Sample Category Title

UK Retail Sales Data Disappoints

Notes/Observations

- German Economic Institutes (Advisors) spring outlook raised its 2018 and 2019 GDP growth forecasts (as expected); viewed protectionism as a headwind

- Softer UK Retail sales data further diminished the expectations of a 2nd hike in 2018 (BOE still seen hiking in May)

Asia:

- Japan PM Abe: agreed with Trump to start talks on 'fair, free and reciprocal' trade.' To continue to negotiate for its steel and aluminum to be exempted from US tariffs; they do not exert any negative influence on US security. TPP is best trade deal for Japan/US

- New Zealand Q1 CPI Q/Q: 0.5% v 0.4%e; Y/Y: 1.1% v 1.1%e

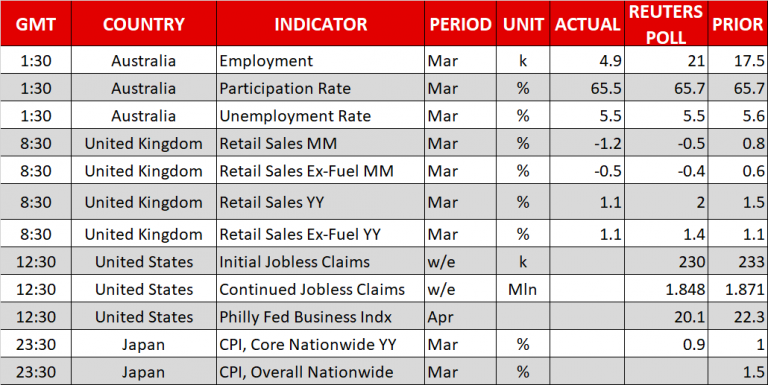

- Australia Mar Employment Change: +4.9K v +20.0Ke; Unemployment Rate: 5.5% v 5.5%e; data suggests that interest rates might stay on hold

- China Commerce Ministry (MOFCOM) stated that its domestic consumption to keep ‘rapid’ growth; US/China trade war will not only hurt US factory workers but also its consumers; reiterates view that US and China had not started talks on 301 investigation. The Ministry also announced that it would implement temporary anti-dumping measures on halogenated butyl rubber imported from US, EU and Singapore

- US said to seek to denuclearize North Korea by 2020. President Trump will walk out of talks planned with North Korea’s Kim if they were not fruitful

Europe:

- UK House of Lords votes for Brexit amendment that would keep the UK in the Customs Union with the EU (as expected); vote was 348-225, going against PM May's wishes

- First formal meeting between the UK and the EU officials on their post-Brexit relationship ended with little in the way of serious progress

- Italy 5-Star party chief Di Maio stated that his party was only open to forming a party with the Northern League (Lega Nord); Northern League had to decide by the end of the week if it wanted to govern with them

- Italy’s Northern League said to ask 5-star to show greater responsibility; end its refusal to work with Berlusconi’s Forza Italia party

Americas:

- Fed’s Beige Book: economy continued to expand at modest-to-moderate pace across all districts. Price rises were expected in steel and building materials due to tariffs. Widespread employment growth continued with modest wage gains

- Fed's Dudley (dove, FOMC voter): Fed should return to neutral policy before labor market tightened; felt confident in the growth outlook. Gradual path of interest rate increases remained appropriate

- Fed's Quarles (hawk, FOMC voter) did not view current flattening of yield curve as a signal for a recession

- Fed's Bullard (dove, non-voter): Fed policy rate should stay flat. Could have inverted yield curve within six months. Market did not see that much inflation pressure

- US reportedly targeting NAFTA deal in 3 weeks. Trade negotiator meeting on Thursday and Friday in D.C. are still not expected to make any announcements this week

- President Trump: We will reduce our large trade deficit with Japan, hope to reach a balance. Reiterated that US sought free, fair, reciprocal trade with Japan, other countries; Japan was in the process of ordering tens of billions of dollars in US aircraft

Economic Data:

- (NL) Netherlands Mar Unemployment Rate: 3.9% v 4.0%e

- (EU) Euro Zone Feb Current Account (Seasonally Adj): €35.1B v €39.0B prior; Current Account NSA (unadj): €22.7B v €12.6B prior

- (IT) Italy Feb Current Account: +€0.8B v -€1.4B prior

- (PL) Poland Mar Sold Industrial Output M/M: 11.4% v 12.4%e; Y/Y: 1.8% v 3.0%e, Construction Output Y/Y: 16.2% v 17.8%e

- (PL) Poland Mar PPI M/M: 0.4% v 0.1%e; Y/Y: 0.3% v 0.0%e

- (UK) Mar Retail Sales (Ex-Auto/Fuel) M/M: -0.5% v -0.4%e; Y/Y: 1.1% v 1.4%e

- (UK) Mar Retail Sales (includes Auto/Fuel) M/M: -1.2% v -0.6%e; Y/Y: 1.1% v 1.9%e

- (HK) Hong Kong Mar Unemployment Rate: 2.9% v 2.9%e ((matches lowest level since Feb 1998)

Fixed Income Issuance:

- (ES) Spain Debt Agency (Tesoro) sold total €B vs. €4.0-5.0B indicated range in 2022, 2028 and 2033 Bonds

- Sold €2.13B in 0.45% Oct 2022 SPGB; Avg yield: 0.194% v 0.294% prior, Bid-to-cover: 1.32x v 1.45x prior

- Sold €1.68B in 1.40% Apr 2028 SPGB; Avg yield: 1.235% v 1.148% prior, Bid-to-cover: 1.30x v 1.51x prior

- Sold €0.76B in 2.35% July 2033 SPGB; Avg Yield: 1.723% v 1.875% prior; Bid-to-cover: 1.96x v 1.65x prior

- (FR) France Debt Agency (AFT) sold total €B vs. €6.0-7.0B indicated range in 2021, 2023, 2024 Oats

- Sold €2.798B in 0.0% Feb 2021 Oat; Avg Yield: -0.32% v -0.24% prior; Bid-to-cover: 2.68x v 2.13x prior (Mar 15th 2018)

- Sold €3.194B in 0.0% Mar 2023 Oat; Avg Yield: 0.06% v 0.11% prior; bid-to-cover: 2.07x v 4.15x prior (Mar 15th 2018)

- Sold €999M in 1.75% Nov 2024 Oat;Avg Yield: 0.30% v 0.18% prior; bid-to-cover: 4.67x v 2.03x prior

- (SE) Sweden sold SEK1.5B in 0.75% 2028 bond; Avg Yield: 0.7084% v 0.6776% prior; Bid-to-cover: 2.13x v 4.36x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.1% at 381.5, FTSE +0.2% at 7329, DAX -0.2% at 12566, CAC-40 +0.1% at 5382, IBEX-35 -0.1% at 9850, FTSE MIB -0.1% at 23739, SMI -0.1% at 8826, S&P 500 Futures -0.2%]

Market Focal Points/Key Themes:

- European Indices trade mixed this morning following mixed earnings, rising Oil and weaker UK Retail sales data. The FTSE 100 continues to outperform as a cweaker cable boosts the Index.

On the earnings front Swiss names ABB, Nestle and Novartis reported, with ABB outperforming after strong revenue numbers. In France Publices outperforms after earnings, Schneider Electric also gaining while Pernod Ricard sees some profit taking. - In the UK, Unilever and Debenhams fall after resutls, with Rentokil a riser after Q1 sales. In the M&A space P&G acquired Merck KGAA consumer division for €3.4B and Weir acquired Oregon based ESCO Corp for $1.05B.

- Looking ahead notable earners include Dow component P&G, as well as Grainger, Philip Morris, BNY, Keycorp and Blackstone to name a few.

Movers

- Consumer Discretionary [Unilever [UNA.NL] -2.3% (Earnings), Pernod Ricard [RI.FR] -1% (Earnings), Publicis [PUB.FR] +6.6% (Earnings), Debenhams [DEB.UK] -7.4% (Earnings)]

- Industrials [ABB [ABBN.CH] +4.1% (Earnings), Rentokil [RTO.UK] +2.6% (Earnings), Weir Group [WEIR.UK] +5.3% (Trading update, acquisition, placing)]

- Healthcare [ Novartis [NOVN.CH] -1.4% (Earnings)]

- Technology [ Schneider Electric [SU.FR] +2.0% (Earnings), Ultra Electronics [ULE.UK] -7.5% (SFO investigation)]

Speakers

- France Fin Min Le Maire: IMF growth forecast for 2018 is optimistic; potential trade war was a major risk to economy

- German Economic Institutes (Advisors) spring outlook raised its 2018 and 2019 GDP growth forecasts to 2.2% and 2.0% respectively. German economy was experiencing a boom and seen increasing reaching capacity. Expected a strong expansion in Q2 but noted the escalating trade conflict would hurt its outlook

- OPEC-Non-OPEC Joint Ministerial Monitoring Committee (JMMC) officials said to see OECD oil inventories as almost cleared Meeting

Currencies

- The USD was slightly firmer against the major European pairs as US yields drifted to 1-month highs

- GBP/USD was lower by 0.3% after another disappointing round of data. Retail sales data missed across the board. The GBP began the session trying to recover after Wed’s selloff after soft wage and inflation data cemented the view of only one more rate hike in 2018. Weak retail sales data further put-off any chance of a 2nd hike in 2018 (BOE still seen hiking in May)

- EUR/USD trading at 1.2365 just ahead of the NY morning while USD/JPY was at 107.37

Fixed Income

- Bund Futures trade 38 ticks lower at 158.63 as Germany's 10-year bond yield jumps back above the 0.50% level. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 121.71 lower by 61 ticks, extending its declines after softer than expected UK retail sales data. Support continues stands at 121.25 then 120.85, with upside resistance at 123.35 then 123.85.

- Thursday’s liquidity report showed Wednesday's excess liquidity fell to €1.849T from €1.857T prior. Use of the marginal lending facility decreased from €170M to €60M.

- Corporate issuance saw 2 issuers raise $5.3B in the primary market last week

Looking Ahead

- (ID) Indonesia Central Bank (BI) Interest Rate Decision: Expected to leave 7-Day Reverse Repo unchanged at 4.25% (no set time)

- (IT) Italy Debt Agency (Tesoro) announce for BTPei and CTZ auction for Tuesday, Apr 24th

- (DE) German Chancellor Merkel with France President Macron in Berlin

- (BR) Brazil Apr CNI Industrial Confidence: No est v 59.0 prior

- (PT) Portugal Feb Current Account: No est v -€0.6B prior

- 05:30 (HU) Hungary Debt Agency (AKK) to sell in 12-month Bills

- 05:30 (HU) Hungary Debt Agency (AKK) to sell Floating-rate bond

- 05:30 (UK) DMO to sell £2.5B in 1.625% Oct 2028 Gilts

- 05:50 (FR) France Debt Agency (AFT) to sell €1.25-1.75B in I/L 2021, 2024 and 2028 Bonds (Oatei)

- 06:00 (CZ) Czech Republic to sell Bills

- 06:45 (US) Daily Libor Fixing

- 07:00 (RO) Romania to sell Bonds

- 07:30 (TR) Turkey Central Bank TCMB Survey of Expectations

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Apr Philadelphia Fed Business Outlook: 21.0e v 22.3 prior

- 08:30 (US) Initial Jobless Claims: 230Ke v 233K prior; Continuing Claims: 1.85Me v 1.871M prior

- 08:30 (CA) Canada Mar ADP Payrolls Report: No est v +32.7K prior

- 08:30 (US) Weekly USDA Net Export Sales

- 08:45 (EU) EU Commissioner Oettinger (Germany) on EU budget impact from Brexit

- 09:00 (RU) Russia Gold and Forex Reserve w/e Apr 13th: No est v $458.9B prior

- 09:10 (US) Fed's Quarles (hawk, FOMC voter) at IIF

- 10:00 (US) Mar Leading Index: 0.3%e v 0.6% prior

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 11:00 (US) Treasury announcement on upcoming 2-year, 5-year and 7-year issuance during week of Apr 23rd

- 12:00 (NO) Norway Central Bank Gov Olsen speaks in Oslo

- 13:00 (US) Treasury to sell 5-Year TIPS Reopening

- 13:15 (NO) Norway Central Bank Dep Gov speaks in Philadelphia

- 18:45 (US) Fed's Mester (FOMC voter, hawk) on economic outlook

Euro Unchanged, US Jobless Claims Next

EUR/USD continues to show limited movement. On Thursday, the pair is trading at 1.2371, down 0.03% on the day. On the release front, the eurozone current account surplus dropped to EUR 35.1 billion, but beat the estimate of EUR 32.3 billion. In the US, unemployment claims is expected to drop to 230 thousand, and the Philly Fed Manufacturing Index is forecast to soften to 20.8 points. On Friday, there are no major events. Germany releases PPI and the Eurozone publishes consumer confidence.

Eurozone inflation improved in March, but still remain short of the ECB target of 2.0%. Final CPI came in at 1.3%, up from 1.1% a month earlier. Still, the reading fell short of the estimate of 1.4%. As long as inflation remains low, there will be little pressure on the ECB to tighten its accommodative monetary policy. The ECB's stimulus program is scheduled to wind up in September, but an increase in interest rates is unlikely before 2019.

The well-respected ZEW Economic Sentiment releases were a disappointment earlier this week. The April reports in Germany and the eurozone were much weaker than expected, but investors shrugged off the numbers as risk appetite has improved. The German release of -8.2 points showed pessimism on the part of institutional investors and analysts and marked the weakest reading since November 2012. The eurozone reading of 1.9 was the lowest since July 2o16. The German and eurozone economies remain solid, making these weak readings all the more surprising. Investors will be hoping that these ZEW releases are one-time blips and that the May readings will be in line with recent releases.

Technical Failure Weighing On EURUSD

The euro currency has turned lower against the U.S dollar during the European trading session, after repeated technical rejections from the key 1.2400 resistance level. The EURUSD currently trades around the 1.2360 level, as a lack of buying demand above the 1.2400 level weighs on the pairs intraday sentiment. The pivotal 1.2344 support level, now remains the gateway to further intraday losses towards the key 1.2300 support region.

The EURUSD remains bearish while trading below the 1.2382 level, further intraday losses towards the 1.2344 and 1.2300 levels seems possible.

If the EURUSD pair moves above the 1.2382 resistance level, buyers may again test the 1.2400 and 1.2413 resistance levels.

GBPUSD Intraday Bearish Below 1.4200 Level

The British pound has moved to a new weekly trading-low against the U.S dollar, following much weaker than expected Retail Sales numbers from the United Kingdom economy. The GBPUSD pair currently trades around the 1.4180 level, after finding interim technical support from the 1.4168 level, as UK monthly Retail Sales fell -1.2 percent. Sterling downside pressures are likely to accelerate below the 1.4168 level, with the 1.4148 and 1.4110 levels key support.

The GBPUSD pair is intraday bearish while trading below the 1.4200 level, key intraday support is now found at the 1.4146 and 1.4110 levels.

Should the GBPUSD pair start to trade back above the 1.4200 level, key intraday resistance is found at the 1.4218 and 1.4230 levels.

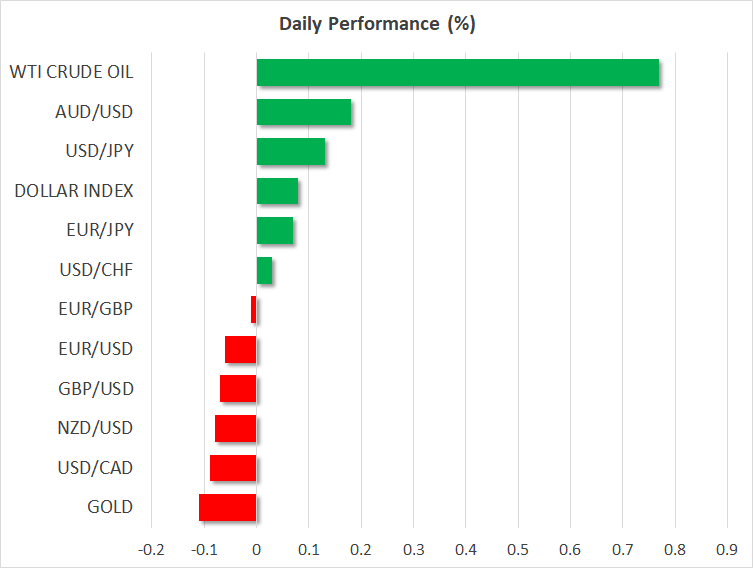

Oil Bulls Unlock Fresh Three-Year Highs

Here are the latest developments in global markets:

FOREX: Sterling tumbled to a five-day low against the greenback (-0.06%) on Thursday during the early European afternoon as UK retail sales recorded their biggest fall in a year. This follows a strong sell-off on Wednesday when the UK CPI dropped surprisingly to one-year lows, raising doubts on whether the Bank of England will proceed with further rate increases after next month’s widely anticipated rate hike. Dollar/yen was moving slightly higher by 0.13% on the day, last trading at 107.39. Euro/dollar edged down to 1.2367 losing 0.06%. Dollar/loonie was weaker at 1.2617 (-0.06%) following a strong rally towards one-week highs on Wednesday, when the BoC stood pat on interest rates but held a cautious stance on future monetary tightening. Antipodean currencies were mixed, with aussie/dollar being up by 0.15% at 0.7791 and kiwi/dollar being down by 0.08% at 0.7309. Aussie shrugged off today’s weaker-than-expected data on job growth from Australia. Turkish lira took a breather, a day after posting its biggest one-day advance in more than a year after President Tayyip Erdogan declared early elections on June 24. Dollar/lira pared some losses, gaining 0.80%.

STOCKS: European stocks were mixed at 0946 GMT. The blue-chip Euro STOXX 50 was down by 0.02%, the German DAX 30 fell by 0.01% and the British FTSE 100 rose by 0.21%. The Italian FTSE MIB ticked significantly higher by 0.62%. The Japanese Nikkei 225 closed higher, posting an almost two month high, while in Hong Kong the Hang Seng surged by 1.40%. Futures tracking the major US benchmarks are currently flashing red after a mixed session on Wednesday.

COMMODITIES: Oil prices recorded new highs due to a decline in US oil inventories and also after sources signaled that Saudi Arabia would be happy to see the price closer to $100 a barrel. WTI continued the bullish rally and rose by 0.79% to $68.99 per barrel, while Brent surged by 0.64% to $74.12 per barrel. Gold was trading marginally lower by 0.05% to $1,348.2 per ounce.

Day ahead: Initial jobless claims, Philly Fed Manufacturing Index & Japanese inflation next in focus

Data out of the US will dominate the economic calendar later in the day, while early on Friday, the focus will shift to Japanese inflation readings after the US President and the Japanese Prime Minister seemed to have found a common ground on the North Korea front at the end of their two-day meeting in Florida yesterday. However, regarding trade, they failed to unify their opinions as the US President highlighted that he wouldn’t rejoin the Trans-Pacific free-trade partnership (TPP) unless Japan offers a deal he “could not refuse”. In contrast, the Japanese Prime Minister reiterated that a bilateral trade agreement, which the US favors, is not Japan’s desirable option.

In the US, figures on initial jobless claims will be delivered along with the Philadelphia’s Fed Manufacturing index at 1230 GMT. Analysts expect the number of people applying for unemployment benefits for the first time to have increased by 230,000 in the week ending April 13 compared to 233,000 seen in the preceding week, while they expect business conditions in Philadelphia to deteriorate slightly in April. Particularly, they anticipate the Philly Fed manufacturing index to fall from 22.3 to 20.1. This would be the lowest level reached since August.

In Japan, the Statistics Bureau will hand out stats on consumer prices at 2330 GMT (0830 AM on Friday in Japan). Projections are for the nationwide core CPI, which excludes fresh food but includes energy items, to inch down by 0.1 percentage points to 0.9% y/y in March as the winter season comes to an end, remaining far below the BoJ’s price target of 2.0%. A strengthening yen and subdued wages seem to be behind the weakness in inflation that reinforces BoJ policymakers’ stance to hold interest rates at record lows and continue to suppress the yields on Japanese bonds.

In equity markets, earnings releases will continue to attract interest.

As for today’s public appearances, the French President, Emmanuel Macron, and the German Chancellor, Angela Merkel, will be meeting in Frankfurt to discuss on how to reform the Eurozone. It would be interesting to see whether Merkel, who extended her term for the fourth time will remain cautious on Macron’s proposals to turn Europe’s existing bailout fund into a European Monetary Fund given the pressures she faces by her party to refuse any plans that could harm German taxpayers. In the US, permanent FOMC voting members Lael Brainard and Randal Quarles will be talking at 1200 GMT and 1330 GMT respectively. Also of interest might be a news conference (1245 GMT) by IMF Managing Director Christine Lagarde and World Bank President Jim Yong Kim ahead of the Spring Meetings of the two organizations; among notable names attending the meetings is ECB President Mario Draghi.

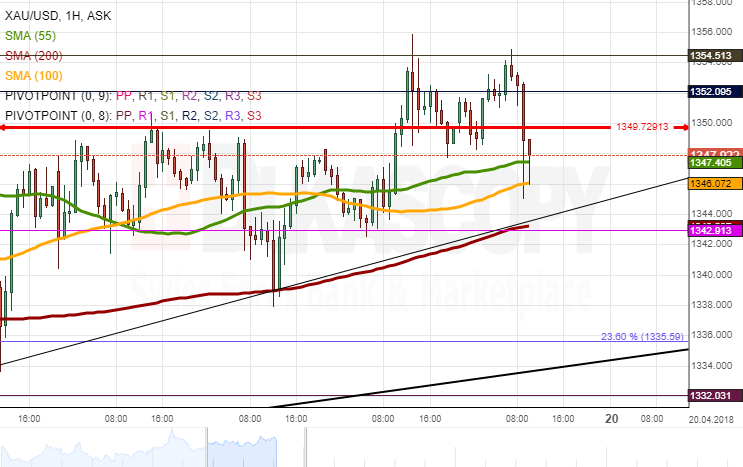

Gold Analysis: Is Bullish Today

After testing the 55– and 100-hour SMAs for a couple of hours, Gold accelerated mid-Wednesday and dashed through a three-day resistance of 1,350.00. Further advance was stopped by the monthly R1 at 1,355.00, thus leaving the rate between the aforementioned two levels until Thursday morning.

Bullish technical indicators suggest that the monthly R1 should be eventually surpassed, thus allowing for a re-test of the senior channel or the 201/2018 high near 1,360.00 and 1,366.00, respectively.

The nearby-located 55-, 100– and 200-hour SMAs likewise point to a price increase today, as these moving averages are expected to guide the pair higher.

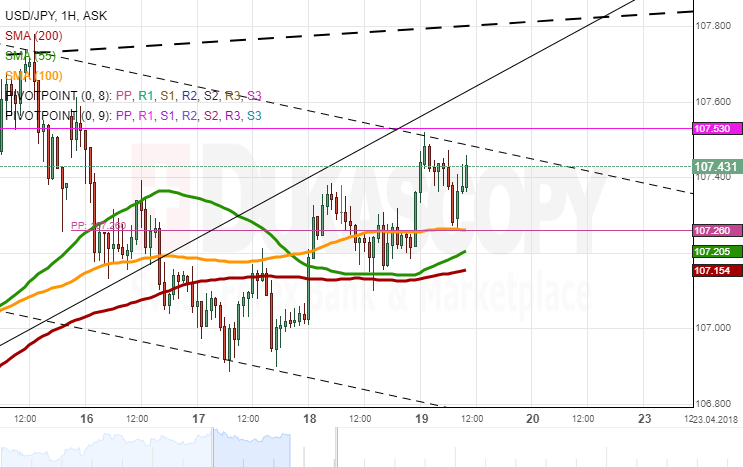

USDJPY Analysis: Reaches Monthly R1

The US Dollar was pushing lower against the Japanese Yen on Wednesday. Bears, however, failed to earn massive gains, as a fall below the 107.15 mark was restricted by the 55– and 200-hour simple moving averages.

The expected bullish push was provided during the Asian session when the pair gained 27 pips and touched the monthly R1 at 107.53. The pair should maintain its up-trend in this session, as well. Apart from the aforementioned monthly R1, the next significant resistance is set by a trend-line circa 107.80.

Meanwhile, the prevalence of the bearish sentiment should send the pair towards the 55– and 200-hour SMAs. Given lack of data releases today, a further decline is unlikely.

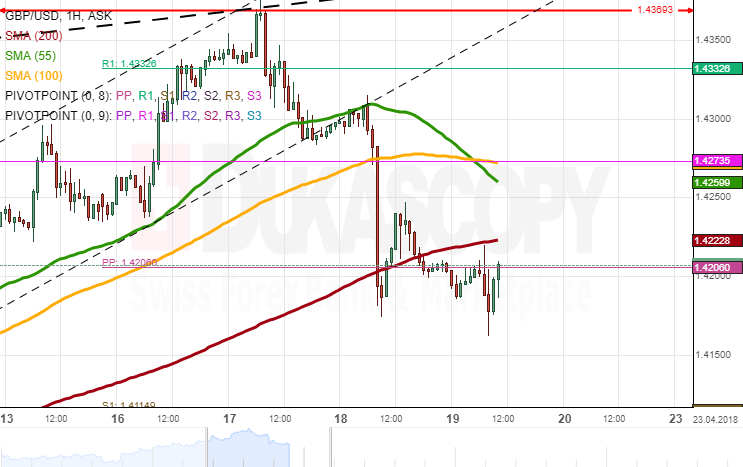

GBPUSD Analysis: Consolidates After Plunge

The Sterling was trading along the 55-hour SMA early on Wednesday. This lack of sentiment was disrupted massively at 0830GMT when the UK released rather disappointing inflation data. The pair plunged 89 pips in the wake of this release down to the 1.42 mark and had remained near this level by Thursday morning.

It is likely that the Sterling tries to recover some of its losses and in this session, as suggested by bullish technical indicators. However, in case of sluggish Retail Sales, the pair could fall even lower, as no restrictions until the weekly S1 at 1.4111 are apparent on the chart.

This data release might likewise have an opposite effect and thus push the pair past the 55– and 100-hour SMAs and the monthly R1 located at 1.4274. In case of weaker bullish sentiment, this area should hold firm.

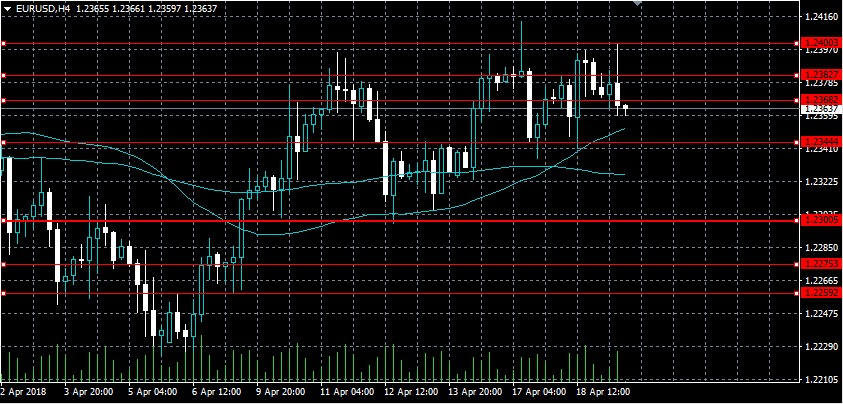

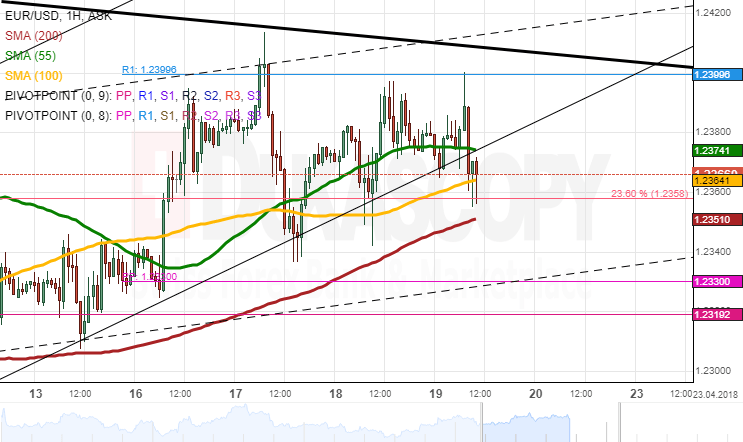

EURUSD Analysis: With No Changes

EUR/USD was driven by slight upside risks on Wednesday. This movement was guided by the 55-hour SMA and a channel line. From the upside, the pair was restricted by the psychological 1.24 mark which has provided strong resistance during the past two weeks. Lack of fundamentals in the given session resulted in the pair returning to its Wednesday morning level of 1.2380.

It seems that the Euro is trying to edge lower, so a decline should occur if the 55– and 100-hour SMAs are breached. The nearest downside target in this case is the 200-hour SMA or the weekly PP at 1.2345 and 1.2330, respectively.

On the other hand, the same lack of fundamental releases may maintain the rate stable, thus allowing for a move along the 55-hour SMA and towards the senior channel near 1.24.

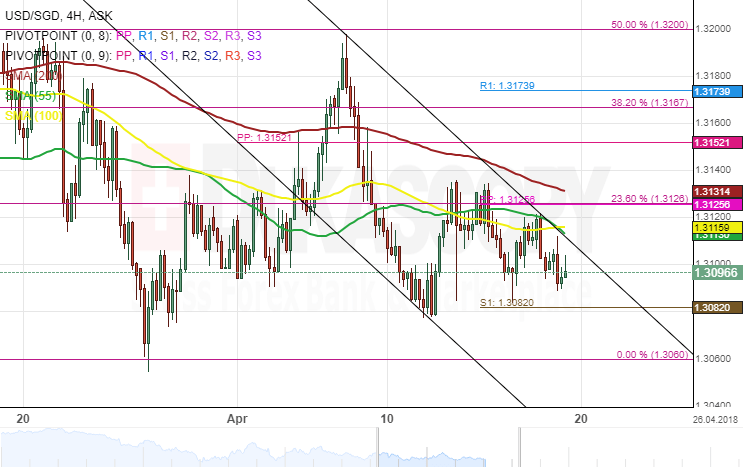

USD/SGD 4H Chart: Declines With Large Volatility

The Greenback bounced of a large scale 50.00% Fibonacci retracement level against the Singapore Dollar at the start of April. As a result of the event a descending channel down pattern has formed.

The channel has already managed to pass two strong support clusters near the 1.3150 and the 1.3125 levels. Moreover, it doesn't seem to face any additional support below it.

The only exception to that is the weekly S1 1.3082, which stands in the way of the Singapore Dollar's surge.

Meanwhile, note that below the weekly S1 the historical low level of 1.3060 might provide support