Sample Category Title

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8713; (P) 0.8741; (R1) 0.8794; More...

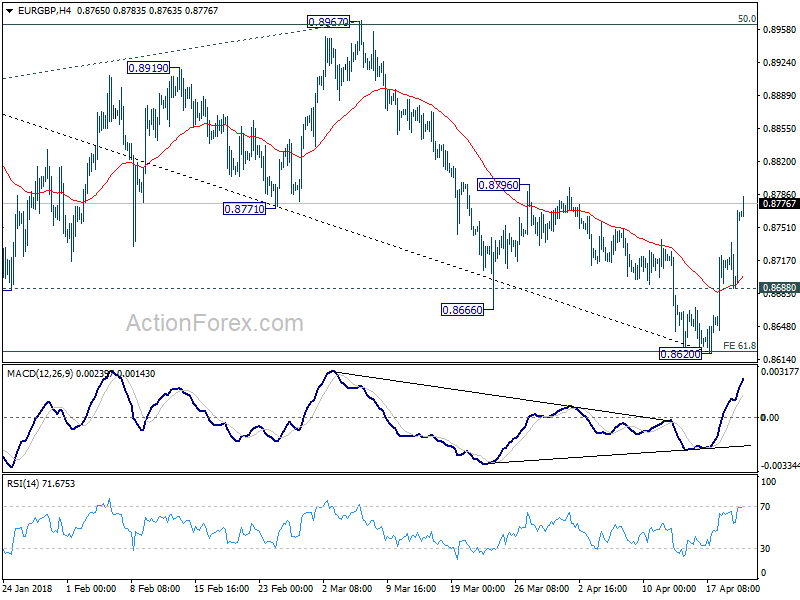

EUR/GBP's strong rebound and firm break of 0.8739 indicates near term reversal. And whole decline from 0.9305 has likely completed after hitting 61.8% projection of 0.9305 to 0.8745 from 0.8967 at 0.8621. Intraday bias is back on the upside for 0.8796 first. Firm break there will target key cluster resistance at 0.8967 (50% retracement of 0.9305 to 0.8620 at 0.8963) next. On the downside, break of 0.8688 minor support will dampen the bullish case and turn focus back to 0.8620 instead.

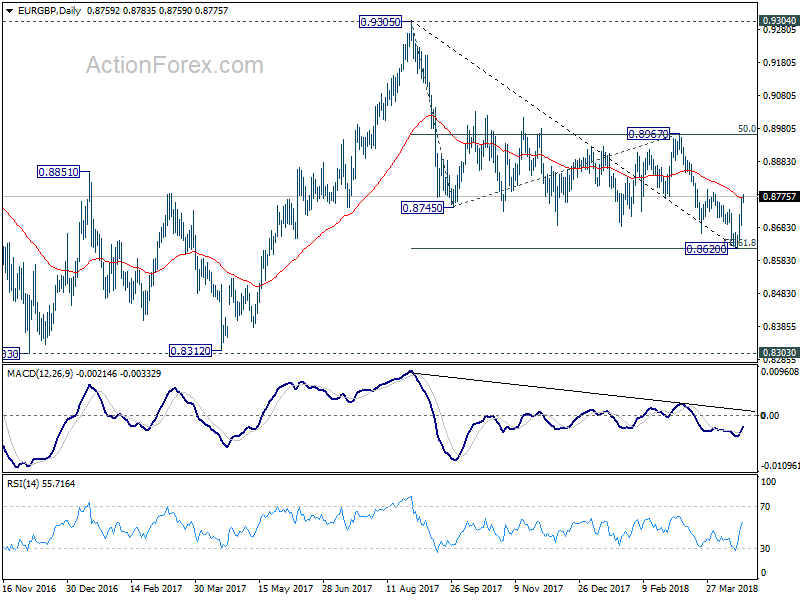

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

EURO Bearish Below 1.2344 Level

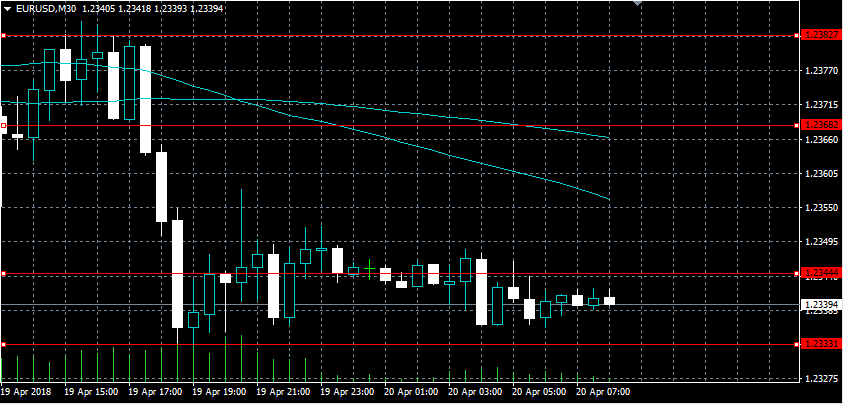

The euro has moved lower against the U.S dollar, hitting 1.2333, as rising long and short-term U.S treasury-yields caused the greenback to strengthen across the board. The EURUSD pair currently trades around the 1.2340 level, after strong technical rejection from the 1.2382 level on Thursday. Euro sellers are in control while price-action is below the 1.2344 level, with traders now looking to the release of PPI inflation data from the German economy.

The EURUSD pair is bearish while trading below 1.2344 level, further losses towards the 1.2300 and 1.2275 support levels remain possible.

If the EURUSD pair trades back above the 1.2382 resistance level, buyers may test towards the 1.2400 and 1.2413 levels.

GBPUSD Strongly Bearish Below 1.4168 Level

The British pound has moved sharply lower against the U.S dollar, after bearish comment on future rate hikes from Bank of England Governor Mark Carney. The GBPUSD pair currently trades around the 1.4070 level, with pound sellers firmly in control while price-action trades below the key 1.4168 level. Traders now look to the 1.4200 level as the daily pivot, while the pairs weekly price-close remains key for medium-term trading sentiment.

The GBPUSD pair retains an intraday bearish bias while trading below the 1.4200 level, key intraday support is found at the 1.4168 and 1.4146 levels.

If the GBPUSD pair trades above the 1.4200 level, buyers may move price-action back towards the 1.4244 and 1.4260 levels.

Canadian Consumer Prices, Fed Speakers On Deck For Friday

North American releases will headline a moderately active session on Friday, giving investors more time to parse through corporate earnings and geopolitical developments. A meeting of the International Monetary Fund (IMF) may also produce tangible headlines.

In terms of economic data, action begins at 06:00 GMT with a report on German producer inflation. Germany's producer price index (PPI) likely rose 0.2% during the month of March, which translates into a year-over-year gain of 2%. PPI fell 0.1% in February.

On the monetary policy front, Bank of England (BOE) official Michael Saunders will deliver a speech at 09:30 GMT.

Shifting gears to North America, the Canadian government will report on retail sales and consumer inflation at 12:30 GMT. The retail sales report is likely to show growth of 0.3% for February after a similar gain the month before. Excluding fuel sales, retail receipts are forecast to rise by a similar amount. Retail receipts are a proxy for consumer spending and are therefore closely watched by the financial markets.

Canada's report on consumer inflation is expected to show growth of 0.4% in March after a gain of 0.6% the month before. In annual terms, this translates into growth of 2.2%.

The North American session will also see the release of the Eurozone consumer confidence report. The monthly indicator, which is released by the European Commission, is expected to show a decline to -0.2 in April from +0.1 in March.

A pair of Federal Reserve officials will also be in the headlines on Friday. Charles Evans of the Chicago Fed and John Williams of San Francisco are scheduled to deliver speeches in the morning. Williams is also a member of this year's Federal Open Market Committee (FOMC), which voted to raise interest rates last month.

EUR/USD

Europe's common currency failed to extend its recovery on Thursday, with prices falling back toward the low-1.2330 region. EUR/USD was last seen trading at 1.2340, where it was down 0.1% from the previous close. The pair is testing immediate support at 1.2330. On the opposite side of the spectrum, resistance is likely found at 1.2400.

USD/CAD

The Canadian dollar bounced off its recent lows on Thursday to return above 1.2600. The USD/CAD exchange rate would add another 70 pips to trade near 1.2670. Canadian retail sales and CPI data will likely determine the pair's next move, although recent price action suggests further gains are in store.

GBP/USD

Cable extended its downside on Thursday, with prices falling around 150 pips. The pair broke beneath 1.4100 and was last seen trading at 1.4074. GBP/USD faces immediate support at 1.4035. On the opposite side of the ledger, resistance is seen at 1.4120.

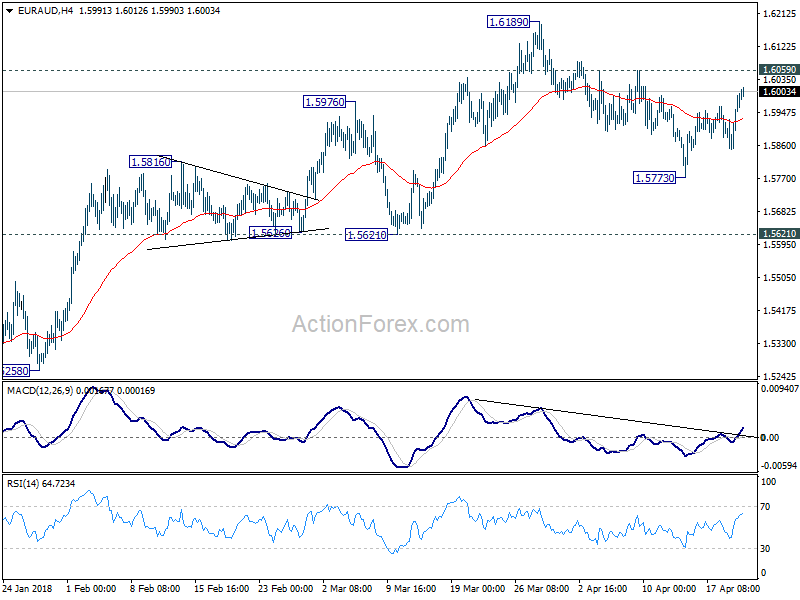

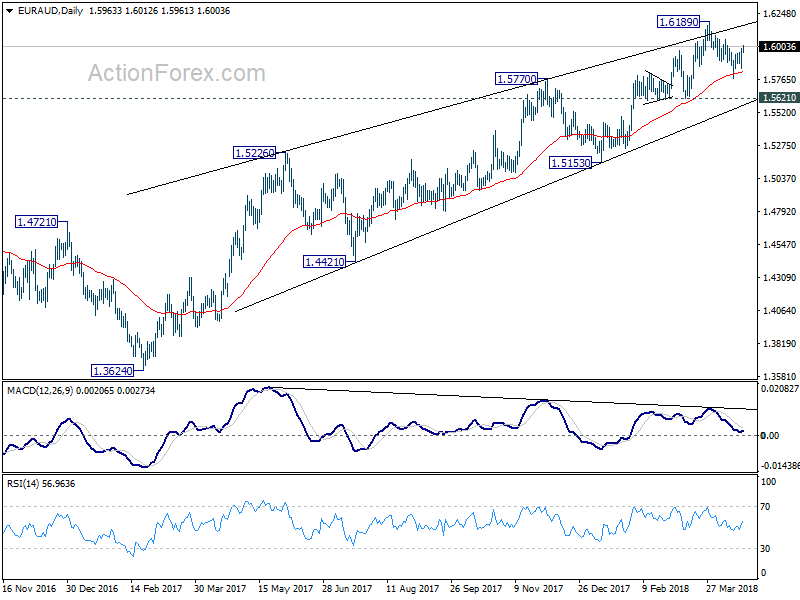

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5882; (P) 1.5936; (R1) 1.6025; More....

EUR/AUD's recovers again but stays in range of 1.5773/6059. Intraday bias remains neutral first. Another fall is in favor as long as 1.6059 holds. Break of 1.5773 will target 1.5621 support first. Decisive break there will be another indication of medium term trend reversal. However, break of 1.6059 will turn bias back to the upside and target a test on 1.6189 high instead.

In the bigger picture, the case for medium term reversal is building up in EUR/AUD. Bearish divergence condition in daily MACD indicates further loss of upside momentum ahead of 1.6587 key resistance (2015 high). Break of 1.5621 should confirm medium term topping and bring deeper fall back to 1.5153 and possibly below. Meanwhile, even in case of up trend resumption, we'd be cautious on strong resistance from 1.6587 to limit upside and bring reversal.

In the bigger picture, the case for medium term reversal is building up in EUR/AUD. Bearish divergence condition in daily MACD indicates further loss of upside momentum ahead of 1.6587 key resistance (2015 high). Break of 1.5621 should confirm medium term topping and bring deeper fall back to 1.5153 and possibly below. Meanwhile, even in case of up trend resumption, we'd be cautious on strong resistance from 1.6587 to limit upside and bring reversal.

In The Euro Area, Consumer Confidence For April Is Due To Be Released

Market movers today

In the euro area, consumer confidence for April is due to be released. Consumer confidence has stagnated at 0.1 for the past two months, after rising steadily throughout 2017 and consensus is for fall to -0.1 in April. Even so, consumer sentiment will remain above its long-run average and point to robust private consumption growth ahead. The Fed's Mester (voter, hawkish) and Evans (non-voter, dovish) are due to speak on the economy and monetary policy.

In Scandinavia, manufacturing confidence for Q1 is being released in Norway and Danish consumer confidence for April is due out (see next page).

Selected market news

Global yields have seen upward pressure over the past 24 hours. The sell-off in global FI markets were most pronounced in the UK Gilt market where the yield on the 10-year Gilt rose 10bp. But also German and periphery yields saw pronounced upward pressure with the 10-year Bund yield 7bp higher. There were no obvious drivers for the sell-off but a combination of renewed focus on commodity prices and supply from France and Spain probably drew yields higher in the European market. The negative sentiment was carried over to the US where 10Y US treasury yields rose 5bp to 2.92%. We note the curves for 2s10s and 5s30s steepened after flattening significantly over the past couple of weeks. We also saw that 10Y US breakeven inflation expectations rose once again, underlining the impact of higher commodity prices.

However, we doubt we are in for a significant new jump in yields as in January and February where 10Y Germany rose 35bp over six weeks. Yesterday, we published a research paper where we looked at the global business cycle (see link to the right). We argue that there are clear signs that the global business cycle peaked in early 2018. Furthermore, our MacroScope models point to a further deceleration over the coming quarters. The recent uncertainty over a potential trade war is likely to reinforce this picture. While the cycle is softening, we still expect growth levels to stay above potential growth, as US fiscal easing will temper any deceleration in 2019. Nevertheless, declining PMI levels across regions tends to cause some anxiety about the strength of the recovery and put a cap on bond yields.

Hence, if global yields are to see a further strong upward pressure the driver needs to be a new spike in commodity prices or change in rhetoric from central banks. We doubt the latter will be the case if the global business cycle is weakening, see also our new ECB update . The sanctions against Russia could still push some metal prices higher and the oil market, which has rebalanced this year (lower stocks), could be affected if the Trump administration decides to take a tougher stance on Iran. In respect of central bank rhetoric, note that GBP weakened last night after BoE Governor Mark Carney struck a dovish tone in an interview, stating that a few rate hikes may be warranted over the next few years, thus essentially questioning whether a May hike is a done deal after all. Carney came after the close of the Gilt market.

The higher yields weighed on US stocks, but the market recovered some of the losses after Deputy Attorney General Rosenstein said Trump is not the target of the Mueller investigation.

Equity Markets Trade Generally Lower After Weakness In The US

Asia Market: Equity markets trade generally lower after weakness in the US; Later today US/Japan talks in focus

- Taiwan Semi declines over 6% after cutting FY outlook, weighs on sector

- Mining shares decline following gains on Thursday

- Japan March CPI slows amid speculation BoJ might cut inflation forecasts at April meeting (26-27th)

- Japan Fin Min Aso said there were no issues with currencies at G-20 meeting; Aso and Mnuchin to meet later on Friday (1:45 PM EST)

- PBoC injects liquidity for the week through its OMOs vs prior drain

- Certain Chinese banks said to raise interest rates on CDs following recent informal guidance from PBoC

- Asian 10-year government bond yields track rise in US interest rates

- Australia Q1 CPI data due for release next week (Tuesday, April 24th)

Australia/New Zealand

- ASX 200 opened -0.3%; closed -0.3%

- ASX 200 Telecom index -1.1%, Utilities -0.8%, Resources -0.4%, REIT -0.3% Financials -0.1%

- Retailer Adaris [ADH.AU] rises over 17% after raising guidance.

- (AU) Australia Treasurer Morrison: Confirms tougher penalties for corporate misconduct

- (AU) Australia sells A$400M v A$400M indicated in Nov 2027 bonds, avg yield 2.7989% v 2.7735% prior, bid to cover: 5.95x v 5.96x prior

China/Hong Kong

- Shanghai Composite opened -0.4%, Hang Seng -0.2%

- Hang Seng Materials index -2%, Info Tech -1.5%, Energy -1.5%, Industrial Goods -1.2%, Property/Construction -1.1%, Consumer Goods -0.9%, Services -0.7%, Financials -0.4%

- Shanghai Property sub-index declines over 1.5%

- (CN) China PBoC auctions 3-month Finance Ministry (MOF) deposits at 4.50%

- (CN) China PBoC sets yuan reference rate at 6.2897 v 6.2832 prior

- (CN) China PBoC Open Market Operation (OMO): Skips OMO v CNY190B injected in 7-day reverse repos prior

- (HK) Hong Kong Exchanges: To announce dual class share and biotech listing rules on Tuesday, April 24th

Japan

- Nikkei 225 opened -0.2%; closed -0.1%

- TOPIX Electric Appliances index -0.5%; Securities +1.2%, Real Estate +0.7%, Retail Trade +0.5%

- (JP) JAPAN MAR NATIONAL CPI Y/Y: 1.1% V 1.1%E; CPI EX FRESH FOOD (CORE): 0.9% V 0.9%E

- (JP) Japan Feb Tertiary Industry Index M/M: 0.0% v 0.0%e

- (JP) Japan Chief Cabinet Sec Suga: Reiterates still will not accept demands for Finance Min Aso to resign

- (JP) Bank of Japan (BoJ): Company loan demand index 3 v 8 prior - April Loan Officer Opinion Survey

- (JP) Japan Finance Ministry (MOF) Official: Talks at between Finance Min Aso and US Treasury Sec Mnuchin to be made in context of view that global imbalances should be dealt with multilaterally and not bilaterally

- (JP) Bank of Japan Kuroda: protectionism is not good for world economy but do not expect it to spread

Korea

- Kospi opened -0.3%

North America

- US equity markets ended lower: Dow -0.3%, S&P500 -0.6%, Nasdaq -0.8%, Russell -0.6%

- S&P 500 Consumer Staples -2.9%, Materials -1.1%, Technology -1.1%

- (US) Fed's Mester (FOMC voter, hawk): Reiterates further rate hikes appropriate in 2018 and 2019

Europe

- (UK) Bank of England (BOE) Gov Carney: should prepare for a few interest rate hikes over next few years; expect there will be differences of opinion at May policy meeting - BBC interview; Believes there will be some differences of opinion at the May MPC Meeting; Conscious there are other meetings throughout remainder of year (NOTE: current market expectations are for a rate hike at the May meeting)

- EU said to comprehensively reject UK Brexit proposals for solution on Irish border – press

- (DE) Germany March Tax Rev +1.9% y/y; Q1 Tax Rev +4.1% y/y (in line with full-year projection) - Finance Ministry Monthly Report

Levels as of 02:00ET

- Hang Seng -0.5%; Shanghai Composite -1.4%; Kospi -0.4%

- Equity Futures: S&P500 flat; Nasdaq100 flat, Dax flat; FTSE100 flat

- EUR 1.2335-1.2350 ; JPY 107.34-107.75 ; AUD 0.7705-0.7734 ;NZD 0.7235-0.7274

- Jun Gold -0.3% at $1,344/oz; May Crude Oil -0.3% at $68.09/brl; May Copper -0.3% at $3.119/lb

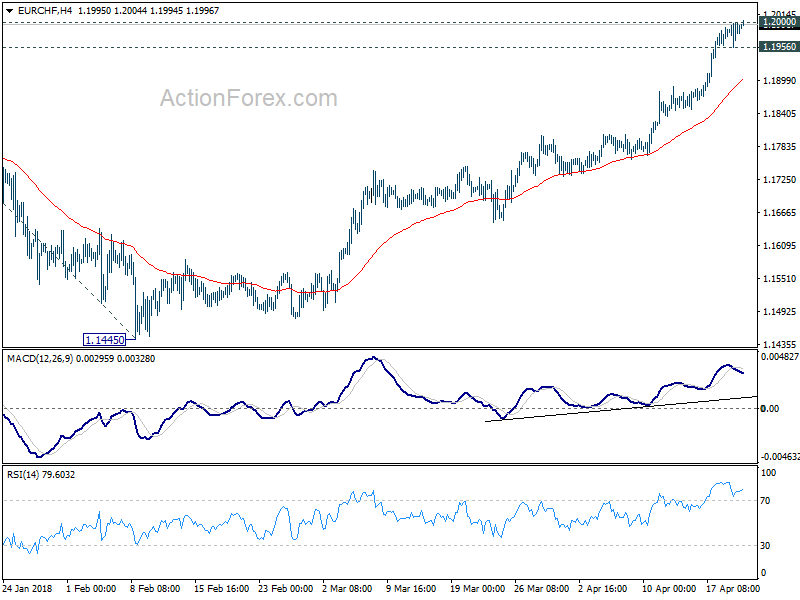

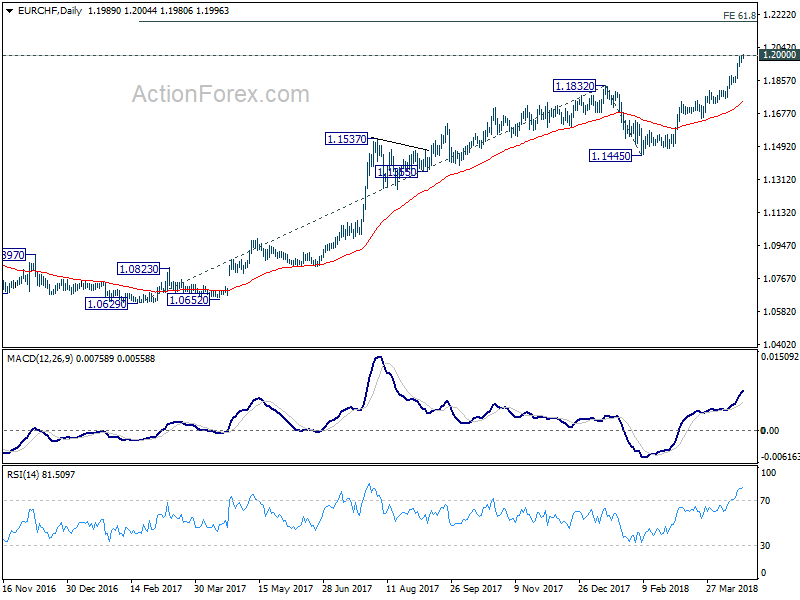

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1955; (P) 1.1974; (R1) 1.2004; More...

EUR/CHF continues to lose upside momentum as it's pressing 1.2 handle. But further rise is expected as long as 1.1956 minor support holds. Sustained break of 1.2 will extend the current up trend to 61.8% projection of 1.0629 to 1.1832 from 1.1445 at 1.2188. On the downside, below 1.1956 will turn bias turn bias to the downside for retreat to 4H 55 EMA (now at 1.1898) or below before staging another rally.

In the bigger picture, decisive break of 1.1832 should now extend the medium term up trend through prior SNB imposed floor at 1.2000. 2013 high at 1.2649 should be the next target. Outlook will remain bullish as long as 1.1445 support holds, even in case of deep pull back.

In the bigger picture, decisive break of 1.1832 should now extend the medium term up trend through prior SNB imposed floor at 1.2000. 2013 high at 1.2649 should be the next target. Outlook will remain bullish as long as 1.1445 support holds, even in case of deep pull back.

Treasury Yield Rally Takes Dollar Higher, EUR/CHF Breaches 1.2

Dollar surged overnight as boosted by the strong rally in US treasury yield. 10 year yield gained 0.047 to close at 2.914, after hitting as high as 2.934. It's now close to a key resistance, February's high at 2.943. The greenback remains firm in Asian session. For the week, Dollar is trading as the second strongest one, follow Euro, which was helped by the strong rebound in EUR/GBP as well as the rally in EUR/CHF. Talking about EUR/CHF, it halted somewhat at 1.2 key level. But buying emerges again as markets are heading into European session. At the time of writing, it just hit 1.2004. US yields and Swiss Franc will continue to be the focuses of today. And attention will also be on Canadian inflation and retail sales.

Technically, there are a few points to note. AUD/USD's sharp fall overnight and break of 0.7443 argues that rebound from 0.7642 has completed. As the pair is bounded well inside near term falling channel, it should now be heading back to 0.7642 and below to extend recent fall from 0.8135. GBP/USD's break of 1.4144 suggests that a short term top was already formed at 1.4376 and deeper fall could now be seen through 1.3965 support. EUR/GBP's firm break of 0.8739 resistance is taken as indication of near term reversal. Stronger rally should be seen through 0.8796, and it's possibly heading back to 0.8967 resistance.

Cleveland Fed Mester: Further gradual tightening is appropriate this year

Cleveland Fed President Loretta Mester expressed her support for more rate hike this year. She said in a prepared speech for University of Pittsburgh's graduate school of business that "If the economy evolves as I anticipate, I believe further gradual increases in interest rates will be appropriate this year and next year." She added that "continued gradual reduction in monetary policy accommodation, given the economic outlook, will put monetary policy in a better position to address whatever risks, whether to the upside or to the downside, are ultimately realized."

SNB Jordan: No need to change monetary policy even though EUR/CHF is back at 1.2

EUR/CHF continues to press the historical level at 1.2, the SNB imposed floor which was suddenly given up in 2015 and caused panic selling. Now the cross is back at this level. SNB Chairman Thomas said in an interview that the depreciation of the Swiss Franc is in the "right direction". Nonetheless, the currency as a safe haven is prone to change and the situation is "fragile". So the SNB will "remain very prudent". Jordan added that "there's no need to do anything regarding monetary policy at this moment", as "we are convinced that the current monetary policy is still necessary."

Japan core inflation slowed in March, BoJ Kuroda warned on protectionism

Japan national CPI core slipped back to 0.9% yoy in March, down from February's 1.0% yoy, meeting market expectations. It will take a few more months to see if it's only a blip or a change in trend. Core inflation had an impressive up this year but momentum has been slowing. It's already looking a be challenging for inflation to meet BoJ's own media projection of 1.4% in the current fiscal year. And BoJ might need to delay the timing for hitting 2% target again, if the slowdown in inflation persists.

Separately, BoJ Governor Haruhiko Kuroda stepped up his warning on protectionism, as he arrived at the G20 summit of finance ministers and central bankers. He said there will be "quite comprehensive" debate on trade during the meeting. And he emphasized that "many countries share the view they benefit greatly from free trade, so I don't think protectionism will spread and lead to a decline in global growth. But the risk is there." He added that "protectionism isn't having a huge impact on Japan's economy yet. But the risk is right in front of us, so we need to carefully watch how developments unfold."

China ambassador to US Cui: Let's have a more positive and cooperative mindset

Chinese Ambassador to the US Cui Tiankai said in an article in the official Xinhua news agency that "forty years of diplomatic ties and cooperation have served the interests of both countries quite well." And, "in addition to all the bilateral benefits we have gained from this relationship, we have also seen its positive impact on the broader region of the Asia-Pacific and the world."

He urged that "if we have a more positive and cooperative mindset, we could see clearly the emerging trends in the world, seize new opportunities, and turn challenges into opportunities." And he emphasized that China is "against any trade war" and believes "any dispute should be worked out through dialogue and consultation." But Cui also warned that if US insists on a trade war, China will retaliate.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1955; (P) 1.1974; (R1) 1.2004; More...

EUR/CHF continues to lose upside momentum as it's pressing 1.2 handle. But further rise is expected as long as 1.1956 minor support holds. Sustained break of 1.2 will extend the current up trend to 61.8% projection of 1.0629 to 1.1832 from 1.1445 at 1.2188. On the downside, below 1.1956 will turn bias turn bias to the downside for retreat to 4H 55 EMA (now at 1.1898) or below before staging another rally.

In the bigger picture, decisive break of 1.1832 should now extend the medium term up trend through prior SNB imposed floor at 1.2000. 2013 high at 1.2649 should be the next target. Outlook will remain bullish as long as 1.1445 support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Mar | 0.90% | 0.90% | 1.00% | |

| 4:30 | JPY | Tertiary Industry Index M/M Feb | 0.00% | 0.00% | -0.60% | -0.40% |

| 6:00 | EUR | German PPI M/M Mar | 0.20% | -0.10% | ||

| 6:00 | EUR | German PPI Y/Y Mar | 2.00% | 1.80% | ||

| 12:30 | CAD | Retail Sales M/M Feb | 0.50% | 0.30% | ||

| 12:30 | CAD | Retail Sales Ex Auto M/M Feb | 0.50% | 0.90% | ||

| 12:30 | CAD | CPI M/M Mar | 0.40% | 0.60% | ||

| 12:30 | CAD | CPI Y/Y Mar | 2.40% | 2.20% | ||

| 12:30 | CAD | CPI Core - Common Y/Y Mar | 2.00% | 1.90% | ||

| 12:30 | CAD | CPI Core - Median Y/Y Mar | 2.20% | 2.10% | ||

| 12:30 | CAD | CPI Core - Trim Y/Y Mar | 2.10% | 2.10% | ||

| 14:00 | EUR | Eurozone Consumer Confidence Apr A | -0.1 | 0.1 |

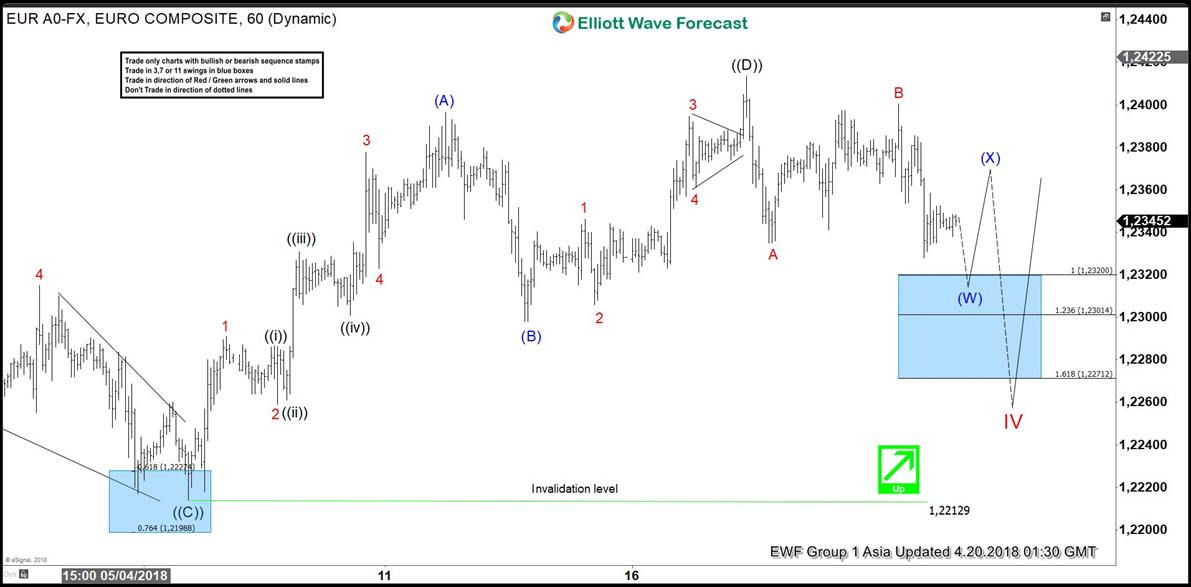

EURUSD Elliott Wave View: Still Trading Sideways

Short-term EURUSD Elliott Wave view suggests that the pair remains in a sideways triangle range between 1.2554 and 1.2153 levels as mentioned in the previous post here. Until we break out of the range, we look for the sideways price action to continue. Triangle doesn't have any particular trend, but it is generally a continuation pattern, thus the pair likely thrust higher to continue the previous bullish trend after the sideways action is over. If we take a look at the previous cycle from January 2017 low. The pair shows a higher high sequence thus the pair is favored to trade higher once triangle consolidation is complete. It's important to note that the Triangle is labeled as A,B,C,D,E.

Currently, we can be in the final stage of triangle structure in Cycle degree wave IV where the decline to 1.2214 low ended Primary wave ((C)) of IV. Above from there, wave ((D)) of IV ended at 1.2414 high. The internals of primary wave ((D)) is unfolding as zigzag Elliott Wave structure where Intermediate wave (A) ended at 1.2396. Afterwards, Intermediate wave (B) pullback ended at 1.2298 low and Intermediate wave (C) of ((D)) ended at 1.2414 high. Down from there, Primary wave ((E)) of IV remains in progress as double three Elliott Wave structure looking to end Intermediate wave (W) of ((E)) in 3 swings at 1.2320-1.2301 100%-123.6% Fibonacci extension area of Minor A-B. Pair should then correct in Intermediate wave (X) of ((E)) and ideally fail below 1.2414 for another extension lower before a thrust higher is seen. We don't like selling the pair.

EURUSD Elliott Wave 1 Hour Chart