24 area early this morning, but there were no follow-through gains even as interest rates today moved slightly in favour of the single currency. EUR/USD hovered in a tight sideways range in the upper half of the 1.24 big figure. USD/JPY jumped to the 107 area in Asia this morning, but also this move could not be extended. USD/JPY currently trades in the 107.40 area. The rise in core yields (both in the US and Europe) might be a tentative negative for the yen. At the same time equities didn’t provide much support for the likes of EUR/JPY and USD/JPY as the equity rebound shifted into a lower gear.

Yesterday, sterling corrected lower on softer than expected UK CPI data. Today, the March UK retail sales were published. Sales again missed the consensus by a big margin. The headlined figure declined 1.2% M/M, reducing the Y/Y gain from 1.5% to 1.1% (1.9% Y/Y was expected). However, there was a good excuse for the poor sales performance: weather conditions were extremely harsh for the time of the year. Sterling briefly lost ground after the publication of the report, but the move had no strong legs. Sterling soon reversed the initial loss. EUR/GBP even returned to the 0.87 area. Cable dropped temporarily below the 1.42 handle, but the pair currently trades again in the 1.4235 area. Underlying sentiment on sterling remains quite constructive given disappointing data of late.

News Headlines

German Chancellor Angela Merkel and French president Macron indicated that they will make a united proposal for the June 19 EU summit on how they want further reforms in the EMU to proceed as both leaders agreed that the euro zone was "not yet sufficiently crisis-proof".

UK retail sales disappointed again in March. Headline sales declined -1.2%M/M. Cold weather was partially to blame. Even so, retail sales were poor in three of the last four months. So, one can expect private consumption to have only a low contribution to Q1 UK GDP growth.

US eco data were close to expectations. Weekly jobless claims were little changed at 232k in the week ending April 14. The Philly Fed business outlook was marginally stronger than expected improving from 22.3 to 23.2 (21 was expected).