Sample Category Title

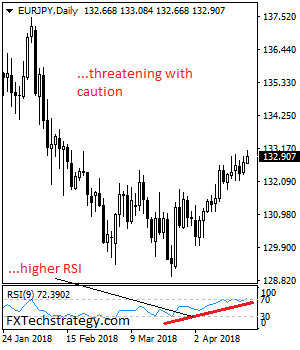

EURJPY: Strengthens But With Caution

EURJPY - The pair looks to consolidate further though seen strengthening on Thursday. On the downside, support comes in at the 132.50 level where a break if seen will aim at the 132.00 level. A cut through here will turn focus to the 131.50 level and possibly lower towards the 131.00 level. On the upside, resistance resides at the 133.50 level. Further out, we envisage a possible move towards the 134.00 level. Further out, resistance resides at the 134.50 level with a turn above here aiming at the 135.00 level. On the whole, EURJPY faces further consolidation threats.

Philadelphia business outlook: General activity, new orders, shipments, and employment all indicated continued expansion

Philadelphia business outlook diffusion index rose from 22.3 to 23.2 in April, beating expectation of 21.2. There were nearly 37% of manufacturers reported increases in overall activity during the month, while 14% reported decreases. Philadelphia Fed noted in the release that the responses " suggest continued growth for the region's manufacturing sector. The indexes for general activity, new orders, shipments, and employment all indicated continued expansion this month." And, "looking ahead six months, the firms continued to be optimistic about the outlook for manufacturing activity."

Also from US, jobless claims dropped 1k to 232k in the week ended April 21, slightly above expectation of 230k. Four week moving average rose 1.25k to 231.25k. Continuing claims dropped 15k to 1.86m in the week ended April 14.

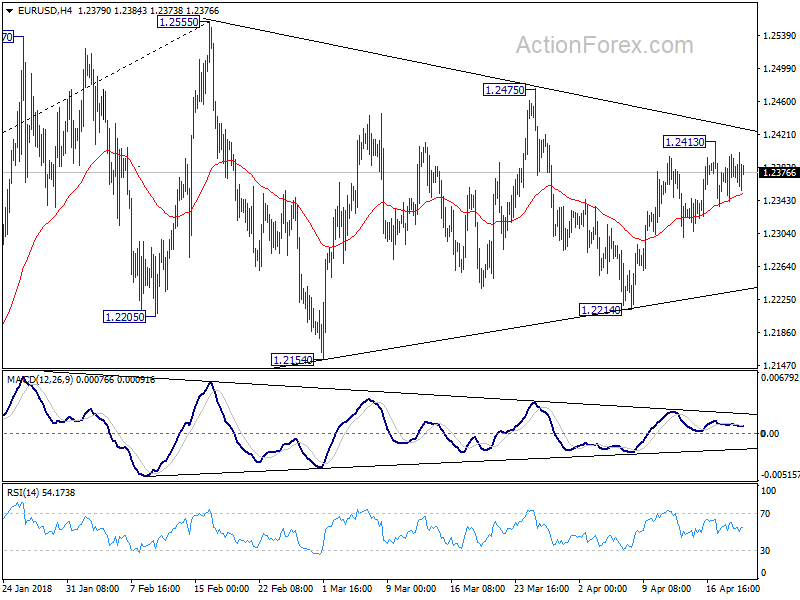

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2345; (P) 1.2371 (R1) 1.2401; More....

EUR/USD is staying in tight range below 1.2413 and intraday bias remains neutral. On the upside, above 1.2413 will extend the rebound from 1.2214 to 1.2475 resistance. Break will target 1.2516/2555 key resistance zone. On the downside, however, break of 1.2214 will revive the case of trend reversal and turn outlook bearish.

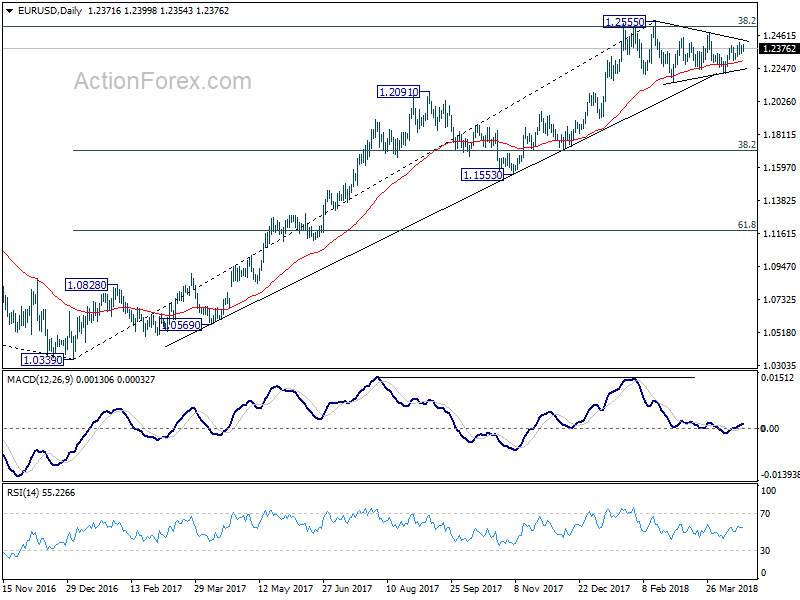

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

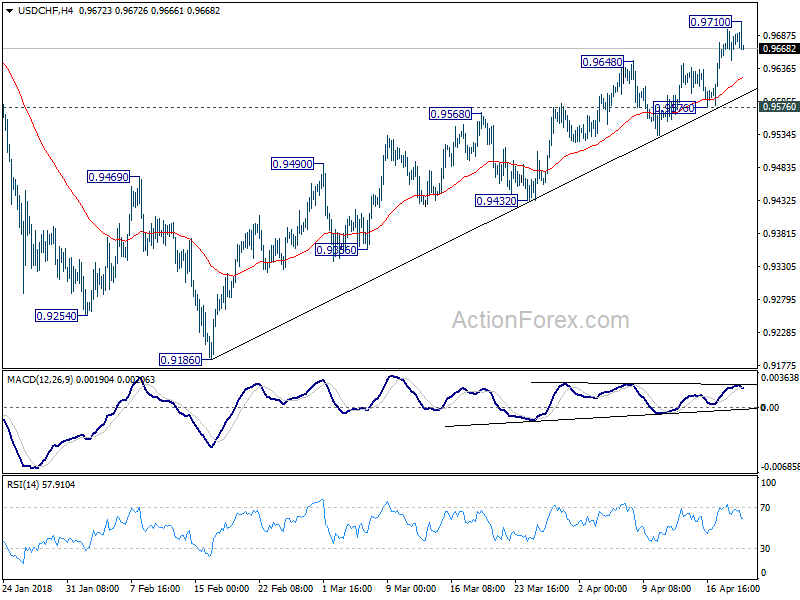

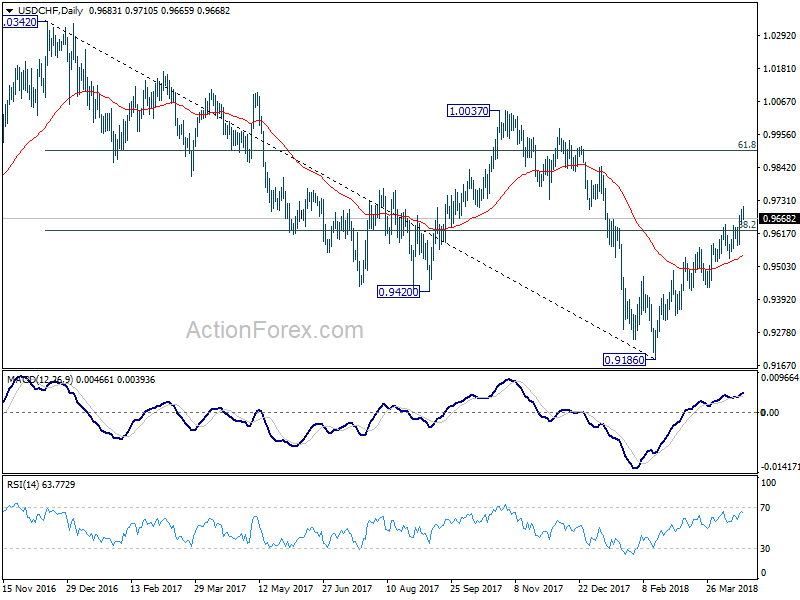

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9658; (P) 0.9678; (R1) 0.9706; More...

A temporary top is formed at 0.9710 as USD/CHF retreats. Intraday bias is turned neutral first. Further rise is still expected as long as 0.9576 support holds. Above 0.9710 will extend recent rally to 0.9900 fibonacci level next. However, break of 0.9576 will indicate short term topping and turn bias to the downside for 0.9432 support and possibly below.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next.

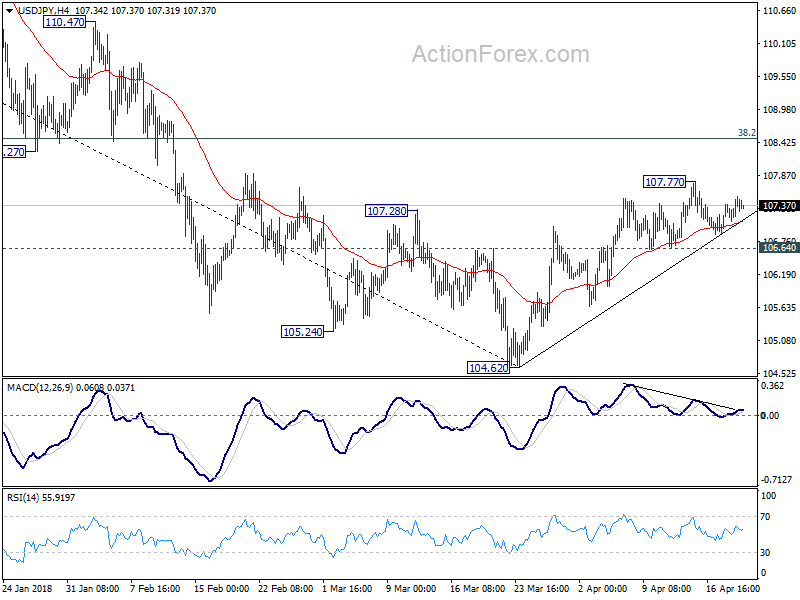

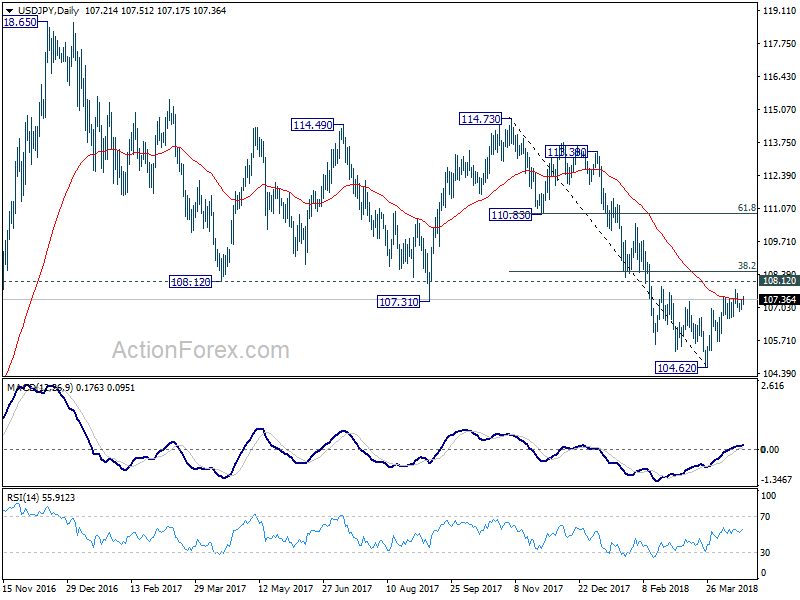

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 107.00; (P) 107.19; (R1) 107.41; More...

At this point, the consolidation pattern from 107.77 is still unfolding and intraday bias stays neutral in USD/JPY. With 106.64 minor support intact, rebound from 104.62 is in favor to continue. Break of 107.77 will target 38.2% retracement of 114.73 to 104.62 at 108.48 which is close to 108.12. This level is crucial in determining the medium outlook. On the downside, break of 106.64, however, will indicate the rebound from 104.62 has completed. And in that case, bias will be turned back to the downside for retesting 104.62.

In the bigger picture, as long as 108.12 support turned resistance holds, the medium term down trend from 118.65 (2016 high) should still continue lower, at least to retest 98.97 (2016 low). However, sustained break of 108.12 will be an early sign of medium term reversal. In that case, further rise would be seen to 114.73 resistance to confirm completion of the fall from 118.65.

In the bigger picture, as long as 108.12 support turned resistance holds, the medium term down trend from 118.65 (2016 high) should still continue lower, at least to retest 98.97 (2016 low). However, sustained break of 108.12 will be an early sign of medium term reversal. In that case, further rise would be seen to 114.73 resistance to confirm completion of the fall from 118.65.

Canadian Dollar Edges Higher, Canadian NFP Sparkles

The Canadian dollar has posted slight gains in the Thursday session. Currently, USD/CAD is trading at 1.2605, down 0.19% on the day. In economic news, Canadian ADP Nonfarm Employment Change posted a sharp gain of 42.8 thousand. In the US unemployment claims ticked lower to 232 thousand, close to the estimate of 230 thousand. As well, the Philly Fed Manufacturing Index improved to 23.2 thousand, easily beating the estimate of 20.8 points. On Friday, Canada releases CPI, which is forecast to drop to 0.4%.

There were no surprises from the Bank of Canada on Wednesday, as the bank maintained the benchmark rate at 1.25 percent. The BoC was in cautious mode in the rate statement, noting that growth in the first quarter was weaker than the bank had forecast, but that it expected better news in the second quarter. Speaking after the statement, BoC Governor Stephen Poloz said that “the economy is in a good place,” but added that “interest rates are very low”. This is a clear signal that the BoC plans to raise rates in the near future, and many analysts are predicting a rate hike in July. Canada’s employment picture has been a bright spot, underscored by an excellent ADP nonfarm payrolls report.

The protectionist US administration has reopened the NAFTA agreement, threatening to walk away if its demands for major concessions in favor of the US are not met. NAFTA is a crucial component of the Canadian economy, and the loss of NAFTA would be a nightmare for Canada. As well, the Federal Reserve plans a number of rate hikes in 2018, and if the BoC does not raise rates on its end, the Canadian dollar could fall sharply against a US currency that would be more attractive to investors.

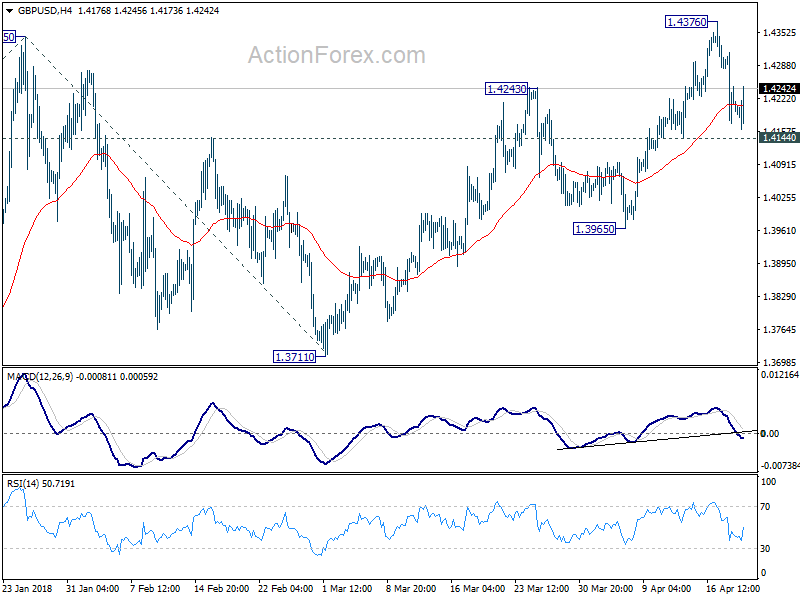

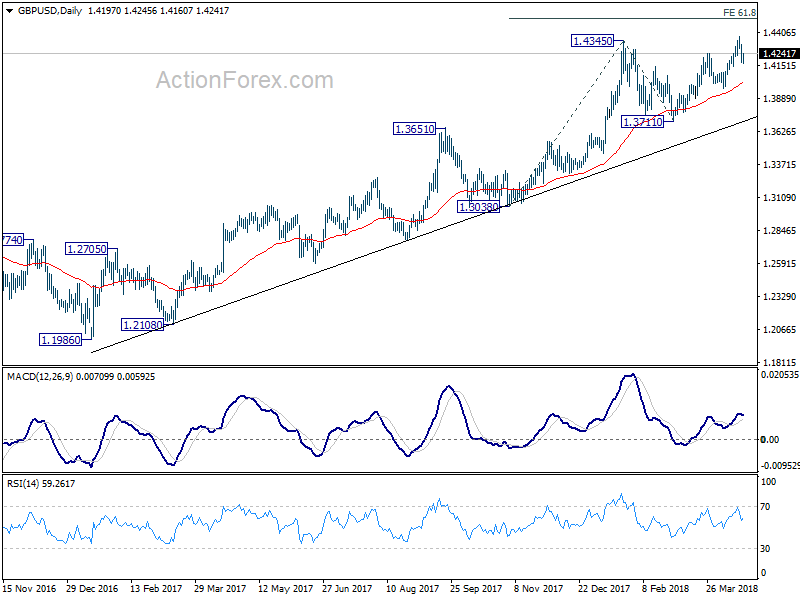

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4145; (P) 1.4229; (R1) 1.4287; More...

GBP/USD recovers ahead of 1.4144 minor support and intraday bias stays neutral. For now, price actions from 1.4376 are viewed as developing into a consolidation pattern, even though such pattern might take a while to complete. Further rise is still expected. On the upside, break of 1.4376 will confirm up trend resumption. In that case, GBP/USD would target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519. However, on the downside, firm break of 1.4144 will be an early sign of medium term topping and turn focus back to 1.3965 support.

In the bigger picture, rise from 1.1946 (2016 low) is in progress and resuming. It is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. We'd continue to favor this medium term bullish view as long as 1.3711 support holds, even in case of deep pull back.

In the bigger picture, rise from 1.1946 (2016 low) is in progress and resuming. It is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. We'd continue to favor this medium term bullish view as long as 1.3711 support holds, even in case of deep pull back.

Sterling and Canadian Dollar Recover Losses, Markets Lack Dominant Theme

The major theme in the forex markets isn't too clear today. Sterling dips initially after retail sales missed expectation, but quickly recovered. Canadian dollar also pare back some of the post BoC decline, as lifted by strength in oil price. Australian Dollar gained earlier today but there is no follow through buying. Dollar continues to trade mixed. In particular, EUR/USD and USD/JPY are gyrating in very tight range. EUR/JPY edged slightly higher, with very week momentum. The more exciting development today is EUR/CHF hits as high as 1.1998/9 (depending on which feed you're reading) but struggles to break through that historical 1.2 handle so far.

Economic data released in US session also provide little inspiration. US jobless claims dropped 1k to 232k in the week ended April 21, slightly above expectation of 230k. Four week moving average rose 1.25k to 231.25k. Continuing claims dropped 15k to 1.86m in the week ended April 14. Philly Fed survey rose fro 22.3 to 23.2 in April. Canada ADP payrolls rose to 42.8k in March.

UK retail sales missed, petrol sales dropped on snow, by online sales surged

UK retail sales including auto and fuel dropped -1.2% mom in March, well below expectation of -0.6%. Annual rate rose 1.1% yoy, below expectation of 1.9% yoy. Retail sales excluding auto and fuel dropped -0.5%, below expectation of -0.4%. Annual rate rose 1.1% yoy, below expectation of 1.4% yoy. The ONS noted in the release that mom decline was "a likely consequence of adverse weather conditions, which impacted travel."

Rhian Murphy, ONS Senior Statistician said that the sharp fall in Q1 retail sales was due to "a large decline in March with petrol sales seeing a significant slump as a result of the poor weather keeping many shoppers indoors." Nonetheless, "the snow actually helped boost online spending with department stores in particular seeing growth in their web sales."

Germany's Joint Economic Forecast Project Group raised 2018 and 2019 growth projections

In the twice a year published Joint Economic Forecast by leading German institutes, growth projection for 2018 and 2019 were raised to 2.2% and 2.0% respectively. Both were upwardly revised by 0.2% from Autumn report. The released warned that while German economy "continues to boom", "the air is getting thinner". Still, "pace of economic expansion nevertheless remains brisk:" It pointed to upturn in the world economy, favorable situation in labor market and fiscal stimulus of the new coalition government as driving forces. Inflation is projected to slow to 1.7% in 2018 then rise again to 1.9% in 2019.

Global growth projection was revised up by 0.3% to 3.4% in 2018. The reported noted that "tax cuts in the USA will stimulate economic activity there, which may have a knock-on effect on other countries". However, it also warned that the dynamic in the world economy will "gradually flatten off over the forecasting period". And that's partly due to "a harsher trade policy climate, which will burden global investments.".

The report also pointed directly to the US announcement of steel and aluminum tariffs as "another step towards greater protectionism". It warned that "any further escalation of the trade conflict will restrict international trade in goods and significantly damage world economic growth in the mid-term." Even "mere discussion of such measures can increase uncertainty over a country's future trade policy and weaken economic sentiment".

Australia employment data miss is not a disaster

Australia Dollar is not too bothered by the weaker than expected headline job data from Australia. 4.9k jobs were added in March, below expectation of 20.3k. Full time jobs dropped by 19.9k to 8.51m while part time jobs rose 24.8k to 3.9m. Total employment was at 12.484m. Prior month's figure was revised down from 17.5k to -6.3k. February now had the first monthly drop in employment since September 2016. The record streak of consecutive monthly job growth has shorted to 16 months.

Seasonally adjusted unemployment rate was unchanged at 5.5%, after downward revision in February's figure from 5.6% to 5.5%. However, labor force participation rate rose to 65.7%, sitting at a record high in since the series began back in 1978. The figures just showed that growth in the Australian labor market is slowing after a very strong period since late 2016. .

Australia NAB business condition rose to highest since 2007

Australia quarterly NAB business confidence was unchanged at 7 in Q1. Quarterly business conditions rose from 15 to 17. In the release, NAB noted that the quarterly business condition was at its highest level since 2007 even though the monthly survey data eased later in the quarter. Business confidence has been relatively stable since Q3 2016, staying within a range of 6 to 8, and was a little above historical average of 5. While there is no upward wage pressure, the conditions are in place due to tightening labor market.

Regarding RBA monetary policy, NAB noted that businesses are pricing in around 80% chance of a 25bps hike within 12 months. RBA itself noted that " RBA will want clear evidence that wages growth and inflation are moving higher before removing some policy accommodation, and we don't expect sufficient evidence of this until late 2018". NAB expects RBA to have the first hike in November "with the risk that it occurs later".

RBNZ Orr: Very benign inflation going forward without doubt

New Zealand CPI slowed notably to 1.1% yoy in Q1, down from prior quarter's 1.6%, meeting expectation. RBNZ Governor Adrian Orr said in Radio New Zealand interview that he expected "very benign inflation going forward without doubt, as we've forecast".

He added that "what really matters is the confidence and expectation and belief that we are aiming for that midpoint of 2 percent all of the time." And he pledged that "we are doggedly determined to aim for two percent, but the accuracy around...that is very limited."

Overall, with CPI now close to bottom of RBNZ's target band, there is little pressure for the central bank to raise interest rates.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4145; (P) 1.4229; (R1) 1.4287; More...

GBP/USD recovers ahead of 1.4144 minor support and intraday bias stays neutral. For now, price actions from 1.4376 are viewed as developing into a consolidation pattern, even though such pattern might take a while to complete. Further rise is still expected. On the upside, break of 1.4376 will confirm up trend resumption. In that case, GBP/USD would target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519. However, on the downside, firm break of 1.4144 will be an early sign of medium term topping and turn focus back to 1.3965 support.

In the bigger picture, rise from 1.1946 (2016 low) is in progress and resuming. It is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. We'd continue to favor this medium term bullish view as long as 1.3711 support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q1 | 0.50% | 0.50% | 0.10% | |

| 22:45 | NZD | CPI Y/Y Q1 | 1.10% | 1.10% | 1.60% | |

| 01:30 | AUD | Employment Change Mar | 4.9K | 20.3K | 17.5K | -6.3K |

| 01:30 | AUD | Unemployment Rate Mar | 5.50% | 5.50% | 5.60% | 5.50% |

| 01:30 | AUD | NAB Business Confidence Q1 | 7 | 6 | 7 | |

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | 35.1B | 32.3B | 37.6B | |

| 08:30 | GBP | Retail Sales M/M Mar | -1.20% | -0.60% | 0.80% | |

| 12:30 | CAD | ADP Payrolls Mar | 42.8K | 32.7K | ||

| 12:30 | USD | Initial Jobless Claims (APR 14) | 232K | 230K | 233K | |

| 12:30 | USD | Philadelphia Fed Business Outlook Apr | 23.2 | 21.2 | 22.3 | |

| 14:00 | USD | Leading Index Mar | 0.30% | 0.60% | ||

| 14:30 | USD | Natural Gas Storage | -23B | -19B |

GBP, CAD recovering; NZD, USD, JPY Pressured

Heading into US session, GBP and CAD recovered some of the losses this week. In particular, GBP is rather immuned from the retail sales miss as that's primarily due to bad weather. CAD, on the other hand is lifted mildly by oil prices. NZD is trading as the weakest one for today as CPI slowed to 1.1% in Q1, close to RBNZ's target band. Governor Adrian Orr's comments that "very benign inflation going forward without doubt" also weigh down the NZD. JPY and USD follow as the second and third weakest for the day.

DAX Trading Sideways, German Inflation Report Ahead

The DAX index is steady in the Thursday session. Currently, the DAX is trading at 12,576 points, down 0.11% on the day. On the release front, the eurozone current account surplus dropped to EUR 35.1 billion, but beat the estimate of EUR 32.3 billion. On Friday, Germany releases PPI and the Eurozone publishes consumer confidence.

Eurozone inflation improved in March, but still remain short of the ECB target of 2.0%. Final CPI came in at 1.3%, up from 1.1% a month earlier. Still, the reading fell short of the estimate of 1.4%. As long as inflation remains low, there will be little pressure on the ECB to tighten its accommodative monetary policy. The ECB’s stimulus program is scheduled to wind up in September, but an increase in interest rates is unlikely before 2019.

After a lull in the trade battle between the US and China, another shot was fired this week. This time it came from China, which tariff announced a tariff of some 179% on US sorghum crops, which is a livestock feed. China imports about $1 billion of sorghum annually, and if the tariff remains in place, will essentially halt US exports of sorghum to China. The Chinese government has threatened to impose tariffs on US soybean exports, valued at some $12 billion each year. If the US administration decides to retaliate, the specter of an ugly trade war between the US and China could spook investors and send global markets into a tailspin.